University Business Finance Assignment: Knowledge and Valuation

VerifiedAdded on 2023/01/11

|11

|2187

|61

Homework Assignment

AI Summary

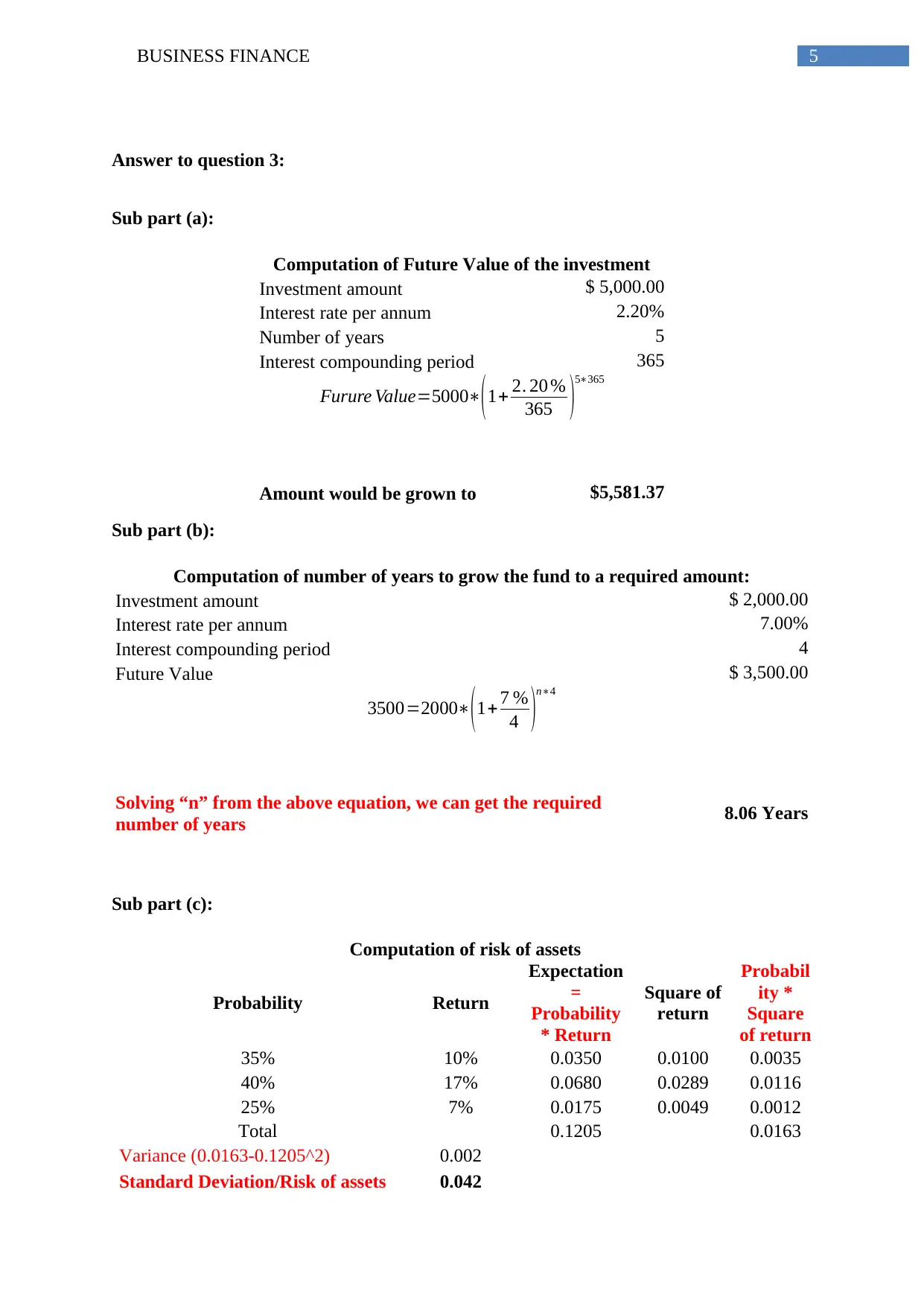

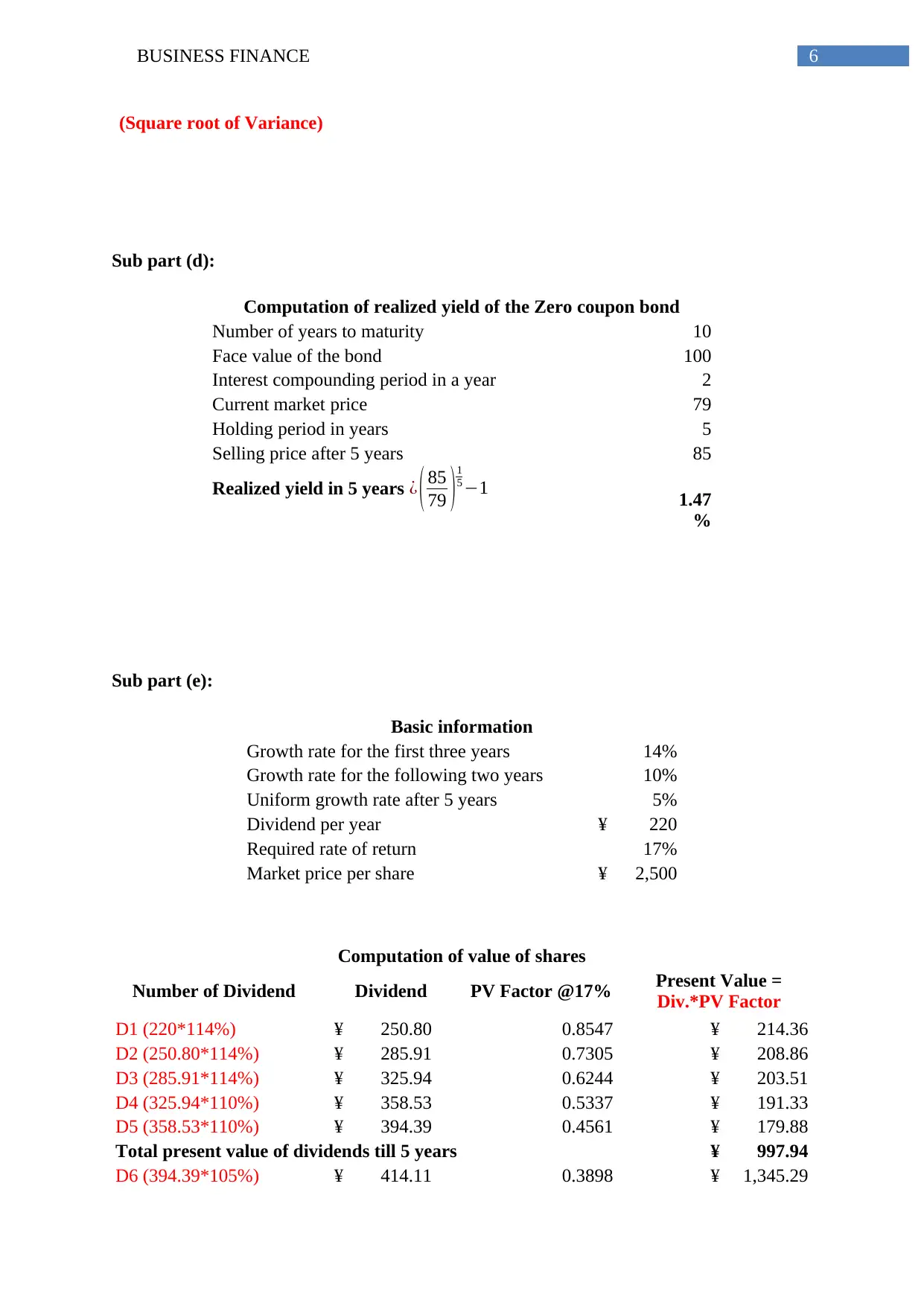

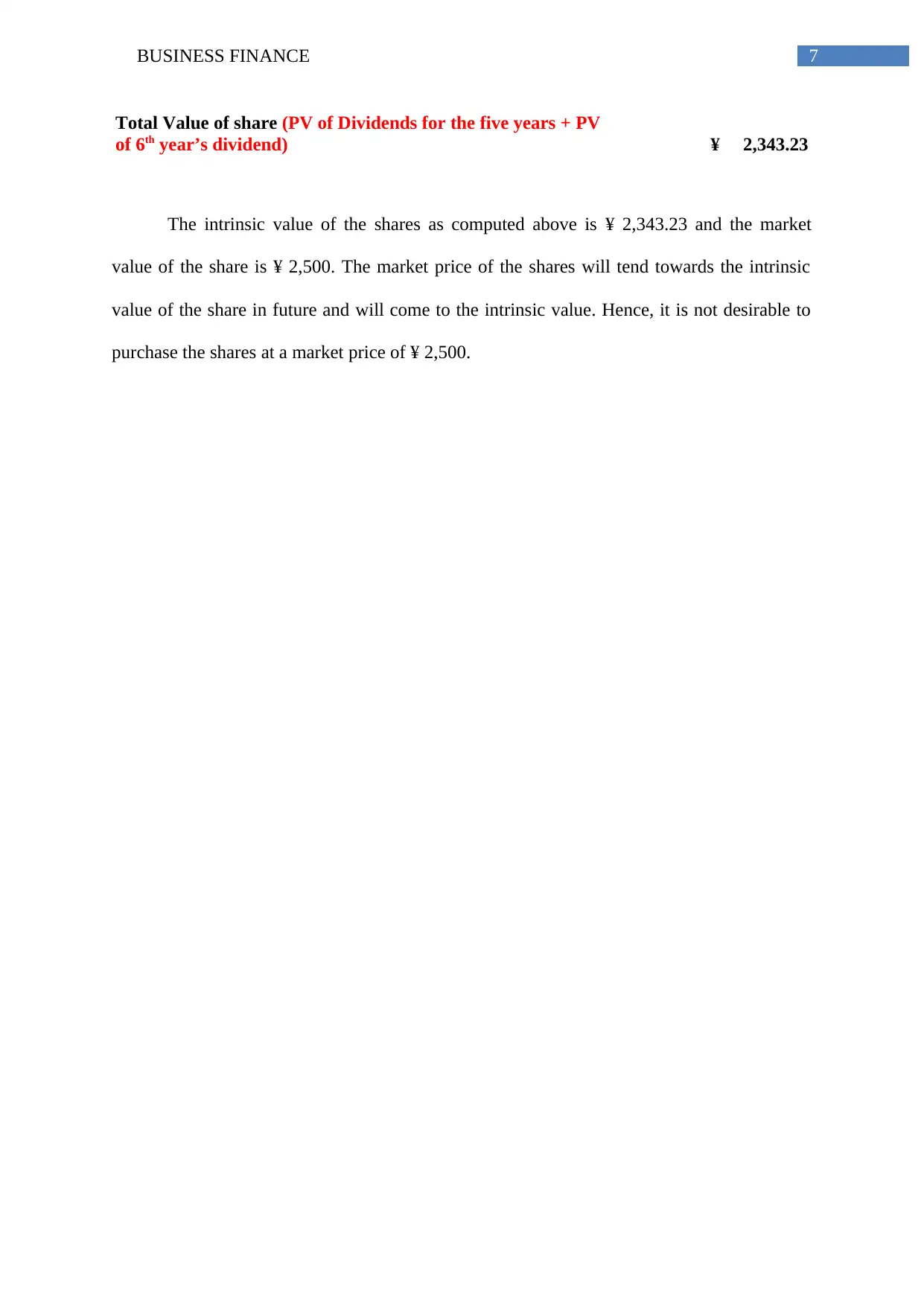

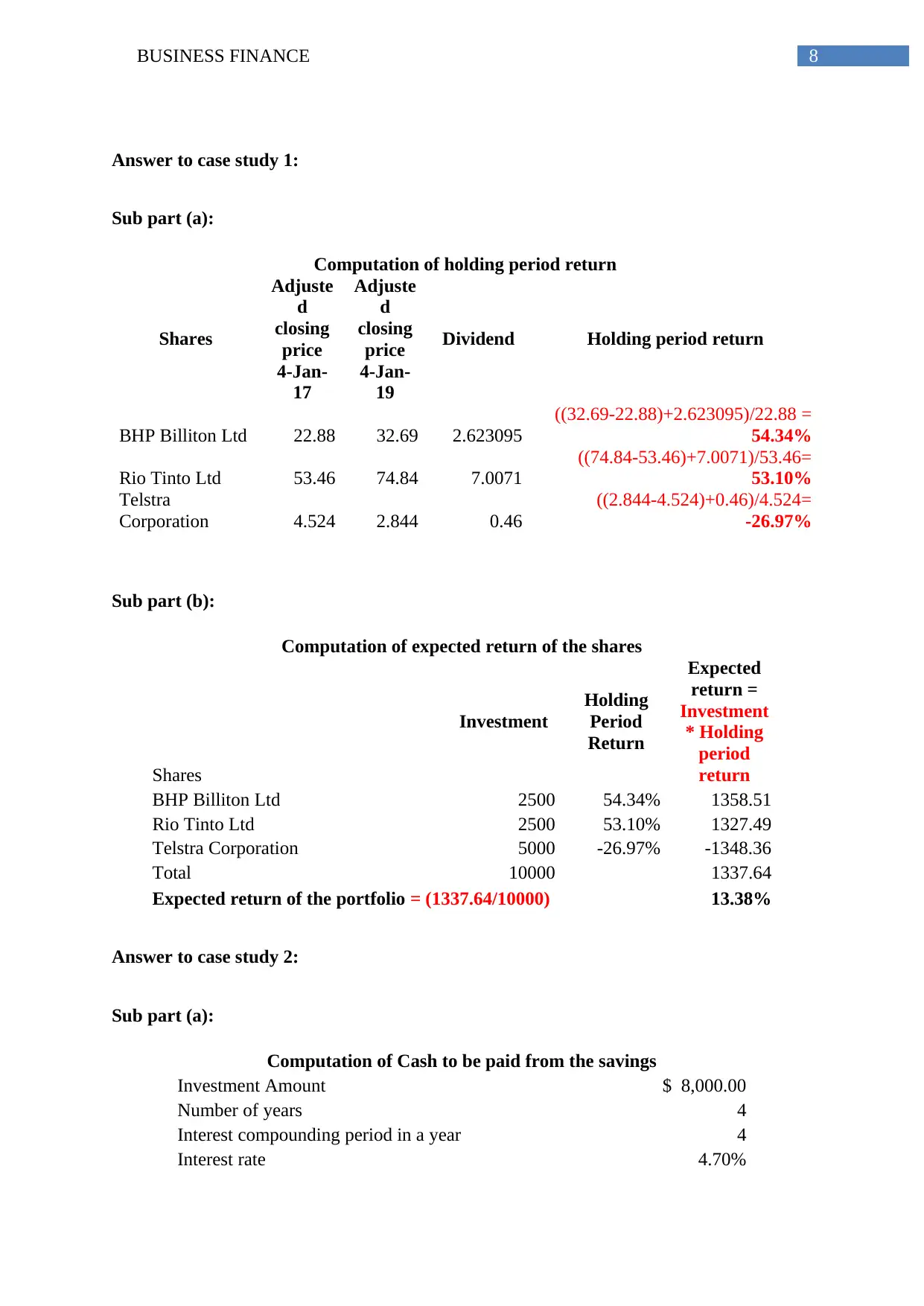

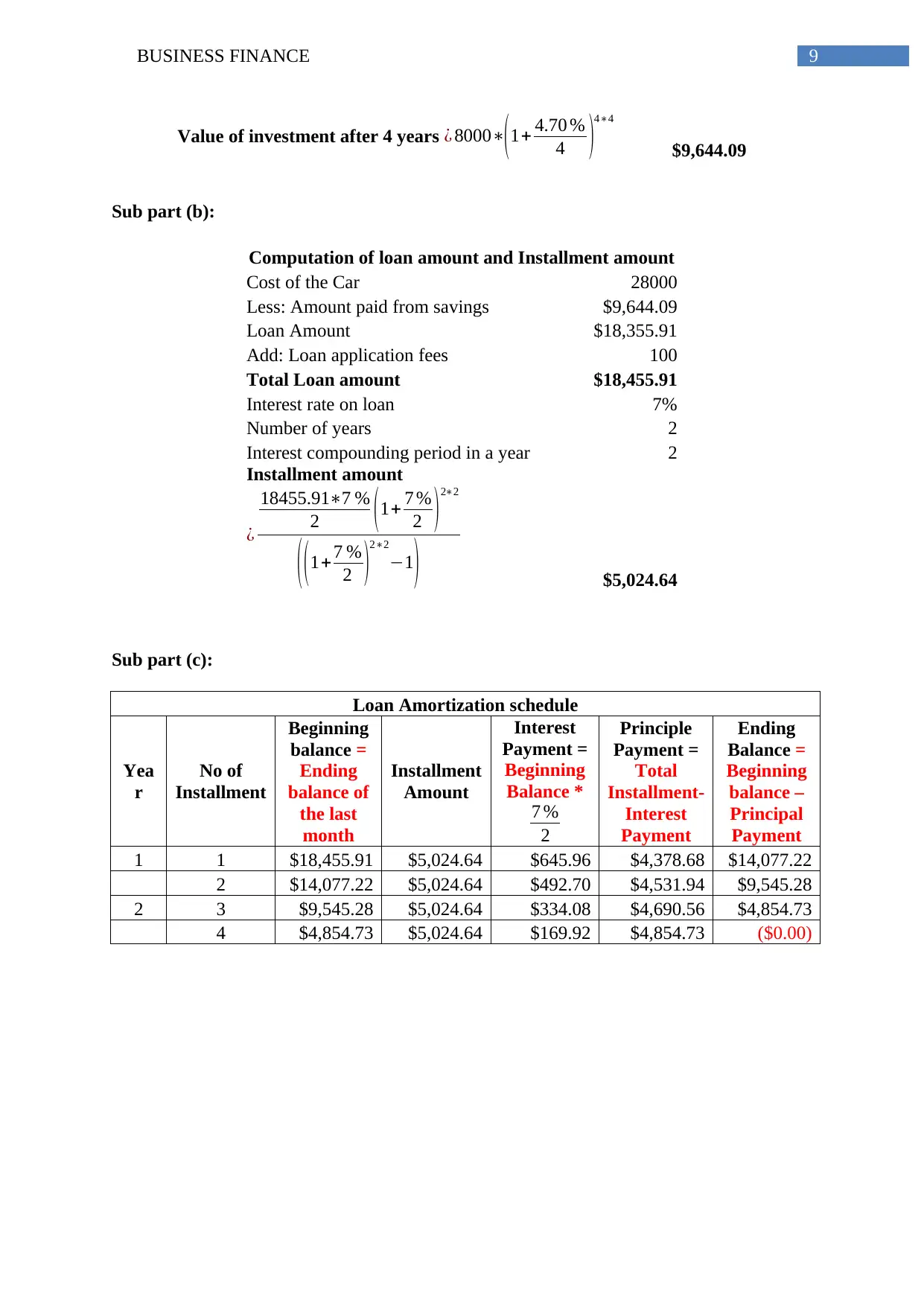

This document presents a detailed solution to a Business Finance assignment, addressing key concepts such as agency costs, systematic and unsystematic risks, and various valuation methods. The solution includes calculations for future value, the number of years to grow a fund, risk assessment of assets, realized yield of a zero-coupon bond, and share valuation using dividend discount models. Additionally, the document analyzes two case studies, covering holding period return calculations for different shares and loan amortization schedules. The solution is meticulously presented with formulas, calculations, and explanations, making it a valuable resource for students studying business finance. The assignment covers topics like agency costs, systematic risks, future value, and share valuation, along with two case studies. The solution provides step-by-step calculations and explanations for each problem, ensuring clarity and understanding. The document is well-structured, providing a comprehensive guide to understanding and solving business finance problems. It includes the formulae, figures inserted into the formulae and then calculation steps. The final answer is shown up to two decimal places as per instructions given in the assignment brief.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.