FINE 3200S Investments Homework 1 Winter 2019: Risk & Return

VerifiedAdded on 2023/04/23

|9

|2450

|367

Homework Assignment

AI Summary

This assignment covers various aspects of investment management, including the analysis of exchange-traded funds that sell covered calls, the evaluation of risk and return profiles under different economic conditions, and the impact of minimum wage laws on employment. It delves into the objectives and strategies of fund managers, comparing fund volatility to market indices and diversified portfolios. The assignment also discusses the use of VIX and other indicators for managing market risk, explores minimum variance frontiers for portfolio optimization, and examines the economic consequences of minimum wage policies. Furthermore, it addresses the application of hedging strategies using options contracts to manage portfolio risk and shift between risk-on and risk-off modes based on short-term market outlooks. The included references from academic journals and reports support the analysis and conclusions presented. Desklib provides a platform to access this and other solved assignments, along with study tools, to aid students in their academic pursuits.

a. What is the fund’s stated investment objective? How do the fund managers seek to

achieve it?

While frequently done on a specially appointed premise, one can collect and deal with an

arrangement of secured call choice positions as either a piece of a bigger portfolio or on an

independent premise. Such a methodology requires more point by point consideration than

dealing with a stock-just portfolio. In any case, methodically dealing with an arrangement of

secured calls has much for me to suggest it (Cohen, Frazzini & Malloy, 2008). Virtually every

financial specialist I know has stocks in their portfolio that they have been holding for a really

long time, and are not benefitting from. Executing a secured call procedure is an incredible

method to make salary against those possessions, and ought to be a piece of each speculator's

exchanging collection.

b. Evaluate the comparative return profile offered to investors: under what economic

circumstances will the fund pay a return higher or lower than the market average?

Given how basic hazard is to speculations, numerous new financial specialists accept that it is a

very much characterized and quantifiable thought. Lamentably, it's definitely not. Peculiar as it

might sound, there is still no genuine concurrence on what "chance" signifies or how it ought to

be estimated. Shockingly, unpredictability is imperfect as a proportion of hazard. While the facts

confirm that an increasingly unstable stock or bond opens the proprietor to a more extensive

scope of conceivable results, it doesn't really affect the probability of those results (Phalippou &

Gottschalg, 2008). In numerous regards unpredictability is increasingly similar to the choppiness

a traveler encounters on a plane – unsavory, maybe, yet not by any stretch of the imagination

bearing much relationship to the probability of an accident.

achieve it?

While frequently done on a specially appointed premise, one can collect and deal with an

arrangement of secured call choice positions as either a piece of a bigger portfolio or on an

independent premise. Such a methodology requires more point by point consideration than

dealing with a stock-just portfolio. In any case, methodically dealing with an arrangement of

secured calls has much for me to suggest it (Cohen, Frazzini & Malloy, 2008). Virtually every

financial specialist I know has stocks in their portfolio that they have been holding for a really

long time, and are not benefitting from. Executing a secured call procedure is an incredible

method to make salary against those possessions, and ought to be a piece of each speculator's

exchanging collection.

b. Evaluate the comparative return profile offered to investors: under what economic

circumstances will the fund pay a return higher or lower than the market average?

Given how basic hazard is to speculations, numerous new financial specialists accept that it is a

very much characterized and quantifiable thought. Lamentably, it's definitely not. Peculiar as it

might sound, there is still no genuine concurrence on what "chance" signifies or how it ought to

be estimated. Shockingly, unpredictability is imperfect as a proportion of hazard. While the facts

confirm that an increasingly unstable stock or bond opens the proprietor to a more extensive

scope of conceivable results, it doesn't really affect the probability of those results (Phalippou &

Gottschalg, 2008). In numerous regards unpredictability is increasingly similar to the choppiness

a traveler encounters on a plane – unsavory, maybe, yet not by any stretch of the imagination

bearing much relationship to the probability of an accident.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A high-hazard venture is one for which there is either an extensive rate possibility of loss of

capital or underperformance or a moderately little shot of a staggering misfortune. The first of

these is natural, if abstract: If you were told there's a 50/50 chance that your speculation will

procure your normal return, you may find that very unsafe. On the off chance that you were

informed that there is a 95% shot that the venture won't procure your normal return, nearly

everyone will concur that that is hazardous.

c. How about the fund’s risk? How does the fund’s volatility of returns compare to the

market index, and to a diversified portfolio of similar equity issues without the covered-call

kicker?

There are five pointer principles in relation to risk specialization that apply to the stock

investigations, securities as well as common store portfolios. These five pointes include alpha, r-

squared, beta, Sharpe proportion and the standard deviation. These measures are chronicled

speculation chance/instability indicators and are on the whole factual segments of the present-

day hypothesis of the portfolio. Present-day portfolio hypothesis is a money-related standard and

a philosophy that is scholastic that is applied in surveying the value execution, salary settled and

reserve speculations that are common by making a contrast with market benchmarks (Baumol,

Goldfeld, Gordon & Koehn, 2012). The hazard estimations are planned to activate the

speculators to make a decision regarding the hazard remunerate parameters as well as their

ventures.

The financial experts hoping to make capital protection do pay attention on the securities and the

store portfolios associated with low betas, while those speculators expected to go out on a limb

seeking for returns that are higher should search for beta ventures that are of high value.

capital or underperformance or a moderately little shot of a staggering misfortune. The first of

these is natural, if abstract: If you were told there's a 50/50 chance that your speculation will

procure your normal return, you may find that very unsafe. On the off chance that you were

informed that there is a 95% shot that the venture won't procure your normal return, nearly

everyone will concur that that is hazardous.

c. How about the fund’s risk? How does the fund’s volatility of returns compare to the

market index, and to a diversified portfolio of similar equity issues without the covered-call

kicker?

There are five pointer principles in relation to risk specialization that apply to the stock

investigations, securities as well as common store portfolios. These five pointes include alpha, r-

squared, beta, Sharpe proportion and the standard deviation. These measures are chronicled

speculation chance/instability indicators and are on the whole factual segments of the present-

day hypothesis of the portfolio. Present-day portfolio hypothesis is a money-related standard and

a philosophy that is scholastic that is applied in surveying the value execution, salary settled and

reserve speculations that are common by making a contrast with market benchmarks (Baumol,

Goldfeld, Gordon & Koehn, 2012). The hazard estimations are planned to activate the

speculators to make a decision regarding the hazard remunerate parameters as well as their

ventures.

The financial experts hoping to make capital protection do pay attention on the securities and the

store portfolios associated with low betas, while those speculators expected to go out on a limb

seeking for returns that are higher should search for beta ventures that are of high value.

Common store financial specialists ought to keep away from effectively overseen assets with

high R-squared proportions, which are by and large scrutinized by examiners as being "storage

room" list reserves. With these cases in place, it looks bad to pay high amounts as charges for

expert administration when one can show signs of improvement results from a file subsidize.

Standard deviation estimates the information scattering derived from the corresponding mean. To

make it clearer, the more that information is widely separated or spread, the higher it matters

from the standard. In the fund context, standard deviation is associated with the yearly return rate

of a venture to gauge its risk A stock that is unstable usually have a deviation that is an exclusive

expectation. With the common assets, the standard deviation disclosure to how much the arrival

associated with a reserve which strays from the profits which are normal based with its

chronicled execution. Numerous financial specialists will in general spotlight solely on

speculation comes back with little worry for venture hazard.

D

The uplifting news for speculators is that these pointers are determined for them and are

accessible on various budgetary sites: they're additionally joined into numerous venture look into

reports. As valuable as these estimations may end up being, it is important to put into

consideration about a stock, shared store speculation or security as the instability risk is only part

of the components one may ought to think about that influences the status of a venture.

2

a.

The decision isn't for the those who give up easily. VIX's moves are regularly outrageous, so on

the off chance that you wager wrong can lose cash in a major rush (think 15% or more in a 24-

hour time frame), obviously, there is the proportionate upside on the off chance that you take

high R-squared proportions, which are by and large scrutinized by examiners as being "storage

room" list reserves. With these cases in place, it looks bad to pay high amounts as charges for

expert administration when one can show signs of improvement results from a file subsidize.

Standard deviation estimates the information scattering derived from the corresponding mean. To

make it clearer, the more that information is widely separated or spread, the higher it matters

from the standard. In the fund context, standard deviation is associated with the yearly return rate

of a venture to gauge its risk A stock that is unstable usually have a deviation that is an exclusive

expectation. With the common assets, the standard deviation disclosure to how much the arrival

associated with a reserve which strays from the profits which are normal based with its

chronicled execution. Numerous financial specialists will in general spotlight solely on

speculation comes back with little worry for venture hazard.

D

The uplifting news for speculators is that these pointers are determined for them and are

accessible on various budgetary sites: they're additionally joined into numerous venture look into

reports. As valuable as these estimations may end up being, it is important to put into

consideration about a stock, shared store speculation or security as the instability risk is only part

of the components one may ought to think about that influences the status of a venture.

2

a.

The decision isn't for the those who give up easily. VIX's moves are regularly outrageous, so on

the off chance that you wager wrong can lose cash in a major rush (think 15% or more in a 24-

hour time frame), obviously, there is the proportionate upside on the off chance that you take

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

care of business. These can be thought of as the devices for informal investors that stay adhered

to their screens and have a brilliant sense for market course. Except if the market is in a

continued high dread, these assets will frequently dissolve drastically over a multi-day time

frame. In any case, in the event that one is searching for the best ETN/ETF to follow the VIX

momentary moves, this is at least somewhat great (Becker, Clements & McClelland, 2009).

b

Besides, the U.S. key value techniques crosswise over profit and income systems select

organizations whose valuations can help oversee valuation hazard. By joining the central

methodology with option and hazard relieving methodologies, financial specialists can remain

contributed, in this way possibly profiting by the expansion that values can offer while as yet

securing drawback (Psychoyios, Dotsis & Markellos, 2010).

c

Rising relationships, in this examination, have proposed that one could be in for a more difficult

market condition than ordinary. This should lead financial specialists to search for enhancing

resource classes—and a portion of the work on oversaw prospects systems that proposes that

might be one zone to search for less related exposures.

3.

to their screens and have a brilliant sense for market course. Except if the market is in a

continued high dread, these assets will frequently dissolve drastically over a multi-day time

frame. In any case, in the event that one is searching for the best ETN/ETF to follow the VIX

momentary moves, this is at least somewhat great (Becker, Clements & McClelland, 2009).

b

Besides, the U.S. key value techniques crosswise over profit and income systems select

organizations whose valuations can help oversee valuation hazard. By joining the central

methodology with option and hazard relieving methodologies, financial specialists can remain

contributed, in this way possibly profiting by the expansion that values can offer while as yet

securing drawback (Psychoyios, Dotsis & Markellos, 2010).

c

Rising relationships, in this examination, have proposed that one could be in for a more difficult

market condition than ordinary. This should lead financial specialists to search for enhancing

resource classes—and a portion of the work on oversaw prospects systems that proposes that

might be one zone to search for less related exposures.

3.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

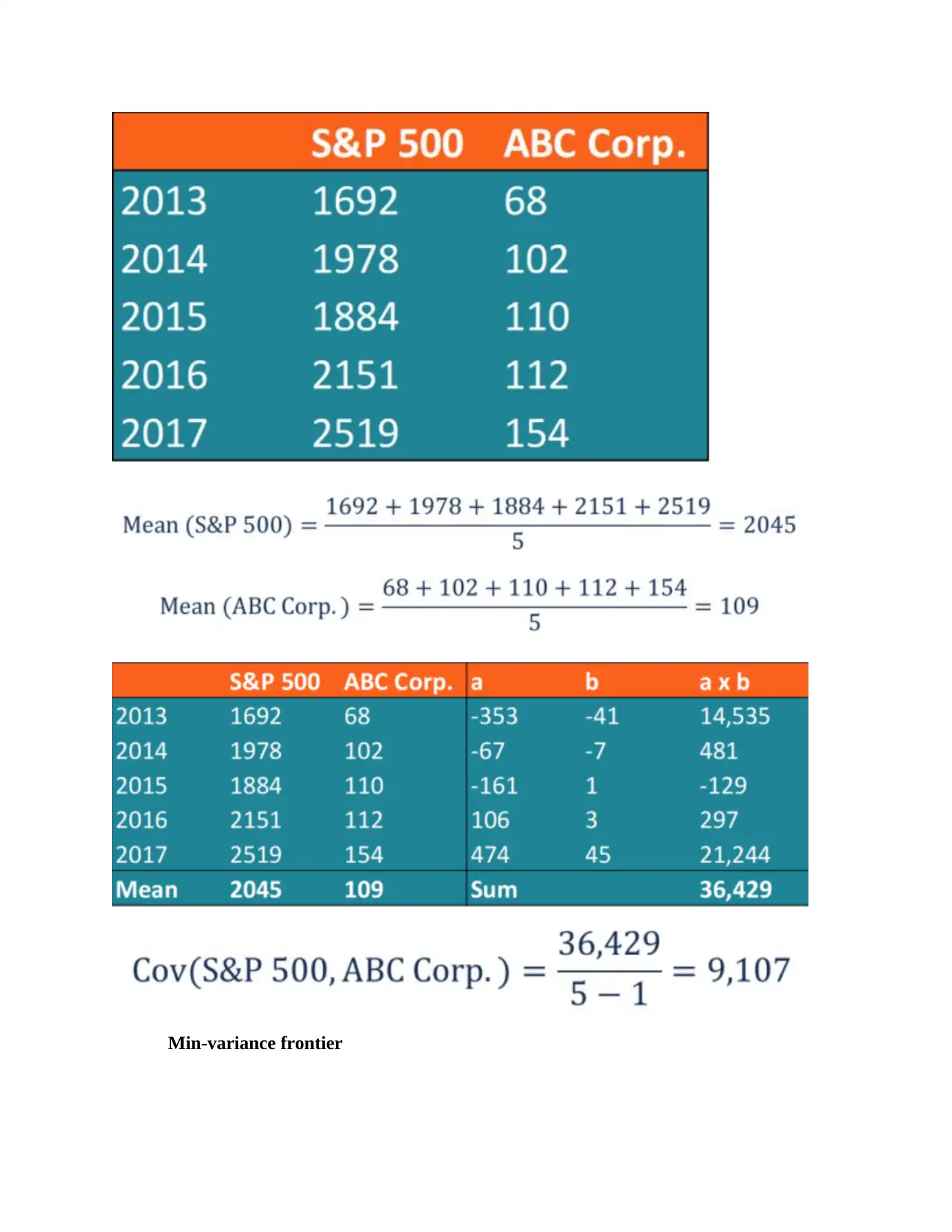

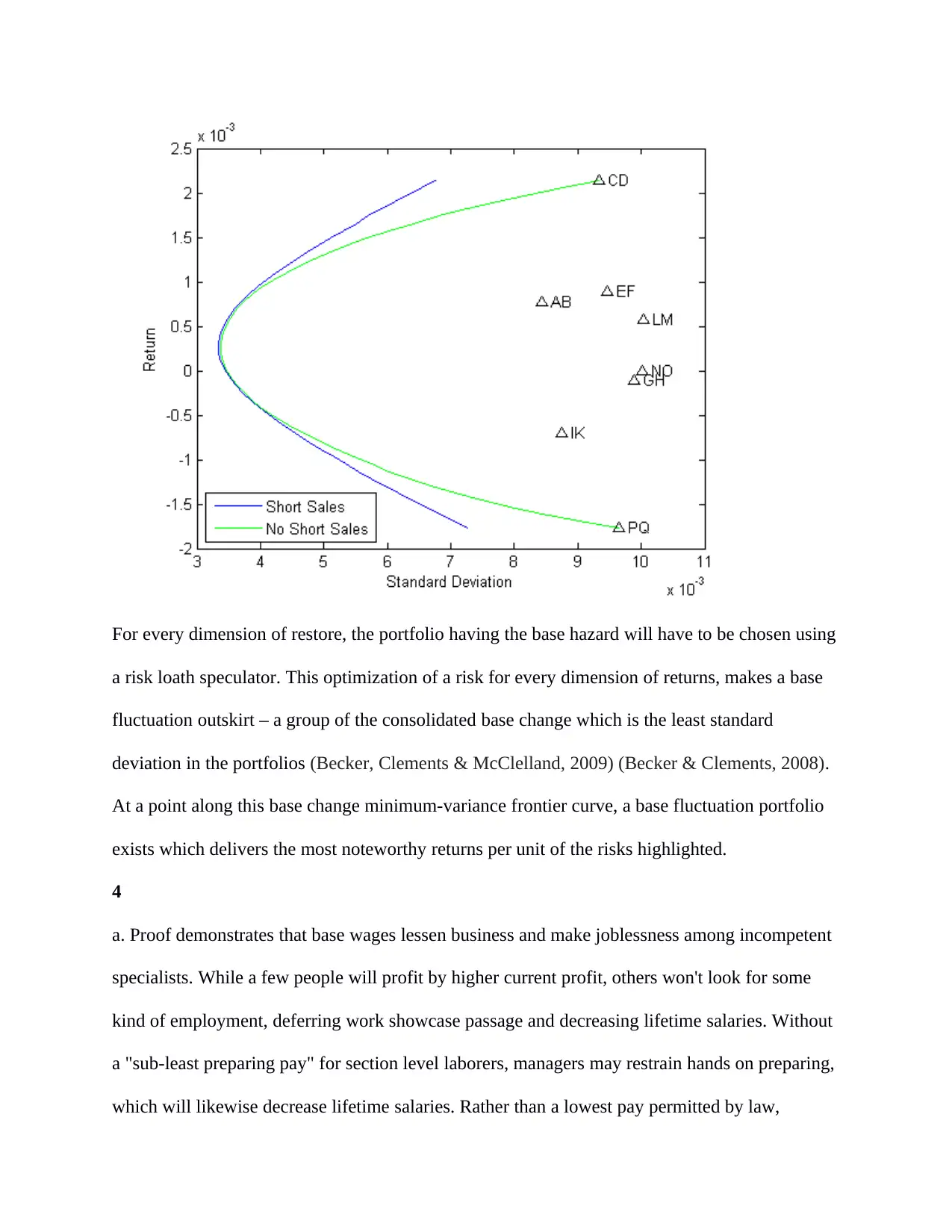

Min-variance frontier

For every dimension of restore, the portfolio having the base hazard will have to be chosen using

a risk loath speculator. This optimization of a risk for every dimension of returns, makes a base

fluctuation outskirt – a group of the consolidated base change which is the least standard

deviation in the portfolios (Becker, Clements & McClelland, 2009) (Becker & Clements, 2008).

At a point along this base change minimum-variance frontier curve, a base fluctuation portfolio

exists which delivers the most noteworthy returns per unit of the risks highlighted.

4

a. Proof demonstrates that base wages lessen business and make joblessness among incompetent

specialists. While a few people will profit by higher current profit, others won't look for some

kind of employment, deferring work showcase passage and decreasing lifetime salaries. Without

a "sub-least preparing pay" for section level laborers, managers may restrain hands on preparing,

which will likewise decrease lifetime salaries. Rather than a lowest pay permitted by law,

a risk loath speculator. This optimization of a risk for every dimension of returns, makes a base

fluctuation outskirt – a group of the consolidated base change which is the least standard

deviation in the portfolios (Becker, Clements & McClelland, 2009) (Becker & Clements, 2008).

At a point along this base change minimum-variance frontier curve, a base fluctuation portfolio

exists which delivers the most noteworthy returns per unit of the risks highlighted.

4

a. Proof demonstrates that base wages lessen business and make joblessness among incompetent

specialists. While a few people will profit by higher current profit, others won't look for some

kind of employment, deferring work showcase passage and decreasing lifetime salaries. Without

a "sub-least preparing pay" for section level laborers, managers may restrain hands on preparing,

which will likewise decrease lifetime salaries. Rather than a lowest pay permitted by law,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

policymakers should utilize less distortionary intends to help incompetent laborers, for example,

money or in-kind help (Low Pay Commission, 2008).

b. The easiest situation considers a focused work push for a solitary kind of employment. A

"competitive" the lowest wage amount permitted by law set higher than the aggressive balance

wage lessens work which is associated to two reasons (Meer & West, 2016). To begin with, the

managers will will have to go for the incompetent/semiskilled workers which will automatically

result to high operation costs, for example, in gear or in other capital. Secondly, the new info

blend and the higher wage suggests expensive rates, thus decreasing products and services

request by clients.

c. The three elements of investment in the scenario of Ontario Liberal party implementation of

the minimum wage change include Reward, Risk and Time. These elements revolves around

remuneration from the venture, and it incorporates both current salary and capital additions or

misfortunes which emerge by the expansion or decline of a speculation.

d. Lawmakers may think they are helping low-salary families put more cash in their pockets, yet

enactment can't cancel the laws of financial aspects. Piles of research uncover that ordered wage

climbs force genuine monetary expenses—and those expenses are to a great extent borne by the

precise individuals officials are endeavoring to help. Tragically endeavors to raise the lowest pay

permitted by law depend more on feeling than financial reality. Supporters regularly depict the

normal the lowest pay permitted by law worker as a solitary parent attempting to put

nourishment on the table.

5.

a. Track the execution prices and cash flows for each of your trades.

money or in-kind help (Low Pay Commission, 2008).

b. The easiest situation considers a focused work push for a solitary kind of employment. A

"competitive" the lowest wage amount permitted by law set higher than the aggressive balance

wage lessens work which is associated to two reasons (Meer & West, 2016). To begin with, the

managers will will have to go for the incompetent/semiskilled workers which will automatically

result to high operation costs, for example, in gear or in other capital. Secondly, the new info

blend and the higher wage suggests expensive rates, thus decreasing products and services

request by clients.

c. The three elements of investment in the scenario of Ontario Liberal party implementation of

the minimum wage change include Reward, Risk and Time. These elements revolves around

remuneration from the venture, and it incorporates both current salary and capital additions or

misfortunes which emerge by the expansion or decline of a speculation.

d. Lawmakers may think they are helping low-salary families put more cash in their pockets, yet

enactment can't cancel the laws of financial aspects. Piles of research uncover that ordered wage

climbs force genuine monetary expenses—and those expenses are to a great extent borne by the

precise individuals officials are endeavoring to help. Tragically endeavors to raise the lowest pay

permitted by law depend more on feeling than financial reality. Supporters regularly depict the

normal the lowest pay permitted by law worker as a solitary parent attempting to put

nourishment on the table.

5.

a. Track the execution prices and cash flows for each of your trades.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To make sure that this objective is achieved, the hedger must figure out the magnitude of the

position of the option on the exposure size, through the utilization of the formula:

N = V ßeta S&P/TSX 60 $10

Let us make an assumption the that a risk of a decline of 5% of the portfolio decline, where it

exhibits 1.2 as the beta value, if the S&P/TSX 60 index experiences a 10%, consequently the

portfolio will end up changing by 12%. With these conditions in place, a 5% decline in the value

of the portfolio is expected to associated with a decline of about 4.17% which is arrived at from

S&P/TSX 60 index (5%/1.2)

b. Evaluate the effectiveness of your hedge.

If the index happens to remain above the strike price, the market exposure will also remain

integral, but the premium that will be paid for the purposes of put will definitely not be recovered

in whatever the case (Ang, Hodrick, Xing & Zhang, 2006). When the strategy is optimally

applied, the value of the option contracts have to be determined in all instances.

c. Explain how this trading strategy can be used by fund managers to shift rapidly into

“riskon” or “risk-off” modes, depending on their very short-term outlook for

markets in general.

The system would be gainful if the list would dip under the put strike cost, with constrained risk

if the value costs were to rise. Utilizing choices contracts to support Equity portfolio directors

who are bearish might need to consider the technique of purchasing put alternatives as a type of

protection. The thought is clear: at the cost of the premium, the financial specialist can secure his

portfolio against the hazard related with a drop in the S&P/TSX 60 below the dimension of the

strike cost.

position of the option on the exposure size, through the utilization of the formula:

N = V ßeta S&P/TSX 60 $10

Let us make an assumption the that a risk of a decline of 5% of the portfolio decline, where it

exhibits 1.2 as the beta value, if the S&P/TSX 60 index experiences a 10%, consequently the

portfolio will end up changing by 12%. With these conditions in place, a 5% decline in the value

of the portfolio is expected to associated with a decline of about 4.17% which is arrived at from

S&P/TSX 60 index (5%/1.2)

b. Evaluate the effectiveness of your hedge.

If the index happens to remain above the strike price, the market exposure will also remain

integral, but the premium that will be paid for the purposes of put will definitely not be recovered

in whatever the case (Ang, Hodrick, Xing & Zhang, 2006). When the strategy is optimally

applied, the value of the option contracts have to be determined in all instances.

c. Explain how this trading strategy can be used by fund managers to shift rapidly into

“riskon” or “risk-off” modes, depending on their very short-term outlook for

markets in general.

The system would be gainful if the list would dip under the put strike cost, with constrained risk

if the value costs were to rise. Utilizing choices contracts to support Equity portfolio directors

who are bearish might need to consider the technique of purchasing put alternatives as a type of

protection. The thought is clear: at the cost of the premium, the financial specialist can secure his

portfolio against the hazard related with a drop in the S&P/TSX 60 below the dimension of the

strike cost.

References

Ang, A., Hodrick, R. J., Xing, Y., & Zhang, X. (2006). The cross‐section of volatility and

expected returns. The Journal of Finance, 61(1), 259-299.

Baumol, W., Goldfeld, S. M., Gordon, L. A., & Koehn, F. M. (2012). The economics of mutual

fund markets: Competition versus regulation (Vol. 7). Springer Science & Business

Media.

Becker, R., & Clements, A. E. (2008). Are combination forecasts of S&P 500 volatility

statistically superior?. International Journal of Forecasting, 24(1), 122-133.

Becker, R., Clements, A. E., & McClelland, A. (2009). The jump component of S&P 500

volatility and the VIX index. Journal of Banking & Finance, 33(6), 1033-1038.

Becker, R., Clements, A. E., & McClelland, A. (2009). The jump component of S&P 500

volatility and the VIX index. Journal of Banking & Finance, 33(6), 1033-1038.

Cohen, L., Frazzini, A., & Malloy, C. (2008). The small world of investing: Board connections

and mutual fund returns. Journal of Political Economy, 116(5), 951-979.

Low Pay Commission. (2008). National minimum wage: Low pay commission report 2008 (Vol.

7333). The Stationery Office.

Meer, J., & West, J. (2016). Effects of the minimum wage on employment dynamics. Journal of

Human Resources, 51(2), 500-522.

Phalippou, L., & Gottschalg, O. (2008). The performance of private equity funds. The Review of

Financial Studies, 22(4), 1747-1776.

Psychoyios, D., Dotsis, G., & Markellos, R. N. (2010). A jump diffusion model for VIX

volatility options and futures. Review of Quantitative Finance and Accounting, 35(3),

245-269.

Ang, A., Hodrick, R. J., Xing, Y., & Zhang, X. (2006). The cross‐section of volatility and

expected returns. The Journal of Finance, 61(1), 259-299.

Baumol, W., Goldfeld, S. M., Gordon, L. A., & Koehn, F. M. (2012). The economics of mutual

fund markets: Competition versus regulation (Vol. 7). Springer Science & Business

Media.

Becker, R., & Clements, A. E. (2008). Are combination forecasts of S&P 500 volatility

statistically superior?. International Journal of Forecasting, 24(1), 122-133.

Becker, R., Clements, A. E., & McClelland, A. (2009). The jump component of S&P 500

volatility and the VIX index. Journal of Banking & Finance, 33(6), 1033-1038.

Becker, R., Clements, A. E., & McClelland, A. (2009). The jump component of S&P 500

volatility and the VIX index. Journal of Banking & Finance, 33(6), 1033-1038.

Cohen, L., Frazzini, A., & Malloy, C. (2008). The small world of investing: Board connections

and mutual fund returns. Journal of Political Economy, 116(5), 951-979.

Low Pay Commission. (2008). National minimum wage: Low pay commission report 2008 (Vol.

7333). The Stationery Office.

Meer, J., & West, J. (2016). Effects of the minimum wage on employment dynamics. Journal of

Human Resources, 51(2), 500-522.

Phalippou, L., & Gottschalg, O. (2008). The performance of private equity funds. The Review of

Financial Studies, 22(4), 1747-1776.

Psychoyios, D., Dotsis, G., & Markellos, R. N. (2010). A jump diffusion model for VIX

volatility options and futures. Review of Quantitative Finance and Accounting, 35(3),

245-269.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.