Solved Exam: FINM01020R Introductory Finance and Accounting

VerifiedAdded on 2023/06/13

|11

|2121

|78

Homework Assignment

AI Summary

This document presents a solved examination paper for the Introductory Finance and Accounting module (FINM01020R). It includes detailed solutions to questions covering cost analysis, keep or drop decisions, cash budgeting, and financial statement preparation. The analysis extends to calculating net profit margins and current ratios to assess the business's financial health. Recommendations are provided for improving cash flow and investment strategies. The document also emphasizes factors beyond numerical analysis, such as employee efficiency and market demand, which influence business decisions. Desklib offers more resources like this to aid students in their studies.

Examination Answer Book – ACC100320R

Examination

Module Number:

FINM01020R

Module Title:

Introductory

Finance and

Accounting

Student Number Date

/ /

For

Exa

min

er’s

Use

Onl

y

Question Marks

Examiner Assessor

Instructions to Students

1. Enter the details required on this cover. Do not write in the

shaded section.

2. All calculations and rough work must be done in this book.

3. When done, submit to the relevant area of your NILE site

1

2

3

4

5

6

7

8

9

10

11

12

13

14

Page 1 of 11

Examination

Module Number:

FINM01020R

Module Title:

Introductory

Finance and

Accounting

Student Number Date

/ /

For

Exa

min

er’s

Use

Onl

y

Question Marks

Examiner Assessor

Instructions to Students

1. Enter the details required on this cover. Do not write in the

shaded section.

2. All calculations and rough work must be done in this book.

3. When done, submit to the relevant area of your NILE site

1

2

3

4

5

6

7

8

9

10

11

12

13

14

Page 1 of 11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

15

Total

%

Examiner’s signature

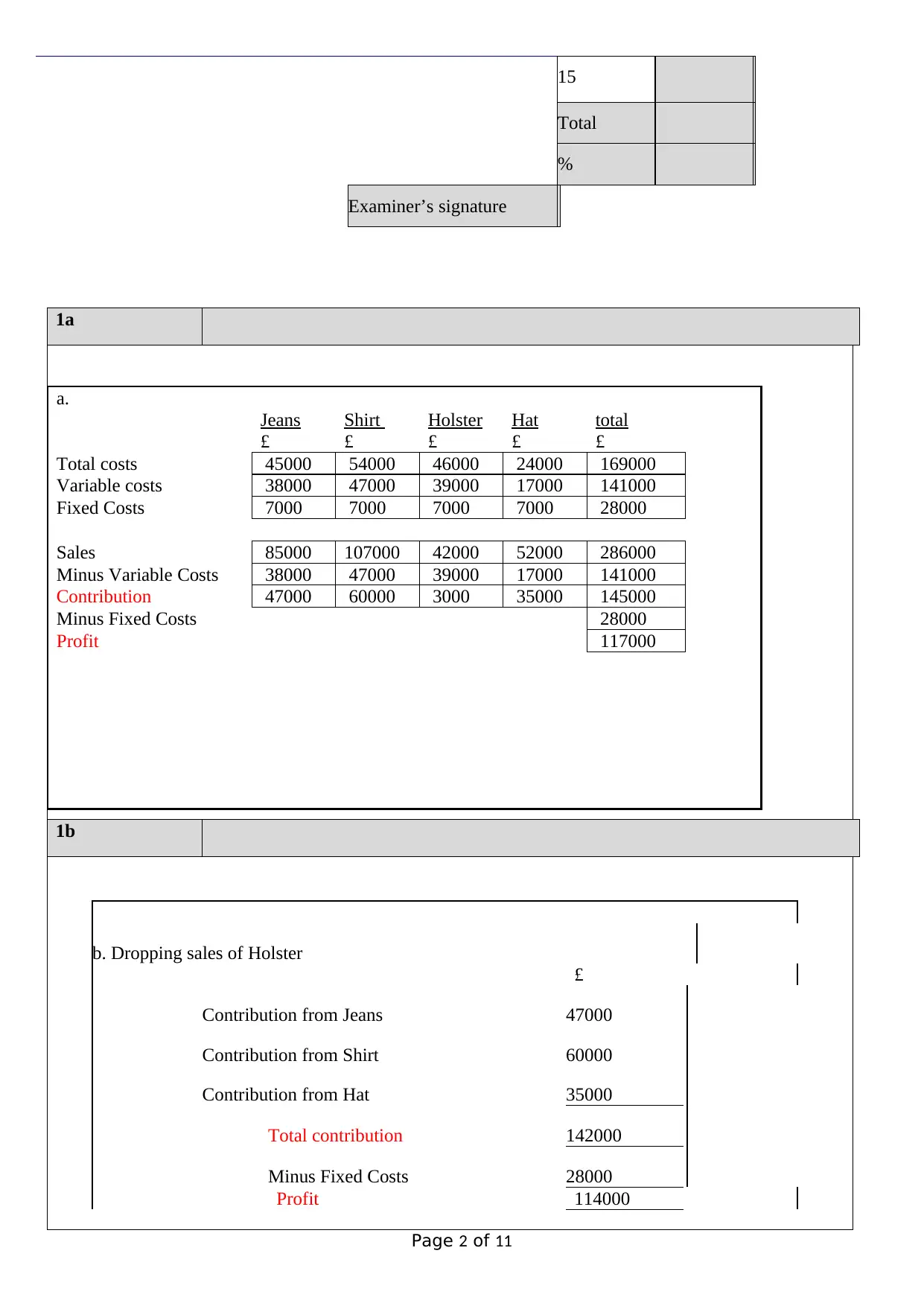

1a

a.

Jeans Shirt Holster Hat total

£ £ £ £ £

Total costs 45000 54000 46000 24000 169000

Variable costs 38000 47000 39000 17000 141000

Fixed Costs 7000 7000 7000 7000 28000

Sales 85000 107000 42000 52000 286000

Minus Variable Costs 38000 47000 39000 17000 141000

Contribution 47000 60000 3000 35000 145000

Minus Fixed Costs 28000

Profit 117000

1b

b. Dropping sales of Holster

£

Contribution from Jeans 47000

Contribution from Shirt 60000

Contribution from Hat 35000

Total contribution 142000

Minus Fixed Costs 28000

Profit 114000

Page 2 of 11

Total

%

Examiner’s signature

1a

a.

Jeans Shirt Holster Hat total

£ £ £ £ £

Total costs 45000 54000 46000 24000 169000

Variable costs 38000 47000 39000 17000 141000

Fixed Costs 7000 7000 7000 7000 28000

Sales 85000 107000 42000 52000 286000

Minus Variable Costs 38000 47000 39000 17000 141000

Contribution 47000 60000 3000 35000 145000

Minus Fixed Costs 28000

Profit 117000

1b

b. Dropping sales of Holster

£

Contribution from Jeans 47000

Contribution from Shirt 60000

Contribution from Hat 35000

Total contribution 142000

Minus Fixed Costs 28000

Profit 114000

Page 2 of 11

1C

On the basis of above result of section (a) and (b), it is advisable to Lucy that they should not dropped the

idea of further production or sales of Holsters. It is because despite of being higher fixed cost than the

contribution, the company can earn more profit if they increase the sales of the Holster product. In the given

scenario, if the company will immediately drop the idea of production and sales of Holster product than

their profit will decrease by £3000. It is because previously the fixed cost of 28000 is equally charged from

all the four product which now charged from only three products only. After analyzing the above result, it is

advisable to Lucy that they should adopt the strategies to enhance the contribution margin of Holster

product rather than dropping production and sales of Holster product. This is advisable to the company on

the basis of decrease in profit by £3000. Now the strategies which are advisable to company on the basis of

which Lucy can enhance its sales are promotion on social media sites. It means Lucy need to promote its

products on social media sites such as Instagram, Facebook, YouTube etc. via offering various discounts

and EMI payment facility on their Holster products. Further, it is also recommendable to Lucy that they

should acquire a equipment with the help of which they can able to produce high units of Holster in

minimum time. The impact of which the overall variable cost of producing a product get decreases and

contribution value and margin of Holster get increases. In addition, it is also recommended to Lucy that

rather than dropping the production and sales of Holster product they should increase the price of their

products after proper promotion strategy (Wolak, 2021). It means if the sales units increases with constant

sales price and variable cost then the contribution margin of that product will not increase. Thus, it is

advisable to the company and Lucy that they should first analyse the demand and on the basis of demand

increase their product sales price. Lastly, it can be said that Lucy have to continue with the production as

well as sales of Holster product without considering the dropping decision. It is because this will result into

the decrease in the profit from £117000 to £114000.

Page 3 of 11

On the basis of above result of section (a) and (b), it is advisable to Lucy that they should not dropped the

idea of further production or sales of Holsters. It is because despite of being higher fixed cost than the

contribution, the company can earn more profit if they increase the sales of the Holster product. In the given

scenario, if the company will immediately drop the idea of production and sales of Holster product than

their profit will decrease by £3000. It is because previously the fixed cost of 28000 is equally charged from

all the four product which now charged from only three products only. After analyzing the above result, it is

advisable to Lucy that they should adopt the strategies to enhance the contribution margin of Holster

product rather than dropping production and sales of Holster product. This is advisable to the company on

the basis of decrease in profit by £3000. Now the strategies which are advisable to company on the basis of

which Lucy can enhance its sales are promotion on social media sites. It means Lucy need to promote its

products on social media sites such as Instagram, Facebook, YouTube etc. via offering various discounts

and EMI payment facility on their Holster products. Further, it is also recommendable to Lucy that they

should acquire a equipment with the help of which they can able to produce high units of Holster in

minimum time. The impact of which the overall variable cost of producing a product get decreases and

contribution value and margin of Holster get increases. In addition, it is also recommended to Lucy that

rather than dropping the production and sales of Holster product they should increase the price of their

products after proper promotion strategy (Wolak, 2021). It means if the sales units increases with constant

sales price and variable cost then the contribution margin of that product will not increase. Thus, it is

advisable to the company and Lucy that they should first analyse the demand and on the basis of demand

increase their product sales price. Lastly, it can be said that Lucy have to continue with the production as

well as sales of Holster product without considering the dropping decision. It is because this will result into

the decrease in the profit from £117000 to £114000.

Page 3 of 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

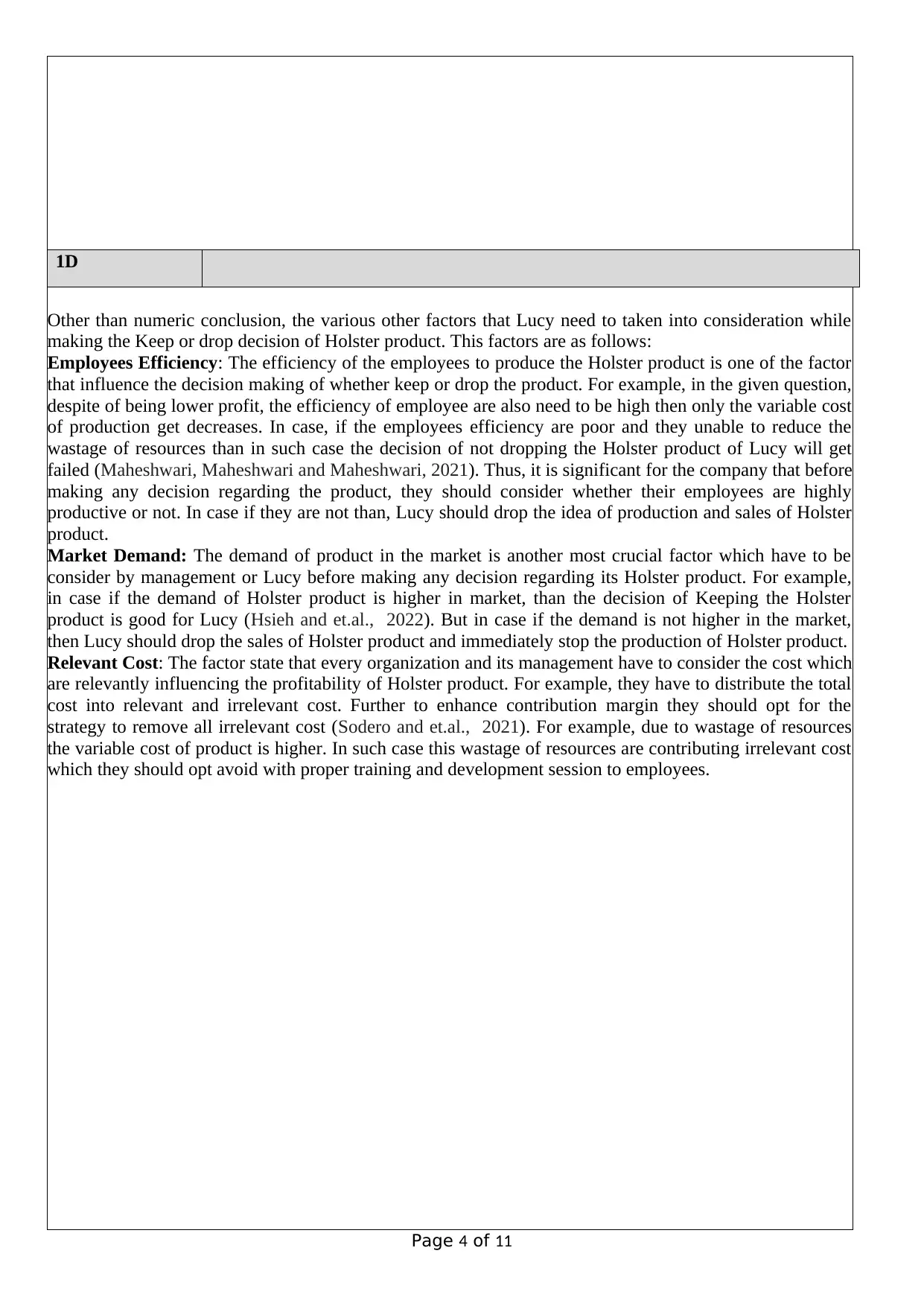

1D

Other than numeric conclusion, the various other factors that Lucy need to taken into consideration while

making the Keep or drop decision of Holster product. This factors are as follows:

Employees Efficiency: The efficiency of the employees to produce the Holster product is one of the factor

that influence the decision making of whether keep or drop the product. For example, in the given question,

despite of being lower profit, the efficiency of employee are also need to be high then only the variable cost

of production get decreases. In case, if the employees efficiency are poor and they unable to reduce the

wastage of resources than in such case the decision of not dropping the Holster product of Lucy will get

failed (Maheshwari, Maheshwari and Maheshwari, 2021). Thus, it is significant for the company that before

making any decision regarding the product, they should consider whether their employees are highly

productive or not. In case if they are not than, Lucy should drop the idea of production and sales of Holster

product.

Market Demand: The demand of product in the market is another most crucial factor which have to be

consider by management or Lucy before making any decision regarding its Holster product. For example,

in case if the demand of Holster product is higher in market, than the decision of Keeping the Holster

product is good for Lucy (Hsieh and et.al., 2022). But in case if the demand is not higher in the market,

then Lucy should drop the sales of Holster product and immediately stop the production of Holster product.

Relevant Cost: The factor state that every organization and its management have to consider the cost which

are relevantly influencing the profitability of Holster product. For example, they have to distribute the total

cost into relevant and irrelevant cost. Further to enhance contribution margin they should opt for the

strategy to remove all irrelevant cost (Sodero and et.al., 2021). For example, due to wastage of resources

the variable cost of product is higher. In such case this wastage of resources are contributing irrelevant cost

which they should opt avoid with proper training and development session to employees.

Page 4 of 11

Other than numeric conclusion, the various other factors that Lucy need to taken into consideration while

making the Keep or drop decision of Holster product. This factors are as follows:

Employees Efficiency: The efficiency of the employees to produce the Holster product is one of the factor

that influence the decision making of whether keep or drop the product. For example, in the given question,

despite of being lower profit, the efficiency of employee are also need to be high then only the variable cost

of production get decreases. In case, if the employees efficiency are poor and they unable to reduce the

wastage of resources than in such case the decision of not dropping the Holster product of Lucy will get

failed (Maheshwari, Maheshwari and Maheshwari, 2021). Thus, it is significant for the company that before

making any decision regarding the product, they should consider whether their employees are highly

productive or not. In case if they are not than, Lucy should drop the idea of production and sales of Holster

product.

Market Demand: The demand of product in the market is another most crucial factor which have to be

consider by management or Lucy before making any decision regarding its Holster product. For example,

in case if the demand of Holster product is higher in market, than the decision of Keeping the Holster

product is good for Lucy (Hsieh and et.al., 2022). But in case if the demand is not higher in the market,

then Lucy should drop the sales of Holster product and immediately stop the production of Holster product.

Relevant Cost: The factor state that every organization and its management have to consider the cost which

are relevantly influencing the profitability of Holster product. For example, they have to distribute the total

cost into relevant and irrelevant cost. Further to enhance contribution margin they should opt for the

strategy to remove all irrelevant cost (Sodero and et.al., 2021). For example, due to wastage of resources

the variable cost of product is higher. In such case this wastage of resources are contributing irrelevant cost

which they should opt avoid with proper training and development session to employees.

Page 4 of 11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

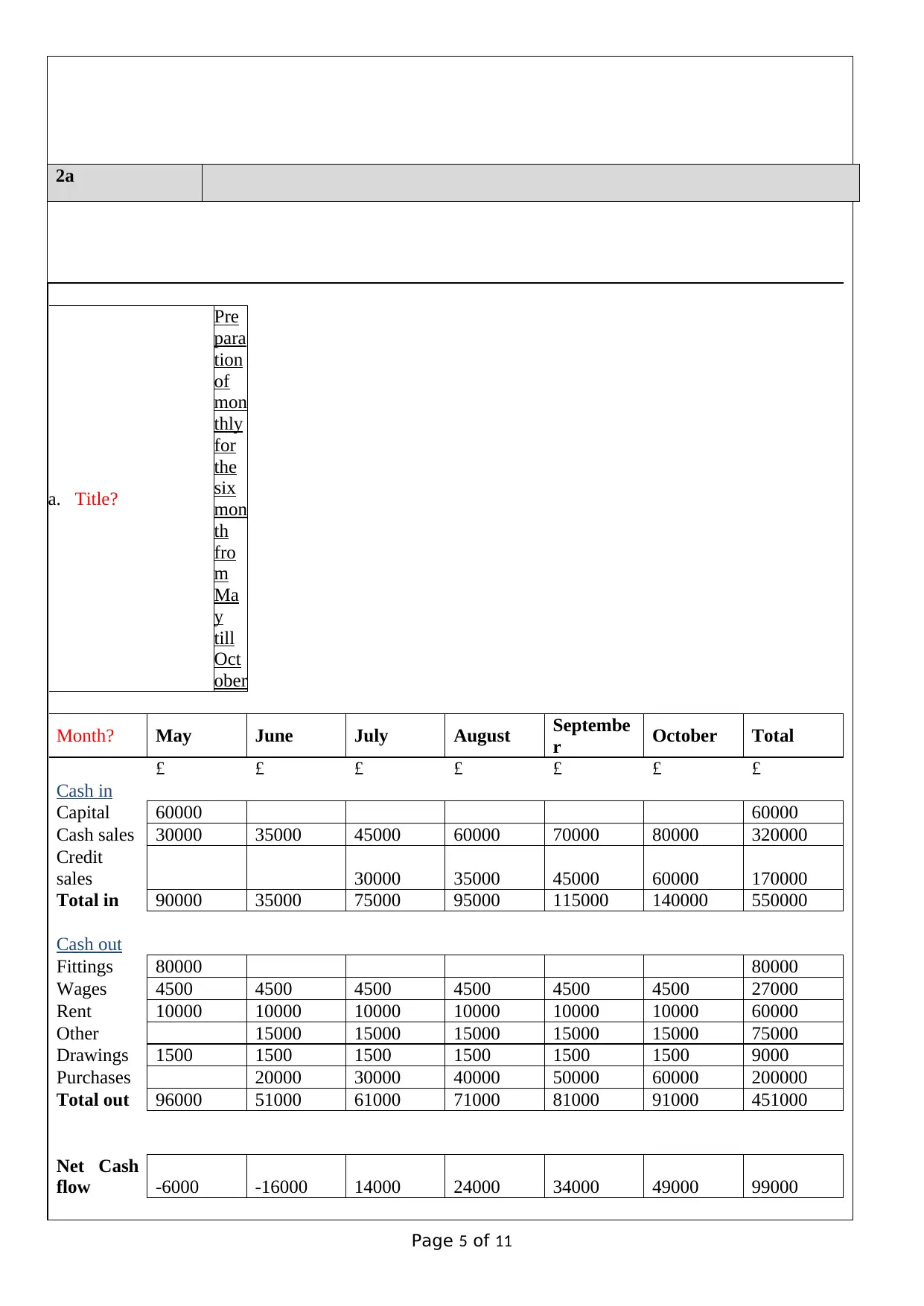

2a

a. Title?

Pre

para

tion

of

mon

thly

for

the

six

mon

th

fro

m

Ma

y

till

Oct

ober

Month? May June July August Septembe

r October Total

£ £ £ £ £ £ £

Cash in

Capital 60000 60000

Cash sales 30000 35000 45000 60000 70000 80000 320000

Credit

sales 30000 35000 45000 60000 170000

Total in 90000 35000 75000 95000 115000 140000 550000

Cash out

Fittings 80000 80000

Wages 4500 4500 4500 4500 4500 4500 27000

Rent 10000 10000 10000 10000 10000 10000 60000

Other 15000 15000 15000 15000 15000 75000

Drawings 1500 1500 1500 1500 1500 1500 9000

Purchases 20000 30000 40000 50000 60000 200000

Total out 96000 51000 61000 71000 81000 91000 451000

Net Cash

flow -6000 -16000 14000 24000 34000 49000 99000

Page 5 of 11

a. Title?

Pre

para

tion

of

mon

thly

for

the

six

mon

th

fro

m

Ma

y

till

Oct

ober

Month? May June July August Septembe

r October Total

£ £ £ £ £ £ £

Cash in

Capital 60000 60000

Cash sales 30000 35000 45000 60000 70000 80000 320000

Credit

sales 30000 35000 45000 60000 170000

Total in 90000 35000 75000 95000 115000 140000 550000

Cash out

Fittings 80000 80000

Wages 4500 4500 4500 4500 4500 4500 27000

Rent 10000 10000 10000 10000 10000 10000 60000

Other 15000 15000 15000 15000 15000 75000

Drawings 1500 1500 1500 1500 1500 1500 9000

Purchases 20000 30000 40000 50000 60000 200000

Total out 96000 51000 61000 71000 81000 91000 451000

Net Cash

flow -6000 -16000 14000 24000 34000 49000 99000

Page 5 of 11

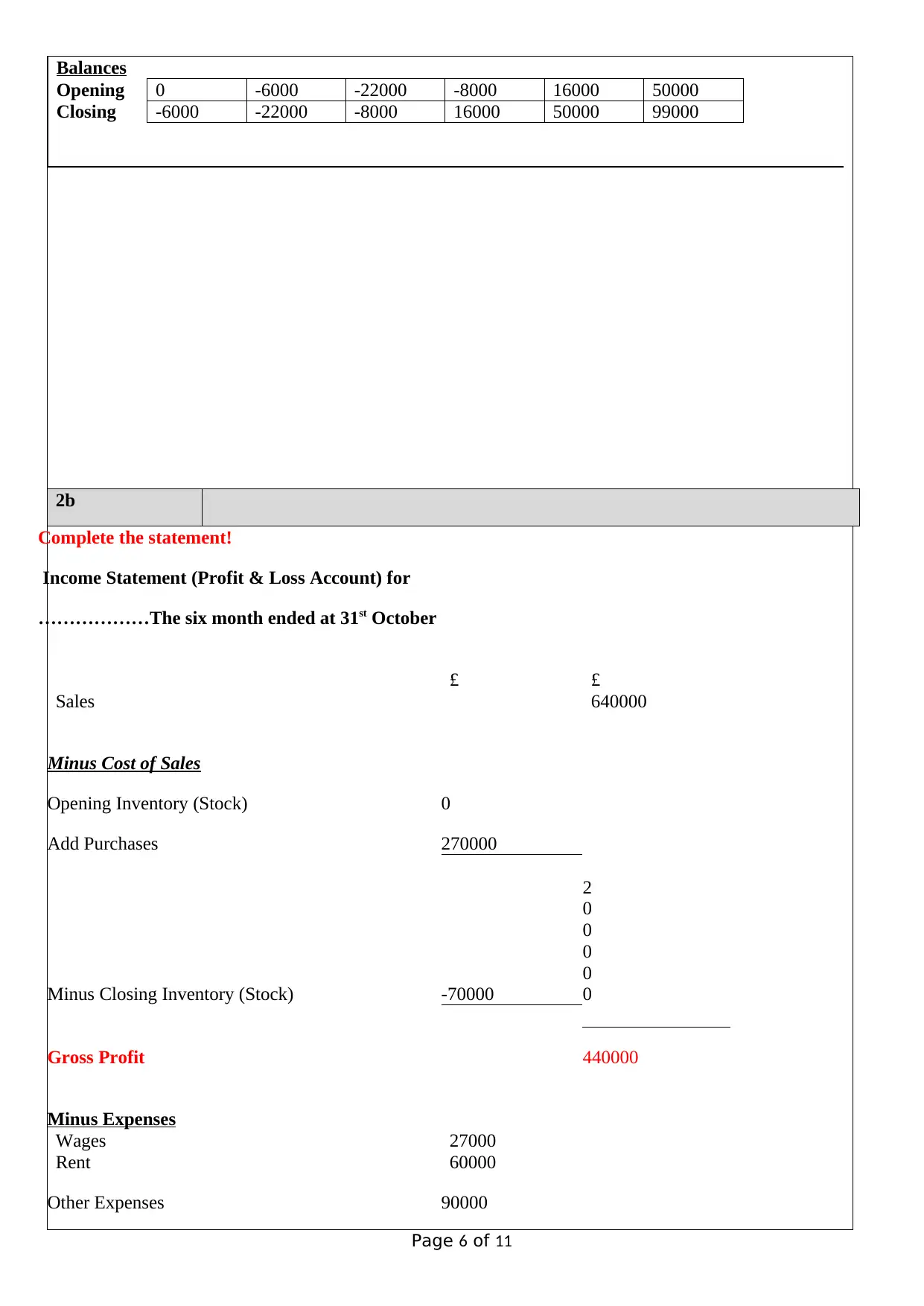

Balances

Opening 0 -6000 -22000 -8000 16000 50000

Closing -6000 -22000 -8000 16000 50000 99000

2b

Complete the statement!

Income Statement (Profit & Loss Account) for

………………The six month ended at 31st October

£ £

Sales 640000

Minus Cost of Sales

Opening Inventory (Stock) 0

Add Purchases 270000

Minus Closing Inventory (Stock) -70000

2

0

0

0

0

0

Gross Profit 440000

Minus Expenses

Wages 27000

Rent 60000

Other Expenses 90000

Page 6 of 11

Opening 0 -6000 -22000 -8000 16000 50000

Closing -6000 -22000 -8000 16000 50000 99000

2b

Complete the statement!

Income Statement (Profit & Loss Account) for

………………The six month ended at 31st October

£ £

Sales 640000

Minus Cost of Sales

Opening Inventory (Stock) 0

Add Purchases 270000

Minus Closing Inventory (Stock) -70000

2

0

0

0

0

0

Gross Profit 440000

Minus Expenses

Wages 27000

Rent 60000

Other Expenses 90000

Page 6 of 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

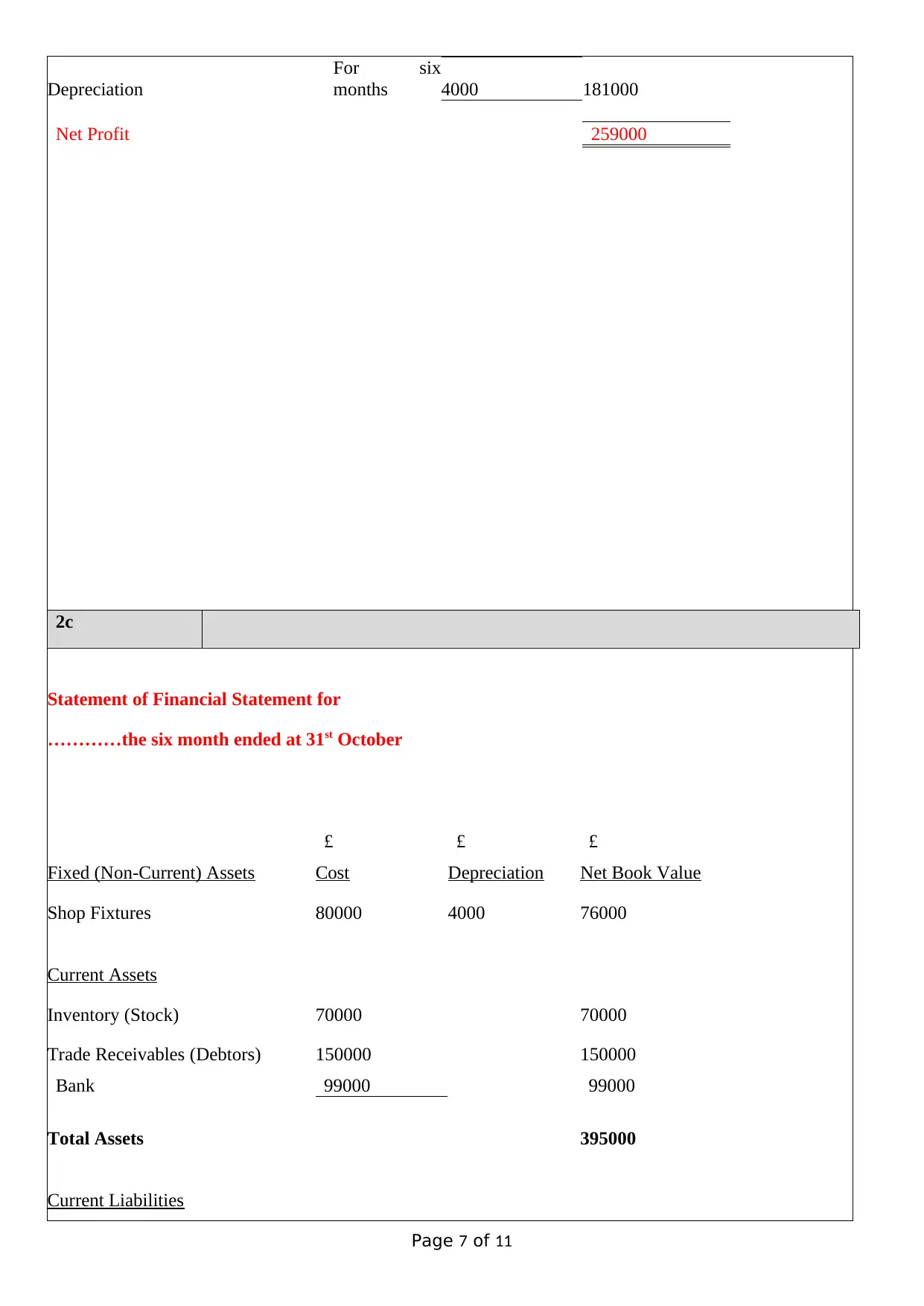

Depreciation

For six

months 4000 181000

Net Profit 259000

2c

Statement of Financial Statement for

…………the six month ended at 31st October

£ £ £

Fixed (Non-Current) Assets Cost Depreciation Net Book Value

Shop Fixtures 80000 4000 76000

Current Assets

Inventory (Stock) 70000 70000

Trade Receivables (Debtors) 150000 150000

Bank 99000 99000

Total Assets 395000

Current Liabilities

Page 7 of 11

For six

months 4000 181000

Net Profit 259000

2c

Statement of Financial Statement for

…………the six month ended at 31st October

£ £ £

Fixed (Non-Current) Assets Cost Depreciation Net Book Value

Shop Fixtures 80000 4000 76000

Current Assets

Inventory (Stock) 70000 70000

Trade Receivables (Debtors) 150000 150000

Bank 99000 99000

Total Assets 395000

Current Liabilities

Page 7 of 11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

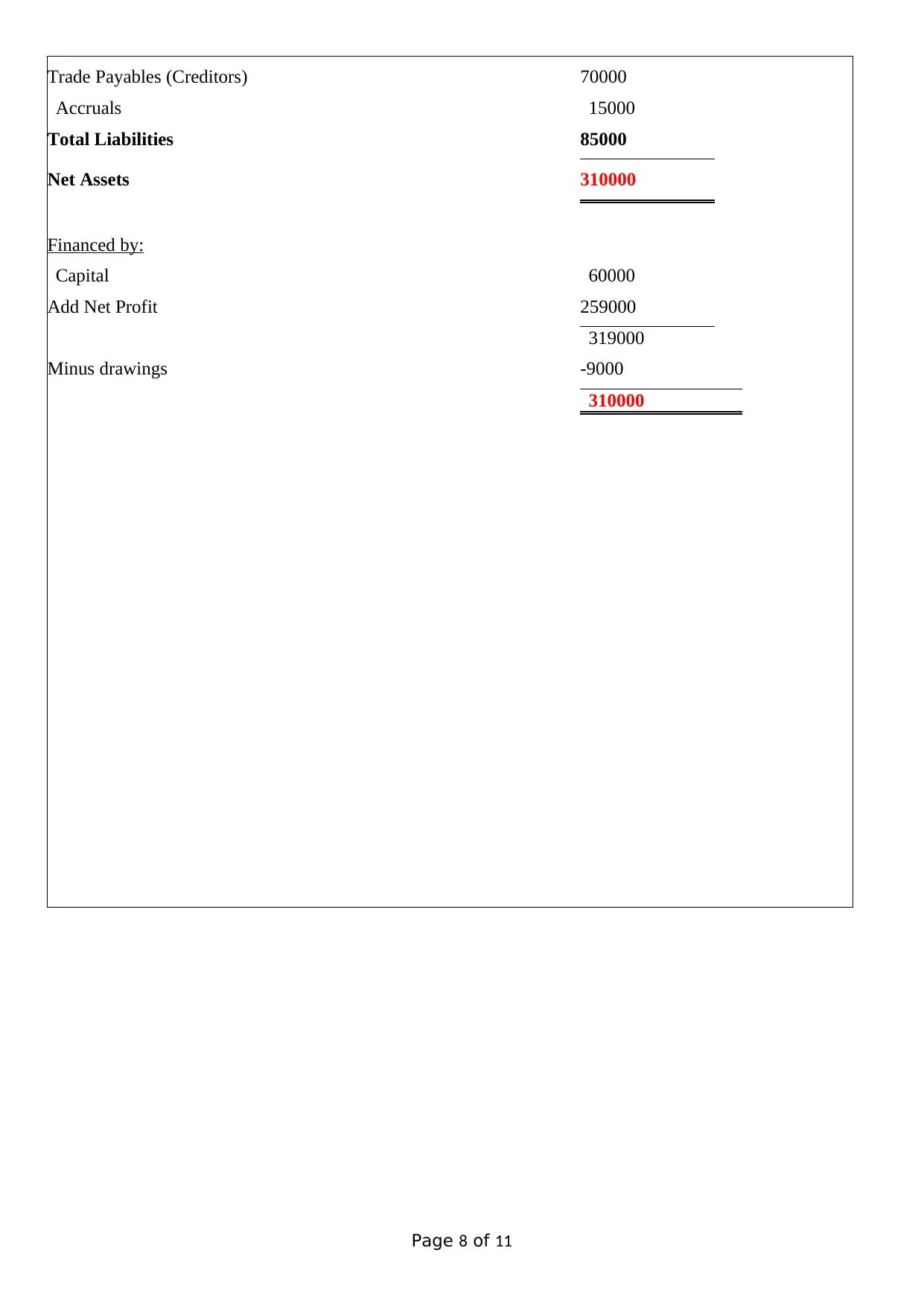

Trade Payables (Creditors) 70000

Accruals 15000

Total Liabilities 85000

Net Assets 310000

Financed by:

Capital 60000

Add Net Profit 259000

319000

Minus drawings -9000

310000

Page 8 of 11

Accruals 15000

Total Liabilities 85000

Net Assets 310000

Financed by:

Capital 60000

Add Net Profit 259000

319000

Minus drawings -9000

310000

Page 8 of 11

2d

From the cash budget as prepared for Lucy's business it has been identified that the business is quite viable

in terms of meeting its obligations on time, however business is facing with negative cash balances which

indicates that to be viable in the months of May and June, it needs to make arrangement for overdraft

facilities with their bankers. Therefore, viability of Lucy's business can be seen post the month of June

where it is able to realize positive cash balances for the business. The reasons for poor viability in the earlier

months is due to the mismatch between the credit period extend to account receivables and credit period

granted by accounts payables (Carreras Simó and Coenders, 2020). Accordingly, there are certain

recommendations that could be provided to Lucy to ensure better viability within the earlier period of their

business, such as the following:

Lucy should reduce the credit period extended to its debtors to one month in order to establish

balance between account receivable collection period and account payables payment period. This

would allow her to avoid the scenario of negative cash balances and extra costs associated with

making arrangements for overdraft facilities.

Also, Lucy could ask for higher credit period from her suppliers to get rid of liquidity crisis in the

initial period of her business start up.

Page 9 of 11

From the cash budget as prepared for Lucy's business it has been identified that the business is quite viable

in terms of meeting its obligations on time, however business is facing with negative cash balances which

indicates that to be viable in the months of May and June, it needs to make arrangement for overdraft

facilities with their bankers. Therefore, viability of Lucy's business can be seen post the month of June

where it is able to realize positive cash balances for the business. The reasons for poor viability in the earlier

months is due to the mismatch between the credit period extend to account receivables and credit period

granted by accounts payables (Carreras Simó and Coenders, 2020). Accordingly, there are certain

recommendations that could be provided to Lucy to ensure better viability within the earlier period of their

business, such as the following:

Lucy should reduce the credit period extended to its debtors to one month in order to establish

balance between account receivable collection period and account payables payment period. This

would allow her to avoid the scenario of negative cash balances and extra costs associated with

making arrangements for overdraft facilities.

Also, Lucy could ask for higher credit period from her suppliers to get rid of liquidity crisis in the

initial period of her business start up.

Page 9 of 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

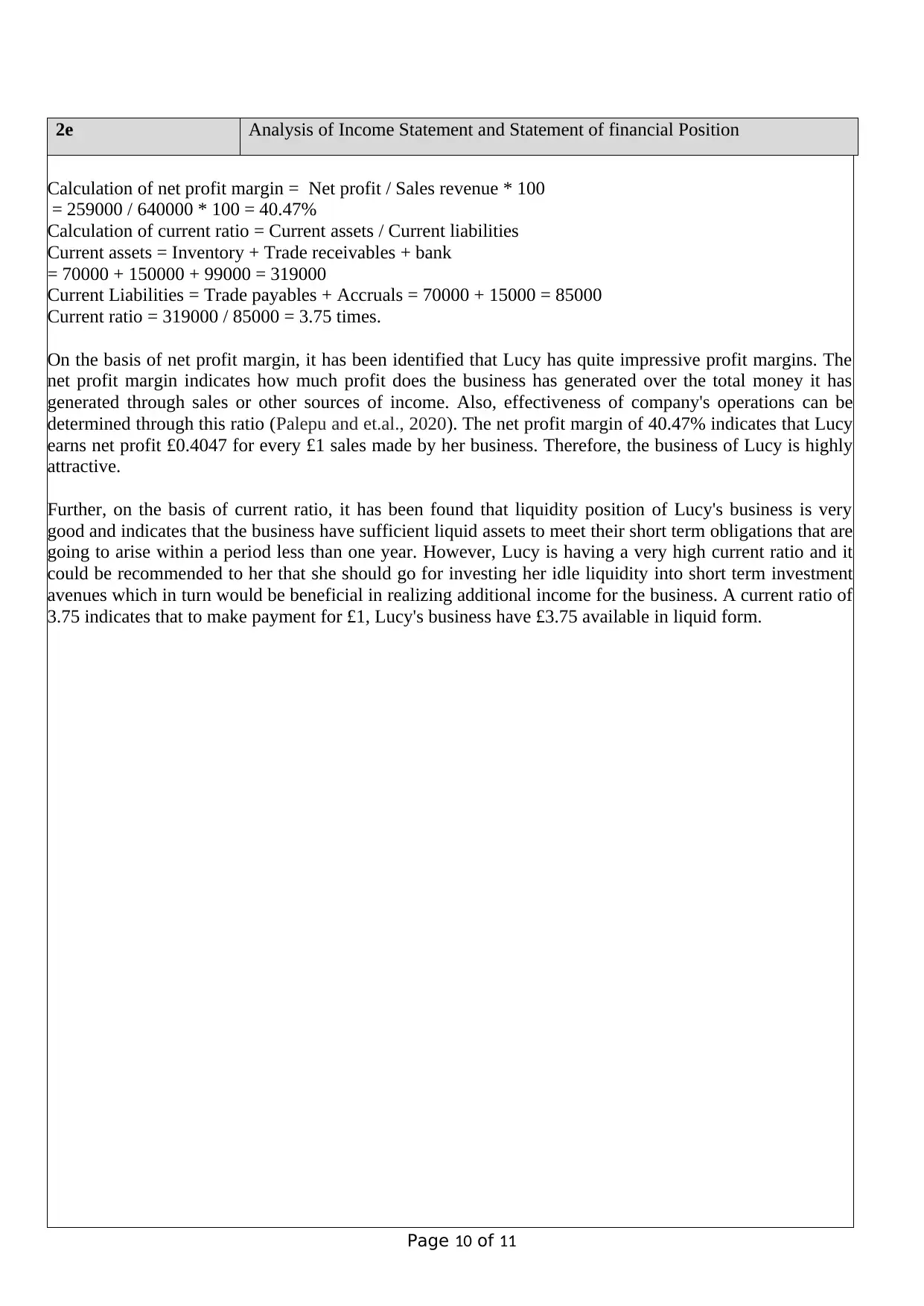

2e Analysis of Income Statement and Statement of financial Position

Calculation of net profit margin = Net profit / Sales revenue * 100

= 259000 / 640000 * 100 = 40.47%

Calculation of current ratio = Current assets / Current liabilities

Current assets = Inventory + Trade receivables + bank

= 70000 + 150000 + 99000 = 319000

Current Liabilities = Trade payables + Accruals = 70000 + 15000 = 85000

Current ratio = 319000 / 85000 = 3.75 times.

On the basis of net profit margin, it has been identified that Lucy has quite impressive profit margins. The

net profit margin indicates how much profit does the business has generated over the total money it has

generated through sales or other sources of income. Also, effectiveness of company's operations can be

determined through this ratio (Palepu and et.al., 2020). The net profit margin of 40.47% indicates that Lucy

earns net profit £0.4047 for every £1 sales made by her business. Therefore, the business of Lucy is highly

attractive.

Further, on the basis of current ratio, it has been found that liquidity position of Lucy's business is very

good and indicates that the business have sufficient liquid assets to meet their short term obligations that are

going to arise within a period less than one year. However, Lucy is having a very high current ratio and it

could be recommended to her that she should go for investing her idle liquidity into short term investment

avenues which in turn would be beneficial in realizing additional income for the business. A current ratio of

3.75 indicates that to make payment for £1, Lucy's business have £3.75 available in liquid form.

Page 10 of 11

Calculation of net profit margin = Net profit / Sales revenue * 100

= 259000 / 640000 * 100 = 40.47%

Calculation of current ratio = Current assets / Current liabilities

Current assets = Inventory + Trade receivables + bank

= 70000 + 150000 + 99000 = 319000

Current Liabilities = Trade payables + Accruals = 70000 + 15000 = 85000

Current ratio = 319000 / 85000 = 3.75 times.

On the basis of net profit margin, it has been identified that Lucy has quite impressive profit margins. The

net profit margin indicates how much profit does the business has generated over the total money it has

generated through sales or other sources of income. Also, effectiveness of company's operations can be

determined through this ratio (Palepu and et.al., 2020). The net profit margin of 40.47% indicates that Lucy

earns net profit £0.4047 for every £1 sales made by her business. Therefore, the business of Lucy is highly

attractive.

Further, on the basis of current ratio, it has been found that liquidity position of Lucy's business is very

good and indicates that the business have sufficient liquid assets to meet their short term obligations that are

going to arise within a period less than one year. However, Lucy is having a very high current ratio and it

could be recommended to her that she should go for investing her idle liquidity into short term investment

avenues which in turn would be beneficial in realizing additional income for the business. A current ratio of

3.75 indicates that to make payment for £1, Lucy's business have £3.75 available in liquid form.

Page 10 of 11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Carreras Simó, M. and Coenders, G., 2020. Principal component analysis of financial statements: a

compositional approach= Análisis en componentes principales de los estados financieros: un

enfoque composicional. Revista de Métodos Cuantitativos para la Economía y la Empresa, 2020,

vol. 29, p. 18-37.

Palepu, K. G., and et.al., 2020. Business analysis and valuation: Using financial statements. Cengage AU.

Wolak, F. A., 2021. Market design in an intermittent renewable future: cost recovery with zero-marginal-

cost resources. IEEE Power and Energy Magazine. 19(1). pp.29-40.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of Management

Accounting. Sultan Chand & Sons.

Hsieh, H. P. and et.al., 2022. A decision framework to recommend cruising locations for taxi drivers under

the constraint of booking information. ACM Transactions on Management Information Systems

(TMIS). 13(3). pp.1-30.

Sodero, A. C. and et.al., 2021. The strategic drivers of drop-shipping and retail store sales for seasonal

products. Journal of Retailing. 97(4). pp.561-581.

Page 11 of 11

Carreras Simó, M. and Coenders, G., 2020. Principal component analysis of financial statements: a

compositional approach= Análisis en componentes principales de los estados financieros: un

enfoque composicional. Revista de Métodos Cuantitativos para la Economía y la Empresa, 2020,

vol. 29, p. 18-37.

Palepu, K. G., and et.al., 2020. Business analysis and valuation: Using financial statements. Cengage AU.

Wolak, F. A., 2021. Market design in an intermittent renewable future: cost recovery with zero-marginal-

cost resources. IEEE Power and Energy Magazine. 19(1). pp.29-40.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of Management

Accounting. Sultan Chand & Sons.

Hsieh, H. P. and et.al., 2022. A decision framework to recommend cruising locations for taxi drivers under

the constraint of booking information. ACM Transactions on Management Information Systems

(TMIS). 13(3). pp.1-30.

Sodero, A. C. and et.al., 2021. The strategic drivers of drop-shipping and retail store sales for seasonal

products. Journal of Retailing. 97(4). pp.561-581.

Page 11 of 11

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.