Research on the Evolution of Fintech: Tech and Payment Processing

VerifiedAdded on 2023/04/17

|7

|5032

|360

Report

AI Summary

This research paper investigates the evolution of fintech, focusing on its development alongside technological advancements and new payment processes. It reviews literature, discusses the concept of fintech, compares traditional and modern financial services, and explores the relationship between fintech and payment solutions. Using secondary research and MS Excel for data analysis, the study examines the impact of technology on fintech evolution. The findings suggest a positive outcome and highlight opportunities for future research. The paper covers the concept of fintech, differences between traditional and fintech services, current payment procedures, and the global impact of fintech evolution. It includes an introduction, literature review, research methodology, data analysis, findings, and conclusion, adhering to IEEE conference-style formatting.

Evolution of Fintech

Name of the Student

Name of the University

Author Note

ABSTRACT

The research paper intends to make investigation on the evolution of fintech. The

basic purpose is to determine how the fintech is evolving in the financial world along

with the change in the technology and the new payment processes. In order to move

forward in the research paper the background study have been done and thereafter

several literatures are reviewed. There is discussion about the concept of fintech, the

traditional and the modern financial services and the relation of the fintech with the

payment solutions. The research paper minutely studies the details about how

technology is evolving and thereafter a relationship has been built between the

evolution of the fintech and technology as well as the payment systems. Secondary

research has been done and the data is analyzed using MS Excel statistical tools. The

findings have been discussed. The research concludes by stating that there is a

positive outcome of this analysis and there are several scopes to work further on it in

the coming future.

1 INTRODUCTION

There have been many changes in the recent period in

relation to the field of technology. Several new inventions and

innovations have taken place. These inventions and

innovations in the field of technology have helped in the

advancements of various services being provided by the

business organizations. These improvements have changed the

way the people are performing their daily activities related to

the communication, learning and development, travelling,

purchase and sales transactions, socializing and many

more(Linton and Solomon 2017). People are demanding for

quick and prompt services in this competitive and busy

market. Easy one-click solutions from anywhere are available

to the customers (Wall et al. 2016). The usage of the smart

phones, tablets and the laptops have made it easier for the

people around the world to make several transactions at any

time from anywhere. These easy solutions are attracting

consumers and thereafter all the financial institutions are being

motivated to adopt these technology advancements in order to

survive the competition and increase the profitability. The

research deals with one such important case of the impact of

the financial technologies on the payment technology.

1.1 BACKGROUND OF THE STUDY

The term Fintech is a shorter version of the term financial

technology. This is a new technology that competes with the

traditional technology and provides the society with several

advantages. It is the process of automation and innovation of

the financial services and thereafter providing those services

in a technologically efficient manner. Financial technologies

are evolving along with the technological innovations and

improvements. There has been a drastic evolution in the

financial procedures over the last 100 years. There have been

changes in relation to the payments solutions, banking

solutions, data storage, foreign trade transactions, and

investments as well (González-Páramo 2017). The financial

procedures have undergone such changes because of the

necessity to allow the global transactions. Fintech has helped

in the business development. Fintech was previously used in

the back office functions and was used in the leveraging of

personnel bank accounts, database management of the

consumers and execution of transaction (Scott, Van Reenen

and Zachariadis 2017). The current scenario implements

fintech for all financial issues. There has development in the

ATMs, online account checking system, online payment

systems and several investment systems as well. These

evolutions in the fintech sector are gaining customers very

quickly and smoothly.

1.2 RESEARCH AIM

The aim of the research is to understand how the fintech

company has evolved along with the innovation in the

technology and improvement in the payment process.

1.3 RESEARCH OBJECTIVE

The research objectives of the study are stated as below:

1. To understand the idea and concept of Fintech.

2. To critically understand the concept of traditional

financial services and the financial technology

services.

3. To understand and get an idea about the current

payment procedures and how fintech is associated

with the same.

4. To understand how fintech is evolving and how is it

affecting the consumers globally.

1.4 RESEARCH QUESTIONS

The research questions are stated as below:

Name of the Student

Name of the University

Author Note

ABSTRACT

The research paper intends to make investigation on the evolution of fintech. The

basic purpose is to determine how the fintech is evolving in the financial world along

with the change in the technology and the new payment processes. In order to move

forward in the research paper the background study have been done and thereafter

several literatures are reviewed. There is discussion about the concept of fintech, the

traditional and the modern financial services and the relation of the fintech with the

payment solutions. The research paper minutely studies the details about how

technology is evolving and thereafter a relationship has been built between the

evolution of the fintech and technology as well as the payment systems. Secondary

research has been done and the data is analyzed using MS Excel statistical tools. The

findings have been discussed. The research concludes by stating that there is a

positive outcome of this analysis and there are several scopes to work further on it in

the coming future.

1 INTRODUCTION

There have been many changes in the recent period in

relation to the field of technology. Several new inventions and

innovations have taken place. These inventions and

innovations in the field of technology have helped in the

advancements of various services being provided by the

business organizations. These improvements have changed the

way the people are performing their daily activities related to

the communication, learning and development, travelling,

purchase and sales transactions, socializing and many

more(Linton and Solomon 2017). People are demanding for

quick and prompt services in this competitive and busy

market. Easy one-click solutions from anywhere are available

to the customers (Wall et al. 2016). The usage of the smart

phones, tablets and the laptops have made it easier for the

people around the world to make several transactions at any

time from anywhere. These easy solutions are attracting

consumers and thereafter all the financial institutions are being

motivated to adopt these technology advancements in order to

survive the competition and increase the profitability. The

research deals with one such important case of the impact of

the financial technologies on the payment technology.

1.1 BACKGROUND OF THE STUDY

The term Fintech is a shorter version of the term financial

technology. This is a new technology that competes with the

traditional technology and provides the society with several

advantages. It is the process of automation and innovation of

the financial services and thereafter providing those services

in a technologically efficient manner. Financial technologies

are evolving along with the technological innovations and

improvements. There has been a drastic evolution in the

financial procedures over the last 100 years. There have been

changes in relation to the payments solutions, banking

solutions, data storage, foreign trade transactions, and

investments as well (González-Páramo 2017). The financial

procedures have undergone such changes because of the

necessity to allow the global transactions. Fintech has helped

in the business development. Fintech was previously used in

the back office functions and was used in the leveraging of

personnel bank accounts, database management of the

consumers and execution of transaction (Scott, Van Reenen

and Zachariadis 2017). The current scenario implements

fintech for all financial issues. There has development in the

ATMs, online account checking system, online payment

systems and several investment systems as well. These

evolutions in the fintech sector are gaining customers very

quickly and smoothly.

1.2 RESEARCH AIM

The aim of the research is to understand how the fintech

company has evolved along with the innovation in the

technology and improvement in the payment process.

1.3 RESEARCH OBJECTIVE

The research objectives of the study are stated as below:

1. To understand the idea and concept of Fintech.

2. To critically understand the concept of traditional

financial services and the financial technology

services.

3. To understand and get an idea about the current

payment procedures and how fintech is associated

with the same.

4. To understand how fintech is evolving and how is it

affecting the consumers globally.

1.4 RESEARCH QUESTIONS

The research questions are stated as below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. What is the concept of fintech in the current market

scenario?

2. What are the differences between the traditional

financial management and the current financial

services being provided?

3. What is the current improvement in the payment

system? How is fintech associated with such

improvements?

4. How is fintech evolving along with technology and

what are the impacts on the consumers globally?

1.5 STRUCTURE OF THE STUDY

The research paper consists of six chapters and they are as

follows:

1. Introduction– This chapter gives a brief overview of

the technological improvements that are leading to

adopting of several financial technologies by the

financial institutions. The chapter also discusses

about the research background, aims and objectives

and the research questions.

2. Literature Review–This chapter consists of the

analysis of several concepts of the financial

technologies and analyses several scientific

literatures.

3. Research Methodology – In this chapter, the

researcher has done a descriptive research work in

order to assess how the fintech company has evolved

along with the evolution of technology and the

payment process.

4. Research Data – the primary data has been analyzed

in this section, the responses are recorded in MS

Excel, and the quantitative analysis has been done

thereafter.

5. Findings–The results of the analysis are explained in

the findings based on which recommendations are

provided.

6. Conclusion–The overall analysis is stated in brief

and the recommendations are given in this chapter.

2 LITERATURE REVIEW

2.1 CONCEPT OF FINTECH

The term “Fintech” has gained a huge importance in the

recent market because of the cheaper, faster and the user-

friendly services that is provided by it. The term has become a

hot topic for several financial institutions and private

companies. There has been more than 50 billion dollars of

investment made in this sector between the period of 2010 and

2015 by the private and the institutional investors (Scott, Van

Reenen and Zachariadis 2017). Fintech is an improvised

service that is actually a mixture of the financial solutions

along with technology. The sector of fintech is evolving

rapidly and there is a variety of definitions of this concept.

The general concept of the term is that fintech are those

companies that develop and thereafter provide financial

products and services by making use of information

technology. It increases the efficiency of the service sector by

using mobile centric IT technologies, software and other

modern technologies (Oshodin et al. 2017). The fintech

companies have responded very promptly to the changing

needs and preferences of the consumers. The fintech

companies are now involved in providing banking solutions,

investment solutions, payment solutions as well as trading

solutions. People consider a huge growth prospective of this

company in the upcoming future. The Global Financial Survey

conducted by PwC in the year 2017 shows that there has been

an increase in the percentage of the people believing in the

growth and evolution of the fintech companies in the coming

future (Demirguc-Kunt et al. 2018).

2.2 TRADITIONAL FINANCIAL MANAGEMENT VS.

FINTECH SERVICES

There has been a lot of changes in the financial

management procedures in today’s market because of the

innovation and evolution of the technology. The technological

advancement has changed how all the business organizations

perceives their risk and performs their tasks and how the

consumers are responding to such changes.

The traditional financial services involve a lot of

documentation process, lot of pen and paper work and a lot of

mental efforts to be provided (Coleman 2016). There is a

necessity to fill forms and other slips and then waiting in the

queue of the bank for depositing and withdrawing money from

the bank under the traditional financial system. The traditional

banks do not have enough digital footprints and hence the

services offered by the traditional banking sectors are very

slow and time consuming. Even the transfer under the

traditional system takes a lot of time as it uses the concept of

cheques, manager’s cheque, demand draft, money order agent

and money transfer agents. In order to transfer money in the

traditional system, all the necessary details of the account

holders as well as the beneficiary are to be recorded and

thereafter verifications of both the parties will be done. The

money is transferred only when the verification is done. The

task of the transfer of money thus takes a huge amount of time

and is very cumbersome in nature (Su 2016). In order to do

trade the merchants and the consumers requires being

physically present. The traditional process of financial

services involves a huge amount of cost as one single

operation involves a lot of people and hence the cost increases.

The traditional financial services are not available throughout

the day.

The fintech services are much advanced and offer a range of

advantages to the consumers. These services are available

throughout the day. The fintech services reduce the

operational cost of any business organization as it removes the

unnecessary intermediaries (Ng and Kwok 2017). It does not

require maintaining huge number of data in pen and paper

formats the fintech company uses the cloud services that help

the organizations using these services to store a large number

of data. The data can be accessed at any time form any place

and there is the least risk of the loss of the data under this

system. The fintech services have offered easy banking

solutions that allow the consumers to access their accounts

form any place and check their balances as well as make

scenario?

2. What are the differences between the traditional

financial management and the current financial

services being provided?

3. What is the current improvement in the payment

system? How is fintech associated with such

improvements?

4. How is fintech evolving along with technology and

what are the impacts on the consumers globally?

1.5 STRUCTURE OF THE STUDY

The research paper consists of six chapters and they are as

follows:

1. Introduction– This chapter gives a brief overview of

the technological improvements that are leading to

adopting of several financial technologies by the

financial institutions. The chapter also discusses

about the research background, aims and objectives

and the research questions.

2. Literature Review–This chapter consists of the

analysis of several concepts of the financial

technologies and analyses several scientific

literatures.

3. Research Methodology – In this chapter, the

researcher has done a descriptive research work in

order to assess how the fintech company has evolved

along with the evolution of technology and the

payment process.

4. Research Data – the primary data has been analyzed

in this section, the responses are recorded in MS

Excel, and the quantitative analysis has been done

thereafter.

5. Findings–The results of the analysis are explained in

the findings based on which recommendations are

provided.

6. Conclusion–The overall analysis is stated in brief

and the recommendations are given in this chapter.

2 LITERATURE REVIEW

2.1 CONCEPT OF FINTECH

The term “Fintech” has gained a huge importance in the

recent market because of the cheaper, faster and the user-

friendly services that is provided by it. The term has become a

hot topic for several financial institutions and private

companies. There has been more than 50 billion dollars of

investment made in this sector between the period of 2010 and

2015 by the private and the institutional investors (Scott, Van

Reenen and Zachariadis 2017). Fintech is an improvised

service that is actually a mixture of the financial solutions

along with technology. The sector of fintech is evolving

rapidly and there is a variety of definitions of this concept.

The general concept of the term is that fintech are those

companies that develop and thereafter provide financial

products and services by making use of information

technology. It increases the efficiency of the service sector by

using mobile centric IT technologies, software and other

modern technologies (Oshodin et al. 2017). The fintech

companies have responded very promptly to the changing

needs and preferences of the consumers. The fintech

companies are now involved in providing banking solutions,

investment solutions, payment solutions as well as trading

solutions. People consider a huge growth prospective of this

company in the upcoming future. The Global Financial Survey

conducted by PwC in the year 2017 shows that there has been

an increase in the percentage of the people believing in the

growth and evolution of the fintech companies in the coming

future (Demirguc-Kunt et al. 2018).

2.2 TRADITIONAL FINANCIAL MANAGEMENT VS.

FINTECH SERVICES

There has been a lot of changes in the financial

management procedures in today’s market because of the

innovation and evolution of the technology. The technological

advancement has changed how all the business organizations

perceives their risk and performs their tasks and how the

consumers are responding to such changes.

The traditional financial services involve a lot of

documentation process, lot of pen and paper work and a lot of

mental efforts to be provided (Coleman 2016). There is a

necessity to fill forms and other slips and then waiting in the

queue of the bank for depositing and withdrawing money from

the bank under the traditional financial system. The traditional

banks do not have enough digital footprints and hence the

services offered by the traditional banking sectors are very

slow and time consuming. Even the transfer under the

traditional system takes a lot of time as it uses the concept of

cheques, manager’s cheque, demand draft, money order agent

and money transfer agents. In order to transfer money in the

traditional system, all the necessary details of the account

holders as well as the beneficiary are to be recorded and

thereafter verifications of both the parties will be done. The

money is transferred only when the verification is done. The

task of the transfer of money thus takes a huge amount of time

and is very cumbersome in nature (Su 2016). In order to do

trade the merchants and the consumers requires being

physically present. The traditional process of financial

services involves a huge amount of cost as one single

operation involves a lot of people and hence the cost increases.

The traditional financial services are not available throughout

the day.

The fintech services are much advanced and offer a range of

advantages to the consumers. These services are available

throughout the day. The fintech services reduce the

operational cost of any business organization as it removes the

unnecessary intermediaries (Ng and Kwok 2017). It does not

require maintaining huge number of data in pen and paper

formats the fintech company uses the cloud services that help

the organizations using these services to store a large number

of data. The data can be accessed at any time form any place

and there is the least risk of the loss of the data under this

system. The fintech services have offered easy banking

solutions that allow the consumers to access their accounts

form any place and check their balances as well as make

transactions just by a click. The online payment system that

has been introduced helps in the transfer of the money from

one account to the other account on a real time basis and the

receiver does not need to wait for a long period of time in

order to receive the money. The transaction histories are

updated through SMS and emails and the consumers need not

go to the banks and the other financial institutions in order to

check the account balance all the time (Navaretti et al. 2018).

2.3 FINTECH AND PAYMENT SERVICES

Payment services usually involve transfer of funds, inward

and outward remittances, financial payments and payments for

online retail trading as well as investment trading. The

traditional payment services involved the visiting of the

financial institutions and filling up of several details and

thereafter making the payments (Ogbanufe and Kim 2018).

The transfer of the money then takes a lot of time to get

transferred to the beneficiary. The traditional process is also

very cumbersome and in certain cases, transparency is also

very low which creates a chance of credit default. The

companies have to incur huge amount of costs in order to

maintain the complicated processes as well as to maintain and

protect a large number of data. The companies therefore

always strive for a cost efficient process. Similarly, the

consumers also want smooth and flexible services at the least

time possible. The evolution of the technology therefore

attracted both the consumers and the financial institutions to

combine the financial services with the technological

innovations (Wang, Hahn and Sutrave 2016). The fact is that

the industries do not need mere production of new products

and services rather there is a requirement of new paradigm.

The combination of the technology with the finance has led

to the creation of the online payment system or the block chain

based payment system (Lai 2018). The new fintech start-ups

are providing with secured mobile wallets and payment

systems by developing secured software, which is the mixture

of integration, availability, confidentiality and authorization.

The unbanked people can also store a large amount of money

hassle free because of the availability of the smart phones and

high-speed internet. Many mobile applications are there that

does not require having a bank account as well. The fintech

company implements the concept of crypto currency and

block chain payment processor to improve the transactions in

the industry. People can now lend, borrow, pay and spend

money as per their wish without even contacting the bank.

Applications like Venmo and Apple provides with secured

payment methods. Several lending apps are also there for

example Chill Money, Dubco, Prosper and Lending Club that

provides credit facilities to the consumers at a minimum rate.

The online remittance system has also gained a huge

popularity because of the timeliness, safety, efficiency,

transparency and reliability. The online remittance

applications offer attractive exchange rates and interest rates

than the traditional remittance institutions. The money is

transferred to the abroad countries in a much faster way than

that of the traditional process. Regular updates of the

transactions are provided to the parties involved in the

transaction through mails messages. The transfer charges are

also minimal or zero. Although there has been several benefits

provided by the fintech services yet there be certain risk

factors related to safety and security of the transactions that

are questionable in nature (de Kerviler, Demoulin and Zidda

2017).

2.4 LITERATURE GAP

The literature review states that the innovation in the

technological field and the evolution of the fintech company

has diverted the minds of the consumers from using the

traditional financial services and hence they prefer the fintech

services. The changes in the tastes and preferences of the

consumers have led to the downfall of the traditional financial

industries and the modern financial technology services are

evolving. The payment services have also been developed

with the advent of the fintech companies. The literature gap in

this scenario is how fintech in the financial world is actually

evolving with the new payment and technology processes? Is

the evolution having a positive impact in the minds of the

consumers?

3 RESEARCH AND METHODOLOGY

3.1 RESEARCH METHOD OUTLINE

The outline is the framework of the research processes and

the steps that will be helpful in arriving at the required

outcome. The objectivity of the methodology is discussed in

this section. The processes and the techniques that will be used

in order to interpret the required calculation have been

mentioned in this section. The researcher has chosen the

positivism philosophy. A deductive approach has been

selected for conducting the research. The research follows a

descriptive research design. The research outline also provides

details about the data collection procedure and the sample

sizes based on which the conclusion is achieved.

3.2 RESEARCH ONION

The research onion helps in the understanding of the

research methodology as well as the research framework

(Saunders et al. 2015). The research work is done on the basis

of the research onion. The outcome of the research can be

obtained by the help of this and it also helps the researcher in

making the proper use of the research philosophy and the

limited time period.

3.3 RESEARCH PHILOSOPHY

The research philosophy helps the researcher in the

recognition of the research objective by efficiently using the

paradigm. There are four types of research philosophies and

they are Pragmatism, Realism, Interpretivism and Positivism.

The researcher in this case tries to find out the evolution of the

fintech with respect to the payment process and technological

innovations and hence the research philosophy followed in

this research work is the philosophy of positivism. The reason

behind choosing this philosophy is that the data collected and

reviewed are scientific in nature and are proven (Ray 2017).

The data cannot be altered while its collection because the

data are not dependent on the research subject. The researcher

has put emphasis on the factors that leads to the evolution of

has been introduced helps in the transfer of the money from

one account to the other account on a real time basis and the

receiver does not need to wait for a long period of time in

order to receive the money. The transaction histories are

updated through SMS and emails and the consumers need not

go to the banks and the other financial institutions in order to

check the account balance all the time (Navaretti et al. 2018).

2.3 FINTECH AND PAYMENT SERVICES

Payment services usually involve transfer of funds, inward

and outward remittances, financial payments and payments for

online retail trading as well as investment trading. The

traditional payment services involved the visiting of the

financial institutions and filling up of several details and

thereafter making the payments (Ogbanufe and Kim 2018).

The transfer of the money then takes a lot of time to get

transferred to the beneficiary. The traditional process is also

very cumbersome and in certain cases, transparency is also

very low which creates a chance of credit default. The

companies have to incur huge amount of costs in order to

maintain the complicated processes as well as to maintain and

protect a large number of data. The companies therefore

always strive for a cost efficient process. Similarly, the

consumers also want smooth and flexible services at the least

time possible. The evolution of the technology therefore

attracted both the consumers and the financial institutions to

combine the financial services with the technological

innovations (Wang, Hahn and Sutrave 2016). The fact is that

the industries do not need mere production of new products

and services rather there is a requirement of new paradigm.

The combination of the technology with the finance has led

to the creation of the online payment system or the block chain

based payment system (Lai 2018). The new fintech start-ups

are providing with secured mobile wallets and payment

systems by developing secured software, which is the mixture

of integration, availability, confidentiality and authorization.

The unbanked people can also store a large amount of money

hassle free because of the availability of the smart phones and

high-speed internet. Many mobile applications are there that

does not require having a bank account as well. The fintech

company implements the concept of crypto currency and

block chain payment processor to improve the transactions in

the industry. People can now lend, borrow, pay and spend

money as per their wish without even contacting the bank.

Applications like Venmo and Apple provides with secured

payment methods. Several lending apps are also there for

example Chill Money, Dubco, Prosper and Lending Club that

provides credit facilities to the consumers at a minimum rate.

The online remittance system has also gained a huge

popularity because of the timeliness, safety, efficiency,

transparency and reliability. The online remittance

applications offer attractive exchange rates and interest rates

than the traditional remittance institutions. The money is

transferred to the abroad countries in a much faster way than

that of the traditional process. Regular updates of the

transactions are provided to the parties involved in the

transaction through mails messages. The transfer charges are

also minimal or zero. Although there has been several benefits

provided by the fintech services yet there be certain risk

factors related to safety and security of the transactions that

are questionable in nature (de Kerviler, Demoulin and Zidda

2017).

2.4 LITERATURE GAP

The literature review states that the innovation in the

technological field and the evolution of the fintech company

has diverted the minds of the consumers from using the

traditional financial services and hence they prefer the fintech

services. The changes in the tastes and preferences of the

consumers have led to the downfall of the traditional financial

industries and the modern financial technology services are

evolving. The payment services have also been developed

with the advent of the fintech companies. The literature gap in

this scenario is how fintech in the financial world is actually

evolving with the new payment and technology processes? Is

the evolution having a positive impact in the minds of the

consumers?

3 RESEARCH AND METHODOLOGY

3.1 RESEARCH METHOD OUTLINE

The outline is the framework of the research processes and

the steps that will be helpful in arriving at the required

outcome. The objectivity of the methodology is discussed in

this section. The processes and the techniques that will be used

in order to interpret the required calculation have been

mentioned in this section. The researcher has chosen the

positivism philosophy. A deductive approach has been

selected for conducting the research. The research follows a

descriptive research design. The research outline also provides

details about the data collection procedure and the sample

sizes based on which the conclusion is achieved.

3.2 RESEARCH ONION

The research onion helps in the understanding of the

research methodology as well as the research framework

(Saunders et al. 2015). The research work is done on the basis

of the research onion. The outcome of the research can be

obtained by the help of this and it also helps the researcher in

making the proper use of the research philosophy and the

limited time period.

3.3 RESEARCH PHILOSOPHY

The research philosophy helps the researcher in the

recognition of the research objective by efficiently using the

paradigm. There are four types of research philosophies and

they are Pragmatism, Realism, Interpretivism and Positivism.

The researcher in this case tries to find out the evolution of the

fintech with respect to the payment process and technological

innovations and hence the research philosophy followed in

this research work is the philosophy of positivism. The reason

behind choosing this philosophy is that the data collected and

reviewed are scientific in nature and are proven (Ray 2017).

The data cannot be altered while its collection because the

data are not dependent on the research subject. The researcher

has put emphasis on the factors that leads to the evolution of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the fintech services. The responses of the respondents are also

separated with the help of scientific tools.

3.4 RESEARCH APPROACH

The research approach plays a fundamental role in helping

the researchers to determine the detailed steps for undertaking

the activities that are expected to be a part of the research.

There are usually two kinds of research approaches and they

are inductive approach and deductive approach (Singh 2015).

The deductive approach has been selected in the research

work. The responses of several financial users will be taken

and their responses will be taken under consideration for

reaching the desired outcome. The paper therefore considers

certain literature and research that has been done previously in

order to get the best result. The deductive approach is used

because certain research questions are considered for

achieving the desired results. The inductive approach is not

used as it involves the application of unique and new models,

development of new theories by the researcher and this paper

does not involve any such applications.

3.5 DATA COLLECTION PROCESS

The data collection process helps in getting a fair view of

the types of the data that has been selected in the research

work. There are two types of data namely the primary data and

the secondary data. The primary data deals with the direct

collection of information from live respondents whereas

secondary data relates to taking information from the journals,

magazines and articles (Johnston 2017). The research paper

makes use of the secondary data. The secondary data is taken

in order to understand the various concepts, review the

literature and find out the gaps as well as financial data related

to payment and remittance have been taken from the online

sources.

3.6 SAMPLING AND SAMPLE SIZE

Sampling refers to the choosing of a particular group from

the total population that has been considered for the research

work (Pitard 2019). The process of sampling helps in the

reduction of the survey size and it also helps in getting the

precise information that is required by mixing all the relevant

information that is required. Simple random sampling is done

in the research work where the respondents are selected at

random from the entire population of Ireland.

3.7 DATA ANALYSIS PLAN

The collection of data is done with the help of the financial

data taken from Statista.com. The data is consolidated in the

MS Excel and thereafter the required calculation is being done

in order to analyze the data and interpret the data.

3.8 ETHICAL CONSIDERATION

The secondary data used are viable in nature. No improper

information is provided in the information. This research

paper is not used for any commercial purposes. The data used

in the analysis has been obtained from authentic sources.

4 RESEARCH DATA ANALYSIS

4.1 INVESTMENT OF FINTECH

Here the investment of Fintech is analyzed based on the

secondary data, which contains the value of worldwide

investment and the number of consumers of Fintech from the

year 2011 to 2016. Now, the data indicates the rise in

investment of Fintech over the year. The below graph presents

the worldwide investment of Fintech through a line.

2011 2012 2013 2014 2015 2016

0

5

10

15

20

25

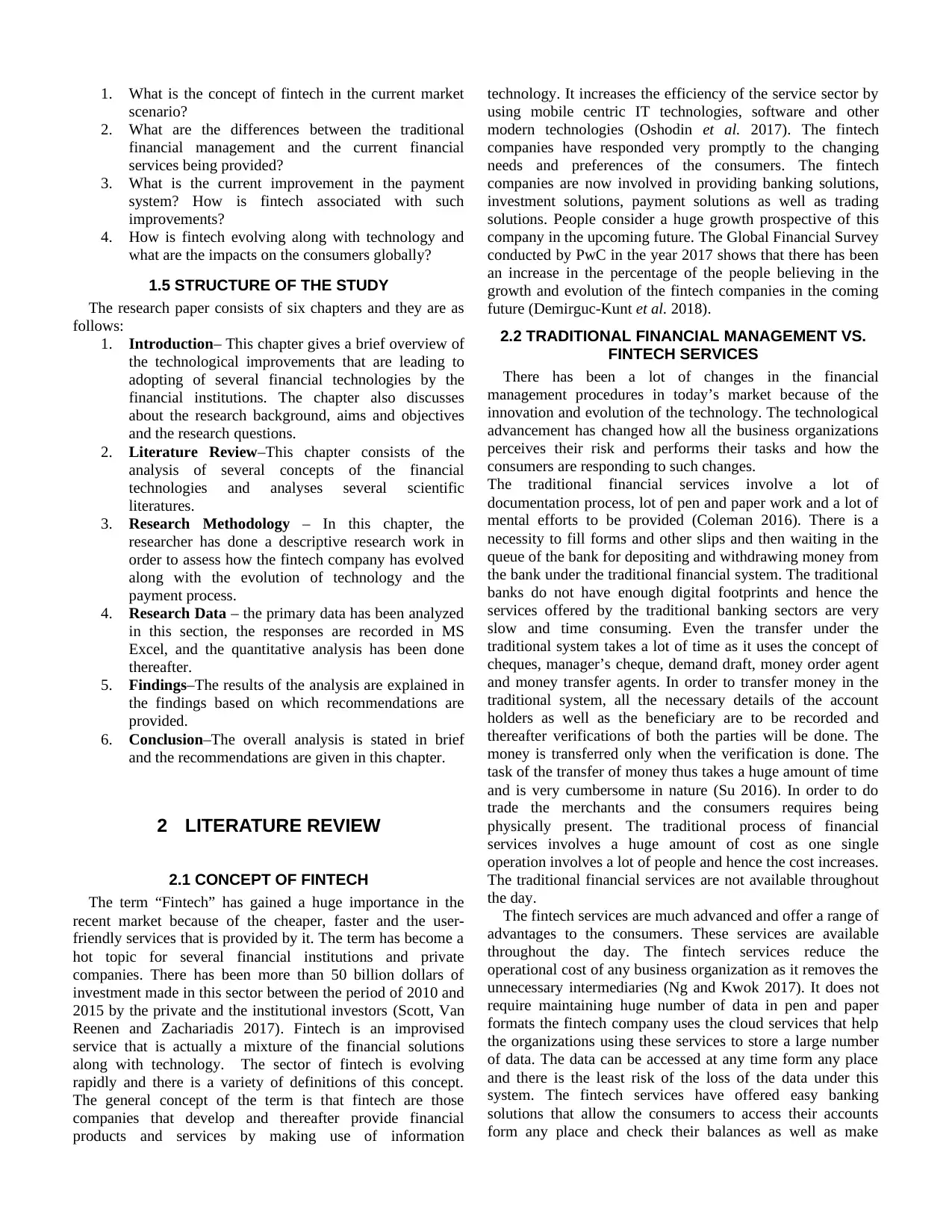

Investment of Fintech from 2011-16

TimeLine

Value (billion dollars)

Figure 1: Worldwide Investment of Fintech

The figure 1 shows the line is upward rising and a change

in slope of the line is there. This means the investment is

rising over the year and the change in slope indicates that the

growth in investment is uneven. Statistics of investment can

express overall change in investment during these years.

Table 1: Mean and standard Deviation of Investment

The above table presents that the mean value of investment

is 10.18 and the standard deviation is 8.21. This means the

fluctuation in investment is precisely high. Which supports the

figure 1. By running a regression, the relation of rise in

investment with the year can be stated evidently.

H0: The coefficient of investment is equal to zero.

HA: The coefficient of investment is not equal to zero.

Table 2: Regression Statistics

Multiple R 0.9348

R Square 0.8738

Adjusted R Square 0.8423

Standard Error 3.2586

Observations 6

Table 2 presents the adjusted R2 =0.8423 that means the

model is 84.23% predictable.

Table 3: Regression Result

Coefficients Standard

Error

t Stat P-value

Intercept -4.1667 3.0336 -1.3735 0.2415

Year 4.1000 0.7789 5.2635 0.0062

Mean 10.18

Standard Deviation 8.21

separated with the help of scientific tools.

3.4 RESEARCH APPROACH

The research approach plays a fundamental role in helping

the researchers to determine the detailed steps for undertaking

the activities that are expected to be a part of the research.

There are usually two kinds of research approaches and they

are inductive approach and deductive approach (Singh 2015).

The deductive approach has been selected in the research

work. The responses of several financial users will be taken

and their responses will be taken under consideration for

reaching the desired outcome. The paper therefore considers

certain literature and research that has been done previously in

order to get the best result. The deductive approach is used

because certain research questions are considered for

achieving the desired results. The inductive approach is not

used as it involves the application of unique and new models,

development of new theories by the researcher and this paper

does not involve any such applications.

3.5 DATA COLLECTION PROCESS

The data collection process helps in getting a fair view of

the types of the data that has been selected in the research

work. There are two types of data namely the primary data and

the secondary data. The primary data deals with the direct

collection of information from live respondents whereas

secondary data relates to taking information from the journals,

magazines and articles (Johnston 2017). The research paper

makes use of the secondary data. The secondary data is taken

in order to understand the various concepts, review the

literature and find out the gaps as well as financial data related

to payment and remittance have been taken from the online

sources.

3.6 SAMPLING AND SAMPLE SIZE

Sampling refers to the choosing of a particular group from

the total population that has been considered for the research

work (Pitard 2019). The process of sampling helps in the

reduction of the survey size and it also helps in getting the

precise information that is required by mixing all the relevant

information that is required. Simple random sampling is done

in the research work where the respondents are selected at

random from the entire population of Ireland.

3.7 DATA ANALYSIS PLAN

The collection of data is done with the help of the financial

data taken from Statista.com. The data is consolidated in the

MS Excel and thereafter the required calculation is being done

in order to analyze the data and interpret the data.

3.8 ETHICAL CONSIDERATION

The secondary data used are viable in nature. No improper

information is provided in the information. This research

paper is not used for any commercial purposes. The data used

in the analysis has been obtained from authentic sources.

4 RESEARCH DATA ANALYSIS

4.1 INVESTMENT OF FINTECH

Here the investment of Fintech is analyzed based on the

secondary data, which contains the value of worldwide

investment and the number of consumers of Fintech from the

year 2011 to 2016. Now, the data indicates the rise in

investment of Fintech over the year. The below graph presents

the worldwide investment of Fintech through a line.

2011 2012 2013 2014 2015 2016

0

5

10

15

20

25

Investment of Fintech from 2011-16

TimeLine

Value (billion dollars)

Figure 1: Worldwide Investment of Fintech

The figure 1 shows the line is upward rising and a change

in slope of the line is there. This means the investment is

rising over the year and the change in slope indicates that the

growth in investment is uneven. Statistics of investment can

express overall change in investment during these years.

Table 1: Mean and standard Deviation of Investment

The above table presents that the mean value of investment

is 10.18 and the standard deviation is 8.21. This means the

fluctuation in investment is precisely high. Which supports the

figure 1. By running a regression, the relation of rise in

investment with the year can be stated evidently.

H0: The coefficient of investment is equal to zero.

HA: The coefficient of investment is not equal to zero.

Table 2: Regression Statistics

Multiple R 0.9348

R Square 0.8738

Adjusted R Square 0.8423

Standard Error 3.2586

Observations 6

Table 2 presents the adjusted R2 =0.8423 that means the

model is 84.23% predictable.

Table 3: Regression Result

Coefficients Standard

Error

t Stat P-value

Intercept -4.1667 3.0336 -1.3735 0.2415

Year 4.1000 0.7789 5.2635 0.0062

Mean 10.18

Standard Deviation 8.21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The regression table presents the p-value of the coefficient

of the year, which indicates that the coefficient is statistically

significant at 5% level. This implies that there is sufficient

evidence to reject the null hypothesis and accept the

alternative hypothesis.

4.2 CONSUMERS OF FINTECH

The consumer of Fintech is analyzed based on the

secondary data. Now, the data indicates the rise in the number

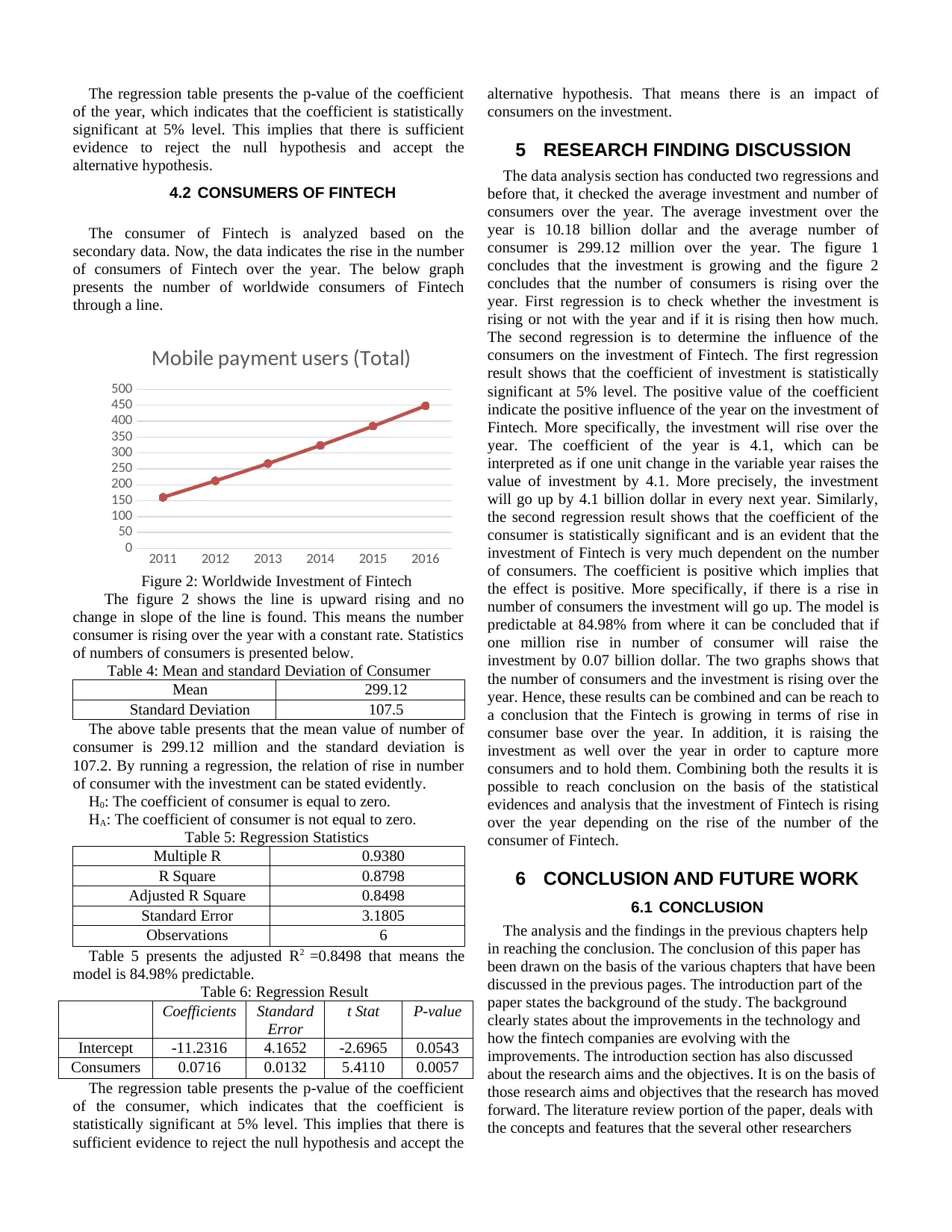

of consumers of Fintech over the year. The below graph

presents the number of worldwide consumers of Fintech

through a line.

2011 2012 2013 2014 2015 2016

0

50

100

150

200

250

300

350

400

450

500

Mobile payment users (Total)

Figure 2: Worldwide Investment of Fintech

The figure 2 shows the line is upward rising and no

change in slope of the line is found. This means the number

consumer is rising over the year with a constant rate. Statistics

of numbers of consumers is presented below.

Table 4: Mean and standard Deviation of Consumer

Mean 299.12

Standard Deviation 107.5

The above table presents that the mean value of number of

consumer is 299.12 million and the standard deviation is

107.2. By running a regression, the relation of rise in number

of consumer with the investment can be stated evidently.

H0: The coefficient of consumer is equal to zero.

HA: The coefficient of consumer is not equal to zero.

Table 5: Regression Statistics

Multiple R 0.9380

R Square 0.8798

Adjusted R Square 0.8498

Standard Error 3.1805

Observations 6

Table 5 presents the adjusted R2 =0.8498 that means the

model is 84.98% predictable.

Table 6: Regression Result

Coefficients Standard

Error

t Stat P-value

Intercept -11.2316 4.1652 -2.6965 0.0543

Consumers 0.0716 0.0132 5.4110 0.0057

The regression table presents the p-value of the coefficient

of the consumer, which indicates that the coefficient is

statistically significant at 5% level. This implies that there is

sufficient evidence to reject the null hypothesis and accept the

alternative hypothesis. That means there is an impact of

consumers on the investment.

5 RESEARCH FINDING DISCUSSION

The data analysis section has conducted two regressions and

before that, it checked the average investment and number of

consumers over the year. The average investment over the

year is 10.18 billion dollar and the average number of

consumer is 299.12 million over the year. The figure 1

concludes that the investment is growing and the figure 2

concludes that the number of consumers is rising over the

year. First regression is to check whether the investment is

rising or not with the year and if it is rising then how much.

The second regression is to determine the influence of the

consumers on the investment of Fintech. The first regression

result shows that the coefficient of investment is statistically

significant at 5% level. The positive value of the coefficient

indicate the positive influence of the year on the investment of

Fintech. More specifically, the investment will rise over the

year. The coefficient of the year is 4.1, which can be

interpreted as if one unit change in the variable year raises the

value of investment by 4.1. More precisely, the investment

will go up by 4.1 billion dollar in every next year. Similarly,

the second regression result shows that the coefficient of the

consumer is statistically significant and is an evident that the

investment of Fintech is very much dependent on the number

of consumers. The coefficient is positive which implies that

the effect is positive. More specifically, if there is a rise in

number of consumers the investment will go up. The model is

predictable at 84.98% from where it can be concluded that if

one million rise in number of consumer will raise the

investment by 0.07 billion dollar. The two graphs shows that

the number of consumers and the investment is rising over the

year. Hence, these results can be combined and can be reach to

a conclusion that the Fintech is growing in terms of rise in

consumer base over the year. In addition, it is raising the

investment as well over the year in order to capture more

consumers and to hold them. Combining both the results it is

possible to reach conclusion on the basis of the statistical

evidences and analysis that the investment of Fintech is rising

over the year depending on the rise of the number of the

consumer of Fintech.

6 CONCLUSION AND FUTURE WORK

6.1 CONCLUSION

The analysis and the findings in the previous chapters help

in reaching the conclusion. The conclusion of this paper has

been drawn on the basis of the various chapters that have been

discussed in the previous pages. The introduction part of the

paper states the background of the study. The background

clearly states about the improvements in the technology and

how the fintech companies are evolving with the

improvements. The introduction section has also discussed

about the research aims and the objectives. It is on the basis of

those research aims and objectives that the research has moved

forward. The literature review portion of the paper, deals with

the concepts and features that the several other researchers

of the year, which indicates that the coefficient is statistically

significant at 5% level. This implies that there is sufficient

evidence to reject the null hypothesis and accept the

alternative hypothesis.

4.2 CONSUMERS OF FINTECH

The consumer of Fintech is analyzed based on the

secondary data. Now, the data indicates the rise in the number

of consumers of Fintech over the year. The below graph

presents the number of worldwide consumers of Fintech

through a line.

2011 2012 2013 2014 2015 2016

0

50

100

150

200

250

300

350

400

450

500

Mobile payment users (Total)

Figure 2: Worldwide Investment of Fintech

The figure 2 shows the line is upward rising and no

change in slope of the line is found. This means the number

consumer is rising over the year with a constant rate. Statistics

of numbers of consumers is presented below.

Table 4: Mean and standard Deviation of Consumer

Mean 299.12

Standard Deviation 107.5

The above table presents that the mean value of number of

consumer is 299.12 million and the standard deviation is

107.2. By running a regression, the relation of rise in number

of consumer with the investment can be stated evidently.

H0: The coefficient of consumer is equal to zero.

HA: The coefficient of consumer is not equal to zero.

Table 5: Regression Statistics

Multiple R 0.9380

R Square 0.8798

Adjusted R Square 0.8498

Standard Error 3.1805

Observations 6

Table 5 presents the adjusted R2 =0.8498 that means the

model is 84.98% predictable.

Table 6: Regression Result

Coefficients Standard

Error

t Stat P-value

Intercept -11.2316 4.1652 -2.6965 0.0543

Consumers 0.0716 0.0132 5.4110 0.0057

The regression table presents the p-value of the coefficient

of the consumer, which indicates that the coefficient is

statistically significant at 5% level. This implies that there is

sufficient evidence to reject the null hypothesis and accept the

alternative hypothesis. That means there is an impact of

consumers on the investment.

5 RESEARCH FINDING DISCUSSION

The data analysis section has conducted two regressions and

before that, it checked the average investment and number of

consumers over the year. The average investment over the

year is 10.18 billion dollar and the average number of

consumer is 299.12 million over the year. The figure 1

concludes that the investment is growing and the figure 2

concludes that the number of consumers is rising over the

year. First regression is to check whether the investment is

rising or not with the year and if it is rising then how much.

The second regression is to determine the influence of the

consumers on the investment of Fintech. The first regression

result shows that the coefficient of investment is statistically

significant at 5% level. The positive value of the coefficient

indicate the positive influence of the year on the investment of

Fintech. More specifically, the investment will rise over the

year. The coefficient of the year is 4.1, which can be

interpreted as if one unit change in the variable year raises the

value of investment by 4.1. More precisely, the investment

will go up by 4.1 billion dollar in every next year. Similarly,

the second regression result shows that the coefficient of the

consumer is statistically significant and is an evident that the

investment of Fintech is very much dependent on the number

of consumers. The coefficient is positive which implies that

the effect is positive. More specifically, if there is a rise in

number of consumers the investment will go up. The model is

predictable at 84.98% from where it can be concluded that if

one million rise in number of consumer will raise the

investment by 0.07 billion dollar. The two graphs shows that

the number of consumers and the investment is rising over the

year. Hence, these results can be combined and can be reach to

a conclusion that the Fintech is growing in terms of rise in

consumer base over the year. In addition, it is raising the

investment as well over the year in order to capture more

consumers and to hold them. Combining both the results it is

possible to reach conclusion on the basis of the statistical

evidences and analysis that the investment of Fintech is rising

over the year depending on the rise of the number of the

consumer of Fintech.

6 CONCLUSION AND FUTURE WORK

6.1 CONCLUSION

The analysis and the findings in the previous chapters help

in reaching the conclusion. The conclusion of this paper has

been drawn on the basis of the various chapters that have been

discussed in the previous pages. The introduction part of the

paper states the background of the study. The background

clearly states about the improvements in the technology and

how the fintech companies are evolving with the

improvements. The introduction section has also discussed

about the research aims and the objectives. It is on the basis of

those research aims and objectives that the research has moved

forward. The literature review portion of the paper, deals with

the concepts and features that the several other researchers

have addressed in similar such papers. With respect to that, the

gap is identified and the methodology is prepared to answer

the gap and come to the solution of the questions that have

accomplished the aims and objective of the research paper.

The various concepts of fintech, traditional and modern

financial services, and the relationship of the fintech with

payment services have been discussed. The secondary

research is done, the data are analyzed, and it has been seen

that there has been a growth in the financial technologies

along with the growth of the technology and the payment

service system has evolved because of the same. A positive

relationship has been found between the research question and

the outcomes. It has been seen that there has been growth in

the technology field and there has been proportional growth in

the fintech as well. The growth in the payment system has also

been improving since the inception of the fintech. The

technological aspects have actually shifted the demands of the

consumer needs and preferences and fintech is evolving

rapidly in the current situation.

6.2 FUTURE WORKS

There is further scope of research in the future period with

respect to this topic as fintech is a budding concept that will

keep on evolving in the upcoming future. Technology is ever

changing as there are no limits to innovation and hence the

fintech concept will keep on changing. The future research on

this particular topic will help in the understanding about the

further exchanges that will take place and a different and new

result can be obtained.

7 REFERENCES AND BIBLIOGRAPHY

Arner, D.W., Barberis, J. and Buckley, R.P., 2015. The evolution of Fintech:

A new post-crisis paradigm. Geo. J. Int'l L., 47, p.1271.

Baker, T. and Dellaert, B., 2017. Regulating robo advice across the financial

services industry. Iowa L. Rev., 103, p.713.

Coleman, W.D., 2016. Financial services, globalization and domestic policy

change. Springer.

Dapp, T., Slomka, L., AG, D.B. and Hoffmann, R., 2015. Fintech reloaded–

Traditional banks as digital ecosystems. Publication of the German original,

pp.261-274.

de Kerviler, G., Demoulin, N.T. and Zidda, P., 2017. Adoption of proximity

m-payment services: Perceived value and experience effect (An Abstract). In

Marketing at the Confluence between Entertainment and Analytics (pp. 275-

276). Springer, Cham.

Demirbas, U., Gewald, H. and Moos, B., 2018. The Impact of Digital

Transformation on Sourcing Strategies in the Financial Services Sector:

Evolution or Revolution?.

Demirguc-Kunt, A., Klapper, L., Singer, D., Ansar, S. and Hess, J., 2018. The

Global Findex Database 2017: Measuring financial inclusion and the fintech

revolution. The World Bank.

González-Páramo, J.M., 2017. Financial innovation in the digital age:

Challenges for regulation and supervision. Revista de estabilidad financiera,

32(9), p.37.

Johnston, M.P., 2017. Secondary data analysis: A method of which the time

has come. Qualitative and quantitative methods in libraries, 3(3), pp.619-626.

Kang, J., 2018. Mobile payment in Fintech environment: trends, security

challenges, and services. Human-centric Computing and Information

Sciences, 8(1), p.32.

Lai, R., 2018. Understanding Interbank Real-Time Retail Payment Systems.

In Handbook of Blockchain, Digital Finance, and Inclusion, Volume 1 (pp.

283-310). Academic Press.

Linton, J.D. and Solomon, G.T., 2017. Technology, Innovation,

Entrepreneurship and The Small Business—Technology and Innovation in

Small Business. Journal of Small Business Management, 55(2), pp.196-199.

Merton, R.C. and Thakor, R.T., 2018. Customers and investors: a framework

for understanding the evolution of financial institutions. Journal of Financial

Intermediation.

Navaretti, G.B., Calzolari, G., Mansilla-Fernandez, J.M. and Pozzolo, A.F.,

2018. Fintech and Banking. Friends or Foes?. Friends or Foes.

Ng, A.W. and Kwok, B.K., 2017. Emergence of Fintech and cybersecurity in

a global financial centre: Strategic approach by a regulator. Journal of

Financial Regulation and Compliance, 25(4), pp.422-434.

Ogbanufe, O. and Kim, D.J., 2018. Comparing fingerprint-based biometrics

authentication versus traditional authentication methods for e-payment.

Decision Support Systems, 106, pp.1-14.

Oshodin, O., Molla, A., Karanasios, S. and Ong, C.E., 2017. Is FinTech a

disruption or a new eco-system? An exploratory investigation of Banksr

response to FinTech in Australia. In Proceeding of Australasian Conference

on Information Systems (pp. 1-11).

Pitard, F.F., 2019. Theory of Sampling and Sampling Practice. Chapman and

Hall/CRC.

Prabhu, R., Sinha, A. and Hayes, J.D., Mastercard Asia/Pacific Pte Ltd, 2016.

Methods and systems for secure online payment. U.S. Patent Application

14/878,167.

Ray, C., 2017. Logical positivism. A companion to the philosophy of science,

pp.243-251.

References

Saunders, M.N., Lewis, P., Thornhill, A. and Bristow, A., 2015.

Understanding research philosophy and approaches to theory development.

Scott, S.V., Van Reenen, J. and Zachariadis, M., 2017. The long-term effect of

digital innovation on bank performance: An empirical study of SWIFT

adoption in financial services. Research Policy, 46(5), pp.984-1004.

Singh, K.D., 2015. Creating your own qualitative research approach:

Selecting, integrating and operationalizing philosophy, methodology and

methods. Vision, 19(2), pp.132-146.

Su, W., 2016, May. Research on the Development of Online Financing and

the Influences on Traditional Financial and Insurance Industry. In 2016

International Conference on Economy, Management and Education

Technology. Atlantis Press.

Wall, J., Von Behren, R. and COLLINE, I.R.E., Google LLC, 2016. One-click

offline buying. U.S. Patent 9,390,414.

Wang, Y., Hahn, C. and Sutrave, K., 2016, February. Mobile payment

security, threats, and challenges. In 2016 second international conference on

mobile and secure services (MobiSecServ) (pp. 1-5). IEEE.

gap is identified and the methodology is prepared to answer

the gap and come to the solution of the questions that have

accomplished the aims and objective of the research paper.

The various concepts of fintech, traditional and modern

financial services, and the relationship of the fintech with

payment services have been discussed. The secondary

research is done, the data are analyzed, and it has been seen

that there has been a growth in the financial technologies

along with the growth of the technology and the payment

service system has evolved because of the same. A positive

relationship has been found between the research question and

the outcomes. It has been seen that there has been growth in

the technology field and there has been proportional growth in

the fintech as well. The growth in the payment system has also

been improving since the inception of the fintech. The

technological aspects have actually shifted the demands of the

consumer needs and preferences and fintech is evolving

rapidly in the current situation.

6.2 FUTURE WORKS

There is further scope of research in the future period with

respect to this topic as fintech is a budding concept that will

keep on evolving in the upcoming future. Technology is ever

changing as there are no limits to innovation and hence the

fintech concept will keep on changing. The future research on

this particular topic will help in the understanding about the

further exchanges that will take place and a different and new

result can be obtained.

7 REFERENCES AND BIBLIOGRAPHY

Arner, D.W., Barberis, J. and Buckley, R.P., 2015. The evolution of Fintech:

A new post-crisis paradigm. Geo. J. Int'l L., 47, p.1271.

Baker, T. and Dellaert, B., 2017. Regulating robo advice across the financial

services industry. Iowa L. Rev., 103, p.713.

Coleman, W.D., 2016. Financial services, globalization and domestic policy

change. Springer.

Dapp, T., Slomka, L., AG, D.B. and Hoffmann, R., 2015. Fintech reloaded–

Traditional banks as digital ecosystems. Publication of the German original,

pp.261-274.

de Kerviler, G., Demoulin, N.T. and Zidda, P., 2017. Adoption of proximity

m-payment services: Perceived value and experience effect (An Abstract). In

Marketing at the Confluence between Entertainment and Analytics (pp. 275-

276). Springer, Cham.

Demirbas, U., Gewald, H. and Moos, B., 2018. The Impact of Digital

Transformation on Sourcing Strategies in the Financial Services Sector:

Evolution or Revolution?.

Demirguc-Kunt, A., Klapper, L., Singer, D., Ansar, S. and Hess, J., 2018. The

Global Findex Database 2017: Measuring financial inclusion and the fintech

revolution. The World Bank.

González-Páramo, J.M., 2017. Financial innovation in the digital age:

Challenges for regulation and supervision. Revista de estabilidad financiera,

32(9), p.37.

Johnston, M.P., 2017. Secondary data analysis: A method of which the time

has come. Qualitative and quantitative methods in libraries, 3(3), pp.619-626.

Kang, J., 2018. Mobile payment in Fintech environment: trends, security

challenges, and services. Human-centric Computing and Information

Sciences, 8(1), p.32.

Lai, R., 2018. Understanding Interbank Real-Time Retail Payment Systems.

In Handbook of Blockchain, Digital Finance, and Inclusion, Volume 1 (pp.

283-310). Academic Press.

Linton, J.D. and Solomon, G.T., 2017. Technology, Innovation,

Entrepreneurship and The Small Business—Technology and Innovation in

Small Business. Journal of Small Business Management, 55(2), pp.196-199.

Merton, R.C. and Thakor, R.T., 2018. Customers and investors: a framework

for understanding the evolution of financial institutions. Journal of Financial

Intermediation.

Navaretti, G.B., Calzolari, G., Mansilla-Fernandez, J.M. and Pozzolo, A.F.,

2018. Fintech and Banking. Friends or Foes?. Friends or Foes.

Ng, A.W. and Kwok, B.K., 2017. Emergence of Fintech and cybersecurity in

a global financial centre: Strategic approach by a regulator. Journal of

Financial Regulation and Compliance, 25(4), pp.422-434.

Ogbanufe, O. and Kim, D.J., 2018. Comparing fingerprint-based biometrics

authentication versus traditional authentication methods for e-payment.

Decision Support Systems, 106, pp.1-14.

Oshodin, O., Molla, A., Karanasios, S. and Ong, C.E., 2017. Is FinTech a

disruption or a new eco-system? An exploratory investigation of Banksr

response to FinTech in Australia. In Proceeding of Australasian Conference

on Information Systems (pp. 1-11).

Pitard, F.F., 2019. Theory of Sampling and Sampling Practice. Chapman and

Hall/CRC.

Prabhu, R., Sinha, A. and Hayes, J.D., Mastercard Asia/Pacific Pte Ltd, 2016.

Methods and systems for secure online payment. U.S. Patent Application

14/878,167.

Ray, C., 2017. Logical positivism. A companion to the philosophy of science,

pp.243-251.

References

Saunders, M.N., Lewis, P., Thornhill, A. and Bristow, A., 2015.

Understanding research philosophy and approaches to theory development.

Scott, S.V., Van Reenen, J. and Zachariadis, M., 2017. The long-term effect of

digital innovation on bank performance: An empirical study of SWIFT

adoption in financial services. Research Policy, 46(5), pp.984-1004.

Singh, K.D., 2015. Creating your own qualitative research approach:

Selecting, integrating and operationalizing philosophy, methodology and

methods. Vision, 19(2), pp.132-146.

Su, W., 2016, May. Research on the Development of Online Financing and

the Influences on Traditional Financial and Insurance Industry. In 2016

International Conference on Economy, Management and Education

Technology. Atlantis Press.

Wall, J., Von Behren, R. and COLLINE, I.R.E., Google LLC, 2016. One-click

offline buying. U.S. Patent 9,390,414.

Wang, Y., Hahn, C. and Sutrave, K., 2016, February. Mobile payment

security, threats, and challenges. In 2016 second international conference on

mobile and secure services (MobiSecServ) (pp. 1-5). IEEE.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.