Impact of Fintech on Liquidity in Global Trade & Supply Chain Finance

VerifiedAdded on 2023/04/22

|31

|6196

|67

Report

AI Summary

This report investigates the impact of financial technology (fintech) on liquidity within global supply chains, highlighting the limitations of traditional banking platforms in processing modern financial transactions. Fintech facilitates faster, real-time money transfers, benefiting ventures and investors alike. The study explores fintech's role in international trade and supply chain finance, emphasizing its ability to enhance liquidity and profitability for suppliers by enabling quicker payments and access to broader markets. It also addresses challenges such as cyber threats and money laundering, suggesting future research should focus on minimizing these issues. The report concludes that fintech's real-time capabilities have revolutionized financial operations, while also acknowledging the need for ongoing improvements to address its inherent risks and maximize its potential.

Running head: FINTECH AND LIQUIDITY

Fintech and Liquidity

Name of the Student:

Name of the University:

Author Note:

Fintech and Liquidity

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINTECH AND LIQUIDITY

1. Abstract:

The research brings into light that fact that

traditional banking platforms are no more

sufficient to process the millions of financial

transactions. Financial technology or fintech

is the newly emerging technology which can

process several transactions per second.

Fintech enables faster and real time transfer

of money. The report then goes onto show

that fintech due to its real time transfer of

funds my using laptops and smart has

facilitated high liquidity in terms of finance

in the global supply chains. The ventures

can avail finance more easily from investors

using fintech platforms and provide ROI on

real time basis using the platform. However,

the report also highlights that fintech suffers

from issues like cyber threats, money

laundering and lack of invetsments. The

study further closes by mention future works

in the fintech area should emphasise on

finding minimising these issues.

FINTECH AND LIQUIDITY

1. Abstract:

The research brings into light that fact that

traditional banking platforms are no more

sufficient to process the millions of financial

transactions. Financial technology or fintech

is the newly emerging technology which can

process several transactions per second.

Fintech enables faster and real time transfer

of money. The report then goes onto show

that fintech due to its real time transfer of

funds my using laptops and smart has

facilitated high liquidity in terms of finance

in the global supply chains. The ventures

can avail finance more easily from investors

using fintech platforms and provide ROI on

real time basis using the platform. However,

the report also highlights that fintech suffers

from issues like cyber threats, money

laundering and lack of invetsments. The

study further closes by mention future works

in the fintech area should emphasise on

finding minimising these issues.

2

FINTECH AND LIQUIDITY

Table of Contents

1. Abstract:.......................................................................................................................................1

2. Introduction:................................................................................................................................3

2.1. Motivation:...........................................................................................................................3

2.3. Research question:................................................................................................................4

2.4. Contribution:.........................................................................................................................4

2.5. Impact and implication:........................................................................................................5

3. Related work:...............................................................................................................................7

3.1. Financial technology:............................................................................................................7

3.2. Fintech and international trade:............................................................................................8

3.3. Fintech and supply chain finance:........................................................................................9

3.4. Trade financing and fintech:...............................................................................................12

3.5. Challenges and threats to implementation of fintech:........................................................15

4. Research methodology:.............................................................................................................17

Justification of using realism:....................................................................................................17

5. Results:......................................................................................................................................18

6. Conclusions and future works:..................................................................................................18

7. Bibleography:............................................................................................................................20

FINTECH AND LIQUIDITY

Table of Contents

1. Abstract:.......................................................................................................................................1

2. Introduction:................................................................................................................................3

2.1. Motivation:...........................................................................................................................3

2.3. Research question:................................................................................................................4

2.4. Contribution:.........................................................................................................................4

2.5. Impact and implication:........................................................................................................5

3. Related work:...............................................................................................................................7

3.1. Financial technology:............................................................................................................7

3.2. Fintech and international trade:............................................................................................8

3.3. Fintech and supply chain finance:........................................................................................9

3.4. Trade financing and fintech:...............................................................................................12

3.5. Challenges and threats to implementation of fintech:........................................................15

4. Research methodology:.............................................................................................................17

Justification of using realism:....................................................................................................17

5. Results:......................................................................................................................................18

6. Conclusions and future works:..................................................................................................18

7. Bibleography:............................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINTECH AND LIQUIDITY

2. Introduction:

2.1. Motivation:

Global business environment has become

extremely dynamic and integrated with

immense amount of the revenue from one

country to another. The growth of

international trade and the ecommerce have

led to the need to process multiple payments

by the existing systems. The traditional

banking platforms are not capable of

handling this immense number of payment

requisitions (Bruton et al. 2015). Clavijo et

al. (2019) strengthen the discussion by

mentioning that business organizations,

especially the multinational companies

today require continuous flow of capital to

support their global operations. Gomber et

al. (2018) throw further light on the

discussion by mentioning companies in

order to diversify their risks of investments

today diversify their asset portfolio among

various types of securities both in their

home countries as well as foreign nations.

Chaney (2016) points out in this respect that

companies in order to ensure high liquidity

often sell their inventories to foreign

markets. Thus, it is evident that the present

global economic situation is characterized

by immense flow of financial resources

which traditional payment processing

platforms fail to process. This gap between

the needs of the business organisations and

the traditional payment processing payment

is served to fintech or financial technology.

Financial technology consists of technology

which enables processing of immense

number of payments which enables the

movement of immense amount financial

resources in the global (Bodenstein, Erceg

and Guerrieri 2017). The increasing role in

financial technology in the global business

processing and the benefits which it

FINTECH AND LIQUIDITY

2. Introduction:

2.1. Motivation:

Global business environment has become

extremely dynamic and integrated with

immense amount of the revenue from one

country to another. The growth of

international trade and the ecommerce have

led to the need to process multiple payments

by the existing systems. The traditional

banking platforms are not capable of

handling this immense number of payment

requisitions (Bruton et al. 2015). Clavijo et

al. (2019) strengthen the discussion by

mentioning that business organizations,

especially the multinational companies

today require continuous flow of capital to

support their global operations. Gomber et

al. (2018) throw further light on the

discussion by mentioning companies in

order to diversify their risks of investments

today diversify their asset portfolio among

various types of securities both in their

home countries as well as foreign nations.

Chaney (2016) points out in this respect that

companies in order to ensure high liquidity

often sell their inventories to foreign

markets. Thus, it is evident that the present

global economic situation is characterized

by immense flow of financial resources

which traditional payment processing

platforms fail to process. This gap between

the needs of the business organisations and

the traditional payment processing payment

is served to fintech or financial technology.

Financial technology consists of technology

which enables processing of immense

number of payments which enables the

movement of immense amount financial

resources in the global (Bodenstein, Erceg

and Guerrieri 2017). The increasing role in

financial technology in the global business

processing and the benefits which it

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINTECH AND LIQUIDITY

ushers has motivated to conduct a research in the area.

2.2. Context of the research:

Financial technology plays a very significant

role in mobilisation of the financial

resources in the global economy. Korpela,

Hallikas and Dahlberg (2017) mention that

fintech comes under external market

environment factors like technology and

economic structure. Further, it can also be

mentioned that use of fintech invites scope

of cyber threats. The advantages which

fintech is capable of attributing to the global

economy and the threats or challenges which

business organisations would face while

implementing fintech would form the

context of the research.

2.3. Research question:

The main research question will be:

Will fintech enable suppliers to achieve more liquidity and profit compared to the

traditional banking channels?

2.4. Contribution:

Financial technology contributes to liquidity

and profitability of commercial

organisations in several ways. The business

organisations are able to market their goods

in several markets and receive payments.

Similarly, the companies are able to pay

dividends to investors on the online

platforms and receive payments. The third

way in which fintech contributes to the

liquidity and profitability is by enabling the

companies invest in foreign assets which in

turn diversify their risks. Thus, fintech

enables the business organisations to

FINTECH AND LIQUIDITY

ushers has motivated to conduct a research in the area.

2.2. Context of the research:

Financial technology plays a very significant

role in mobilisation of the financial

resources in the global economy. Korpela,

Hallikas and Dahlberg (2017) mention that

fintech comes under external market

environment factors like technology and

economic structure. Further, it can also be

mentioned that use of fintech invites scope

of cyber threats. The advantages which

fintech is capable of attributing to the global

economy and the threats or challenges which

business organisations would face while

implementing fintech would form the

context of the research.

2.3. Research question:

The main research question will be:

Will fintech enable suppliers to achieve more liquidity and profit compared to the

traditional banking channels?

2.4. Contribution:

Financial technology contributes to liquidity

and profitability of commercial

organisations in several ways. The business

organisations are able to market their goods

in several markets and receive payments.

Similarly, the companies are able to pay

dividends to investors on the online

platforms and receive payments. The third

way in which fintech contributes to the

liquidity and profitability is by enabling the

companies invest in foreign assets which in

turn diversify their risks. Thus, fintech

enables the business organisations to

5

FINTECH AND LIQUIDITY

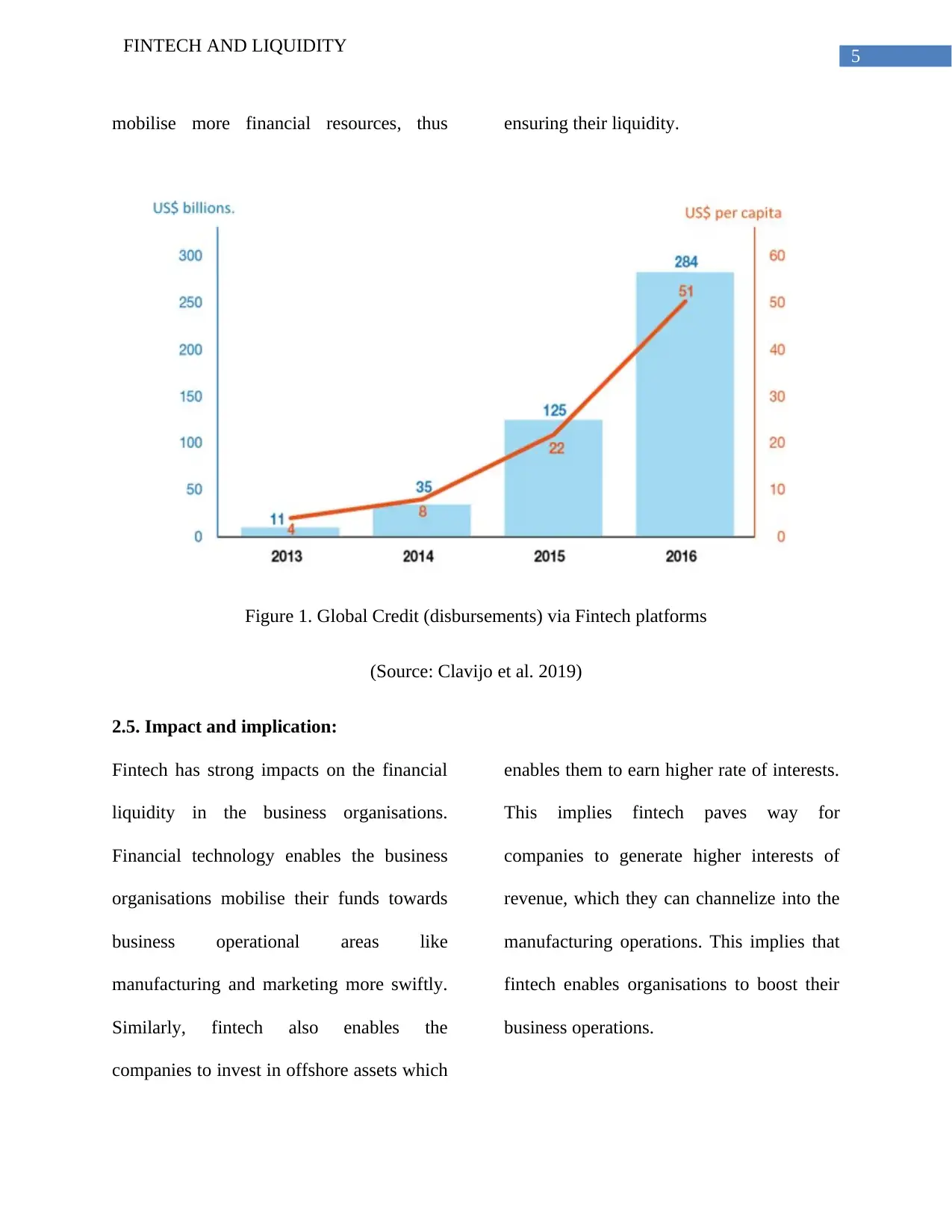

mobilise more financial resources, thus ensuring their liquidity.

Figure 1. Global Credit (disbursements) via Fintech platforms

(Source: Clavijo et al. 2019)

2.5. Impact and implication:

Fintech has strong impacts on the financial

liquidity in the business organisations.

Financial technology enables the business

organisations mobilise their funds towards

business operational areas like

manufacturing and marketing more swiftly.

Similarly, fintech also enables the

companies to invest in offshore assets which

enables them to earn higher rate of interests.

This implies fintech paves way for

companies to generate higher interests of

revenue, which they can channelize into the

manufacturing operations. This implies that

fintech enables organisations to boost their

business operations.

FINTECH AND LIQUIDITY

mobilise more financial resources, thus ensuring their liquidity.

Figure 1. Global Credit (disbursements) via Fintech platforms

(Source: Clavijo et al. 2019)

2.5. Impact and implication:

Fintech has strong impacts on the financial

liquidity in the business organisations.

Financial technology enables the business

organisations mobilise their funds towards

business operational areas like

manufacturing and marketing more swiftly.

Similarly, fintech also enables the

companies to invest in offshore assets which

enables them to earn higher rate of interests.

This implies fintech paves way for

companies to generate higher interests of

revenue, which they can channelize into the

manufacturing operations. This implies that

fintech enables organisations to boost their

business operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINTECH AND LIQUIDITY

Investors

Companies using fintech

Suppliers

Customers

Foreign

securities

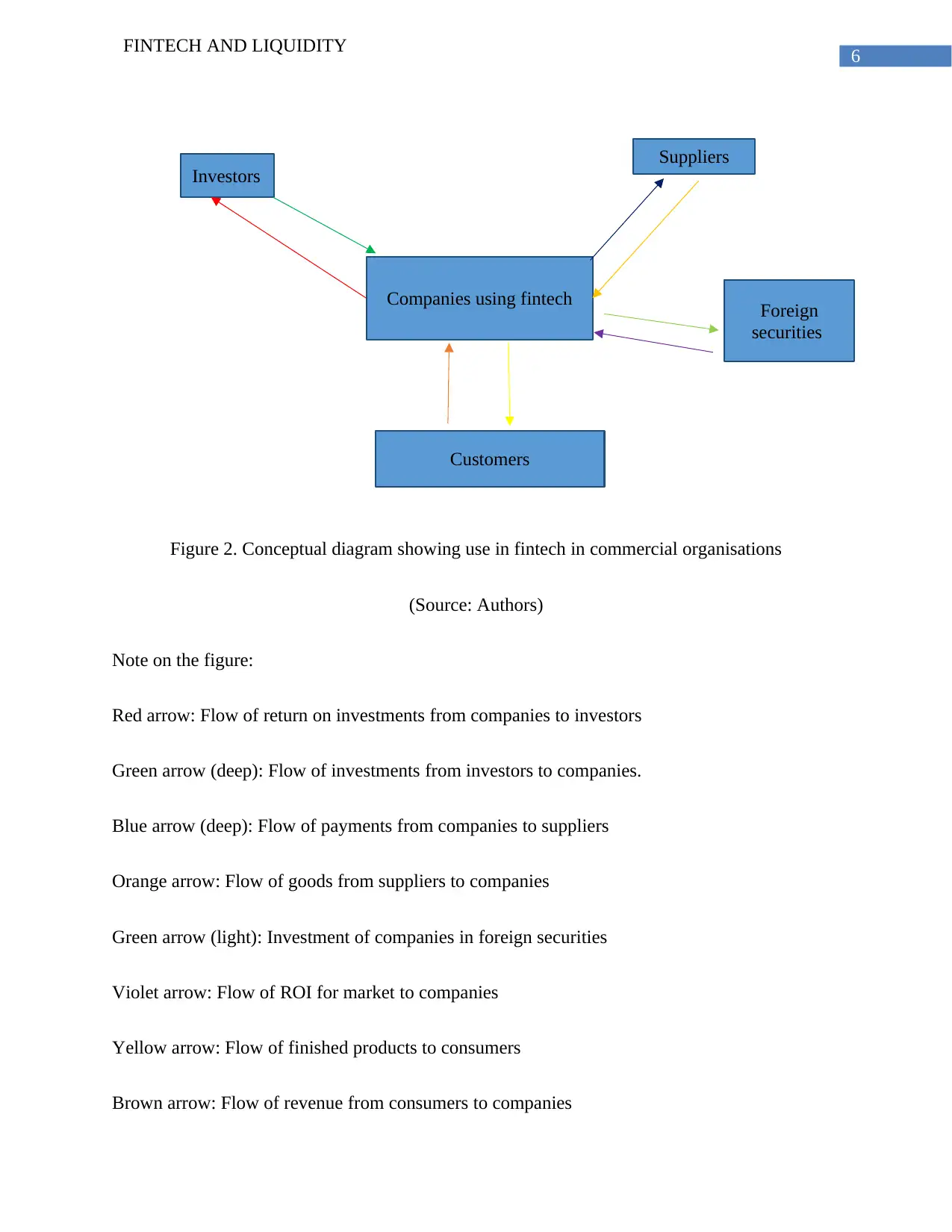

Figure 2. Conceptual diagram showing use in fintech in commercial organisations

(Source: Authors)

Note on the figure:

Red arrow: Flow of return on investments from companies to investors

Green arrow (deep): Flow of investments from investors to companies.

Blue arrow (deep): Flow of payments from companies to suppliers

Orange arrow: Flow of goods from suppliers to companies

Green arrow (light): Investment of companies in foreign securities

Violet arrow: Flow of ROI for market to companies

Yellow arrow: Flow of finished products to consumers

Brown arrow: Flow of revenue from consumers to companies

FINTECH AND LIQUIDITY

Investors

Companies using fintech

Suppliers

Customers

Foreign

securities

Figure 2. Conceptual diagram showing use in fintech in commercial organisations

(Source: Authors)

Note on the figure:

Red arrow: Flow of return on investments from companies to investors

Green arrow (deep): Flow of investments from investors to companies.

Blue arrow (deep): Flow of payments from companies to suppliers

Orange arrow: Flow of goods from suppliers to companies

Green arrow (light): Investment of companies in foreign securities

Violet arrow: Flow of ROI for market to companies

Yellow arrow: Flow of finished products to consumers

Brown arrow: Flow of revenue from consumers to companies

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINTECH AND LIQUIDITY

3. Related work:

3.1. Financial technology:

Farboodi and Veldkamp (2017) mentions

that the term financial technology

abbreviated as fintech refers to use of

technology in the facilitating financial

transactions. Fntech involves use of

technologically advanced devices like

laptops, smart phones and mobile banking to

conduct financial transactions. The use of

financial technology include use of

electronic devices which enables companies

to manage their financial conditions more

effectively that traditional banking

platforms. Crosby et al. (2016) throw light

on another aspect of financial technology

which is block chain technology. The

logistics companies use block chain to

ensure efficient management of their

business information to ensure strict

management of the financial resources to

ensure reduction of expenditures and

increase of profit. The firms supplying

goods and services use fintech to receive

prompt payments for the supply of

inventories to their business customers. The

investors can view real time share market

data on their laptops and smart phones. The

investors can invest in the shares of the

companies as per their discretion. Thus, it

can be inferred from the discussion that

fintech plays important roles in financial

management of business organisations.

FINTECH AND LIQUIDITY

3. Related work:

3.1. Financial technology:

Farboodi and Veldkamp (2017) mentions

that the term financial technology

abbreviated as fintech refers to use of

technology in the facilitating financial

transactions. Fntech involves use of

technologically advanced devices like

laptops, smart phones and mobile banking to

conduct financial transactions. The use of

financial technology include use of

electronic devices which enables companies

to manage their financial conditions more

effectively that traditional banking

platforms. Crosby et al. (2016) throw light

on another aspect of financial technology

which is block chain technology. The

logistics companies use block chain to

ensure efficient management of their

business information to ensure strict

management of the financial resources to

ensure reduction of expenditures and

increase of profit. The firms supplying

goods and services use fintech to receive

prompt payments for the supply of

inventories to their business customers. The

investors can view real time share market

data on their laptops and smart phones. The

investors can invest in the shares of the

companies as per their discretion. Thus, it

can be inferred from the discussion that

fintech plays important roles in financial

management of business organisations.

8

FINTECH AND LIQUIDITY

Figure 3. Drivers of fintech

(Source: Riemer et al. 2017)

3.2. Fintech and international trade:

Fintech plays a very important role in

international trade and revenue generation in

the business organisations. Okere (2017)

mentions that customers can purchase goods

on the ecommerce platforms. They can

make payments using internet banking and

mobile banking network which gets credited

to the bank accounts of the companies

marketing the goods concerned. Fang and

Zhang (2016) strengthens the argument by

pointing out that customers while making

payment input their details like names. The

companies can acquire immense amount of

customer data which they can use to predict

the patterns of customer preferences. Curtis

and Sweeney (2017) support the argument

by pointing out that fintech enables the

companies to make real business strategies

based on the customer information acquired

using the technologically advanced

platforms. Carney (2017) agrees the fintech

makes more financial resources to both start-

FINTECH AND LIQUIDITY

Figure 3. Drivers of fintech

(Source: Riemer et al. 2017)

3.2. Fintech and international trade:

Fintech plays a very important role in

international trade and revenue generation in

the business organisations. Okere (2017)

mentions that customers can purchase goods

on the ecommerce platforms. They can

make payments using internet banking and

mobile banking network which gets credited

to the bank accounts of the companies

marketing the goods concerned. Fang and

Zhang (2016) strengthens the argument by

pointing out that customers while making

payment input their details like names. The

companies can acquire immense amount of

customer data which they can use to predict

the patterns of customer preferences. Curtis

and Sweeney (2017) support the argument

by pointing out that fintech enables the

companies to make real business strategies

based on the customer information acquired

using the technologically advanced

platforms. Carney (2017) agrees the fintech

makes more financial resources to both start-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINTECH AND LIQUIDITY

ups and existing companies. This

encourages product innovation which makes

more goods and services available to

customers. These facts are more applicable

for multinational companies which serve

global consumer base. The global companies

are able to sell their products in several

markets and receive huge amount of revenue

for sale of products on the ecommerce

portals. They are able to channelize portions

of revenue towards making payments to

suppliers and ROI to investors. The

companies in return are able to obtain more

raw materials and capital from suppliers and

investors as a result (Gomber et al. 2018).

Thus, in other words fintech provides a

strong base for global flow of revenue and

capital, thus empowering international trade.

FINTECH AND LIQUIDITY

ups and existing companies. This

encourages product innovation which makes

more goods and services available to

customers. These facts are more applicable

for multinational companies which serve

global consumer base. The global companies

are able to sell their products in several

markets and receive huge amount of revenue

for sale of products on the ecommerce

portals. They are able to channelize portions

of revenue towards making payments to

suppliers and ROI to investors. The

companies in return are able to obtain more

raw materials and capital from suppliers and

investors as a result (Gomber et al. 2018).

Thus, in other words fintech provides a

strong base for global flow of revenue and

capital, thus empowering international trade.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINTECH AND LIQUIDITY

Companies

Goods and services

Customers

Online payment through banks

Premium and interest

on invetstment

Investors Investments

Suppliers

Online payment for materials

Raw materials

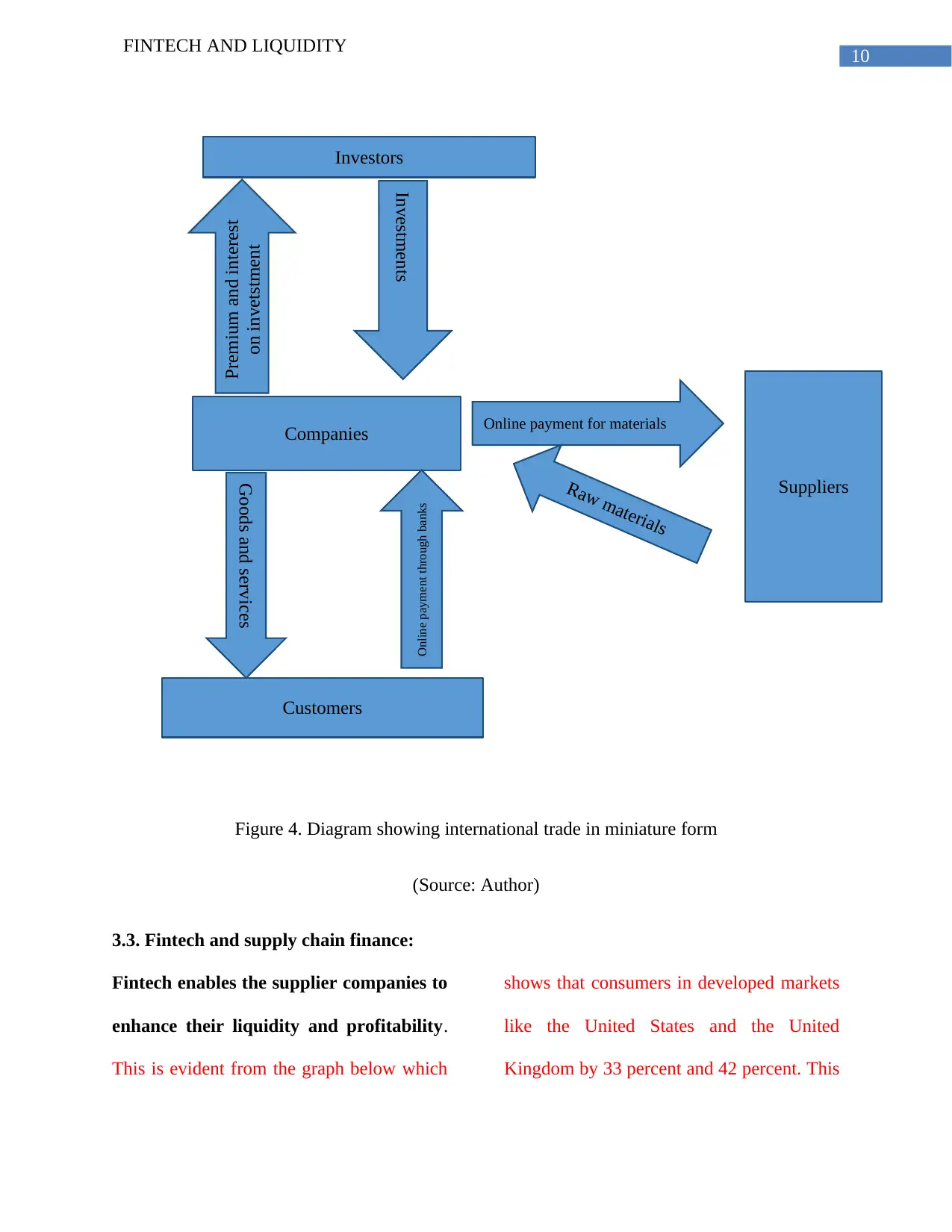

Figure 4. Diagram showing international trade in miniature form

(Source: Author)

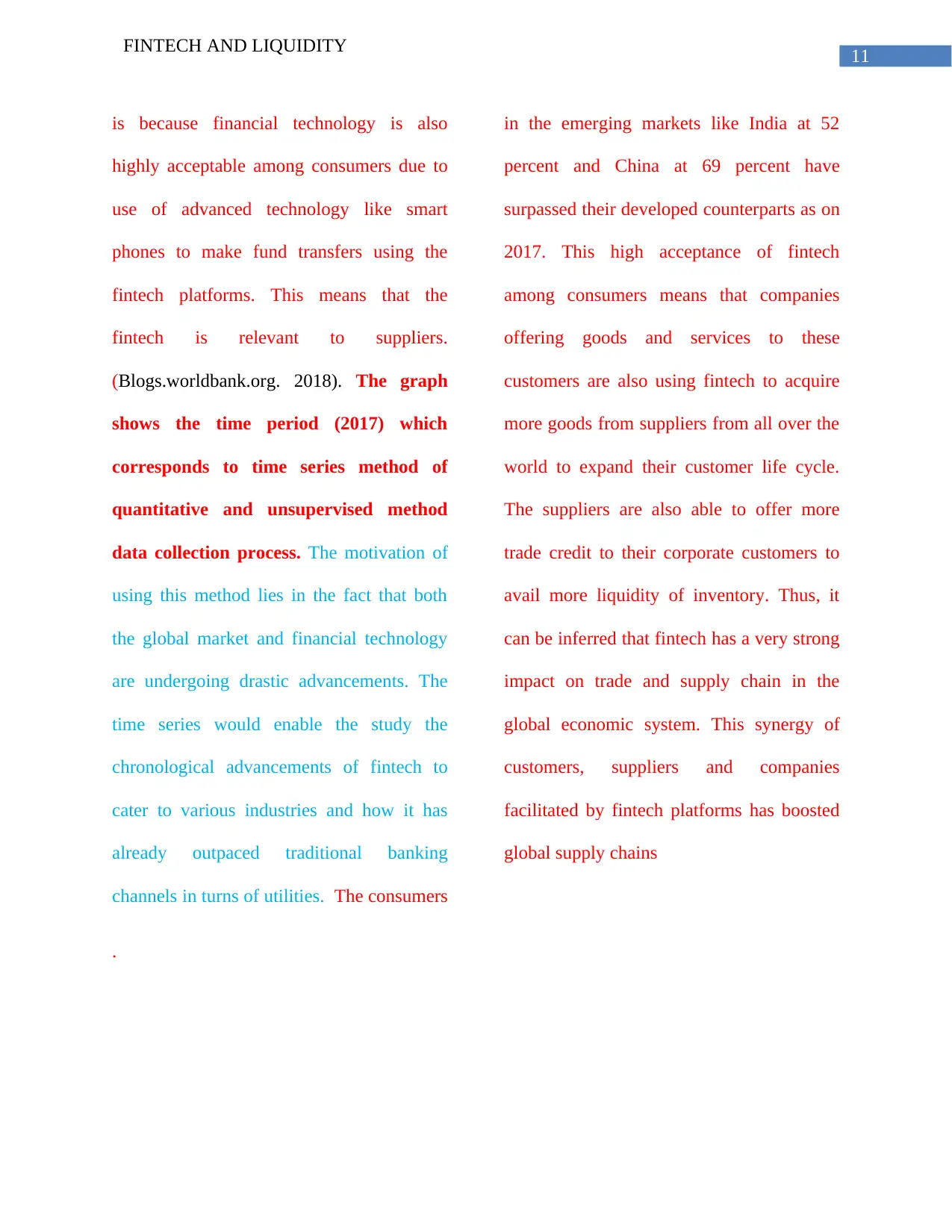

3.3. Fintech and supply chain finance:

Fintech enables the supplier companies to

enhance their liquidity and profitability.

This is evident from the graph below which

shows that consumers in developed markets

like the United States and the United

Kingdom by 33 percent and 42 percent. This

FINTECH AND LIQUIDITY

Companies

Goods and services

Customers

Online payment through banks

Premium and interest

on invetstment

Investors Investments

Suppliers

Online payment for materials

Raw materials

Figure 4. Diagram showing international trade in miniature form

(Source: Author)

3.3. Fintech and supply chain finance:

Fintech enables the supplier companies to

enhance their liquidity and profitability.

This is evident from the graph below which

shows that consumers in developed markets

like the United States and the United

Kingdom by 33 percent and 42 percent. This

11

FINTECH AND LIQUIDITY

is because financial technology is also

highly acceptable among consumers due to

use of advanced technology like smart

phones to make fund transfers using the

fintech platforms. This means that the

fintech is relevant to suppliers.

(Blogs.worldbank.org. 2018). The graph

shows the time period (2017) which

corresponds to time series method of

quantitative and unsupervised method

data collection process. The motivation of

using this method lies in the fact that both

the global market and financial technology

are undergoing drastic advancements. The

time series would enable the study the

chronological advancements of fintech to

cater to various industries and how it has

already outpaced traditional banking

channels in turns of utilities. The consumers

in the emerging markets like India at 52

percent and China at 69 percent have

surpassed their developed counterparts as on

2017. This high acceptance of fintech

among consumers means that companies

offering goods and services to these

customers are also using fintech to acquire

more goods from suppliers from all over the

world to expand their customer life cycle.

The suppliers are also able to offer more

trade credit to their corporate customers to

avail more liquidity of inventory. Thus, it

can be inferred that fintech has a very strong

impact on trade and supply chain in the

global economic system. This synergy of

customers, suppliers and companies

facilitated by fintech platforms has boosted

global supply chains

.

FINTECH AND LIQUIDITY

is because financial technology is also

highly acceptable among consumers due to

use of advanced technology like smart

phones to make fund transfers using the

fintech platforms. This means that the

fintech is relevant to suppliers.

(Blogs.worldbank.org. 2018). The graph

shows the time period (2017) which

corresponds to time series method of

quantitative and unsupervised method

data collection process. The motivation of

using this method lies in the fact that both

the global market and financial technology

are undergoing drastic advancements. The

time series would enable the study the

chronological advancements of fintech to

cater to various industries and how it has

already outpaced traditional banking

channels in turns of utilities. The consumers

in the emerging markets like India at 52

percent and China at 69 percent have

surpassed their developed counterparts as on

2017. This high acceptance of fintech

among consumers means that companies

offering goods and services to these

customers are also using fintech to acquire

more goods from suppliers from all over the

world to expand their customer life cycle.

The suppliers are also able to offer more

trade credit to their corporate customers to

avail more liquidity of inventory. Thus, it

can be inferred that fintech has a very strong

impact on trade and supply chain in the

global economic system. This synergy of

customers, suppliers and companies

facilitated by fintech platforms has boosted

global supply chains

.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.