Fintech and Sustainability: A Comprehensive Literature Review

VerifiedAdded on 2021/09/27

|19

|14114

|150

Report

AI Summary

This report examines the evolving relationship between Fintech and sustainability, focusing on the impact of digital transformation and the rise of sustainable finance. It explores how Fintech innovations, such as digital platforms and applications, are influencing green finance, green investment, and socially responsible investing (SRI). The report delves into the challenges of greenwashing and deceptive practices within the financial sector, emphasizing the importance of consumer protection and regulatory oversight. It analyzes the potential of Fintech to promote sustainability by facilitating access to green investments and enhancing transparency. Furthermore, the report provides examples of Fintech initiatives like Clarity AI and Pensumo, along with proposals to improve the detection of misleading environmental claims by firms. The conclusion highlights the common aspects of sustainable finance and Fintech and underscores the significance of European and global regulations in this evolving landscape. The report also touches on the role of digitization, internationalization, and risk analysis in the financial field, highlighting the importance of Fintech's advantages, such as greater customer control and rapid financial decision-making.

sustainability

Review

Fintech and Sustainability: Do They Affect Each Other?

Cristina Chueca Vergara * and Luis Ferruz Agudo

Citation:Chueca Vergara, C.; Ferruz

Agudo, L. Fintech and Sustainability:

Do They Affect Each Other?.

Sustainability 2021, 13, 7012.https://

doi.org/10.3390/su13137012

Academic Editors: Salvador

Cruz Rambaud, Joaquín

López Pascual and Bruce Morley

Received: 14 April 2021

Accepted: 19 June 2021

Published: 22 June 2021

Publisher’s Note: MDPI stays neutral

with regard to jurisdictional claims in

published maps and institutional affil-

iations.

Copyright:© 2021 by the authors.

LicenseeMDPI, Basel, Switzerland.

This article is an open access article

distributed under the terms and

conditions of the Creative Commons

Attribution (CC BY) license (https://

creativecommons.org/licenses/by/

4.0/).

Accounting and Finance Department, Faculty of Economics and Business, University of Zaragoza,

50005 Zaragoza, Spain; lferruz@unizar.es

* Correspondence: 720270@unizar.es

Abstract: Current concerns about environmental issues have led to many new trends in techn

and financial management.Within this context of digital transformation and sustainable financ

Fintech has emerged as an alternative to traditional financial institutions.This paper, through a

literature review and case study approach, analyzes the relationship between Fintech and s

ability, and the different areas of collaboration between Fintech and sustainable finance, from

a theoretical and descriptive perspective, while giving specific examples of current technol

platforms. Additionally, in this paper, two Fintech initiatives (Clarity AI and Pensumo) are descri

as well as several proposals to improve the detection of greenwashing and other deceptive be

by firms. The results lead to the conclusion that sustainable finance and Fintech have many as

in common, and that Fintech can make financial businesses more sustainable overall by promo

green finance. Furthermore, this paper highlights the importance of European and global regu

mainly from the perspective of consumer protection.

Keywords:Fintech;sustainability;green investment;socially responsible investing (SRI);green

finance; greenwashing; digitization

1. Introduction

Currently, more and more new issues are emerging that affect financial managem

These are the consequence of increasing customer concerns for sustainability and res

for the environment in the goods and services they purchase and consume, as well as

growing digitization.

Important examples of these issues are corporate social responsibility (CSR) and e

ronmental, social, and governance (ESG) factors. Similarly, the 2030 Agenda for Susta

Development Goals (SDGs) promoted by the United Nations plays an important role

combating climate change.

The growing awareness of global warming and its negative impact on the plane

means that customers are increasingly demanding ecological or environmentally frie

products for a more sustainable lifestyle. Customers, investors, and public administrati

are exerting increasing pressure on organizations to obtain more transparent informa

on the environmental impact of their activities.For example,Nielsen Media Research

reports that “66% of global consumers” (and 73% of millennials) [1] “are willing to pay

more for environmentally friendly products. Thus, when these customers perceive firm

be socially responsible, they may be more willing to buy the products of these firms, an

a higher price” [2].

Hence, firms strive to differentiate their products and their brands from their c

petitors,setting up “green marketing” campaigns and modernizing their technologie

In addition, they compete for consumers’ approval by advertising their products as

vironmentally friendly.These green marketing initiatives “are helpful to consumers b

letting them know which products possess said green properties, but only if the claim

advertisements and product descriptions are honest and accurate” [3].

Sustainability 2021, 13, 7012. https://doi.org/10.3390/su13137012 https://www.mdpi.com/journal/sustainability

Review

Fintech and Sustainability: Do They Affect Each Other?

Cristina Chueca Vergara * and Luis Ferruz Agudo

Citation:Chueca Vergara, C.; Ferruz

Agudo, L. Fintech and Sustainability:

Do They Affect Each Other?.

Sustainability 2021, 13, 7012.https://

doi.org/10.3390/su13137012

Academic Editors: Salvador

Cruz Rambaud, Joaquín

López Pascual and Bruce Morley

Received: 14 April 2021

Accepted: 19 June 2021

Published: 22 June 2021

Publisher’s Note: MDPI stays neutral

with regard to jurisdictional claims in

published maps and institutional affil-

iations.

Copyright:© 2021 by the authors.

LicenseeMDPI, Basel, Switzerland.

This article is an open access article

distributed under the terms and

conditions of the Creative Commons

Attribution (CC BY) license (https://

creativecommons.org/licenses/by/

4.0/).

Accounting and Finance Department, Faculty of Economics and Business, University of Zaragoza,

50005 Zaragoza, Spain; lferruz@unizar.es

* Correspondence: 720270@unizar.es

Abstract: Current concerns about environmental issues have led to many new trends in techn

and financial management.Within this context of digital transformation and sustainable financ

Fintech has emerged as an alternative to traditional financial institutions.This paper, through a

literature review and case study approach, analyzes the relationship between Fintech and s

ability, and the different areas of collaboration between Fintech and sustainable finance, from

a theoretical and descriptive perspective, while giving specific examples of current technol

platforms. Additionally, in this paper, two Fintech initiatives (Clarity AI and Pensumo) are descri

as well as several proposals to improve the detection of greenwashing and other deceptive be

by firms. The results lead to the conclusion that sustainable finance and Fintech have many as

in common, and that Fintech can make financial businesses more sustainable overall by promo

green finance. Furthermore, this paper highlights the importance of European and global regu

mainly from the perspective of consumer protection.

Keywords:Fintech;sustainability;green investment;socially responsible investing (SRI);green

finance; greenwashing; digitization

1. Introduction

Currently, more and more new issues are emerging that affect financial managem

These are the consequence of increasing customer concerns for sustainability and res

for the environment in the goods and services they purchase and consume, as well as

growing digitization.

Important examples of these issues are corporate social responsibility (CSR) and e

ronmental, social, and governance (ESG) factors. Similarly, the 2030 Agenda for Susta

Development Goals (SDGs) promoted by the United Nations plays an important role

combating climate change.

The growing awareness of global warming and its negative impact on the plane

means that customers are increasingly demanding ecological or environmentally frie

products for a more sustainable lifestyle. Customers, investors, and public administrati

are exerting increasing pressure on organizations to obtain more transparent informa

on the environmental impact of their activities.For example,Nielsen Media Research

reports that “66% of global consumers” (and 73% of millennials) [1] “are willing to pay

more for environmentally friendly products. Thus, when these customers perceive firm

be socially responsible, they may be more willing to buy the products of these firms, an

a higher price” [2].

Hence, firms strive to differentiate their products and their brands from their c

petitors,setting up “green marketing” campaigns and modernizing their technologie

In addition, they compete for consumers’ approval by advertising their products as

vironmentally friendly.These green marketing initiatives “are helpful to consumers b

letting them know which products possess said green properties, but only if the claim

advertisements and product descriptions are honest and accurate” [3].

Sustainability 2021, 13, 7012. https://doi.org/10.3390/su13137012 https://www.mdpi.com/journal/sustainability

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sustainability 2021, 13, 7012 2 of 19

On the one hand, the innovations of green technologies provide additional financ

resources, because green investment is an alternative option for financing such mode

tion. On the other hand, the existing competition for obtaining green-oriented inves

and consumers leads to the use of “greenwashing” by companies as an unfair market

instrument [4].

Greenwashing is a set of deceptive behaviors or practices that deliberately mis

consumers about the ecological activities of an organization or the environmental ben

of a given product, which appear to be sustainable but are not. Such practices are cond

using ambiguous words and images in the description of the environmental feature

a product or via vague, unprovable, and even false ecological claims, exaggerating

ecological features of the product by omitting or masking important information, o

presenting data in a misleading way.

In other words, “greenwashing” is an attempt by a company to make its produc

appear environmentally friendly when, in reality, they are not. The concept was cre

by Jay Westerveld in 1986 and can be defined as “the intersection of two firm beha

iors: poor environmental performance and positive communication about environmen

performance” [5].

Certain factors, such as CO2-neutral certification, contribute to this phenomenon

they allow a highly polluting company to appear ecologically sound by attaching a gre

label with this kind of certification for its products. However, such labels are not al

meaningful,and it is important to distinguish reliable companies and those providing

independent verification with standardized protocols from those that are not.

Greenwashing practices undermine the credibility of any corporate social respons

ity (CSR) endeavor, since they threaten to negate the effects of communicating a comp

efforts to act in an environmentally and socially responsible manner. At the same time,

threaten to erode customer confidence. “Whereas reporting about corporate social re

sibility (CSR) initiatives is a reasonable and even often economically sound thing to

greenwashing threatens to dilute the entire CSR movement, thereby reducing the pre

on companies to act economically and socially responsibly”. Moreover, we must cons

that “greenwashing is hard to detect with reasonable effort, so it goes unnoticed m

the time”, and “even if greenwashing is detected, it is not perceived as very negative

As a result, “consumers increasingly mistrust statements regarding CSR, as they

pect they are being lied to, or important information is being withheld”. Moreover, bec

greenwashing is not often detected, it “thereby does not have any negative conseque

for the respective manufacturer or vendor” [3].

In addition, concern for the environment and sustainability not only affects consum

but also investors,who increasingly consider certain non-financialattributes in their

investments,such as environmental,social,and governance (ESG) criteria.Related to

this is socially responsible investment (SRI),which “appeals to investors who wish to

go beyond the financial utility of their investments and derive non-financial utility b

investing in companies that reflect their social values” [7].

It must also be considered that “investors are increasingly willing to incorpora

into their investment decisions not only financial criteria (returns and risk), but als

non-financial attributes of SRI” [8] and that “country-specific factors tend to affect the

relationship between corporate social and financial performance” of a company. Anot

issue to bear in mind is that “there is some evidence that the label “socially respon

might be more a marketing strategy, thus not assuring investors that an SRI fund is r

socially responsible” [8].

Related to the above are “green bonds”, a type of fixed-income instrument app

exclusively to the partial or full financing or refinancing of eligible green projects, whe

new and/or existing,which are in line with the four core components of Green Bond

Principles (GBP) [9]. There are different kinds of green bonds on the market, and in 201

$257.7 billion in green bonds were issued, a 51% increase on the 2018 figure and cons

a new world record [9].

On the one hand, the innovations of green technologies provide additional financ

resources, because green investment is an alternative option for financing such mode

tion. On the other hand, the existing competition for obtaining green-oriented inves

and consumers leads to the use of “greenwashing” by companies as an unfair market

instrument [4].

Greenwashing is a set of deceptive behaviors or practices that deliberately mis

consumers about the ecological activities of an organization or the environmental ben

of a given product, which appear to be sustainable but are not. Such practices are cond

using ambiguous words and images in the description of the environmental feature

a product or via vague, unprovable, and even false ecological claims, exaggerating

ecological features of the product by omitting or masking important information, o

presenting data in a misleading way.

In other words, “greenwashing” is an attempt by a company to make its produc

appear environmentally friendly when, in reality, they are not. The concept was cre

by Jay Westerveld in 1986 and can be defined as “the intersection of two firm beha

iors: poor environmental performance and positive communication about environmen

performance” [5].

Certain factors, such as CO2-neutral certification, contribute to this phenomenon

they allow a highly polluting company to appear ecologically sound by attaching a gre

label with this kind of certification for its products. However, such labels are not al

meaningful,and it is important to distinguish reliable companies and those providing

independent verification with standardized protocols from those that are not.

Greenwashing practices undermine the credibility of any corporate social respons

ity (CSR) endeavor, since they threaten to negate the effects of communicating a comp

efforts to act in an environmentally and socially responsible manner. At the same time,

threaten to erode customer confidence. “Whereas reporting about corporate social re

sibility (CSR) initiatives is a reasonable and even often economically sound thing to

greenwashing threatens to dilute the entire CSR movement, thereby reducing the pre

on companies to act economically and socially responsibly”. Moreover, we must cons

that “greenwashing is hard to detect with reasonable effort, so it goes unnoticed m

the time”, and “even if greenwashing is detected, it is not perceived as very negative

As a result, “consumers increasingly mistrust statements regarding CSR, as they

pect they are being lied to, or important information is being withheld”. Moreover, bec

greenwashing is not often detected, it “thereby does not have any negative conseque

for the respective manufacturer or vendor” [3].

In addition, concern for the environment and sustainability not only affects consum

but also investors,who increasingly consider certain non-financialattributes in their

investments,such as environmental,social,and governance (ESG) criteria.Related to

this is socially responsible investment (SRI),which “appeals to investors who wish to

go beyond the financial utility of their investments and derive non-financial utility b

investing in companies that reflect their social values” [7].

It must also be considered that “investors are increasingly willing to incorpora

into their investment decisions not only financial criteria (returns and risk), but als

non-financial attributes of SRI” [8] and that “country-specific factors tend to affect the

relationship between corporate social and financial performance” of a company. Anot

issue to bear in mind is that “there is some evidence that the label “socially respon

might be more a marketing strategy, thus not assuring investors that an SRI fund is r

socially responsible” [8].

Related to the above are “green bonds”, a type of fixed-income instrument app

exclusively to the partial or full financing or refinancing of eligible green projects, whe

new and/or existing,which are in line with the four core components of Green Bond

Principles (GBP) [9]. There are different kinds of green bonds on the market, and in 201

$257.7 billion in green bonds were issued, a 51% increase on the 2018 figure and cons

a new world record [9].

Sustainability 2021, 13, 7012 3 of 19

Furthermore,as the supply and demand for sustainable financing have evolved,

several providers of (new) products and services have emerged over recent years. T

providers offer solutions for the (new) needs or demands set out in the new sustainab

paradigm.These new products and services have emerged in support of the ecologic

transition process to promote the link between sustainability and economic and finan

activities. Their various objectives include increasingly available information on clim

support for the design of more sustainable products and services; and the improvem

of public transparency and information. For example, in Spain, the Fundación Ecolog

Desarrollo, or ECODES (Ecology and Development Foundation), offers a climate-chan

risk assessment model that enables the financial sector to assess the predisposition to

and opportunities of its credit and investment portfolios. This service was designed to

used by the banking sector, but is also useful for other financial sector entities, such as

managers, investment advisers, insurance companies, and public sector entities in ch

of socio-economic planning and development [10]. On a global level, the organization that

conducts this kind of activity is the Intergovernmental Panel on Climate Change (IP

the United Nations body for assessing the science related to climate change [11].

Notwithstanding the above, digitization, internationalization, and risk analysis m

not be forgotten.These are some of the most widespread business practices in the cu

rent era and are being increasingly used in the financial field, in general, and finan

management, in particular.

Within the digitaland technologicalcontext,the specialimportance of so-called

“Fintech” must be highlighted. Fintech refers to the latest technologies used in innov

financial products and services. This is one of the most important new markets in re

times, and this cutting-edge business model has great potential for the collaboratio

different types of institutions, both public and private.

Fintech [12] comprises digital innovation and modern technology to improve,de-

velop, and automate financial services and is used to assist and support firms, inve

and customers in managing their financial activities using specialized applications

software [13]. Fintech generally attracts customers with more user-friendly, efficient, tr

parent, and automated products and services [14].

More specifically, Fintech includes new applications, processes, products, and bus

models in the area of financial services, consisting of one or more financial services, m

or entirely provided over the internet, “simultaneously by various independent serv

providers,typically including at least one licensed bank or insurance company” [15].

Some of the financial services provided may include investment advice (robo-advisi

credit decisions, asset trading, digital currencies, automatic transactions, payment se

crowdfunding, person-to-person transactions (P2P), and smartphone wallets [15].

The current era in the evolution of Fintech is called “Fintech 3.0”, which began

2008,and whose first years were dominated by the global crisis and financial turmo

when there was a loss in trust in the banking system.Then, technological firms began

to operate using peer-to-peer networks outside the regulatory framework (in fact, 2

of these platforms were developed in China) [16] and to apply new technologies in the

financial markets, changing the way of doing business in all financial sectors [17]. This

development is ongoing [17], and banks today are being displaced by technological fi

and start-ups at a rapid pace [16]. According to Moro-Visconti, Cruz Rambaud, and López

Pascual, some of the reasons for this rapid evolution of Fintech are the sharing and cir

economy, favorable regulation, and information technology [14].

Initially, the largest Fintech market was developed in the US, followed by the U

(the most important Fintech market in Europe) [18]. The European and American Fintech

properties and background differ from the Asian Fintech, which specifically offers solu

for a lack of existing banking infrastructure [19].

Establishing Fintech is easier in well-developed economies, because the infrastruc

and market regulations are there already. This infrastructure and affordable technolog

critical to creating sustainable, unique financial innovation, although Fintech developm

Furthermore,as the supply and demand for sustainable financing have evolved,

several providers of (new) products and services have emerged over recent years. T

providers offer solutions for the (new) needs or demands set out in the new sustainab

paradigm.These new products and services have emerged in support of the ecologic

transition process to promote the link between sustainability and economic and finan

activities. Their various objectives include increasingly available information on clim

support for the design of more sustainable products and services; and the improvem

of public transparency and information. For example, in Spain, the Fundación Ecolog

Desarrollo, or ECODES (Ecology and Development Foundation), offers a climate-chan

risk assessment model that enables the financial sector to assess the predisposition to

and opportunities of its credit and investment portfolios. This service was designed to

used by the banking sector, but is also useful for other financial sector entities, such as

managers, investment advisers, insurance companies, and public sector entities in ch

of socio-economic planning and development [10]. On a global level, the organization that

conducts this kind of activity is the Intergovernmental Panel on Climate Change (IP

the United Nations body for assessing the science related to climate change [11].

Notwithstanding the above, digitization, internationalization, and risk analysis m

not be forgotten.These are some of the most widespread business practices in the cu

rent era and are being increasingly used in the financial field, in general, and finan

management, in particular.

Within the digitaland technologicalcontext,the specialimportance of so-called

“Fintech” must be highlighted. Fintech refers to the latest technologies used in innov

financial products and services. This is one of the most important new markets in re

times, and this cutting-edge business model has great potential for the collaboratio

different types of institutions, both public and private.

Fintech [12] comprises digital innovation and modern technology to improve,de-

velop, and automate financial services and is used to assist and support firms, inve

and customers in managing their financial activities using specialized applications

software [13]. Fintech generally attracts customers with more user-friendly, efficient, tr

parent, and automated products and services [14].

More specifically, Fintech includes new applications, processes, products, and bus

models in the area of financial services, consisting of one or more financial services, m

or entirely provided over the internet, “simultaneously by various independent serv

providers,typically including at least one licensed bank or insurance company” [15].

Some of the financial services provided may include investment advice (robo-advisi

credit decisions, asset trading, digital currencies, automatic transactions, payment se

crowdfunding, person-to-person transactions (P2P), and smartphone wallets [15].

The current era in the evolution of Fintech is called “Fintech 3.0”, which began

2008,and whose first years were dominated by the global crisis and financial turmo

when there was a loss in trust in the banking system.Then, technological firms began

to operate using peer-to-peer networks outside the regulatory framework (in fact, 2

of these platforms were developed in China) [16] and to apply new technologies in the

financial markets, changing the way of doing business in all financial sectors [17]. This

development is ongoing [17], and banks today are being displaced by technological fi

and start-ups at a rapid pace [16]. According to Moro-Visconti, Cruz Rambaud, and López

Pascual, some of the reasons for this rapid evolution of Fintech are the sharing and cir

economy, favorable regulation, and information technology [14].

Initially, the largest Fintech market was developed in the US, followed by the U

(the most important Fintech market in Europe) [18]. The European and American Fintech

properties and background differ from the Asian Fintech, which specifically offers solu

for a lack of existing banking infrastructure [19].

Establishing Fintech is easier in well-developed economies, because the infrastruc

and market regulations are there already. This infrastructure and affordable technolog

critical to creating sustainable, unique financial innovation, although Fintech developm

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sustainability 2021, 13, 7012 4 of 19

often occurs in economies where access to loans is more difficult [18]. In fact, “scalability

plays a key role in new financial start-ups, and Fintech’s profits remain quite small

a scalable number of customers has been convinced. This scalability of processes c

achieved by platform creation,which leads to economies of scale and,hence,reduced

costs, and user networks being built” [17]. Additionally, “financial inclusion can positively

affect the economy in terms of poverty reduction and economic growth, and innovatio

in digital finance can positively influence banks’ performance and profitability” [17,20].

“Fintech’s key advantages are greater control of customers’ personal finance, rapid fin

decision-making, and the ability to make and receive payments within seconds, althou

this results in a trade-off between efficiency and (data) security” [17,20]. Therefore, “from

a regulatory perspective, the greatest challenges are then to ensure both consume

investor protection and to guarantee financial stability” [17].

Fintech “allows performing business transactions from anywhere at any time, wh

gives flexibility to all actors” [13]. Companies that have developed Fintech have more

innovative methods of extending banking services to customers and investors throu

cellphone apps, with increased flexibility and efficiency of financial services, and with

promise of saving time and costs through the use of digital technologies [13]. Furthermore,

Fintech is a key driver “for financial development, inclusion, social stability, and integ

and consequential sustainable development through building an infrastructure for

innovative digital financial ecosystem” [12]. It makes financial services more accessible,

efficient,and affordable for customers and changes the ways of providing traditiona

services, representing the digitization of the financial industry [17].

“Fintech is also regarded as an engine for sustainable economic growth as a ne

industry having different characteristics from the traditional financial industry”. With h

expectations for growth, global Fintech investments have greatly increased. In fact, K

reported that “global investment in Fintech has doubled more than six times, from $

billion to $111.8 billion between 2013 and 2018” [21].

Moro-Visconti, Cruz Rambaud, and López Pascual state that, “despite the young

of Fintech,many of these firms are experiencing significantly faster growth than the

traditional financial services peers” [14]. In addition,since they belong to a growing

industry and not a mature one, they are slightly more volatile than IT firms and mu

more volatile than traditional, established banks.This higher volatility was reflected in

March 2020 in a much steeper fall than banks,followed by a more sustained recovery,

“incorporating the digital resilience typical of most technological firms”. “Whereas Fint

and technology stocks have fully recovered from the negative peak of 23 March 2020,

(as of 30 June 2020) were still some 25% below their pre-COVID-19 prices” [14].

Experts claim that “Fintech has the potential to disrupt and transform the finan

sector by making it more transparent, secure, and less expensive” [15], as financial products

traditionally offered by licensed credit institutions (payment services and loans, am

others) are now also offered by Fintech.It supports a greater diversity of products and

providers, and offers improved risk management, with its ability to obtain instant custo

feedback and use it to power real-time adjustments in the services offered [14].

However, for the last decade, large financial institutions have increased their inte

along with investments, in Fintech innovations, to the point that, in 2019, most compet

financial institutions considered Fintech to be their major investment [15]. Both operate

in the same (financial) market and sometimes share customers [14]. In fact, it is expected

that financial institutions will be able to reduce their costs and increase customer incl

with the help of Fintech,leading to an increase in profits.Thus,Moro-Visconti,Cruz

Rambaud,and López Pascual also believe that Fintech will “disrupt and reshape the

financial industry by cutting costs, improving the quality of financial services, and crea

a more diverse and more stable financial landscape” [14]. It will also lead to greater access

to finance and investment, which offers great potential to transform not only finance

economies and societies, in general, through financial inclusion and sustainable, bala

development [14].

often occurs in economies where access to loans is more difficult [18]. In fact, “scalability

plays a key role in new financial start-ups, and Fintech’s profits remain quite small

a scalable number of customers has been convinced. This scalability of processes c

achieved by platform creation,which leads to economies of scale and,hence,reduced

costs, and user networks being built” [17]. Additionally, “financial inclusion can positively

affect the economy in terms of poverty reduction and economic growth, and innovatio

in digital finance can positively influence banks’ performance and profitability” [17,20].

“Fintech’s key advantages are greater control of customers’ personal finance, rapid fin

decision-making, and the ability to make and receive payments within seconds, althou

this results in a trade-off between efficiency and (data) security” [17,20]. Therefore, “from

a regulatory perspective, the greatest challenges are then to ensure both consume

investor protection and to guarantee financial stability” [17].

Fintech “allows performing business transactions from anywhere at any time, wh

gives flexibility to all actors” [13]. Companies that have developed Fintech have more

innovative methods of extending banking services to customers and investors throu

cellphone apps, with increased flexibility and efficiency of financial services, and with

promise of saving time and costs through the use of digital technologies [13]. Furthermore,

Fintech is a key driver “for financial development, inclusion, social stability, and integ

and consequential sustainable development through building an infrastructure for

innovative digital financial ecosystem” [12]. It makes financial services more accessible,

efficient,and affordable for customers and changes the ways of providing traditiona

services, representing the digitization of the financial industry [17].

“Fintech is also regarded as an engine for sustainable economic growth as a ne

industry having different characteristics from the traditional financial industry”. With h

expectations for growth, global Fintech investments have greatly increased. In fact, K

reported that “global investment in Fintech has doubled more than six times, from $

billion to $111.8 billion between 2013 and 2018” [21].

Moro-Visconti, Cruz Rambaud, and López Pascual state that, “despite the young

of Fintech,many of these firms are experiencing significantly faster growth than the

traditional financial services peers” [14]. In addition,since they belong to a growing

industry and not a mature one, they are slightly more volatile than IT firms and mu

more volatile than traditional, established banks.This higher volatility was reflected in

March 2020 in a much steeper fall than banks,followed by a more sustained recovery,

“incorporating the digital resilience typical of most technological firms”. “Whereas Fint

and technology stocks have fully recovered from the negative peak of 23 March 2020,

(as of 30 June 2020) were still some 25% below their pre-COVID-19 prices” [14].

Experts claim that “Fintech has the potential to disrupt and transform the finan

sector by making it more transparent, secure, and less expensive” [15], as financial products

traditionally offered by licensed credit institutions (payment services and loans, am

others) are now also offered by Fintech.It supports a greater diversity of products and

providers, and offers improved risk management, with its ability to obtain instant custo

feedback and use it to power real-time adjustments in the services offered [14].

However, for the last decade, large financial institutions have increased their inte

along with investments, in Fintech innovations, to the point that, in 2019, most compet

financial institutions considered Fintech to be their major investment [15]. Both operate

in the same (financial) market and sometimes share customers [14]. In fact, it is expected

that financial institutions will be able to reduce their costs and increase customer incl

with the help of Fintech,leading to an increase in profits.Thus,Moro-Visconti,Cruz

Rambaud,and López Pascual also believe that Fintech will “disrupt and reshape the

financial industry by cutting costs, improving the quality of financial services, and crea

a more diverse and more stable financial landscape” [14]. It will also lead to greater access

to finance and investment, which offers great potential to transform not only finance

economies and societies, in general, through financial inclusion and sustainable, bala

development [14].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sustainability 2021, 13, 7012 5 of 19

At present, new sector entrants aim to develop new, more customer-centric and d

itally enabled services and, with key technology evolving “rapidly alongside changi

consumer needs, industry leaders will be forced to compete with start-ups and tech com

nies for the new business models” [15]. Market leaders can benefit from this technological

disruption, since “they have more financial resources and greater economies of sca

introducing new lines of business, compared to competitors”, and the “amount of resou

allocated to R&D&I can increase the agility of market leaders to mitigate damage f

potential external disruptive innovations” [15].

“Fintech’s technological advantage over traditional financial institutions is the

driver of success and competitive advantage. Fintech’s technologies should have a va

added for the customer (“customer-centricity”), and mobile and data-based services

enhance efficiency.Another characteristic of Fintech is its ability to connect people o

services through platforms” [17].

“Nowadays,customers choose the best service from a variety of companies,and

traditional financial institutions increase their investments in external financial star

to stay competitive” [17]. This type of collaboration between Fintech and traditional

institutions can take different forms, such as partnering, outsourcing, or investmen

venture capitalist [17].

Banks have changed their role in funding new financial technology entrepreneu

since they now serve as a major provider of funding for young companies. Thanks to di

technology development, they have shifted from traditional money-lending activitie

become stakeholders in Fintech and, therefore, equity investors [17]. Some authors [17]

recommend “collaboration and trust-based relationships to mutually benefit Fintech a

established banks”, as Fintech “must be operated by experienced founders with a c

vision”,because “investors expect founders to run the business successfully from D

1” [17]. Moro-Visconti, Cruz Rambaud, and López Pascual state that all these ideas ca

summarized by the word “co-opetition”, according to which Fintech and banks are b

able to compete and cooperate [14]. It is frequent practice for banks to internalize Fintech

by buying it, so both “converge towards a common market, with co-opetition strate

that reduce conflicts of interest and other governance concerns. This strategic conver

is also catalyzed by the very fact that banks are digitizing their business models,thus

reducing their atavistic differences” [14].

Fintech is the most cutting-edge technological innovation in the field of finance

though most Fintech is specialized in one market segment, it can create value in ev

field of finance, using different business models, such as: payments, wealth managem

crowdfunding,lending,and capital market business models [17]. They also use vari-

ous tools, such as “cryptocurrencies and blockchain, new digital advisory and tradi

systems, artificial intelligence and machine learning, peer-to-peer lending (P2P), eq

crowdfunding, and mobile payment systems” [22]. Currently, M-banking (mobile banking)

and digital payments are the most popular Fintech solutions, with growing significa

due to contactless pandemic prescriptions [14].

Fintech is quite disruptive because of its great innovations for the financial sys

and other infrastructure, which affect many other areas, such as the economy, societ

the energy sector [22]. Furthermore, Fintech has several effects on social, environmen

and ecologicalbenefits in promoting the use of funds for energy and environmental

projects, as well as the construction of renewable energy and environmental infrastru

“leading to environmental and ecological development by providing cheap and adequ

financing” [22].

To summarize, Fintech offers new ways of doing business in financial markets thro

the implementation of platforms, thanks to “technological implementation, related di

economy business models, and integrated services from different areas”, providing “o

ings beyond the traditional banking boundaries” [17]. Moreover, technology is creating

value in financial services, as costs are being dramatically cut (for instance, branch

At present, new sector entrants aim to develop new, more customer-centric and d

itally enabled services and, with key technology evolving “rapidly alongside changi

consumer needs, industry leaders will be forced to compete with start-ups and tech com

nies for the new business models” [15]. Market leaders can benefit from this technological

disruption, since “they have more financial resources and greater economies of sca

introducing new lines of business, compared to competitors”, and the “amount of resou

allocated to R&D&I can increase the agility of market leaders to mitigate damage f

potential external disruptive innovations” [15].

“Fintech’s technological advantage over traditional financial institutions is the

driver of success and competitive advantage. Fintech’s technologies should have a va

added for the customer (“customer-centricity”), and mobile and data-based services

enhance efficiency.Another characteristic of Fintech is its ability to connect people o

services through platforms” [17].

“Nowadays,customers choose the best service from a variety of companies,and

traditional financial institutions increase their investments in external financial star

to stay competitive” [17]. This type of collaboration between Fintech and traditional

institutions can take different forms, such as partnering, outsourcing, or investmen

venture capitalist [17].

Banks have changed their role in funding new financial technology entrepreneu

since they now serve as a major provider of funding for young companies. Thanks to di

technology development, they have shifted from traditional money-lending activitie

become stakeholders in Fintech and, therefore, equity investors [17]. Some authors [17]

recommend “collaboration and trust-based relationships to mutually benefit Fintech a

established banks”, as Fintech “must be operated by experienced founders with a c

vision”,because “investors expect founders to run the business successfully from D

1” [17]. Moro-Visconti, Cruz Rambaud, and López Pascual state that all these ideas ca

summarized by the word “co-opetition”, according to which Fintech and banks are b

able to compete and cooperate [14]. It is frequent practice for banks to internalize Fintech

by buying it, so both “converge towards a common market, with co-opetition strate

that reduce conflicts of interest and other governance concerns. This strategic conver

is also catalyzed by the very fact that banks are digitizing their business models,thus

reducing their atavistic differences” [14].

Fintech is the most cutting-edge technological innovation in the field of finance

though most Fintech is specialized in one market segment, it can create value in ev

field of finance, using different business models, such as: payments, wealth managem

crowdfunding,lending,and capital market business models [17]. They also use vari-

ous tools, such as “cryptocurrencies and blockchain, new digital advisory and tradi

systems, artificial intelligence and machine learning, peer-to-peer lending (P2P), eq

crowdfunding, and mobile payment systems” [22]. Currently, M-banking (mobile banking)

and digital payments are the most popular Fintech solutions, with growing significa

due to contactless pandemic prescriptions [14].

Fintech is quite disruptive because of its great innovations for the financial sys

and other infrastructure, which affect many other areas, such as the economy, societ

the energy sector [22]. Furthermore, Fintech has several effects on social, environmen

and ecologicalbenefits in promoting the use of funds for energy and environmental

projects, as well as the construction of renewable energy and environmental infrastru

“leading to environmental and ecological development by providing cheap and adequ

financing” [22].

To summarize, Fintech offers new ways of doing business in financial markets thro

the implementation of platforms, thanks to “technological implementation, related di

economy business models, and integrated services from different areas”, providing “o

ings beyond the traditional banking boundaries” [17]. Moreover, technology is creating

value in financial services, as costs are being dramatically cut (for instance, branch

Sustainability 2021, 13, 7012 6 of 19

customers do not need to spend time or energy going to the bank), revenues are increa

because banking is available anytime and anywhere, and transactions are faster [14]

The main purpose of this paper is to research the relationship between Fintech

sustainability, analyzing the particular case of two different Fintech initiatives:“Clarity

AI” [23], a technological platform aimed at aligning financial portfolios with ESG crite

and “Pensumo” [24], which is linked to consumption and savings for pension plans.

Specifically, the effect of greenwashing in Fintech companies and the possibility of

Fintech to promote sustainability will be analyzed, and how “Clarity AI” and “Pensum

can contribute to this goal will be discussed. A set of recommendations and improvem

measures will be proposed for apps related to sustainability, corporate social responsib

(CSR), and greenwashing, all via a literature review and case study approach.

This paper contributes to a global view of the subject by harmonizing theoretic

literature about Fintech,the digital transformation context,and sustainability,as well

as presenting several practical examples that consider sustainable and environmen

concerns. Furthermore, the paper proposes a wide range of improvement measure

emphasizes the importance of consumer protection in the digitization and financial con

The paper is organized as follows: first, the materials and methods used in the rese

will be explained; then, the Fintech and sustainability research results will be analy

paying particular attention to two Fintech platforms (Clarity AI and Pensumo). Propo

for improvement will then be discussed, and conclusions will be drawn.

2. Materials and Methods

This paper will analyze and study the relationship that exists between Fintech

sustainability via a fundamentally theoretical and descriptive methodology, with a rev

of the literature and several current Fintech examples.

To conduct the research,this paper builds upon a number of articles and reports,

selected mainly from SSRN and the Sustainability journal, as is the case with Moro-Vis

R.; Cruz Rambaud, S.; López Pascual, J., Sustainability in FinTechs: An Explanation thr

Business Model Scalability and Market Valuation.Sustainability 2020, 12, 10316.These

authors firmly believe that Fintech plays a key role in the quest for sustainability.

These articles pose several issues related to greenwashing, sustainability, and Fi

from a general perspective, offering examples of currently sustainable Fintech, as se

Table 1.

Two interesting reports from Afi and Spainsif have been used for further introduct

information.

In addition to these academic resources,several Fintech websites were visited for

actual examples, and the sites of Pensumo and Clarity AI were used to provide an in-de

description of Fintech. Other Fintech websites visited are listed in the References sec

(The Pensumo Brochure was a useful tool in describing Fintech).

Table 1. Literature Review.

Section Articles

Introduction

de Freitas Netto, S.V.; Sobral, M.F.F.; Ribeiro, A.R.B.; Soares, G.R.L. Concepts and forms of greenwash

systematic review. Environmental Sciences Europe 2020, 32(19).

Gräuler, M.; Teuteberg, F. Greenwashing in Sustainability Communication—A Quantitative Investigation

Trust-Building Factors. 2014.

Pimonenko, T.; Bilan, Y., Horák, J.; Starchenko, L.; Gajda, W. Green Brand of Companies and Greenwas

under Sustainable Development Goals. Sustainability 2020, 12(4), 1679.

Delmas, M.A.; Burbano, V.C. The Drivers of Greenwashing. California Management Review 2011, 54(1)

Gräuler, M.; Teuteberg, F. Greenwashing in Online Marketing—Investigating Trust-Building Factors Influe

Greenwashing Detection. 2014.

Badía, G.; Cortez, M.C.; Ferruz, L. Socially responsible investing worldwide: Do markets value corporate

responsibility? Corporate Social Responsibility and Environmental Management 2020, 27, 2751–2

Badía, G.; Ferruz, L.; Cortez, M.C. The performance of socially responsible investing from retail investo

perspective: international evidence. International Journal of Finance & Economics 2020.

customers do not need to spend time or energy going to the bank), revenues are increa

because banking is available anytime and anywhere, and transactions are faster [14]

The main purpose of this paper is to research the relationship between Fintech

sustainability, analyzing the particular case of two different Fintech initiatives:“Clarity

AI” [23], a technological platform aimed at aligning financial portfolios with ESG crite

and “Pensumo” [24], which is linked to consumption and savings for pension plans.

Specifically, the effect of greenwashing in Fintech companies and the possibility of

Fintech to promote sustainability will be analyzed, and how “Clarity AI” and “Pensum

can contribute to this goal will be discussed. A set of recommendations and improvem

measures will be proposed for apps related to sustainability, corporate social responsib

(CSR), and greenwashing, all via a literature review and case study approach.

This paper contributes to a global view of the subject by harmonizing theoretic

literature about Fintech,the digital transformation context,and sustainability,as well

as presenting several practical examples that consider sustainable and environmen

concerns. Furthermore, the paper proposes a wide range of improvement measure

emphasizes the importance of consumer protection in the digitization and financial con

The paper is organized as follows: first, the materials and methods used in the rese

will be explained; then, the Fintech and sustainability research results will be analy

paying particular attention to two Fintech platforms (Clarity AI and Pensumo). Propo

for improvement will then be discussed, and conclusions will be drawn.

2. Materials and Methods

This paper will analyze and study the relationship that exists between Fintech

sustainability via a fundamentally theoretical and descriptive methodology, with a rev

of the literature and several current Fintech examples.

To conduct the research,this paper builds upon a number of articles and reports,

selected mainly from SSRN and the Sustainability journal, as is the case with Moro-Vis

R.; Cruz Rambaud, S.; López Pascual, J., Sustainability in FinTechs: An Explanation thr

Business Model Scalability and Market Valuation.Sustainability 2020, 12, 10316.These

authors firmly believe that Fintech plays a key role in the quest for sustainability.

These articles pose several issues related to greenwashing, sustainability, and Fi

from a general perspective, offering examples of currently sustainable Fintech, as se

Table 1.

Two interesting reports from Afi and Spainsif have been used for further introduct

information.

In addition to these academic resources,several Fintech websites were visited for

actual examples, and the sites of Pensumo and Clarity AI were used to provide an in-de

description of Fintech. Other Fintech websites visited are listed in the References sec

(The Pensumo Brochure was a useful tool in describing Fintech).

Table 1. Literature Review.

Section Articles

Introduction

de Freitas Netto, S.V.; Sobral, M.F.F.; Ribeiro, A.R.B.; Soares, G.R.L. Concepts and forms of greenwash

systematic review. Environmental Sciences Europe 2020, 32(19).

Gräuler, M.; Teuteberg, F. Greenwashing in Sustainability Communication—A Quantitative Investigation

Trust-Building Factors. 2014.

Pimonenko, T.; Bilan, Y., Horák, J.; Starchenko, L.; Gajda, W. Green Brand of Companies and Greenwas

under Sustainable Development Goals. Sustainability 2020, 12(4), 1679.

Delmas, M.A.; Burbano, V.C. The Drivers of Greenwashing. California Management Review 2011, 54(1)

Gräuler, M.; Teuteberg, F. Greenwashing in Online Marketing—Investigating Trust-Building Factors Influe

Greenwashing Detection. 2014.

Badía, G.; Cortez, M.C.; Ferruz, L. Socially responsible investing worldwide: Do markets value corporate

responsibility? Corporate Social Responsibility and Environmental Management 2020, 27, 2751–2

Badía, G.; Ferruz, L.; Cortez, M.C. The performance of socially responsible investing from retail investo

perspective: international evidence. International Journal of Finance & Economics 2020.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sustainability 2021, 13, 7012 7 of 19

Table 1. Cont.

Section Articles

Results

Zhang-Zhang, Y.; Rohlfer, S.; Rajasekera, J. An Eco-Systematic View of Cross-Sector Fintech: The Case of Al

and Tencent. Sustainability 2020, 12, 8907.

al Hammadi, T.; Nobanee, H. FinTech and Sustainability: A Mini-Review. SSRN Electronic Journal 20

Moro-Visconti, R.; Cruz Rambaud, S.; López Pascual, J. Sustainability in FinTechs: An Explanation throu

Business Model Scalability and Market Valuation. Sustainability 2020, 12, 10316.

Kabulova, J.; Stankeviˇcien˙e, J. Valuation of FinTech Innovation Based on Patent Applications. Sustainability2020,

12, 10158.

Fernandez-Vazquez, S.; Rosillo, R.; de La Fuente, D; Priore, P. Blockchain in FinTech: A Mapping Stud

Sustainability 2019, 11, 6366.

Hommel, K.; Bican, P.M. Digital Entrepreneurship in Finance: Fintechs and Funding Decision Criteria

Sustainability 2020, 12, 8035.

Haddad, C.; Hornuf, L. The emergence of the global Fintech market: Economic and technological determ

Small Business Economics 2019, 53, 81–105.

Arner, D.W.; Barberis, J.; Buckley, R.P. The Evolution of Fintech: A New Post-Crisis Paradigm? Georget

Journal of International Law 2016, 47, 1271–1319.

Ozili, P.K. Impact of digital finance on financial inclusion and stability. Borsa Istanbul Review 2018, 18,

Ryu, H.S.; Ko, K.S. Sustainable Development of Fintech: Focused on Uncertainty and Perceived Quality I

Sustainability 2020, 12, 7669.

Deng, X.; Huang, Z.; Cheng, X. FinTech and Sustainable Development: Evidence from China Based on P2P

Sustainability 2019, 11, 6434.

Alonso, A.; Marqués, J.M. Financial Innovation for a Sustainable Economy. Banco de España Occasional

2019, 1916.

Macchiavello, E.; Siri, M. Sustainable Finance and Fintech: Can Technology Contribute to Achieving

Environmental Goals? A Preliminary Assessment of ‘Green FinTech’. European Banking Institute Workin

2020, 71

Arner, D.W.; Buckley, R.P.; Zetzsche, D.A.; Veidt, R. Sustainability, FinTech and Financial Inclusion. Eur

Banking Institute Working Paper 2019, 41; University of Luxembourg Law Working Paper 2019, 006;

Research Paper 2019, 63; University of Hong Kong Faculty of Law Research Paper 2019, 038; Europea

Organization Law Review (Forthcoming).

Anshari, M.; Almunawar, M.N.; Masri, M.; Hamdan, M. Digital marketplace and FinTech to support agricu

sustainability. Energy Procedia 2019, 156, 234–238.

Leong, C.; Tan, B.; Xiao, X.; Tan, F.T.C.; Sun, Y. Nurturing a FinTech ecosystem: The case of a youth mic

startup in China. International Journal of Information Management 2017, 37(2), 92–97.

Caseiro, N.; Coelho, A. The influence of Business Intelligence capacity, network learning and innovativen

startups performance. Journal of Innovation & Knowledge 2019, 4(3), 139–145.

Crovetto, M. Proyectos Sociales—La Responsabilidad Social Corporativa. Final Degree Dissertation,

Universidad de Barcelona, Barcelona (Spain), June 2017.

Discussion

Macchiavello, E.; Siri, M. Sustainable Finance and Fintech: Can Technology Contribute to Achieving

Environmental Goals? A Preliminary Assessment of ‘Green FinTech’. European Banking Institute Workin

2020, 71.

Moro-Visconti, R.; Cruz Rambaud, S.; López Pascual, J. Sustainability in FinTechs: An Explanation throu

Business Model Scalability and Market Valuation. Sustainability 2020, 12, 10316.

3. Results

3.1. Fintech and Sustainability

In recent years, considerable progress has been made in the areas of both Fintech

sustainability [14]. The financial sector plays a key role in the challenge to mitigate clim

change, one of the primary risks facing our society in the coming decades. In this con

according to Moro-Visconti, Cruz Rambaud, and López Pascual, “sustainability has gro

from a niche preoccupation for business to a mainstream concern” [14], and the financial

sector has the task of financing the investments needed to transform our economy i

more sustainable one [25]. There are various initiatives in the private financial sector aime

at introducing “sustainability” into its decision-making process to “achieve a balance sh

with a smaller carbon footprint and to develop a business strategy aligned with respon

investment principles and international standards” [25]. These new financial services

Table 1. Cont.

Section Articles

Results

Zhang-Zhang, Y.; Rohlfer, S.; Rajasekera, J. An Eco-Systematic View of Cross-Sector Fintech: The Case of Al

and Tencent. Sustainability 2020, 12, 8907.

al Hammadi, T.; Nobanee, H. FinTech and Sustainability: A Mini-Review. SSRN Electronic Journal 20

Moro-Visconti, R.; Cruz Rambaud, S.; López Pascual, J. Sustainability in FinTechs: An Explanation throu

Business Model Scalability and Market Valuation. Sustainability 2020, 12, 10316.

Kabulova, J.; Stankeviˇcien˙e, J. Valuation of FinTech Innovation Based on Patent Applications. Sustainability2020,

12, 10158.

Fernandez-Vazquez, S.; Rosillo, R.; de La Fuente, D; Priore, P. Blockchain in FinTech: A Mapping Stud

Sustainability 2019, 11, 6366.

Hommel, K.; Bican, P.M. Digital Entrepreneurship in Finance: Fintechs and Funding Decision Criteria

Sustainability 2020, 12, 8035.

Haddad, C.; Hornuf, L. The emergence of the global Fintech market: Economic and technological determ

Small Business Economics 2019, 53, 81–105.

Arner, D.W.; Barberis, J.; Buckley, R.P. The Evolution of Fintech: A New Post-Crisis Paradigm? Georget

Journal of International Law 2016, 47, 1271–1319.

Ozili, P.K. Impact of digital finance on financial inclusion and stability. Borsa Istanbul Review 2018, 18,

Ryu, H.S.; Ko, K.S. Sustainable Development of Fintech: Focused on Uncertainty and Perceived Quality I

Sustainability 2020, 12, 7669.

Deng, X.; Huang, Z.; Cheng, X. FinTech and Sustainable Development: Evidence from China Based on P2P

Sustainability 2019, 11, 6434.

Alonso, A.; Marqués, J.M. Financial Innovation for a Sustainable Economy. Banco de España Occasional

2019, 1916.

Macchiavello, E.; Siri, M. Sustainable Finance and Fintech: Can Technology Contribute to Achieving

Environmental Goals? A Preliminary Assessment of ‘Green FinTech’. European Banking Institute Workin

2020, 71

Arner, D.W.; Buckley, R.P.; Zetzsche, D.A.; Veidt, R. Sustainability, FinTech and Financial Inclusion. Eur

Banking Institute Working Paper 2019, 41; University of Luxembourg Law Working Paper 2019, 006;

Research Paper 2019, 63; University of Hong Kong Faculty of Law Research Paper 2019, 038; Europea

Organization Law Review (Forthcoming).

Anshari, M.; Almunawar, M.N.; Masri, M.; Hamdan, M. Digital marketplace and FinTech to support agricu

sustainability. Energy Procedia 2019, 156, 234–238.

Leong, C.; Tan, B.; Xiao, X.; Tan, F.T.C.; Sun, Y. Nurturing a FinTech ecosystem: The case of a youth mic

startup in China. International Journal of Information Management 2017, 37(2), 92–97.

Caseiro, N.; Coelho, A. The influence of Business Intelligence capacity, network learning and innovativen

startups performance. Journal of Innovation & Knowledge 2019, 4(3), 139–145.

Crovetto, M. Proyectos Sociales—La Responsabilidad Social Corporativa. Final Degree Dissertation,

Universidad de Barcelona, Barcelona (Spain), June 2017.

Discussion

Macchiavello, E.; Siri, M. Sustainable Finance and Fintech: Can Technology Contribute to Achieving

Environmental Goals? A Preliminary Assessment of ‘Green FinTech’. European Banking Institute Workin

2020, 71.

Moro-Visconti, R.; Cruz Rambaud, S.; López Pascual, J. Sustainability in FinTechs: An Explanation throu

Business Model Scalability and Market Valuation. Sustainability 2020, 12, 10316.

3. Results

3.1. Fintech and Sustainability

In recent years, considerable progress has been made in the areas of both Fintech

sustainability [14]. The financial sector plays a key role in the challenge to mitigate clim

change, one of the primary risks facing our society in the coming decades. In this con

according to Moro-Visconti, Cruz Rambaud, and López Pascual, “sustainability has gro

from a niche preoccupation for business to a mainstream concern” [14], and the financial

sector has the task of financing the investments needed to transform our economy i

more sustainable one [25]. There are various initiatives in the private financial sector aime

at introducing “sustainability” into its decision-making process to “achieve a balance sh

with a smaller carbon footprint and to develop a business strategy aligned with respon

investment principles and international standards” [25]. These new financial services

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sustainability 2021, 13, 7012 8 of 19

relating to sustainability are provided by both traditional suppliers and, above all, Fint

It must be noted that the COVID-19 pandemic has demonstrated the existing link betw

sustainability, finance, and technology, since all countries have been urged to re-thin

traditional models and to rely more heavily on technology and sustainability [26].

The development of new technologies has transformed the financial sector, and cli

risk management is an important part of this transformation. Furthermore, sustainab

criteria may play an important role in all these changes. Certain initiatives are being in

ingly used, such as applications that employ artificial intelligence techniques to mo

the sustainability metrics cited in firms’ annual reports and financial statements [25]

Although technology is not often associated with environmental goals, Fintech sho

coherence and continuity with the ESG world, aimed at a “more inclusive, ESG-resil

circular, and environment-friendly financial system supporting sustainable developme

In fact, “the G-20 has included “Sustainable digital finance” as one of its 2030 work-str

and the UN,since 2016,has been studying the link between Fintech and Sustainable

development” [26].

Digital finance and Fintech both play a part in SDG achievement. One of the way

which they do so is by enhancing the allocation of existing financial resources to supp

sustainable development, which occurs through “business models, incentives, policies,

regulations to redirect financial resources globally and in individual countries to prov

SDG-related finance”. Some examples of this process include ESG and socially respon

investment (SRI) and the significant growth of ESG-related financing in the EU, China,

Japan [27].

The authors of [14] state that Fintech “could help accelerate the development of

green and inclusive financial markets and help realign finance to support sustainab

development”, as “it offers the prospect of quickening the integration of the financial s

with the real economy, which will in turn enhance opportunities for greater decentraliz

and increased participation”.

Moreover, the traditional barrier between developed economies and emerging

kets is being lowered thanks to the rapid digitization and development of the Finte

industry. Thus, Moro-Visconti, Cruz Rambaud, and López Pascual state that Fintech

“the potential to mobilize green finance and, for instance, enable poorer people aroun

world to access innovative clean energy projects” [14]. In addition, these authors believe

that Fintech “can unlock greater financial inclusion for new businesses that will de

both impact and financial returns; mobilize domestic savings at scale by providing chan

or platforms for retail investors to access impact investing opportunities; collect, ana

and distribute information on both financial performance and impact performance

better economic decision-making, regulation, and risk management; and provide finan

markets with the level playing-field and market integrity needed for long-term sustaina

investment” [14].

One of the main fields of collaboration between Fintech and sustainable financ

crowdfunding, which involves either individuals or enterprises being provided with

large number of small amounts of money from other users via an online platform. T

green crowdfunding platforms and apps can help environmentally sustainable firms ob

finance and resources in a faster, cheaper, and more affordable way. In addition, these

crowdfunding platforms offer investors the chance to invest their money in sustain

initiatives [26].

Some examples of this are the following: “Abundance” [28] (UK), which allows invest-

ments in renewable energy projects and in generating and selling low-carbon elect

having set up a marketplace where users can buy or sell financial instruments previo

issued on the platform; “Ecomill” [29] (Italy), which promotes online equity investments to

low-environmental impact projects and local renovation; and Lendosphere [30] (France),

which provides loans from individuals for enterprises in the renewable energy sector26].

In addition, blockchain technology has great potential in the sustainable finance se

In fact,tokens are usually used to reward contributions to lower carbon emissions o

relating to sustainability are provided by both traditional suppliers and, above all, Fint

It must be noted that the COVID-19 pandemic has demonstrated the existing link betw

sustainability, finance, and technology, since all countries have been urged to re-thin

traditional models and to rely more heavily on technology and sustainability [26].

The development of new technologies has transformed the financial sector, and cli

risk management is an important part of this transformation. Furthermore, sustainab

criteria may play an important role in all these changes. Certain initiatives are being in

ingly used, such as applications that employ artificial intelligence techniques to mo

the sustainability metrics cited in firms’ annual reports and financial statements [25]

Although technology is not often associated with environmental goals, Fintech sho

coherence and continuity with the ESG world, aimed at a “more inclusive, ESG-resil

circular, and environment-friendly financial system supporting sustainable developme

In fact, “the G-20 has included “Sustainable digital finance” as one of its 2030 work-str

and the UN,since 2016,has been studying the link between Fintech and Sustainable

development” [26].

Digital finance and Fintech both play a part in SDG achievement. One of the way

which they do so is by enhancing the allocation of existing financial resources to supp

sustainable development, which occurs through “business models, incentives, policies,

regulations to redirect financial resources globally and in individual countries to prov

SDG-related finance”. Some examples of this process include ESG and socially respon

investment (SRI) and the significant growth of ESG-related financing in the EU, China,

Japan [27].

The authors of [14] state that Fintech “could help accelerate the development of

green and inclusive financial markets and help realign finance to support sustainab

development”, as “it offers the prospect of quickening the integration of the financial s

with the real economy, which will in turn enhance opportunities for greater decentraliz

and increased participation”.

Moreover, the traditional barrier between developed economies and emerging

kets is being lowered thanks to the rapid digitization and development of the Finte

industry. Thus, Moro-Visconti, Cruz Rambaud, and López Pascual state that Fintech

“the potential to mobilize green finance and, for instance, enable poorer people aroun

world to access innovative clean energy projects” [14]. In addition, these authors believe

that Fintech “can unlock greater financial inclusion for new businesses that will de

both impact and financial returns; mobilize domestic savings at scale by providing chan

or platforms for retail investors to access impact investing opportunities; collect, ana

and distribute information on both financial performance and impact performance

better economic decision-making, regulation, and risk management; and provide finan

markets with the level playing-field and market integrity needed for long-term sustaina

investment” [14].

One of the main fields of collaboration between Fintech and sustainable financ

crowdfunding, which involves either individuals or enterprises being provided with

large number of small amounts of money from other users via an online platform. T

green crowdfunding platforms and apps can help environmentally sustainable firms ob

finance and resources in a faster, cheaper, and more affordable way. In addition, these

crowdfunding platforms offer investors the chance to invest their money in sustain

initiatives [26].

Some examples of this are the following: “Abundance” [28] (UK), which allows invest-

ments in renewable energy projects and in generating and selling low-carbon elect

having set up a marketplace where users can buy or sell financial instruments previo

issued on the platform; “Ecomill” [29] (Italy), which promotes online equity investments to

low-environmental impact projects and local renovation; and Lendosphere [30] (France),

which provides loans from individuals for enterprises in the renewable energy sector26].

In addition, blockchain technology has great potential in the sustainable finance se

In fact,tokens are usually used to reward contributions to lower carbon emissions o

Sustainability 2021, 13, 7012 9 of 19

other green behaviors, thus creating incentives for the use of solar panels.For instance,

Drop in the Ocean [31] (Switzerland) is a platform that brings together individuals and

businesses and rewards responsible behavior with a virtual currency, which can be

to buy services or products from participating businesses. Climatrade [32] (Switzerland)

has created a market in carbon credits represented by tokens, which can be used to o

carbon emissions by buying from mitigation projects.Similarly, SolarCoin [33] rewards

solar energy producers with coins that can be exchanged, used in participating busine

or traded in market exchanges; and Power Ledger [34] (Australia) has created a trading

platform based on blockchain technology where residents can trade solar energy [26

Then, artificial intelligence (AI) and big data analytics are used to collect and pro

information on companies and their environmental behavior. For instance, RepRisk35]

(based in Switzerland but with a global reach) uses both artificial intelligence and hu

analysis to translate big data (not only publicly disclosed information but also satel

data), in twenty languages, into research and metrics, evaluating the ESG risks of liste

non-listed companies [26]. Sustainalytics [36] (Netherlands) uses big data and AI for the

cheaper incorporation of ESG considerations into investment decision-making [26]. Other

initiatives are Your SRI [37], which uses traditional financial data, ESG data and carbon

data to automatically determine a fund’s ESG score and its carbon footprint [26], and APG

(Netherlands), which [38] “has scanned more than 10,000 companies in twelve month

for sustainability contributions, while Ecochain [39] software maps the entire life cycle

of companies, including their environmental footprint, allowing the creation of carb

savings certificates digitally” [26].

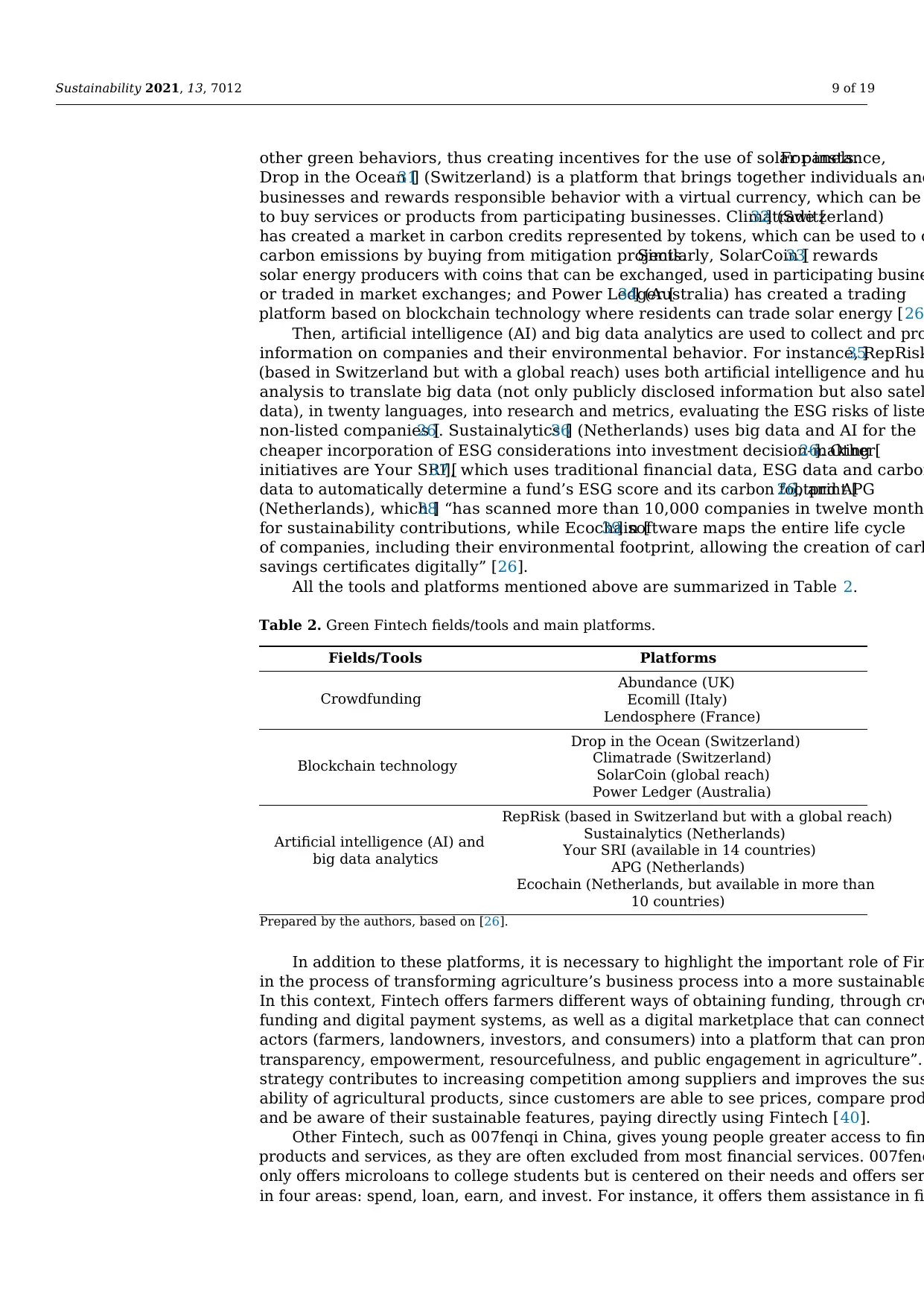

All the tools and platforms mentioned above are summarized in Table 2.

Table 2. Green Fintech fields/tools and main platforms.

Fields/Tools Platforms

Crowdfunding

Abundance (UK)

Ecomill (Italy)

Lendosphere (France)

Blockchain technology

Drop in the Ocean (Switzerland)

Climatrade (Switzerland)

SolarCoin (global reach)

Power Ledger (Australia)

Artificial intelligence (AI) and

big data analytics

RepRisk (based in Switzerland but with a global reach)

Sustainalytics (Netherlands)

Your SRI (available in 14 countries)

APG (Netherlands)

Ecochain (Netherlands, but available in more than

10 countries)

Prepared by the authors, based on [26].

In addition to these platforms, it is necessary to highlight the important role of Fin

in the process of transforming agriculture’s business process into a more sustainable

In this context, Fintech offers farmers different ways of obtaining funding, through cro

funding and digital payment systems, as well as a digital marketplace that can connect

actors (farmers, landowners, investors, and consumers) into a platform that can prom

transparency, empowerment, resourcefulness, and public engagement in agriculture”.

strategy contributes to increasing competition among suppliers and improves the sus

ability of agricultural products, since customers are able to see prices, compare prod

and be aware of their sustainable features, paying directly using Fintech [40].

Other Fintech, such as 007fenqi in China, gives young people greater access to fin

products and services, as they are often excluded from most financial services. 007fenq

only offers microloans to college students but is centered on their needs and offers ser

in four areas: spend, loan, earn, and invest. For instance, it offers them assistance in fi

other green behaviors, thus creating incentives for the use of solar panels.For instance,

Drop in the Ocean [31] (Switzerland) is a platform that brings together individuals and

businesses and rewards responsible behavior with a virtual currency, which can be