FireOut, Inc. Cost Accounting: Product Costing and Decision Making

VerifiedAdded on 2022/08/27

|24

|6292

|59

Homework Assignment

AI Summary

This assignment solution analyzes the cost accounting practices of FireOut, Inc., a manufacturer of fire extinguishers. The solution begins by calculating product costs using traditional costing methods, followed by an activity-based costing (ABC) analysis, including the determination of overhead rates and cost assignments. The assignment then explores break-even analysis, the impact of sales mix changes, and the preparation of CVP income statements for different product lines. Decision-making scenarios are addressed through incremental analysis, including make-or-buy decisions and the evaluation of new equipment purchases. Furthermore, the solution includes a variable-costing income statement and a job-order costing analysis, providing a complete overview of the company's financial performance and cost management strategies.

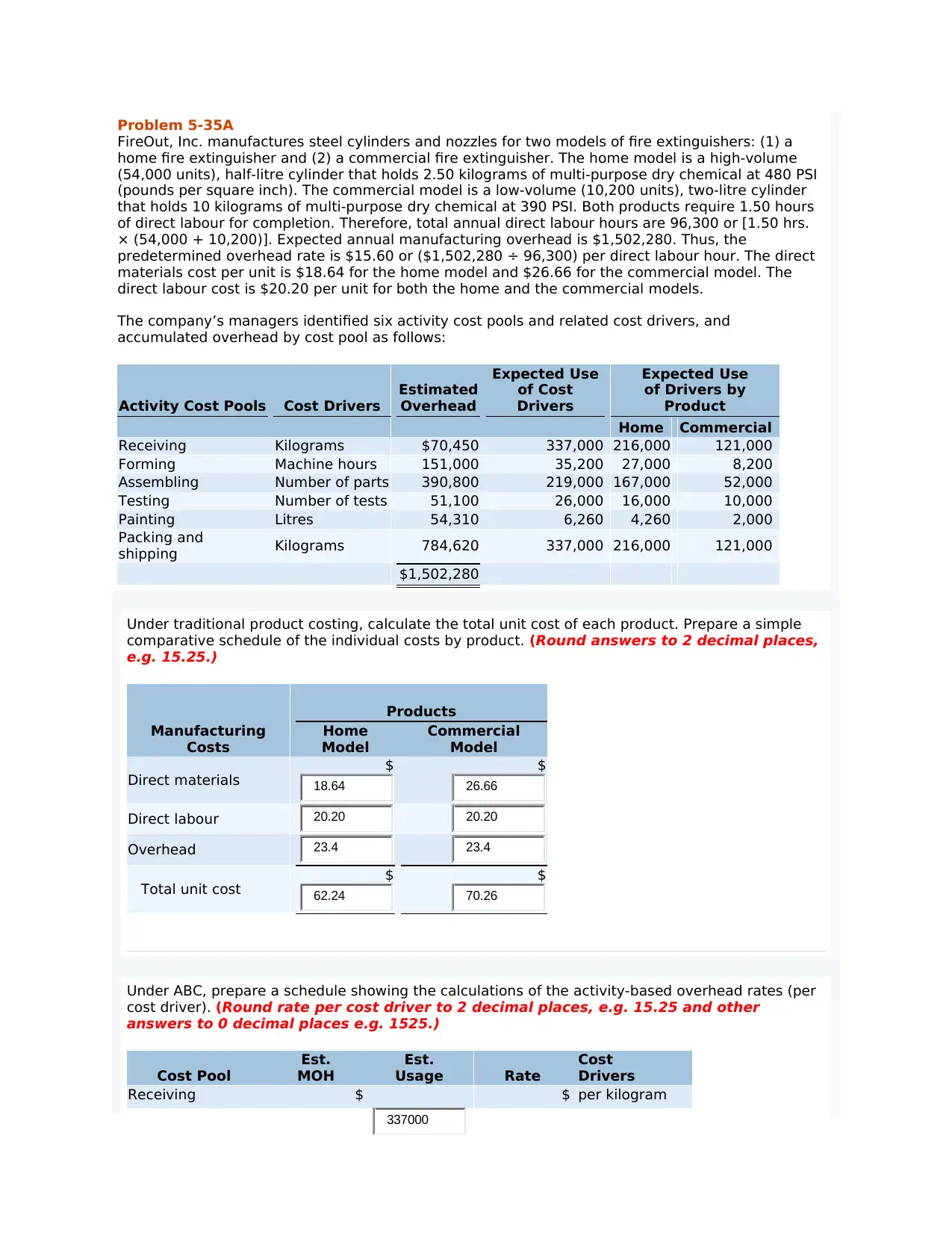

Problem 5-35A

FireOut, Inc. manufactures steel cylinders and nozzles for two models of fire extinguishers: (1) a

home fire extinguisher and (2) a commercial fire extinguisher. The home model is a high-volume

(54,000 units), half-litre cylinder that holds 2.50 kilograms of multi-purpose dry chemical at 480 PSI

(pounds per square inch). The commercial model is a low-volume (10,200 units), two-litre cylinder

that holds 10 kilograms of multi-purpose dry chemical at 390 PSI. Both products require 1.50 hours

of direct labour for completion. Therefore, total annual direct labour hours are 96,300 or [1.50 hrs.

× (54,000 + 10,200)]. Expected annual manufacturing overhead is $1,502,280. Thus, the

predetermined overhead rate is $15.60 or ($1,502,280 ÷ 96,300) per direct labour hour. The direct

materials cost per unit is $18.64 for the home model and $26.66 for the commercial model. The

direct labour cost is $20.20 per unit for both the home and the commercial models.

The company’s managers identified six activity cost pools and related cost drivers, and

accumulated overhead by cost pool as follows:

Activity Cost Pools Cost Drivers

Estimated

Overhead

Expected Use

of Cost

Drivers

Expected Use

of Drivers by

Product

Home Commercial

Receiving Kilograms $70,450 337,000 216,000 121,000

Forming Machine hours 151,000 35,200 27,000 8,200

Assembling Number of parts 390,800 219,000 167,000 52,000

Testing Number of tests 51,100 26,000 16,000 10,000

Painting Litres 54,310 6,260 4,260 2,000

Packing and

shipping Kilograms 784,620 337,000 216,000 121,000

$1,502,280

Under traditional product costing, calculate the total unit cost of each product. Prepare a simple

comparative schedule of the individual costs by product. (Round answers to 2 decimal places,

e.g. 15.25.)

Products

Manufacturing

Costs

Home

Model

Commercial

Model

Direct materials

$ $

Direct labour

Overhead

Total unit cost

$ $

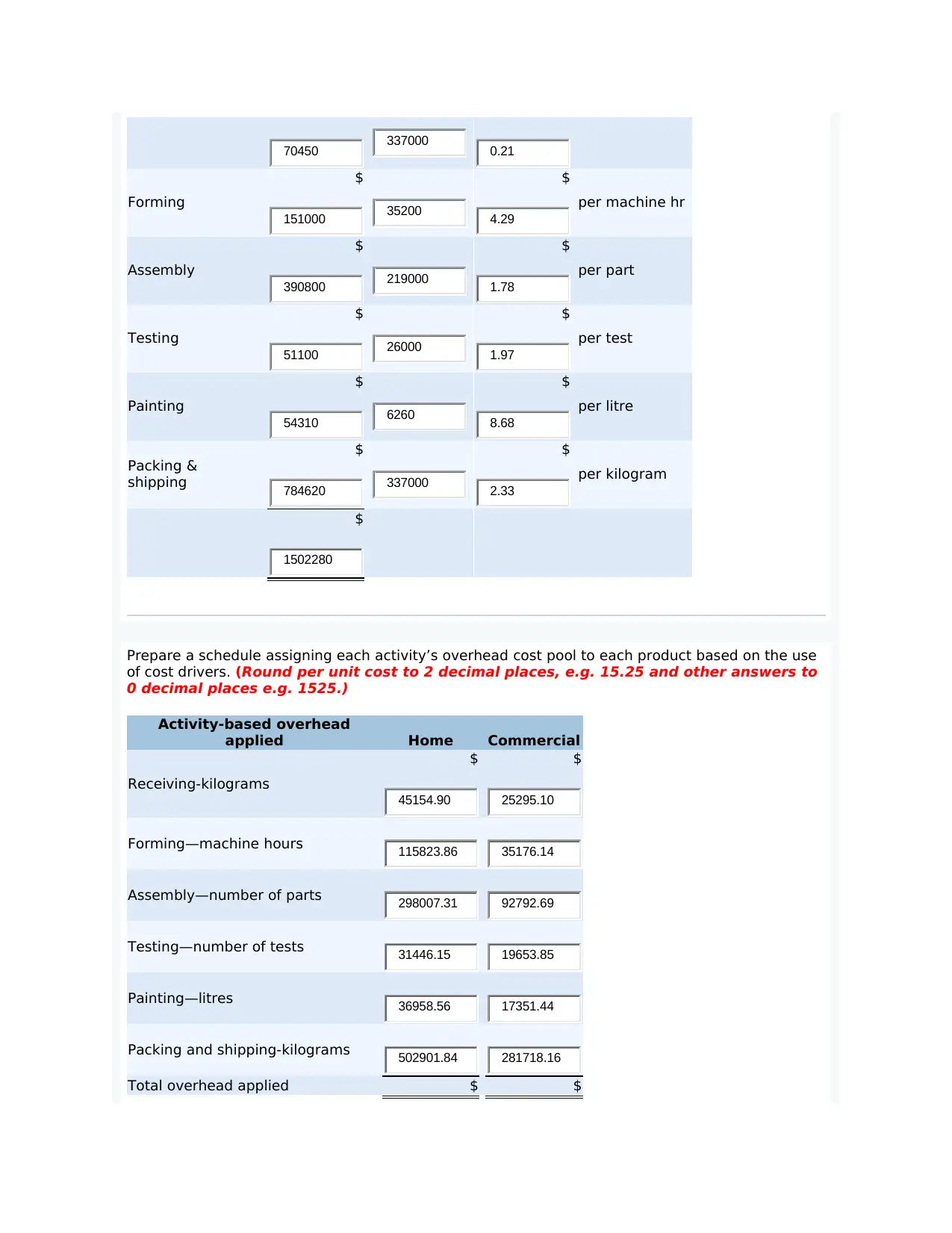

Under ABC, prepare a schedule showing the calculations of the activity-based overhead rates (per

cost driver). (Round rate per cost driver to 2 decimal places, e.g. 15.25 and other

answers to 0 decimal places e.g. 1525.)

Cost Pool

Est.

MOH

Est.

Usage Rate

Cost

Drivers

Receiving $ $ per kilogram

18.64 26.66

20.20 20.20

23.4 23.4

62.24 70.26

337000

FireOut, Inc. manufactures steel cylinders and nozzles for two models of fire extinguishers: (1) a

home fire extinguisher and (2) a commercial fire extinguisher. The home model is a high-volume

(54,000 units), half-litre cylinder that holds 2.50 kilograms of multi-purpose dry chemical at 480 PSI

(pounds per square inch). The commercial model is a low-volume (10,200 units), two-litre cylinder

that holds 10 kilograms of multi-purpose dry chemical at 390 PSI. Both products require 1.50 hours

of direct labour for completion. Therefore, total annual direct labour hours are 96,300 or [1.50 hrs.

× (54,000 + 10,200)]. Expected annual manufacturing overhead is $1,502,280. Thus, the

predetermined overhead rate is $15.60 or ($1,502,280 ÷ 96,300) per direct labour hour. The direct

materials cost per unit is $18.64 for the home model and $26.66 for the commercial model. The

direct labour cost is $20.20 per unit for both the home and the commercial models.

The company’s managers identified six activity cost pools and related cost drivers, and

accumulated overhead by cost pool as follows:

Activity Cost Pools Cost Drivers

Estimated

Overhead

Expected Use

of Cost

Drivers

Expected Use

of Drivers by

Product

Home Commercial

Receiving Kilograms $70,450 337,000 216,000 121,000

Forming Machine hours 151,000 35,200 27,000 8,200

Assembling Number of parts 390,800 219,000 167,000 52,000

Testing Number of tests 51,100 26,000 16,000 10,000

Painting Litres 54,310 6,260 4,260 2,000

Packing and

shipping Kilograms 784,620 337,000 216,000 121,000

$1,502,280

Under traditional product costing, calculate the total unit cost of each product. Prepare a simple

comparative schedule of the individual costs by product. (Round answers to 2 decimal places,

e.g. 15.25.)

Products

Manufacturing

Costs

Home

Model

Commercial

Model

Direct materials

$ $

Direct labour

Overhead

Total unit cost

$ $

Under ABC, prepare a schedule showing the calculations of the activity-based overhead rates (per

cost driver). (Round rate per cost driver to 2 decimal places, e.g. 15.25 and other

answers to 0 decimal places e.g. 1525.)

Cost Pool

Est.

MOH

Est.

Usage Rate

Cost

Drivers

Receiving $ $ per kilogram

18.64 26.66

20.20 20.20

23.4 23.4

62.24 70.26

337000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Forming

$ $

per machine hr

Assembly

$ $

per part

Testing

$ $

per test

Painting

$ $

per litre

Packing &

shipping

$ $

per kilogram

$

Prepare a schedule assigning each activity’s overhead cost pool to each product based on the use

of cost drivers. (Round per unit cost to 2 decimal places, e.g. 15.25 and other answers to

0 decimal places e.g. 1525.)

Activity-based overhead

applied Home Commercial

Receiving-kilograms

$ $

Forming—machine hours

Assembly—number of parts

Testing—number of tests

Painting—litres

Packing and shipping-kilograms

Total overhead applied $ $

70450 337000 0.21

151000 35200 4.29

390800 219000 1.78

51100 26000 1.97

54310 6260 8.68

784620 337000 2.33

1502280

45154.90 25295.10

115823.86 35176.14

298007.31 92792.69

31446.15 19653.85

36958.56 17351.44

502901.84 281718.16

$ $

per machine hr

Assembly

$ $

per part

Testing

$ $

per test

Painting

$ $

per litre

Packing &

shipping

$ $

per kilogram

$

Prepare a schedule assigning each activity’s overhead cost pool to each product based on the use

of cost drivers. (Round per unit cost to 2 decimal places, e.g. 15.25 and other answers to

0 decimal places e.g. 1525.)

Activity-based overhead

applied Home Commercial

Receiving-kilograms

$ $

Forming—machine hours

Assembly—number of parts

Testing—number of tests

Painting—litres

Packing and shipping-kilograms

Total overhead applied $ $

70450 337000 0.21

151000 35200 4.29

390800 219000 1.78

51100 26000 1.97

54310 6260 8.68

784620 337000 2.33

1502280

45154.90 25295.10

115823.86 35176.14

298007.31 92792.69

31446.15 19653.85

36958.56 17351.44

502901.84 281718.16

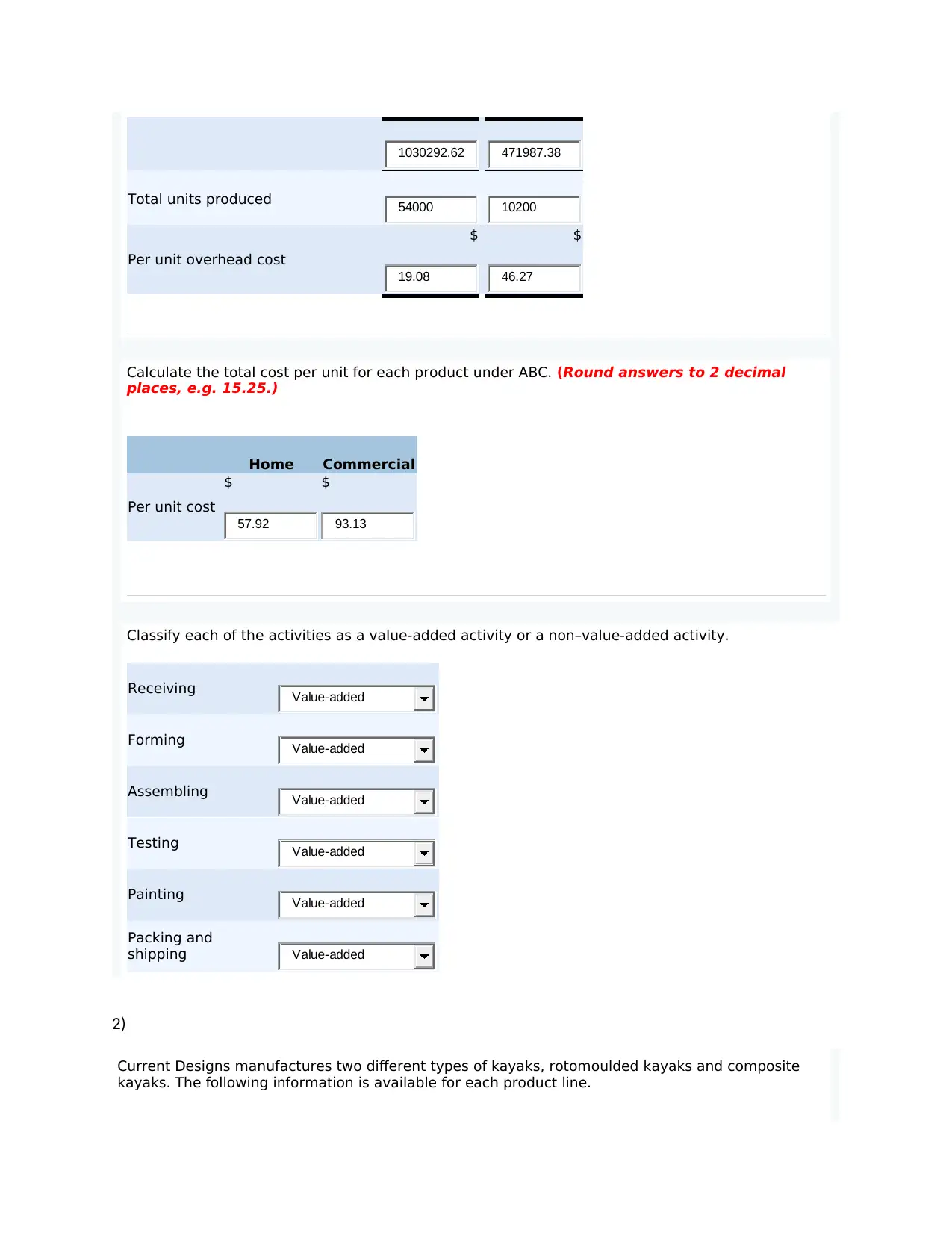

Total units produced

Per unit overhead cost

$ $

Calculate the total cost per unit for each product under ABC. (Round answers to 2 decimal

places, e.g. 15.25.)

Home Commercial

Per unit cost

$ $

Classify each of the activities as a value-added activity or a non–value-added activity.

Receiving

Forming

Assembling

Testing

Painting

Packing and

shipping

2)

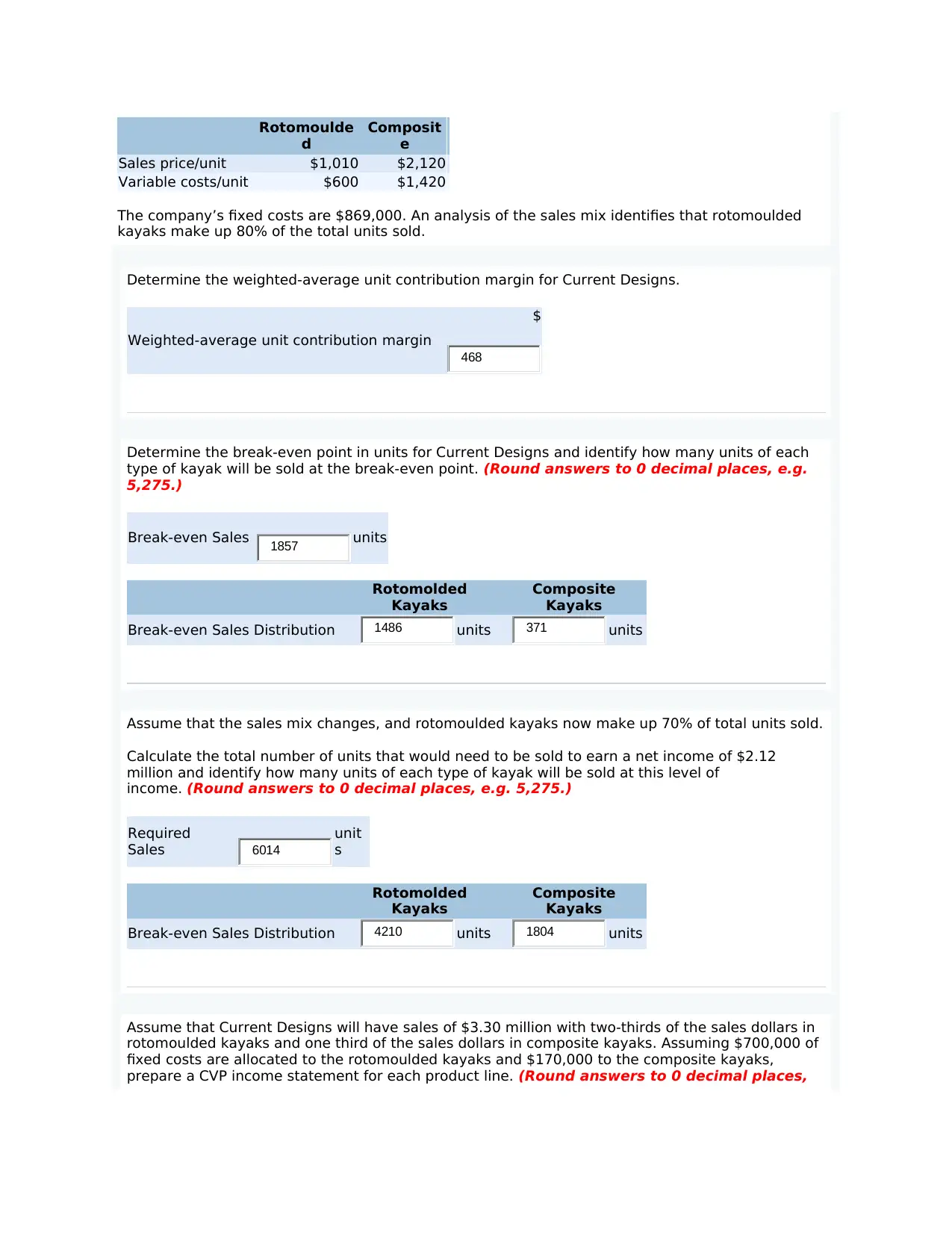

Current Designs manufactures two different types of kayaks, rotomoulded kayaks and composite

kayaks. The following information is available for each product line.

1030292.62 471987.38

54000 10200

19.08 46.27

57.92 93.13

Value-added

Value-added

Value-added

Value-added

Value-added

Value-added

Per unit overhead cost

$ $

Calculate the total cost per unit for each product under ABC. (Round answers to 2 decimal

places, e.g. 15.25.)

Home Commercial

Per unit cost

$ $

Classify each of the activities as a value-added activity or a non–value-added activity.

Receiving

Forming

Assembling

Testing

Painting

Packing and

shipping

2)

Current Designs manufactures two different types of kayaks, rotomoulded kayaks and composite

kayaks. The following information is available for each product line.

1030292.62 471987.38

54000 10200

19.08 46.27

57.92 93.13

Value-added

Value-added

Value-added

Value-added

Value-added

Value-added

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Rotomoulde

d

Composit

e

Sales price/unit $1,010 $2,120

Variable costs/unit $600 $1,420

The company’s fixed costs are $869,000. An analysis of the sales mix identifies that rotomoulded

kayaks make up 80% of the total units sold.

Determine the weighted-average unit contribution margin for Current Designs.

Weighted-average unit contribution margin

$

Determine the break-even point in units for Current Designs and identify how many units of each

type of kayak will be sold at the break-even point. (Round answers to 0 decimal places, e.g.

5,275.)

Break-even Sales units

Rotomolded

Kayaks

Composite

Kayaks

Break-even Sales Distribution units units

Assume that the sales mix changes, and rotomoulded kayaks now make up 70% of total units sold.

Calculate the total number of units that would need to be sold to earn a net income of $2.12

million and identify how many units of each type of kayak will be sold at this level of

income. (Round answers to 0 decimal places, e.g. 5,275.)

Required

Sales

unit

s

Rotomolded

Kayaks

Composite

Kayaks

Break-even Sales Distribution units units

Assume that Current Designs will have sales of $3.30 million with two-thirds of the sales dollars in

rotomoulded kayaks and one third of the sales dollars in composite kayaks. Assuming $700,000 of

fixed costs are allocated to the rotomoulded kayaks and $170,000 to the composite kayaks,

prepare a CVP income statement for each product line. (Round answers to 0 decimal places,

468

1857

1486 371

6014

4210 1804

d

Composit

e

Sales price/unit $1,010 $2,120

Variable costs/unit $600 $1,420

The company’s fixed costs are $869,000. An analysis of the sales mix identifies that rotomoulded

kayaks make up 80% of the total units sold.

Determine the weighted-average unit contribution margin for Current Designs.

Weighted-average unit contribution margin

$

Determine the break-even point in units for Current Designs and identify how many units of each

type of kayak will be sold at the break-even point. (Round answers to 0 decimal places, e.g.

5,275.)

Break-even Sales units

Rotomolded

Kayaks

Composite

Kayaks

Break-even Sales Distribution units units

Assume that the sales mix changes, and rotomoulded kayaks now make up 70% of total units sold.

Calculate the total number of units that would need to be sold to earn a net income of $2.12

million and identify how many units of each type of kayak will be sold at this level of

income. (Round answers to 0 decimal places, e.g. 5,275.)

Required

Sales

unit

s

Rotomolded

Kayaks

Composite

Kayaks

Break-even Sales Distribution units units

Assume that Current Designs will have sales of $3.30 million with two-thirds of the sales dollars in

rotomoulded kayaks and one third of the sales dollars in composite kayaks. Assuming $700,000 of

fixed costs are allocated to the rotomoulded kayaks and $170,000 to the composite kayaks,

prepare a CVP income statement for each product line. (Round answers to 0 decimal places,

468

1857

1486 371

6014

4210 1804

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

e.g. 5,275.)

Rotomolded

Kayaks

Composite

Kayaks

$ $

$ $

Calculate the degree of operating leverage for each product line. (Round answers to 2 decimal

places, e.g. 52.75.)

Rotomolded

Kayaks

Composite

Kayaks

Degree of operating

leverage

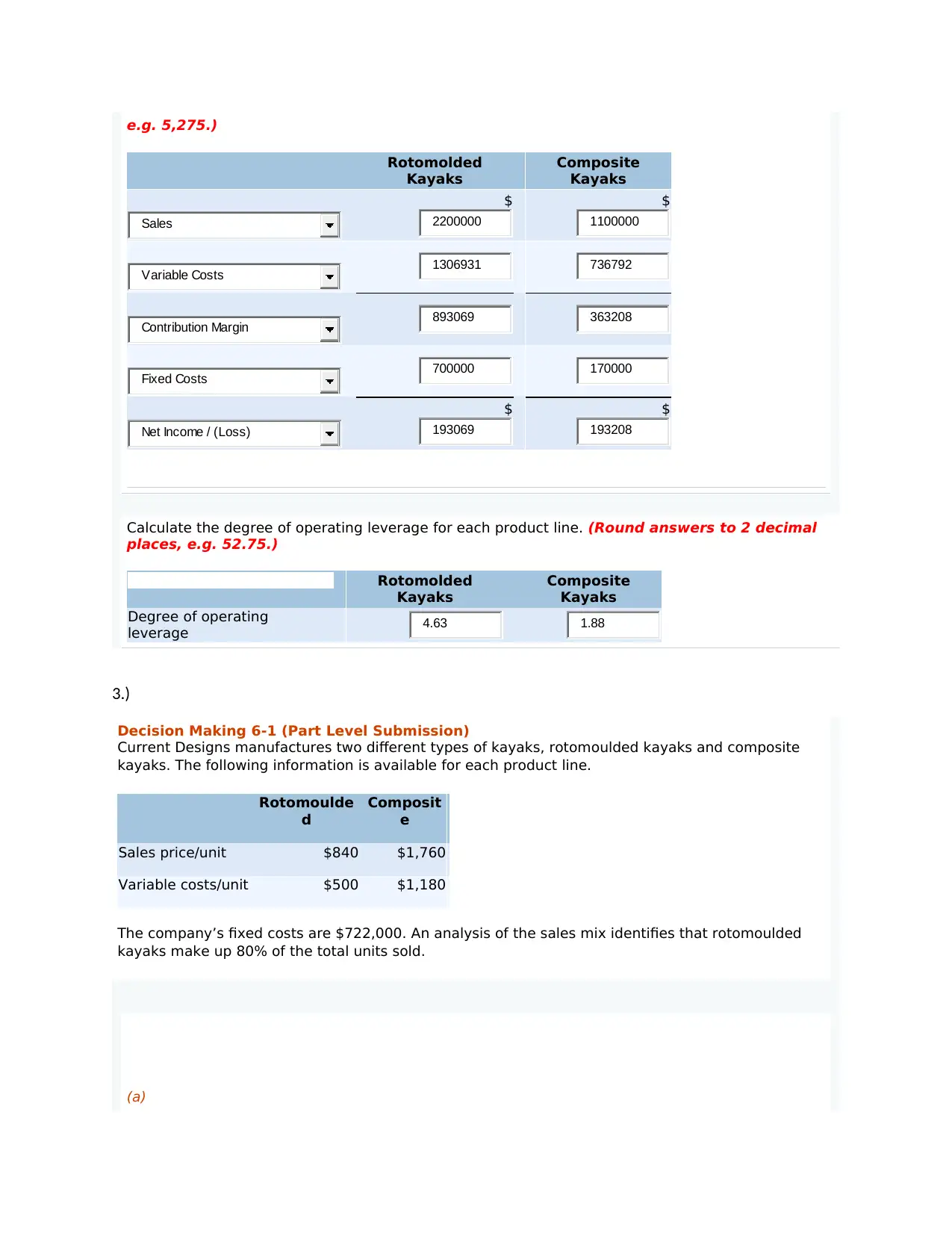

3.)

Decision Making 6-1 (Part Level Submission)

Current Designs manufactures two different types of kayaks, rotomoulded kayaks and composite

kayaks. The following information is available for each product line.

Rotomoulde

d

Composit

e

Sales price/unit $840 $1,760

Variable costs/unit $500 $1,180

The company’s fixed costs are $722,000. An analysis of the sales mix identifies that rotomoulded

kayaks make up 80% of the total units sold.

(a)

Sales 2200000 1100000

Variable Costs 1306931 736792

Contribution Margin 893069 363208

Fixed Costs 700000 170000

Net Income / (Loss) 193069 193208

4.63 1.88

Rotomolded

Kayaks

Composite

Kayaks

$ $

$ $

Calculate the degree of operating leverage for each product line. (Round answers to 2 decimal

places, e.g. 52.75.)

Rotomolded

Kayaks

Composite

Kayaks

Degree of operating

leverage

3.)

Decision Making 6-1 (Part Level Submission)

Current Designs manufactures two different types of kayaks, rotomoulded kayaks and composite

kayaks. The following information is available for each product line.

Rotomoulde

d

Composit

e

Sales price/unit $840 $1,760

Variable costs/unit $500 $1,180

The company’s fixed costs are $722,000. An analysis of the sales mix identifies that rotomoulded

kayaks make up 80% of the total units sold.

(a)

Sales 2200000 1100000

Variable Costs 1306931 736792

Contribution Margin 893069 363208

Fixed Costs 700000 170000

Net Income / (Loss) 193069 193208

4.63 1.88

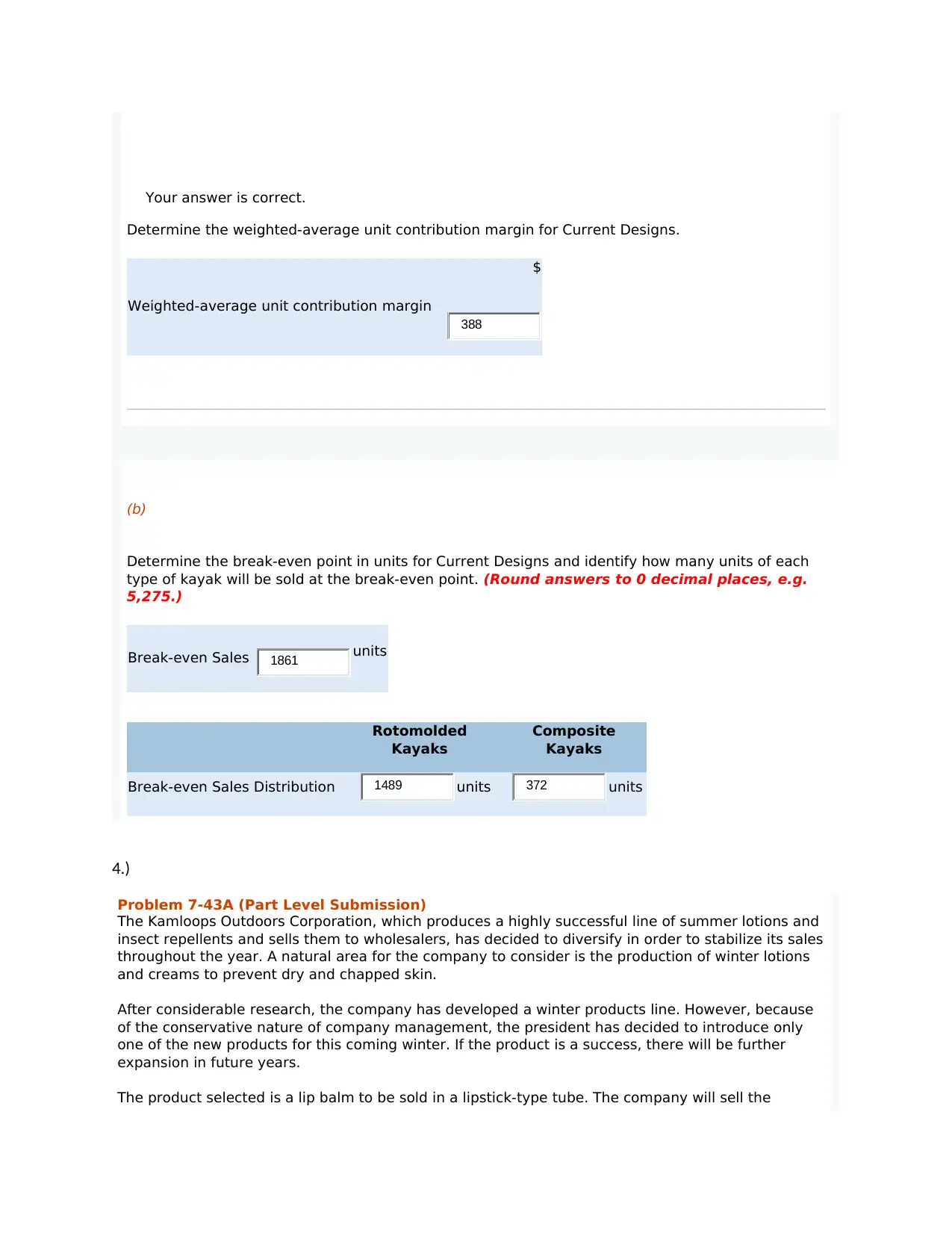

Your answer is correct.

Determine the weighted-average unit contribution margin for Current Designs.

Weighted-average unit contribution margin

$

(b)

Determine the break-even point in units for Current Designs and identify how many units of each

type of kayak will be sold at the break-even point. (Round answers to 0 decimal places, e.g.

5,275.)

Break-even Sales units

Rotomolded

Kayaks

Composite

Kayaks

Break-even Sales Distribution units units

4.)

Problem 7-43A (Part Level Submission)

The Kamloops Outdoors Corporation, which produces a highly successful line of summer lotions and

insect repellents and sells them to wholesalers, has decided to diversify in order to stabilize its sales

throughout the year. A natural area for the company to consider is the production of winter lotions

and creams to prevent dry and chapped skin.

After considerable research, the company has developed a winter products line. However, because

of the conservative nature of company management, the president has decided to introduce only

one of the new products for this coming winter. If the product is a success, there will be further

expansion in future years.

The product selected is a lip balm to be sold in a lipstick-type tube. The company will sell the

388

1861

1489 372

Determine the weighted-average unit contribution margin for Current Designs.

Weighted-average unit contribution margin

$

(b)

Determine the break-even point in units for Current Designs and identify how many units of each

type of kayak will be sold at the break-even point. (Round answers to 0 decimal places, e.g.

5,275.)

Break-even Sales units

Rotomolded

Kayaks

Composite

Kayaks

Break-even Sales Distribution units units

4.)

Problem 7-43A (Part Level Submission)

The Kamloops Outdoors Corporation, which produces a highly successful line of summer lotions and

insect repellents and sells them to wholesalers, has decided to diversify in order to stabilize its sales

throughout the year. A natural area for the company to consider is the production of winter lotions

and creams to prevent dry and chapped skin.

After considerable research, the company has developed a winter products line. However, because

of the conservative nature of company management, the president has decided to introduce only

one of the new products for this coming winter. If the product is a success, there will be further

expansion in future years.

The product selected is a lip balm to be sold in a lipstick-type tube. The company will sell the

388

1861

1489 372

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

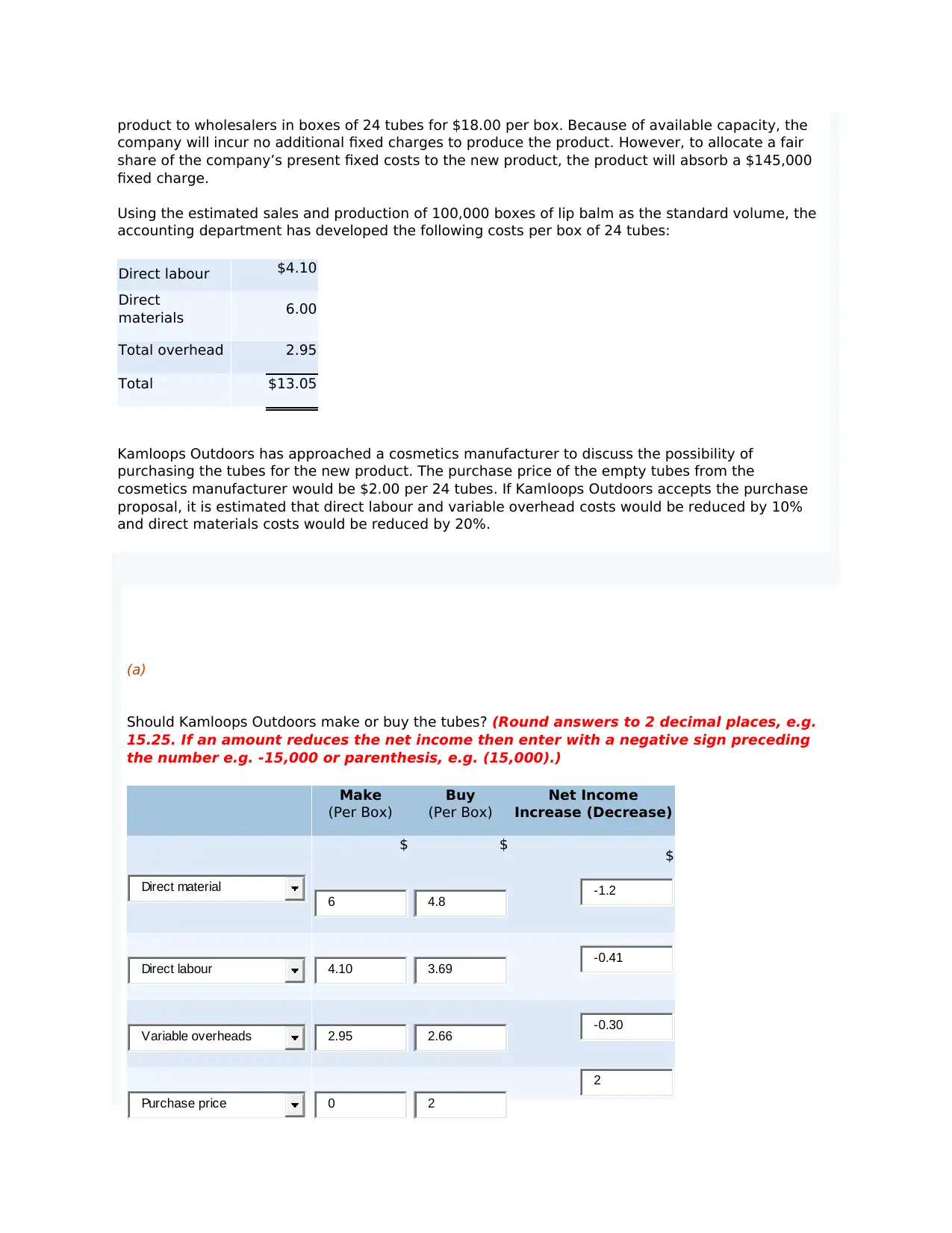

product to wholesalers in boxes of 24 tubes for $18.00 per box. Because of available capacity, the

company will incur no additional fixed charges to produce the product. However, to allocate a fair

share of the company’s present fixed costs to the new product, the product will absorb a $145,000

fixed charge.

Using the estimated sales and production of 100,000 boxes of lip balm as the standard volume, the

accounting department has developed the following costs per box of 24 tubes:

Direct labour $4.10

Direct

materials 6.00

Total overhead 2.95

Total $13.05

Kamloops Outdoors has approached a cosmetics manufacturer to discuss the possibility of

purchasing the tubes for the new product. The purchase price of the empty tubes from the

cosmetics manufacturer would be $2.00 per 24 tubes. If Kamloops Outdoors accepts the purchase

proposal, it is estimated that direct labour and variable overhead costs would be reduced by 10%

and direct materials costs would be reduced by 20%.

(a)

Should Kamloops Outdoors make or buy the tubes? (Round answers to 2 decimal places, e.g.

15.25. If an amount reduces the net income then enter with a negative sign preceding

the number e.g. -15,000 or parenthesis, e.g. (15,000).)

Make

(Per Box)

Buy

(Per Box)

Net Income

Increase (Decrease)

$ $ $

Direct material

6 4.8 -1.2

Direct labour 4.10 3.69 -0.41

Variable overheads 2.95 2.66 -0.30

Purchase price 0 2

2

company will incur no additional fixed charges to produce the product. However, to allocate a fair

share of the company’s present fixed costs to the new product, the product will absorb a $145,000

fixed charge.

Using the estimated sales and production of 100,000 boxes of lip balm as the standard volume, the

accounting department has developed the following costs per box of 24 tubes:

Direct labour $4.10

Direct

materials 6.00

Total overhead 2.95

Total $13.05

Kamloops Outdoors has approached a cosmetics manufacturer to discuss the possibility of

purchasing the tubes for the new product. The purchase price of the empty tubes from the

cosmetics manufacturer would be $2.00 per 24 tubes. If Kamloops Outdoors accepts the purchase

proposal, it is estimated that direct labour and variable overhead costs would be reduced by 10%

and direct materials costs would be reduced by 20%.

(a)

Should Kamloops Outdoors make or buy the tubes? (Round answers to 2 decimal places, e.g.

15.25. If an amount reduces the net income then enter with a negative sign preceding

the number e.g. -15,000 or parenthesis, e.g. (15,000).)

Make

(Per Box)

Buy

(Per Box)

Net Income

Increase (Decrease)

$ $ $

Direct material

6 4.8 -1.2

Direct labour 4.10 3.69 -0.41

Variable overheads 2.95 2.66 -0.30

Purchase price 0 2

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

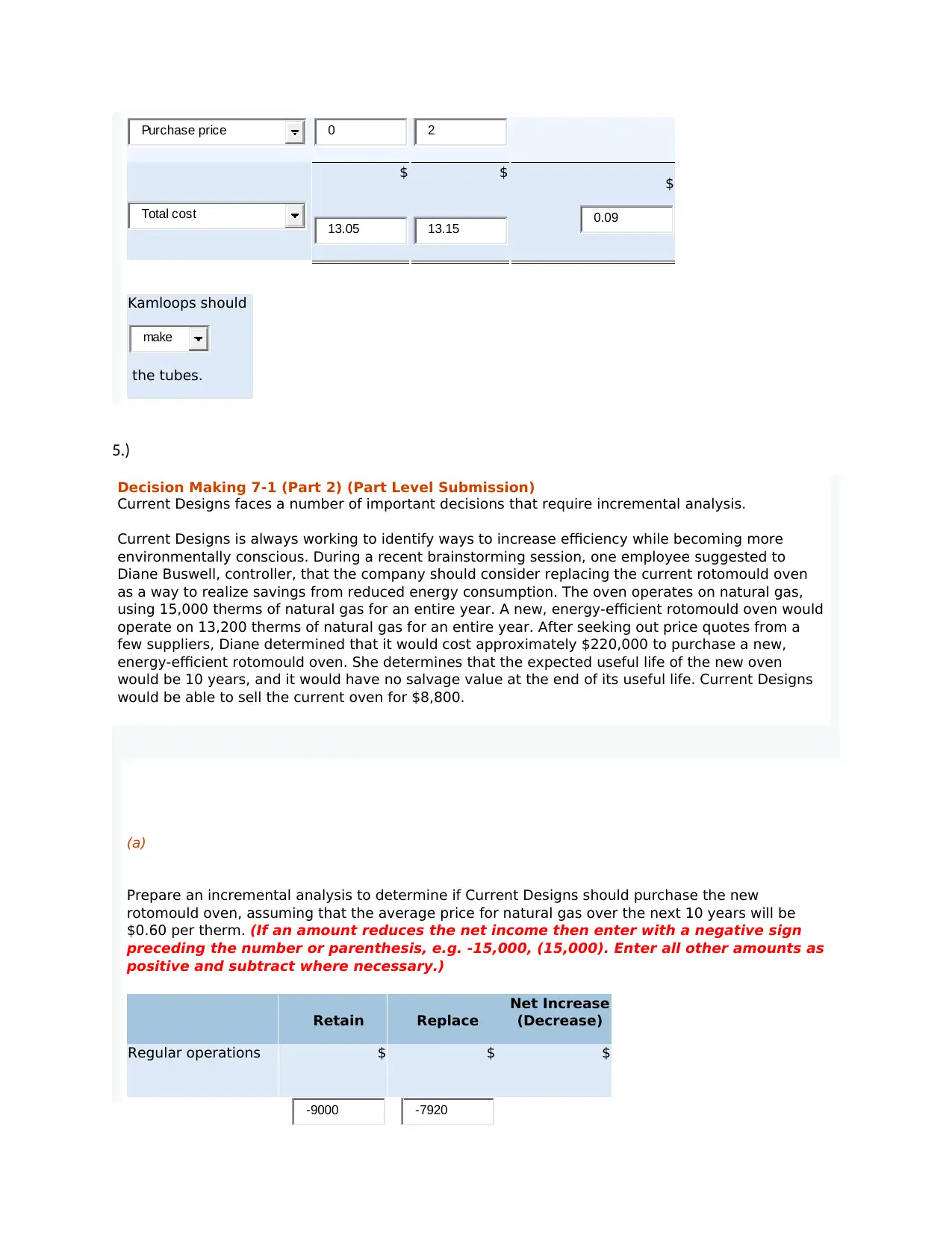

$ $ $

Kamloops should

the tubes.

5.)

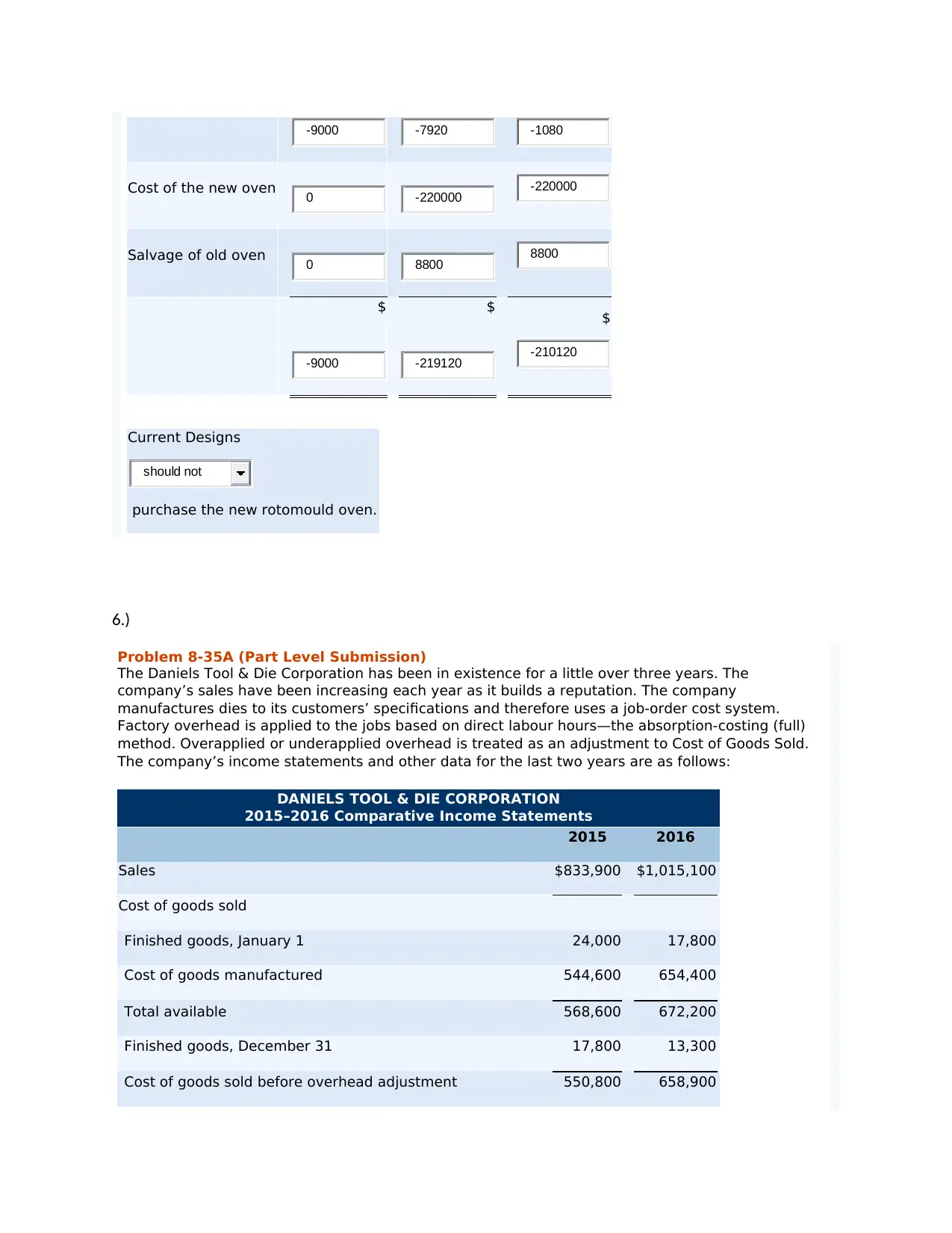

Decision Making 7-1 (Part 2) (Part Level Submission)

Current Designs faces a number of important decisions that require incremental analysis.

Current Designs is always working to identify ways to increase efficiency while becoming more

environmentally conscious. During a recent brainstorming session, one employee suggested to

Diane Buswell, controller, that the company should consider replacing the current rotomould oven

as a way to realize savings from reduced energy consumption. The oven operates on natural gas,

using 15,000 therms of natural gas for an entire year. A new, energy-efficient rotomould oven would

operate on 13,200 therms of natural gas for an entire year. After seeking out price quotes from a

few suppliers, Diane determined that it would cost approximately $220,000 to purchase a new,

energy-efficient rotomould oven. She determines that the expected useful life of the new oven

would be 10 years, and it would have no salvage value at the end of its useful life. Current Designs

would be able to sell the current oven for $8,800.

(a)

Prepare an incremental analysis to determine if Current Designs should purchase the new

rotomould oven, assuming that the average price for natural gas over the next 10 years will be

$0.60 per therm. (If an amount reduces the net income then enter with a negative sign

preceding the number or parenthesis, e.g. -15,000, (15,000). Enter all other amounts as

positive and subtract where necessary.)

Retain Replace

Net Increase

(Decrease)

Regular operations $ $ $

Purchase price 0 2

Total cost

13.05 13.15 0.09

make

-9000 -7920

Kamloops should

the tubes.

5.)

Decision Making 7-1 (Part 2) (Part Level Submission)

Current Designs faces a number of important decisions that require incremental analysis.

Current Designs is always working to identify ways to increase efficiency while becoming more

environmentally conscious. During a recent brainstorming session, one employee suggested to

Diane Buswell, controller, that the company should consider replacing the current rotomould oven

as a way to realize savings from reduced energy consumption. The oven operates on natural gas,

using 15,000 therms of natural gas for an entire year. A new, energy-efficient rotomould oven would

operate on 13,200 therms of natural gas for an entire year. After seeking out price quotes from a

few suppliers, Diane determined that it would cost approximately $220,000 to purchase a new,

energy-efficient rotomould oven. She determines that the expected useful life of the new oven

would be 10 years, and it would have no salvage value at the end of its useful life. Current Designs

would be able to sell the current oven for $8,800.

(a)

Prepare an incremental analysis to determine if Current Designs should purchase the new

rotomould oven, assuming that the average price for natural gas over the next 10 years will be

$0.60 per therm. (If an amount reduces the net income then enter with a negative sign

preceding the number or parenthesis, e.g. -15,000, (15,000). Enter all other amounts as

positive and subtract where necessary.)

Retain Replace

Net Increase

(Decrease)

Regular operations $ $ $

Purchase price 0 2

Total cost

13.05 13.15 0.09

make

-9000 -7920

Cost of the new oven

Salvage of old oven

$ $ $

Current Designs

purchase the new rotomould oven.

6.)

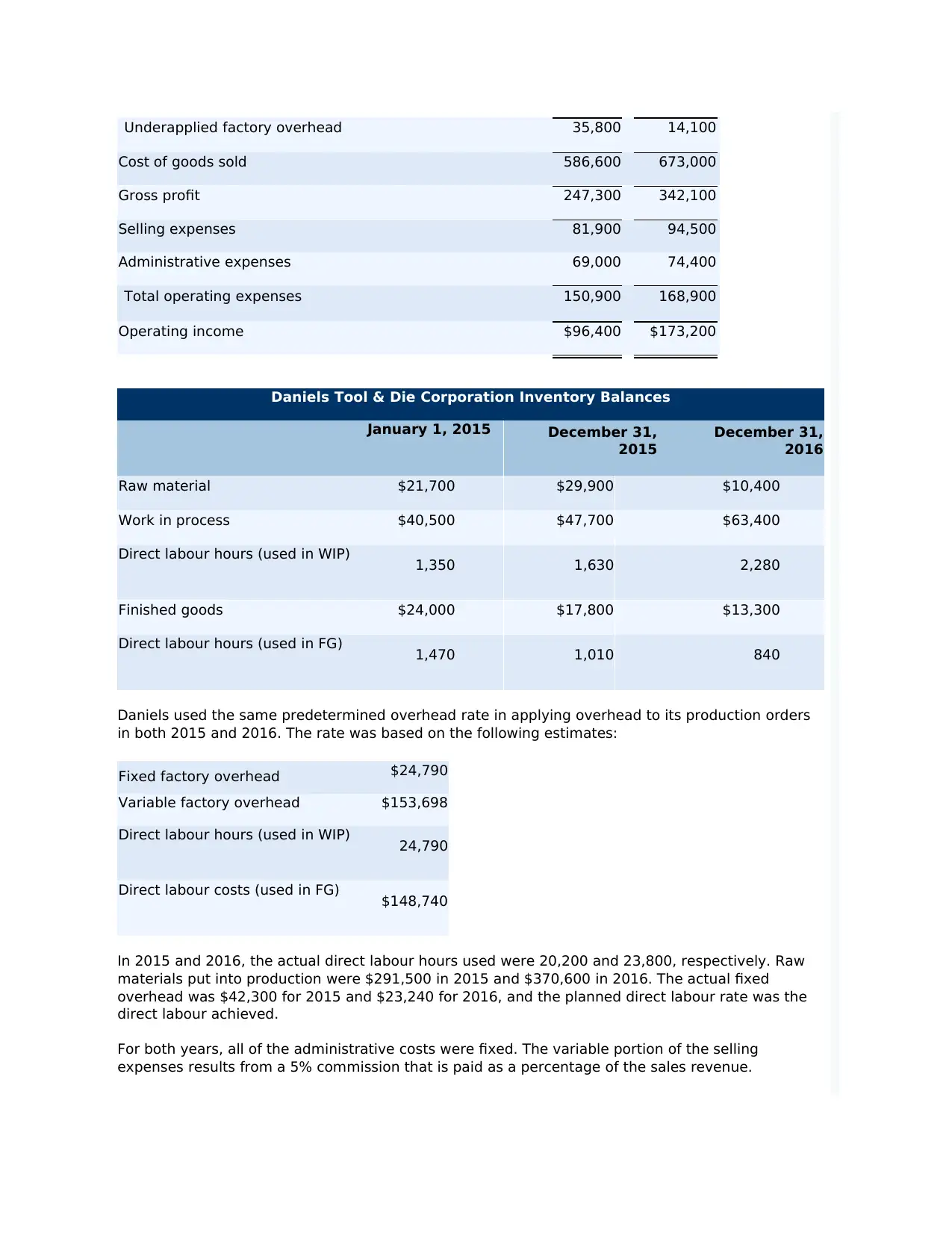

Problem 8-35A (Part Level Submission)

The Daniels Tool & Die Corporation has been in existence for a little over three years. The

company’s sales have been increasing each year as it builds a reputation. The company

manufactures dies to its customers’ specifications and therefore uses a job-order cost system.

Factory overhead is applied to the jobs based on direct labour hours—the absorption-costing (full)

method. Overapplied or underapplied overhead is treated as an adjustment to Cost of Goods Sold.

The company’s income statements and other data for the last two years are as follows:

DANIELS TOOL & DIE CORPORATION

2015–2016 Comparative Income Statements

2015 2016

Sales $833,900 $1,015,100

Cost of goods sold

Finished goods, January 1 24,000 17,800

Cost of goods manufactured 544,600 654,400

Total available 568,600 672,200

Finished goods, December 31 17,800 13,300

Cost of goods sold before overhead adjustment 550,800 658,900

-9000 -7920 -1080

0 -220000 -220000

0 8800 8800

-9000 -219120 -210120

should not

Salvage of old oven

$ $ $

Current Designs

purchase the new rotomould oven.

6.)

Problem 8-35A (Part Level Submission)

The Daniels Tool & Die Corporation has been in existence for a little over three years. The

company’s sales have been increasing each year as it builds a reputation. The company

manufactures dies to its customers’ specifications and therefore uses a job-order cost system.

Factory overhead is applied to the jobs based on direct labour hours—the absorption-costing (full)

method. Overapplied or underapplied overhead is treated as an adjustment to Cost of Goods Sold.

The company’s income statements and other data for the last two years are as follows:

DANIELS TOOL & DIE CORPORATION

2015–2016 Comparative Income Statements

2015 2016

Sales $833,900 $1,015,100

Cost of goods sold

Finished goods, January 1 24,000 17,800

Cost of goods manufactured 544,600 654,400

Total available 568,600 672,200

Finished goods, December 31 17,800 13,300

Cost of goods sold before overhead adjustment 550,800 658,900

-9000 -7920 -1080

0 -220000 -220000

0 8800 8800

-9000 -219120 -210120

should not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Underapplied factory overhead 35,800 14,100

Cost of goods sold 586,600 673,000

Gross profit 247,300 342,100

Selling expenses 81,900 94,500

Administrative expenses 69,000 74,400

Total operating expenses 150,900 168,900

Operating income $96,400 $173,200

Daniels Tool & Die Corporation Inventory Balances

January 1, 2015 December 31,

2015

December 31,

2016

Raw material $21,700 $29,900 $10,400

Work in process $40,500 $47,700 $63,400

Direct labour hours (used in WIP) 1,350 1,630 2,280

Finished goods $24,000 $17,800 $13,300

Direct labour hours (used in FG) 1,470 1,010 840

Daniels used the same predetermined overhead rate in applying overhead to its production orders

in both 2015 and 2016. The rate was based on the following estimates:

Fixed factory overhead $24,790

Variable factory overhead $153,698

Direct labour hours (used in WIP) 24,790

Direct labour costs (used in FG) $148,740

In 2015 and 2016, the actual direct labour hours used were 20,200 and 23,800, respectively. Raw

materials put into production were $291,500 in 2015 and $370,600 in 2016. The actual fixed

overhead was $42,300 for 2015 and $23,240 for 2016, and the planned direct labour rate was the

direct labour achieved.

For both years, all of the administrative costs were fixed. The variable portion of the selling

expenses results from a 5% commission that is paid as a percentage of the sales revenue.

Cost of goods sold 586,600 673,000

Gross profit 247,300 342,100

Selling expenses 81,900 94,500

Administrative expenses 69,000 74,400

Total operating expenses 150,900 168,900

Operating income $96,400 $173,200

Daniels Tool & Die Corporation Inventory Balances

January 1, 2015 December 31,

2015

December 31,

2016

Raw material $21,700 $29,900 $10,400

Work in process $40,500 $47,700 $63,400

Direct labour hours (used in WIP) 1,350 1,630 2,280

Finished goods $24,000 $17,800 $13,300

Direct labour hours (used in FG) 1,470 1,010 840

Daniels used the same predetermined overhead rate in applying overhead to its production orders

in both 2015 and 2016. The rate was based on the following estimates:

Fixed factory overhead $24,790

Variable factory overhead $153,698

Direct labour hours (used in WIP) 24,790

Direct labour costs (used in FG) $148,740

In 2015 and 2016, the actual direct labour hours used were 20,200 and 23,800, respectively. Raw

materials put into production were $291,500 in 2015 and $370,600 in 2016. The actual fixed

overhead was $42,300 for 2015 and $23,240 for 2016, and the planned direct labour rate was the

direct labour achieved.

For both years, all of the administrative costs were fixed. The variable portion of the selling

expenses results from a 5% commission that is paid as a percentage of the sales revenue.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

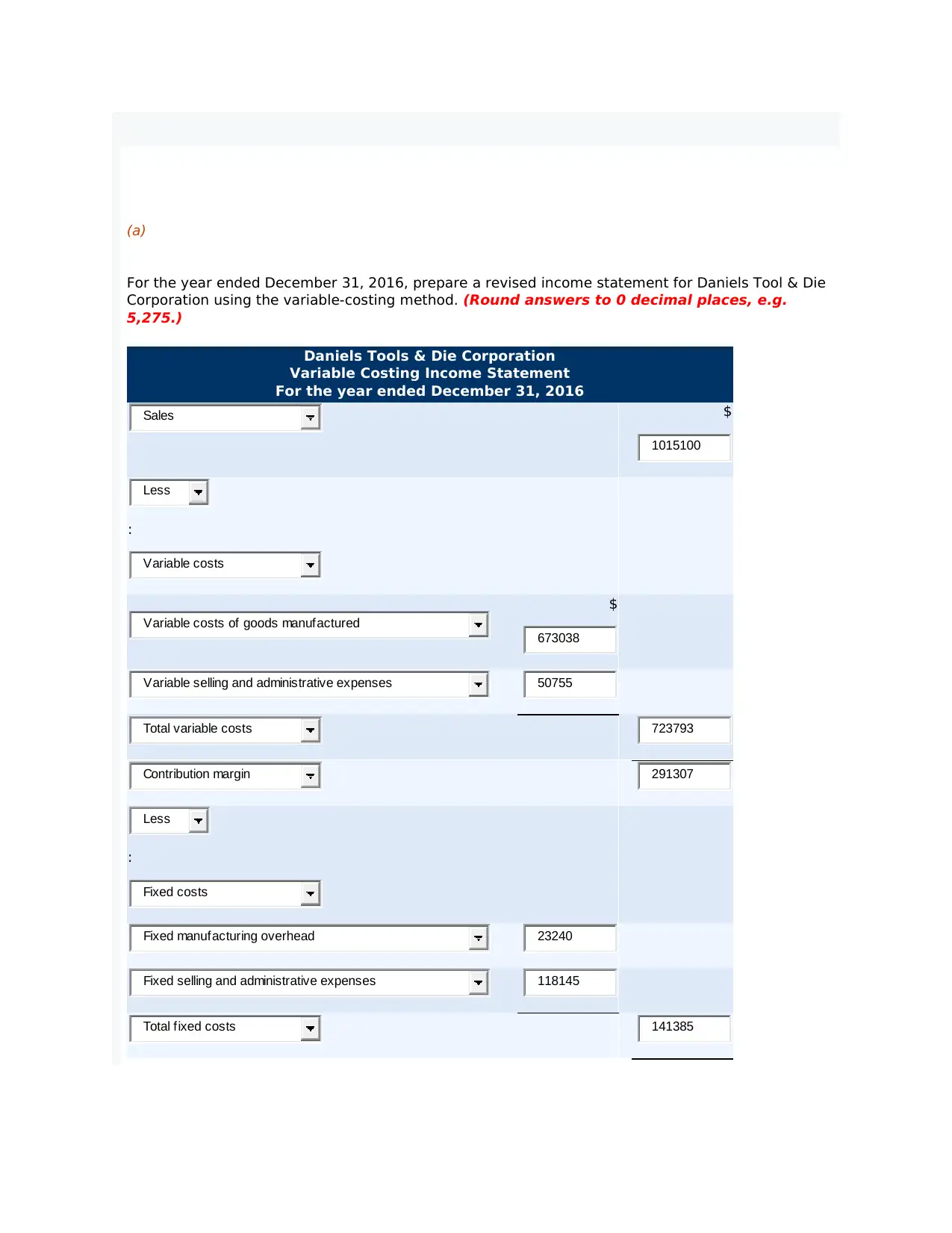

(a)

For the year ended December 31, 2016, prepare a revised income statement for Daniels Tool & Die

Corporation using the variable-costing method. (Round answers to 0 decimal places, e.g.

5,275.)

Daniels Tools & Die Corporation

Variable Costing Income Statement

For the year ended December 31, 2016

$

:

$

:

Sales

1015100

Less

Variable costs

Variable costs of goods manufactured

673038

Variable selling and administrative expenses 50755

Total variable costs 723793

Contribution margin 291307

Less

Fixed costs

Fixed manufacturing overhead 23240

Fixed selling and administrative expenses 118145

Total fixed costs 141385

For the year ended December 31, 2016, prepare a revised income statement for Daniels Tool & Die

Corporation using the variable-costing method. (Round answers to 0 decimal places, e.g.

5,275.)

Daniels Tools & Die Corporation

Variable Costing Income Statement

For the year ended December 31, 2016

$

:

$

:

Sales

1015100

Less

Variable costs

Variable costs of goods manufactured

673038

Variable selling and administrative expenses 50755

Total variable costs 723793

Contribution margin 291307

Less

Fixed costs

Fixed manufacturing overhead 23240

Fixed selling and administrative expenses 118145

Total fixed costs 141385

$

7.)

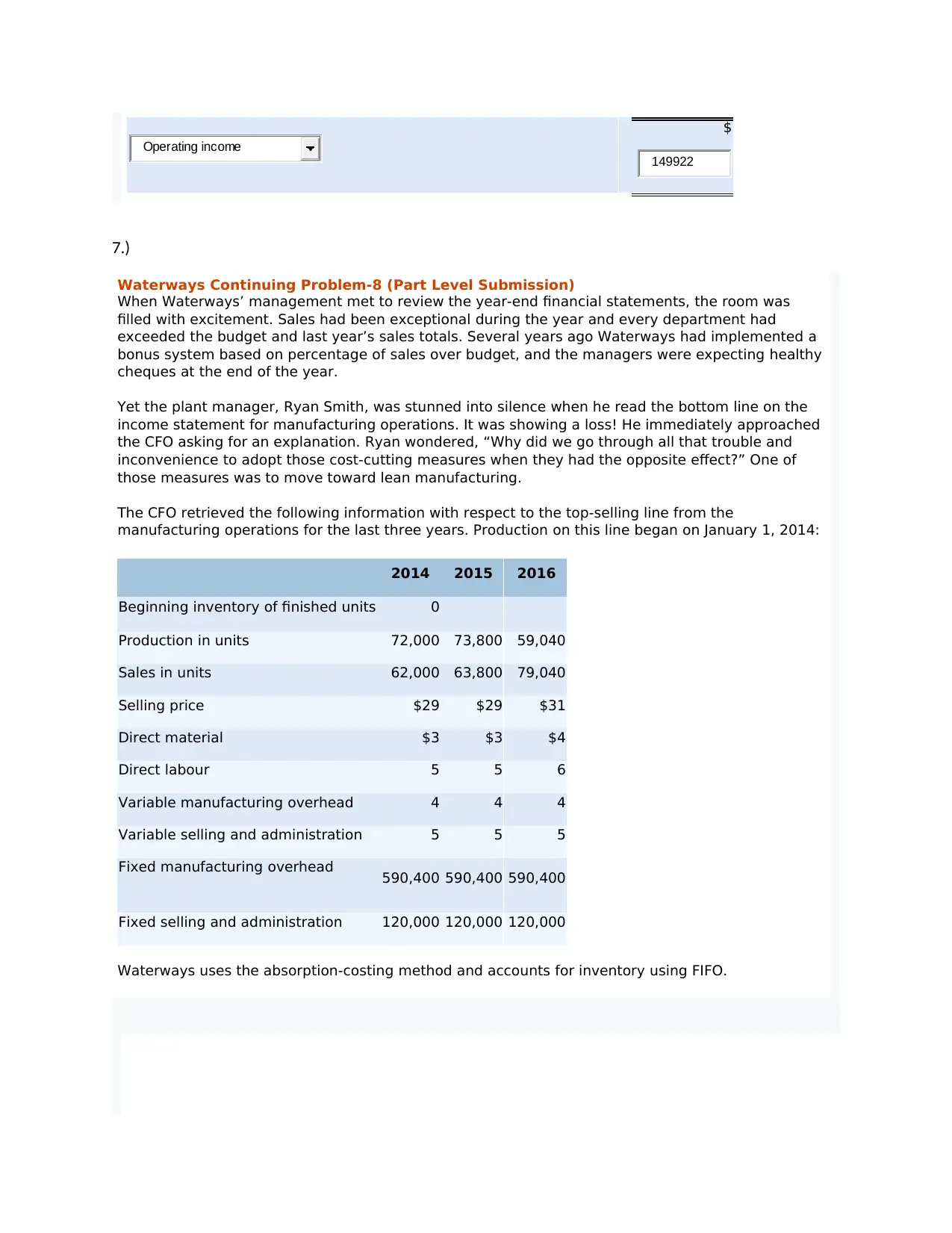

Waterways Continuing Problem-8 (Part Level Submission)

When Waterways’ management met to review the year-end financial statements, the room was

filled with excitement. Sales had been exceptional during the year and every department had

exceeded the budget and last year’s sales totals. Several years ago Waterways had implemented a

bonus system based on percentage of sales over budget, and the managers were expecting healthy

cheques at the end of the year.

Yet the plant manager, Ryan Smith, was stunned into silence when he read the bottom line on the

income statement for manufacturing operations. It was showing a loss! He immediately approached

the CFO asking for an explanation. Ryan wondered, “Why did we go through all that trouble and

inconvenience to adopt those cost-cutting measures when they had the opposite effect?” One of

those measures was to move toward lean manufacturing.

The CFO retrieved the following information with respect to the top-selling line from the

manufacturing operations for the last three years. Production on this line began on January 1, 2014:

2014 2015 2016

Beginning inventory of finished units 0

Production in units 72,000 73,800 59,040

Sales in units 62,000 63,800 79,040

Selling price $29 $29 $31

Direct material $3 $3 $4

Direct labour 5 5 6

Variable manufacturing overhead 4 4 4

Variable selling and administration 5 5 5

Fixed manufacturing overhead 590,400 590,400 590,400

Fixed selling and administration 120,000 120,000 120,000

Waterways uses the absorption-costing method and accounts for inventory using FIFO.

Operating income

149922

7.)

Waterways Continuing Problem-8 (Part Level Submission)

When Waterways’ management met to review the year-end financial statements, the room was

filled with excitement. Sales had been exceptional during the year and every department had

exceeded the budget and last year’s sales totals. Several years ago Waterways had implemented a

bonus system based on percentage of sales over budget, and the managers were expecting healthy

cheques at the end of the year.

Yet the plant manager, Ryan Smith, was stunned into silence when he read the bottom line on the

income statement for manufacturing operations. It was showing a loss! He immediately approached

the CFO asking for an explanation. Ryan wondered, “Why did we go through all that trouble and

inconvenience to adopt those cost-cutting measures when they had the opposite effect?” One of

those measures was to move toward lean manufacturing.

The CFO retrieved the following information with respect to the top-selling line from the

manufacturing operations for the last three years. Production on this line began on January 1, 2014:

2014 2015 2016

Beginning inventory of finished units 0

Production in units 72,000 73,800 59,040

Sales in units 62,000 63,800 79,040

Selling price $29 $29 $31

Direct material $3 $3 $4

Direct labour 5 5 6

Variable manufacturing overhead 4 4 4

Variable selling and administration 5 5 5

Fixed manufacturing overhead 590,400 590,400 590,400

Fixed selling and administration 120,000 120,000 120,000

Waterways uses the absorption-costing method and accounts for inventory using FIFO.

Operating income

149922

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.