Analyzing the Impact of Tax Avoidance on Firm Risk in the UK

VerifiedAdded on 2023/06/07

|19

|5289

|50

Report

AI Summary

This report presents an analysis of the impact of tax avoidance on firm risk within the UK. The study utilizes data from 100 listed companies and employs various statistical tools, including descriptive statistics, correlation analysis, and regression analysis, to examine the relationships between key variables. The findings reveal insights into the effects of GAAP ETR, Cash ETR, BTD, firm size, fixed assets, ROA, debt, leverage, and NOL on Tobin’s Q ratio, a measure of firm value. The analysis suggests that while GAAP ETR and Cash ETR show weak correlations with Tobin’s Q, control variables like firm size and ROA play significant roles. The report concludes with interpretations of the correlations and implications for firm risk management, highlighting how tax avoidance strategies can influence financial performance and overall firm value. The study also discusses the impact of variables like debt and leverage on firm risk.

The effect of tax avoidance on

firm risk in the UK

firm risk in the UK

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

FINDINGS & ANALYSIS..............................................................................................................3

REFERENCES..............................................................................................................................17

Books and Journals....................................................................................................................17

FINDINGS & ANALYSIS..............................................................................................................3

REFERENCES..............................................................................................................................17

Books and Journals....................................................................................................................17

FINDINGS & ANALYSIS

In this chapter, the findings have been presented through the analysis of data pertaining to 100

listed companies. The findings have been obtained through the application of various statistical

tools and tests, which includes the following:

Descriptive statistics: Through descriptive statistics the characteristics or nature of data set have

been determined through generating the summary of the data set so that, better understanding

could be developed for further analysis and identification of relationship among the variables.

Through this statistical tool, the averages have been calculated for each & every variable along

with identification of how data set are deviating from the mean.

Correlation: This statistical tool will be used to determine the degree of relationship existing

among the variables of interest such as GAAP ETR, Cash ETR, BTD, Tobin’s Q ratio (stock

return), firm size, fixed assets, ROA, Debt, Leverage and NOL. This will be done to determine to

what extent does each of the variable can affect the Tobin’s Q ratio of the firm.

Regression: This statistical method will be applied to determine the character and strength of

relationship existing among a single dependent variable (Tobin’s Q ratio) and several other

variables which includes both independent & controlled variables such as Cash ETR, GAAP

ETR, BTD, firm size, etc.

ANOVA test: As the group of data involves more than three variables, the one – way ANOVA

test will be applied to determine whether there is any statistical significance lies between the

independent and dependent variable. In other words, whether independent or controlled variables

either in a group or individually affect the Tobin’s Q of the firm.

Frequencies

Statistics

GAA

P_ET

R

Cash

_ET

R

Tob

in_

Q

Firm

_Siz

e

Fixed

_Asse

ts

R

O

A

Deb

t

Levera

ge

N

O

L

BTD

N Val 100 100 100 100 100 10 100 99 10 100

In this chapter, the findings have been presented through the analysis of data pertaining to 100

listed companies. The findings have been obtained through the application of various statistical

tools and tests, which includes the following:

Descriptive statistics: Through descriptive statistics the characteristics or nature of data set have

been determined through generating the summary of the data set so that, better understanding

could be developed for further analysis and identification of relationship among the variables.

Through this statistical tool, the averages have been calculated for each & every variable along

with identification of how data set are deviating from the mean.

Correlation: This statistical tool will be used to determine the degree of relationship existing

among the variables of interest such as GAAP ETR, Cash ETR, BTD, Tobin’s Q ratio (stock

return), firm size, fixed assets, ROA, Debt, Leverage and NOL. This will be done to determine to

what extent does each of the variable can affect the Tobin’s Q ratio of the firm.

Regression: This statistical method will be applied to determine the character and strength of

relationship existing among a single dependent variable (Tobin’s Q ratio) and several other

variables which includes both independent & controlled variables such as Cash ETR, GAAP

ETR, BTD, firm size, etc.

ANOVA test: As the group of data involves more than three variables, the one – way ANOVA

test will be applied to determine whether there is any statistical significance lies between the

independent and dependent variable. In other words, whether independent or controlled variables

either in a group or individually affect the Tobin’s Q of the firm.

Frequencies

Statistics

GAA

P_ET

R

Cash

_ET

R

Tob

in_

Q

Firm

_Siz

e

Fixed

_Asse

ts

R

O

A

Deb

t

Levera

ge

N

O

L

BTD

N Val 100 100 100 100 100 10 100 99 10 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

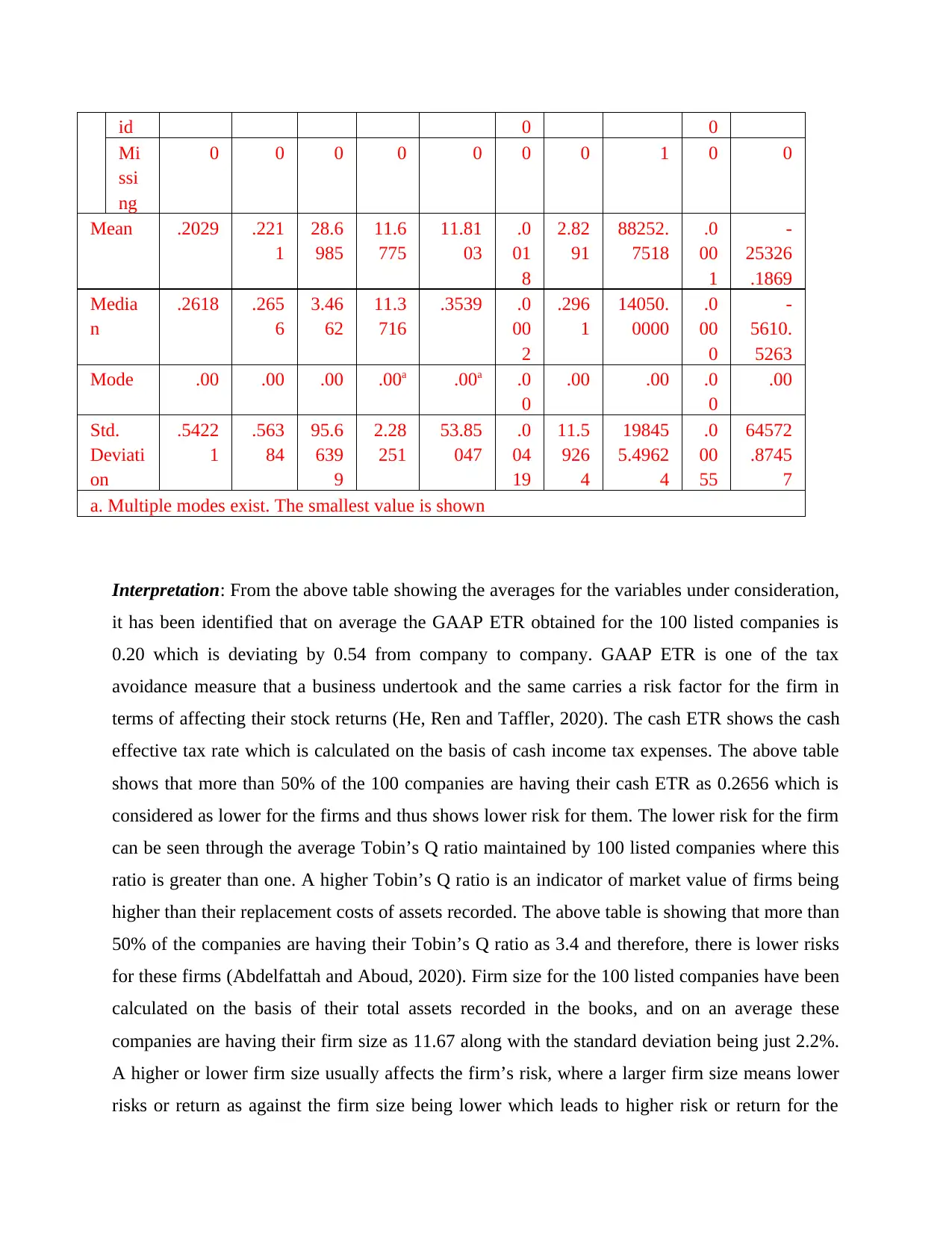

id 0 0

Mi

ssi

ng

0 0 0 0 0 0 0 1 0 0

Mean .2029 .221

1

28.6

985

11.6

775

11.81

03

.0

01

8

2.82

91

88252.

7518

.0

00

1

-

25326

.1869

Media

n

.2618 .265

6

3.46

62

11.3

716

.3539 .0

00

2

.296

1

14050.

0000

.0

00

0

-

5610.

5263

Mode .00 .00 .00 .00a .00a .0

0

.00 .00 .0

0

.00

Std.

Deviati

on

.5422

1

.563

84

95.6

639

9

2.28

251

53.85

047

.0

04

19

11.5

926

4

19845

5.4962

4

.0

00

55

64572

.8745

7

a. Multiple modes exist. The smallest value is shown

Interpretation: From the above table showing the averages for the variables under consideration,

it has been identified that on average the GAAP ETR obtained for the 100 listed companies is

0.20 which is deviating by 0.54 from company to company. GAAP ETR is one of the tax

avoidance measure that a business undertook and the same carries a risk factor for the firm in

terms of affecting their stock returns (He, Ren and Taffler, 2020). The cash ETR shows the cash

effective tax rate which is calculated on the basis of cash income tax expenses. The above table

shows that more than 50% of the 100 companies are having their cash ETR as 0.2656 which is

considered as lower for the firms and thus shows lower risk for them. The lower risk for the firm

can be seen through the average Tobin’s Q ratio maintained by 100 listed companies where this

ratio is greater than one. A higher Tobin’s Q ratio is an indicator of market value of firms being

higher than their replacement costs of assets recorded. The above table is showing that more than

50% of the companies are having their Tobin’s Q ratio as 3.4 and therefore, there is lower risks

for these firms (Abdelfattah and Aboud, 2020). Firm size for the 100 listed companies have been

calculated on the basis of their total assets recorded in the books, and on an average these

companies are having their firm size as 11.67 along with the standard deviation being just 2.2%.

A higher or lower firm size usually affects the firm’s risk, where a larger firm size means lower

risks or return as against the firm size being lower which leads to higher risk or return for the

Mi

ssi

ng

0 0 0 0 0 0 0 1 0 0

Mean .2029 .221

1

28.6

985

11.6

775

11.81

03

.0

01

8

2.82

91

88252.

7518

.0

00

1

-

25326

.1869

Media

n

.2618 .265

6

3.46

62

11.3

716

.3539 .0

00

2

.296

1

14050.

0000

.0

00

0

-

5610.

5263

Mode .00 .00 .00 .00a .00a .0

0

.00 .00 .0

0

.00

Std.

Deviati

on

.5422

1

.563

84

95.6

639

9

2.28

251

53.85

047

.0

04

19

11.5

926

4

19845

5.4962

4

.0

00

55

64572

.8745

7

a. Multiple modes exist. The smallest value is shown

Interpretation: From the above table showing the averages for the variables under consideration,

it has been identified that on average the GAAP ETR obtained for the 100 listed companies is

0.20 which is deviating by 0.54 from company to company. GAAP ETR is one of the tax

avoidance measure that a business undertook and the same carries a risk factor for the firm in

terms of affecting their stock returns (He, Ren and Taffler, 2020). The cash ETR shows the cash

effective tax rate which is calculated on the basis of cash income tax expenses. The above table

shows that more than 50% of the 100 companies are having their cash ETR as 0.2656 which is

considered as lower for the firms and thus shows lower risk for them. The lower risk for the firm

can be seen through the average Tobin’s Q ratio maintained by 100 listed companies where this

ratio is greater than one. A higher Tobin’s Q ratio is an indicator of market value of firms being

higher than their replacement costs of assets recorded. The above table is showing that more than

50% of the companies are having their Tobin’s Q ratio as 3.4 and therefore, there is lower risks

for these firms (Abdelfattah and Aboud, 2020). Firm size for the 100 listed companies have been

calculated on the basis of their total assets recorded in the books, and on an average these

companies are having their firm size as 11.67 along with the standard deviation being just 2.2%.

A higher or lower firm size usually affects the firm’s risk, where a larger firm size means lower

risks or return as against the firm size being lower which leads to higher risk or return for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

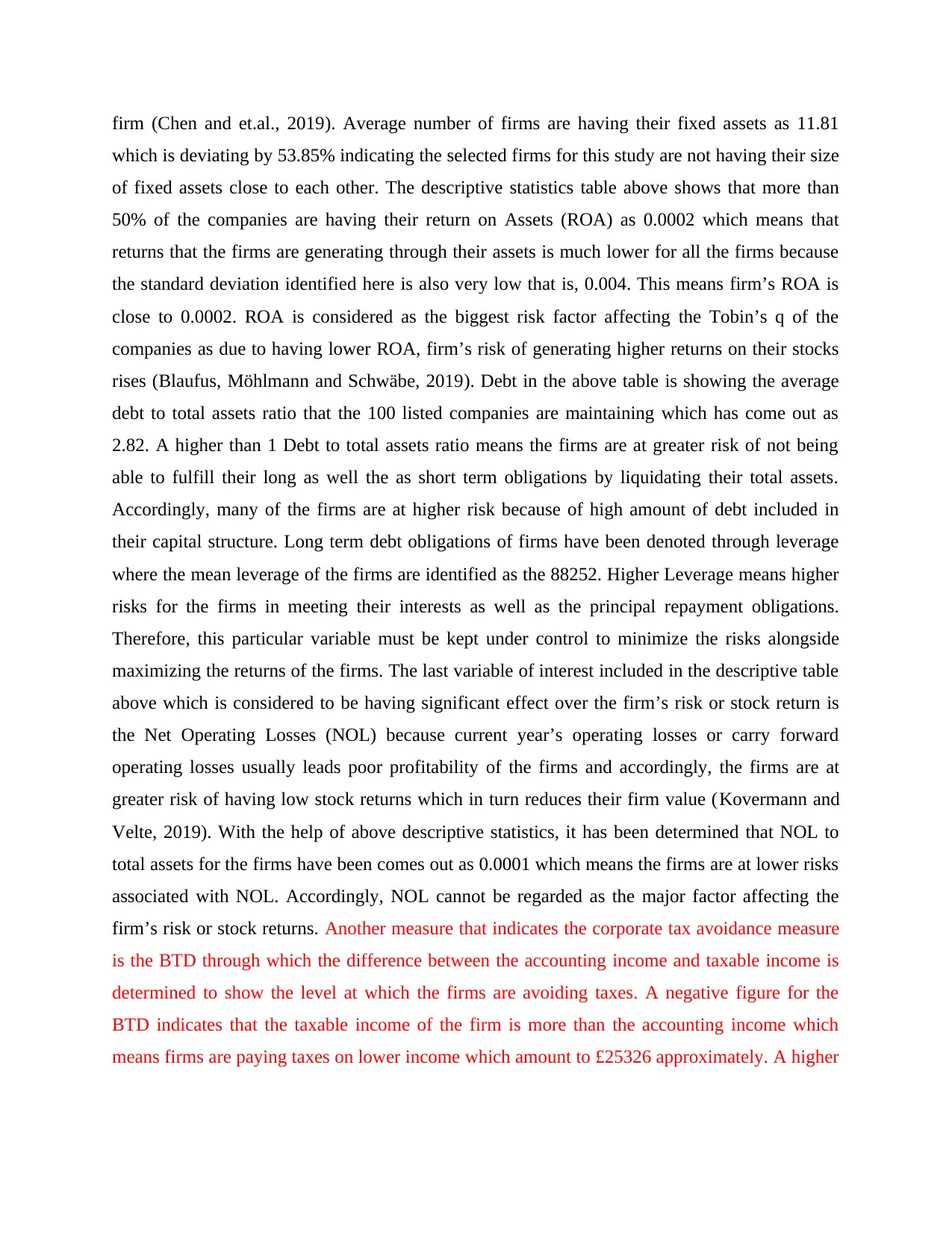

firm (Chen and et.al., 2019). Average number of firms are having their fixed assets as 11.81

which is deviating by 53.85% indicating the selected firms for this study are not having their size

of fixed assets close to each other. The descriptive statistics table above shows that more than

50% of the companies are having their return on Assets (ROA) as 0.0002 which means that

returns that the firms are generating through their assets is much lower for all the firms because

the standard deviation identified here is also very low that is, 0.004. This means firm’s ROA is

close to 0.0002. ROA is considered as the biggest risk factor affecting the Tobin’s q of the

companies as due to having lower ROA, firm’s risk of generating higher returns on their stocks

rises (Blaufus, Möhlmann and Schwäbe, 2019). Debt in the above table is showing the average

debt to total assets ratio that the 100 listed companies are maintaining which has come out as

2.82. A higher than 1 Debt to total assets ratio means the firms are at greater risk of not being

able to fulfill their long as well the as short term obligations by liquidating their total assets.

Accordingly, many of the firms are at higher risk because of high amount of debt included in

their capital structure. Long term debt obligations of firms have been denoted through leverage

where the mean leverage of the firms are identified as the 88252. Higher Leverage means higher

risks for the firms in meeting their interests as well as the principal repayment obligations.

Therefore, this particular variable must be kept under control to minimize the risks alongside

maximizing the returns of the firms. The last variable of interest included in the descriptive table

above which is considered to be having significant effect over the firm’s risk or stock return is

the Net Operating Losses (NOL) because current year’s operating losses or carry forward

operating losses usually leads poor profitability of the firms and accordingly, the firms are at

greater risk of having low stock returns which in turn reduces their firm value (Kovermann and

Velte, 2019). With the help of above descriptive statistics, it has been determined that NOL to

total assets for the firms have been comes out as 0.0001 which means the firms are at lower risks

associated with NOL. Accordingly, NOL cannot be regarded as the major factor affecting the

firm’s risk or stock returns. Another measure that indicates the corporate tax avoidance measure

is the BTD through which the difference between the accounting income and taxable income is

determined to show the level at which the firms are avoiding taxes. A negative figure for the

BTD indicates that the taxable income of the firm is more than the accounting income which

means firms are paying taxes on lower income which amount to £25326 approximately. A higher

which is deviating by 53.85% indicating the selected firms for this study are not having their size

of fixed assets close to each other. The descriptive statistics table above shows that more than

50% of the companies are having their return on Assets (ROA) as 0.0002 which means that

returns that the firms are generating through their assets is much lower for all the firms because

the standard deviation identified here is also very low that is, 0.004. This means firm’s ROA is

close to 0.0002. ROA is considered as the biggest risk factor affecting the Tobin’s q of the

companies as due to having lower ROA, firm’s risk of generating higher returns on their stocks

rises (Blaufus, Möhlmann and Schwäbe, 2019). Debt in the above table is showing the average

debt to total assets ratio that the 100 listed companies are maintaining which has come out as

2.82. A higher than 1 Debt to total assets ratio means the firms are at greater risk of not being

able to fulfill their long as well the as short term obligations by liquidating their total assets.

Accordingly, many of the firms are at higher risk because of high amount of debt included in

their capital structure. Long term debt obligations of firms have been denoted through leverage

where the mean leverage of the firms are identified as the 88252. Higher Leverage means higher

risks for the firms in meeting their interests as well as the principal repayment obligations.

Therefore, this particular variable must be kept under control to minimize the risks alongside

maximizing the returns of the firms. The last variable of interest included in the descriptive table

above which is considered to be having significant effect over the firm’s risk or stock return is

the Net Operating Losses (NOL) because current year’s operating losses or carry forward

operating losses usually leads poor profitability of the firms and accordingly, the firms are at

greater risk of having low stock returns which in turn reduces their firm value (Kovermann and

Velte, 2019). With the help of above descriptive statistics, it has been determined that NOL to

total assets for the firms have been comes out as 0.0001 which means the firms are at lower risks

associated with NOL. Accordingly, NOL cannot be regarded as the major factor affecting the

firm’s risk or stock returns. Another measure that indicates the corporate tax avoidance measure

is the BTD through which the difference between the accounting income and taxable income is

determined to show the level at which the firms are avoiding taxes. A negative figure for the

BTD indicates that the taxable income of the firm is more than the accounting income which

means firms are paying taxes on lower income which amount to £25326 approximately. A higher

negative BTD means greater stock returns because of paying taxes on lower income (accounting

income).

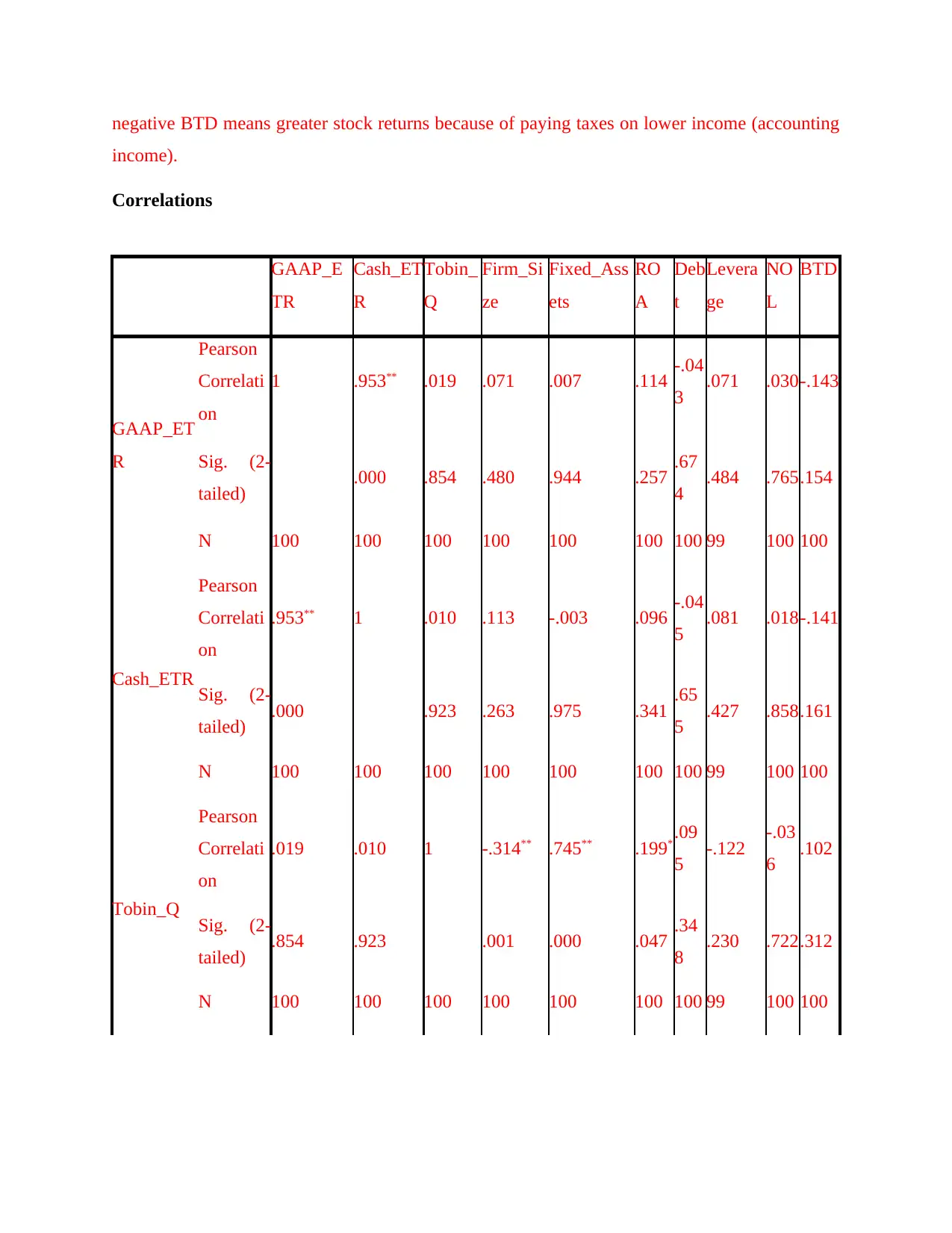

Correlations

GAAP_E

TR

Cash_ET

R

Tobin_

Q

Firm_Si

ze

Fixed_Ass

ets

RO

A

Deb

t

Levera

ge

NO

L

BTD

GAAP_ET

R

Pearson

Correlati

on

1 .953** .019 .071 .007 .114 -.04

3 .071 .030-.143

Sig. (2-

tailed) .000 .854 .480 .944 .257 .67

4 .484 .765.154

N 100 100 100 100 100 100 100 99 100 100

Cash_ETR

Pearson

Correlati

on

.953** 1 .010 .113 -.003 .096 -.04

5 .081 .018-.141

Sig. (2-

tailed) .000 .923 .263 .975 .341 .65

5 .427 .858.161

N 100 100 100 100 100 100 100 99 100 100

Tobin_Q

Pearson

Correlati

on

.019 .010 1 -.314** .745** .199* .09

5 -.122 -.03

6 .102

Sig. (2-

tailed) .854 .923 .001 .000 .047 .34

8 .230 .722.312

N 100 100 100 100 100 100 100 99 100 100

income).

Correlations

GAAP_E

TR

Cash_ET

R

Tobin_

Q

Firm_Si

ze

Fixed_Ass

ets

RO

A

Deb

t

Levera

ge

NO

L

BTD

GAAP_ET

R

Pearson

Correlati

on

1 .953** .019 .071 .007 .114 -.04

3 .071 .030-.143

Sig. (2-

tailed) .000 .854 .480 .944 .257 .67

4 .484 .765.154

N 100 100 100 100 100 100 100 99 100 100

Cash_ETR

Pearson

Correlati

on

.953** 1 .010 .113 -.003 .096 -.04

5 .081 .018-.141

Sig. (2-

tailed) .000 .923 .263 .975 .341 .65

5 .427 .858.161

N 100 100 100 100 100 100 100 99 100 100

Tobin_Q

Pearson

Correlati

on

.019 .010 1 -.314** .745** .199* .09

5 -.122 -.03

6 .102

Sig. (2-

tailed) .854 .923 .001 .000 .047 .34

8 .230 .722.312

N 100 100 100 100 100 100 100 99 100 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Firm_Size

Pearson

Correlati

on

.071 .113 -.314** 1 -.321** -.327

**

-.17

4 .610** -.07

0

-.434

**

Sig. (2-

tailed) .480 .263 .001 .001 .001 .08

4 .000 .488.000

N 100 100 100 100 100 100 100 99 100 100

Fixed_Ass

ets

Pearson

Correlati

on

.007 -.003 .745** -.321** 1 .030 .06

3 -.094 -.02

5 .078

Sig. (2-

tailed) .944 .975 .000 .001 .768 .53

6 .352 .803.443

N 100 100 100 100 100 100 100 99 100 100

ROA

Pearson

Correlati

on

.114 .096 .199* -.327** .030 1 -.00

9 -.175 .128.143

Sig. (2-

tailed) .257 .341 .047 .001 .768 .92

8 .083 .205.156

N 100 100 100 100 100 100 100 99 100 100

Debt

Pearson

Correlati

on

-.043 -.045 .095 -.174 .063 -.0091 -.096 -.01

1 .075

Sig. (2-

tailed) .674 .655 .348 .084 .536 .928 .346 .914.459

N 100 100 100 100 100 100 100 99 100 100

Pearson

Correlati

on

.071 .113 -.314** 1 -.321** -.327

**

-.17

4 .610** -.07

0

-.434

**

Sig. (2-

tailed) .480 .263 .001 .001 .001 .08

4 .000 .488.000

N 100 100 100 100 100 100 100 99 100 100

Fixed_Ass

ets

Pearson

Correlati

on

.007 -.003 .745** -.321** 1 .030 .06

3 -.094 -.02

5 .078

Sig. (2-

tailed) .944 .975 .000 .001 .768 .53

6 .352 .803.443

N 100 100 100 100 100 100 100 99 100 100

ROA

Pearson

Correlati

on

.114 .096 .199* -.327** .030 1 -.00

9 -.175 .128.143

Sig. (2-

tailed) .257 .341 .047 .001 .768 .92

8 .083 .205.156

N 100 100 100 100 100 100 100 99 100 100

Debt

Pearson

Correlati

on

-.043 -.045 .095 -.174 .063 -.0091 -.096 -.01

1 .075

Sig. (2-

tailed) .674 .655 .348 .084 .536 .928 .346 .914.459

N 100 100 100 100 100 100 100 99 100 100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

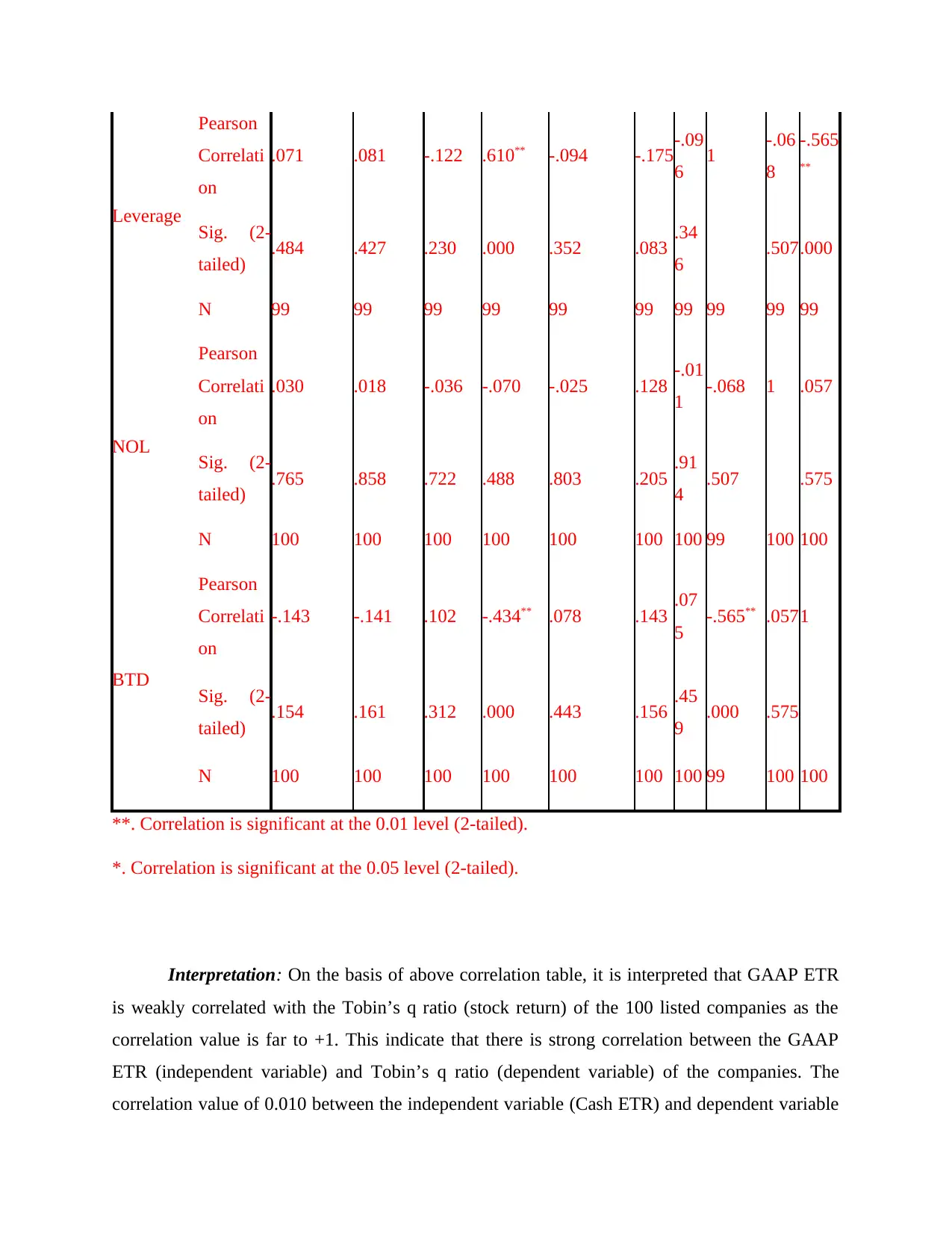

Leverage

Pearson

Correlati

on

.071 .081 -.122 .610** -.094 -.175-.09

6 1 -.06

8

-.565

**

Sig. (2-

tailed) .484 .427 .230 .000 .352 .083 .34

6 .507.000

N 99 99 99 99 99 99 99 99 99 99

NOL

Pearson

Correlati

on

.030 .018 -.036 -.070 -.025 .128 -.01

1 -.068 1 .057

Sig. (2-

tailed) .765 .858 .722 .488 .803 .205 .91

4 .507 .575

N 100 100 100 100 100 100 100 99 100 100

BTD

Pearson

Correlati

on

-.143 -.141 .102 -.434** .078 .143 .07

5 -.565** .0571

Sig. (2-

tailed) .154 .161 .312 .000 .443 .156 .45

9 .000 .575

N 100 100 100 100 100 100 100 99 100 100

**. Correlation is significant at the 0.01 level (2-tailed).

*. Correlation is significant at the 0.05 level (2-tailed).

Interpretation: On the basis of above correlation table, it is interpreted that GAAP ETR

is weakly correlated with the Tobin’s q ratio (stock return) of the 100 listed companies as the

correlation value is far to +1. This indicate that there is strong correlation between the GAAP

ETR (independent variable) and Tobin’s q ratio (dependent variable) of the companies. The

correlation value of 0.010 between the independent variable (Cash ETR) and dependent variable

Pearson

Correlati

on

.071 .081 -.122 .610** -.094 -.175-.09

6 1 -.06

8

-.565

**

Sig. (2-

tailed) .484 .427 .230 .000 .352 .083 .34

6 .507.000

N 99 99 99 99 99 99 99 99 99 99

NOL

Pearson

Correlati

on

.030 .018 -.036 -.070 -.025 .128 -.01

1 -.068 1 .057

Sig. (2-

tailed) .765 .858 .722 .488 .803 .205 .91

4 .507 .575

N 100 100 100 100 100 100 100 99 100 100

BTD

Pearson

Correlati

on

-.143 -.141 .102 -.434** .078 .143 .07

5 -.565** .0571

Sig. (2-

tailed) .154 .161 .312 .000 .443 .156 .45

9 .000 .575

N 100 100 100 100 100 100 100 99 100 100

**. Correlation is significant at the 0.01 level (2-tailed).

*. Correlation is significant at the 0.05 level (2-tailed).

Interpretation: On the basis of above correlation table, it is interpreted that GAAP ETR

is weakly correlated with the Tobin’s q ratio (stock return) of the 100 listed companies as the

correlation value is far to +1. This indicate that there is strong correlation between the GAAP

ETR (independent variable) and Tobin’s q ratio (dependent variable) of the companies. The

correlation value of 0.010 between the independent variable (Cash ETR) and dependent variable

(Tobin’s q ratio) indicate that cash effective tax rate (corporate tax avoidance measure) is weakly

correlated with the firm risk measurement of the company. It is because analyzing the stock

return and firm risk of the company using only GAAP and cash ETR is not possible because this

two corporate tax avoidance measurement factor does not strongly affect the stock return or firm

value of company (Oats and Tuck, 2019).

However, the correlation value also indicates that the association between the dependent

and independent variable is positive. This means that with the change (upward/ downward) in the

cash or GAAP ETR of company, the stock return will also change in same direction. But it is

also important to understand that if the stock return of the company increases, then the firm value

increases which ultimately result into lower firm risk (Kovermann and Velte, 2019). This

statement indicates that there is negative association between the corporate tax avoidance (cash

and GAAP ETR) and firm risk of UK 100 listed companies as with the increase in stock return of

company, the firm risk will automatically reduce.

On the other side, the control variables also play significant role in establishing the

correlational or causal relationship between the variable of interest. After analyzing the above

data, it is identified that firm size (control variable) is negatively correlated with the Tobin’s q

ratio (Dependent variable). .745 value indicate that there is moderate correlation exist between

the fixed assets and Tobin’s q ratio. Further, it is also interpreted from the above correlation

matrix table is that there is weak correlation exist between the ROA (Control variable) and

Tobin’s q ratio (dependent variable) of the company. This indicate that companies should keep

close eye towards variables such as cash ETR, GAAP ETR, ROA of the company in order to

reduce the firm risk of the company. However, firm size has negative relation with the stock

return and firm risk of the company. So, 100 listed companies of UK can avoid this variable.

It is also interpreted from the above table that there is strong correlation between debt and

Tobin’s q ratio of listed companies which indicate that companies should manage its long term

debt as well to increase the stock return and reduce the firm risk. 0.610 and .71 value indicate

that there is moderate correlation exits between leverage and NOL with the Tobin’s q return. At

last, it can be seen that the correlation between the BTD and Tobin’s Q is 0.102 which is falling

in the lower range of degree of correlation and accordingly, BTD is not affecting the firm’s stock

return to a great extent.

correlated with the firm risk measurement of the company. It is because analyzing the stock

return and firm risk of the company using only GAAP and cash ETR is not possible because this

two corporate tax avoidance measurement factor does not strongly affect the stock return or firm

value of company (Oats and Tuck, 2019).

However, the correlation value also indicates that the association between the dependent

and independent variable is positive. This means that with the change (upward/ downward) in the

cash or GAAP ETR of company, the stock return will also change in same direction. But it is

also important to understand that if the stock return of the company increases, then the firm value

increases which ultimately result into lower firm risk (Kovermann and Velte, 2019). This

statement indicates that there is negative association between the corporate tax avoidance (cash

and GAAP ETR) and firm risk of UK 100 listed companies as with the increase in stock return of

company, the firm risk will automatically reduce.

On the other side, the control variables also play significant role in establishing the

correlational or causal relationship between the variable of interest. After analyzing the above

data, it is identified that firm size (control variable) is negatively correlated with the Tobin’s q

ratio (Dependent variable). .745 value indicate that there is moderate correlation exist between

the fixed assets and Tobin’s q ratio. Further, it is also interpreted from the above correlation

matrix table is that there is weak correlation exist between the ROA (Control variable) and

Tobin’s q ratio (dependent variable) of the company. This indicate that companies should keep

close eye towards variables such as cash ETR, GAAP ETR, ROA of the company in order to

reduce the firm risk of the company. However, firm size has negative relation with the stock

return and firm risk of the company. So, 100 listed companies of UK can avoid this variable.

It is also interpreted from the above table that there is strong correlation between debt and

Tobin’s q ratio of listed companies which indicate that companies should manage its long term

debt as well to increase the stock return and reduce the firm risk. 0.610 and .71 value indicate

that there is moderate correlation exits between leverage and NOL with the Tobin’s q return. At

last, it can be seen that the correlation between the BTD and Tobin’s Q is 0.102 which is falling

in the lower range of degree of correlation and accordingly, BTD is not affecting the firm’s stock

return to a great extent.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Overall, it is analyzed from the correlation matrix is that companies are required to

manage and control all independent and control variable to reduce the firm risk (Wang and et.al.,

2020).

Regression

Hypothesis 1:

Null Hypothesis (HO) = There is no statistical relationship between GAAP ETR and stock return

(Tobin’s Q) of 100 UK listed companies.

Alternative Hypothesis (H1) = There is statistical relationship between GAAP ETR and stock

return (Tobin’s Q) of 100 UK listed companies.

Model Summary

Model R R Square Adjusted R

Square

Std. Error of

the Estimate

1 .774a .598 .568 63.05202

a. Predictors: (Constant), NOL, Debt, GAAP_ETR,

Fixed_Assets, Leverage, ROA, Firm_Size

ANOVAa

Model Sum of

Squares

df Mean Square F Sig.

1

Regression 539254.115 7 77036.302 19.377 .000b

Residual 361775.730 91 3975.557

Total 901029.845 98

a. Dependent Variable: Tobin_Q

b. Predictors: (Constant), NOL, Debt, GAAP_ETR, Fixed_Assets, Leverage, ROA,

Firm_Size

Coefficientsa

manage and control all independent and control variable to reduce the firm risk (Wang and et.al.,

2020).

Regression

Hypothesis 1:

Null Hypothesis (HO) = There is no statistical relationship between GAAP ETR and stock return

(Tobin’s Q) of 100 UK listed companies.

Alternative Hypothesis (H1) = There is statistical relationship between GAAP ETR and stock

return (Tobin’s Q) of 100 UK listed companies.

Model Summary

Model R R Square Adjusted R

Square

Std. Error of

the Estimate

1 .774a .598 .568 63.05202

a. Predictors: (Constant), NOL, Debt, GAAP_ETR,

Fixed_Assets, Leverage, ROA, Firm_Size

ANOVAa

Model Sum of

Squares

df Mean Square F Sig.

1

Regression 539254.115 7 77036.302 19.377 .000b

Residual 361775.730 91 3975.557

Total 901029.845 98

a. Dependent Variable: Tobin_Q

b. Predictors: (Constant), NOL, Debt, GAAP_ETR, Fixed_Assets, Leverage, ROA,

Firm_Size

Coefficientsa

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Model Unstandardized Coefficients Standardized

Coefficients

t Sig.

B Std. Error Beta

1

(Constant) 1.122 46.457 .024 .981

GAAP_ETR -.703 11.867 -.004 -.059 .953

Firm_Size .346 3.964 .008 .087 .931

Fixed_Assets 1.311 .126 .740 10.384 .000

ROA 4256.535 1642.467 .187 2.592 .011

Debt .425 .557 .052 .763 .447

Leverage -1.046E-005 .000 -.022 -.255 .799

NOL -6846.442 11551.730 -.040 -.593 .555

a. Dependent Variable: Tobin_Q

Interpretation: After analyzing the linear regression result, it is identified that the

significance p value is 0.000 which is lower than standard criteria of 0.05. This further interpret

that the alternative hypothesis will be accepted and null hypothesis will be rejected. It is

identified from the outcome that there is statistical relationship between the GAAP ETR and

Tobin’s Q stock return on the company (Ozili, 2020). Here, the GAAP ETR is considered as a

tax avoidance measurement factor and on the other hand, Tobin’s Q stock return is considered as

a factor measuring risk firm risk. To identify the relation between GAAP ETR and Tobin’s q

(stock return), the selected independent variable is GAAP ETR, dependent variable is Tobin’s q

(firm risk measurement) and other six control variable. It is interpreted from the above table that

there is statistical relationship exist between the GAAP ETR and Tobin’s q ratio. The GAAP

ETR is a corporate tax avoidance measure which should be low within the company. It is

because with the help of maintaining low GAAP effective tax rate, the companies able to avoid

high volume of corporate tax which ultimately increases the profitability as well as liquidity of

the company.

Further, it is also analyzed from the above table, that there is a positive relation between

the GAAP ETR (tax avoidance measure) and stock return. This indicate that if GAAP ETR of

the company increases than the stock return of corporate will also increase. Corporate tax

avoidance has a significant impact over the stock return of the company is statistically proved

through ANNOVA table. The GAAP ETR is one of the factor of measuring corporate tax

Coefficients

t Sig.

B Std. Error Beta

1

(Constant) 1.122 46.457 .024 .981

GAAP_ETR -.703 11.867 -.004 -.059 .953

Firm_Size .346 3.964 .008 .087 .931

Fixed_Assets 1.311 .126 .740 10.384 .000

ROA 4256.535 1642.467 .187 2.592 .011

Debt .425 .557 .052 .763 .447

Leverage -1.046E-005 .000 -.022 -.255 .799

NOL -6846.442 11551.730 -.040 -.593 .555

a. Dependent Variable: Tobin_Q

Interpretation: After analyzing the linear regression result, it is identified that the

significance p value is 0.000 which is lower than standard criteria of 0.05. This further interpret

that the alternative hypothesis will be accepted and null hypothesis will be rejected. It is

identified from the outcome that there is statistical relationship between the GAAP ETR and

Tobin’s Q stock return on the company (Ozili, 2020). Here, the GAAP ETR is considered as a

tax avoidance measurement factor and on the other hand, Tobin’s Q stock return is considered as

a factor measuring risk firm risk. To identify the relation between GAAP ETR and Tobin’s q

(stock return), the selected independent variable is GAAP ETR, dependent variable is Tobin’s q

(firm risk measurement) and other six control variable. It is interpreted from the above table that

there is statistical relationship exist between the GAAP ETR and Tobin’s q ratio. The GAAP

ETR is a corporate tax avoidance measure which should be low within the company. It is

because with the help of maintaining low GAAP effective tax rate, the companies able to avoid

high volume of corporate tax which ultimately increases the profitability as well as liquidity of

the company.

Further, it is also analyzed from the above table, that there is a positive relation between

the GAAP ETR (tax avoidance measure) and stock return. This indicate that if GAAP ETR of

the company increases than the stock return of corporate will also increase. Corporate tax

avoidance has a significant impact over the stock return of the company is statistically proved

through ANNOVA table. The GAAP ETR is one of the factor of measuring corporate tax

avoidance and stock return is a firm risk measurement which indicate that if the company stock

return increases than this leads to reduction in the firm risk of companies. Hence, on this basis, it

is interpreted that if the GAAP ETR of 100 listed companies increases than their stock return will

also increases because of positive association. The increase in stock return will ultimately result

into the reduction in firm risk. With the ANNOVA table, it is identified that GAAP ETR have a

significant impact on the stock return (Tobin’s q) of the company but on the other hand, from the

coefficient table, it is identified that GAAP ETR have no significant impact on stock return

because of significance value of 0.953 (Zeng, 2018). The ANNOVA table state that the

alternative hypothesis is accepted or proved. This means that overall the GAAP ETR affect the

stock return of the company. While on the other hand, the coefficient table state that GAAP ETR

individually do not affect the Tobin’s Q (stock return) of 100 listed companies.

However, the coefficient table has also stated that individual factors such as firm size,

leverage and NOL has no significant association or impact on the Tobin’s q ratio of the company

which is basically a firm risk measurement. It is because their significance value is more than

0.05. While the individual variable such as ROA, Debt and fixed assets have significant impact

on the stock return (Tobin’s q) of the company (Yee, Sapiei and Abdullah, 2018). On this basis,

it can be said that this individual variable is not affecting the Tobin’s q value of the company, but

while considering it together this are affecting the Tobin’s q (stock return) of the company as per

ANNOVA table.

From the present data and its findings, it is analyzed that 100 listed companies of UK

adopt the strategies to reduce the GAAP ETR of the company. It is because if the GAAP ETR of

the company reduces, the firm value of company will increase which further result into lower

firm risk. Hence, on this basis, it is statistically proved that there is negative effect of corporate

tax avoidance (GAAP ETR) on the firm risk of the companies. It is because with the increase in

GAAP ETR, the firm value or stock return on companies will reduce which ultimately leads to

lower firm risk. Overall, it is interpreted that 100 listed companies of UK adopted different

strategies to reduce the GAAP effective tax rate in order to reduce firm risk (Mao, 2019).

Hypothesis 2:

Null hypothesis: There is no statistical relationship between Cash ETR and Stock returns

(Tobin’s Q ratio) of the 100 listed firms.

return increases than this leads to reduction in the firm risk of companies. Hence, on this basis, it

is interpreted that if the GAAP ETR of 100 listed companies increases than their stock return will

also increases because of positive association. The increase in stock return will ultimately result

into the reduction in firm risk. With the ANNOVA table, it is identified that GAAP ETR have a

significant impact on the stock return (Tobin’s q) of the company but on the other hand, from the

coefficient table, it is identified that GAAP ETR have no significant impact on stock return

because of significance value of 0.953 (Zeng, 2018). The ANNOVA table state that the

alternative hypothesis is accepted or proved. This means that overall the GAAP ETR affect the

stock return of the company. While on the other hand, the coefficient table state that GAAP ETR

individually do not affect the Tobin’s Q (stock return) of 100 listed companies.

However, the coefficient table has also stated that individual factors such as firm size,

leverage and NOL has no significant association or impact on the Tobin’s q ratio of the company

which is basically a firm risk measurement. It is because their significance value is more than

0.05. While the individual variable such as ROA, Debt and fixed assets have significant impact

on the stock return (Tobin’s q) of the company (Yee, Sapiei and Abdullah, 2018). On this basis,

it can be said that this individual variable is not affecting the Tobin’s q value of the company, but

while considering it together this are affecting the Tobin’s q (stock return) of the company as per

ANNOVA table.

From the present data and its findings, it is analyzed that 100 listed companies of UK

adopt the strategies to reduce the GAAP ETR of the company. It is because if the GAAP ETR of

the company reduces, the firm value of company will increase which further result into lower

firm risk. Hence, on this basis, it is statistically proved that there is negative effect of corporate

tax avoidance (GAAP ETR) on the firm risk of the companies. It is because with the increase in

GAAP ETR, the firm value or stock return on companies will reduce which ultimately leads to

lower firm risk. Overall, it is interpreted that 100 listed companies of UK adopted different

strategies to reduce the GAAP effective tax rate in order to reduce firm risk (Mao, 2019).

Hypothesis 2:

Null hypothesis: There is no statistical relationship between Cash ETR and Stock returns

(Tobin’s Q ratio) of the 100 listed firms.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.