EMBFDM - Firm X's Capital Structure Decision: A Financial Analysis

VerifiedAdded on 2023/06/04

|20

|4622

|109

Case Study

AI Summary

This case study analyzes Firm X's capital structure decision, focusing on optimizing the debt-equity mix for a new $100,000 project with expected annual cash flows of $40,000. It explores Modigliani-Miller propositions under scenarios of risk-free and risky debt, with and without a 40% corporate tax rate. The analysis involves computing the weighted average cost of capital (WACC) for various debt-equity combinations, considering the impact of taxes and the increasing cost of equity due to financial distress. The findings suggest that with tax considerations, a higher proportion of debt leads to a lower cost of capital, while without taxes, the capital structure has less impact on WACC. The study concludes by highlighting the importance of capital structure decisions in minimizing the cost of capital and maximizing firm value.

FINANCE FOR DECISION MAKING

FIRM X-CAPITAL STRUCTURE DECISION

FIRM X-CAPITAL STRUCTURE DECISION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table Of Contents

Analysis..................................................................................................................................................3

Computation of Capital Structure under different scenario..................................................................5

Case 1: Risk Free Debt without tax....................................................................................................5

Case 1: Risk Free Debt with tax..........................................................................................................7

Case 2: Risky Debt without tax..........................................................................................................9

Case 2: Risky Debt with tax..............................................................................................................10

Problems under Capital Financing.......................................................................................................12

Conclusion...........................................................................................................................................14

References...........................................................................................................................................14

Analysis..................................................................................................................................................3

Computation of Capital Structure under different scenario..................................................................5

Case 1: Risk Free Debt without tax....................................................................................................5

Case 1: Risk Free Debt with tax..........................................................................................................7

Case 2: Risky Debt without tax..........................................................................................................9

Case 2: Risky Debt with tax..............................................................................................................10

Problems under Capital Financing.......................................................................................................12

Conclusion...........................................................................................................................................14

References...........................................................................................................................................14

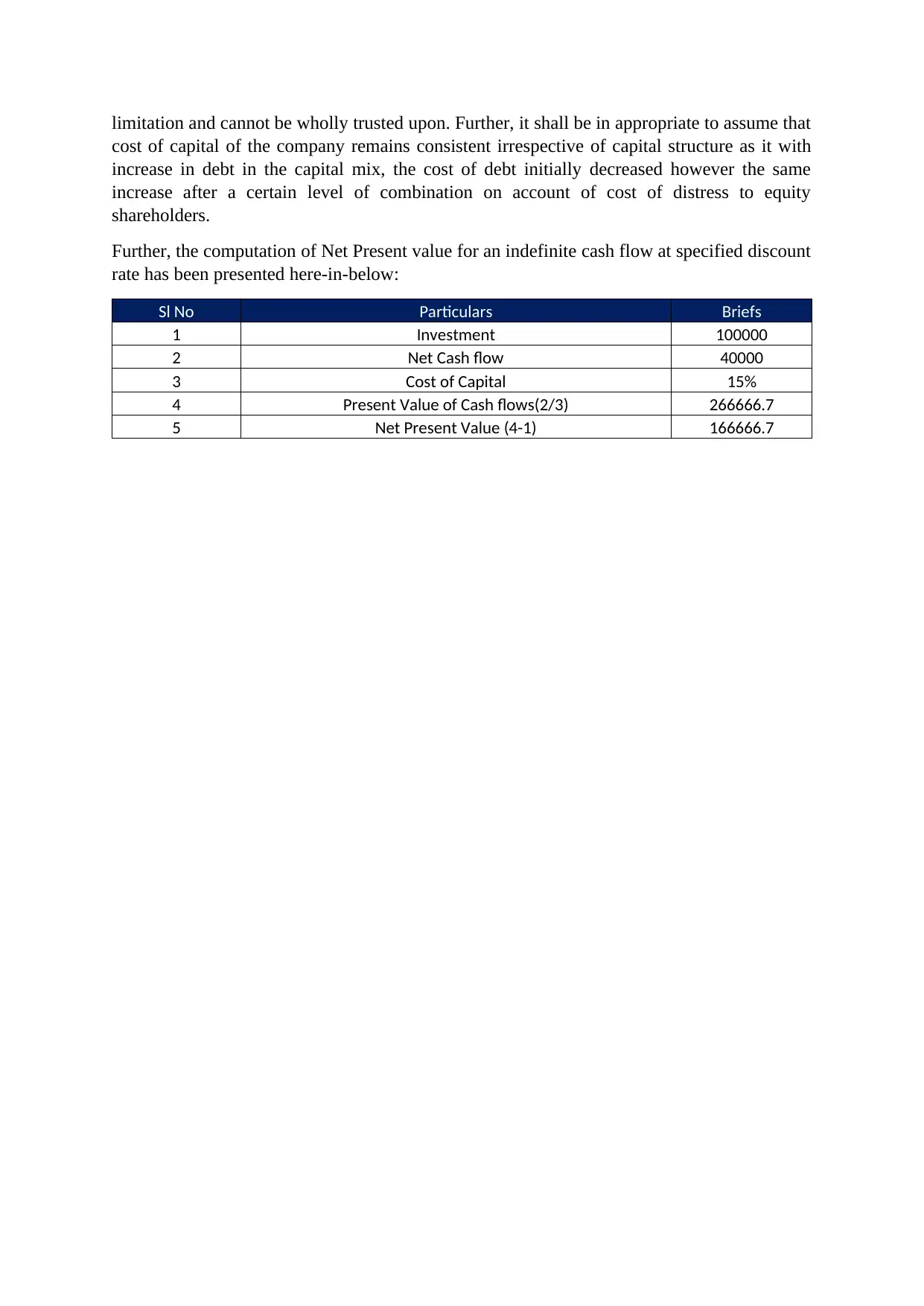

Introduction

The report has been written to explore proposed business decision making for raising finance

via equity or debt. X Company is trying to explore different venues of procuring funds and

has surveyed and collected data regarding the cost of capital of the company under different

structure and different level of risk.

X company has an investment opportunity of $100,000 and for the purpose of the same the

company has listed various funding options and trying to explore an optimal combination of

debt and equity to fund the project at low cost of capital while emphasizing on the qualitative

aspects of loan procurement like agency effect and signalling effect of capital structure. The

report in detail deals with the same.

It shall also be pertinent to note that Net Present Value of the project is positive at 15% rate

of discount. Thus, the ideal financing shall have ideal combination of debt and equity under

which the cost of capital shall be lower than 15%.

Analysis

The report contains two case: case 1 and case 2 with different range of combination of debt

and equity. Under case 1 there is risk free debt while under case 2 there is risky debt. Further,

the corporate rate of taxation is 40% and the tax saving in account if interest shall be

available. The report also assumes that the pre and post cost of equity remains the same and

thus there is no impact of corporate tax.

The analysis starts with explaining the proposition of Modigliani Miller under which it has

been stated that the market capitalisation of the company is not dependent on the capital

structure of the company rather the same is dependent on the net operating cash flows.

Further, the model assumes that there is no transaction cost and taxes. However, under the

present scenario, there is corporation tax of 40%, thus the proposition 1 does not hold good.

Under the second proposition it has been stated that the market value of the firm shall

increase by the present value of tax savings on account of interest on debt. Further, the above

proposition states that the ideal debt equity combination is 100% and 0% symbolising fully

funded by debt which is not a good idea. The proposition is set back by many drawbacks and

The report has been written to explore proposed business decision making for raising finance

via equity or debt. X Company is trying to explore different venues of procuring funds and

has surveyed and collected data regarding the cost of capital of the company under different

structure and different level of risk.

X company has an investment opportunity of $100,000 and for the purpose of the same the

company has listed various funding options and trying to explore an optimal combination of

debt and equity to fund the project at low cost of capital while emphasizing on the qualitative

aspects of loan procurement like agency effect and signalling effect of capital structure. The

report in detail deals with the same.

It shall also be pertinent to note that Net Present Value of the project is positive at 15% rate

of discount. Thus, the ideal financing shall have ideal combination of debt and equity under

which the cost of capital shall be lower than 15%.

Analysis

The report contains two case: case 1 and case 2 with different range of combination of debt

and equity. Under case 1 there is risk free debt while under case 2 there is risky debt. Further,

the corporate rate of taxation is 40% and the tax saving in account if interest shall be

available. The report also assumes that the pre and post cost of equity remains the same and

thus there is no impact of corporate tax.

The analysis starts with explaining the proposition of Modigliani Miller under which it has

been stated that the market capitalisation of the company is not dependent on the capital

structure of the company rather the same is dependent on the net operating cash flows.

Further, the model assumes that there is no transaction cost and taxes. However, under the

present scenario, there is corporation tax of 40%, thus the proposition 1 does not hold good.

Under the second proposition it has been stated that the market value of the firm shall

increase by the present value of tax savings on account of interest on debt. Further, the above

proposition states that the ideal debt equity combination is 100% and 0% symbolising fully

funded by debt which is not a good idea. The proposition is set back by many drawbacks and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

limitation and cannot be wholly trusted upon. Further, it shall be in appropriate to assume that

cost of capital of the company remains consistent irrespective of capital structure as it with

increase in debt in the capital mix, the cost of debt initially decreased however the same

increase after a certain level of combination on account of cost of distress to equity

shareholders.

Further, the computation of Net Present value for an indefinite cash flow at specified discount

rate has been presented here-in-below:

Sl No Particulars Briefs

1 Investment 100000

2 Net Cash flow 40000

3 Cost of Capital 15%

4 Present Value of Cash flows(2/3) 266666.7

5 Net Present Value (4-1) 166666.7

cost of capital of the company remains consistent irrespective of capital structure as it with

increase in debt in the capital mix, the cost of debt initially decreased however the same

increase after a certain level of combination on account of cost of distress to equity

shareholders.

Further, the computation of Net Present value for an indefinite cash flow at specified discount

rate has been presented here-in-below:

Sl No Particulars Briefs

1 Investment 100000

2 Net Cash flow 40000

3 Cost of Capital 15%

4 Present Value of Cash flows(2/3) 266666.7

5 Net Present Value (4-1) 166666.7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

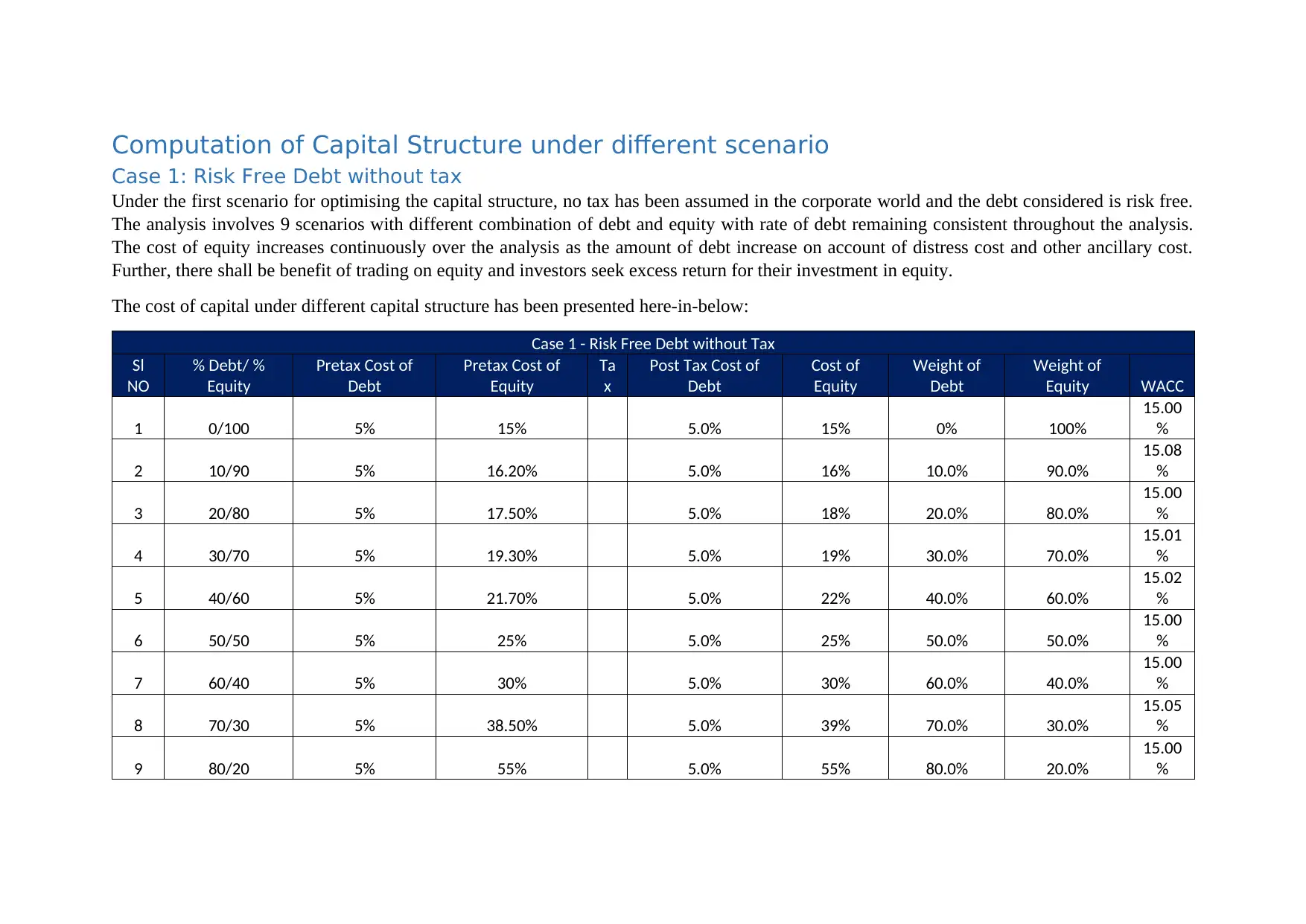

Computation of Capital Structure under different scenario

Case 1: Risk Free Debt without tax

Under the first scenario for optimising the capital structure, no tax has been assumed in the corporate world and the debt considered is risk free.

The analysis involves 9 scenarios with different combination of debt and equity with rate of debt remaining consistent throughout the analysis.

The cost of equity increases continuously over the analysis as the amount of debt increase on account of distress cost and other ancillary cost.

Further, there shall be benefit of trading on equity and investors seek excess return for their investment in equity.

The cost of capital under different capital structure has been presented here-in-below:

Case 1 - Risk Free Debt without Tax

Sl

NO

% Debt/ %

Equity

Pretax Cost of

Debt

Pretax Cost of

Equity

Ta

x

Post Tax Cost of

Debt

Cost of

Equity

Weight of

Debt

Weight of

Equity WACC

1 0/100 5% 15% 5.0% 15% 0% 100%

15.00

%

2 10/90 5% 16.20% 5.0% 16% 10.0% 90.0%

15.08

%

3 20/80 5% 17.50% 5.0% 18% 20.0% 80.0%

15.00

%

4 30/70 5% 19.30% 5.0% 19% 30.0% 70.0%

15.01

%

5 40/60 5% 21.70% 5.0% 22% 40.0% 60.0%

15.02

%

6 50/50 5% 25% 5.0% 25% 50.0% 50.0%

15.00

%

7 60/40 5% 30% 5.0% 30% 60.0% 40.0%

15.00

%

8 70/30 5% 38.50% 5.0% 39% 70.0% 30.0%

15.05

%

9 80/20 5% 55% 5.0% 55% 80.0% 20.0%

15.00

%

Case 1: Risk Free Debt without tax

Under the first scenario for optimising the capital structure, no tax has been assumed in the corporate world and the debt considered is risk free.

The analysis involves 9 scenarios with different combination of debt and equity with rate of debt remaining consistent throughout the analysis.

The cost of equity increases continuously over the analysis as the amount of debt increase on account of distress cost and other ancillary cost.

Further, there shall be benefit of trading on equity and investors seek excess return for their investment in equity.

The cost of capital under different capital structure has been presented here-in-below:

Case 1 - Risk Free Debt without Tax

Sl

NO

% Debt/ %

Equity

Pretax Cost of

Debt

Pretax Cost of

Equity

Ta

x

Post Tax Cost of

Debt

Cost of

Equity

Weight of

Debt

Weight of

Equity WACC

1 0/100 5% 15% 5.0% 15% 0% 100%

15.00

%

2 10/90 5% 16.20% 5.0% 16% 10.0% 90.0%

15.08

%

3 20/80 5% 17.50% 5.0% 18% 20.0% 80.0%

15.00

%

4 30/70 5% 19.30% 5.0% 19% 30.0% 70.0%

15.01

%

5 40/60 5% 21.70% 5.0% 22% 40.0% 60.0%

15.02

%

6 50/50 5% 25% 5.0% 25% 50.0% 50.0%

15.00

%

7 60/40 5% 30% 5.0% 30% 60.0% 40.0%

15.00

%

8 70/30 5% 38.50% 5.0% 39% 70.0% 30.0%

15.05

%

9 80/20 5% 55% 5.0% 55% 80.0% 20.0%

15.00

%

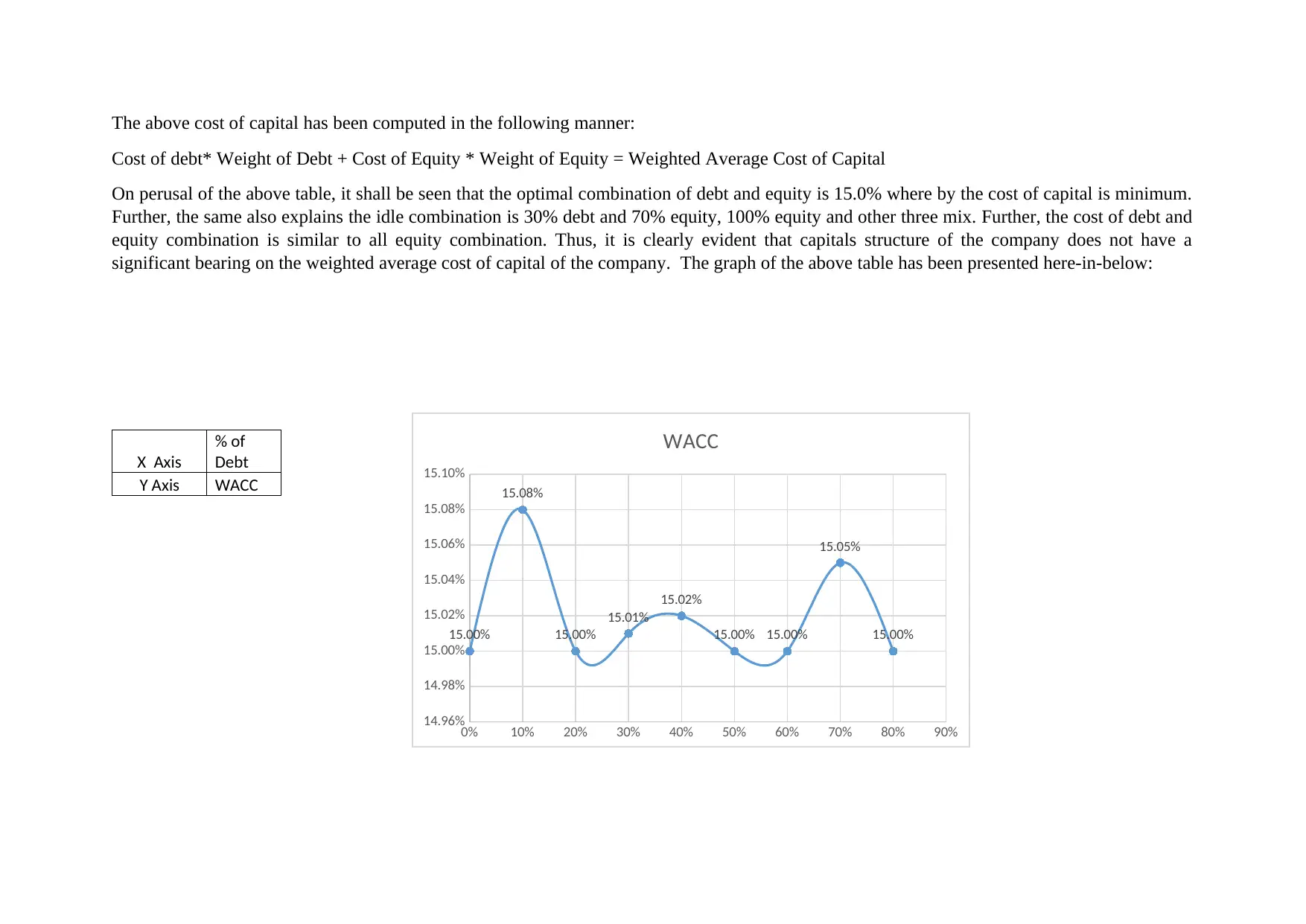

The above cost of capital has been computed in the following manner:

Cost of debt* Weight of Debt + Cost of Equity * Weight of Equity = Weighted Average Cost of Capital

On perusal of the above table, it shall be seen that the optimal combination of debt and equity is 15.0% where by the cost of capital is minimum.

Further, the same also explains the idle combination is 30% debt and 70% equity, 100% equity and other three mix. Further, the cost of debt and

equity combination is similar to all equity combination. Thus, it is clearly evident that capitals structure of the company does not have a

significant bearing on the weighted average cost of capital of the company. The graph of the above table has been presented here-in-below:

X Axis

% of

Debt

Y Axis WACC

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

14.96%

14.98%

15.00%

15.02%

15.04%

15.06%

15.08%

15.10%

15.00%

15.08%

15.00%

15.01%

15.02%

15.00% 15.00%

15.05%

15.00%

WACC

Cost of debt* Weight of Debt + Cost of Equity * Weight of Equity = Weighted Average Cost of Capital

On perusal of the above table, it shall be seen that the optimal combination of debt and equity is 15.0% where by the cost of capital is minimum.

Further, the same also explains the idle combination is 30% debt and 70% equity, 100% equity and other three mix. Further, the cost of debt and

equity combination is similar to all equity combination. Thus, it is clearly evident that capitals structure of the company does not have a

significant bearing on the weighted average cost of capital of the company. The graph of the above table has been presented here-in-below:

X Axis

% of

Debt

Y Axis WACC

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

14.96%

14.98%

15.00%

15.02%

15.04%

15.06%

15.08%

15.10%

15.00%

15.08%

15.00%

15.01%

15.02%

15.00% 15.00%

15.05%

15.00%

WACC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Thus, under the first scenario, the idle mix of debt and equity results in the optimal cost of capital of the company is 15.0%.

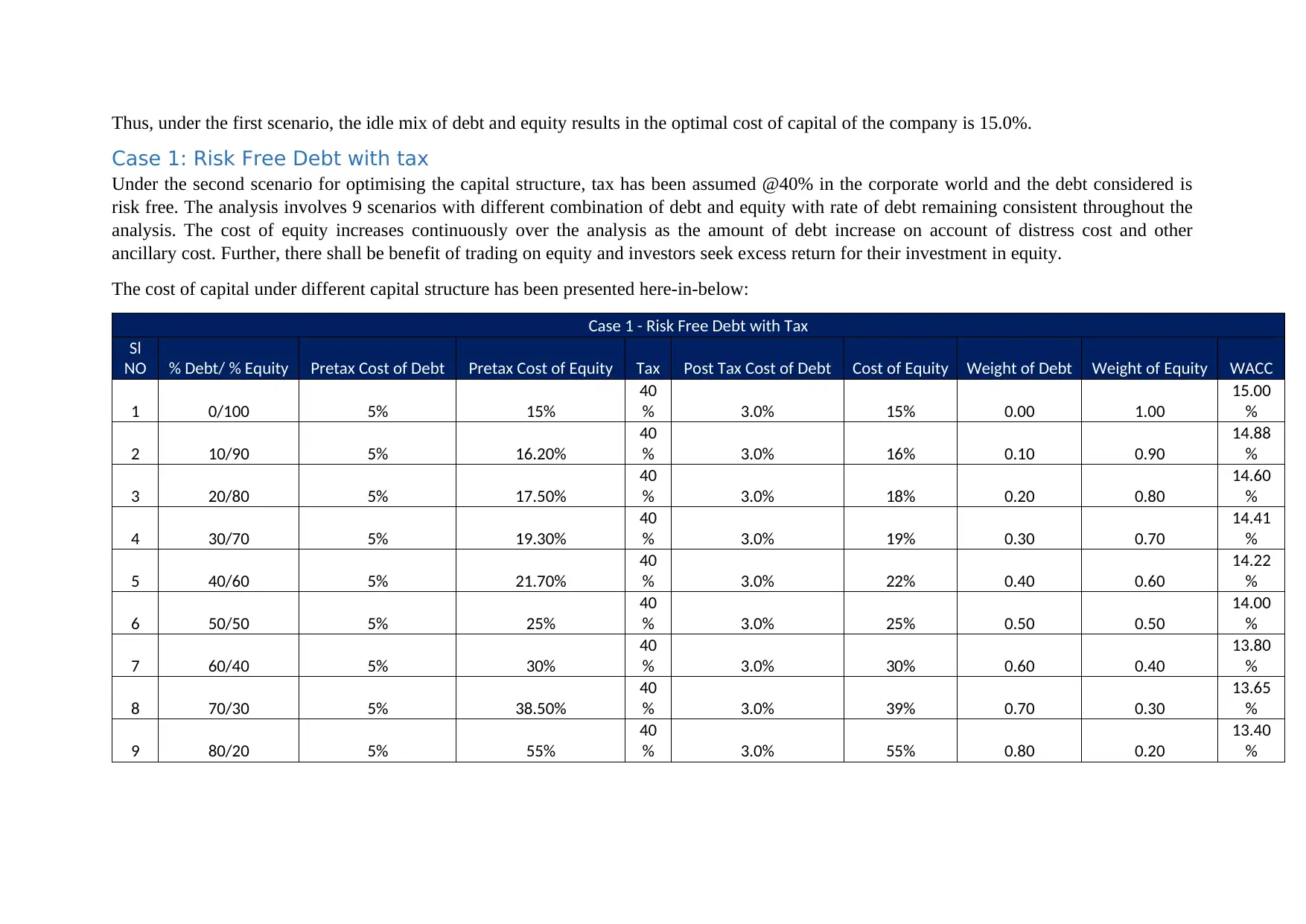

Case 1: Risk Free Debt with tax

Under the second scenario for optimising the capital structure, tax has been assumed @40% in the corporate world and the debt considered is

risk free. The analysis involves 9 scenarios with different combination of debt and equity with rate of debt remaining consistent throughout the

analysis. The cost of equity increases continuously over the analysis as the amount of debt increase on account of distress cost and other

ancillary cost. Further, there shall be benefit of trading on equity and investors seek excess return for their investment in equity.

The cost of capital under different capital structure has been presented here-in-below:

Case 1 - Risk Free Debt with Tax

Sl

NO % Debt/ % Equity Pretax Cost of Debt Pretax Cost of Equity Tax Post Tax Cost of Debt Cost of Equity Weight of Debt Weight of Equity WACC

1 0/100 5% 15%

40

% 3.0% 15% 0.00 1.00

15.00

%

2 10/90 5% 16.20%

40

% 3.0% 16% 0.10 0.90

14.88

%

3 20/80 5% 17.50%

40

% 3.0% 18% 0.20 0.80

14.60

%

4 30/70 5% 19.30%

40

% 3.0% 19% 0.30 0.70

14.41

%

5 40/60 5% 21.70%

40

% 3.0% 22% 0.40 0.60

14.22

%

6 50/50 5% 25%

40

% 3.0% 25% 0.50 0.50

14.00

%

7 60/40 5% 30%

40

% 3.0% 30% 0.60 0.40

13.80

%

8 70/30 5% 38.50%

40

% 3.0% 39% 0.70 0.30

13.65

%

9 80/20 5% 55%

40

% 3.0% 55% 0.80 0.20

13.40

%

Case 1: Risk Free Debt with tax

Under the second scenario for optimising the capital structure, tax has been assumed @40% in the corporate world and the debt considered is

risk free. The analysis involves 9 scenarios with different combination of debt and equity with rate of debt remaining consistent throughout the

analysis. The cost of equity increases continuously over the analysis as the amount of debt increase on account of distress cost and other

ancillary cost. Further, there shall be benefit of trading on equity and investors seek excess return for their investment in equity.

The cost of capital under different capital structure has been presented here-in-below:

Case 1 - Risk Free Debt with Tax

Sl

NO % Debt/ % Equity Pretax Cost of Debt Pretax Cost of Equity Tax Post Tax Cost of Debt Cost of Equity Weight of Debt Weight of Equity WACC

1 0/100 5% 15%

40

% 3.0% 15% 0.00 1.00

15.00

%

2 10/90 5% 16.20%

40

% 3.0% 16% 0.10 0.90

14.88

%

3 20/80 5% 17.50%

40

% 3.0% 18% 0.20 0.80

14.60

%

4 30/70 5% 19.30%

40

% 3.0% 19% 0.30 0.70

14.41

%

5 40/60 5% 21.70%

40

% 3.0% 22% 0.40 0.60

14.22

%

6 50/50 5% 25%

40

% 3.0% 25% 0.50 0.50

14.00

%

7 60/40 5% 30%

40

% 3.0% 30% 0.60 0.40

13.80

%

8 70/30 5% 38.50%

40

% 3.0% 39% 0.70 0.30

13.65

%

9 80/20 5% 55%

40

% 3.0% 55% 0.80 0.20

13.40

%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

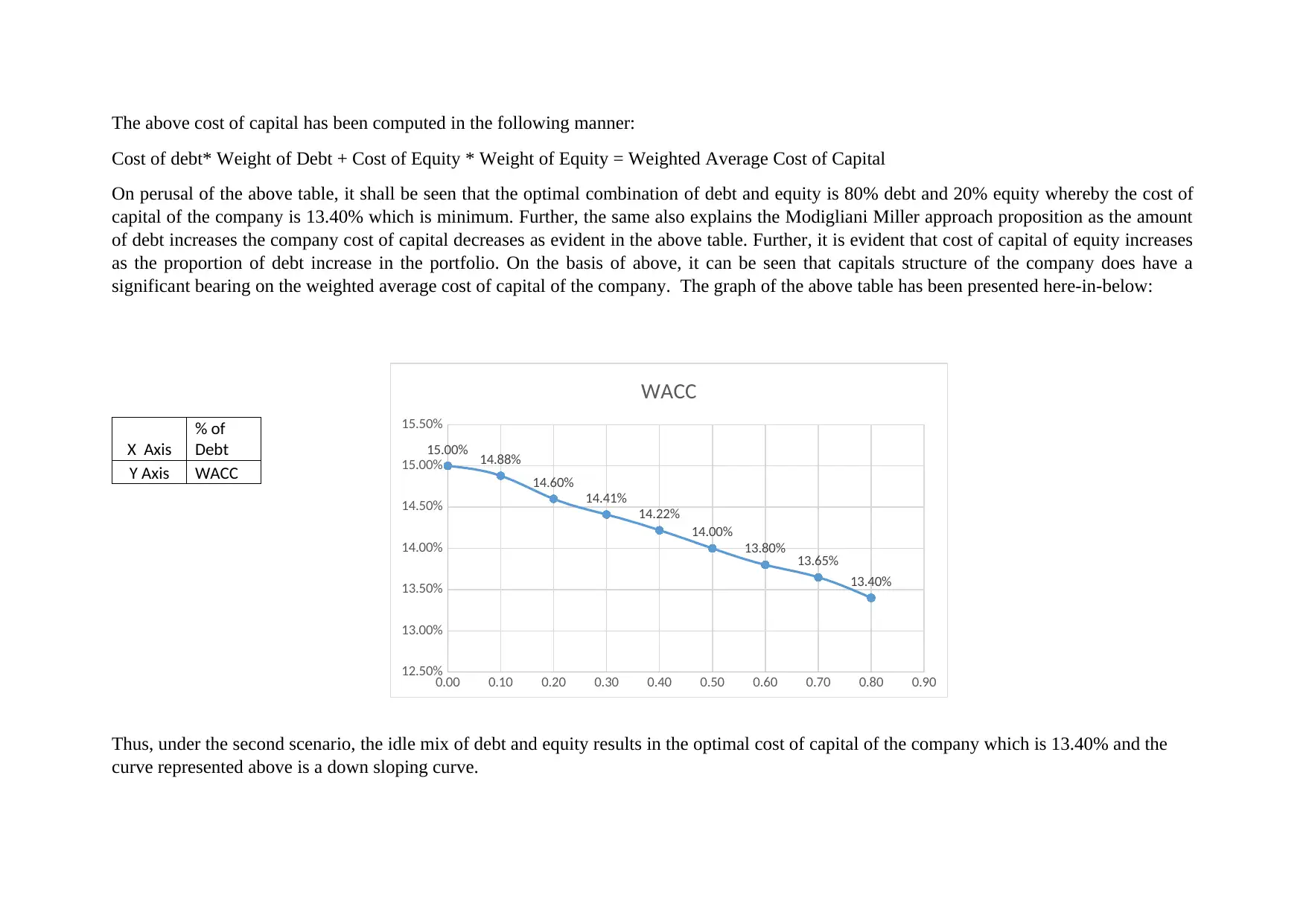

The above cost of capital has been computed in the following manner:

Cost of debt* Weight of Debt + Cost of Equity * Weight of Equity = Weighted Average Cost of Capital

On perusal of the above table, it shall be seen that the optimal combination of debt and equity is 80% debt and 20% equity whereby the cost of

capital of the company is 13.40% which is minimum. Further, the same also explains the Modigliani Miller approach proposition as the amount

of debt increases the company cost of capital decreases as evident in the above table. Further, it is evident that cost of capital of equity increases

as the proportion of debt increase in the portfolio. On the basis of above, it can be seen that capitals structure of the company does have a

significant bearing on the weighted average cost of capital of the company. The graph of the above table has been presented here-in-below:

X Axis

% of

Debt

Y Axis WACC

Thus, under the second scenario, the idle mix of debt and equity results in the optimal cost of capital of the company which is 13.40% and the

curve represented above is a down sloping curve.

0.00 0.10 0.20 0.30 0.40 0.50 0.60 0.70 0.80 0.90

12.50%

13.00%

13.50%

14.00%

14.50%

15.00%

15.50%

15.00% 14.88%

14.60%

14.41%

14.22%

14.00%

13.80% 13.65%

13.40%

WACC

Cost of debt* Weight of Debt + Cost of Equity * Weight of Equity = Weighted Average Cost of Capital

On perusal of the above table, it shall be seen that the optimal combination of debt and equity is 80% debt and 20% equity whereby the cost of

capital of the company is 13.40% which is minimum. Further, the same also explains the Modigliani Miller approach proposition as the amount

of debt increases the company cost of capital decreases as evident in the above table. Further, it is evident that cost of capital of equity increases

as the proportion of debt increase in the portfolio. On the basis of above, it can be seen that capitals structure of the company does have a

significant bearing on the weighted average cost of capital of the company. The graph of the above table has been presented here-in-below:

X Axis

% of

Debt

Y Axis WACC

Thus, under the second scenario, the idle mix of debt and equity results in the optimal cost of capital of the company which is 13.40% and the

curve represented above is a down sloping curve.

0.00 0.10 0.20 0.30 0.40 0.50 0.60 0.70 0.80 0.90

12.50%

13.00%

13.50%

14.00%

14.50%

15.00%

15.50%

15.00% 14.88%

14.60%

14.41%

14.22%

14.00%

13.80% 13.65%

13.40%

WACC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

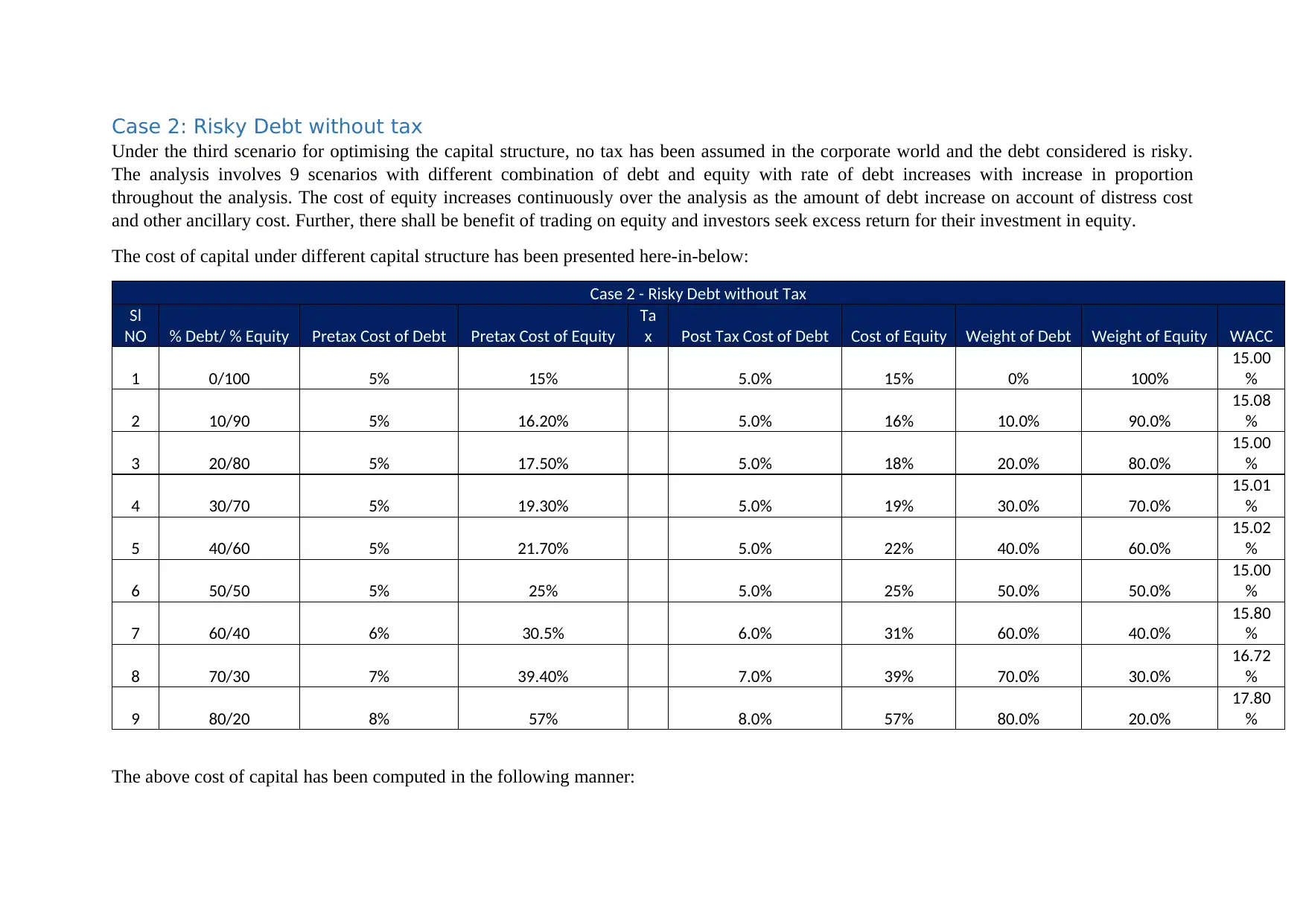

Case 2: Risky Debt without tax

Under the third scenario for optimising the capital structure, no tax has been assumed in the corporate world and the debt considered is risky.

The analysis involves 9 scenarios with different combination of debt and equity with rate of debt increases with increase in proportion

throughout the analysis. The cost of equity increases continuously over the analysis as the amount of debt increase on account of distress cost

and other ancillary cost. Further, there shall be benefit of trading on equity and investors seek excess return for their investment in equity.

The cost of capital under different capital structure has been presented here-in-below:

Case 2 - Risky Debt without Tax

Sl

NO % Debt/ % Equity Pretax Cost of Debt Pretax Cost of Equity

Ta

x Post Tax Cost of Debt Cost of Equity Weight of Debt Weight of Equity WACC

1 0/100 5% 15% 5.0% 15% 0% 100%

15.00

%

2 10/90 5% 16.20% 5.0% 16% 10.0% 90.0%

15.08

%

3 20/80 5% 17.50% 5.0% 18% 20.0% 80.0%

15.00

%

4 30/70 5% 19.30% 5.0% 19% 30.0% 70.0%

15.01

%

5 40/60 5% 21.70% 5.0% 22% 40.0% 60.0%

15.02

%

6 50/50 5% 25% 5.0% 25% 50.0% 50.0%

15.00

%

7 60/40 6% 30.5% 6.0% 31% 60.0% 40.0%

15.80

%

8 70/30 7% 39.40% 7.0% 39% 70.0% 30.0%

16.72

%

9 80/20 8% 57% 8.0% 57% 80.0% 20.0%

17.80

%

The above cost of capital has been computed in the following manner:

Under the third scenario for optimising the capital structure, no tax has been assumed in the corporate world and the debt considered is risky.

The analysis involves 9 scenarios with different combination of debt and equity with rate of debt increases with increase in proportion

throughout the analysis. The cost of equity increases continuously over the analysis as the amount of debt increase on account of distress cost

and other ancillary cost. Further, there shall be benefit of trading on equity and investors seek excess return for their investment in equity.

The cost of capital under different capital structure has been presented here-in-below:

Case 2 - Risky Debt without Tax

Sl

NO % Debt/ % Equity Pretax Cost of Debt Pretax Cost of Equity

Ta

x Post Tax Cost of Debt Cost of Equity Weight of Debt Weight of Equity WACC

1 0/100 5% 15% 5.0% 15% 0% 100%

15.00

%

2 10/90 5% 16.20% 5.0% 16% 10.0% 90.0%

15.08

%

3 20/80 5% 17.50% 5.0% 18% 20.0% 80.0%

15.00

%

4 30/70 5% 19.30% 5.0% 19% 30.0% 70.0%

15.01

%

5 40/60 5% 21.70% 5.0% 22% 40.0% 60.0%

15.02

%

6 50/50 5% 25% 5.0% 25% 50.0% 50.0%

15.00

%

7 60/40 6% 30.5% 6.0% 31% 60.0% 40.0%

15.80

%

8 70/30 7% 39.40% 7.0% 39% 70.0% 30.0%

16.72

%

9 80/20 8% 57% 8.0% 57% 80.0% 20.0%

17.80

%

The above cost of capital has been computed in the following manner:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

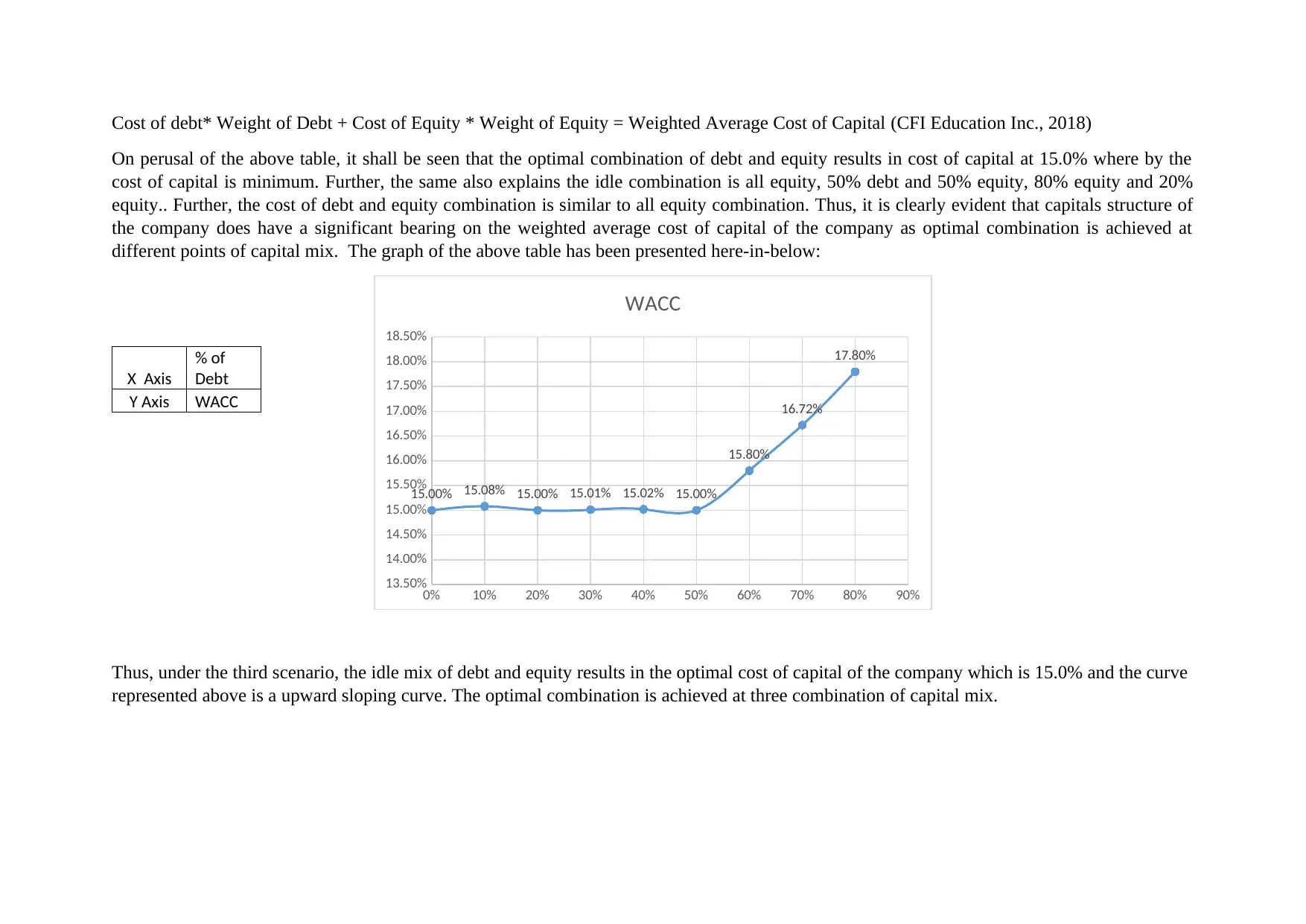

Cost of debt* Weight of Debt + Cost of Equity * Weight of Equity = Weighted Average Cost of Capital (CFI Education Inc., 2018)

On perusal of the above table, it shall be seen that the optimal combination of debt and equity results in cost of capital at 15.0% where by the

cost of capital is minimum. Further, the same also explains the idle combination is all equity, 50% debt and 50% equity, 80% equity and 20%

equity.. Further, the cost of debt and equity combination is similar to all equity combination. Thus, it is clearly evident that capitals structure of

the company does have a significant bearing on the weighted average cost of capital of the company as optimal combination is achieved at

different points of capital mix. The graph of the above table has been presented here-in-below:

X Axis

% of

Debt

Y Axis WACC

Thus, under the third scenario, the idle mix of debt and equity results in the optimal cost of capital of the company which is 15.0% and the curve

represented above is a upward sloping curve. The optimal combination is achieved at three combination of capital mix.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

13.50%

14.00%

14.50%

15.00%

15.50%

16.00%

16.50%

17.00%

17.50%

18.00%

18.50%

15.00% 15.08% 15.00% 15.01% 15.02% 15.00%

15.80%

16.72%

17.80%

WACC

On perusal of the above table, it shall be seen that the optimal combination of debt and equity results in cost of capital at 15.0% where by the

cost of capital is minimum. Further, the same also explains the idle combination is all equity, 50% debt and 50% equity, 80% equity and 20%

equity.. Further, the cost of debt and equity combination is similar to all equity combination. Thus, it is clearly evident that capitals structure of

the company does have a significant bearing on the weighted average cost of capital of the company as optimal combination is achieved at

different points of capital mix. The graph of the above table has been presented here-in-below:

X Axis

% of

Debt

Y Axis WACC

Thus, under the third scenario, the idle mix of debt and equity results in the optimal cost of capital of the company which is 15.0% and the curve

represented above is a upward sloping curve. The optimal combination is achieved at three combination of capital mix.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

13.50%

14.00%

14.50%

15.00%

15.50%

16.00%

16.50%

17.00%

17.50%

18.00%

18.50%

15.00% 15.08% 15.00% 15.01% 15.02% 15.00%

15.80%

16.72%

17.80%

WACC

Case 2: Risky Debt with tax

Under the second scenario for optimising the capital structure, tax has been assumed @40% in the corporate world and the debt considered is

risky. The analysis involves 9 scenarios with different combination of debt and equity with rate of debt increasing at different level of analysis.

The cost of equity increases continuously over the analysis as the amount of debt increase on account of distress cost and other ancillary cost.

Further, there shall be benefit of trading on equity and investors seek excess return for their investment in equity.

The cost of capital under different capital structure has been presented here-in-below:

Case 2 - Risky Debt with Tax

Sl

NO % Debt/ % Equity Pretax Cost of Debt Pretax Cost of Equity Tax Post Tax Cost of Debt Cost of Equity Weight of Debt Weight of Equity WACC

1 0/100 5% 15%

40

% 3.0% 15% 0% 100%

15.00

%

2 10/90 5% 16.20%

40

% 3.0% 16% 10.0% 90.0%

14.88

%

3 20/80 5% 17.50%

40

% 3.0% 18% 20.0% 80.0%

14.60

%

4 30/70 5% 19.30%

40

% 3.0% 19% 30.0% 70.0%

14.41

%

5 40/60 5% 21.70%

40

% 3.0% 22% 40.0% 60.0%

14.22

%

6 50/50 5% 25%

40

% 3.0% 25% 50.0% 50.0%

14.00

%

7 60/40 6% 30.5%

40

% 3.6% 31% 60.0% 40.0%

14.36

%

8 70/30 7% 39.40%

40

% 4.2% 39% 70.0% 30.0%

14.76

%

9 80/20 8% 57%

40

% 4.8% 57% 80.0% 20.0%

15.24

%

Under the second scenario for optimising the capital structure, tax has been assumed @40% in the corporate world and the debt considered is

risky. The analysis involves 9 scenarios with different combination of debt and equity with rate of debt increasing at different level of analysis.

The cost of equity increases continuously over the analysis as the amount of debt increase on account of distress cost and other ancillary cost.

Further, there shall be benefit of trading on equity and investors seek excess return for their investment in equity.

The cost of capital under different capital structure has been presented here-in-below:

Case 2 - Risky Debt with Tax

Sl

NO % Debt/ % Equity Pretax Cost of Debt Pretax Cost of Equity Tax Post Tax Cost of Debt Cost of Equity Weight of Debt Weight of Equity WACC

1 0/100 5% 15%

40

% 3.0% 15% 0% 100%

15.00

%

2 10/90 5% 16.20%

40

% 3.0% 16% 10.0% 90.0%

14.88

%

3 20/80 5% 17.50%

40

% 3.0% 18% 20.0% 80.0%

14.60

%

4 30/70 5% 19.30%

40

% 3.0% 19% 30.0% 70.0%

14.41

%

5 40/60 5% 21.70%

40

% 3.0% 22% 40.0% 60.0%

14.22

%

6 50/50 5% 25%

40

% 3.0% 25% 50.0% 50.0%

14.00

%

7 60/40 6% 30.5%

40

% 3.6% 31% 60.0% 40.0%

14.36

%

8 70/30 7% 39.40%

40

% 4.2% 39% 70.0% 30.0%

14.76

%

9 80/20 8% 57%

40

% 4.8% 57% 80.0% 20.0%

15.24

%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.