Finance for Global Business: Investment Appraisal of Fitness Guru PLC

VerifiedAdded on 2020/07/22

|13

|2600

|36

Report

AI Summary

This report provides a detailed financial analysis of Fitness Guru PLC, focusing on investment appraisal techniques, financing options, and risk management strategies. It begins by calculating revenues, costs, and profits to determine cash inflows and outflows, followed by discounted cash flow analysis, including Net Present Value (NPV) and Payback Period calculations, to assess the viability of a project. The report also analyzes the company's cost of capital, including the cost of equity and debt, and calculates the Weighted Average Cost of Capital (WACC). Furthermore, it explores different financing options such as debt and equity funds, trade-off theory, and pecking order theory. Finally, the report addresses potential risks, including foreign exchange risk, interest rate risk, leverage risk, and transaction risk, and advises the company on managing these risks effectively. The conclusion summarizes the key findings and recommendations based on the financial analysis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance for Global Business

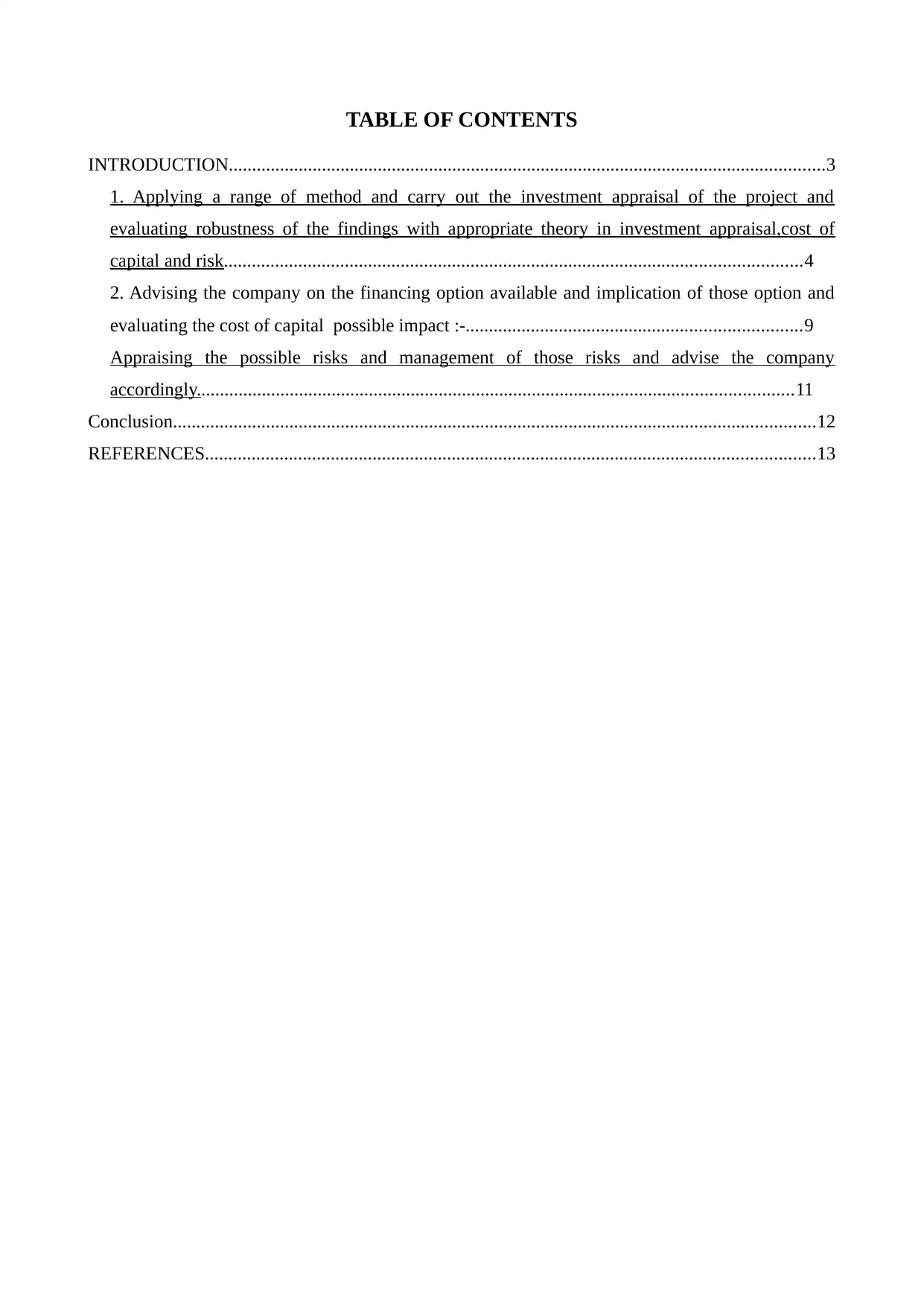

TABLE OF CONTENTS

INTRODUCTION................................................................................................................................3

1. Applying a range of method and carry out the investment appraisal of the project and

evaluating robustness of the findings with appropriate theory in investment appraisal,cost of

capital and risk............................................................................................................................4

2. Advising the company on the financing option available and implication of those option and

evaluating the cost of capital possible impact :-........................................................................9

Appraising the possible risks and management of those risks and advise the company

accordingly................................................................................................................................11

Conclusion..........................................................................................................................................12

REFERENCES...................................................................................................................................13

INTRODUCTION................................................................................................................................3

1. Applying a range of method and carry out the investment appraisal of the project and

evaluating robustness of the findings with appropriate theory in investment appraisal,cost of

capital and risk............................................................................................................................4

2. Advising the company on the financing option available and implication of those option and

evaluating the cost of capital possible impact :-........................................................................9

Appraising the possible risks and management of those risks and advise the company

accordingly................................................................................................................................11

Conclusion..........................................................................................................................................12

REFERENCES...................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial management means planning, organizing, directing, controlling of financial

activities for as procurement and optimum utilization of resources of the organisation. Finance is a

field that contains topics such as landing of money and greater return on the funds. Finance allows a

company to pay debt and expenditure without giving the ownership right. Finance is needed in to

promote business strategies, acquiring fixed assets in global scenario. In this context fitness guru plc

stats the investment appraisal and evaluating of the result including the assumption and techniques

with respect to appropriate theory which are helpful in identification and evaluation of additional

risk.

Financial management means planning, organizing, directing, controlling of financial

activities for as procurement and optimum utilization of resources of the organisation. Finance is a

field that contains topics such as landing of money and greater return on the funds. Finance allows a

company to pay debt and expenditure without giving the ownership right. Finance is needed in to

promote business strategies, acquiring fixed assets in global scenario. In this context fitness guru plc

stats the investment appraisal and evaluating of the result including the assumption and techniques

with respect to appropriate theory which are helpful in identification and evaluation of additional

risk.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SECTION A

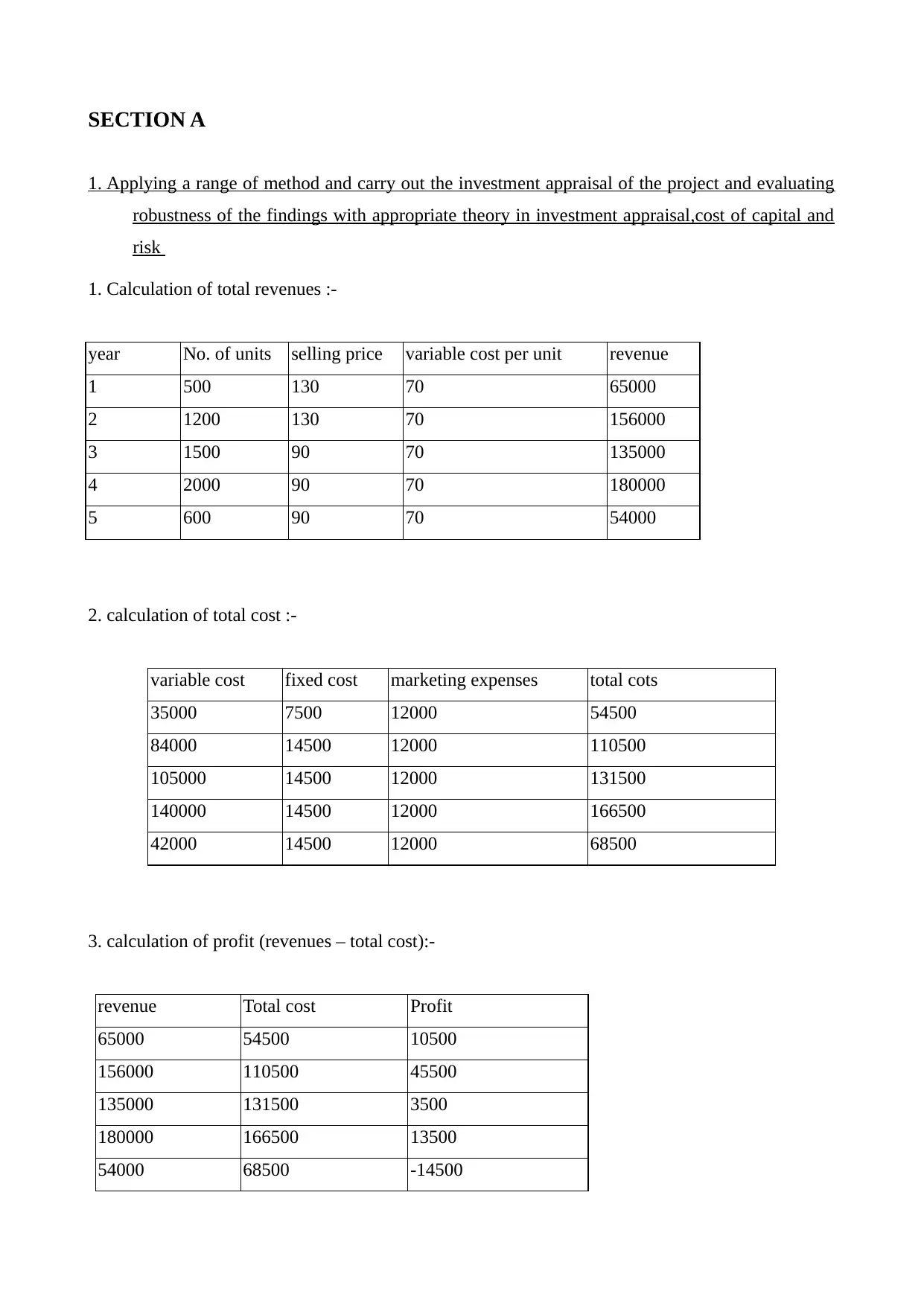

1. Applying a range of method and carry out the investment appraisal of the project and evaluating

robustness of the findings with appropriate theory in investment appraisal,cost of capital and

risk

1. Calculation of total revenues :-

year No. of units selling price variable cost per unit revenue

1 500 130 70 65000

2 1200 130 70 156000

3 1500 90 70 135000

4 2000 90 70 180000

5 600 90 70 54000

2. calculation of total cost :-

variable cost fixed cost marketing expenses total cots

35000 7500 12000 54500

84000 14500 12000 110500

105000 14500 12000 131500

140000 14500 12000 166500

42000 14500 12000 68500

3. calculation of profit (revenues – total cost):-

revenue Total cost Profit

65000 54500 10500

156000 110500 45500

135000 131500 3500

180000 166500 13500

54000 68500 -14500

1. Applying a range of method and carry out the investment appraisal of the project and evaluating

robustness of the findings with appropriate theory in investment appraisal,cost of capital and

risk

1. Calculation of total revenues :-

year No. of units selling price variable cost per unit revenue

1 500 130 70 65000

2 1200 130 70 156000

3 1500 90 70 135000

4 2000 90 70 180000

5 600 90 70 54000

2. calculation of total cost :-

variable cost fixed cost marketing expenses total cots

35000 7500 12000 54500

84000 14500 12000 110500

105000 14500 12000 131500

140000 14500 12000 166500

42000 14500 12000 68500

3. calculation of profit (revenues – total cost):-

revenue Total cost Profit

65000 54500 10500

156000 110500 45500

135000 131500 3500

180000 166500 13500

54000 68500 -14500

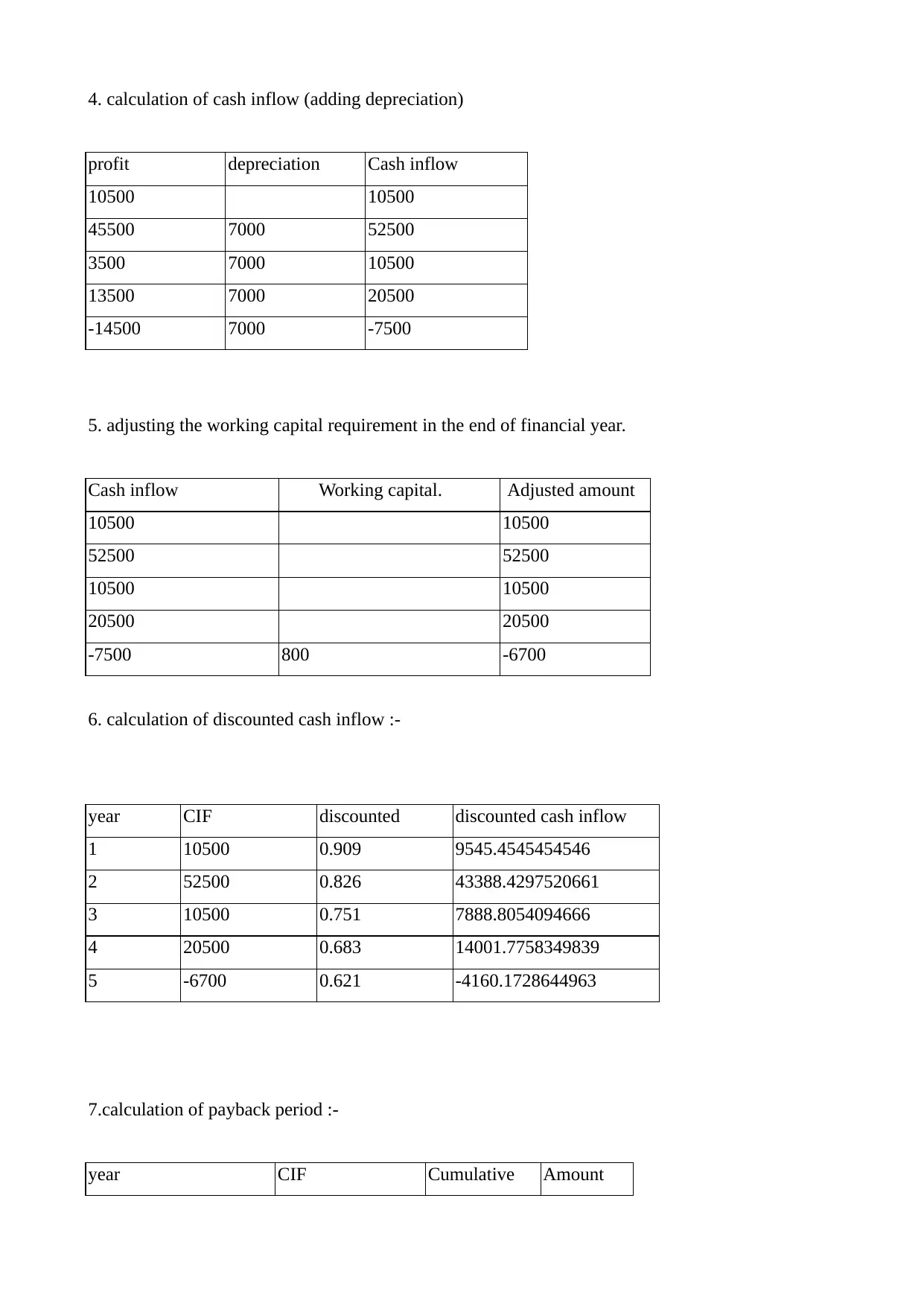

4. calculation of cash inflow (adding depreciation)

profit depreciation Cash inflow

10500 10500

45500 7000 52500

3500 7000 10500

13500 7000 20500

-14500 7000 -7500

5. adjusting the working capital requirement in the end of financial year.

Cash inflow Working capital. Adjusted amount

10500 10500

52500 52500

10500 10500

20500 20500

-7500 800 -6700

6. calculation of discounted cash inflow :-

year CIF discounted discounted cash inflow

1 10500 0.909 9545.4545454546

2 52500 0.826 43388.4297520661

3 10500 0.751 7888.8054094666

4 20500 0.683 14001.7758349839

5 -6700 0.621 -4160.1728644963

7.calculation of payback period :-

year CIF Cumulative Amount

profit depreciation Cash inflow

10500 10500

45500 7000 52500

3500 7000 10500

13500 7000 20500

-14500 7000 -7500

5. adjusting the working capital requirement in the end of financial year.

Cash inflow Working capital. Adjusted amount

10500 10500

52500 52500

10500 10500

20500 20500

-7500 800 -6700

6. calculation of discounted cash inflow :-

year CIF discounted discounted cash inflow

1 10500 0.909 9545.4545454546

2 52500 0.826 43388.4297520661

3 10500 0.751 7888.8054094666

4 20500 0.683 14001.7758349839

5 -6700 0.621 -4160.1728644963

7.calculation of payback period :-

year CIF Cumulative Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

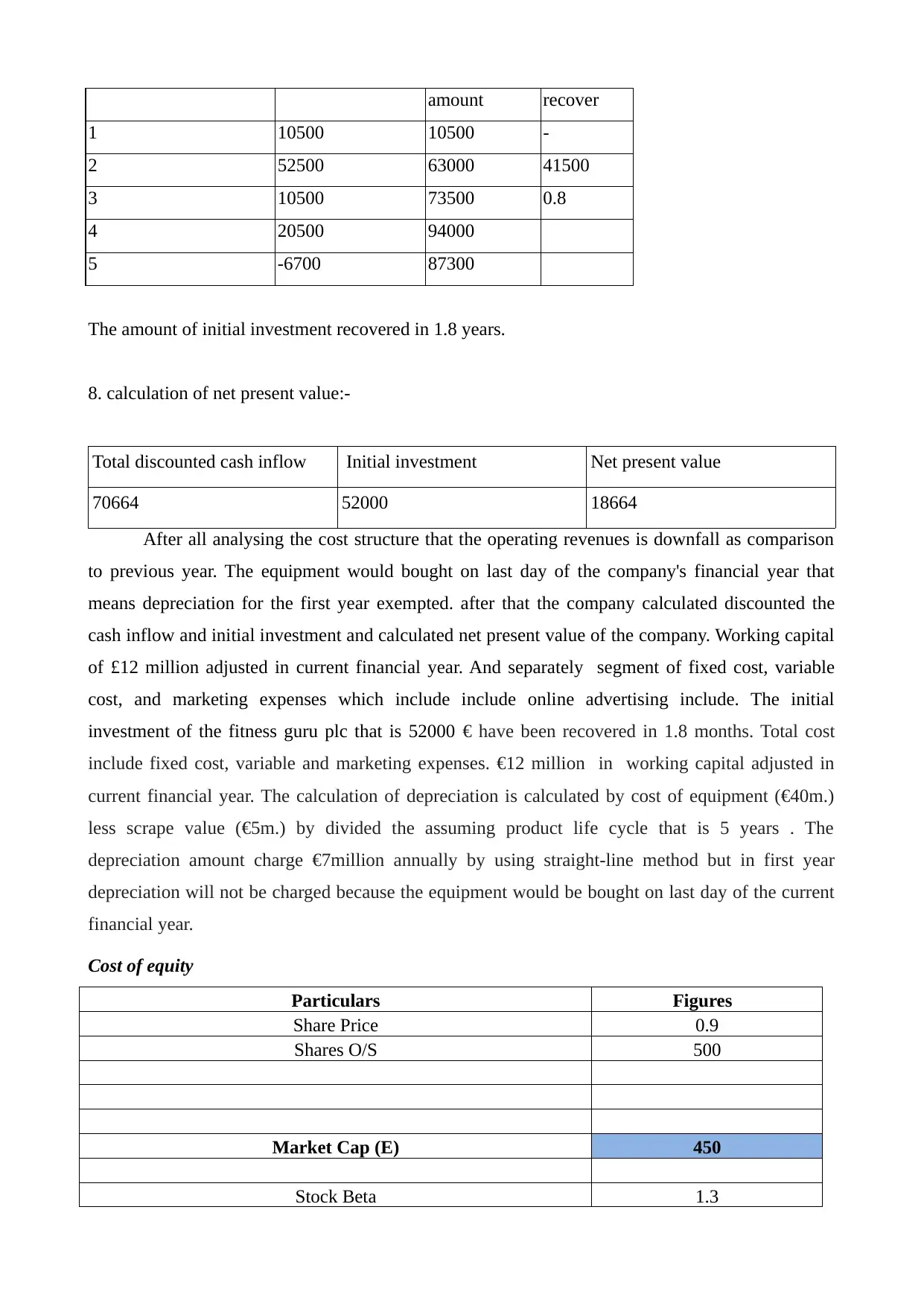

amount recover

1 10500 10500 -

2 52500 63000 41500

3 10500 73500 0.8

4 20500 94000

5 -6700 87300

The amount of initial investment recovered in 1.8 years.

8. calculation of net present value:-

Total discounted cash inflow Initial investment Net present value

70664 52000 18664

After all analysing the cost structure that the operating revenues is downfall as comparison

to previous year. The equipment would bought on last day of the company's financial year that

means depreciation for the first year exempted. after that the company calculated discounted the

cash inflow and initial investment and calculated net present value of the company. Working capital

of £12 million adjusted in current financial year. And separately segment of fixed cost, variable

cost, and marketing expenses which include include online advertising include. The initial

investment of the fitness guru plc that is 52000 € have been recovered in 1.8 months. Total cost

include fixed cost, variable and marketing expenses. €12 million in working capital adjusted in

current financial year. The calculation of depreciation is calculated by cost of equipment (€40m.)

less scrape value (€5m.) by divided the assuming product life cycle that is 5 years . The

depreciation amount charge €7million annually by using straight-line method but in first year

depreciation will not be charged because the equipment would be bought on last day of the current

financial year.

Cost of equity

Particulars Figures

Share Price 0.9

Shares O/S 500

Market Cap (E) 450

Stock Beta 1.3

1 10500 10500 -

2 52500 63000 41500

3 10500 73500 0.8

4 20500 94000

5 -6700 87300

The amount of initial investment recovered in 1.8 years.

8. calculation of net present value:-

Total discounted cash inflow Initial investment Net present value

70664 52000 18664

After all analysing the cost structure that the operating revenues is downfall as comparison

to previous year. The equipment would bought on last day of the company's financial year that

means depreciation for the first year exempted. after that the company calculated discounted the

cash inflow and initial investment and calculated net present value of the company. Working capital

of £12 million adjusted in current financial year. And separately segment of fixed cost, variable

cost, and marketing expenses which include include online advertising include. The initial

investment of the fitness guru plc that is 52000 € have been recovered in 1.8 months. Total cost

include fixed cost, variable and marketing expenses. €12 million in working capital adjusted in

current financial year. The calculation of depreciation is calculated by cost of equipment (€40m.)

less scrape value (€5m.) by divided the assuming product life cycle that is 5 years . The

depreciation amount charge €7million annually by using straight-line method but in first year

depreciation will not be charged because the equipment would be bought on last day of the current

financial year.

Cost of equity

Particulars Figures

Share Price 0.9

Shares O/S 500

Market Cap (E) 450

Stock Beta 1.3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

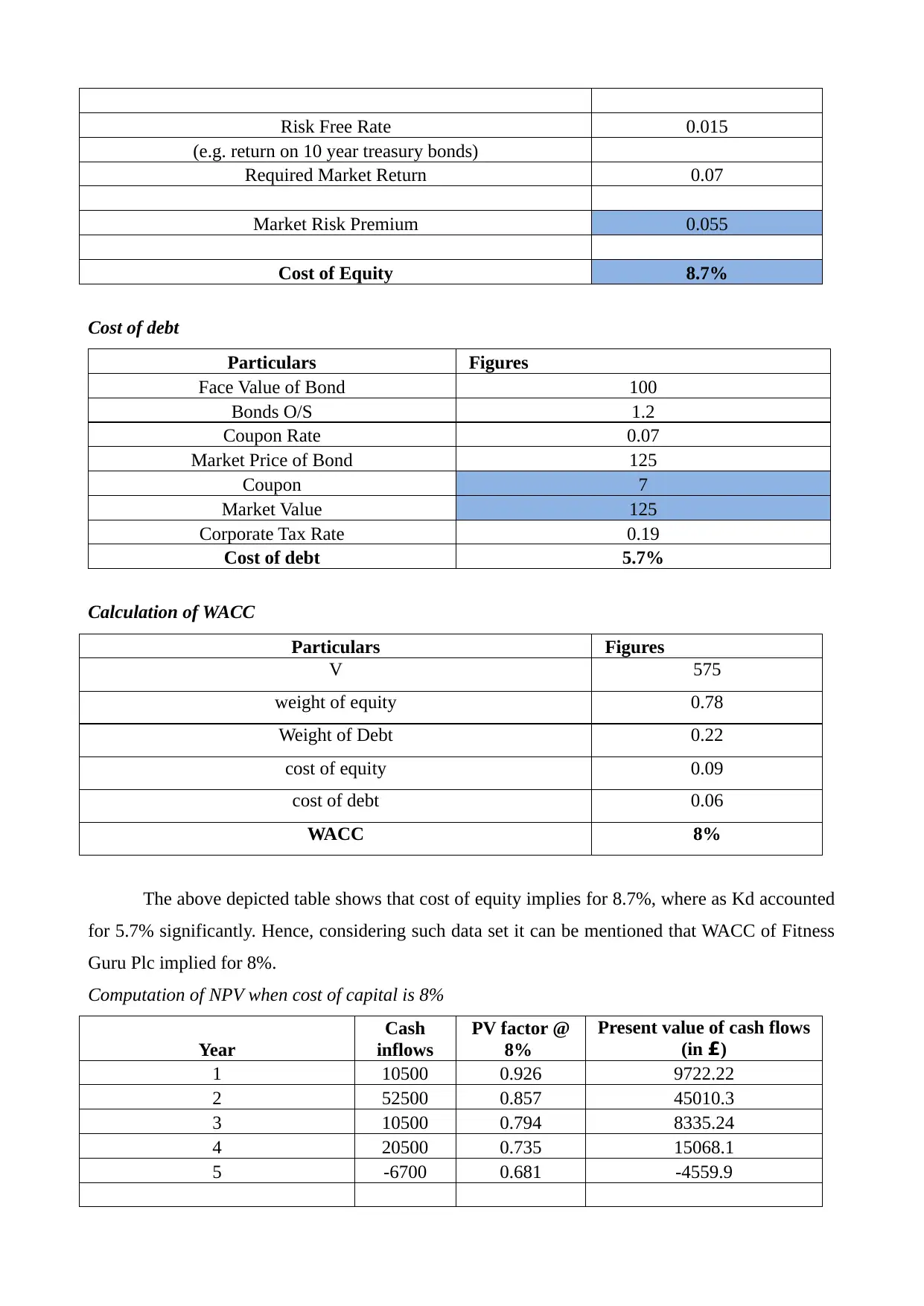

Risk Free Rate 0.015

(e.g. return on 10 year treasury bonds)

Required Market Return 0.07

Market Risk Premium 0.055

Cost of Equity 8.7%

Cost of debt

Particulars Figures

Face Value of Bond 100

Bonds O/S 1.2

Coupon Rate 0.07

Market Price of Bond 125

Coupon 7

Market Value 125

Corporate Tax Rate 0.19

Cost of debt 5.7%

Calculation of WACC

Particulars Figures

V 575

weight of equity 0.78

Weight of Debt 0.22

cost of equity 0.09

cost of debt 0.06

WACC 8%

The above depicted table shows that cost of equity implies for 8.7%, where as Kd accounted

for 5.7% significantly. Hence, considering such data set it can be mentioned that WACC of Fitness

Guru Plc implied for 8%.

Computation of NPV when cost of capital is 8%

Year

Cash

inflows

PV factor @

8%

Present value of cash flows

(in £)

1 10500 0.926 9722.22

2 52500 0.857 45010.3

3 10500 0.794 8335.24

4 20500 0.735 15068.1

5 -6700 0.681 -4559.9

(e.g. return on 10 year treasury bonds)

Required Market Return 0.07

Market Risk Premium 0.055

Cost of Equity 8.7%

Cost of debt

Particulars Figures

Face Value of Bond 100

Bonds O/S 1.2

Coupon Rate 0.07

Market Price of Bond 125

Coupon 7

Market Value 125

Corporate Tax Rate 0.19

Cost of debt 5.7%

Calculation of WACC

Particulars Figures

V 575

weight of equity 0.78

Weight of Debt 0.22

cost of equity 0.09

cost of debt 0.06

WACC 8%

The above depicted table shows that cost of equity implies for 8.7%, where as Kd accounted

for 5.7% significantly. Hence, considering such data set it can be mentioned that WACC of Fitness

Guru Plc implied for 8%.

Computation of NPV when cost of capital is 8%

Year

Cash

inflows

PV factor @

8%

Present value of cash flows

(in £)

1 10500 0.926 9722.22

2 52500 0.857 45010.3

3 10500 0.794 8335.24

4 20500 0.735 15068.1

5 -6700 0.681 -4559.9

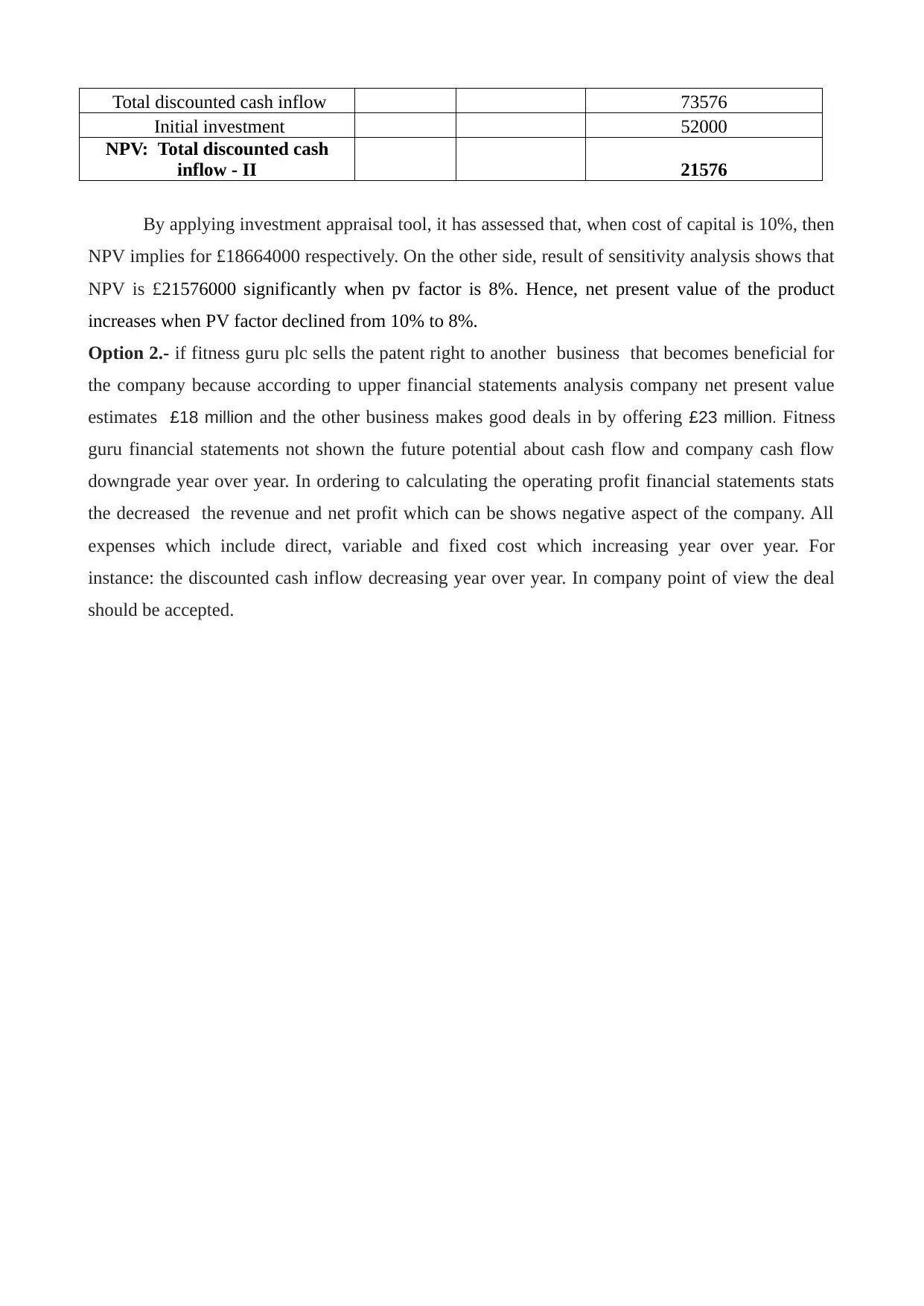

Total discounted cash inflow 73576

Initial investment 52000

NPV: Total discounted cash

inflow - II 21576

By applying investment appraisal tool, it has assessed that, when cost of capital is 10%, then

NPV implies for £18664000 respectively. On the other side, result of sensitivity analysis shows that

NPV is £21576000 significantly when pv factor is 8%. Hence, net present value of the product

increases when PV factor declined from 10% to 8%.

Option 2.- if fitness guru plc sells the patent right to another business that becomes beneficial for

the company because according to upper financial statements analysis company net present value

estimates £18 million and the other business makes good deals in by offering £23 million. Fitness

guru financial statements not shown the future potential about cash flow and company cash flow

downgrade year over year. In ordering to calculating the operating profit financial statements stats

the decreased the revenue and net profit which can be shows negative aspect of the company. All

expenses which include direct, variable and fixed cost which increasing year over year. For

instance: the discounted cash inflow decreasing year over year. In company point of view the deal

should be accepted.

Initial investment 52000

NPV: Total discounted cash

inflow - II 21576

By applying investment appraisal tool, it has assessed that, when cost of capital is 10%, then

NPV implies for £18664000 respectively. On the other side, result of sensitivity analysis shows that

NPV is £21576000 significantly when pv factor is 8%. Hence, net present value of the product

increases when PV factor declined from 10% to 8%.

Option 2.- if fitness guru plc sells the patent right to another business that becomes beneficial for

the company because according to upper financial statements analysis company net present value

estimates £18 million and the other business makes good deals in by offering £23 million. Fitness

guru financial statements not shown the future potential about cash flow and company cash flow

downgrade year over year. In ordering to calculating the operating profit financial statements stats

the decreased the revenue and net profit which can be shows negative aspect of the company. All

expenses which include direct, variable and fixed cost which increasing year over year. For

instance: the discounted cash inflow decreasing year over year. In company point of view the deal

should be accepted.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SECTION B

2. Advising the company on the financing option available and implication of those option and

evaluating the cost of capital possible impact :-

Debt and equity fund:- after the analysing the financial statement company can use the debt

equity fund. The total liabilities of the company is 370 m And shareholders equities in company as

£ 250. for calculating the debt equity ratio :- total liabilities/ shareholders equities that means

1.48%. debt equity may include all long term debt and also exclude long term debt near maturity

period. Debt fund include fixed instruments like government bonds, non convertible debenture

(Jakhotiya, 2002). for instance in balance sheet fitness guru have a government bond is currently

trading £0.9. the ideal ratio between debt & equity is .5:1 that shows company stability.

Trade off theory:- in trade of theory fitness guru plc can choose how much cost of debt

finance and equity finance to use by the maintaining the cost and benefits. It explain the financially

partly with debt and partly with equity. It indicating the advantage the financing along with debt.

Trade of theory states that capital structure is trade off among the savings and distress cost of debt.

Fitness guru plc have higher debt ratio which can be not capable for payment in long term debt.

This theory determined by a single period trade off among the tax benefits of debt and the cost of

bankruptcy (Kawai, Mayes and Morgan, 2012). By adopting this theory helped in cost benefits,

trade of between debt and equity, tax saving and direct cost. Trade-off theory directly effect upon

company's debt level:- increase in financial distress, increase in the debt level at optimal capital

structure.

pecking order theory :- it stats the cost of financing increase with asymmetric information.

Hierarchy of pecking order theory depends upon three factors which consists:-1. Internal financing

2.external financing debt 3.external financing equities. This hierarchy help to risk increase so cost

of finance increase. Lopsided information favours the issue of debt over equity as the issue of debt

signals. In this theory there are three sources of funding available to the organization Retained

earning, debt and the equity .retained earning have not untoward selection problem. Equity that

contains to untoward selection problems while debt refers to minor untoward problem (Kunc and

Bhandari, 2011). This theory assumes that there is no target capital structure. Due to untoward

company prefer internal and external finance. By adopting this strategies fitness guru plc can

differentiate the inverse relationship between debt ratios and profitability. This strategies

emphasizes on internal financing and dividend payout ratios of their investment opportunities .

Sticky dividend policy means overall internally cash flow generated. If external finance is

compulsory that means company issues safety security first.

2. Advising the company on the financing option available and implication of those option and

evaluating the cost of capital possible impact :-

Debt and equity fund:- after the analysing the financial statement company can use the debt

equity fund. The total liabilities of the company is 370 m And shareholders equities in company as

£ 250. for calculating the debt equity ratio :- total liabilities/ shareholders equities that means

1.48%. debt equity may include all long term debt and also exclude long term debt near maturity

period. Debt fund include fixed instruments like government bonds, non convertible debenture

(Jakhotiya, 2002). for instance in balance sheet fitness guru have a government bond is currently

trading £0.9. the ideal ratio between debt & equity is .5:1 that shows company stability.

Trade off theory:- in trade of theory fitness guru plc can choose how much cost of debt

finance and equity finance to use by the maintaining the cost and benefits. It explain the financially

partly with debt and partly with equity. It indicating the advantage the financing along with debt.

Trade of theory states that capital structure is trade off among the savings and distress cost of debt.

Fitness guru plc have higher debt ratio which can be not capable for payment in long term debt.

This theory determined by a single period trade off among the tax benefits of debt and the cost of

bankruptcy (Kawai, Mayes and Morgan, 2012). By adopting this theory helped in cost benefits,

trade of between debt and equity, tax saving and direct cost. Trade-off theory directly effect upon

company's debt level:- increase in financial distress, increase in the debt level at optimal capital

structure.

pecking order theory :- it stats the cost of financing increase with asymmetric information.

Hierarchy of pecking order theory depends upon three factors which consists:-1. Internal financing

2.external financing debt 3.external financing equities. This hierarchy help to risk increase so cost

of finance increase. Lopsided information favours the issue of debt over equity as the issue of debt

signals. In this theory there are three sources of funding available to the organization Retained

earning, debt and the equity .retained earning have not untoward selection problem. Equity that

contains to untoward selection problems while debt refers to minor untoward problem (Kunc and

Bhandari, 2011). This theory assumes that there is no target capital structure. Due to untoward

company prefer internal and external finance. By adopting this strategies fitness guru plc can

differentiate the inverse relationship between debt ratios and profitability. This strategies

emphasizes on internal financing and dividend payout ratios of their investment opportunities .

Sticky dividend policy means overall internally cash flow generated. If external finance is

compulsory that means company issues safety security first.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Retained profit:- retained earnings is a long term internal source of finance for a company

there is no compulsory methods like term loans and debenture. No additional equity issued or not

transfer of ownership. in retained profit there is no fixed obligation of interest and periodically basis

payment. Internally sources of finance retained earnings are cost effective and get better internal

rate of return as compare to return on investment (Thomas, 2009). Assuming that the generated

funds are belonging to shareholders so that cost of fund becomes equivalent to equity.

there is no compulsory methods like term loans and debenture. No additional equity issued or not

transfer of ownership. in retained profit there is no fixed obligation of interest and periodically basis

payment. Internally sources of finance retained earnings are cost effective and get better internal

rate of return as compare to return on investment (Thomas, 2009). Assuming that the generated

funds are belonging to shareholders so that cost of fund becomes equivalent to equity.

SECTION C

Appraising the possible risks and management of those risks and advise the company accordingly.

Foreign exchange risk it means when a financial transaction is put forward in a monetary

system other than that of the base currency of the company. If fitness guru plc importing the

component part in euros that may influence by many factors:-

1. Exchange rate risk :- this risk be caused by volatile movement in globally market by

supply and demand power of foreign exchange market. For the certain time period traders

position is superior and subject to all price changes. Forex is mostly unregulated and no

daily price are limited and exist for the future exchange. For instance fitness guru can import

cheaper component from the Belgium which gave him good offering price but with future

instability by the global marke. Fitness guru plc can trying to control exchange rate risk by

measuring their intended gain against possible outcomes.

2. Interest rate risk :- if the country interest rates high that means the exporter county

dominant the other country (Newell and Seabrook, 2006). For instance if Belgium

government induce new EXIM policy that may cause be hike price in component which

fitness guru import from belgium. In nature of interest rate risk roundabout effect of

exchange rates. The difference between currency value can be reason to downfall of forex

prices change.

3. Leverage risk :- this required a small investment known as margin to gain access for

substantial trades in foreign market. Small prices fluctuation causes by margin calls where

the fitness guru may pay an additional margin that may be causes by during the volatile

market position.

4. Transaction risk :- this risk associated with rime period that may cause in the beginning of

the contract and when the deal is locked. Currencies may be traded at a different prices at

different time period. The greater time settling in a contract that can be cause the higher

transaction risk. A currency crisis can occurred due to frequent balance of payment and

bring negative and deficit valuation in currencies (Peirson and et.al., 2014). Foreign

exchange trading may be larger then the initially renounced and while forex assets have

higher trading risk that can be caused to transaction risk.

5. Counterparty risk :- this may be caused by risk of bankruptcy of dealer or brokers in a

particular transaction. In forex trades future and pot market on currencies not bonded by an

transaction. In time of volatile conditions the counter party may be not capable to match to

Appraising the possible risks and management of those risks and advise the company accordingly.

Foreign exchange risk it means when a financial transaction is put forward in a monetary

system other than that of the base currency of the company. If fitness guru plc importing the

component part in euros that may influence by many factors:-

1. Exchange rate risk :- this risk be caused by volatile movement in globally market by

supply and demand power of foreign exchange market. For the certain time period traders

position is superior and subject to all price changes. Forex is mostly unregulated and no

daily price are limited and exist for the future exchange. For instance fitness guru can import

cheaper component from the Belgium which gave him good offering price but with future

instability by the global marke. Fitness guru plc can trying to control exchange rate risk by

measuring their intended gain against possible outcomes.

2. Interest rate risk :- if the country interest rates high that means the exporter county

dominant the other country (Newell and Seabrook, 2006). For instance if Belgium

government induce new EXIM policy that may cause be hike price in component which

fitness guru import from belgium. In nature of interest rate risk roundabout effect of

exchange rates. The difference between currency value can be reason to downfall of forex

prices change.

3. Leverage risk :- this required a small investment known as margin to gain access for

substantial trades in foreign market. Small prices fluctuation causes by margin calls where

the fitness guru may pay an additional margin that may be causes by during the volatile

market position.

4. Transaction risk :- this risk associated with rime period that may cause in the beginning of

the contract and when the deal is locked. Currencies may be traded at a different prices at

different time period. The greater time settling in a contract that can be cause the higher

transaction risk. A currency crisis can occurred due to frequent balance of payment and

bring negative and deficit valuation in currencies (Peirson and et.al., 2014). Foreign

exchange trading may be larger then the initially renounced and while forex assets have

higher trading risk that can be caused to transaction risk.

5. Counterparty risk :- this may be caused by risk of bankruptcy of dealer or brokers in a

particular transaction. In forex trades future and pot market on currencies not bonded by an

transaction. In time of volatile conditions the counter party may be not capable to match to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.