University of Hong Kong: MFIN7012 Fixed Income Assignment Solution

VerifiedAdded on 2022/09/12

|8

|342

|16

Homework Assignment

AI Summary

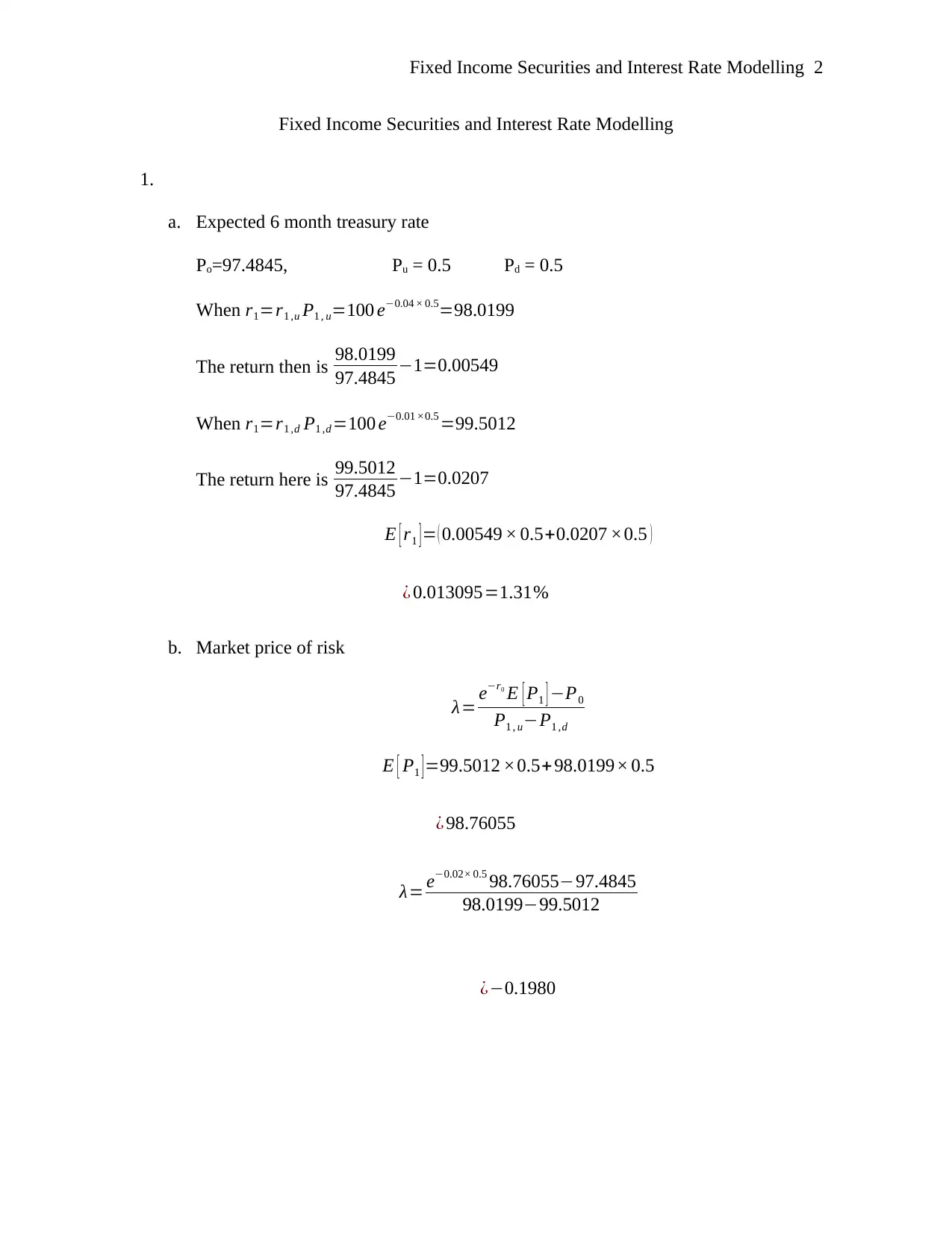

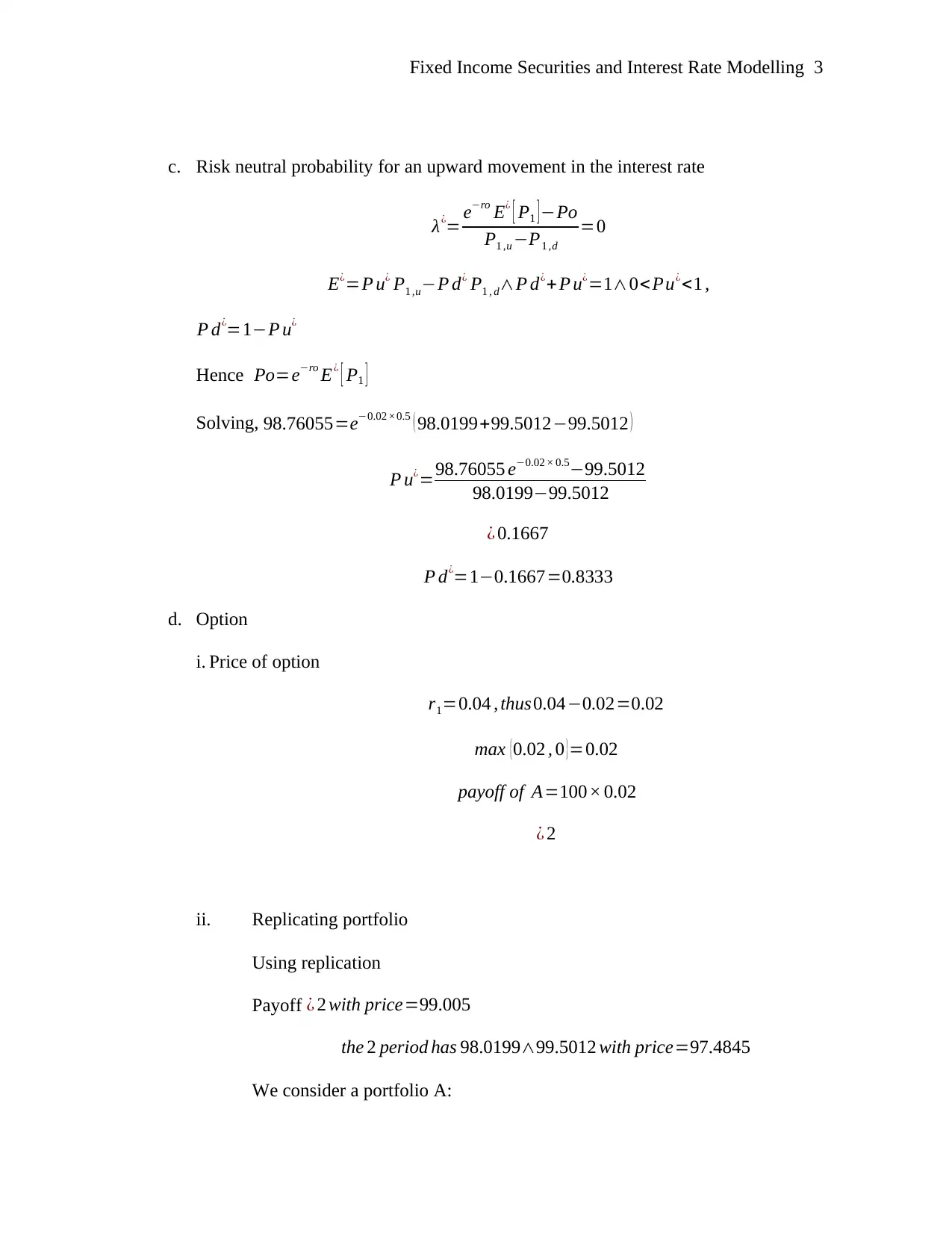

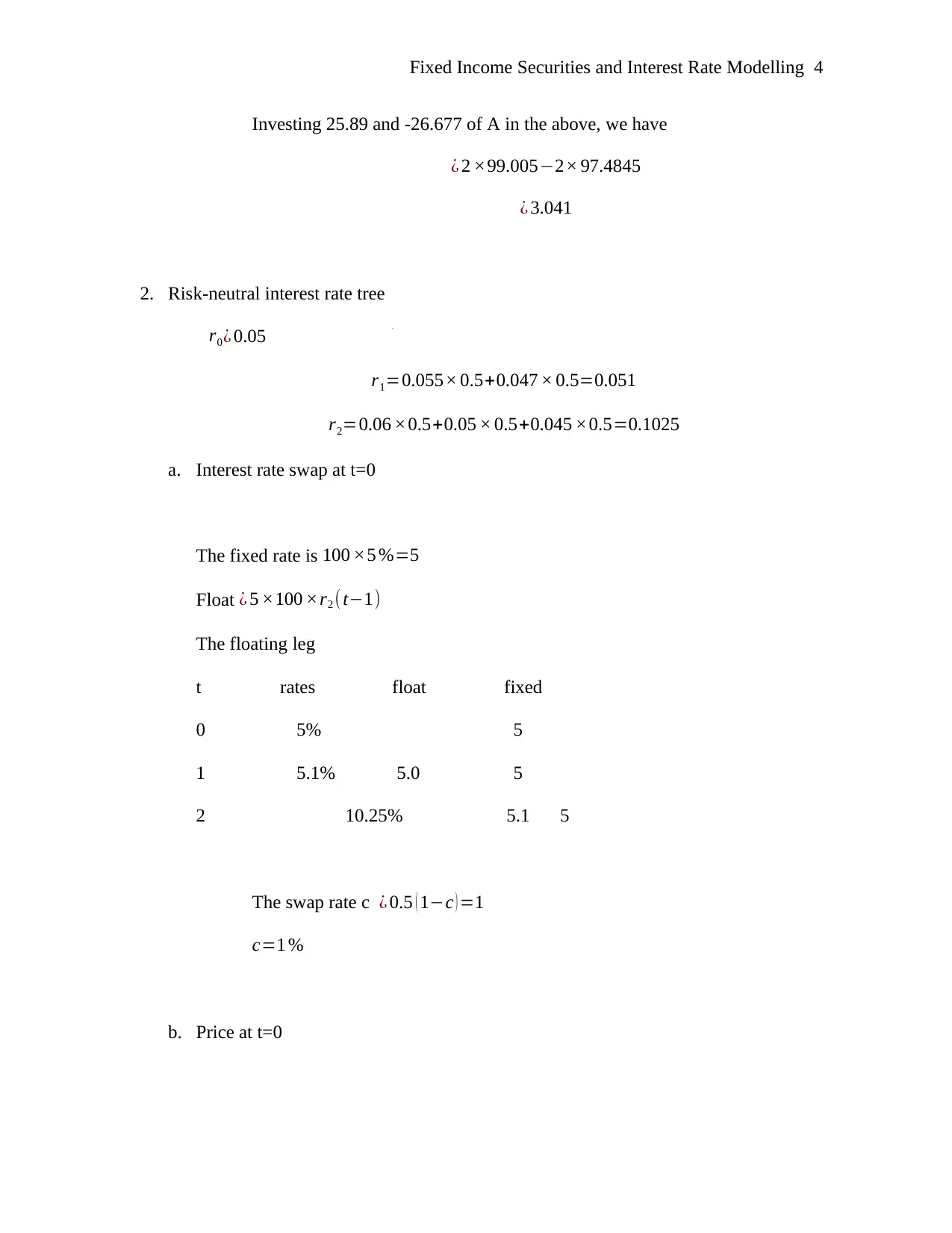

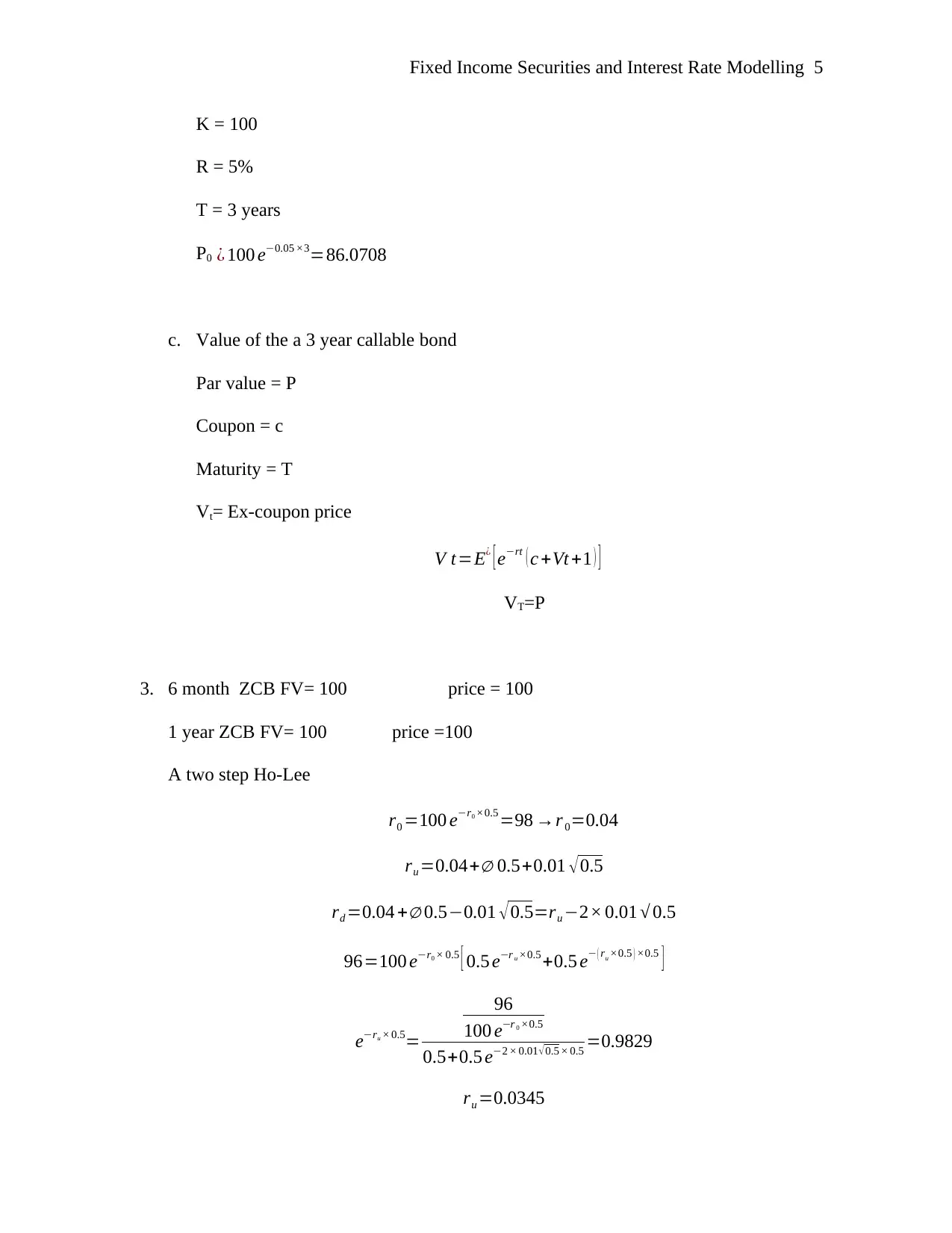

This document presents a comprehensive solution to an assignment on Fixed Income Securities and Interest Rate Modelling, likely for a Master's level finance course at the University of Hong Kong. The solution addresses key concepts such as one-step interest rate trees, the calculation of expected rates, market price of risk, and risk-neutral probabilities. It includes detailed calculations for option pricing, replicating portfolios using ZCBs, and the construction of risk-neutral interest rate trees. The assignment also covers interest rate swaps and the application of the Ho-Lee and Vasicek interest rate models, including parameter estimation and term structure analysis. Furthermore, the solution explores the impact of varying parameters on the term structure of interest rates and discusses derivative markets, including forwards, futures, swaps, and options. Finally, it touches upon the binomial model and its application in pricing and risk management.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.