Financial Accounting: Flash Cleaning Services & ABC Learning Study

VerifiedAdded on 2023/04/10

|18

|4607

|133

Case Study

AI Summary

This assignment provides a comprehensive solution to accounting tasks related to Flash Cleaning Services, including the preparation of journal entries, T-accounts, an unadjusted trial balance, adjusting entries, a ten-column worksheet, and financial statements. It also includes ratio calculations and their evaluation, along with recommendations for the company. Furthermore, the assignment features an essay on the history of accounting and a case study analysis of ABC Learning, focusing on the reasons for its failure and the ethical issues involved. The detailed solutions and analysis make this document a valuable resource for understanding accounting principles and case study methodologies. Desklib offers similar solved assignments and past papers to aid students in their studies.

ASSIGNMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Solution – 1 - Preparation of accounting records – using spreadsheets......................................................2

Journal Entries.........................................................................................................................................2

T. accounts..............................................................................................................................................3

Unadjusted Trial Balance.........................................................................................................................5

Types of Adjusting Entries.......................................................................................................................6

Adjusting Entries for Flash Cleaning Services as at 31 July 2018..............................................................7

Ten Column Worksheet in the books of Flash Cleaning Services.............................................................8

Financial Statements...............................................................................................................................9

Ratio Calculation....................................................................................................................................11

Evaluation of ratios................................................................................................................................11

Change in ratio’s if company repays the bank loan...............................................................................12

Recommendation..................................................................................................................................12

Solution – 2 - History of accounting – essay..............................................................................................13

Solution – 3 - ABC Learning Case Study.....................................................................................................15

3 (1). Failure of ABC Learning................................................................................................................15

3(2) The Ethical Issues...........................................................................................................................16

References.................................................................................................................................................17

Solution – 1 - Preparation of accounting records – using spreadsheets......................................................2

Journal Entries.........................................................................................................................................2

T. accounts..............................................................................................................................................3

Unadjusted Trial Balance.........................................................................................................................5

Types of Adjusting Entries.......................................................................................................................6

Adjusting Entries for Flash Cleaning Services as at 31 July 2018..............................................................7

Ten Column Worksheet in the books of Flash Cleaning Services.............................................................8

Financial Statements...............................................................................................................................9

Ratio Calculation....................................................................................................................................11

Evaluation of ratios................................................................................................................................11

Change in ratio’s if company repays the bank loan...............................................................................12

Recommendation..................................................................................................................................12

Solution – 2 - History of accounting – essay..............................................................................................13

Solution – 3 - ABC Learning Case Study.....................................................................................................15

3 (1). Failure of ABC Learning................................................................................................................15

3(2) The Ethical Issues...........................................................................................................................16

References.................................................................................................................................................17

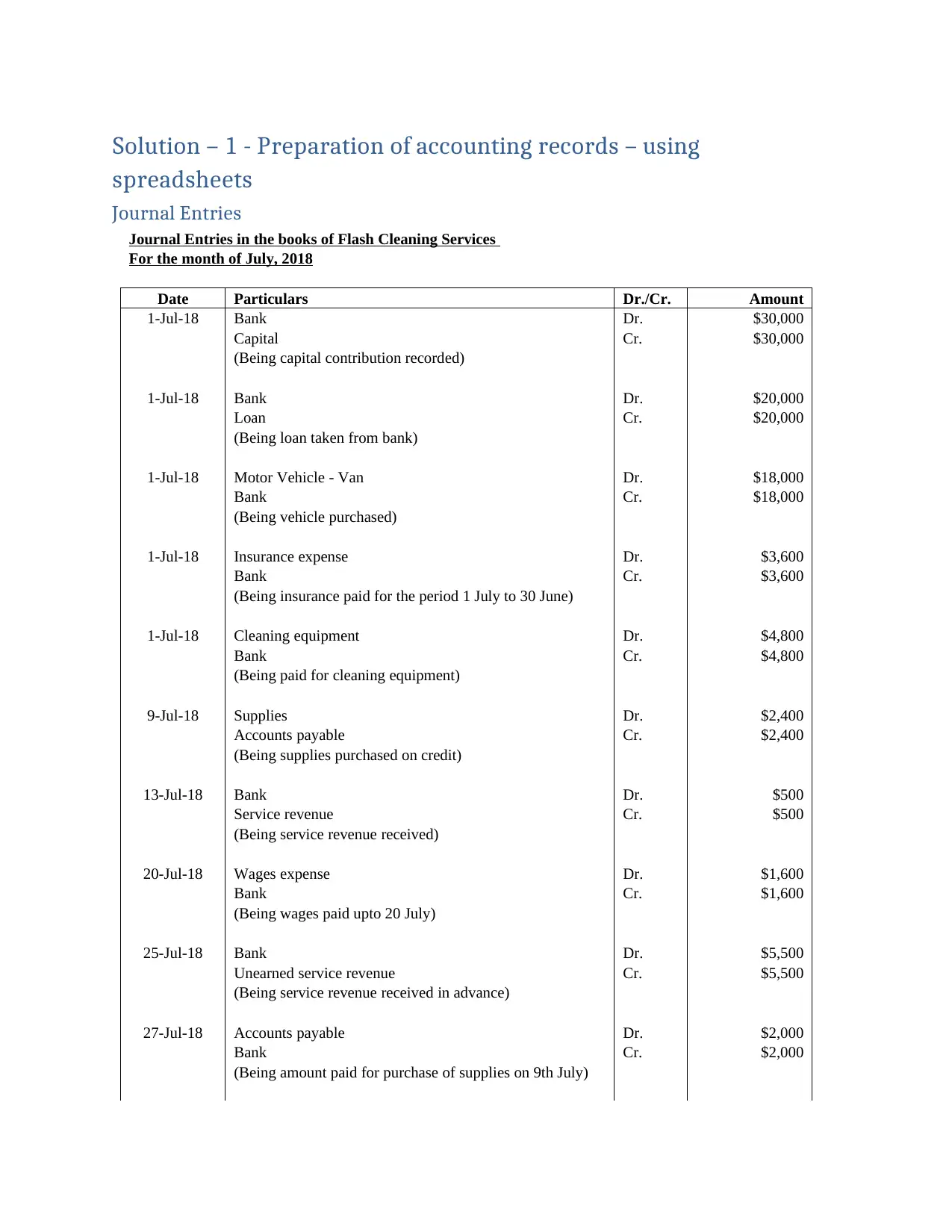

Solution – 1 - Preparation of accounting records – using

spreadsheets

Journal Entries

Journal Entries in the books of Flash Cleaning Services

For the month of July, 2018

Date Particulars Dr./Cr. Amount

1-Jul-18 Bank Dr. $30,000

Capital Cr. $30,000

(Being capital contribution recorded)

1-Jul-18 Bank Dr. $20,000

Loan Cr. $20,000

(Being loan taken from bank)

1-Jul-18 Motor Vehicle - Van Dr. $18,000

Bank Cr. $18,000

(Being vehicle purchased)

1-Jul-18 Insurance expense Dr. $3,600

Bank Cr. $3,600

(Being insurance paid for the period 1 July to 30 June)

1-Jul-18 Cleaning equipment Dr. $4,800

Bank Cr. $4,800

(Being paid for cleaning equipment)

9-Jul-18 Supplies Dr. $2,400

Accounts payable Cr. $2,400

(Being supplies purchased on credit)

13-Jul-18 Bank Dr. $500

Service revenue Cr. $500

(Being service revenue received)

20-Jul-18 Wages expense Dr. $1,600

Bank Cr. $1,600

(Being wages paid upto 20 July)

25-Jul-18 Bank Dr. $5,500

Unearned service revenue Cr. $5,500

(Being service revenue received in advance)

27-Jul-18 Accounts payable Dr. $2,000

Bank Cr. $2,000

(Being amount paid for purchase of supplies on 9th July)

spreadsheets

Journal Entries

Journal Entries in the books of Flash Cleaning Services

For the month of July, 2018

Date Particulars Dr./Cr. Amount

1-Jul-18 Bank Dr. $30,000

Capital Cr. $30,000

(Being capital contribution recorded)

1-Jul-18 Bank Dr. $20,000

Loan Cr. $20,000

(Being loan taken from bank)

1-Jul-18 Motor Vehicle - Van Dr. $18,000

Bank Cr. $18,000

(Being vehicle purchased)

1-Jul-18 Insurance expense Dr. $3,600

Bank Cr. $3,600

(Being insurance paid for the period 1 July to 30 June)

1-Jul-18 Cleaning equipment Dr. $4,800

Bank Cr. $4,800

(Being paid for cleaning equipment)

9-Jul-18 Supplies Dr. $2,400

Accounts payable Cr. $2,400

(Being supplies purchased on credit)

13-Jul-18 Bank Dr. $500

Service revenue Cr. $500

(Being service revenue received)

20-Jul-18 Wages expense Dr. $1,600

Bank Cr. $1,600

(Being wages paid upto 20 July)

25-Jul-18 Bank Dr. $5,500

Unearned service revenue Cr. $5,500

(Being service revenue received in advance)

27-Jul-18 Accounts payable Dr. $2,000

Bank Cr. $2,000

(Being amount paid for purchase of supplies on 9th July)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

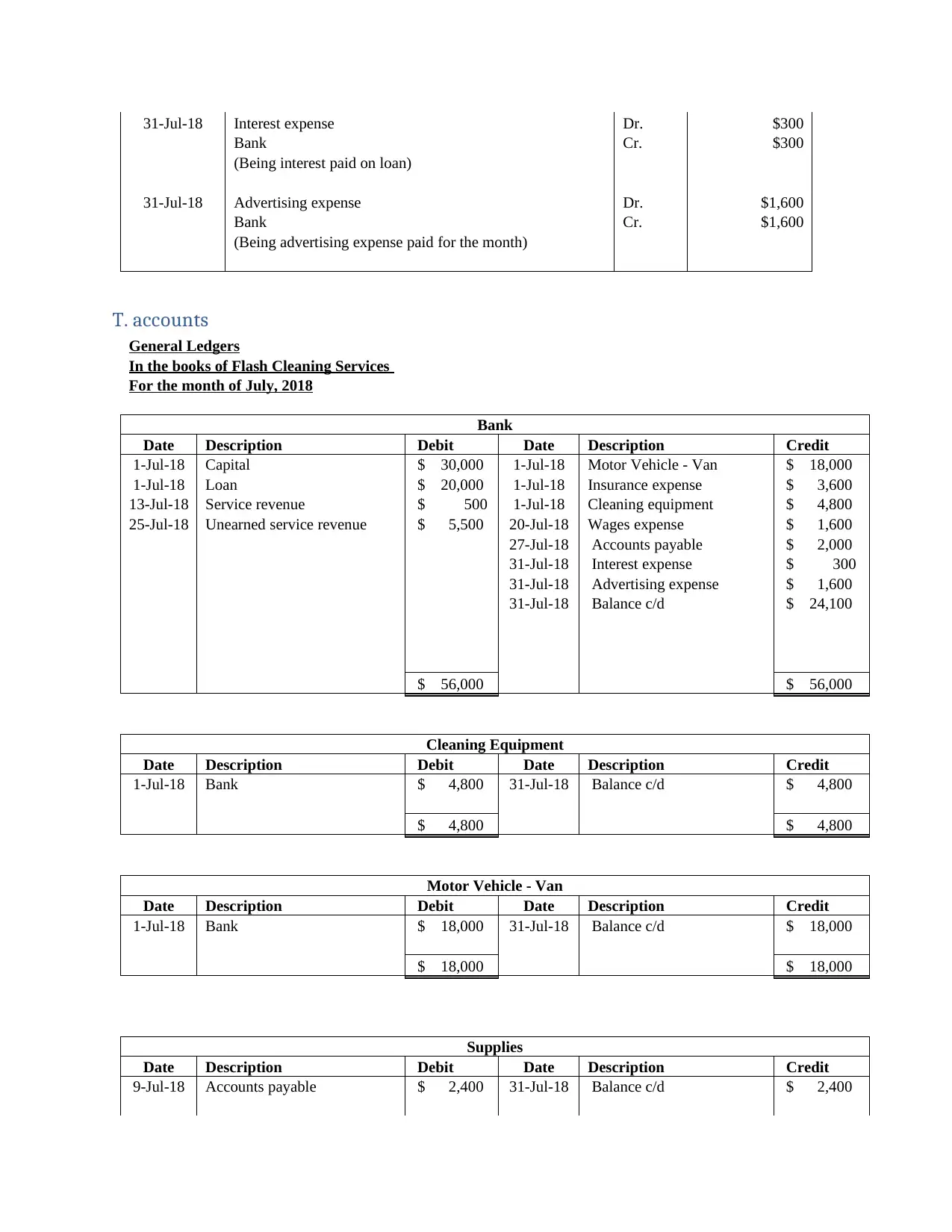

31-Jul-18 Interest expense Dr. $300

Bank Cr. $300

(Being interest paid on loan)

31-Jul-18 Advertising expense Dr. $1,600

Bank Cr. $1,600

(Being advertising expense paid for the month)

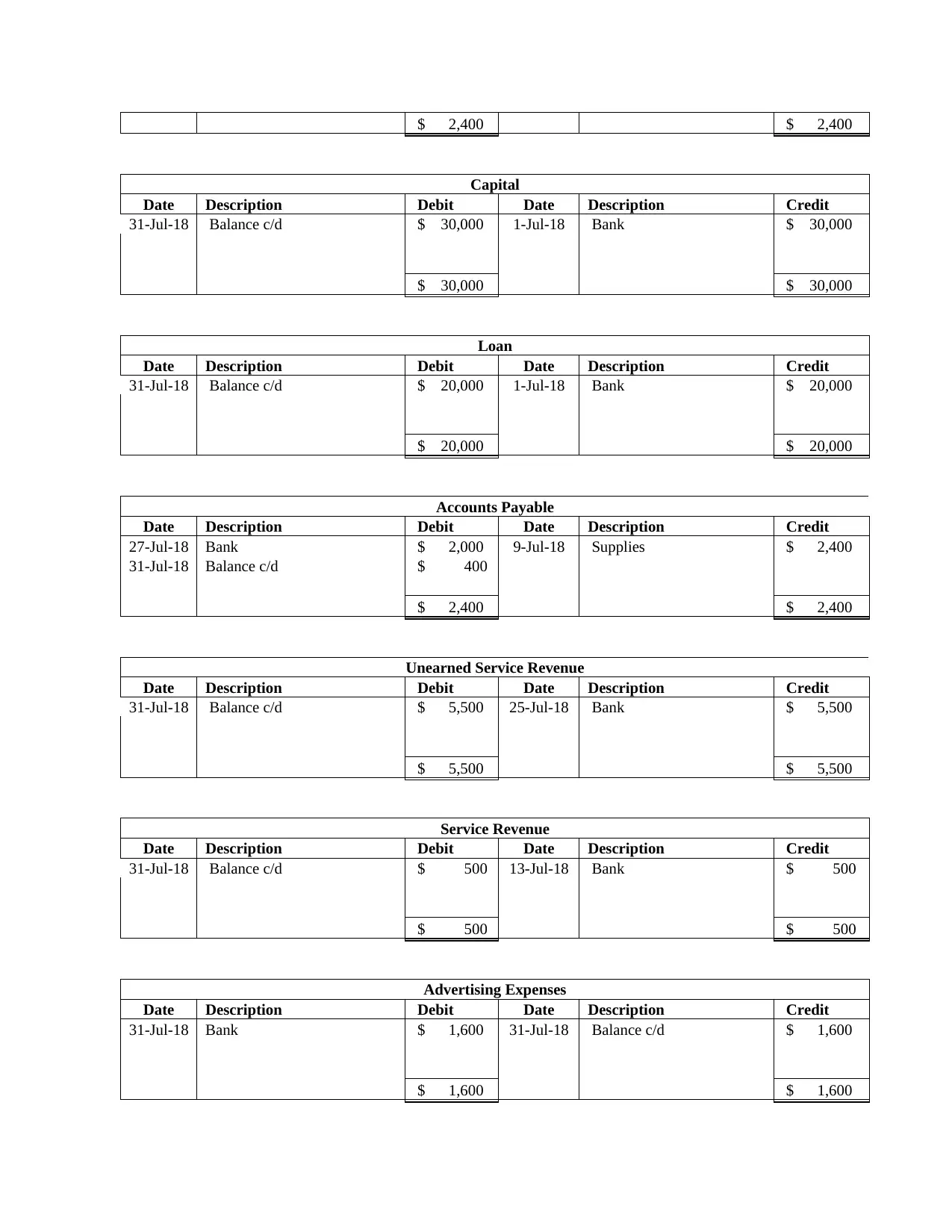

T. accounts

General Ledgers

In the books of Flash Cleaning Services

For the month of July, 2018

Bank

Date Description Debit Date Description Credit

1-Jul-18 Capital $ 30,000 1-Jul-18 Motor Vehicle - Van $ 18,000

1-Jul-18 Loan $ 20,000 1-Jul-18 Insurance expense $ 3,600

13-Jul-18 Service revenue $ 500 1-Jul-18 Cleaning equipment $ 4,800

25-Jul-18 Unearned service revenue $ 5,500 20-Jul-18 Wages expense $ 1,600

27-Jul-18 Accounts payable $ 2,000

31-Jul-18 Interest expense $ 300

31-Jul-18 Advertising expense $ 1,600

31-Jul-18 Balance c/d $ 24,100

$ 56,000 $ 56,000

Cleaning Equipment

Date Description Debit Date Description Credit

1-Jul-18 Bank $ 4,800 31-Jul-18 Balance c/d $ 4,800

$ 4,800 $ 4,800

Motor Vehicle - Van

Date Description Debit Date Description Credit

1-Jul-18 Bank $ 18,000 31-Jul-18 Balance c/d $ 18,000

$ 18,000 $ 18,000

Supplies

Date Description Debit Date Description Credit

9-Jul-18 Accounts payable $ 2,400 31-Jul-18 Balance c/d $ 2,400

Bank Cr. $300

(Being interest paid on loan)

31-Jul-18 Advertising expense Dr. $1,600

Bank Cr. $1,600

(Being advertising expense paid for the month)

T. accounts

General Ledgers

In the books of Flash Cleaning Services

For the month of July, 2018

Bank

Date Description Debit Date Description Credit

1-Jul-18 Capital $ 30,000 1-Jul-18 Motor Vehicle - Van $ 18,000

1-Jul-18 Loan $ 20,000 1-Jul-18 Insurance expense $ 3,600

13-Jul-18 Service revenue $ 500 1-Jul-18 Cleaning equipment $ 4,800

25-Jul-18 Unearned service revenue $ 5,500 20-Jul-18 Wages expense $ 1,600

27-Jul-18 Accounts payable $ 2,000

31-Jul-18 Interest expense $ 300

31-Jul-18 Advertising expense $ 1,600

31-Jul-18 Balance c/d $ 24,100

$ 56,000 $ 56,000

Cleaning Equipment

Date Description Debit Date Description Credit

1-Jul-18 Bank $ 4,800 31-Jul-18 Balance c/d $ 4,800

$ 4,800 $ 4,800

Motor Vehicle - Van

Date Description Debit Date Description Credit

1-Jul-18 Bank $ 18,000 31-Jul-18 Balance c/d $ 18,000

$ 18,000 $ 18,000

Supplies

Date Description Debit Date Description Credit

9-Jul-18 Accounts payable $ 2,400 31-Jul-18 Balance c/d $ 2,400

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

$ 2,400 $ 2,400

Capital

Date Description Debit Date Description Credit

31-Jul-18 Balance c/d $ 30,000 1-Jul-18 Bank $ 30,000

$ 30,000 $ 30,000

Loan

Date Description Debit Date Description Credit

31-Jul-18 Balance c/d $ 20,000 1-Jul-18 Bank $ 20,000

$ 20,000 $ 20,000

Accounts Payable

Date Description Debit Date Description Credit

27-Jul-18 Bank $ 2,000 9-Jul-18 Supplies $ 2,400

31-Jul-18 Balance c/d $ 400

$ 2,400 $ 2,400

Unearned Service Revenue

Date Description Debit Date Description Credit

31-Jul-18 Balance c/d $ 5,500 25-Jul-18 Bank $ 5,500

$ 5,500 $ 5,500

Service Revenue

Date Description Debit Date Description Credit

31-Jul-18 Balance c/d $ 500 13-Jul-18 Bank $ 500

$ 500 $ 500

Advertising Expenses

Date Description Debit Date Description Credit

31-Jul-18 Bank $ 1,600 31-Jul-18 Balance c/d $ 1,600

$ 1,600 $ 1,600

Capital

Date Description Debit Date Description Credit

31-Jul-18 Balance c/d $ 30,000 1-Jul-18 Bank $ 30,000

$ 30,000 $ 30,000

Loan

Date Description Debit Date Description Credit

31-Jul-18 Balance c/d $ 20,000 1-Jul-18 Bank $ 20,000

$ 20,000 $ 20,000

Accounts Payable

Date Description Debit Date Description Credit

27-Jul-18 Bank $ 2,000 9-Jul-18 Supplies $ 2,400

31-Jul-18 Balance c/d $ 400

$ 2,400 $ 2,400

Unearned Service Revenue

Date Description Debit Date Description Credit

31-Jul-18 Balance c/d $ 5,500 25-Jul-18 Bank $ 5,500

$ 5,500 $ 5,500

Service Revenue

Date Description Debit Date Description Credit

31-Jul-18 Balance c/d $ 500 13-Jul-18 Bank $ 500

$ 500 $ 500

Advertising Expenses

Date Description Debit Date Description Credit

31-Jul-18 Bank $ 1,600 31-Jul-18 Balance c/d $ 1,600

$ 1,600 $ 1,600

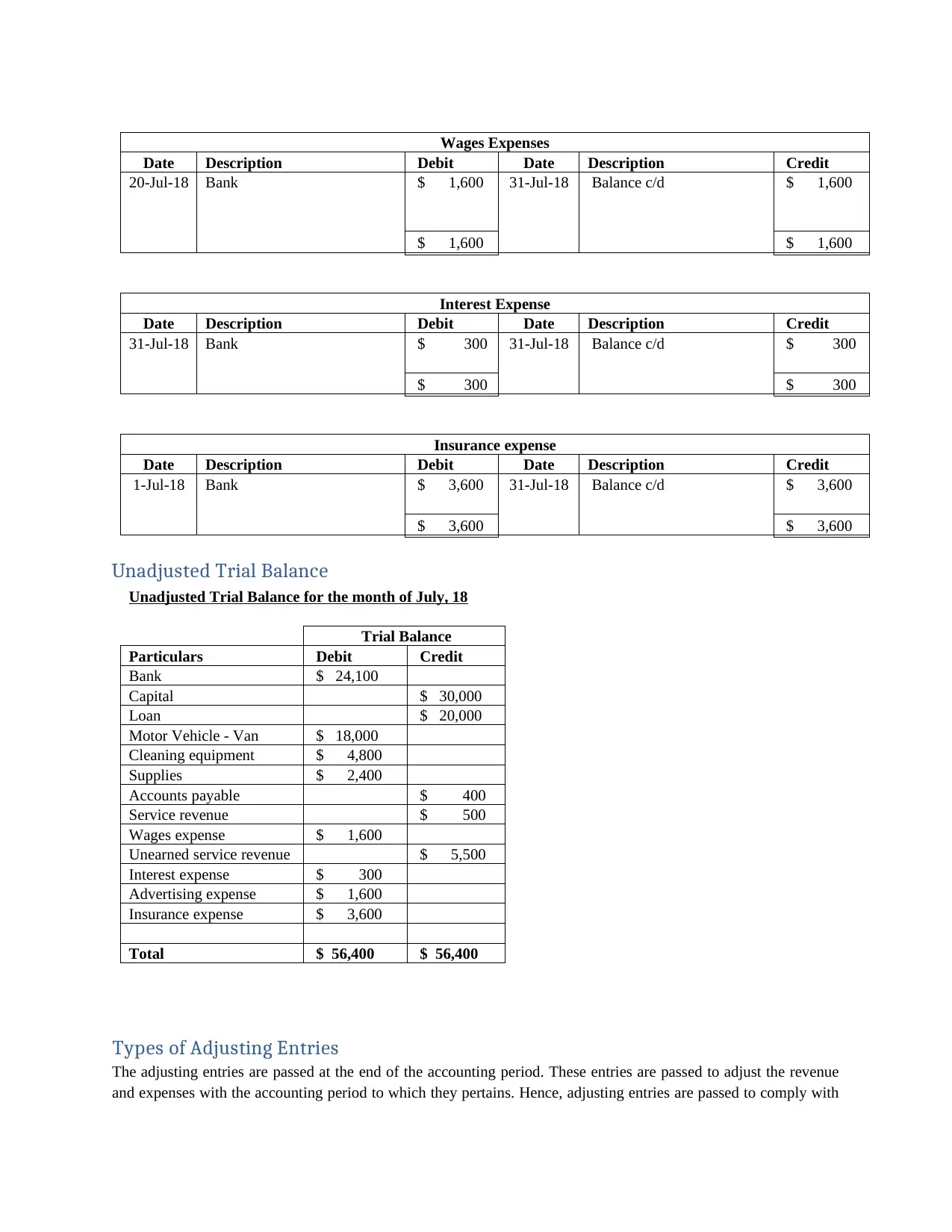

Wages Expenses

Date Description Debit Date Description Credit

20-Jul-18 Bank $ 1,600 31-Jul-18 Balance c/d $ 1,600

$ 1,600 $ 1,600

Interest Expense

Date Description Debit Date Description Credit

31-Jul-18 Bank $ 300 31-Jul-18 Balance c/d $ 300

$ 300 $ 300

Insurance expense

Date Description Debit Date Description Credit

1-Jul-18 Bank $ 3,600 31-Jul-18 Balance c/d $ 3,600

$ 3,600 $ 3,600

Unadjusted Trial Balance

Unadjusted Trial Balance for the month of July, 18

Trial Balance

Particulars Debit Credit

Bank $ 24,100

Capital $ 30,000

Loan $ 20,000

Motor Vehicle - Van $ 18,000

Cleaning equipment $ 4,800

Supplies $ 2,400

Accounts payable $ 400

Service revenue $ 500

Wages expense $ 1,600

Unearned service revenue $ 5,500

Interest expense $ 300

Advertising expense $ 1,600

Insurance expense $ 3,600

Total $ 56,400 $ 56,400

Types of Adjusting Entries

The adjusting entries are passed at the end of the accounting period. These entries are passed to adjust the revenue

and expenses with the accounting period to which they pertains. Hence, adjusting entries are passed to comply with

Date Description Debit Date Description Credit

20-Jul-18 Bank $ 1,600 31-Jul-18 Balance c/d $ 1,600

$ 1,600 $ 1,600

Interest Expense

Date Description Debit Date Description Credit

31-Jul-18 Bank $ 300 31-Jul-18 Balance c/d $ 300

$ 300 $ 300

Insurance expense

Date Description Debit Date Description Credit

1-Jul-18 Bank $ 3,600 31-Jul-18 Balance c/d $ 3,600

$ 3,600 $ 3,600

Unadjusted Trial Balance

Unadjusted Trial Balance for the month of July, 18

Trial Balance

Particulars Debit Credit

Bank $ 24,100

Capital $ 30,000

Loan $ 20,000

Motor Vehicle - Van $ 18,000

Cleaning equipment $ 4,800

Supplies $ 2,400

Accounts payable $ 400

Service revenue $ 500

Wages expense $ 1,600

Unearned service revenue $ 5,500

Interest expense $ 300

Advertising expense $ 1,600

Insurance expense $ 3,600

Total $ 56,400 $ 56,400

Types of Adjusting Entries

The adjusting entries are passed at the end of the accounting period. These entries are passed to adjust the revenue

and expenses with the accounting period to which they pertains. Hence, adjusting entries are passed to comply with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

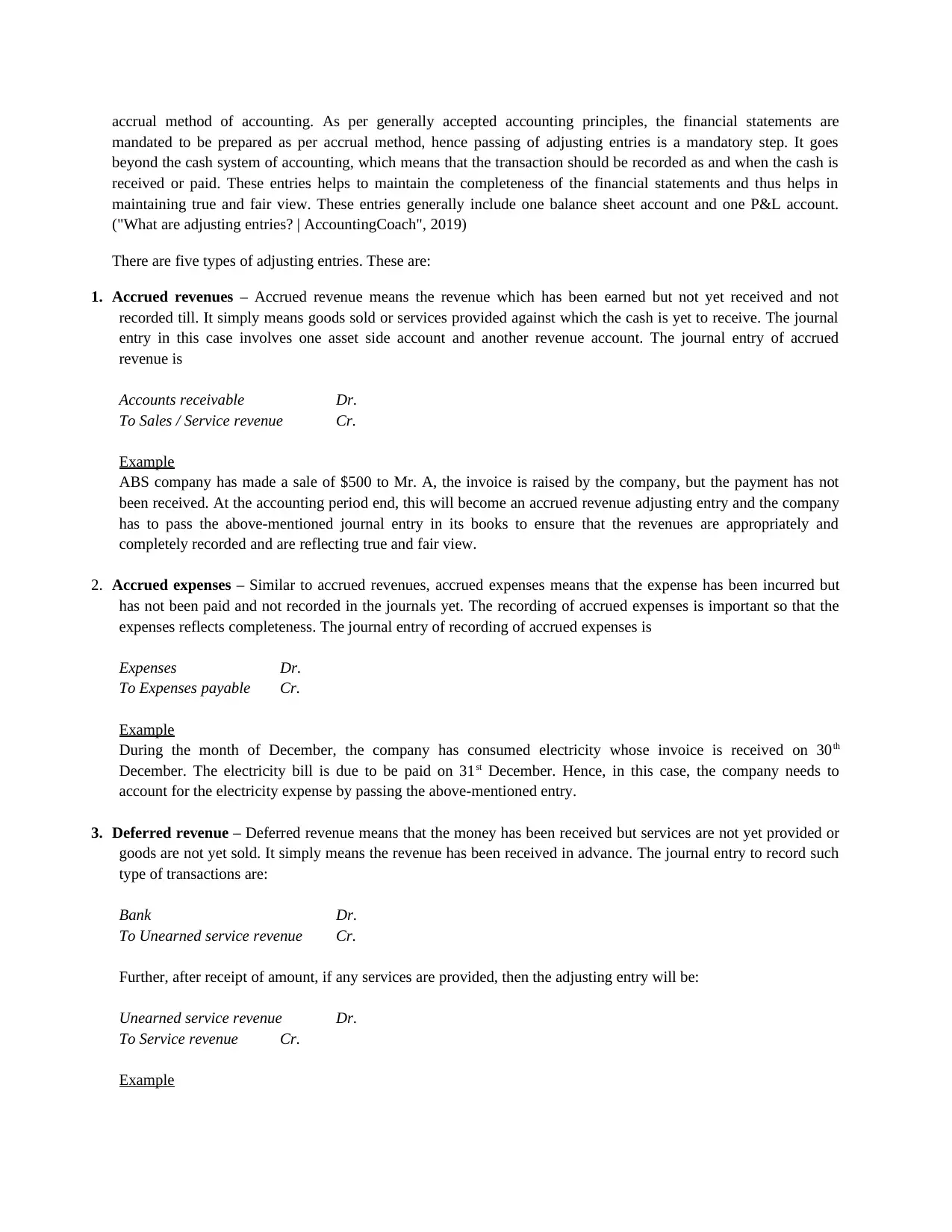

accrual method of accounting. As per generally accepted accounting principles, the financial statements are

mandated to be prepared as per accrual method, hence passing of adjusting entries is a mandatory step. It goes

beyond the cash system of accounting, which means that the transaction should be recorded as and when the cash is

received or paid. These entries helps to maintain the completeness of the financial statements and thus helps in

maintaining true and fair view. These entries generally include one balance sheet account and one P&L account.

("What are adjusting entries? | AccountingCoach", 2019)

There are five types of adjusting entries. These are:

1. Accrued revenues – Accrued revenue means the revenue which has been earned but not yet received and not

recorded till. It simply means goods sold or services provided against which the cash is yet to receive. The journal

entry in this case involves one asset side account and another revenue account. The journal entry of accrued

revenue is

Accounts receivable Dr.

To Sales / Service revenue Cr.

Example

ABS company has made a sale of $500 to Mr. A, the invoice is raised by the company, but the payment has not

been received. At the accounting period end, this will become an accrued revenue adjusting entry and the company

has to pass the above-mentioned journal entry in its books to ensure that the revenues are appropriately and

completely recorded and are reflecting true and fair view.

2. Accrued expenses – Similar to accrued revenues, accrued expenses means that the expense has been incurred but

has not been paid and not recorded in the journals yet. The recording of accrued expenses is important so that the

expenses reflects completeness. The journal entry of recording of accrued expenses is

Expenses Dr.

To Expenses payable Cr.

Example

During the month of December, the company has consumed electricity whose invoice is received on 30th

December. The electricity bill is due to be paid on 31st December. Hence, in this case, the company needs to

account for the electricity expense by passing the above-mentioned entry.

3. Deferred revenue – Deferred revenue means that the money has been received but services are not yet provided or

goods are not yet sold. It simply means the revenue has been received in advance. The journal entry to record such

type of transactions are:

Bank Dr.

To Unearned service revenue Cr.

Further, after receipt of amount, if any services are provided, then the adjusting entry will be:

Unearned service revenue Dr.

To Service revenue Cr.

Example

mandated to be prepared as per accrual method, hence passing of adjusting entries is a mandatory step. It goes

beyond the cash system of accounting, which means that the transaction should be recorded as and when the cash is

received or paid. These entries helps to maintain the completeness of the financial statements and thus helps in

maintaining true and fair view. These entries generally include one balance sheet account and one P&L account.

("What are adjusting entries? | AccountingCoach", 2019)

There are five types of adjusting entries. These are:

1. Accrued revenues – Accrued revenue means the revenue which has been earned but not yet received and not

recorded till. It simply means goods sold or services provided against which the cash is yet to receive. The journal

entry in this case involves one asset side account and another revenue account. The journal entry of accrued

revenue is

Accounts receivable Dr.

To Sales / Service revenue Cr.

Example

ABS company has made a sale of $500 to Mr. A, the invoice is raised by the company, but the payment has not

been received. At the accounting period end, this will become an accrued revenue adjusting entry and the company

has to pass the above-mentioned journal entry in its books to ensure that the revenues are appropriately and

completely recorded and are reflecting true and fair view.

2. Accrued expenses – Similar to accrued revenues, accrued expenses means that the expense has been incurred but

has not been paid and not recorded in the journals yet. The recording of accrued expenses is important so that the

expenses reflects completeness. The journal entry of recording of accrued expenses is

Expenses Dr.

To Expenses payable Cr.

Example

During the month of December, the company has consumed electricity whose invoice is received on 30th

December. The electricity bill is due to be paid on 31st December. Hence, in this case, the company needs to

account for the electricity expense by passing the above-mentioned entry.

3. Deferred revenue – Deferred revenue means that the money has been received but services are not yet provided or

goods are not yet sold. It simply means the revenue has been received in advance. The journal entry to record such

type of transactions are:

Bank Dr.

To Unearned service revenue Cr.

Further, after receipt of amount, if any services are provided, then the adjusting entry will be:

Unearned service revenue Dr.

To Service revenue Cr.

Example

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

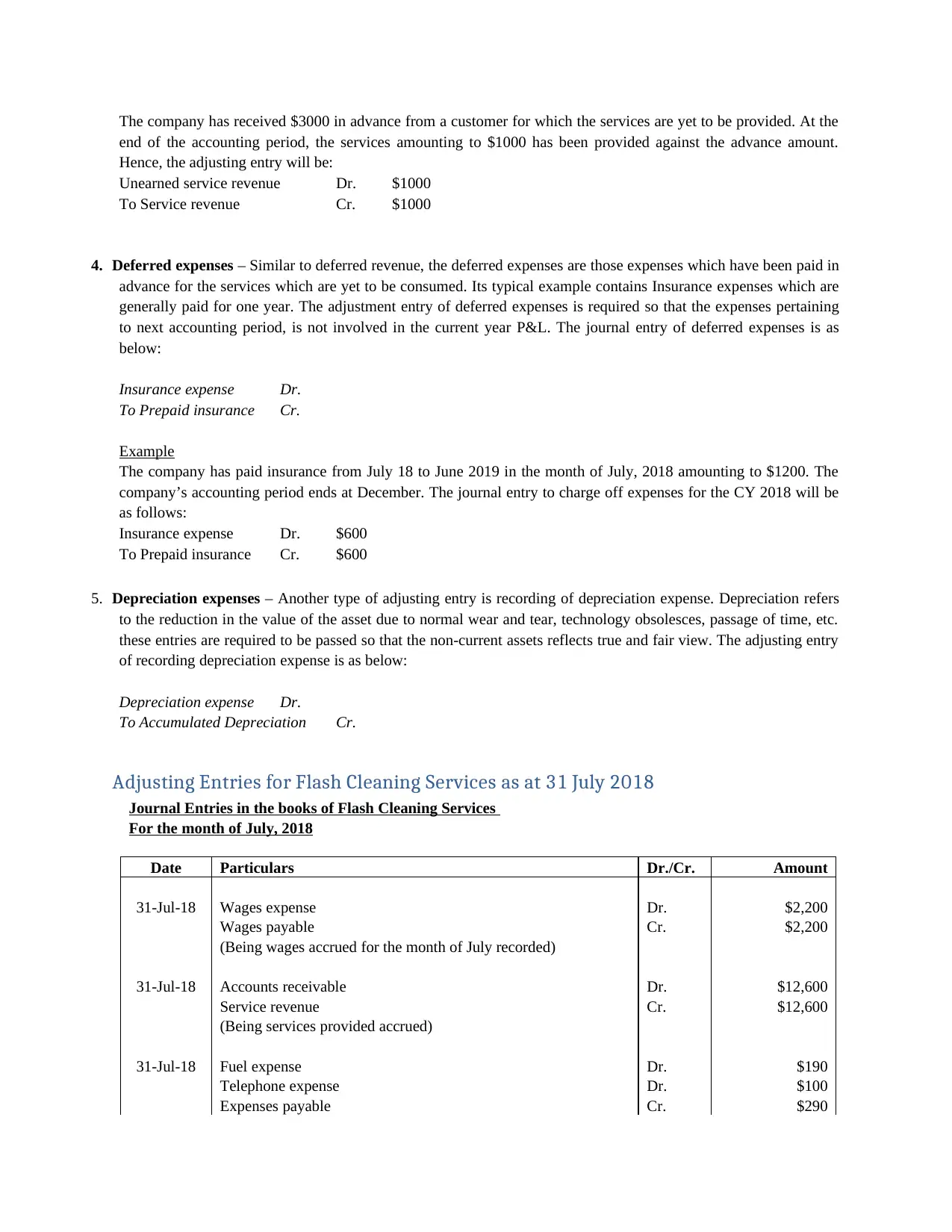

The company has received $3000 in advance from a customer for which the services are yet to be provided. At the

end of the accounting period, the services amounting to $1000 has been provided against the advance amount.

Hence, the adjusting entry will be:

Unearned service revenue Dr. $1000

To Service revenue Cr. $1000

4. Deferred expenses – Similar to deferred revenue, the deferred expenses are those expenses which have been paid in

advance for the services which are yet to be consumed. Its typical example contains Insurance expenses which are

generally paid for one year. The adjustment entry of deferred expenses is required so that the expenses pertaining

to next accounting period, is not involved in the current year P&L. The journal entry of deferred expenses is as

below:

Insurance expense Dr.

To Prepaid insurance Cr.

Example

The company has paid insurance from July 18 to June 2019 in the month of July, 2018 amounting to $1200. The

company’s accounting period ends at December. The journal entry to charge off expenses for the CY 2018 will be

as follows:

Insurance expense Dr. $600

To Prepaid insurance Cr. $600

5. Depreciation expenses – Another type of adjusting entry is recording of depreciation expense. Depreciation refers

to the reduction in the value of the asset due to normal wear and tear, technology obsolesces, passage of time, etc.

these entries are required to be passed so that the non-current assets reflects true and fair view. The adjusting entry

of recording depreciation expense is as below:

Depreciation expense Dr.

To Accumulated Depreciation Cr.

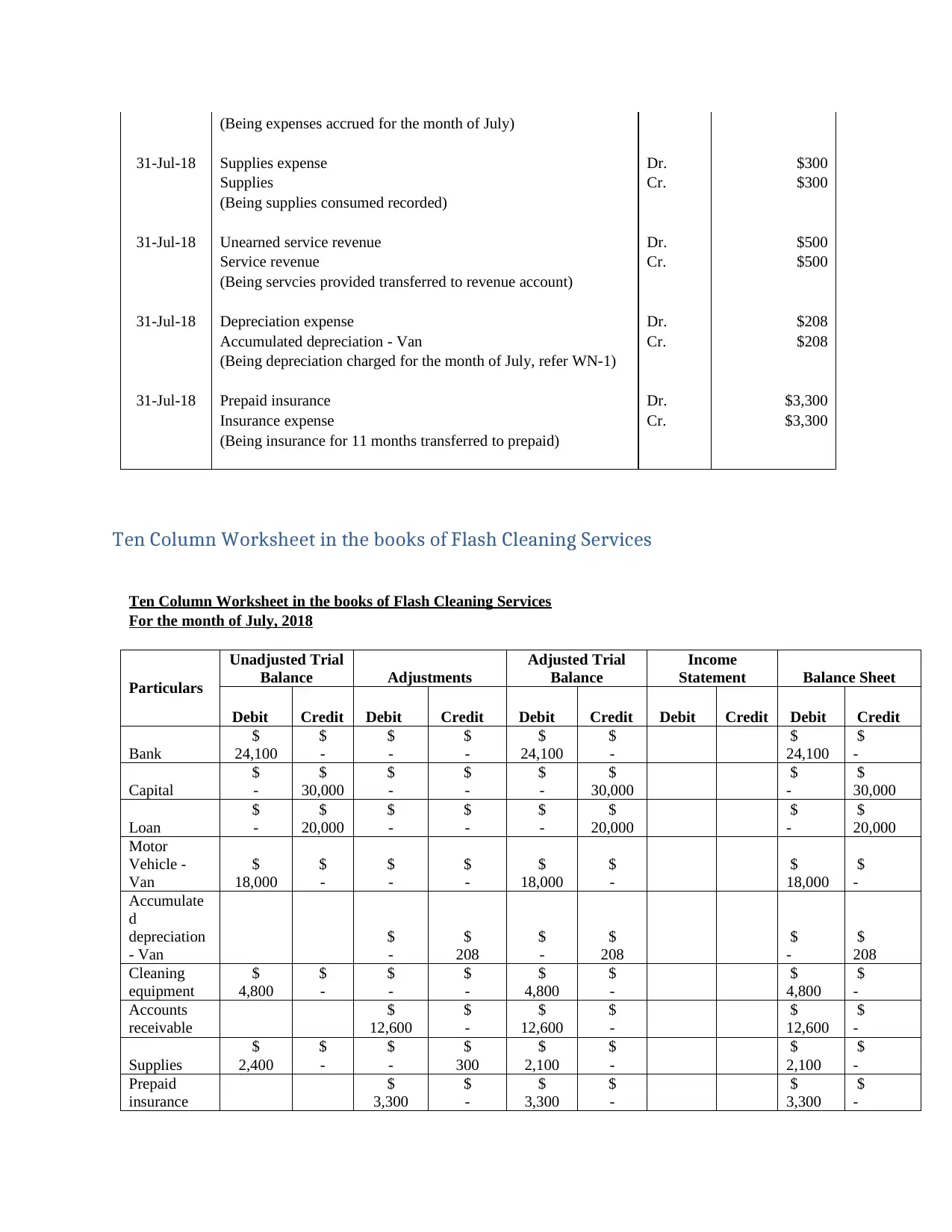

Adjusting Entries for Flash Cleaning Services as at 31 July 2018

Journal Entries in the books of Flash Cleaning Services

For the month of July, 2018

Date Particulars Dr./Cr. Amount

31-Jul-18 Wages expense Dr. $2,200

Wages payable Cr. $2,200

(Being wages accrued for the month of July recorded)

31-Jul-18 Accounts receivable Dr. $12,600

Service revenue Cr. $12,600

(Being services provided accrued)

31-Jul-18 Fuel expense Dr. $190

Telephone expense Dr. $100

Expenses payable Cr. $290

end of the accounting period, the services amounting to $1000 has been provided against the advance amount.

Hence, the adjusting entry will be:

Unearned service revenue Dr. $1000

To Service revenue Cr. $1000

4. Deferred expenses – Similar to deferred revenue, the deferred expenses are those expenses which have been paid in

advance for the services which are yet to be consumed. Its typical example contains Insurance expenses which are

generally paid for one year. The adjustment entry of deferred expenses is required so that the expenses pertaining

to next accounting period, is not involved in the current year P&L. The journal entry of deferred expenses is as

below:

Insurance expense Dr.

To Prepaid insurance Cr.

Example

The company has paid insurance from July 18 to June 2019 in the month of July, 2018 amounting to $1200. The

company’s accounting period ends at December. The journal entry to charge off expenses for the CY 2018 will be

as follows:

Insurance expense Dr. $600

To Prepaid insurance Cr. $600

5. Depreciation expenses – Another type of adjusting entry is recording of depreciation expense. Depreciation refers

to the reduction in the value of the asset due to normal wear and tear, technology obsolesces, passage of time, etc.

these entries are required to be passed so that the non-current assets reflects true and fair view. The adjusting entry

of recording depreciation expense is as below:

Depreciation expense Dr.

To Accumulated Depreciation Cr.

Adjusting Entries for Flash Cleaning Services as at 31 July 2018

Journal Entries in the books of Flash Cleaning Services

For the month of July, 2018

Date Particulars Dr./Cr. Amount

31-Jul-18 Wages expense Dr. $2,200

Wages payable Cr. $2,200

(Being wages accrued for the month of July recorded)

31-Jul-18 Accounts receivable Dr. $12,600

Service revenue Cr. $12,600

(Being services provided accrued)

31-Jul-18 Fuel expense Dr. $190

Telephone expense Dr. $100

Expenses payable Cr. $290

(Being expenses accrued for the month of July)

31-Jul-18 Supplies expense Dr. $300

Supplies Cr. $300

(Being supplies consumed recorded)

31-Jul-18 Unearned service revenue Dr. $500

Service revenue Cr. $500

(Being servcies provided transferred to revenue account)

31-Jul-18 Depreciation expense Dr. $208

Accumulated depreciation - Van Cr. $208

(Being depreciation charged for the month of July, refer WN-1)

31-Jul-18 Prepaid insurance Dr. $3,300

Insurance expense Cr. $3,300

(Being insurance for 11 months transferred to prepaid)

Ten Column Worksheet in the books of Flash Cleaning Services

Ten Column Worksheet in the books of Flash Cleaning Services

For the month of July, 2018

Particulars

Unadjusted Trial

Balance Adjustments

Adjusted Trial

Balance

Income

Statement Balance Sheet

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Bank

$

24,100

$

-

$

-

$

-

$

24,100

$

-

$

24,100

$

-

Capital

$

-

$

30,000

$

-

$

-

$

-

$

30,000

$

-

$

30,000

Loan

$

-

$

20,000

$

-

$

-

$

-

$

20,000

$

-

$

20,000

Motor

Vehicle -

Van

$

18,000

$

-

$

-

$

-

$

18,000

$

-

$

18,000

$

-

Accumulate

d

depreciation

- Van

$

-

$

208

$

-

$

208

$

-

$

208

Cleaning

equipment

$

4,800

$

-

$

-

$

-

$

4,800

$

-

$

4,800

$

-

Accounts

receivable

$

12,600

$

-

$

12,600

$

-

$

12,600

$

-

Supplies

$

2,400

$

-

$

-

$

300

$

2,100

$

-

$

2,100

$

-

Prepaid

insurance

$

3,300

$

-

$

3,300

$

-

$

3,300

$

-

31-Jul-18 Supplies expense Dr. $300

Supplies Cr. $300

(Being supplies consumed recorded)

31-Jul-18 Unearned service revenue Dr. $500

Service revenue Cr. $500

(Being servcies provided transferred to revenue account)

31-Jul-18 Depreciation expense Dr. $208

Accumulated depreciation - Van Cr. $208

(Being depreciation charged for the month of July, refer WN-1)

31-Jul-18 Prepaid insurance Dr. $3,300

Insurance expense Cr. $3,300

(Being insurance for 11 months transferred to prepaid)

Ten Column Worksheet in the books of Flash Cleaning Services

Ten Column Worksheet in the books of Flash Cleaning Services

For the month of July, 2018

Particulars

Unadjusted Trial

Balance Adjustments

Adjusted Trial

Balance

Income

Statement Balance Sheet

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Bank

$

24,100

$

-

$

-

$

-

$

24,100

$

-

$

24,100

$

-

Capital

$

-

$

30,000

$

-

$

-

$

-

$

30,000

$

-

$

30,000

Loan

$

-

$

20,000

$

-

$

-

$

-

$

20,000

$

-

$

20,000

Motor

Vehicle -

Van

$

18,000

$

-

$

-

$

-

$

18,000

$

-

$

18,000

$

-

Accumulate

d

depreciation

- Van

$

-

$

208

$

-

$

208

$

-

$

208

Cleaning

equipment

$

4,800

$

-

$

-

$

-

$

4,800

$

-

$

4,800

$

-

Accounts

receivable

$

12,600

$

-

$

12,600

$

-

$

12,600

$

-

Supplies

$

2,400

$

-

$

-

$

300

$

2,100

$

-

$

2,100

$

-

Prepaid

insurance

$

3,300

$

-

$

3,300

$

-

$

3,300

$

-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

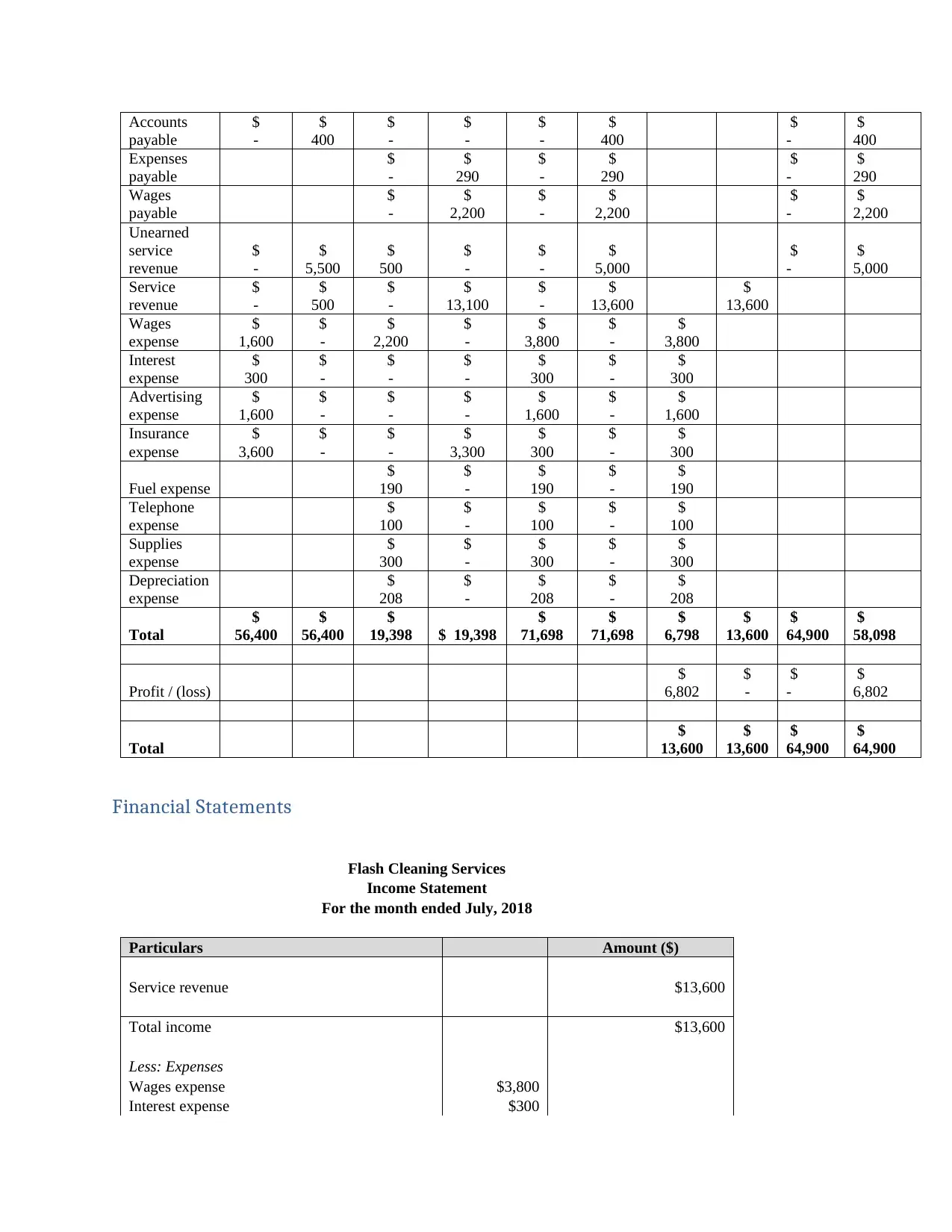

Accounts

payable

$

-

$

400

$

-

$

-

$

-

$

400

$

-

$

400

Expenses

payable

$

-

$

290

$

-

$

290

$

-

$

290

Wages

payable

$

-

$

2,200

$

-

$

2,200

$

-

$

2,200

Unearned

service

revenue

$

-

$

5,500

$

500

$

-

$

-

$

5,000

$

-

$

5,000

Service

revenue

$

-

$

500

$

-

$

13,100

$

-

$

13,600

$

13,600

Wages

expense

$

1,600

$

-

$

2,200

$

-

$

3,800

$

-

$

3,800

Interest

expense

$

300

$

-

$

-

$

-

$

300

$

-

$

300

Advertising

expense

$

1,600

$

-

$

-

$

-

$

1,600

$

-

$

1,600

Insurance

expense

$

3,600

$

-

$

-

$

3,300

$

300

$

-

$

300

Fuel expense

$

190

$

-

$

190

$

-

$

190

Telephone

expense

$

100

$

-

$

100

$

-

$

100

Supplies

expense

$

300

$

-

$

300

$

-

$

300

Depreciation

expense

$

208

$

-

$

208

$

-

$

208

Total

$

56,400

$

56,400

$

19,398 $ 19,398

$

71,698

$

71,698

$

6,798

$

13,600

$

64,900

$

58,098

Profit / (loss)

$

6,802

$

-

$

-

$

6,802

Total

$

13,600

$

13,600

$

64,900

$

64,900

Financial Statements

Flash Cleaning Services

Income Statement

For the month ended July, 2018

Particulars Amount ($)

Service revenue $13,600

Total income $13,600

Less: Expenses

Wages expense $3,800

Interest expense $300

payable

$

-

$

400

$

-

$

-

$

-

$

400

$

-

$

400

Expenses

payable

$

-

$

290

$

-

$

290

$

-

$

290

Wages

payable

$

-

$

2,200

$

-

$

2,200

$

-

$

2,200

Unearned

service

revenue

$

-

$

5,500

$

500

$

-

$

-

$

5,000

$

-

$

5,000

Service

revenue

$

-

$

500

$

-

$

13,100

$

-

$

13,600

$

13,600

Wages

expense

$

1,600

$

-

$

2,200

$

-

$

3,800

$

-

$

3,800

Interest

expense

$

300

$

-

$

-

$

-

$

300

$

-

$

300

Advertising

expense

$

1,600

$

-

$

-

$

-

$

1,600

$

-

$

1,600

Insurance

expense

$

3,600

$

-

$

-

$

3,300

$

300

$

-

$

300

Fuel expense

$

190

$

-

$

190

$

-

$

190

Telephone

expense

$

100

$

-

$

100

$

-

$

100

Supplies

expense

$

300

$

-

$

300

$

-

$

300

Depreciation

expense

$

208

$

-

$

208

$

-

$

208

Total

$

56,400

$

56,400

$

19,398 $ 19,398

$

71,698

$

71,698

$

6,798

$

13,600

$

64,900

$

58,098

Profit / (loss)

$

6,802

$

-

$

-

$

6,802

Total

$

13,600

$

13,600

$

64,900

$

64,900

Financial Statements

Flash Cleaning Services

Income Statement

For the month ended July, 2018

Particulars Amount ($)

Service revenue $13,600

Total income $13,600

Less: Expenses

Wages expense $3,800

Interest expense $300

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

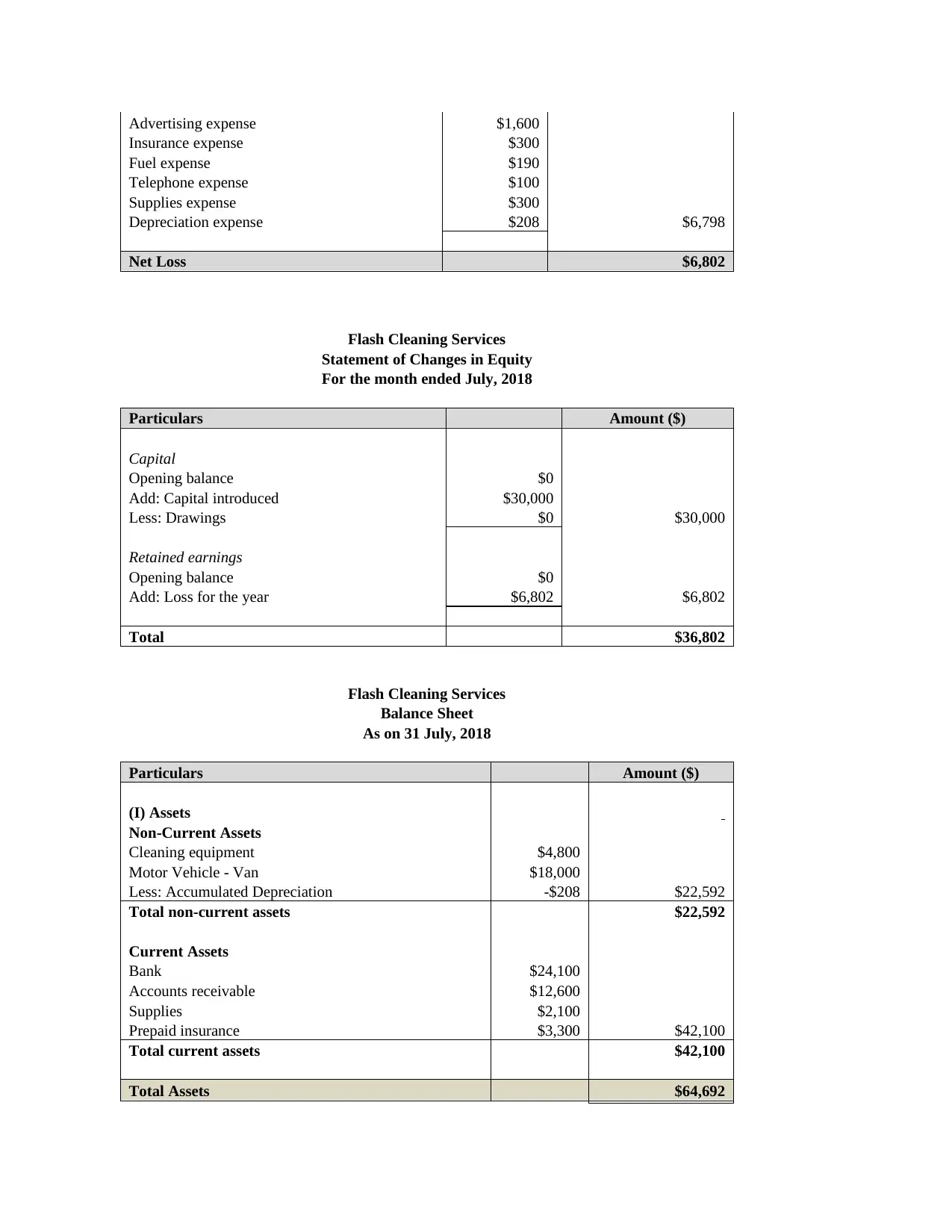

Advertising expense $1,600

Insurance expense $300

Fuel expense $190

Telephone expense $100

Supplies expense $300

Depreciation expense $208 $6,798

Net Loss $6,802

Flash Cleaning Services

Statement of Changes in Equity

For the month ended July, 2018

Particulars Amount ($)

Capital

Opening balance $0

Add: Capital introduced $30,000

Less: Drawings $0 $30,000

Retained earnings

Opening balance $0

Add: Loss for the year $6,802 $6,802

Total $36,802

Flash Cleaning Services

Balance Sheet

As on 31 July, 2018

Particulars Amount ($)

(I) Assets

Non-Current Assets

Cleaning equipment $4,800

Motor Vehicle - Van $18,000

Less: Accumulated Depreciation -$208 $22,592

Total non-current assets $22,592

Current Assets

Bank $24,100

Accounts receivable $12,600

Supplies $2,100

Prepaid insurance $3,300 $42,100

Total current assets $42,100

Total Assets $64,692

Insurance expense $300

Fuel expense $190

Telephone expense $100

Supplies expense $300

Depreciation expense $208 $6,798

Net Loss $6,802

Flash Cleaning Services

Statement of Changes in Equity

For the month ended July, 2018

Particulars Amount ($)

Capital

Opening balance $0

Add: Capital introduced $30,000

Less: Drawings $0 $30,000

Retained earnings

Opening balance $0

Add: Loss for the year $6,802 $6,802

Total $36,802

Flash Cleaning Services

Balance Sheet

As on 31 July, 2018

Particulars Amount ($)

(I) Assets

Non-Current Assets

Cleaning equipment $4,800

Motor Vehicle - Van $18,000

Less: Accumulated Depreciation -$208 $22,592

Total non-current assets $22,592

Current Assets

Bank $24,100

Accounts receivable $12,600

Supplies $2,100

Prepaid insurance $3,300 $42,100

Total current assets $42,100

Total Assets $64,692

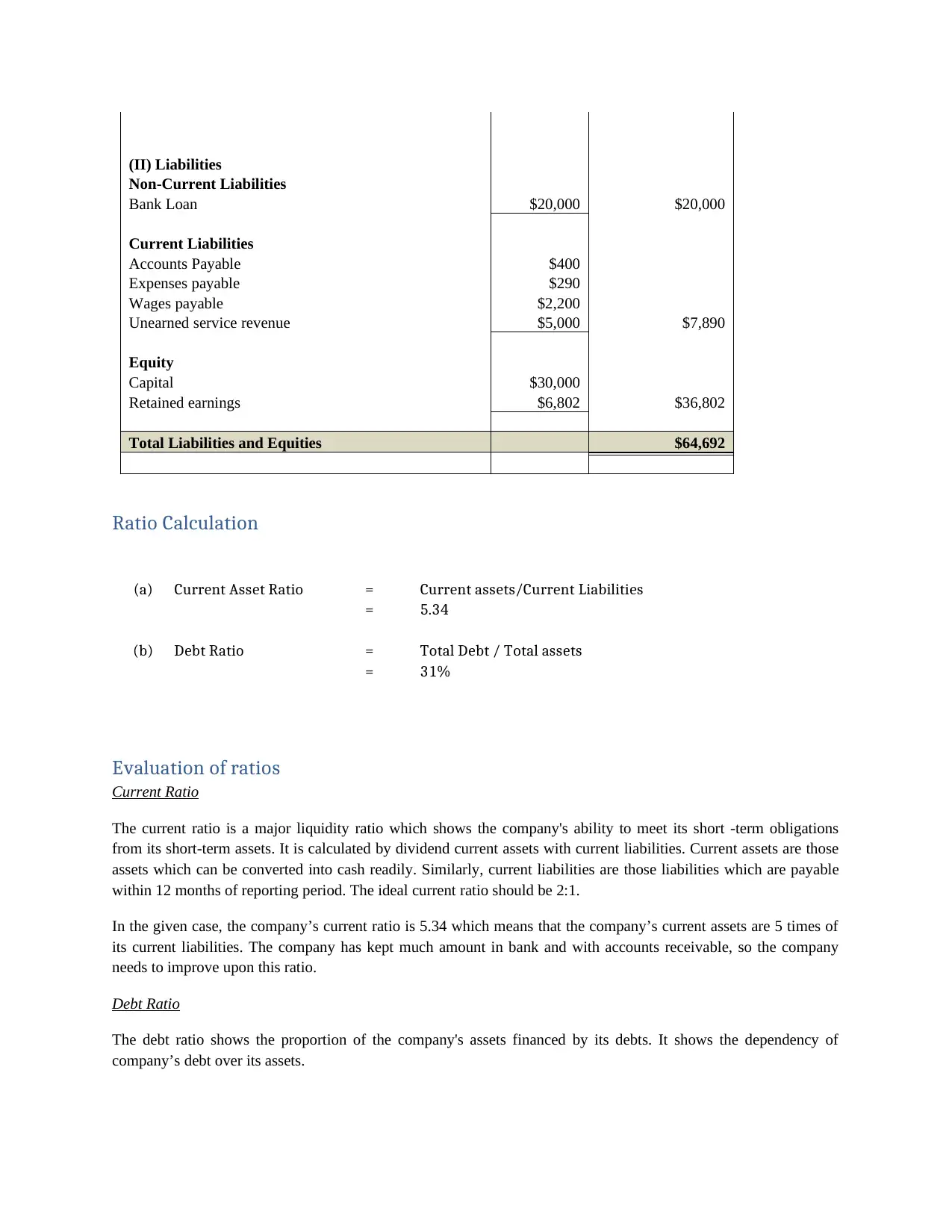

(II) Liabilities

Non-Current Liabilities

Bank Loan $20,000 $20,000

Current Liabilities

Accounts Payable $400

Expenses payable $290

Wages payable $2,200

Unearned service revenue $5,000 $7,890

Equity

Capital $30,000

Retained earnings $6,802 $36,802

Total Liabilities and Equities $64,692

Ratio Calculation

(a) Current Asset Ratio = Current assets/Current Liabilities

= 5.34

(b) Debt Ratio = Total Debt / Total assets

= 31%

Evaluation of ratios

Current Ratio

The current ratio is a major liquidity ratio which shows the company's ability to meet its short -term obligations

from its short-term assets. It is calculated by dividend current assets with current liabilities. Current assets are those

assets which can be converted into cash readily. Similarly, current liabilities are those liabilities which are payable

within 12 months of reporting period. The ideal current ratio should be 2:1.

In the given case, the company’s current ratio is 5.34 which means that the company’s current assets are 5 times of

its current liabilities. The company has kept much amount in bank and with accounts receivable, so the company

needs to improve upon this ratio.

Debt Ratio

The debt ratio shows the proportion of the company's assets financed by its debts. It shows the dependency of

company’s debt over its assets.

Non-Current Liabilities

Bank Loan $20,000 $20,000

Current Liabilities

Accounts Payable $400

Expenses payable $290

Wages payable $2,200

Unearned service revenue $5,000 $7,890

Equity

Capital $30,000

Retained earnings $6,802 $36,802

Total Liabilities and Equities $64,692

Ratio Calculation

(a) Current Asset Ratio = Current assets/Current Liabilities

= 5.34

(b) Debt Ratio = Total Debt / Total assets

= 31%

Evaluation of ratios

Current Ratio

The current ratio is a major liquidity ratio which shows the company's ability to meet its short -term obligations

from its short-term assets. It is calculated by dividend current assets with current liabilities. Current assets are those

assets which can be converted into cash readily. Similarly, current liabilities are those liabilities which are payable

within 12 months of reporting period. The ideal current ratio should be 2:1.

In the given case, the company’s current ratio is 5.34 which means that the company’s current assets are 5 times of

its current liabilities. The company has kept much amount in bank and with accounts receivable, so the company

needs to improve upon this ratio.

Debt Ratio

The debt ratio shows the proportion of the company's assets financed by its debts. It shows the dependency of

company’s debt over its assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.