Fleet Highlands Cafe: Revenue, Spending, and Variance Analysis Report

VerifiedAdded on 2023/01/10

|9

|2130

|21

Report

AI Summary

This report analyzes the Fleet Highlands Cafe's budget, revenue, and spending variances for March 2019. It begins by outlining the objectives of preparing a budget, including comparing results, providing structure, and guiding managerial decisions. The main body then presents the revenue and spending variances, differentiating between favorable and unfavorable outcomes. The analysis reveals variances in raw materials, wages, utilities, facility rent, insurance, and fuel. The report emphasizes that management should focus on these variances and offers advice to maintain profitability and sustainability, such as developing a strategic plan and conducting a financial stress test. In conclusion, the report summarizes the variances and highlights the importance of financial planning for the cafe's future growth.

Human Resource

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

(a) Objective of preparing of budget for fleet highland cafe....................................................................3

(b) Showing the company’s revenue and spending variance for March...................................................4

(c) Variance should be concern to management......................................................................................5

(d) Advise to maintain their profitability and sustainability going forward.............................................7

CONCLUSION...........................................................................................................................................7

REFRENCES..............................................................................................................................................8

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

(a) Objective of preparing of budget for fleet highland cafe....................................................................3

(b) Showing the company’s revenue and spending variance for March...................................................4

(c) Variance should be concern to management......................................................................................5

(d) Advise to maintain their profitability and sustainability going forward.............................................7

CONCLUSION...........................................................................................................................................7

REFRENCES..............................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management of human resources is a systematic mechanism in which the necessary

manpower is acquired and engaged, suited for the position and associated only with production,

maintenance and exploitation of the working population (Adler and et. al, 2017). Human

resources management is planning, organizing, monitoring and controlling the implementation,

intensity and segregation of living thing activities in order to meet individual, organizational and

organizational change. Company's basic task is to put staff and company on the very same forum

but at the same time achieve the personal goals and also strategic performance. This report has

been based on the Fleet Highlands café company. It is providing meals for tourists and citizen

kitchen at the local report. This report covers the main objective of preparing budget, presenting

the revenues & spending variance of the café. Moreover, variance concern with management and

provide suggestions to maintain profitability and sustainability for longer period of time.

MAIN BODY

(a) Objective of preparing of budget for fleet highland cafe

The budget is defined as an objective document, reflecting a monetary projection of the

administration's revenue and spending for a given period. Budget is a supposed to make in cost

accounting, planned before every given time to act as an estimation of projected revenues and tax

payments. A budget is often used to predict future and organizations financial outcomes and

financial condition over a future time period. It can be used for scheduling and measuring

production objectives that may include expenditure on current assets, implementing new goods,

coaching employees, setting referral bonus proposals, relay module, etc. The Fleet café prepare

budget to predict the business activities for future. There are defined various objectives to

prepare of budget such as:

Comparing results: Another goal of a budget would provide a comparative analysis outcomes

with those previously paid, and to evaluate and interpret variances by roles and responsibilities to

identify course work of enforcement measures and result in better in career intentions. The café

fleet uses of budgeting method to compare results and take right decision for the business growth

and development.

Management of human resources is a systematic mechanism in which the necessary

manpower is acquired and engaged, suited for the position and associated only with production,

maintenance and exploitation of the working population (Adler and et. al, 2017). Human

resources management is planning, organizing, monitoring and controlling the implementation,

intensity and segregation of living thing activities in order to meet individual, organizational and

organizational change. Company's basic task is to put staff and company on the very same forum

but at the same time achieve the personal goals and also strategic performance. This report has

been based on the Fleet Highlands café company. It is providing meals for tourists and citizen

kitchen at the local report. This report covers the main objective of preparing budget, presenting

the revenues & spending variance of the café. Moreover, variance concern with management and

provide suggestions to maintain profitability and sustainability for longer period of time.

MAIN BODY

(a) Objective of preparing of budget for fleet highland cafe

The budget is defined as an objective document, reflecting a monetary projection of the

administration's revenue and spending for a given period. Budget is a supposed to make in cost

accounting, planned before every given time to act as an estimation of projected revenues and tax

payments. A budget is often used to predict future and organizations financial outcomes and

financial condition over a future time period. It can be used for scheduling and measuring

production objectives that may include expenditure on current assets, implementing new goods,

coaching employees, setting referral bonus proposals, relay module, etc. The Fleet café prepare

budget to predict the business activities for future. There are defined various objectives to

prepare of budget such as:

Comparing results: Another goal of a budget would provide a comparative analysis outcomes

with those previously paid, and to evaluate and interpret variances by roles and responsibilities to

identify course work of enforcement measures and result in better in career intentions. The café

fleet uses of budgeting method to compare results and take right decision for the business growth

and development.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Provide structure: A budget is extremely effective in giving instructions to an organization

about the direction it is expected to go in. Therefore, it builds the basis on which to decide what

to do about it. A CEO will be well served to enforce a budget on a corporation which has no

clear direction. In example, a plan does not have a lot of concentration if the CEO documents the

expenditure immediately and does not update this until coming years. A budget offers only a

small level of support as place orders relates to it, and measures job satisfaction depending on the

specification established inside it (Bornay-Barrachina, López-Cabrales and Valle-Cabrera, 2017)

.

Provide guidance: Budget can help choose a framework for managerial decisions in schedule

changes and priorities if circumstances change uncontrollably. With the help of budget the Fleet

café understands that how to execute different activities in different situations. As a result it

helps to expand business activities at large level.

(b) Showing the company’s revenue and spending variance for March

Revenue variance: Revenue variance is the distinct between, based on the actual volume

of engagement, how much more the income ought to have been and the buyer behavior for the

time frame. A beneficial (undesirable) income variation arises when, regardless of actual level of

the organization for the time, the income is greater (less) as planned.

Spending variance: Spending variance is the difference among, due to the expected level

of operation, how often a cost would have been and the expected sum of the expense. A desirable

(unpleasant) variation in expenditure arises since, given the real volume of engagement for the

era, the price is reduced (greater) than anticipated.

Revenue/cost

formulas

Planning Actual Revenue and

spending

variance

Budgeted meals

quantity

(q) 20000 18000 2000 (F)

Revenues (5.00q) £100 000 £90 000 £10000 (F)

Expenses

Raw material (£2.50q 50000 45000 5000 (F)

about the direction it is expected to go in. Therefore, it builds the basis on which to decide what

to do about it. A CEO will be well served to enforce a budget on a corporation which has no

clear direction. In example, a plan does not have a lot of concentration if the CEO documents the

expenditure immediately and does not update this until coming years. A budget offers only a

small level of support as place orders relates to it, and measures job satisfaction depending on the

specification established inside it (Bornay-Barrachina, López-Cabrales and Valle-Cabrera, 2017)

.

Provide guidance: Budget can help choose a framework for managerial decisions in schedule

changes and priorities if circumstances change uncontrollably. With the help of budget the Fleet

café understands that how to execute different activities in different situations. As a result it

helps to expand business activities at large level.

(b) Showing the company’s revenue and spending variance for March

Revenue variance: Revenue variance is the distinct between, based on the actual volume

of engagement, how much more the income ought to have been and the buyer behavior for the

time frame. A beneficial (undesirable) income variation arises when, regardless of actual level of

the organization for the time, the income is greater (less) as planned.

Spending variance: Spending variance is the difference among, due to the expected level

of operation, how often a cost would have been and the expected sum of the expense. A desirable

(unpleasant) variation in expenditure arises since, given the real volume of engagement for the

era, the price is reduced (greater) than anticipated.

Revenue/cost

formulas

Planning Actual Revenue and

spending

variance

Budgeted meals

quantity

(q) 20000 18000 2000 (F)

Revenues (5.00q) £100 000 £90 000 £10000 (F)

Expenses

Raw material (£2.50q 50000 45000 5000 (F)

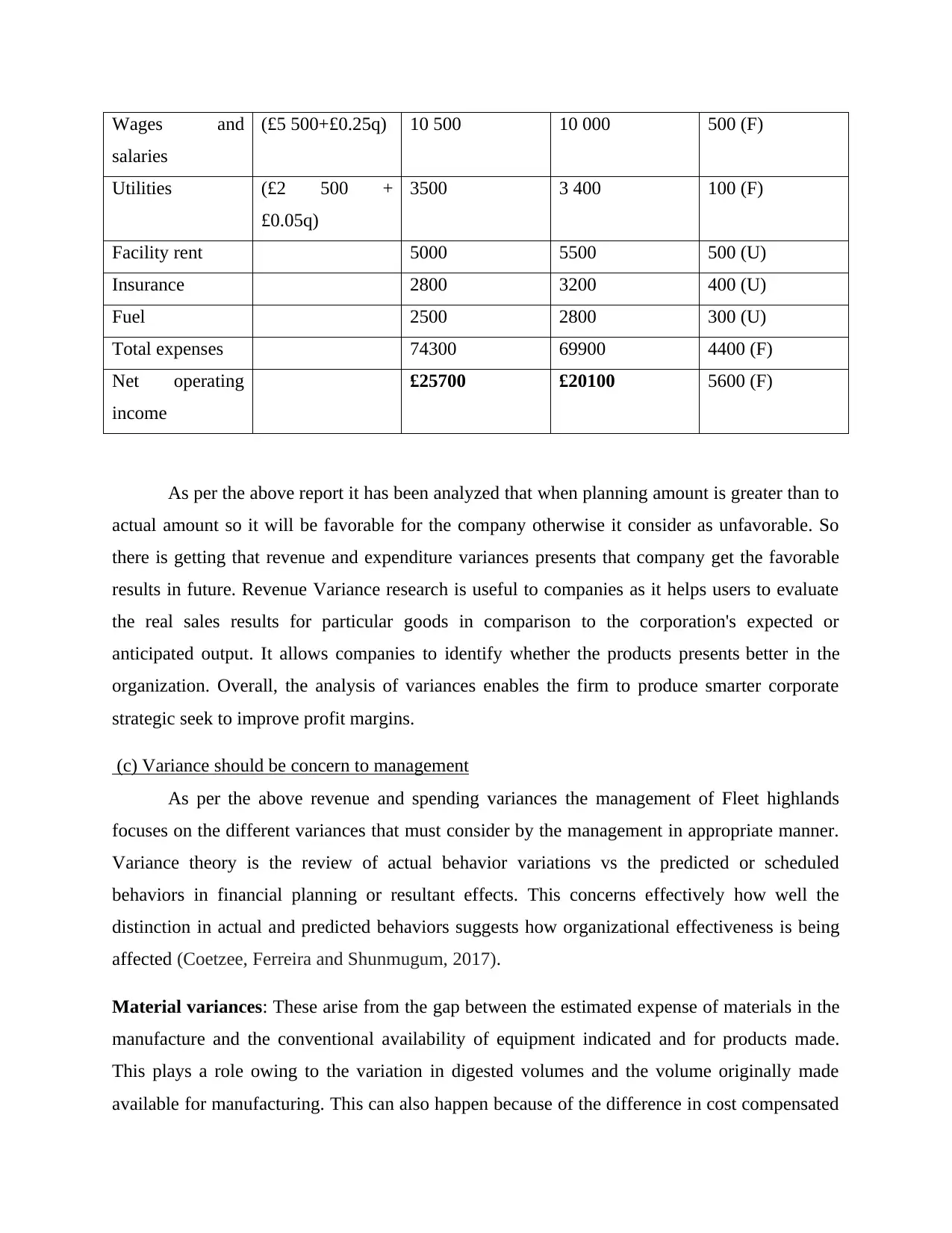

Wages and

salaries

(£5 500+£0.25q) 10 500 10 000 500 (F)

Utilities (£2 500 +

£0.05q)

3500 3 400 100 (F)

Facility rent 5000 5500 500 (U)

Insurance 2800 3200 400 (U)

Fuel 2500 2800 300 (U)

Total expenses 74300 69900 4400 (F)

Net operating

income

£25700 £20100 5600 (F)

As per the above report it has been analyzed that when planning amount is greater than to

actual amount so it will be favorable for the company otherwise it consider as unfavorable. So

there is getting that revenue and expenditure variances presents that company get the favorable

results in future. Revenue Variance research is useful to companies as it helps users to evaluate

the real sales results for particular goods in comparison to the corporation's expected or

anticipated output. It allows companies to identify whether the products presents better in the

organization. Overall, the analysis of variances enables the firm to produce smarter corporate

strategic seek to improve profit margins.

(c) Variance should be concern to management

As per the above revenue and spending variances the management of Fleet highlands

focuses on the different variances that must consider by the management in appropriate manner.

Variance theory is the review of actual behavior variations vs the predicted or scheduled

behaviors in financial planning or resultant effects. This concerns effectively how well the

distinction in actual and predicted behaviors suggests how organizational effectiveness is being

affected (Coetzee, Ferreira and Shunmugum, 2017).

Material variances: These arise from the gap between the estimated expense of materials in the

manufacture and the conventional availability of equipment indicated and for products made.

This plays a role owing to the variation in digested volumes and the volume originally made

available for manufacturing. This can also happen because of the difference in cost compensated

salaries

(£5 500+£0.25q) 10 500 10 000 500 (F)

Utilities (£2 500 +

£0.05q)

3500 3 400 100 (F)

Facility rent 5000 5500 500 (U)

Insurance 2800 3200 400 (U)

Fuel 2500 2800 300 (U)

Total expenses 74300 69900 4400 (F)

Net operating

income

£25700 £20100 5600 (F)

As per the above report it has been analyzed that when planning amount is greater than to

actual amount so it will be favorable for the company otherwise it consider as unfavorable. So

there is getting that revenue and expenditure variances presents that company get the favorable

results in future. Revenue Variance research is useful to companies as it helps users to evaluate

the real sales results for particular goods in comparison to the corporation's expected or

anticipated output. It allows companies to identify whether the products presents better in the

organization. Overall, the analysis of variances enables the firm to produce smarter corporate

strategic seek to improve profit margins.

(c) Variance should be concern to management

As per the above revenue and spending variances the management of Fleet highlands

focuses on the different variances that must consider by the management in appropriate manner.

Variance theory is the review of actual behavior variations vs the predicted or scheduled

behaviors in financial planning or resultant effects. This concerns effectively how well the

distinction in actual and predicted behaviors suggests how organizational effectiveness is being

affected (Coetzee, Ferreira and Shunmugum, 2017).

Material variances: These arise from the gap between the estimated expense of materials in the

manufacture and the conventional availability of equipment indicated and for products made.

This plays a role owing to the variation in digested volumes and the volume originally made

available for manufacturing. This can also happen because of the difference in cost compensated

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and the market value money earmarked for the components was using. The difference in cost for

direct products is defined as the difference in purchase price, which is the real cost per unit of

output less the normal price per unit, compounded by the amount of items bought.

Labor variances: The difference in expenditure on manufacturing overhead is defined as the

difference in the labor rate, which is the real labor price each day less the regular rate each hour,

compounded by the average hours worked. This denotes the employee's wages given to

employees as opposed to the traditional pay prevailing for the defined production. The variance

is the difference, if the actual labor costs will be more than that money earmarked.

Overhead variances: It can be expressed as the sum effective cost of ingredients, labor, and

expenses. Overhead differences could emerge because of the variation between the budget period

conventional capital expenses and the fixed overhead extra costs.

Fixed overhead: The variability in expenditure for fixed overhead is recognized as the

variability in variable production expenditure. It is the real expenditure incurred minus the

expenditure total budget.

Variable overhead: The actual costs expenditure variability is recognized as the actual costs

expenditure variability, and is the standard costs rate except for the overhead absorption rate,

equal to the number of distribution basis components (DeGeest and et. al, 2017).

Volume variances: The volume variance calculates the gap between the estimated amounts sold

or purchased and the amount budgeted for purchase or sale, standard cost price per item. The

variance in quantity is a basic indicator about whether the company generates the quantity of

products this had scheduled.

Purchase price variances: Buy Price Variance outcomes when the real value charged for

materials differs from the estimated budget for that equipment. It is normally used as a negative

factor to measure the supply chain component's effectiveness.

direct products is defined as the difference in purchase price, which is the real cost per unit of

output less the normal price per unit, compounded by the amount of items bought.

Labor variances: The difference in expenditure on manufacturing overhead is defined as the

difference in the labor rate, which is the real labor price each day less the regular rate each hour,

compounded by the average hours worked. This denotes the employee's wages given to

employees as opposed to the traditional pay prevailing for the defined production. The variance

is the difference, if the actual labor costs will be more than that money earmarked.

Overhead variances: It can be expressed as the sum effective cost of ingredients, labor, and

expenses. Overhead differences could emerge because of the variation between the budget period

conventional capital expenses and the fixed overhead extra costs.

Fixed overhead: The variability in expenditure for fixed overhead is recognized as the

variability in variable production expenditure. It is the real expenditure incurred minus the

expenditure total budget.

Variable overhead: The actual costs expenditure variability is recognized as the actual costs

expenditure variability, and is the standard costs rate except for the overhead absorption rate,

equal to the number of distribution basis components (DeGeest and et. al, 2017).

Volume variances: The volume variance calculates the gap between the estimated amounts sold

or purchased and the amount budgeted for purchase or sale, standard cost price per item. The

variance in quantity is a basic indicator about whether the company generates the quantity of

products this had scheduled.

Purchase price variances: Buy Price Variance outcomes when the real value charged for

materials differs from the estimated budget for that equipment. It is normally used as a negative

factor to measure the supply chain component's effectiveness.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(d) Advise to maintain their profitability and sustainability going forward

There are providing the advice to Fleet Highlands café to maintain profitability and

sustainability going forward such as:

Develop a strategic plan: Businesses that speak the peaks and troughs of the economic

system share so many characteristics that add functionality continuously. Such companies are

offering convincing items / solutions, both from consumer and tactical points of view. They have

sound majority stakes and solid financial statements. They preserve a pricing structure which is

flexible. And those who schedule to take advantage of opportunities forward with and can

distribute information rapidly to confiscate those possibilities. The café must produce a plan for

maintain effective profitability in efficient way (Newman, Rose and Teo, 2016).

Conduct a financial stress test: A key strategic plan is an interconnected financial model based

on assumptions which involves a predicted statement of income, financial statements, cash flows

and, in which appropriate, measurement of the debt base. This method can also be used to

evaluate how your corporation would execute if the effect of a prospective downturn on

maximum volumes of trade is same as previous recessions.

Checklist: Improving the profitability of businesses can help lower costs, increase turnover and

efficiency, and ensure the comfort for development and improvement. The success of the

company will vary depending on a number of considerations-such as the finance industry

working in, the nature of the firm or its operational costs.

CONCLUSION

As per the above report it has been concluded that the café can analysis various variances

in order to conduct various activities. These variances mainly categorize into revenues and

spending. The café must focus on the various plan that will use by them for maintain profitability

s well as for sustainability growth.

There are providing the advice to Fleet Highlands café to maintain profitability and

sustainability going forward such as:

Develop a strategic plan: Businesses that speak the peaks and troughs of the economic

system share so many characteristics that add functionality continuously. Such companies are

offering convincing items / solutions, both from consumer and tactical points of view. They have

sound majority stakes and solid financial statements. They preserve a pricing structure which is

flexible. And those who schedule to take advantage of opportunities forward with and can

distribute information rapidly to confiscate those possibilities. The café must produce a plan for

maintain effective profitability in efficient way (Newman, Rose and Teo, 2016).

Conduct a financial stress test: A key strategic plan is an interconnected financial model based

on assumptions which involves a predicted statement of income, financial statements, cash flows

and, in which appropriate, measurement of the debt base. This method can also be used to

evaluate how your corporation would execute if the effect of a prospective downturn on

maximum volumes of trade is same as previous recessions.

Checklist: Improving the profitability of businesses can help lower costs, increase turnover and

efficiency, and ensure the comfort for development and improvement. The success of the

company will vary depending on a number of considerations-such as the finance industry

working in, the nature of the firm or its operational costs.

CONCLUSION

As per the above report it has been concluded that the café can analysis various variances

in order to conduct various activities. These variances mainly categorize into revenues and

spending. The café must focus on the various plan that will use by them for maintain profitability

s well as for sustainability growth.

REFRENCES

Books and Journal

Adler, P. and et. al, 2017. Do factory managers know what workers want? Manager–worker

information asymmetries and pareto optimal human resource management policies. Asian

Development Review. 34(1). pp.65-87.

Bornay-Barrachina, M., López-Cabrales, A. and Valle-Cabrera, R., 2017. How do employment

relationships enhance firm innovation? The role of human and social capital. The

InTernaTIonal Journal of human resource management. 28(9). pp.1363-1391.

Coetzee, M., Ferreira, N. and Shunmugum, C., 2017. Psychological career resources, career

adaptability and work engagement of generational cohorts in the media industry. SA

Journal of Human Resource Management. 15. p.12.

DeGeest, D. S. and et. al, 2017. Retracted: The benefits of benefits: A dynamic approach to

motivation-enhancing human resource practices and entrepreneurial survival. Journal of

Management. 43(7). pp.2303-2332.

Newman, A., Rose, P. S. and Teo, S. T., 2016. The role of participative leadership and trust‐

based mechanisms in eliciting intern performance: Evidence from China. Human

Resource Management. 55(1). pp.53-67.

Ouyang, C., Liu, X. and Zhang, Z., 2016. Organizational and regional influences on the adoption

of high-involvement human resource systems in China: Evidence from service

establishments. The International Journal of Human Resource Management. 27(18).

pp.2058-2074.

Roh, H. and Kim, E., 2016. The business case for gender diversity: Examining the role of human

resource management investments. Human Resource Management. 55(3). pp.519-534.

Books and Journal

Adler, P. and et. al, 2017. Do factory managers know what workers want? Manager–worker

information asymmetries and pareto optimal human resource management policies. Asian

Development Review. 34(1). pp.65-87.

Bornay-Barrachina, M., López-Cabrales, A. and Valle-Cabrera, R., 2017. How do employment

relationships enhance firm innovation? The role of human and social capital. The

InTernaTIonal Journal of human resource management. 28(9). pp.1363-1391.

Coetzee, M., Ferreira, N. and Shunmugum, C., 2017. Psychological career resources, career

adaptability and work engagement of generational cohorts in the media industry. SA

Journal of Human Resource Management. 15. p.12.

DeGeest, D. S. and et. al, 2017. Retracted: The benefits of benefits: A dynamic approach to

motivation-enhancing human resource practices and entrepreneurial survival. Journal of

Management. 43(7). pp.2303-2332.

Newman, A., Rose, P. S. and Teo, S. T., 2016. The role of participative leadership and trust‐

based mechanisms in eliciting intern performance: Evidence from China. Human

Resource Management. 55(1). pp.53-67.

Ouyang, C., Liu, X. and Zhang, Z., 2016. Organizational and regional influences on the adoption

of high-involvement human resource systems in China: Evidence from service

establishments. The International Journal of Human Resource Management. 27(18).

pp.2058-2074.

Roh, H. and Kim, E., 2016. The business case for gender diversity: Examining the role of human

resource management investments. Human Resource Management. 55(3). pp.519-534.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.