Tax Analysis of Fleetwood Corporation's Financial Statements

VerifiedAdded on 2020/05/16

|17

|2837

|55

Report

AI Summary

This report provides a comprehensive analysis of Fleetwood Corporation's financial statements, focusing on key aspects of tax and equity. It begins with an introduction to the financial statement analysis, followed by a discussion of equity items like issued capital, reserves, and retained earnings and the reasons for changes in these items. The report then critically examines the tax expense provided in the financial statements, comparing accounting income with income tax expense, and explaining the relationship between deferred tax assets and liabilities. The analysis further explores the differences between income tax payable and income tax expenses, as well as the relationship between income tax payments and expenses as presented in the cash flow statement. The report concludes with insights learned and a summary of the key findings, emphasizing the importance of understanding various tax-related items in financial reporting. The report leverages the annual reports of Fleetwood Corporation to critically assess the company's financial performance and position.

Running head: TAX

Tax

Name of the Student:

Name of the University:

Authors Note:

Tax

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAX

Table of Contents

Introduction:....................................................................................................................................2

Discussion related to Items of equity and reason for change..........................................................2

Tax expense provided in the financial statement:............................................................................3

Accounting income and income tax expense:.................................................................................3

Deferred tax assets and deferred tax liabilities:...............................................................................3

Income tax payable and comparing with income tax expenses:......................................................6

Income tax payment and income tax expense:................................................................................7

Insights learned:...............................................................................................................................8

Conclusion:......................................................................................................................................9

Reference.......................................................................................................................................10

Appendix 1:...................................................................................................................................12

Appendix 2:...................................................................................................................................13

Appendix 3:...................................................................................................................................14

Appendix 4:...................................................................................................................................15

Table of Contents

Introduction:....................................................................................................................................2

Discussion related to Items of equity and reason for change..........................................................2

Tax expense provided in the financial statement:............................................................................3

Accounting income and income tax expense:.................................................................................3

Deferred tax assets and deferred tax liabilities:...............................................................................3

Income tax payable and comparing with income tax expenses:......................................................6

Income tax payment and income tax expense:................................................................................7

Insights learned:...............................................................................................................................8

Conclusion:......................................................................................................................................9

Reference.......................................................................................................................................10

Appendix 1:...................................................................................................................................12

Appendix 2:...................................................................................................................................13

Appendix 3:...................................................................................................................................14

Appendix 4:...................................................................................................................................15

2TAX

Introduction:

In this report, an attempt is made to analyse the financial statement of Fleetwood

Corporation. The Annual reports of the company contain all necessary information, financial as

well as non-financial, to assess the performance and position of an entity. However, it is

important to have proper knowledge about different items in financial statements to understand

the actual implication of different items in the financial statements. The main aim of this report

is to critically analyse the significant areas related to movement in equity and tax expenses.

Discussion related to Items of equity and reason for change

Issued capital:

Fleetwood Corporation has issued equity shares to the public to arrange the required

amount of funds to finance the operations of the company. Issued capital represents that part of

the capital which has been issued and subscribed by the shareholders of the company. The issued

capital of the company is $195,079m for the financial year ending in 2016.

Reserves:

The company has created different reserves to be used for specific purposes. These

reserves are not allowed to be used for distribution of dividend. Thus, these are not free reserves

and are to be used only for specific purposes. The amount of reserves that the company has at the

end of the financial year 2016 is $244m (Muller and Kolk 2015).

Retained earnings:

The company has retained earnings of $8,508m in the financial year 2016 that is the

accumulated balance of profit over the years. The balance of profit that have not been distributed

Introduction:

In this report, an attempt is made to analyse the financial statement of Fleetwood

Corporation. The Annual reports of the company contain all necessary information, financial as

well as non-financial, to assess the performance and position of an entity. However, it is

important to have proper knowledge about different items in financial statements to understand

the actual implication of different items in the financial statements. The main aim of this report

is to critically analyse the significant areas related to movement in equity and tax expenses.

Discussion related to Items of equity and reason for change

Issued capital:

Fleetwood Corporation has issued equity shares to the public to arrange the required

amount of funds to finance the operations of the company. Issued capital represents that part of

the capital which has been issued and subscribed by the shareholders of the company. The issued

capital of the company is $195,079m for the financial year ending in 2016.

Reserves:

The company has created different reserves to be used for specific purposes. These

reserves are not allowed to be used for distribution of dividend. Thus, these are not free reserves

and are to be used only for specific purposes. The amount of reserves that the company has at the

end of the financial year 2016 is $244m (Muller and Kolk 2015).

Retained earnings:

The company has retained earnings of $8,508m in the financial year 2016 that is the

accumulated balance of profit over the years. The balance of profit that have not been distributed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAX

by the company neither transferred for any specific purposes to any reserves (Alstadsæter et al.

2016).

Tax expense provided in the financial statement:

The company recorded current tax benefit in the income statement for the financial year

2016 of $1531m as against a tax expense of $508m in the previous year 2015.

Comparing the income tax expenses and the Accounting income:

No, the current tax expense or benefit in this case is not similar to that of the tax rate

multiplied to the income of the company. In-fact the company incurred a loss from the business

operations in the financial year 2016 (Dowling 2015). The reason for the difference is that there

are other tax items such as deferred tax assets, deferred tax liabilities, advance tax which are

adjusted against the current tax liabilities to determine the amount of current tax expense or

benefit which is to be provided in the profit and loss account of an entity.

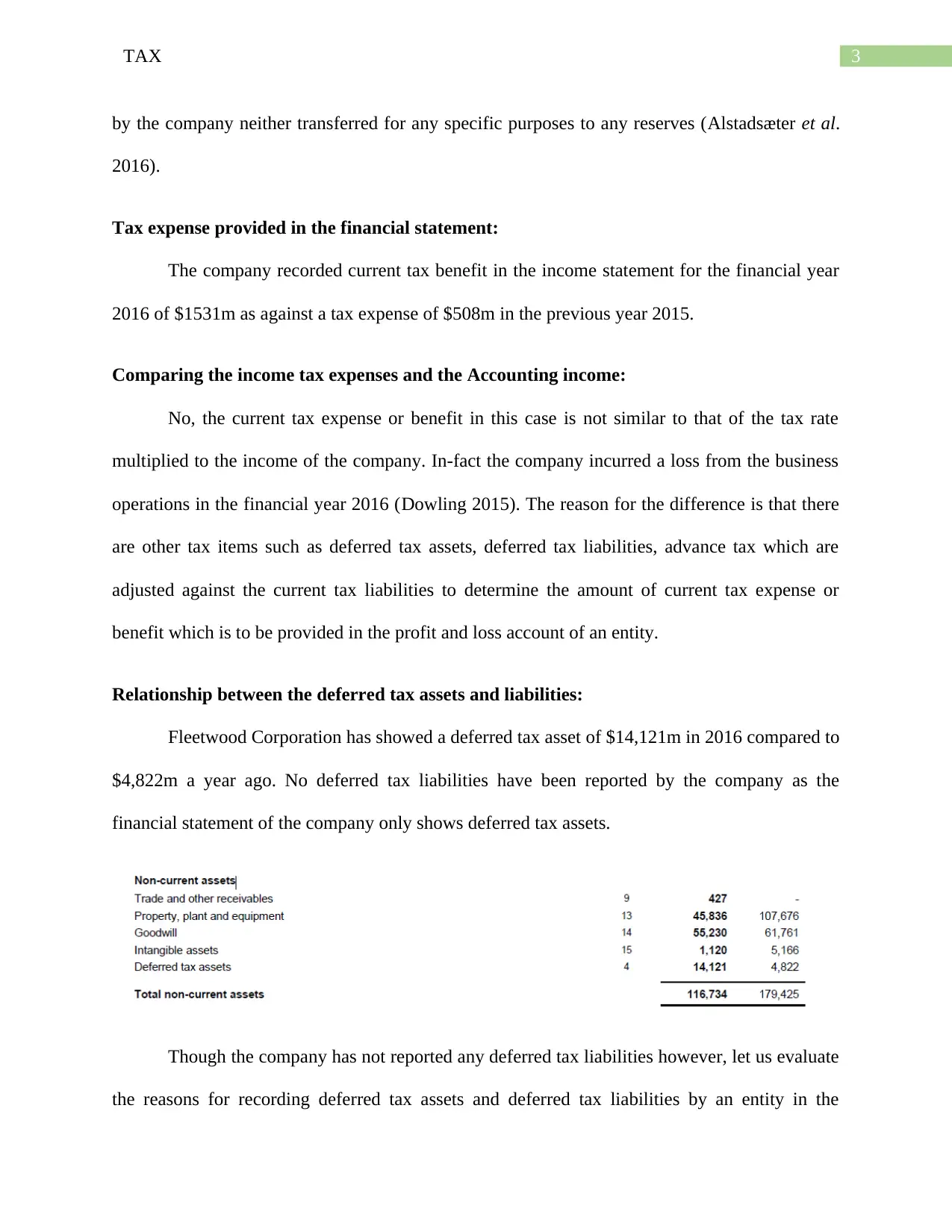

Relationship between the deferred tax assets and liabilities:

Fleetwood Corporation has showed a deferred tax asset of $14,121m in 2016 compared to

$4,822m a year ago. No deferred tax liabilities have been reported by the company as the

financial statement of the company only shows deferred tax assets.

Though the company has not reported any deferred tax liabilities however, let us evaluate

the reasons for recording deferred tax assets and deferred tax liabilities by an entity in the

by the company neither transferred for any specific purposes to any reserves (Alstadsæter et al.

2016).

Tax expense provided in the financial statement:

The company recorded current tax benefit in the income statement for the financial year

2016 of $1531m as against a tax expense of $508m in the previous year 2015.

Comparing the income tax expenses and the Accounting income:

No, the current tax expense or benefit in this case is not similar to that of the tax rate

multiplied to the income of the company. In-fact the company incurred a loss from the business

operations in the financial year 2016 (Dowling 2015). The reason for the difference is that there

are other tax items such as deferred tax assets, deferred tax liabilities, advance tax which are

adjusted against the current tax liabilities to determine the amount of current tax expense or

benefit which is to be provided in the profit and loss account of an entity.

Relationship between the deferred tax assets and liabilities:

Fleetwood Corporation has showed a deferred tax asset of $14,121m in 2016 compared to

$4,822m a year ago. No deferred tax liabilities have been reported by the company as the

financial statement of the company only shows deferred tax assets.

Though the company has not reported any deferred tax liabilities however, let us evaluate

the reasons for recording deferred tax assets and deferred tax liabilities by an entity in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAX

financial statements. Before directly getting into the reasons for creation of deferred tax

liabilities or assets in the financial statements of an entity let us provide brief descriptions on

deferred tax assets and deferred tax liabilities.

Deferred tax asset is created due to the difference between the accounting profits and

taxable profits calculated in accordance with the provisions of income tax rules. The accounting

profits are calculated by an entity in accordance with the accounting standards issued by the

Australian Accounting Standards Board (AASB) and in accordance with the provisions of the

Corporations Act, 2001. Whereas, the assessable profit of an entity is ascertained in accordance

with provisions of the Income Tax Assessment Act, 1997. Thus, the taxable profit on which the

amount of income tax has to be paid by an entity is seldom the same with that of the accounting

profit. In case the accounting profit is lower than the taxable profit, an entity generally

recognizes deferred tax assets in the books of account as long as the difference between the two

is due to the timing difference and not permanent difference (Cai et al. 2014).

In the report, discuss the reasons for creation of deferred tax assets in the books of

accounts of an entity. The following points broadly cover these reasons.

Difference amount of Depreciation under accounting and taxable provisions:

The income tax provisions have different rates that are allowed as depreciation on non-

current assets to determine the amount of taxable profit of an entity compare to the rates that

have been prescribed in AASB 116. Thus, in case the amount of depreciation is allowed under

the income tax act is lower than the amount of depreciation under AASB 116 then that will result

in creation of deferred tax assets (Towery 2015).

Expenditures disallowed by income tax provisions:

financial statements. Before directly getting into the reasons for creation of deferred tax

liabilities or assets in the financial statements of an entity let us provide brief descriptions on

deferred tax assets and deferred tax liabilities.

Deferred tax asset is created due to the difference between the accounting profits and

taxable profits calculated in accordance with the provisions of income tax rules. The accounting

profits are calculated by an entity in accordance with the accounting standards issued by the

Australian Accounting Standards Board (AASB) and in accordance with the provisions of the

Corporations Act, 2001. Whereas, the assessable profit of an entity is ascertained in accordance

with provisions of the Income Tax Assessment Act, 1997. Thus, the taxable profit on which the

amount of income tax has to be paid by an entity is seldom the same with that of the accounting

profit. In case the accounting profit is lower than the taxable profit, an entity generally

recognizes deferred tax assets in the books of account as long as the difference between the two

is due to the timing difference and not permanent difference (Cai et al. 2014).

In the report, discuss the reasons for creation of deferred tax assets in the books of

accounts of an entity. The following points broadly cover these reasons.

Difference amount of Depreciation under accounting and taxable provisions:

The income tax provisions have different rates that are allowed as depreciation on non-

current assets to determine the amount of taxable profit of an entity compare to the rates that

have been prescribed in AASB 116. Thus, in case the amount of depreciation is allowed under

the income tax act is lower than the amount of depreciation under AASB 116 then that will result

in creation of deferred tax assets (Towery 2015).

Expenditures disallowed by income tax provisions:

5TAX

The income tax provisions do not allow certain expenditures to calculate the taxable

profit on which income tax is to be charged which may have been deducted in computing the

accounting profit. Thus, the taxable profit will be higher in such case to result in creation of

deferred tax asset for the entity concerned (Dyreng and Markle 2016).

Incomes that may have been deferred to compute accounting profit of a year might needed to be

included to compute the taxable profit:

The taxable provisions might need an entity to record a particular income to be included

in the income statement to compute the taxable profit that might have been deferred to later

periods in the income statement prepared under the accounting rules of the country. As a result

of this the taxable profit of an entity will be higher than the accounting profit to create deferred

tax assets (Shen et al. 2016).

Deferred tax liabilities are also created due to the timing differences in accounting and

taxable provisions. The deferred tax liabilities will be created in case the accounting profit of an

entity is higher than the taxable profit ascertained in accordance with the provisions of the

income tax rules and regulations provided in the Income Tax Assessment Act, 1997.

The deferred tax liabilities are created for the following raesons:

Accounting profit higher than the taxable profit:

The accounting profit if is higher than the amount of taxable profit then an entity will

require to create deferred tax liabilities is the difference in taxable and accounting profit is due to

timing differences.

Higher amount of depreciation is allowed in the income tax rules:

The income tax provisions do not allow certain expenditures to calculate the taxable

profit on which income tax is to be charged which may have been deducted in computing the

accounting profit. Thus, the taxable profit will be higher in such case to result in creation of

deferred tax asset for the entity concerned (Dyreng and Markle 2016).

Incomes that may have been deferred to compute accounting profit of a year might needed to be

included to compute the taxable profit:

The taxable provisions might need an entity to record a particular income to be included

in the income statement to compute the taxable profit that might have been deferred to later

periods in the income statement prepared under the accounting rules of the country. As a result

of this the taxable profit of an entity will be higher than the accounting profit to create deferred

tax assets (Shen et al. 2016).

Deferred tax liabilities are also created due to the timing differences in accounting and

taxable provisions. The deferred tax liabilities will be created in case the accounting profit of an

entity is higher than the taxable profit ascertained in accordance with the provisions of the

income tax rules and regulations provided in the Income Tax Assessment Act, 1997.

The deferred tax liabilities are created for the following raesons:

Accounting profit higher than the taxable profit:

The accounting profit if is higher than the amount of taxable profit then an entity will

require to create deferred tax liabilities is the difference in taxable and accounting profit is due to

timing differences.

Higher amount of depreciation is allowed in the income tax rules:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAX

In case the taxable provisions allow higher rate of depreciation on non-current assets than

the rate prescribed and used to charge depreciation on non-current assets to calculate accounting

profit of an entity. In that case, the accounting profit will be higher than the amount calculated as

profit under taxable provisions (Bratten et al. 2016). As a result of this the entity will have to

create deferred tax liabilities in the books of accounts of an entity.

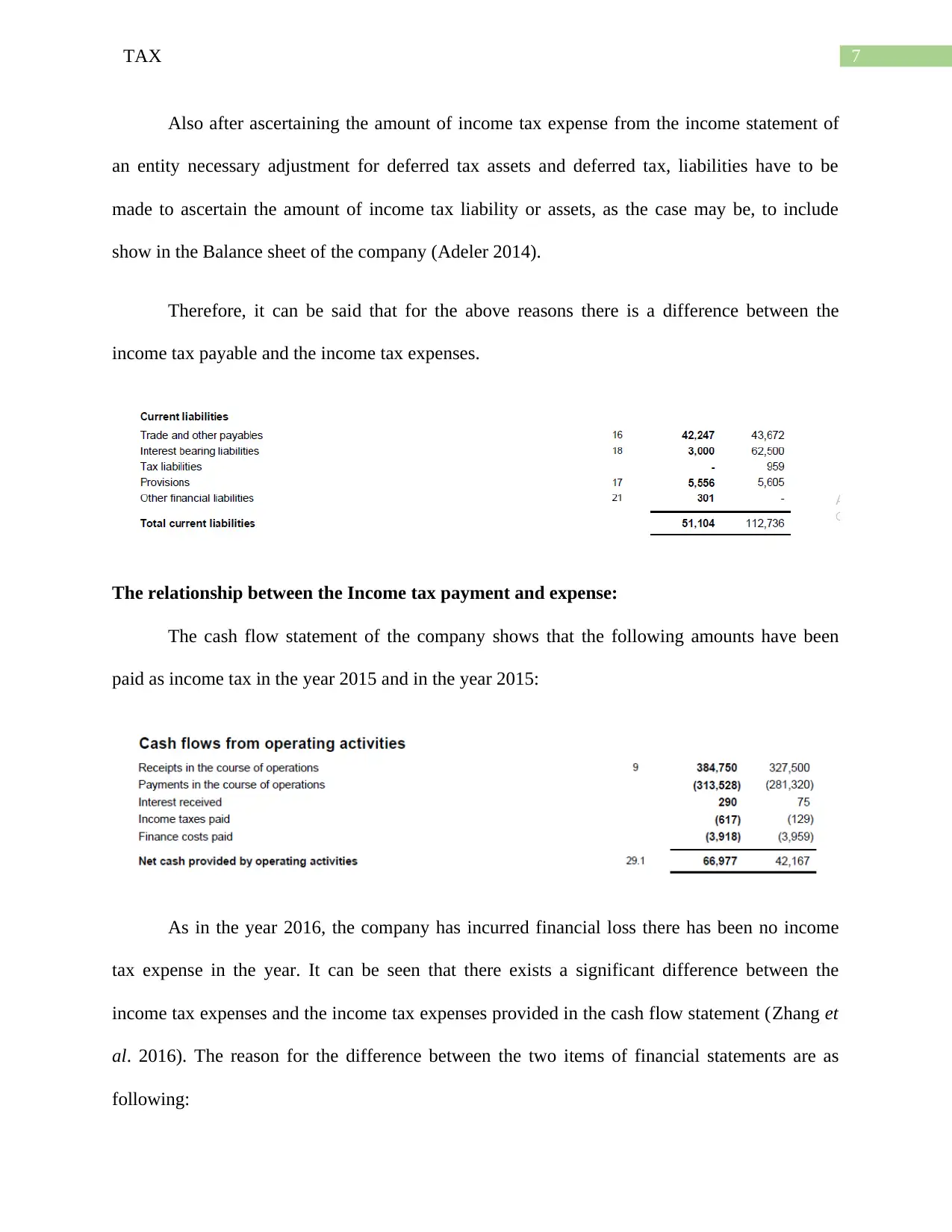

Comparing income tax expenses with income tax payable:

The company, i.e. Fleetwood Corporation, though has recorded any tax liabilities under

current liabilities as can be seen from the financial statements of the company for the financial

year ending in 2016 however, a year before the company did record an amount of $959m as

current tax liabilities (Rao 2016).

The reason are discussed below:

An entity often need to pay advance tax:

In case, an entity pays certain amount of advance tax on provisional income basis to

comply with the income tax rules and regulations in the country. In that case, it must be adjusted

against the income tax expense of the entity at the end of the financial year when the amount of

income tax is ascertained for the financial year (Agrawal et al. 2014). Generally the difference

between the income tax expense and advance amount of income tax is either recorded as the

amount of income tax payable or tax assets under current liabilities or current assets in the

statement of financial position as the case may be.

Adjustment of deferred tax items:

In case the taxable provisions allow higher rate of depreciation on non-current assets than

the rate prescribed and used to charge depreciation on non-current assets to calculate accounting

profit of an entity. In that case, the accounting profit will be higher than the amount calculated as

profit under taxable provisions (Bratten et al. 2016). As a result of this the entity will have to

create deferred tax liabilities in the books of accounts of an entity.

Comparing income tax expenses with income tax payable:

The company, i.e. Fleetwood Corporation, though has recorded any tax liabilities under

current liabilities as can be seen from the financial statements of the company for the financial

year ending in 2016 however, a year before the company did record an amount of $959m as

current tax liabilities (Rao 2016).

The reason are discussed below:

An entity often need to pay advance tax:

In case, an entity pays certain amount of advance tax on provisional income basis to

comply with the income tax rules and regulations in the country. In that case, it must be adjusted

against the income tax expense of the entity at the end of the financial year when the amount of

income tax is ascertained for the financial year (Agrawal et al. 2014). Generally the difference

between the income tax expense and advance amount of income tax is either recorded as the

amount of income tax payable or tax assets under current liabilities or current assets in the

statement of financial position as the case may be.

Adjustment of deferred tax items:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAX

Also after ascertaining the amount of income tax expense from the income statement of

an entity necessary adjustment for deferred tax assets and deferred tax, liabilities have to be

made to ascertain the amount of income tax liability or assets, as the case may be, to include

show in the Balance sheet of the company (Adeler 2014).

Therefore, it can be said that for the above reasons there is a difference between the

income tax payable and the income tax expenses.

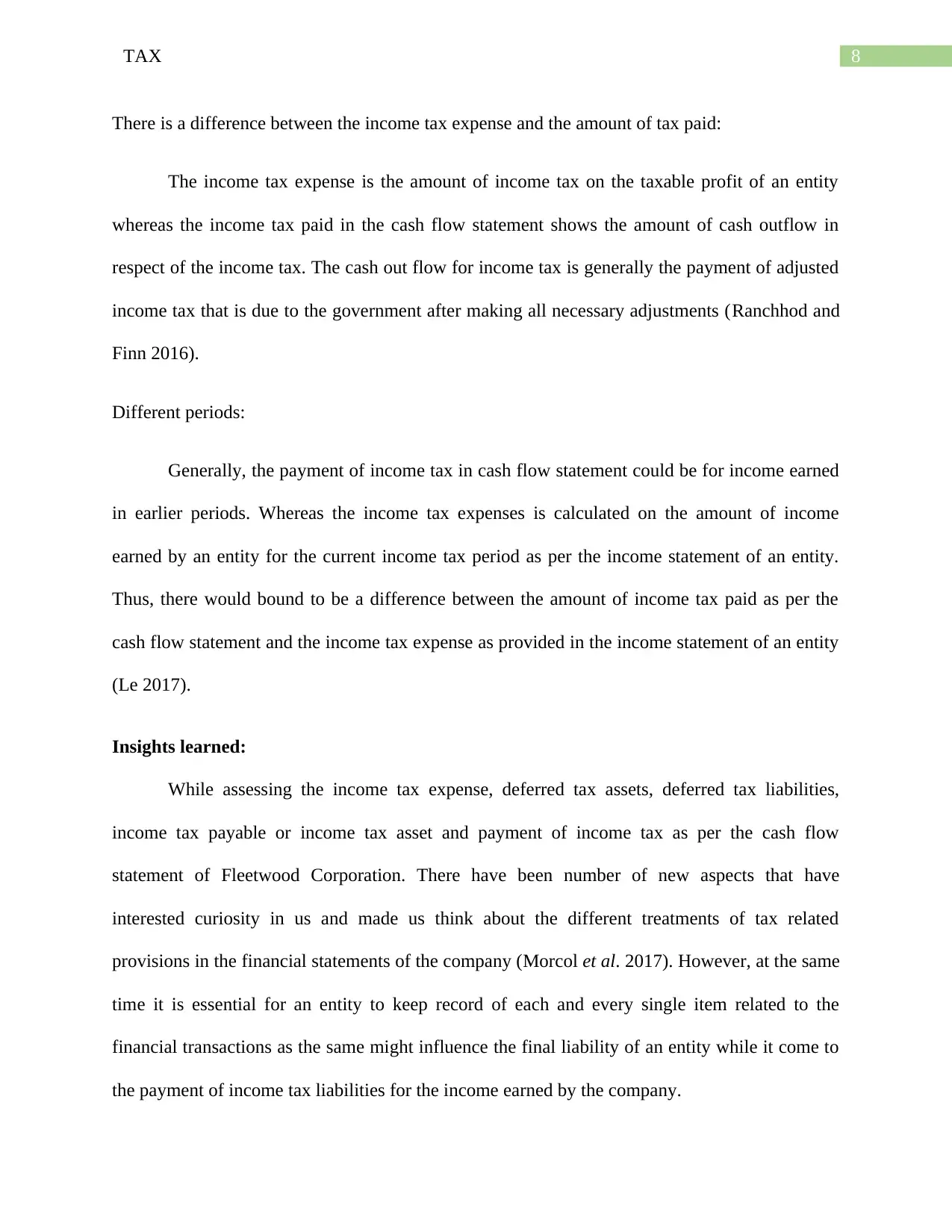

The relationship between the Income tax payment and expense:

The cash flow statement of the company shows that the following amounts have been

paid as income tax in the year 2015 and in the year 2015:

As in the year 2016, the company has incurred financial loss there has been no income

tax expense in the year. It can be seen that there exists a significant difference between the

income tax expenses and the income tax expenses provided in the cash flow statement (Zhang et

al. 2016). The reason for the difference between the two items of financial statements are as

following:

Also after ascertaining the amount of income tax expense from the income statement of

an entity necessary adjustment for deferred tax assets and deferred tax, liabilities have to be

made to ascertain the amount of income tax liability or assets, as the case may be, to include

show in the Balance sheet of the company (Adeler 2014).

Therefore, it can be said that for the above reasons there is a difference between the

income tax payable and the income tax expenses.

The relationship between the Income tax payment and expense:

The cash flow statement of the company shows that the following amounts have been

paid as income tax in the year 2015 and in the year 2015:

As in the year 2016, the company has incurred financial loss there has been no income

tax expense in the year. It can be seen that there exists a significant difference between the

income tax expenses and the income tax expenses provided in the cash flow statement (Zhang et

al. 2016). The reason for the difference between the two items of financial statements are as

following:

8TAX

There is a difference between the income tax expense and the amount of tax paid:

The income tax expense is the amount of income tax on the taxable profit of an entity

whereas the income tax paid in the cash flow statement shows the amount of cash outflow in

respect of the income tax. The cash out flow for income tax is generally the payment of adjusted

income tax that is due to the government after making all necessary adjustments (Ranchhod and

Finn 2016).

Different periods:

Generally, the payment of income tax in cash flow statement could be for income earned

in earlier periods. Whereas the income tax expenses is calculated on the amount of income

earned by an entity for the current income tax period as per the income statement of an entity.

Thus, there would bound to be a difference between the amount of income tax paid as per the

cash flow statement and the income tax expense as provided in the income statement of an entity

(Le 2017).

Insights learned:

While assessing the income tax expense, deferred tax assets, deferred tax liabilities,

income tax payable or income tax asset and payment of income tax as per the cash flow

statement of Fleetwood Corporation. There have been number of new aspects that have

interested curiosity in us and made us think about the different treatments of tax related

provisions in the financial statements of the company (Morcol et al. 2017). However, at the same

time it is essential for an entity to keep record of each and every single item related to the

financial transactions as the same might influence the final liability of an entity while it come to

the payment of income tax liabilities for the income earned by the company.

There is a difference between the income tax expense and the amount of tax paid:

The income tax expense is the amount of income tax on the taxable profit of an entity

whereas the income tax paid in the cash flow statement shows the amount of cash outflow in

respect of the income tax. The cash out flow for income tax is generally the payment of adjusted

income tax that is due to the government after making all necessary adjustments (Ranchhod and

Finn 2016).

Different periods:

Generally, the payment of income tax in cash flow statement could be for income earned

in earlier periods. Whereas the income tax expenses is calculated on the amount of income

earned by an entity for the current income tax period as per the income statement of an entity.

Thus, there would bound to be a difference between the amount of income tax paid as per the

cash flow statement and the income tax expense as provided in the income statement of an entity

(Le 2017).

Insights learned:

While assessing the income tax expense, deferred tax assets, deferred tax liabilities,

income tax payable or income tax asset and payment of income tax as per the cash flow

statement of Fleetwood Corporation. There have been number of new aspects that have

interested curiosity in us and made us think about the different treatments of tax related

provisions in the financial statements of the company (Morcol et al. 2017). However, at the same

time it is essential for an entity to keep record of each and every single item related to the

financial transactions as the same might influence the final liability of an entity while it come to

the payment of income tax liabilities for the income earned by the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAX

Conclusion:

The most interesting aspect of them all is the number of different items which are related

with the income tax provisions for the income earned by the company. It is not only about

current income tax expense on the amount of taxable profit but the recognition of deferred tax

assets or deferred tax liabilities, providing for income tax liability as income tax payable under

current liabilities and finally the payment of income tax in the cash flow statement of the

company. However, while evaluating the financial statements of the company the number of

items that have to be recorded to keep track of income tax provision of the company is quite

difficult to summarize in a single place.

Conclusion:

The most interesting aspect of them all is the number of different items which are related

with the income tax provisions for the income earned by the company. It is not only about

current income tax expense on the amount of taxable profit but the recognition of deferred tax

assets or deferred tax liabilities, providing for income tax liability as income tax payable under

current liabilities and finally the payment of income tax in the cash flow statement of the

company. However, while evaluating the financial statements of the company the number of

items that have to be recorded to keep track of income tax provision of the company is quite

difficult to summarize in a single place.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAX

Reference

Adeler, M.C., 2014. Enabling policy environments for co-operative development: A comparative

experience. Canadian Public Policy, 40(Supplement 1), pp.S50-S59.

Agrawal, A., Rosell, C. and Simcoe, T.S., 2014. Do tax credits affect R&D expenditures by

small firms? Evidence from Canada (No. w20615). National Bureau of Economic Research.

Alstadsæter, A., Jacob, M., Kopczuk, W. and Telle, K., 2016. Accounting for business income in

measuring top income shares: Integrated accrual approach using individual and firm data from

Norway (No. w22888). National Bureau of Economic Research.

Bratten, B., Gleason, C.A., Larocque, S.A. and Mills, L.F., 2016. Forecasting taxes: New

evidence from analysts. The Accounting Review, 92(3), pp.1-29.

Cai, D., Wang, T. and Ai, C., 2014. Development of low-carbon economy in Heilongjiang

province tax incentive policy analysis. Advanced Materials Research.

Dowling, G.R., 2014. The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), pp.173-184.

Dyreng, S.D. and Markle, K.S., 2016. The effect of financial constraints on income shifting by

US multinationals. The Accounting Review, 91(6), pp.1601-1627.

Le, T.T., 2017. Incentivizing Orphan Product Development: United States Food and Drug

Administration Orphan Incentive Programs. In Rare Diseases Epidemiology: Update and

Overview (pp. 183-196). Springer, Cham.

Reference

Adeler, M.C., 2014. Enabling policy environments for co-operative development: A comparative

experience. Canadian Public Policy, 40(Supplement 1), pp.S50-S59.

Agrawal, A., Rosell, C. and Simcoe, T.S., 2014. Do tax credits affect R&D expenditures by

small firms? Evidence from Canada (No. w20615). National Bureau of Economic Research.

Alstadsæter, A., Jacob, M., Kopczuk, W. and Telle, K., 2016. Accounting for business income in

measuring top income shares: Integrated accrual approach using individual and firm data from

Norway (No. w22888). National Bureau of Economic Research.

Bratten, B., Gleason, C.A., Larocque, S.A. and Mills, L.F., 2016. Forecasting taxes: New

evidence from analysts. The Accounting Review, 92(3), pp.1-29.

Cai, D., Wang, T. and Ai, C., 2014. Development of low-carbon economy in Heilongjiang

province tax incentive policy analysis. Advanced Materials Research.

Dowling, G.R., 2014. The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), pp.173-184.

Dyreng, S.D. and Markle, K.S., 2016. The effect of financial constraints on income shifting by

US multinationals. The Accounting Review, 91(6), pp.1601-1627.

Le, T.T., 2017. Incentivizing Orphan Product Development: United States Food and Drug

Administration Orphan Incentive Programs. In Rare Diseases Epidemiology: Update and

Overview (pp. 183-196). Springer, Cham.

11TAX

Morcol, G., Hoyt, L., Meek, J.W. and Zimmermann, U. eds., 2017. Business improvement

districts: Research, theories, and controversies. Routledge.

Muller, A. and Kolk, A., 2015. Responsible tax as corporate social responsibility: the case of

multinational enterprises and effective tax in India. Business & Society, 54(4), pp.435-463.

Ranchhod, V. and Finn, A., 2016. Estimating the Short Run Effects of South Africa's

Employment Tax Incentive on Youth Employment Probabilities using A Difference‐in‐

Differences Approach. South African Journal of Economics, 84(2), pp.199-216.

Rao, N., 2016. Do tax credits stimulate R&D spending? The effect of the R&D tax credit in its

first decade. Journal of Public Economics, 140, pp.1-12.

Ryan, C., 2016. Are you experimenting with the R&D tax incentive?. Taxation in

Australia, 50(9), p.529.

Shen, L., He, B., Jiao, L., Song, X. and Zhang, X., 2016. Research on the development of main

policy instruments for improving building energy-efficiency. Journal of Cleaner

Production, 112, pp.1789-1803.

Towery, E.M., 2017. Unintended consequences of linking tax return disclosures to financial

reporting for income taxes: Evidence from Schedule UTP. The Accounting Review.

Zhang, K., Wang, Q., Liang, Q.M. and Chen, H., 2016. A bibliometric analysis of research on

carbon tax from 1989 to 2014. Renewable and Sustainable Energy Reviews, 58, pp.297-310.

Morcol, G., Hoyt, L., Meek, J.W. and Zimmermann, U. eds., 2017. Business improvement

districts: Research, theories, and controversies. Routledge.

Muller, A. and Kolk, A., 2015. Responsible tax as corporate social responsibility: the case of

multinational enterprises and effective tax in India. Business & Society, 54(4), pp.435-463.

Ranchhod, V. and Finn, A., 2016. Estimating the Short Run Effects of South Africa's

Employment Tax Incentive on Youth Employment Probabilities using A Difference‐in‐

Differences Approach. South African Journal of Economics, 84(2), pp.199-216.

Rao, N., 2016. Do tax credits stimulate R&D spending? The effect of the R&D tax credit in its

first decade. Journal of Public Economics, 140, pp.1-12.

Ryan, C., 2016. Are you experimenting with the R&D tax incentive?. Taxation in

Australia, 50(9), p.529.

Shen, L., He, B., Jiao, L., Song, X. and Zhang, X., 2016. Research on the development of main

policy instruments for improving building energy-efficiency. Journal of Cleaner

Production, 112, pp.1789-1803.

Towery, E.M., 2017. Unintended consequences of linking tax return disclosures to financial

reporting for income taxes: Evidence from Schedule UTP. The Accounting Review.

Zhang, K., Wang, Q., Liang, Q.M. and Chen, H., 2016. A bibliometric analysis of research on

carbon tax from 1989 to 2014. Renewable and Sustainable Energy Reviews, 58, pp.297-310.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.