Advanced Management Accounting Analysis: Fletcher Building Limited

VerifiedAdded on 2023/06/04

|13

|3073

|305

Report

AI Summary

This report presents an in-depth analysis of advanced management accounting, specifically focusing on its application to Fletcher Building Limited. The report begins by exploring fundamental concepts such as vision, mission, and strategy, providing insights into how Fletcher Building Limited defines its objectives. It then delves into strategic cost management, examining the company's current costing methods and advocating for the adoption of activity-based costing and a just-in-time (JIT) system to enhance cost information reliability and efficiency. The report also evaluates the company's performance measures, assessing their effectiveness and suggesting improvements, particularly in tracking sales growth. Furthermore, the report explores the use of a balanced scorecard to align strategic objectives with performance measures and concludes with a discussion on competitor accounting and analysis, emphasizing the importance of understanding competitors' strengths and weaknesses for strategic decision-making. This comprehensive analysis offers valuable insights into the financial and strategic management practices of Fletcher Building Limited.

Running head: ADVANCED MANAGEMENT ACCOUNTING 1

Advanced Management Accounting

Your Name

Name of Institution

Advanced Management Accounting

Your Name

Name of Institution

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED MANAGEMENT ACCOUNTING 2

Task 1. Concepts of Management Accounting

Vision

A Vision statement should explain where the business targets to be in future and where

the business wants to go in future.

New Vision for Fletcher building Limited

Modelling the future of New Zealand and Australia by discovering and providing

differentiated construction products suitable for every construction in the upcoming diversified

economic structure.

Mission

It is the statement which reflects the reason and purpose for business existence

New Mission for Fletcher Building Limited

To create building solutions by offering differentiated types of construction materials so

as to promote customer satisfaction by giving them best compelling experience in building

products.

Strategy

It explains how the business intends to fulfill its goals, vision and compete its competitors

New Strategy for Fletcher building Limited.

To act effectively and efficiently in managing our business by providing quality building

materials at low prices through focusing on the primary objectives and purpose of the business,

Task 1. Concepts of Management Accounting

Vision

A Vision statement should explain where the business targets to be in future and where

the business wants to go in future.

New Vision for Fletcher building Limited

Modelling the future of New Zealand and Australia by discovering and providing

differentiated construction products suitable for every construction in the upcoming diversified

economic structure.

Mission

It is the statement which reflects the reason and purpose for business existence

New Mission for Fletcher Building Limited

To create building solutions by offering differentiated types of construction materials so

as to promote customer satisfaction by giving them best compelling experience in building

products.

Strategy

It explains how the business intends to fulfill its goals, vision and compete its competitors

New Strategy for Fletcher building Limited.

To act effectively and efficiently in managing our business by providing quality building

materials at low prices through focusing on the primary objectives and purpose of the business,

ADVANCED MANAGEMENT ACCOUNTING 3

strengthening our relationship with customers through brand loyalty and simplifying the business

to both the customers and employees

The Type of Strategy a Company Should Use

A company should use a type of strategy which enables it achieve its set objectives,

perform well financially and be able to compete favorably with its competitors. According to

William (2002), the strategy of a company should majorly arise from its objectives and should

therefore formulate mechanisms which will help the company in achieving those objectives. The

strategy of a company should clearly elaborate the steps that will be used in differentiating

products, achieving goals and how it generates income.

A company should formulate a strategy that clearly reveals its strengths, its material resources,

the market it operates and the available opportunities which a company can venture in while

striving to achieve its objectives. According to Harrison (1999) strategy to be used by a company

should contain the pricing strategy of the company, company’s financial strategy and its

operational strategy. The strategy should also have an action plan. The strategic framework of a

company should have precise goals of different strategies and the relationship between strategies

in a company should be mapped together.

Task 2. Strategic Cost Management

Fletcher building limited uses the conventional costing method. There are nine divisions

in this company which comprise of; building products, distribution, construction, steel, concrete,

Australia, residential development and Formica and roof tile group. In the different division the

manufacturing overhead costs are allocated to goods which are produced in each department.

The indirect costs of different divisions are allocated based on the volume of products

strengthening our relationship with customers through brand loyalty and simplifying the business

to both the customers and employees

The Type of Strategy a Company Should Use

A company should use a type of strategy which enables it achieve its set objectives,

perform well financially and be able to compete favorably with its competitors. According to

William (2002), the strategy of a company should majorly arise from its objectives and should

therefore formulate mechanisms which will help the company in achieving those objectives. The

strategy of a company should clearly elaborate the steps that will be used in differentiating

products, achieving goals and how it generates income.

A company should formulate a strategy that clearly reveals its strengths, its material resources,

the market it operates and the available opportunities which a company can venture in while

striving to achieve its objectives. According to Harrison (1999) strategy to be used by a company

should contain the pricing strategy of the company, company’s financial strategy and its

operational strategy. The strategy should also have an action plan. The strategic framework of a

company should have precise goals of different strategies and the relationship between strategies

in a company should be mapped together.

Task 2. Strategic Cost Management

Fletcher building limited uses the conventional costing method. There are nine divisions

in this company which comprise of; building products, distribution, construction, steel, concrete,

Australia, residential development and Formica and roof tile group. In the different division the

manufacturing overhead costs are allocated to goods which are produced in each department.

The indirect costs of different divisions are allocated based on the volume of products

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED MANAGEMENT ACCOUNTING 4

manufactured and produced in each department. Every division reports its estimated expenses

used in the whole production process without assigning those costs to specific items for example

the building products division reported an expenditure of $ 19 million

(https://fletcherbuilding.com). The divisions also allocate machine hours to the production

overhead products. The company does not report the exact cost used in manufacturing of specific

products as the divisions report all the expenses used in production as cost incurred in

production.

The best costing system to be used by Fletcher building limited is the activity based

costing method. Every division in the company should assign its cost to specific overhead

activities and then be able to assign the resulting costs to specific products (Kaplan & Cooper

1998). This will enable the company to identify the specific costs which are involved in the

production of specific goods. If this company uses the activity based costing it will improve the

cost information reliability and by so doing it will produce exact costs of goods produced and the

divisions will classify the cost of production during the manufacturing process. By using the

activity based costing, Fletcher building limited will be able to analyze their profits, target their

costs in different divisions and service their pricing methods (Jaya, Pathirage& Sutrisna,2010). If

Fletcher traps their manufacturing costs very well, they will be able come up with good strategies

and focus well in their business.

I think it is good for Fletcher building limited to move to JIT system. Since the company

has many divisions it should purchase products that will make it meet the customer needs. The

company can purchase goods frequently as needed and the managers in different divisions

should check the goods that they need in production but are out of stock. This method will also

help the company in managing products that are stored. JIT costing system will help the

manufactured and produced in each department. Every division reports its estimated expenses

used in the whole production process without assigning those costs to specific items for example

the building products division reported an expenditure of $ 19 million

(https://fletcherbuilding.com). The divisions also allocate machine hours to the production

overhead products. The company does not report the exact cost used in manufacturing of specific

products as the divisions report all the expenses used in production as cost incurred in

production.

The best costing system to be used by Fletcher building limited is the activity based

costing method. Every division in the company should assign its cost to specific overhead

activities and then be able to assign the resulting costs to specific products (Kaplan & Cooper

1998). This will enable the company to identify the specific costs which are involved in the

production of specific goods. If this company uses the activity based costing it will improve the

cost information reliability and by so doing it will produce exact costs of goods produced and the

divisions will classify the cost of production during the manufacturing process. By using the

activity based costing, Fletcher building limited will be able to analyze their profits, target their

costs in different divisions and service their pricing methods (Jaya, Pathirage& Sutrisna,2010). If

Fletcher traps their manufacturing costs very well, they will be able come up with good strategies

and focus well in their business.

I think it is good for Fletcher building limited to move to JIT system. Since the company

has many divisions it should purchase products that will make it meet the customer needs. The

company can purchase goods frequently as needed and the managers in different divisions

should check the goods that they need in production but are out of stock. This method will also

help the company in managing products that are stored. JIT costing system will help the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED MANAGEMENT ACCOUNTING 5

company to reduce wastage of goods by avoiding investments in unnecessary resources and also

minimizing the needs of old stock replacements. According to Tanaka, Yoshikawa and Mitchel

(1993) this method will help the company due to its many divisions to achieve its production

target by purchasing products which are necessary. JIT method will also minimize space needed

to store goods because goods will be used as they are purchased.

Task 3. Performance Measures

Fletcher building limited uses the following performance measures. Tracing the

capability of department of accounting in collecting debt and coming up with estimations of

uncollectible debts. Tracing the speed of production by every division in the company. Tracing

funds liquidity which are overseen by the department of finance. Tracking the level of inventory

that is maintained by the company. The inventories are valued on the basis of first in first out

(FIFO) and are recorded using the net realizable value and the lower of cost method. Inventories’

cost of completion is added to inventories in order to determine the amount of inventory used

and remaining. The company also measures the level of revenue earning and growth and in this

case there is a steady growth in revenue earnings and in terms of growth. Lastly the company

also traces its ability to increase sales. The company checks improvements in terms of sales for

example there is an increase in gains of sales in sims metal JV and Dongwah

(https://fletcherbuilding.com).

Evaluation

Performance evaluation gives the company managers ability to assess their workers and

find out their level of contribution to the company (Wruck &Jensen 1994). The performance

evaluation is done in five steps which comprise of; developing an evaluation form, identifying

company to reduce wastage of goods by avoiding investments in unnecessary resources and also

minimizing the needs of old stock replacements. According to Tanaka, Yoshikawa and Mitchel

(1993) this method will help the company due to its many divisions to achieve its production

target by purchasing products which are necessary. JIT method will also minimize space needed

to store goods because goods will be used as they are purchased.

Task 3. Performance Measures

Fletcher building limited uses the following performance measures. Tracing the

capability of department of accounting in collecting debt and coming up with estimations of

uncollectible debts. Tracing the speed of production by every division in the company. Tracing

funds liquidity which are overseen by the department of finance. Tracking the level of inventory

that is maintained by the company. The inventories are valued on the basis of first in first out

(FIFO) and are recorded using the net realizable value and the lower of cost method. Inventories’

cost of completion is added to inventories in order to determine the amount of inventory used

and remaining. The company also measures the level of revenue earning and growth and in this

case there is a steady growth in revenue earnings and in terms of growth. Lastly the company

also traces its ability to increase sales. The company checks improvements in terms of sales for

example there is an increase in gains of sales in sims metal JV and Dongwah

(https://fletcherbuilding.com).

Evaluation

Performance evaluation gives the company managers ability to assess their workers and

find out their level of contribution to the company (Wruck &Jensen 1994). The performance

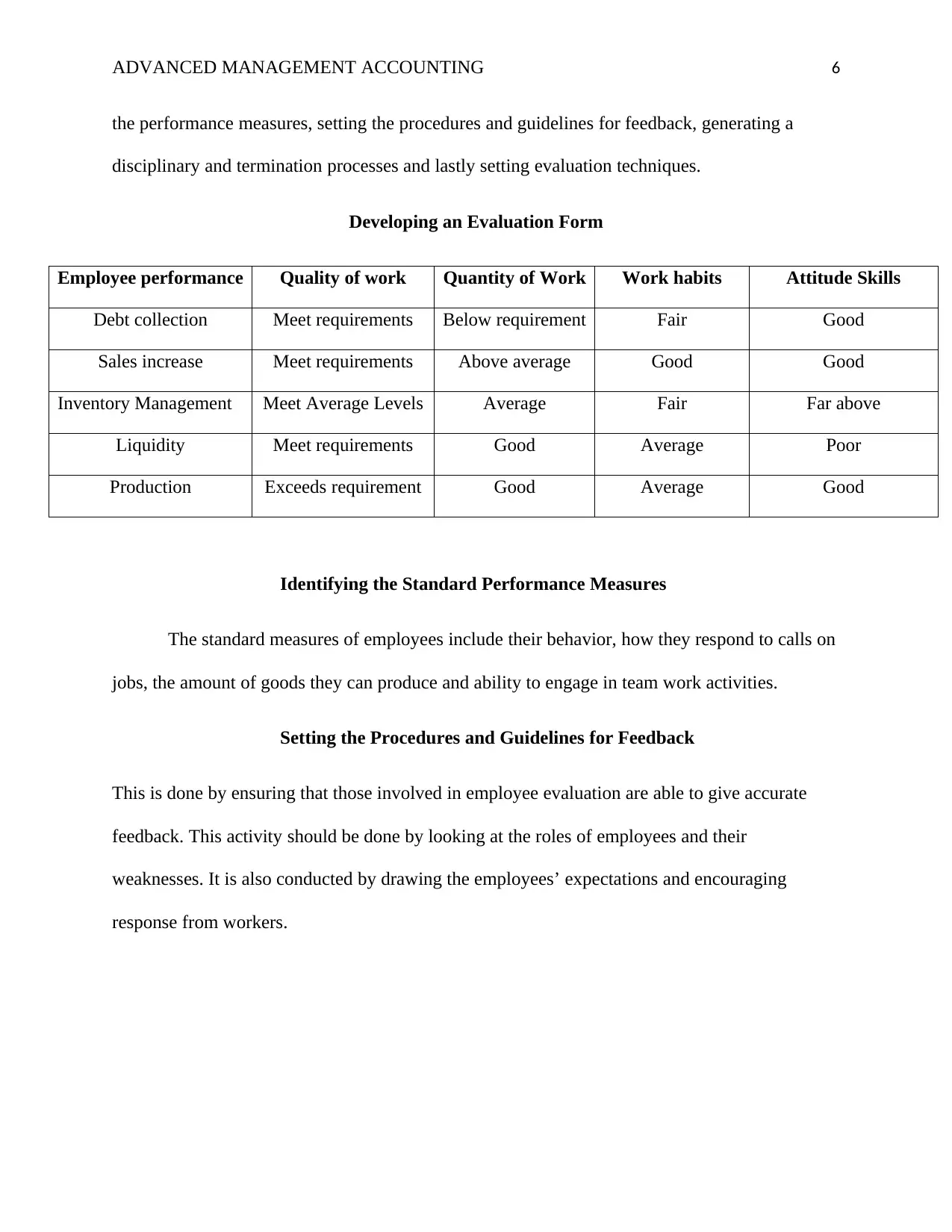

evaluation is done in five steps which comprise of; developing an evaluation form, identifying

ADVANCED MANAGEMENT ACCOUNTING 6

the performance measures, setting the procedures and guidelines for feedback, generating a

disciplinary and termination processes and lastly setting evaluation techniques.

Developing an Evaluation Form

Employee performance Quality of work Quantity of Work Work habits Attitude Skills

Debt collection Meet requirements Below requirement Fair Good

Sales increase Meet requirements Above average Good Good

Inventory Management Meet Average Levels Average Fair Far above

Liquidity Meet requirements Good Average Poor

Production Exceeds requirement Good Average Good

Identifying the Standard Performance Measures

The standard measures of employees include their behavior, how they respond to calls on

jobs, the amount of goods they can produce and ability to engage in team work activities.

Setting the Procedures and Guidelines for Feedback

This is done by ensuring that those involved in employee evaluation are able to give accurate

feedback. This activity should be done by looking at the roles of employees and their

weaknesses. It is also conducted by drawing the employees’ expectations and encouraging

response from workers.

the performance measures, setting the procedures and guidelines for feedback, generating a

disciplinary and termination processes and lastly setting evaluation techniques.

Developing an Evaluation Form

Employee performance Quality of work Quantity of Work Work habits Attitude Skills

Debt collection Meet requirements Below requirement Fair Good

Sales increase Meet requirements Above average Good Good

Inventory Management Meet Average Levels Average Fair Far above

Liquidity Meet requirements Good Average Poor

Production Exceeds requirement Good Average Good

Identifying the Standard Performance Measures

The standard measures of employees include their behavior, how they respond to calls on

jobs, the amount of goods they can produce and ability to engage in team work activities.

Setting the Procedures and Guidelines for Feedback

This is done by ensuring that those involved in employee evaluation are able to give accurate

feedback. This activity should be done by looking at the roles of employees and their

weaknesses. It is also conducted by drawing the employees’ expectations and encouraging

response from workers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED MANAGEMENT ACCOUNTING 7

Generation of Disciplinary and Termination Techniques

In these step it outlines the steps that the management will take if the conditions gets

worse even after conducting the performance appraisal for example if the workers rates of sales

continues to deteriorate, the employees in that department will be terminated. Verbal warning

should also be given to underperforming employees for example those who manage inventory

poorly. Other employees should be given written warnings by describing what they are doing

and what is expected of them.

Setting an Evaluation Schedule

Once the four steps have been followed then the management should set time for

employee appraisal. Once the schedule is set, every person doing appraisal should meet the

stipulated deadlines. Employee performance evaluation can be done at the same time or in

different times depending on the evaluation schedule.

The best performance measurement that suits Fletcher building company is tracking the sales

increase and growth. This will be done by tracking the revenues generated in each division by

looking at their ability to make sales. The company should track its ability to sale its

manufactured products in every division so as to be able to set mechanisms that will help in

revenue generation through sales.

Task four. Balanced Score Card.

Balanced scorecard according to Schneiderman (2006) can be described as a system of

strategic management and planning which enables companies to articulate the achievements they

are trying to meet, the products, projects and services they give more priority, how they measure,

Generation of Disciplinary and Termination Techniques

In these step it outlines the steps that the management will take if the conditions gets

worse even after conducting the performance appraisal for example if the workers rates of sales

continues to deteriorate, the employees in that department will be terminated. Verbal warning

should also be given to underperforming employees for example those who manage inventory

poorly. Other employees should be given written warnings by describing what they are doing

and what is expected of them.

Setting an Evaluation Schedule

Once the four steps have been followed then the management should set time for

employee appraisal. Once the schedule is set, every person doing appraisal should meet the

stipulated deadlines. Employee performance evaluation can be done at the same time or in

different times depending on the evaluation schedule.

The best performance measurement that suits Fletcher building company is tracking the sales

increase and growth. This will be done by tracking the revenues generated in each division by

looking at their ability to make sales. The company should track its ability to sale its

manufactured products in every division so as to be able to set mechanisms that will help in

revenue generation through sales.

Task four. Balanced Score Card.

Balanced scorecard according to Schneiderman (2006) can be described as a system of

strategic management and planning which enables companies to articulate the achievements they

are trying to meet, the products, projects and services they give more priority, how they measure,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED MANAGEMENT ACCOUNTING 8

evaluate and monitor their projects in order to make sure they meet their set objectives and lastly

enable the companies to align their daily activities to be able to meet their strategic objectives.

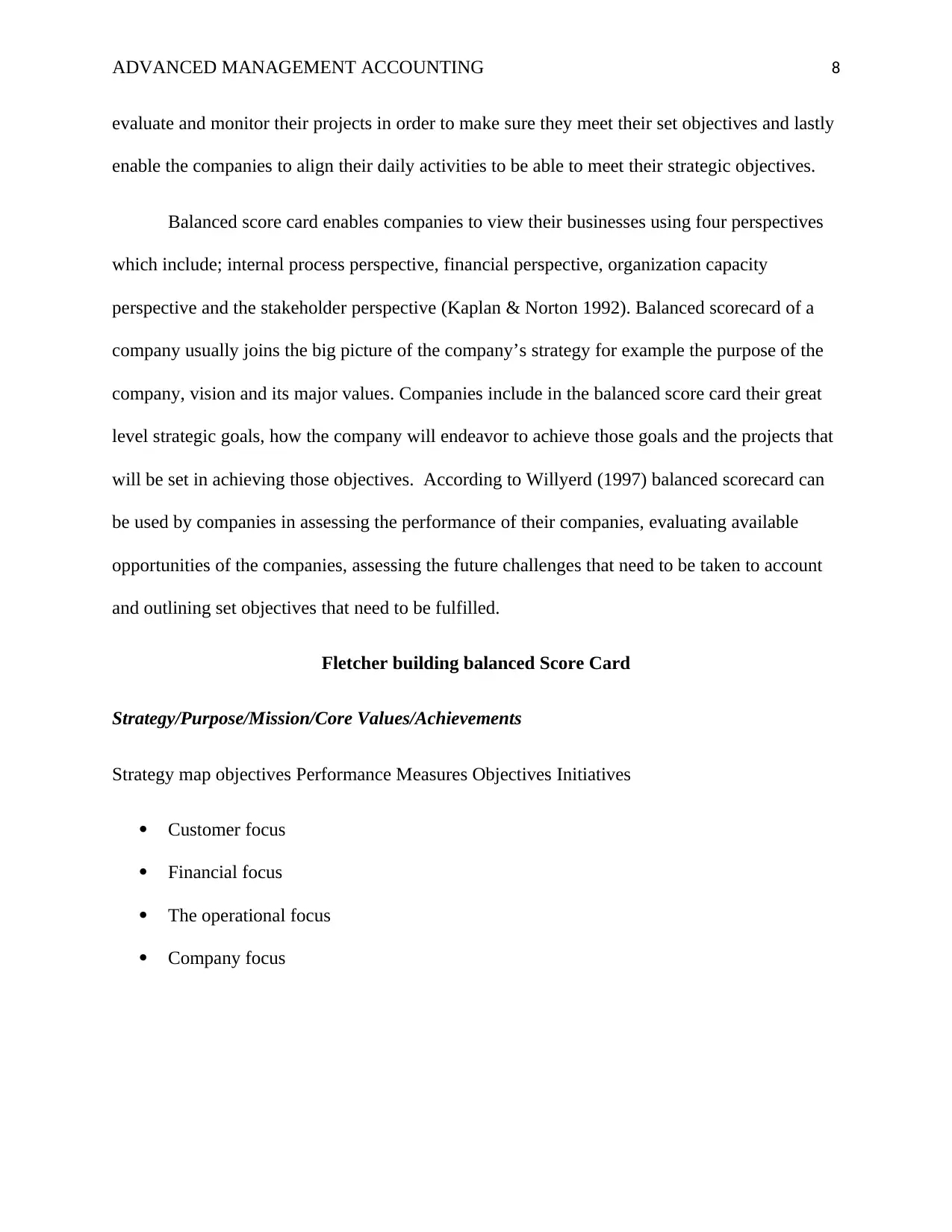

Balanced score card enables companies to view their businesses using four perspectives

which include; internal process perspective, financial perspective, organization capacity

perspective and the stakeholder perspective (Kaplan & Norton 1992). Balanced scorecard of a

company usually joins the big picture of the company’s strategy for example the purpose of the

company, vision and its major values. Companies include in the balanced score card their great

level strategic goals, how the company will endeavor to achieve those goals and the projects that

will be set in achieving those objectives. According to Willyerd (1997) balanced scorecard can

be used by companies in assessing the performance of their companies, evaluating available

opportunities of the companies, assessing the future challenges that need to be taken to account

and outlining set objectives that need to be fulfilled.

Fletcher building balanced Score Card

Strategy/Purpose/Mission/Core Values/Achievements

Strategy map objectives Performance Measures Objectives Initiatives

Customer focus

Financial focus

The operational focus

Company focus

evaluate and monitor their projects in order to make sure they meet their set objectives and lastly

enable the companies to align their daily activities to be able to meet their strategic objectives.

Balanced score card enables companies to view their businesses using four perspectives

which include; internal process perspective, financial perspective, organization capacity

perspective and the stakeholder perspective (Kaplan & Norton 1992). Balanced scorecard of a

company usually joins the big picture of the company’s strategy for example the purpose of the

company, vision and its major values. Companies include in the balanced score card their great

level strategic goals, how the company will endeavor to achieve those goals and the projects that

will be set in achieving those objectives. According to Willyerd (1997) balanced scorecard can

be used by companies in assessing the performance of their companies, evaluating available

opportunities of the companies, assessing the future challenges that need to be taken to account

and outlining set objectives that need to be fulfilled.

Fletcher building balanced Score Card

Strategy/Purpose/Mission/Core Values/Achievements

Strategy map objectives Performance Measures Objectives Initiatives

Customer focus

Financial focus

The operational focus

Company focus

ADVANCED MANAGEMENT ACCOUNTING 9

Linking Performance Measures with the Balanced Scorecard

For every strategic objective identified in the balanced score card, one performance

measure will be identified and traced over a certain period. Linking the balanced score card with

performance measures helps the company to develop towards achieving set objectives. The

performance measures assist in checking and controlling the implementation of the mapped

objectives in the balanced scorecard (Lawrie & Cobbold 2004). Performance measures of

Fletcher building limited will be used in determining if the strategic objectives have been

achieved and if not determine the existing gap between the objectives that have been achieved

and the expected target.

Performance measures are linked to the balance scorecard in order to offer a way of

determining if the company strategic objectives are working and will lead to attaining a desirable

goal. Linking also help in minimizing uncertainty of intangibles. Setting goals and linking with

performance measurements will help the company in making work done. If the objectives of the

company and the performance measurements are linked it will mean that the company has same

motive of fulfilling its objectives. According to Trzcienski and Brooke (1997) Performance

measures will be used to scale the rate at which employees perform as required over time

Task Five. Competitor Accounting

Competitor analysis can be described as the evaluation of the competitors’ strengths and

weaknesses. Competitor analysis offers defensive and offensive prospects and strengths contexts.

Competitor analysis can be termed as the SWOT analysis. This analysis is a vital element in any

business strategy (David, Marian &Joel 2005). The managers are supposed to consistently

receive competitors’ information.

Linking Performance Measures with the Balanced Scorecard

For every strategic objective identified in the balanced score card, one performance

measure will be identified and traced over a certain period. Linking the balanced score card with

performance measures helps the company to develop towards achieving set objectives. The

performance measures assist in checking and controlling the implementation of the mapped

objectives in the balanced scorecard (Lawrie & Cobbold 2004). Performance measures of

Fletcher building limited will be used in determining if the strategic objectives have been

achieved and if not determine the existing gap between the objectives that have been achieved

and the expected target.

Performance measures are linked to the balance scorecard in order to offer a way of

determining if the company strategic objectives are working and will lead to attaining a desirable

goal. Linking also help in minimizing uncertainty of intangibles. Setting goals and linking with

performance measurements will help the company in making work done. If the objectives of the

company and the performance measurements are linked it will mean that the company has same

motive of fulfilling its objectives. According to Trzcienski and Brooke (1997) Performance

measures will be used to scale the rate at which employees perform as required over time

Task Five. Competitor Accounting

Competitor analysis can be described as the evaluation of the competitors’ strengths and

weaknesses. Competitor analysis offers defensive and offensive prospects and strengths contexts.

Competitor analysis can be termed as the SWOT analysis. This analysis is a vital element in any

business strategy (David, Marian &Joel 2005). The managers are supposed to consistently

receive competitors’ information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED MANAGEMENT ACCOUNTING 10

Competitor analysis according to Porter (1985) has two core activities which includes

attaining information concerning the significant competitors and secondly using the obtained

information in forecasting the behavior of competitors. Competitor analysis help the company to

know the type of competitors to compete with, to enable the company to understand the planned

actions of competitors and strategies, to take advantage and influence competitors activities for

the benefit of the company and lastly to understand the influence of competitors on the

company’s activities.

Companies should be able to know the driving motives of their competitors in terms of

objectives and strategies. They should also look at their competitor performance by looking at

their annual reports, look at their websites and press releases (Roderick, Andre & Justine).

Companies should also look at their competitors believes and assumptions by majorly basing on

the industrial trends, rules of the thumb among others. Look at competitors’ resources and

capabilities and this will help in knowing how they may respond to competitive actions and

lastly look at the competitors’ ability to respond profiles.

Competitors of Fletcher building Limited

The main competitors of Fletcher building limited are Hawkins, Fulton Hogan and

Naylor Love. Hawkins has been a fletcher competitor for a long period. Hawkins also

manufactures and process differentiated materials just like Fletcher building limited. Although it

has fewer employees (20307) it managed to raise revenue of $ 700 million which is less than that

of Fletcher.

Competitor analysis according to Porter (1985) has two core activities which includes

attaining information concerning the significant competitors and secondly using the obtained

information in forecasting the behavior of competitors. Competitor analysis help the company to

know the type of competitors to compete with, to enable the company to understand the planned

actions of competitors and strategies, to take advantage and influence competitors activities for

the benefit of the company and lastly to understand the influence of competitors on the

company’s activities.

Companies should be able to know the driving motives of their competitors in terms of

objectives and strategies. They should also look at their competitor performance by looking at

their annual reports, look at their websites and press releases (Roderick, Andre & Justine).

Companies should also look at their competitors believes and assumptions by majorly basing on

the industrial trends, rules of the thumb among others. Look at competitors’ resources and

capabilities and this will help in knowing how they may respond to competitive actions and

lastly look at the competitors’ ability to respond profiles.

Competitors of Fletcher building Limited

The main competitors of Fletcher building limited are Hawkins, Fulton Hogan and

Naylor Love. Hawkins has been a fletcher competitor for a long period. Hawkins also

manufactures and process differentiated materials just like Fletcher building limited. Although it

has fewer employees (20307) it managed to raise revenue of $ 700 million which is less than that

of Fletcher.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED MANAGEMENT ACCOUNTING 11

Fulton Hogan is ranked as one of the biggest competitors to Fletcher building limited. It

is also a private company which produces diversified construction materials. It has fewer

employees and managed to raise revenues of $ 320 million.

Naylor Love is another competitor which threatens Fletcher building limited in the

construction sector. It produces diversified construction materials. This company raised revenue

of $ 600 million

Fletcher Building Limited Competitors

Look at the three companies’ strategies by considering how they hire employees, their

shareholder reports and financial interviews. Look at their goals so as to estimate the actions the

three companies may take towards a competitive activity. Look at how the companies’ leaders

hold their firms in terms of trends. Look at the companies’ strengths and weaknesses, how they

price their commodities (Bruce,clerk & David, 1996). Have knowledge about the three

competitors so as to have a competitive advantage over them. Understand their marketing

techniques and the workforce in order to improve on that and gain competitive advantage. Lastly

look at the materials of construction and the capability as this will give a good indication of

competitors’ ability to react to a competitive move.

Fulton Hogan is ranked as one of the biggest competitors to Fletcher building limited. It

is also a private company which produces diversified construction materials. It has fewer

employees and managed to raise revenues of $ 320 million.

Naylor Love is another competitor which threatens Fletcher building limited in the

construction sector. It produces diversified construction materials. This company raised revenue

of $ 600 million

Fletcher Building Limited Competitors

Look at the three companies’ strategies by considering how they hire employees, their

shareholder reports and financial interviews. Look at their goals so as to estimate the actions the

three companies may take towards a competitive activity. Look at how the companies’ leaders

hold their firms in terms of trends. Look at the companies’ strengths and weaknesses, how they

price their commodities (Bruce,clerk & David, 1996). Have knowledge about the three

competitors so as to have a competitive advantage over them. Understand their marketing

techniques and the workforce in order to improve on that and gain competitive advantage. Lastly

look at the materials of construction and the capability as this will give a good indication of

competitors’ ability to react to a competitive move.

ADVANCED MANAGEMENT ACCOUNTING 12

References

Bruce H. Clerk and David B. Montgomery. (1996). Perceiving competitive reactions. Journal:

marketing letters 7(2) pp,115.

David B, Montgomery, Marian Chapman Moore and Joel, E Urbany (2005). Reasoning about

competitive reactions. Journal marketing science 24(1), pp 138

Fletcher building limited annual report. (2018). (Online) Available at

https://fletcherbuilding.com/investor-centre/reports-and-/2018-annual- report

Harrison, E. Frank (1999). The Managerial Decision-Making Process (5th ed.). Boston:

Houghton Mifflin.

Jaya, N. M., Pathirage, C. P. & Sutrisna, M. 2010. The development of a conceptual framework

on activity-based cost controlling for better management of project overheads during the

construction stage. TIIMI 2010 International Scientific Conference.London, United

Kingdom.

Kaplan, R. and cooper, R. (1998). Cost and Effect: Using Integrated Cost Systems to Drive

Profitability and Performance Boston, Massachusetts, Harvard Business School Press.

Kaplan, Robert S and Norton, D.P. (1992).”The balanced scorecard- measures that drive

performance” Harvard business review pp,71-79

Lawrie, Gavin J G and Cobbold, I (2004). “3rd generation balanced scorecard: Evolution of an

effective strategic control tool”. International journal and productivity performance

References

Bruce H. Clerk and David B. Montgomery. (1996). Perceiving competitive reactions. Journal:

marketing letters 7(2) pp,115.

David B, Montgomery, Marian Chapman Moore and Joel, E Urbany (2005). Reasoning about

competitive reactions. Journal marketing science 24(1), pp 138

Fletcher building limited annual report. (2018). (Online) Available at

https://fletcherbuilding.com/investor-centre/reports-and-/2018-annual- report

Harrison, E. Frank (1999). The Managerial Decision-Making Process (5th ed.). Boston:

Houghton Mifflin.

Jaya, N. M., Pathirage, C. P. & Sutrisna, M. 2010. The development of a conceptual framework

on activity-based cost controlling for better management of project overheads during the

construction stage. TIIMI 2010 International Scientific Conference.London, United

Kingdom.

Kaplan, R. and cooper, R. (1998). Cost and Effect: Using Integrated Cost Systems to Drive

Profitability and Performance Boston, Massachusetts, Harvard Business School Press.

Kaplan, Robert S and Norton, D.P. (1992).”The balanced scorecard- measures that drive

performance” Harvard business review pp,71-79

Lawrie, Gavin J G and Cobbold, I (2004). “3rd generation balanced scorecard: Evolution of an

effective strategic control tool”. International journal and productivity performance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.