Accounting: Flexible Budgeting, Labour Costs, and CVP Analysis

VerifiedAdded on 2020/04/21

|10

|1661

|362

Homework Assignment

AI Summary

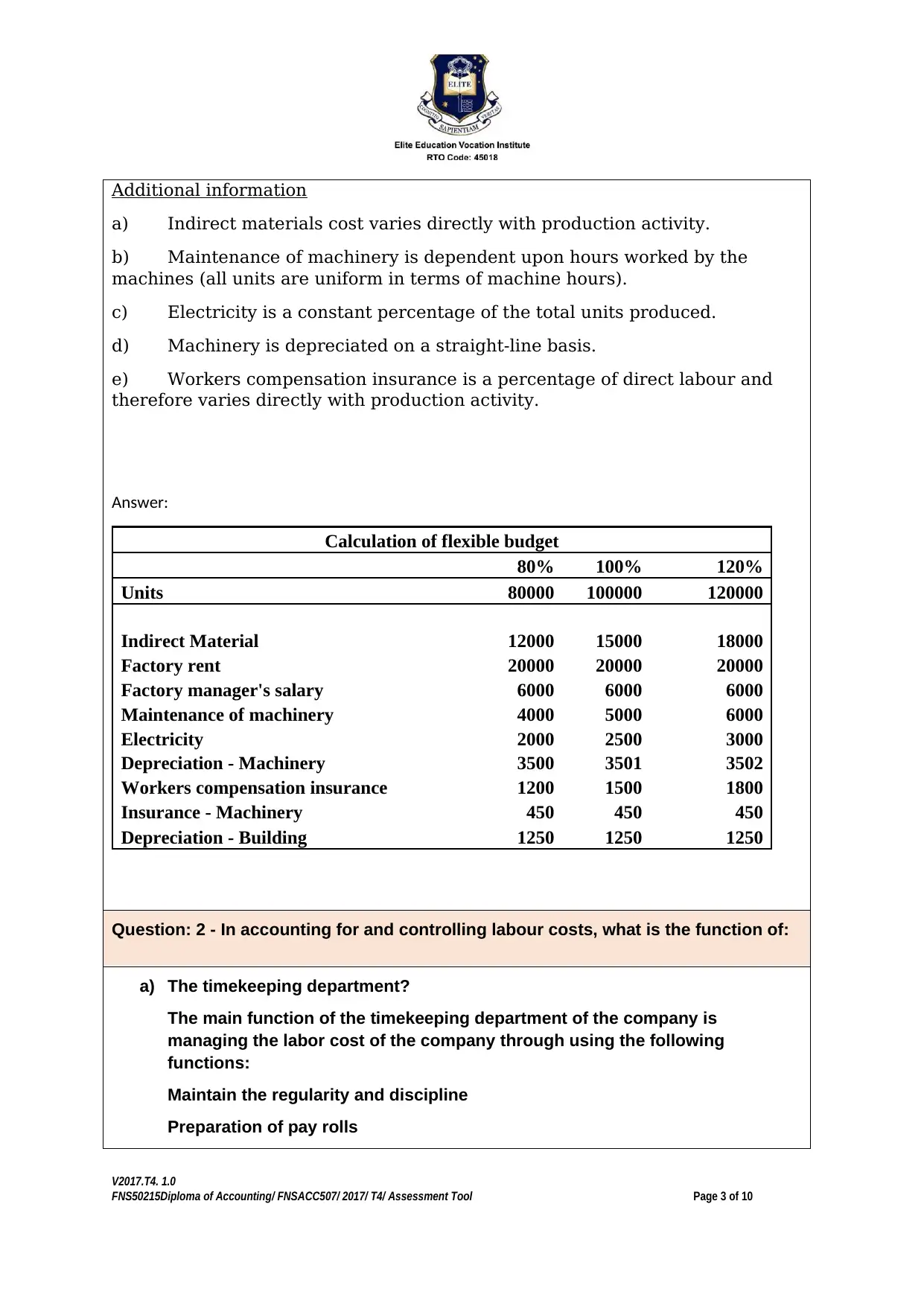

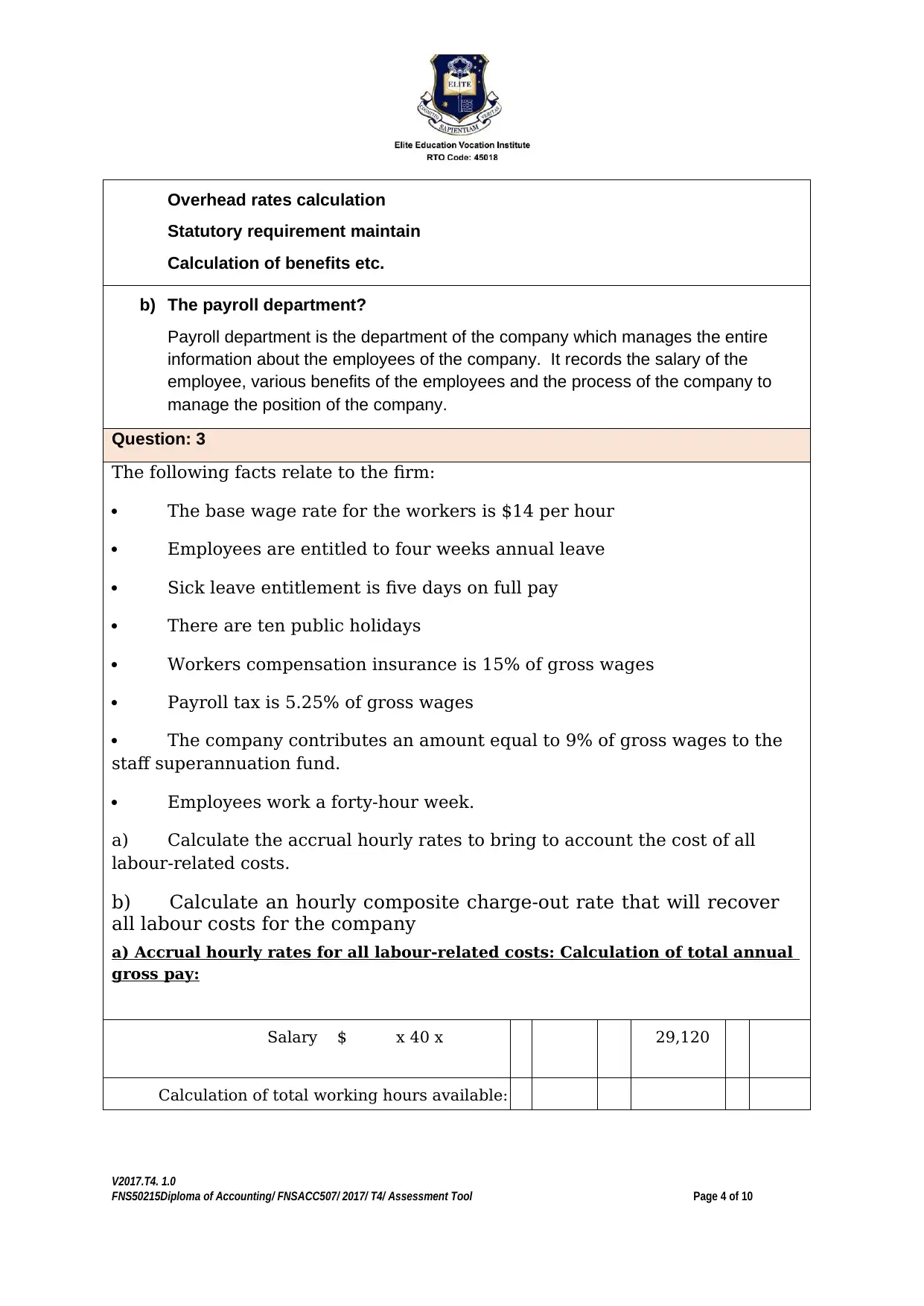

This document presents a comprehensive solution to an accounting assignment, addressing key concepts in financial management. The assignment begins with the preparation of a flexible manufacturing overhead budget, demonstrating the calculation of overhead costs at different production levels (80%, 100%, and 120% of normal activity). It then delves into labor cost accounting, explaining the roles of the timekeeping and payroll departments in controlling and managing labor costs, including the preparation of payroll and calculation of benefits. Furthermore, the assignment includes calculations of accrual hourly rates and composite charge-out rates to account for all labor-related costs. The document also covers cost-volume-profit (CVP) analysis, including the assumptions and limitations of CVP, and the construction of a CVP graph to determine the break-even point, profit potential, and loss potential. Finally, a performance report for sales department operating expenses is prepared and analyzed, comparing budgeted versus actual expenses to assess the company's financial performance. The solution provides detailed calculations and explanations for each question, making it a valuable resource for students studying financial accounting and cost management.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.