Flight Centre Valuation Project: Comprehensive Financial Analysis

VerifiedAdded on 2021/01/01

|19

|4456

|121

Project

AI Summary

This project provides a comprehensive financial analysis and valuation of Flight Centre Travel Group Limited over a five-year period. The analysis includes an overview of financial performance, peer group comparisons, and an examination of current issues and their impact on future earnings. The project utilizes profitability, liquidity, and solvency ratio analyses to assess the company's financial health. A DuPont analysis is employed to estimate the Return on Equity (ROE), and a regression analysis is conducted to estimate and adjust beta for risk assessment. The Capital Asset Pricing Model (CAPM) is used to estimate the cost of equity for stock valuation. Furthermore, the project evaluates the intrinsic value of the company against its current share price using the Dividend Discount Model (DDM) to make informed investment decisions. SWOT and PEST analyses are also used to provide a holistic view of the company's position.

COMPANY VALUATION project

MASTERS

MASTERS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Overview of financial performance of five year....................................................................3

2. Peer group comparison.......................................................................................................6

3. Analysing the present issues with their impact of future earnings.....................................8

4. Estimating ROE of company for past 5 years with DuPont ROE approach....................11

Comparison of financial performance from Dupont approach.............................................12

PART 2..........................................................................................................................................12

2.a.........................................................................................................................................12

2.b.........................................................................................................................................13

3. Evaluation of value or price of organization....................................................................14

3.a Is Intrinsic value is differing from current share price?.................................................14

3.b Presenting that dividend discount model is appropriate or not......................................14

3.c Investment decision on basis of above evaluation of stock price...................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

Overview of financial performance of five year....................................................................3

2. Peer group comparison.......................................................................................................6

3. Analysing the present issues with their impact of future earnings.....................................8

4. Estimating ROE of company for past 5 years with DuPont ROE approach....................11

Comparison of financial performance from Dupont approach.............................................12

PART 2..........................................................................................................................................12

2.a.........................................................................................................................................12

2.b.........................................................................................................................................13

3. Evaluation of value or price of organization....................................................................14

3.a Is Intrinsic value is differing from current share price?.................................................14

3.b Presenting that dividend discount model is appropriate or not......................................14

3.c Investment decision on basis of above evaluation of stock price...................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

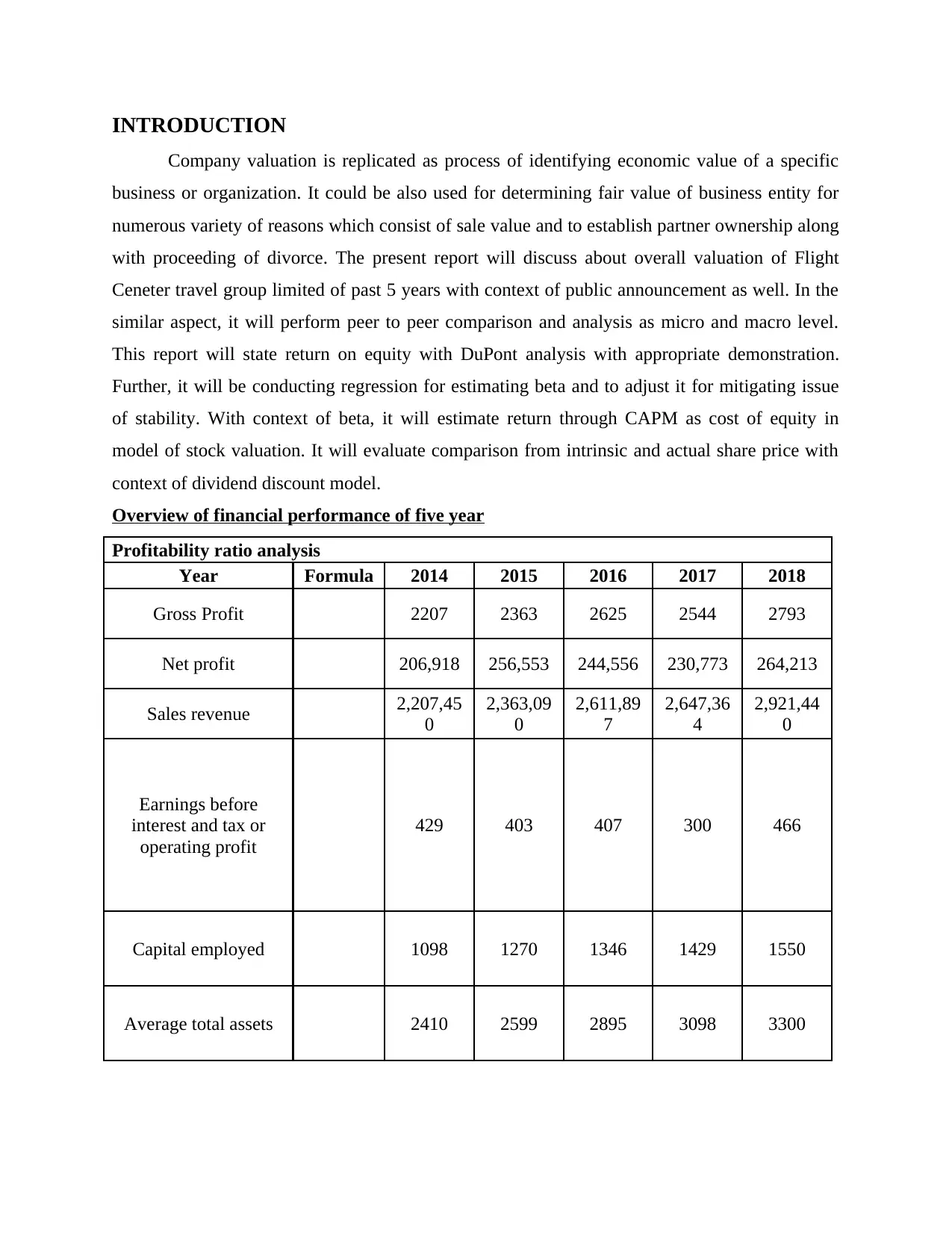

INTRODUCTION

Company valuation is replicated as process of identifying economic value of a specific

business or organization. It could be also used for determining fair value of business entity for

numerous variety of reasons which consist of sale value and to establish partner ownership along

with proceeding of divorce. The present report will discuss about overall valuation of Flight

Ceneter travel group limited of past 5 years with context of public announcement as well. In the

similar aspect, it will perform peer to peer comparison and analysis as micro and macro level.

This report will state return on equity with DuPont analysis with appropriate demonstration.

Further, it will be conducting regression for estimating beta and to adjust it for mitigating issue

of stability. With context of beta, it will estimate return through CAPM as cost of equity in

model of stock valuation. It will evaluate comparison from intrinsic and actual share price with

context of dividend discount model.

Overview of financial performance of five year

Profitability ratio analysis

Year Formula 2014 2015 2016 2017 2018

Gross Profit 2207 2363 2625 2544 2793

Net profit 206,918 256,553 244,556 230,773 264,213

Sales revenue 2,207,45

0

2,363,09

0

2,611,89

7

2,647,36

4

2,921,44

0

Earnings before

interest and tax or

operating profit

429 403 407 300 466

Capital employed 1098 1270 1346 1429 1550

Average total assets 2410 2599 2895 3098 3300

Company valuation is replicated as process of identifying economic value of a specific

business or organization. It could be also used for determining fair value of business entity for

numerous variety of reasons which consist of sale value and to establish partner ownership along

with proceeding of divorce. The present report will discuss about overall valuation of Flight

Ceneter travel group limited of past 5 years with context of public announcement as well. In the

similar aspect, it will perform peer to peer comparison and analysis as micro and macro level.

This report will state return on equity with DuPont analysis with appropriate demonstration.

Further, it will be conducting regression for estimating beta and to adjust it for mitigating issue

of stability. With context of beta, it will estimate return through CAPM as cost of equity in

model of stock valuation. It will evaluate comparison from intrinsic and actual share price with

context of dividend discount model.

Overview of financial performance of five year

Profitability ratio analysis

Year Formula 2014 2015 2016 2017 2018

Gross Profit 2207 2363 2625 2544 2793

Net profit 206,918 256,553 244,556 230,773 264,213

Sales revenue 2,207,45

0

2,363,09

0

2,611,89

7

2,647,36

4

2,921,44

0

Earnings before

interest and tax or

operating profit

429 403 407 300 466

Capital employed 1098 1270 1346 1429 1550

Average total assets 2410 2599 2895 3098 3300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

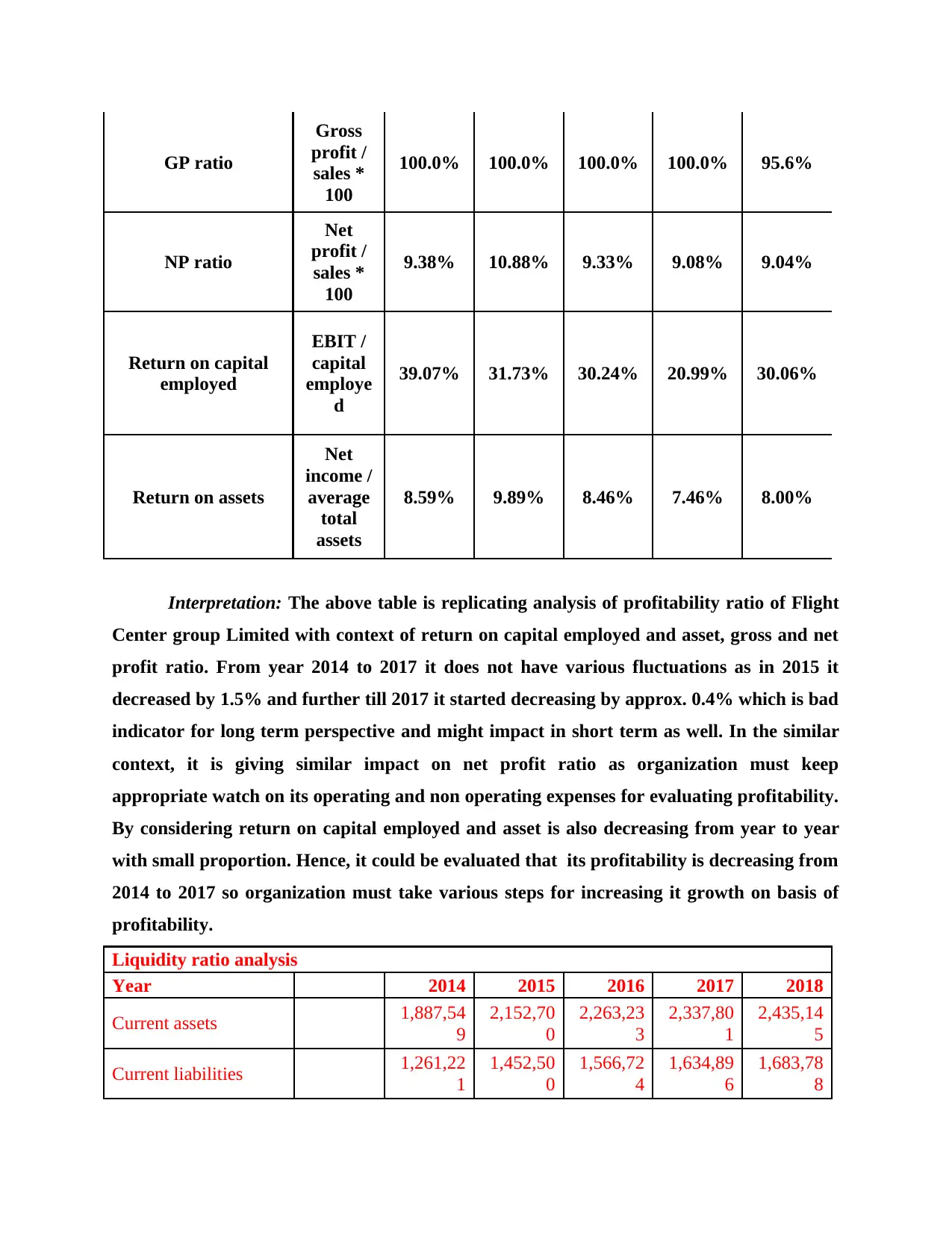

GP ratio

Gross

profit /

sales *

100

100.0% 100.0% 100.0% 100.0% 95.6%

NP ratio

Net

profit /

sales *

100

9.38% 10.88% 9.33% 9.08% 9.04%

Return on capital

employed

EBIT /

capital

employe

d

39.07% 31.73% 30.24% 20.99% 30.06%

Return on assets

Net

income /

average

total

assets

8.59% 9.89% 8.46% 7.46% 8.00%

Interpretation: The above table is replicating analysis of profitability ratio of Flight

Center group Limited with context of return on capital employed and asset, gross and net

profit ratio. From year 2014 to 2017 it does not have various fluctuations as in 2015 it

decreased by 1.5% and further till 2017 it started decreasing by approx. 0.4% which is bad

indicator for long term perspective and might impact in short term as well. In the similar

context, it is giving similar impact on net profit ratio as organization must keep

appropriate watch on its operating and non operating expenses for evaluating profitability.

By considering return on capital employed and asset is also decreasing from year to year

with small proportion. Hence, it could be evaluated that its profitability is decreasing from

2014 to 2017 so organization must take various steps for increasing it growth on basis of

profitability.

Liquidity ratio analysis

Year 2014 2015 2016 2017 2018

Current assets 1,887,54

9

2,152,70

0

2,263,23

3

2,337,80

1

2,435,14

5

Current liabilities 1,261,22

1

1,452,50

0

1,566,72

4

1,634,89

6

1,683,78

8

Gross

profit /

sales *

100

100.0% 100.0% 100.0% 100.0% 95.6%

NP ratio

Net

profit /

sales *

100

9.38% 10.88% 9.33% 9.08% 9.04%

Return on capital

employed

EBIT /

capital

employe

d

39.07% 31.73% 30.24% 20.99% 30.06%

Return on assets

Net

income /

average

total

assets

8.59% 9.89% 8.46% 7.46% 8.00%

Interpretation: The above table is replicating analysis of profitability ratio of Flight

Center group Limited with context of return on capital employed and asset, gross and net

profit ratio. From year 2014 to 2017 it does not have various fluctuations as in 2015 it

decreased by 1.5% and further till 2017 it started decreasing by approx. 0.4% which is bad

indicator for long term perspective and might impact in short term as well. In the similar

context, it is giving similar impact on net profit ratio as organization must keep

appropriate watch on its operating and non operating expenses for evaluating profitability.

By considering return on capital employed and asset is also decreasing from year to year

with small proportion. Hence, it could be evaluated that its profitability is decreasing from

2014 to 2017 so organization must take various steps for increasing it growth on basis of

profitability.

Liquidity ratio analysis

Year 2014 2015 2016 2017 2018

Current assets 1,887,54

9

2,152,70

0

2,263,23

3

2,337,80

1

2,435,14

5

Current liabilities 1,261,22

1

1,452,50

0

1,566,72

4

1,634,89

6

1,683,78

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

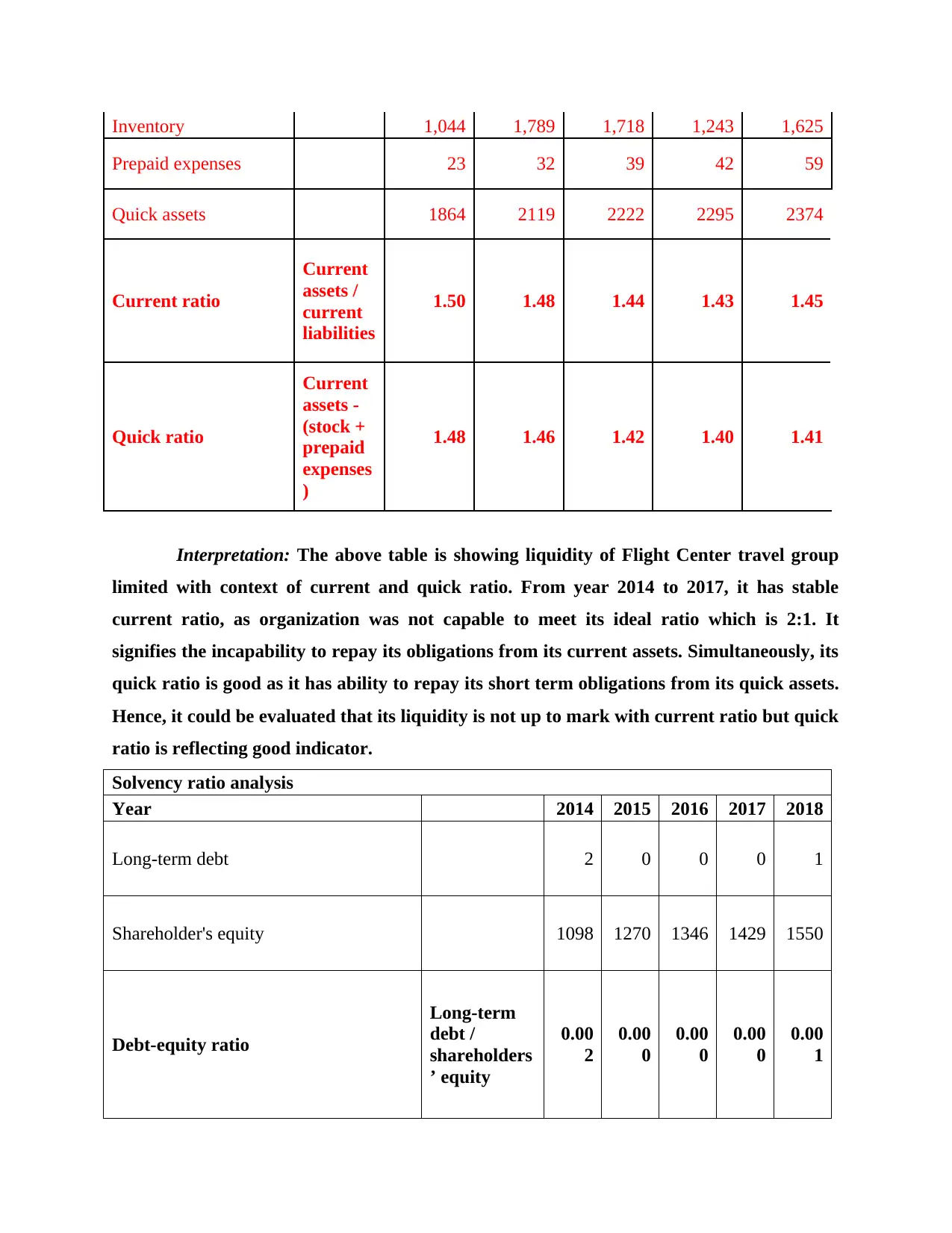

Inventory 1,044 1,789 1,718 1,243 1,625

Prepaid expenses 23 32 39 42 59

Quick assets 1864 2119 2222 2295 2374

Current ratio

Current

assets /

current

liabilities

1.50 1.48 1.44 1.43 1.45

Quick ratio

Current

assets -

(stock +

prepaid

expenses

)

1.48 1.46 1.42 1.40 1.41

Interpretation: The above table is showing liquidity of Flight Center travel group

limited with context of current and quick ratio. From year 2014 to 2017, it has stable

current ratio, as organization was not capable to meet its ideal ratio which is 2:1. It

signifies the incapability to repay its obligations from its current assets. Simultaneously, its

quick ratio is good as it has ability to repay its short term obligations from its quick assets.

Hence, it could be evaluated that its liquidity is not up to mark with current ratio but quick

ratio is reflecting good indicator.

Solvency ratio analysis

Year 2014 2015 2016 2017 2018

Long-term debt 2 0 0 0 1

Shareholder's equity 1098 1270 1346 1429 1550

Debt-equity ratio

Long-term

debt /

shareholders

’ equity

0.00

2

0.00

0

0.00

0

0.00

0

0.00

1

Prepaid expenses 23 32 39 42 59

Quick assets 1864 2119 2222 2295 2374

Current ratio

Current

assets /

current

liabilities

1.50 1.48 1.44 1.43 1.45

Quick ratio

Current

assets -

(stock +

prepaid

expenses

)

1.48 1.46 1.42 1.40 1.41

Interpretation: The above table is showing liquidity of Flight Center travel group

limited with context of current and quick ratio. From year 2014 to 2017, it has stable

current ratio, as organization was not capable to meet its ideal ratio which is 2:1. It

signifies the incapability to repay its obligations from its current assets. Simultaneously, its

quick ratio is good as it has ability to repay its short term obligations from its quick assets.

Hence, it could be evaluated that its liquidity is not up to mark with current ratio but quick

ratio is reflecting good indicator.

Solvency ratio analysis

Year 2014 2015 2016 2017 2018

Long-term debt 2 0 0 0 1

Shareholder's equity 1098 1270 1346 1429 1550

Debt-equity ratio

Long-term

debt /

shareholders

’ equity

0.00

2

0.00

0

0.00

0

0.00

0

0.00

1

Interpretation: The above table is replicating capital structure of Flight Center

travel group Limited. It could be clearly viewed that organization has absence of

borrowing as it is highly financing through equity. In year 2014 and 2018 it has borrowed

but in 2015, 2016 and 2017 there was zero borrowings. Hence, it could be evaluated that the

owner of organization has lost its ownership and power in process of decision making

(Annual report of Flight Center travel Group Limited, 2016).

Efficiency ratio analysis

Year 2014 2015 2016 2017 2018

Turnover or sales revenue 2207 2363 2625 2544 2921

Average total assets 2410 2599 2895 3098 3300

Receivables or debtors 544 449 454 533 594

Total assets turnover ratio

Sales /

average

total

assets

0.92 0.91 0.91 0.82 0.89

Receivables or debtors turnover ratio (in

days)

(Debtor

s *

365) /

Credit

sales

89.9

7

69.3

5

63.1

3

76.4

7

74.2

2

Interpretation: The above table is showing efficiency of organization with context of

total asset turnover ratio and debtors turnover ratio. In year 2014, it was generating 92 cents of

its sales which was decreasing from year as it was 0.89 in 2017. In the similar context, debtors

turnovers was increasing from year to year which could be articulated that its debtors were set

off in 89.97 days in 2014 as it suddenly rose to 69.35 days in 2015 but for recovering its position

it decreased to 63.13 days. As the situation was not in control which is 76.47 in 2016 and 74.22

travel group Limited. It could be clearly viewed that organization has absence of

borrowing as it is highly financing through equity. In year 2014 and 2018 it has borrowed

but in 2015, 2016 and 2017 there was zero borrowings. Hence, it could be evaluated that the

owner of organization has lost its ownership and power in process of decision making

(Annual report of Flight Center travel Group Limited, 2016).

Efficiency ratio analysis

Year 2014 2015 2016 2017 2018

Turnover or sales revenue 2207 2363 2625 2544 2921

Average total assets 2410 2599 2895 3098 3300

Receivables or debtors 544 449 454 533 594

Total assets turnover ratio

Sales /

average

total

assets

0.92 0.91 0.91 0.82 0.89

Receivables or debtors turnover ratio (in

days)

(Debtor

s *

365) /

Credit

sales

89.9

7

69.3

5

63.1

3

76.4

7

74.2

2

Interpretation: The above table is showing efficiency of organization with context of

total asset turnover ratio and debtors turnover ratio. In year 2014, it was generating 92 cents of

its sales which was decreasing from year as it was 0.89 in 2017. In the similar context, debtors

turnovers was increasing from year to year which could be articulated that its debtors were set

off in 89.97 days in 2014 as it suddenly rose to 69.35 days in 2015 but for recovering its position

it decreased to 63.13 days. As the situation was not in control which is 76.47 in 2016 and 74.22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in year 2017. Hence, it could be evaluated that Flight center travel group limited is not efficient

on basis of efficiency ratio.

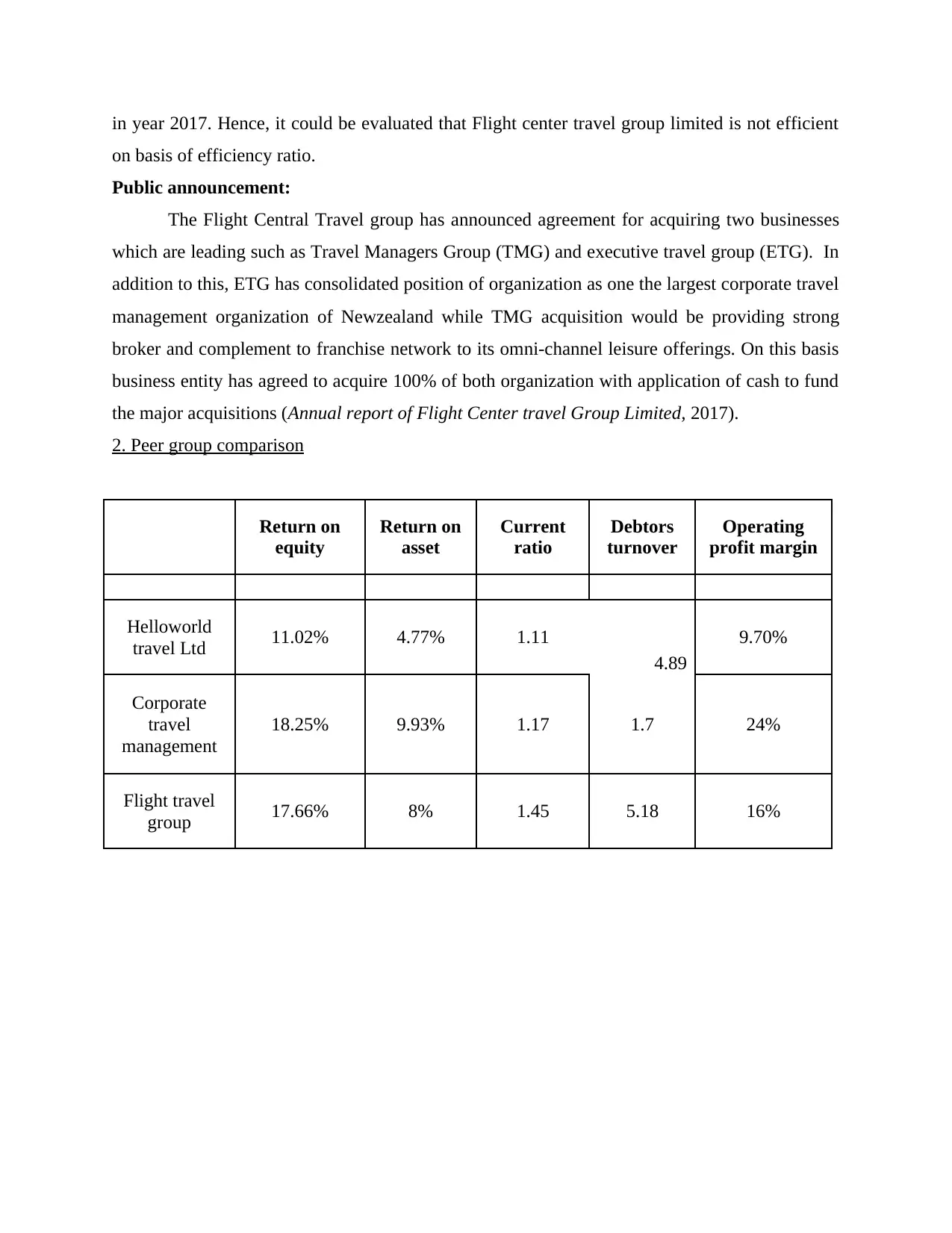

Public announcement:

The Flight Central Travel group has announced agreement for acquiring two businesses

which are leading such as Travel Managers Group (TMG) and executive travel group (ETG). In

addition to this, ETG has consolidated position of organization as one the largest corporate travel

management organization of Newzealand while TMG acquisition would be providing strong

broker and complement to franchise network to its omni-channel leisure offerings. On this basis

business entity has agreed to acquire 100% of both organization with application of cash to fund

the major acquisitions (Annual report of Flight Center travel Group Limited, 2017).

2. Peer group comparison

Return on

equity

Return on

asset

Current

ratio

Debtors

turnover

Operating

profit margin

Helloworld

travel Ltd 11.02% 4.77% 1.11

4.89

9.70%

Corporate

travel

management

18.25% 9.93% 1.17 1.7 24%

Flight travel

group 17.66% 8% 1.45 5.18 16%

on basis of efficiency ratio.

Public announcement:

The Flight Central Travel group has announced agreement for acquiring two businesses

which are leading such as Travel Managers Group (TMG) and executive travel group (ETG). In

addition to this, ETG has consolidated position of organization as one the largest corporate travel

management organization of Newzealand while TMG acquisition would be providing strong

broker and complement to franchise network to its omni-channel leisure offerings. On this basis

business entity has agreed to acquire 100% of both organization with application of cash to fund

the major acquisitions (Annual report of Flight Center travel Group Limited, 2017).

2. Peer group comparison

Return on

equity

Return on

asset

Current

ratio

Debtors

turnover

Operating

profit margin

Helloworld

travel Ltd 11.02% 4.77% 1.11

4.89

9.70%

Corporate

travel

management

18.25% 9.93% 1.17 1.7 24%

Flight travel

group 17.66% 8% 1.45 5.18 16%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

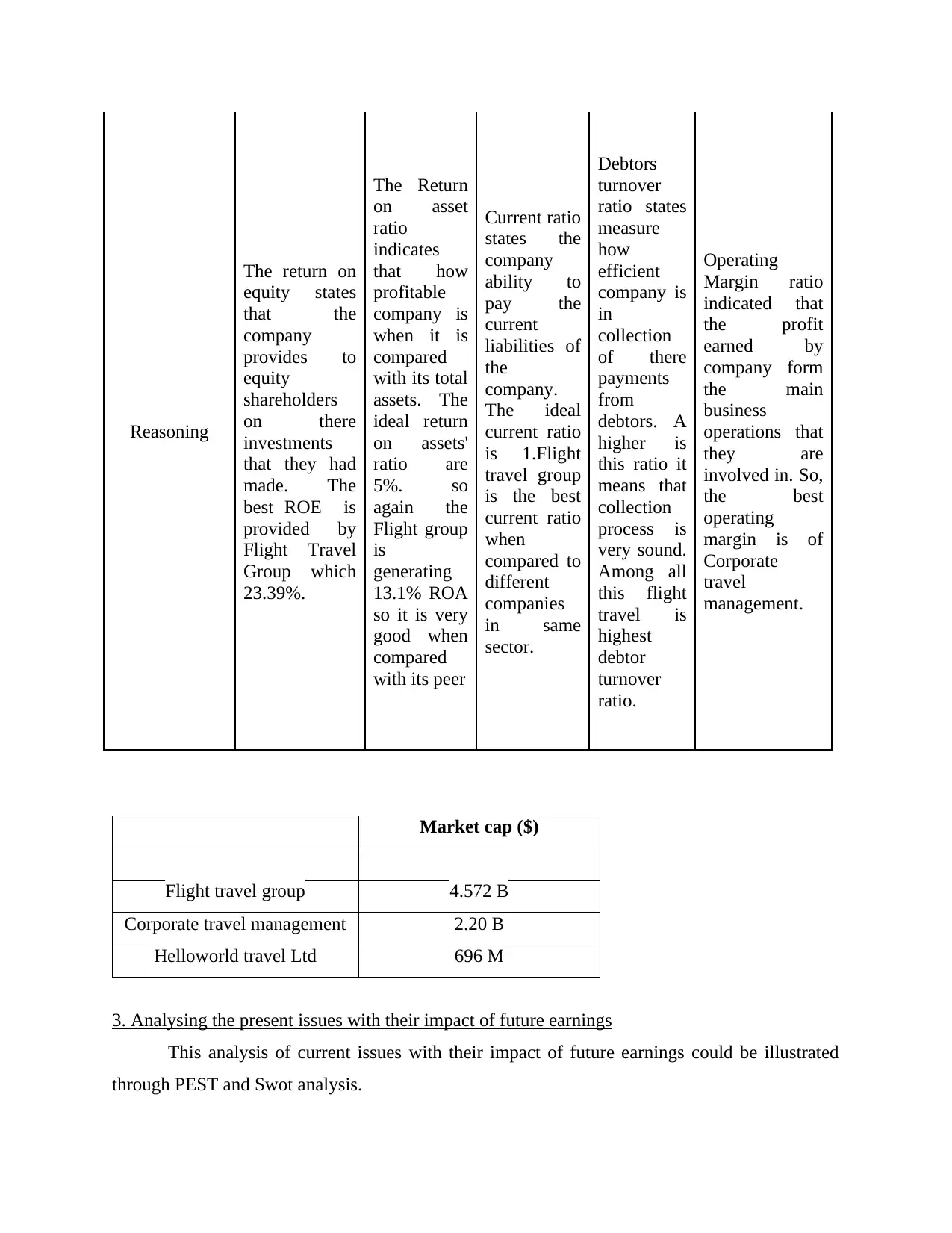

Reasoning

The return on

equity states

that the

company

provides to

equity

shareholders

on there

investments

that they had

made. The

best ROE is

provided by

Flight Travel

Group which

23.39%.

The Return

on asset

ratio

indicates

that how

profitable

company is

when it is

compared

with its total

assets. The

ideal return

on assets'

ratio are

5%. so

again the

Flight group

is

generating

13.1% ROA

so it is very

good when

compared

with its peer

Current ratio

states the

company

ability to

pay the

current

liabilities of

the

company.

The ideal

current ratio

is 1.Flight

travel group

is the best

current ratio

when

compared to

different

companies

in same

sector.

Debtors

turnover

ratio states

measure

how

efficient

company is

in

collection

of there

payments

from

debtors. A

higher is

this ratio it

means that

collection

process is

very sound.

Among all

this flight

travel is

highest

debtor

turnover

ratio.

Operating

Margin ratio

indicated that

the profit

earned by

company form

the main

business

operations that

they are

involved in. So,

the best

operating

margin is of

Corporate

travel

management.

Market cap ($)

Flight travel group 4.572 B

Corporate travel management 2.20 B

Helloworld travel Ltd 696 M

3. Analysing the present issues with their impact of future earnings

This analysis of current issues with their impact of future earnings could be illustrated

through PEST and Swot analysis.

The return on

equity states

that the

company

provides to

equity

shareholders

on there

investments

that they had

made. The

best ROE is

provided by

Flight Travel

Group which

23.39%.

The Return

on asset

ratio

indicates

that how

profitable

company is

when it is

compared

with its total

assets. The

ideal return

on assets'

ratio are

5%. so

again the

Flight group

is

generating

13.1% ROA

so it is very

good when

compared

with its peer

Current ratio

states the

company

ability to

pay the

current

liabilities of

the

company.

The ideal

current ratio

is 1.Flight

travel group

is the best

current ratio

when

compared to

different

companies

in same

sector.

Debtors

turnover

ratio states

measure

how

efficient

company is

in

collection

of there

payments

from

debtors. A

higher is

this ratio it

means that

collection

process is

very sound.

Among all

this flight

travel is

highest

debtor

turnover

ratio.

Operating

Margin ratio

indicated that

the profit

earned by

company form

the main

business

operations that

they are

involved in. So,

the best

operating

margin is of

Corporate

travel

management.

Market cap ($)

Flight travel group 4.572 B

Corporate travel management 2.20 B

Helloworld travel Ltd 696 M

3. Analysing the present issues with their impact of future earnings

This analysis of current issues with their impact of future earnings could be illustrated

through PEST and Swot analysis.

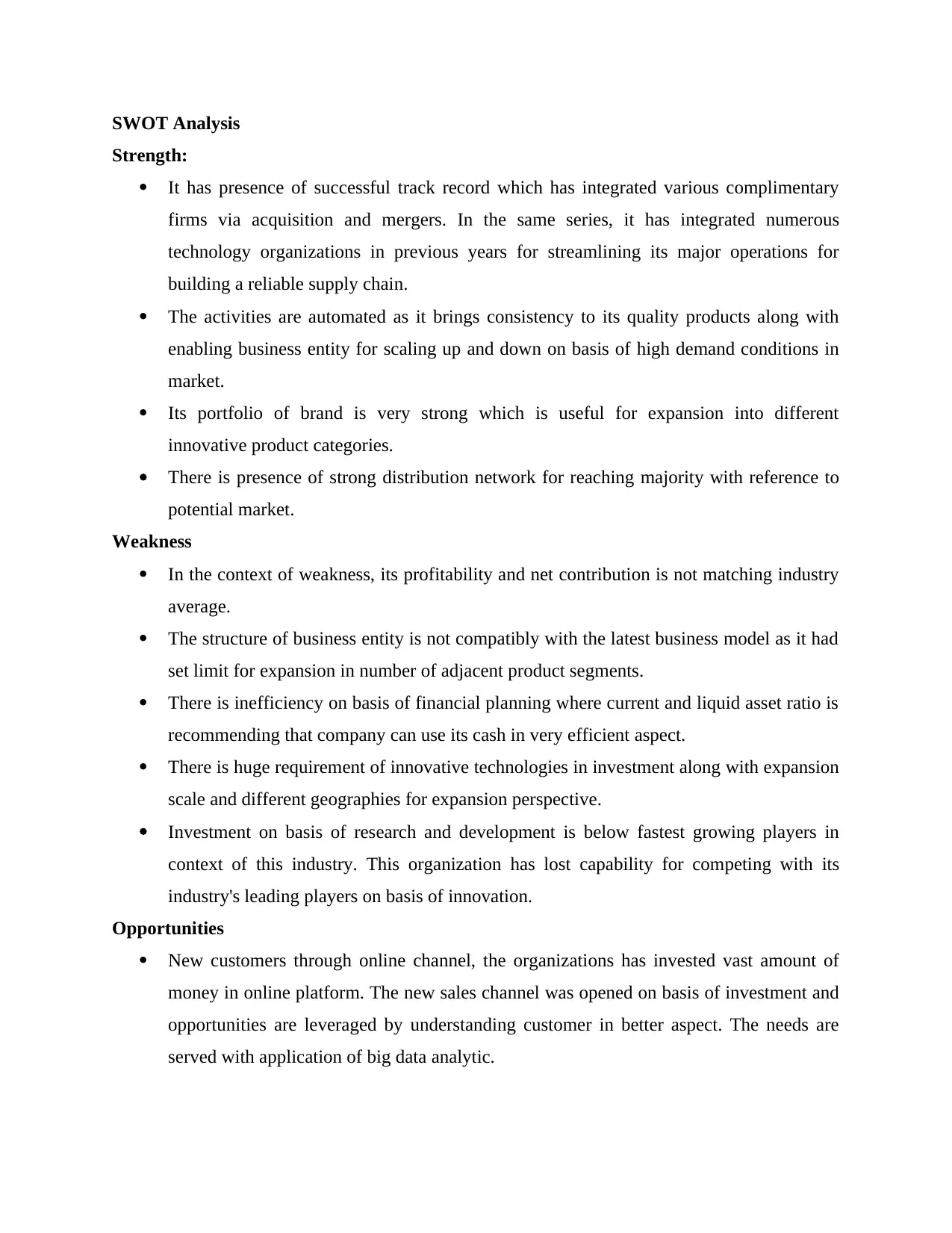

SWOT Analysis

Strength:

It has presence of successful track record which has integrated various complimentary

firms via acquisition and mergers. In the same series, it has integrated numerous

technology organizations in previous years for streamlining its major operations for

building a reliable supply chain.

The activities are automated as it brings consistency to its quality products along with

enabling business entity for scaling up and down on basis of high demand conditions in

market.

Its portfolio of brand is very strong which is useful for expansion into different

innovative product categories.

There is presence of strong distribution network for reaching majority with reference to

potential market.

Weakness

In the context of weakness, its profitability and net contribution is not matching industry

average.

The structure of business entity is not compatibly with the latest business model as it had

set limit for expansion in number of adjacent product segments.

There is inefficiency on basis of financial planning where current and liquid asset ratio is

recommending that company can use its cash in very efficient aspect.

There is huge requirement of innovative technologies in investment along with expansion

scale and different geographies for expansion perspective.

Investment on basis of research and development is below fastest growing players in

context of this industry. This organization has lost capability for competing with its

industry's leading players on basis of innovation.

Opportunities

New customers through online channel, the organizations has invested vast amount of

money in online platform. The new sales channel was opened on basis of investment and

opportunities are leveraged by understanding customer in better aspect. The needs are

served with application of big data analytic.

Strength:

It has presence of successful track record which has integrated various complimentary

firms via acquisition and mergers. In the same series, it has integrated numerous

technology organizations in previous years for streamlining its major operations for

building a reliable supply chain.

The activities are automated as it brings consistency to its quality products along with

enabling business entity for scaling up and down on basis of high demand conditions in

market.

Its portfolio of brand is very strong which is useful for expansion into different

innovative product categories.

There is presence of strong distribution network for reaching majority with reference to

potential market.

Weakness

In the context of weakness, its profitability and net contribution is not matching industry

average.

The structure of business entity is not compatibly with the latest business model as it had

set limit for expansion in number of adjacent product segments.

There is inefficiency on basis of financial planning where current and liquid asset ratio is

recommending that company can use its cash in very efficient aspect.

There is huge requirement of innovative technologies in investment along with expansion

scale and different geographies for expansion perspective.

Investment on basis of research and development is below fastest growing players in

context of this industry. This organization has lost capability for competing with its

industry's leading players on basis of innovation.

Opportunities

New customers through online channel, the organizations has invested vast amount of

money in online platform. The new sales channel was opened on basis of investment and

opportunities are leveraged by understanding customer in better aspect. The needs are

served with application of big data analytic.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

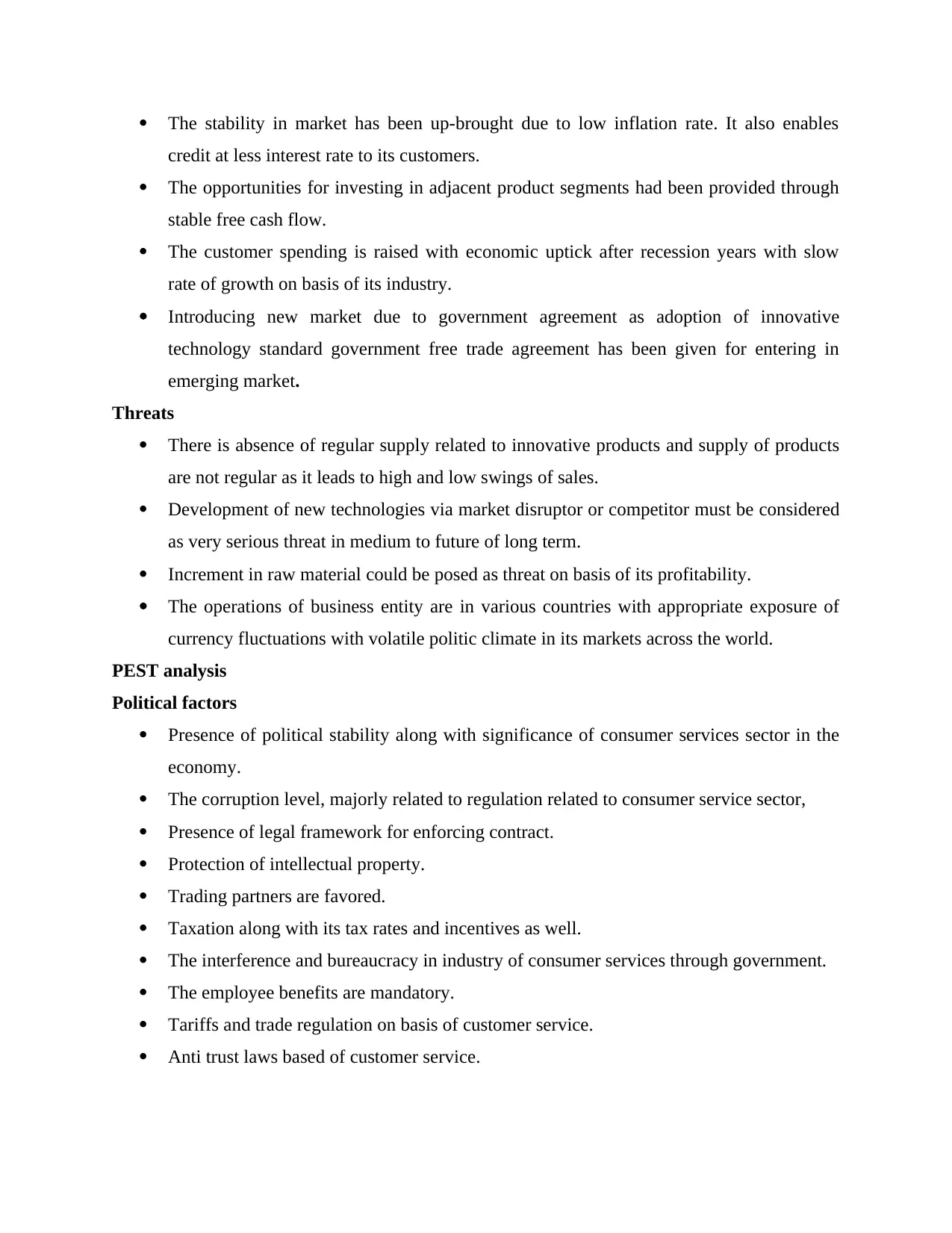

The stability in market has been up-brought due to low inflation rate. It also enables

credit at less interest rate to its customers.

The opportunities for investing in adjacent product segments had been provided through

stable free cash flow.

The customer spending is raised with economic uptick after recession years with slow

rate of growth on basis of its industry.

Introducing new market due to government agreement as adoption of innovative

technology standard government free trade agreement has been given for entering in

emerging market.

Threats

There is absence of regular supply related to innovative products and supply of products

are not regular as it leads to high and low swings of sales.

Development of new technologies via market disruptor or competitor must be considered

as very serious threat in medium to future of long term.

Increment in raw material could be posed as threat on basis of its profitability.

The operations of business entity are in various countries with appropriate exposure of

currency fluctuations with volatile politic climate in its markets across the world.

PEST analysis

Political factors

Presence of political stability along with significance of consumer services sector in the

economy.

The corruption level, majorly related to regulation related to consumer service sector,

Presence of legal framework for enforcing contract.

Protection of intellectual property.

Trading partners are favored.

Taxation along with its tax rates and incentives as well.

The interference and bureaucracy in industry of consumer services through government.

The employee benefits are mandatory.

Tariffs and trade regulation on basis of customer service.

Anti trust laws based of customer service.

credit at less interest rate to its customers.

The opportunities for investing in adjacent product segments had been provided through

stable free cash flow.

The customer spending is raised with economic uptick after recession years with slow

rate of growth on basis of its industry.

Introducing new market due to government agreement as adoption of innovative

technology standard government free trade agreement has been given for entering in

emerging market.

Threats

There is absence of regular supply related to innovative products and supply of products

are not regular as it leads to high and low swings of sales.

Development of new technologies via market disruptor or competitor must be considered

as very serious threat in medium to future of long term.

Increment in raw material could be posed as threat on basis of its profitability.

The operations of business entity are in various countries with appropriate exposure of

currency fluctuations with volatile politic climate in its markets across the world.

PEST analysis

Political factors

Presence of political stability along with significance of consumer services sector in the

economy.

The corruption level, majorly related to regulation related to consumer service sector,

Presence of legal framework for enforcing contract.

Protection of intellectual property.

Trading partners are favored.

Taxation along with its tax rates and incentives as well.

The interference and bureaucracy in industry of consumer services through government.

The employee benefits are mandatory.

Tariffs and trade regulation on basis of customer service.

Anti trust laws based of customer service.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

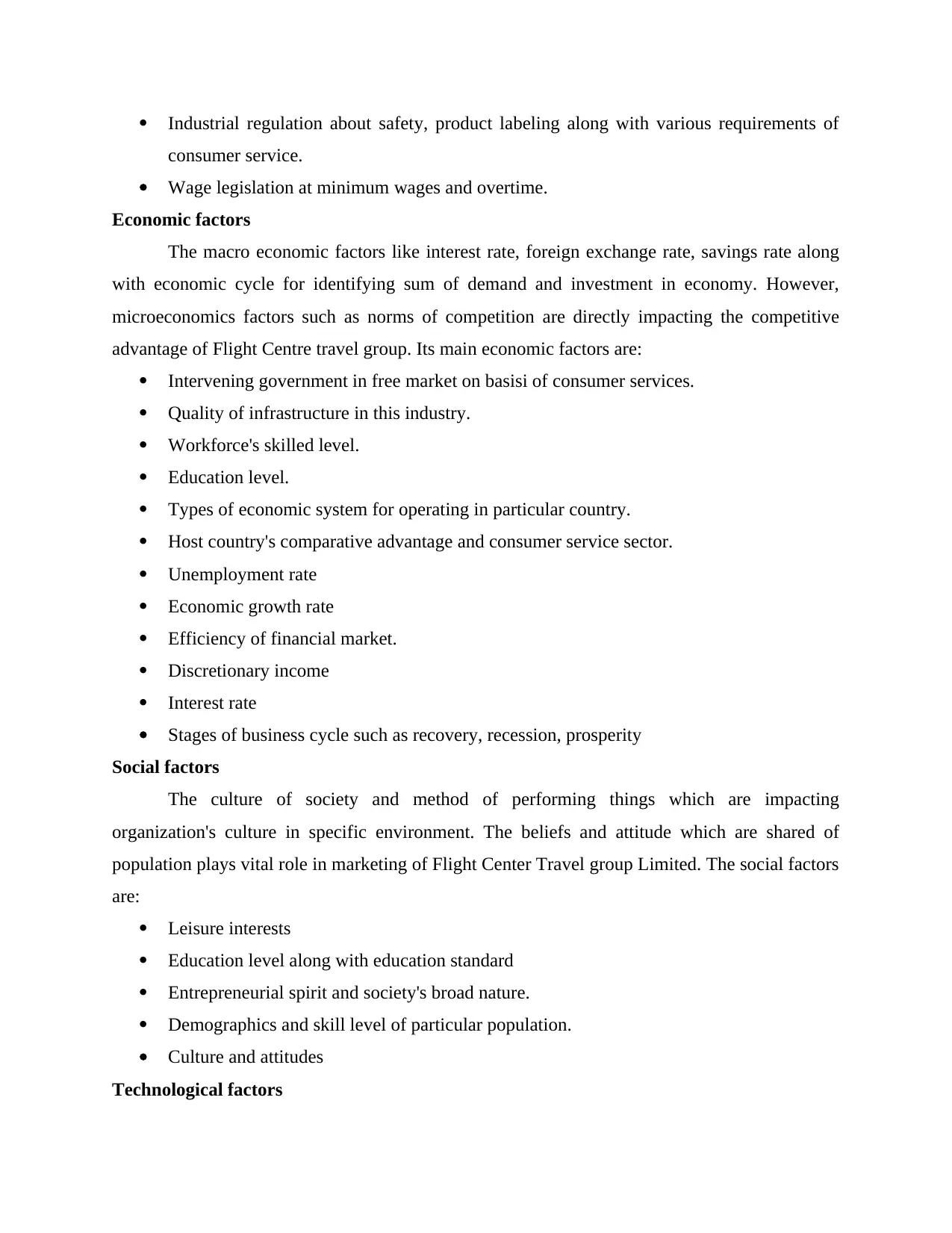

Industrial regulation about safety, product labeling along with various requirements of

consumer service.

Wage legislation at minimum wages and overtime.

Economic factors

The macro economic factors like interest rate, foreign exchange rate, savings rate along

with economic cycle for identifying sum of demand and investment in economy. However,

microeconomics factors such as norms of competition are directly impacting the competitive

advantage of Flight Centre travel group. Its main economic factors are:

Intervening government in free market on basisi of consumer services.

Quality of infrastructure in this industry.

Workforce's skilled level.

Education level.

Types of economic system for operating in particular country.

Host country's comparative advantage and consumer service sector.

Unemployment rate

Economic growth rate

Efficiency of financial market.

Discretionary income

Interest rate

Stages of business cycle such as recovery, recession, prosperity

Social factors

The culture of society and method of performing things which are impacting

organization's culture in specific environment. The beliefs and attitude which are shared of

population plays vital role in marketing of Flight Center Travel group Limited. The social factors

are:

Leisure interests

Education level along with education standard

Entrepreneurial spirit and society's broad nature.

Demographics and skill level of particular population.

Culture and attitudes

Technological factors

consumer service.

Wage legislation at minimum wages and overtime.

Economic factors

The macro economic factors like interest rate, foreign exchange rate, savings rate along

with economic cycle for identifying sum of demand and investment in economy. However,

microeconomics factors such as norms of competition are directly impacting the competitive

advantage of Flight Centre travel group. Its main economic factors are:

Intervening government in free market on basisi of consumer services.

Quality of infrastructure in this industry.

Workforce's skilled level.

Education level.

Types of economic system for operating in particular country.

Host country's comparative advantage and consumer service sector.

Unemployment rate

Economic growth rate

Efficiency of financial market.

Discretionary income

Interest rate

Stages of business cycle such as recovery, recession, prosperity

Social factors

The culture of society and method of performing things which are impacting

organization's culture in specific environment. The beliefs and attitude which are shared of

population plays vital role in marketing of Flight Center Travel group Limited. The social factors

are:

Leisure interests

Education level along with education standard

Entrepreneurial spirit and society's broad nature.

Demographics and skill level of particular population.

Culture and attitudes

Technological factors

In the present scenario, technology is disrupting different industries as transportation is

replicated as best example. Generally. Business must not analyze technology of industry along

with speed through which industry is disrupted. Technological factors impacts the things are

stated below:

Cost structure on consumer service industry impacted through technology.

value chain structure is impacted

technological developments

Technological diffusion's rate

Cost structure is impacted in basis of its cost.

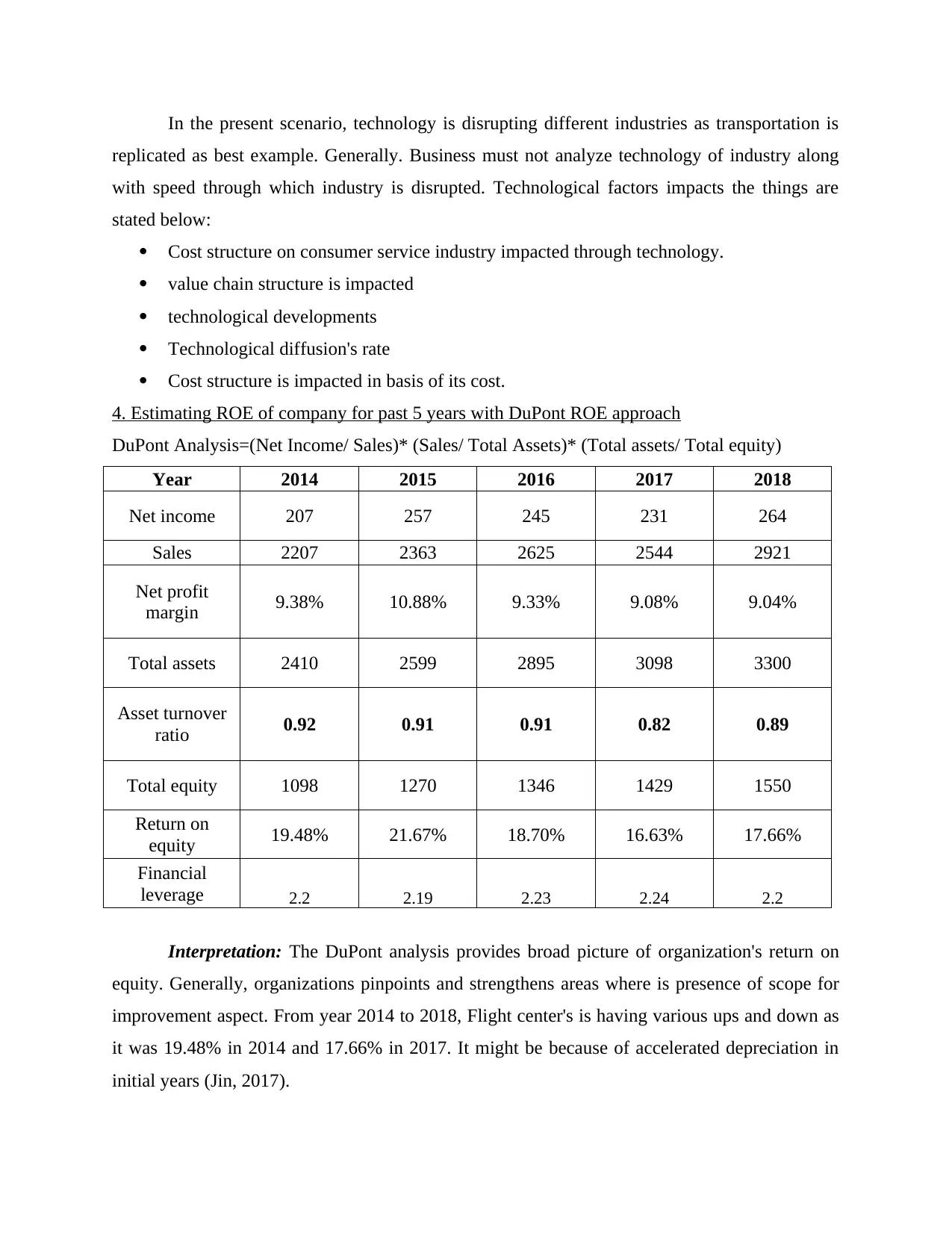

4. Estimating ROE of company for past 5 years with DuPont ROE approach

DuPont Analysis=(Net Income/ Sales)* (Sales/ Total Assets)* (Total assets/ Total equity)

Year 2014 2015 2016 2017 2018

Net income 207 257 245 231 264

Sales 2207 2363 2625 2544 2921

Net profit

margin 9.38% 10.88% 9.33% 9.08% 9.04%

Total assets 2410 2599 2895 3098 3300

Asset turnover

ratio 0.92 0.91 0.91 0.82 0.89

Total equity 1098 1270 1346 1429 1550

Return on

equity 19.48% 21.67% 18.70% 16.63% 17.66%

Financial

leverage 2.2 2.19 2.23 2.24 2.2

Interpretation: The DuPont analysis provides broad picture of organization's return on

equity. Generally, organizations pinpoints and strengthens areas where is presence of scope for

improvement aspect. From year 2014 to 2018, Flight center's is having various ups and down as

it was 19.48% in 2014 and 17.66% in 2017. It might be because of accelerated depreciation in

initial years (Jin, 2017).

replicated as best example. Generally. Business must not analyze technology of industry along

with speed through which industry is disrupted. Technological factors impacts the things are

stated below:

Cost structure on consumer service industry impacted through technology.

value chain structure is impacted

technological developments

Technological diffusion's rate

Cost structure is impacted in basis of its cost.

4. Estimating ROE of company for past 5 years with DuPont ROE approach

DuPont Analysis=(Net Income/ Sales)* (Sales/ Total Assets)* (Total assets/ Total equity)

Year 2014 2015 2016 2017 2018

Net income 207 257 245 231 264

Sales 2207 2363 2625 2544 2921

Net profit

margin 9.38% 10.88% 9.33% 9.08% 9.04%

Total assets 2410 2599 2895 3098 3300

Asset turnover

ratio 0.92 0.91 0.91 0.82 0.89

Total equity 1098 1270 1346 1429 1550

Return on

equity 19.48% 21.67% 18.70% 16.63% 17.66%

Financial

leverage 2.2 2.19 2.23 2.24 2.2

Interpretation: The DuPont analysis provides broad picture of organization's return on

equity. Generally, organizations pinpoints and strengthens areas where is presence of scope for

improvement aspect. From year 2014 to 2018, Flight center's is having various ups and down as

it was 19.48% in 2014 and 17.66% in 2017. It might be because of accelerated depreciation in

initial years (Jin, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.