Performance Analysis of Flight Centre Travel (FLT) - HI5002 Finance

VerifiedAdded on 2023/03/17

|16

|5047

|92

Report

AI Summary

This report presents a financial performance analysis of Flight Centre Travel Group Limited (FLT), an ASX-listed company in the travel industry. The analysis, conducted for an international investor, examines FLT's financial health using its 2016, 2017, and 2018 financial statements. The report focuses on profitability, efficiency, working capital, and financial structure through the calculation and interpretation of various financial ratios, including gross margin, return on assets, and accounts receivable turnover. The study is divided into two main parts, namely the financial analysis of the Flight Centre Travel Group Limited and a recommendation letter based on findings of the performance analysis. The report concludes with recommendations for investment, suggesting that FLT could be part of a diversified investment portfolio, while also highlighting the need for further investigation into its valuation and management.

Performance Analysis 1

Flight Centre Travel (ASX: FLT) Performance Analysis

by Student Name

Class & Course

Professor

University

The City & State

Date

Flight Centre Travel (ASX: FLT) Performance Analysis

by Student Name

Class & Course

Professor

University

The City & State

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance Analysis 2

Abstract

The report analyses the Flight Centre Travel Company as a potential investment

opportunity for an international company. The analysis focuses more on FLT’s working

capital, financial structure, activity, and profitability. The study is divided into two main

parts, namely the financial analysis of the Flight Centre Travel Group Limited and a

recommendation letter based on findings of the performance analysis. The financial

report is further divided into several sections. Based on the comparative financial

performance analysis, FLT has an unfavourable but a promising future. The company is

not worth investing in as a single investment option. However, the company has a

positive performance outlook, which is encouraging to investors. FLT will be in a position

to sustain its cash requirements in the future. FLT pays 40-60% dividends from its net

income annually after taking future cash and investment requirements into

consideration. The company has paid out a dividend in the past three consecutive years.

The risk associated with the company can be managed by adding it in the diversified

investment portfolio. In conclusion, BACA consultancy recommends that FLT should be

part of the diversified investment portfolio. Further investigation should be conducted on

the company’s valuation and its management team.

Abstract

The report analyses the Flight Centre Travel Company as a potential investment

opportunity for an international company. The analysis focuses more on FLT’s working

capital, financial structure, activity, and profitability. The study is divided into two main

parts, namely the financial analysis of the Flight Centre Travel Group Limited and a

recommendation letter based on findings of the performance analysis. The financial

report is further divided into several sections. Based on the comparative financial

performance analysis, FLT has an unfavourable but a promising future. The company is

not worth investing in as a single investment option. However, the company has a

positive performance outlook, which is encouraging to investors. FLT will be in a position

to sustain its cash requirements in the future. FLT pays 40-60% dividends from its net

income annually after taking future cash and investment requirements into

consideration. The company has paid out a dividend in the past three consecutive years.

The risk associated with the company can be managed by adding it in the diversified

investment portfolio. In conclusion, BACA consultancy recommends that FLT should be

part of the diversified investment portfolio. Further investigation should be conducted on

the company’s valuation and its management team.

Performance Analysis 3

I. Introduction

Financial performance analysis report represents a summarised version of a company’s

annual reports. Performance reports help investors to understand the financial health of

a company before making investment decisions. In this scenario, an international

investor is interested in investing in the Australian market. The investor is particularly

interested in an ASX listed company. BACA Consultancy has been contracted to choose

a potential investment company for the investor. The consultancy has settled for the

Flight Centre Travel (ASX: FLT). However, the BACA has to conduct a financial

performance analysis on the company to evaluate whether or not it is a viable

investment option. The performance analysis relies on the three latest financial

statements of the company-income statements, cash flow statements, and balance

sheets to make an informed opinion about investing in the company as well as

projecting the future performance. The analysis focuses more on FLT’s working capital,

financial structure, activity, and profitability.

The paper is divided into two main parts, namely the financial analysis of the Flight

Centre Travel Group Limited and a recommendation letter based on findings of the

performance analysis. The financial analysis is further divided into several sections. The

sections are;

a) Description of FLT,

b) Performance ratios calculation and analysis,

c) Cash management analysis,

d) Perform a sensitivity analysis,

e) Systemic risks and un-systemic risks,

f) And, dividend payout ratio and dividend policy.

The Consultancy firm believes that the investor will benefit from the report by making the

right investment decision based on the informed opinion presented in this report.

1.0. Financial Analysis of FLT Company

Financial analysis refers to the process of analysing suitability and performance of

businesses. The process applies several analysis techniques such as ratio, risk, cash

management, and sensitivity to evaluate whether or not a business is liquid, stable,

profitable, or solvent enough to invest in (English, 2011, p. 67). This section relies on

2016, 2017, and 2018 financial statements of FLT to conduct a financial analysis.

1.1. Description of FLT Company

Flight Centre Travel Group Ltd (FLT) is an ASX listed company which operates in the

traveling industry. FLT was established in 1982 and had its headquarters in South

Brisbane. The company offers services such as corporate travel management, retail,

and wholesale travelling. FLT offers thirty brands in four business segments, which are

Retail, Wholesale, Corporate, and Leisure across over 50 countries (Flight Centre Travel

Group Limited, 2019, p. 14). The key global destinations for the company are Australia,

Europe, the United States, Africa, the United Kingdom, Asia, and New Zealand. FLT has

over 20,200 employees you have been employed on a full-time basis. Moreover, the

company engages indirectly in the employment of over one million people. The company

I. Introduction

Financial performance analysis report represents a summarised version of a company’s

annual reports. Performance reports help investors to understand the financial health of

a company before making investment decisions. In this scenario, an international

investor is interested in investing in the Australian market. The investor is particularly

interested in an ASX listed company. BACA Consultancy has been contracted to choose

a potential investment company for the investor. The consultancy has settled for the

Flight Centre Travel (ASX: FLT). However, the BACA has to conduct a financial

performance analysis on the company to evaluate whether or not it is a viable

investment option. The performance analysis relies on the three latest financial

statements of the company-income statements, cash flow statements, and balance

sheets to make an informed opinion about investing in the company as well as

projecting the future performance. The analysis focuses more on FLT’s working capital,

financial structure, activity, and profitability.

The paper is divided into two main parts, namely the financial analysis of the Flight

Centre Travel Group Limited and a recommendation letter based on findings of the

performance analysis. The financial analysis is further divided into several sections. The

sections are;

a) Description of FLT,

b) Performance ratios calculation and analysis,

c) Cash management analysis,

d) Perform a sensitivity analysis,

e) Systemic risks and un-systemic risks,

f) And, dividend payout ratio and dividend policy.

The Consultancy firm believes that the investor will benefit from the report by making the

right investment decision based on the informed opinion presented in this report.

1.0. Financial Analysis of FLT Company

Financial analysis refers to the process of analysing suitability and performance of

businesses. The process applies several analysis techniques such as ratio, risk, cash

management, and sensitivity to evaluate whether or not a business is liquid, stable,

profitable, or solvent enough to invest in (English, 2011, p. 67). This section relies on

2016, 2017, and 2018 financial statements of FLT to conduct a financial analysis.

1.1. Description of FLT Company

Flight Centre Travel Group Ltd (FLT) is an ASX listed company which operates in the

traveling industry. FLT was established in 1982 and had its headquarters in South

Brisbane. The company offers services such as corporate travel management, retail,

and wholesale travelling. FLT offers thirty brands in four business segments, which are

Retail, Wholesale, Corporate, and Leisure across over 50 countries (Flight Centre Travel

Group Limited, 2019, p. 14). The key global destinations for the company are Australia,

Europe, the United States, Africa, the United Kingdom, Asia, and New Zealand. FLT has

over 20,200 employees you have been employed on a full-time basis. Moreover, the

company engages indirectly in the employment of over one million people. The company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Performance Analysis 4

posted a 2.9billion during the 2018 financial year which a 10.35% compared to the

revenue realised in 2017.

Several investment decisions contributed to the company's group in recent years. First,

the introduction of low-cost new systems that improved productivity. Second, the

introduction of unique brands and products to the customers. Third, the introduction of

flexible working programs for employees to enhance their performance. Fourth, high

presence on the online and digital market which enhanced the company’s capability to

deliver. And fifth, expanding the organic growth strategy by acquiring in the Mexico,

Netherland, and Malaysia markets (Flight Centre Travel Group Limited, 2018).

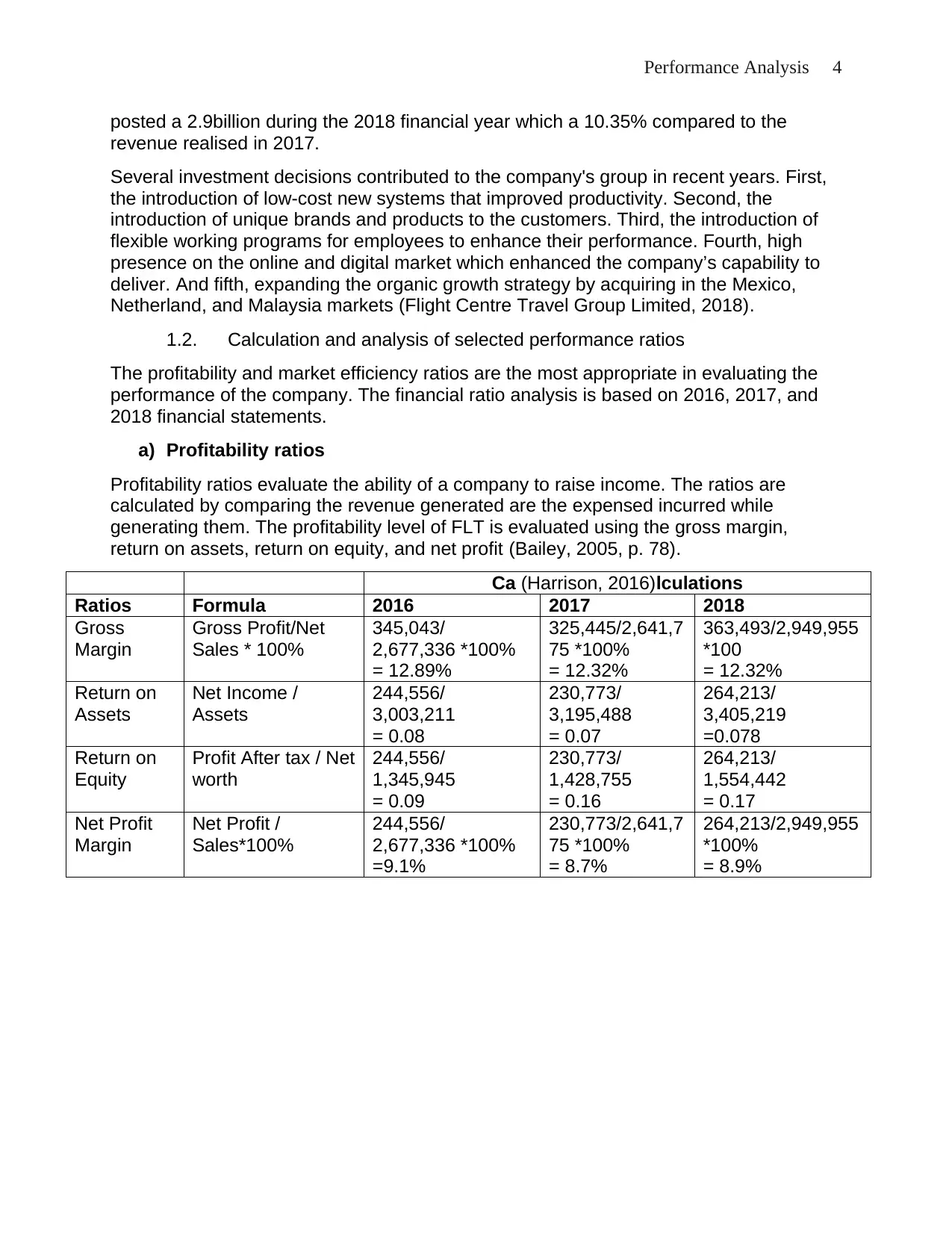

1.2. Calculation and analysis of selected performance ratios

The profitability and market efficiency ratios are the most appropriate in evaluating the

performance of the company. The financial ratio analysis is based on 2016, 2017, and

2018 financial statements.

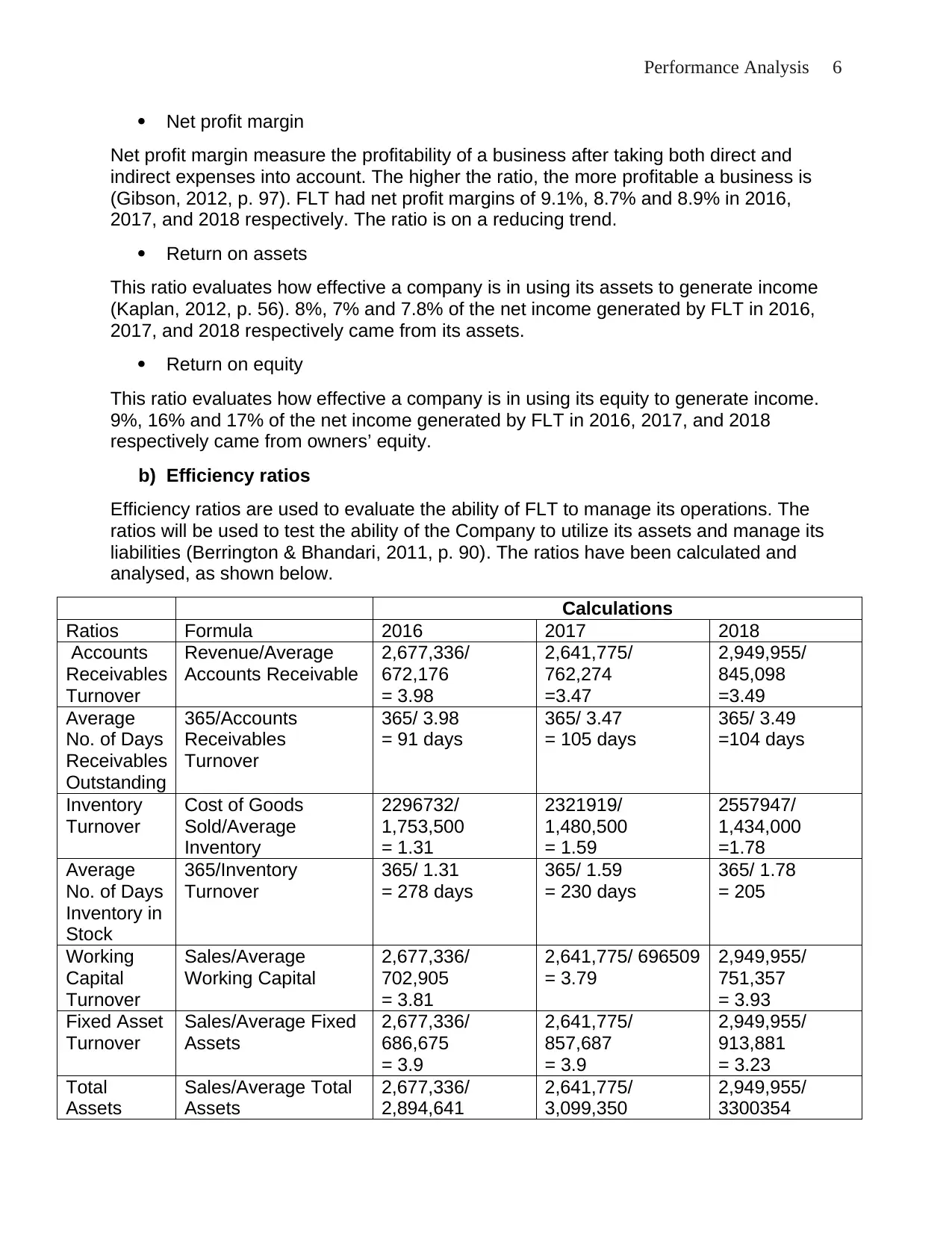

a) Profitability ratios

Profitability ratios evaluate the ability of a company to raise income. The ratios are

calculated by comparing the revenue generated are the expensed incurred while

generating them. The profitability level of FLT is evaluated using the gross margin,

return on assets, return on equity, and net profit (Bailey, 2005, p. 78).

Ca (Harrison, 2016)lculations

Ratios Formula 2016 2017 2018

Gross

Margin

Gross Profit/Net

Sales * 100%

345,043/

2,677,336 *100%

= 12.89%

325,445/2,641,7

75 *100%

= 12.32%

363,493/2,949,955

*100

= 12.32%

Return on

Assets

Net Income /

Assets

244,556/

3,003,211

= 0.08

230,773/

3,195,488

= 0.07

264,213/

3,405,219

=0.078

Return on

Equity

Profit After tax / Net

worth

244,556/

1,345,945

= 0.09

230,773/

1,428,755

= 0.16

264,213/

1,554,442

= 0.17

Net Profit

Margin

Net Profit /

Sales*100%

244,556/

2,677,336 *100%

=9.1%

230,773/2,641,7

75 *100%

= 8.7%

264,213/2,949,955

*100%

= 8.9%

posted a 2.9billion during the 2018 financial year which a 10.35% compared to the

revenue realised in 2017.

Several investment decisions contributed to the company's group in recent years. First,

the introduction of low-cost new systems that improved productivity. Second, the

introduction of unique brands and products to the customers. Third, the introduction of

flexible working programs for employees to enhance their performance. Fourth, high

presence on the online and digital market which enhanced the company’s capability to

deliver. And fifth, expanding the organic growth strategy by acquiring in the Mexico,

Netherland, and Malaysia markets (Flight Centre Travel Group Limited, 2018).

1.2. Calculation and analysis of selected performance ratios

The profitability and market efficiency ratios are the most appropriate in evaluating the

performance of the company. The financial ratio analysis is based on 2016, 2017, and

2018 financial statements.

a) Profitability ratios

Profitability ratios evaluate the ability of a company to raise income. The ratios are

calculated by comparing the revenue generated are the expensed incurred while

generating them. The profitability level of FLT is evaluated using the gross margin,

return on assets, return on equity, and net profit (Bailey, 2005, p. 78).

Ca (Harrison, 2016)lculations

Ratios Formula 2016 2017 2018

Gross

Margin

Gross Profit/Net

Sales * 100%

345,043/

2,677,336 *100%

= 12.89%

325,445/2,641,7

75 *100%

= 12.32%

363,493/2,949,955

*100

= 12.32%

Return on

Assets

Net Income /

Assets

244,556/

3,003,211

= 0.08

230,773/

3,195,488

= 0.07

264,213/

3,405,219

=0.078

Return on

Equity

Profit After tax / Net

worth

244,556/

1,345,945

= 0.09

230,773/

1,428,755

= 0.16

264,213/

1,554,442

= 0.17

Net Profit

Margin

Net Profit /

Sales*100%

244,556/

2,677,336 *100%

=9.1%

230,773/2,641,7

75 *100%

= 8.7%

264,213/2,949,955

*100%

= 8.9%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance Analysis 5

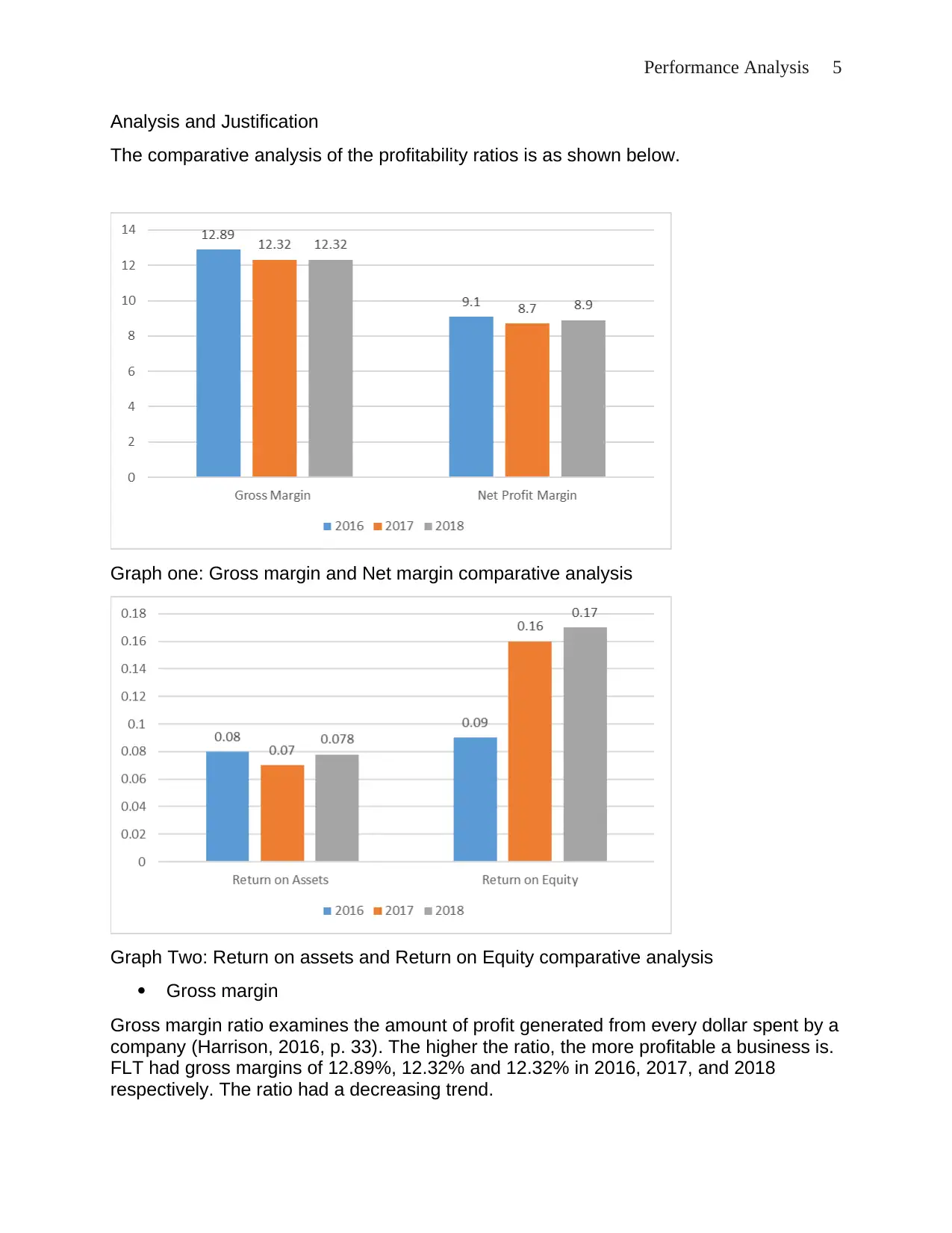

Analysis and Justification

The comparative analysis of the profitability ratios is as shown below.

Graph one: Gross margin and Net margin comparative analysis

Graph Two: Return on assets and Return on Equity comparative analysis

Gross margin

Gross margin ratio examines the amount of profit generated from every dollar spent by a

company (Harrison, 2016, p. 33). The higher the ratio, the more profitable a business is.

FLT had gross margins of 12.89%, 12.32% and 12.32% in 2016, 2017, and 2018

respectively. The ratio had a decreasing trend.

Analysis and Justification

The comparative analysis of the profitability ratios is as shown below.

Graph one: Gross margin and Net margin comparative analysis

Graph Two: Return on assets and Return on Equity comparative analysis

Gross margin

Gross margin ratio examines the amount of profit generated from every dollar spent by a

company (Harrison, 2016, p. 33). The higher the ratio, the more profitable a business is.

FLT had gross margins of 12.89%, 12.32% and 12.32% in 2016, 2017, and 2018

respectively. The ratio had a decreasing trend.

Performance Analysis 6

Net profit margin

Net profit margin measure the profitability of a business after taking both direct and

indirect expenses into account. The higher the ratio, the more profitable a business is

(Gibson, 2012, p. 97). FLT had net profit margins of 9.1%, 8.7% and 8.9% in 2016,

2017, and 2018 respectively. The ratio is on a reducing trend.

Return on assets

This ratio evaluates how effective a company is in using its assets to generate income

(Kaplan, 2012, p. 56). 8%, 7% and 7.8% of the net income generated by FLT in 2016,

2017, and 2018 respectively came from its assets.

Return on equity

This ratio evaluates how effective a company is in using its equity to generate income.

9%, 16% and 17% of the net income generated by FLT in 2016, 2017, and 2018

respectively came from owners’ equity.

b) Efficiency ratios

Efficiency ratios are used to evaluate the ability of FLT to manage its operations. The

ratios will be used to test the ability of the Company to utilize its assets and manage its

liabilities (Berrington & Bhandari, 2011, p. 90). The ratios have been calculated and

analysed, as shown below.

Calculations

Ratios Formula 2016 2017 2018

Accounts

Receivables

Turnover

Revenue/Average

Accounts Receivable

2,677,336/

672,176

= 3.98

2,641,775/

762,274

=3.47

2,949,955/

845,098

=3.49

Average

No. of Days

Receivables

Outstanding

365/Accounts

Receivables

Turnover

365/ 3.98

= 91 days

365/ 3.47

= 105 days

365/ 3.49

=104 days

Inventory

Turnover

Cost of Goods

Sold/Average

Inventory

2296732/

1,753,500

= 1.31

2321919/

1,480,500

= 1.59

2557947/

1,434,000

=1.78

Average

No. of Days

Inventory in

Stock

365/Inventory

Turnover

365/ 1.31

= 278 days

365/ 1.59

= 230 days

365/ 1.78

= 205

Working

Capital

Turnover

Sales/Average

Working Capital

2,677,336/

702,905

= 3.81

2,641,775/ 696509

= 3.79

2,949,955/

751,357

= 3.93

Fixed Asset

Turnover

Sales/Average Fixed

Assets

2,677,336/

686,675

= 3.9

2,641,775/

857,687

= 3.9

2,949,955/

913,881

= 3.23

Total

Assets

Sales/Average Total

Assets

2,677,336/

2,894,641

2,641,775/

3,099,350

2,949,955/

3300354

Net profit margin

Net profit margin measure the profitability of a business after taking both direct and

indirect expenses into account. The higher the ratio, the more profitable a business is

(Gibson, 2012, p. 97). FLT had net profit margins of 9.1%, 8.7% and 8.9% in 2016,

2017, and 2018 respectively. The ratio is on a reducing trend.

Return on assets

This ratio evaluates how effective a company is in using its assets to generate income

(Kaplan, 2012, p. 56). 8%, 7% and 7.8% of the net income generated by FLT in 2016,

2017, and 2018 respectively came from its assets.

Return on equity

This ratio evaluates how effective a company is in using its equity to generate income.

9%, 16% and 17% of the net income generated by FLT in 2016, 2017, and 2018

respectively came from owners’ equity.

b) Efficiency ratios

Efficiency ratios are used to evaluate the ability of FLT to manage its operations. The

ratios will be used to test the ability of the Company to utilize its assets and manage its

liabilities (Berrington & Bhandari, 2011, p. 90). The ratios have been calculated and

analysed, as shown below.

Calculations

Ratios Formula 2016 2017 2018

Accounts

Receivables

Turnover

Revenue/Average

Accounts Receivable

2,677,336/

672,176

= 3.98

2,641,775/

762,274

=3.47

2,949,955/

845,098

=3.49

Average

No. of Days

Receivables

Outstanding

365/Accounts

Receivables

Turnover

365/ 3.98

= 91 days

365/ 3.47

= 105 days

365/ 3.49

=104 days

Inventory

Turnover

Cost of Goods

Sold/Average

Inventory

2296732/

1,753,500

= 1.31

2321919/

1,480,500

= 1.59

2557947/

1,434,000

=1.78

Average

No. of Days

Inventory in

Stock

365/Inventory

Turnover

365/ 1.31

= 278 days

365/ 1.59

= 230 days

365/ 1.78

= 205

Working

Capital

Turnover

Sales/Average

Working Capital

2,677,336/

702,905

= 3.81

2,641,775/ 696509

= 3.79

2,949,955/

751,357

= 3.93

Fixed Asset

Turnover

Sales/Average Fixed

Assets

2,677,336/

686,675

= 3.9

2,641,775/

857,687

= 3.9

2,949,955/

913,881

= 3.23

Total

Assets

Sales/Average Total

Assets

2,677,336/

2,894,641

2,641,775/

3,099,350

2,949,955/

3300354

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Performance Analysis 7

Turnover = 0.92 = 0.85 = 0.89

Analysis and Justification

The comparative analysis of the efficiency ratios is as shown below.

Graph Three: Efficiency ratio comparative analysis

Graph Four: Efficiency ratio comparative analysis

Accounts Receivables Turnover

The ratio evaluates the efficiency of a company’s credit policies. Accounts receivable

turnover ratio evaluates how quick customers pay their bills to the company. The lower

the number of days it takes for a company to collect debts from customers, the better.

On the other hand, many collection days shows the inefficiency of a company’s credit

Turnover = 0.92 = 0.85 = 0.89

Analysis and Justification

The comparative analysis of the efficiency ratios is as shown below.

Graph Three: Efficiency ratio comparative analysis

Graph Four: Efficiency ratio comparative analysis

Accounts Receivables Turnover

The ratio evaluates the efficiency of a company’s credit policies. Accounts receivable

turnover ratio evaluates how quick customers pay their bills to the company. The lower

the number of days it takes for a company to collect debts from customers, the better.

On the other hand, many collection days shows the inefficiency of a company’s credit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance Analysis 8

policy (Gassen & Schwedler, 2010, p. 112). FLT’s account receivables turnover was

3.98, 3.47, and 3.49 in 2016, 2017, and 2018, respectively. The ratio is high meaning

that FLT has ineffective credit policies.

Inventory Turnover

Inventory turnover evaluates the efficiency of a company in managing inventory. A lower

ratio shows that a company has failed in efficiently managing its inventory. On the other

hand, a higher ratio indicates that a company is efficient in managing its inventory (Van,

2009, p. 66). FLT had an inventory turnover ratio of 1.31, 1.59, and 1.78 in 2016, 2017,

and 2018, respectively. The trend is increasing. Therefore, the inventories are staying

longer in the company before they are sold.

Working Capital Turnover

The ratio measures the operating capital that is required by a company to maintain its

sales. A company with a higher working capital turnover is considered to be efficient in

managing its working capital. On the other had a low ratio indicates that a company has

not utilized its working capital to the maximum (Deegan, 2013, p. 71). FLT’s working

capital turnover ratio was 3.81, 3.79, and 3.93 in 2016, 2017, and 2018, respectively.

The ratios show that the company is efficient in managing its working capital.

Fixed Asset Turnover

Fixed asset turnover ratio measures sales that a company generates from its long term

capital investments. The ratio evaluates how efficient is a company’s capital investments

(Demirgüneş, 2015, p. 34). Higher the ratio, the better for a company. FLT’s fixed asset

turnover ratio was 3.9, 3.9, and 3.28 in 2016, 2017, and 2018, respectively. FLT was

efficient in using its long term capital investments to generate sales.

Total Assets Turnover

Total assets turnover ratios measure a company’s efficiency to generate income using

current and fixed assets. A higher ratio is better because it shows how effective a

company is when utilizing its entire funds (Edmonds, et al., 2015, p. 75). FLT’s total

asset turnover ratio was 0.92, 0.85, and 0.89 in 2016, 2017, and 2018 respectively. The

three ratios are less than one showing that FLT was ineffective in utilizing its funds to

generate sales.

Average No. of Days Receivables Outstanding

The ratio measures the number of days in a year; it takes a company to collect a debt

from customers. The lower the number of days, the better. On average it takes FLT a

100 days to collect its debts from customers (Brigham & Ehrhardt, 2014, p. 62). The

collections days were 91, 105, and 104 in 2016, 2017, and 2018, respectively. The

company has an ineffective credit because the number of collection days has increased

between 2016 and 2018.

Average No. of Days Inventory in Stock

The ratio evaluates the number of days it takes before inventory is sold out. The fewer

the days inventory is help before being sold, the better. FLT held its inventory for 278

policy (Gassen & Schwedler, 2010, p. 112). FLT’s account receivables turnover was

3.98, 3.47, and 3.49 in 2016, 2017, and 2018, respectively. The ratio is high meaning

that FLT has ineffective credit policies.

Inventory Turnover

Inventory turnover evaluates the efficiency of a company in managing inventory. A lower

ratio shows that a company has failed in efficiently managing its inventory. On the other

hand, a higher ratio indicates that a company is efficient in managing its inventory (Van,

2009, p. 66). FLT had an inventory turnover ratio of 1.31, 1.59, and 1.78 in 2016, 2017,

and 2018, respectively. The trend is increasing. Therefore, the inventories are staying

longer in the company before they are sold.

Working Capital Turnover

The ratio measures the operating capital that is required by a company to maintain its

sales. A company with a higher working capital turnover is considered to be efficient in

managing its working capital. On the other had a low ratio indicates that a company has

not utilized its working capital to the maximum (Deegan, 2013, p. 71). FLT’s working

capital turnover ratio was 3.81, 3.79, and 3.93 in 2016, 2017, and 2018, respectively.

The ratios show that the company is efficient in managing its working capital.

Fixed Asset Turnover

Fixed asset turnover ratio measures sales that a company generates from its long term

capital investments. The ratio evaluates how efficient is a company’s capital investments

(Demirgüneş, 2015, p. 34). Higher the ratio, the better for a company. FLT’s fixed asset

turnover ratio was 3.9, 3.9, and 3.28 in 2016, 2017, and 2018, respectively. FLT was

efficient in using its long term capital investments to generate sales.

Total Assets Turnover

Total assets turnover ratios measure a company’s efficiency to generate income using

current and fixed assets. A higher ratio is better because it shows how effective a

company is when utilizing its entire funds (Edmonds, et al., 2015, p. 75). FLT’s total

asset turnover ratio was 0.92, 0.85, and 0.89 in 2016, 2017, and 2018 respectively. The

three ratios are less than one showing that FLT was ineffective in utilizing its funds to

generate sales.

Average No. of Days Receivables Outstanding

The ratio measures the number of days in a year; it takes a company to collect a debt

from customers. The lower the number of days, the better. On average it takes FLT a

100 days to collect its debts from customers (Brigham & Ehrhardt, 2014, p. 62). The

collections days were 91, 105, and 104 in 2016, 2017, and 2018, respectively. The

company has an ineffective credit because the number of collection days has increased

between 2016 and 2018.

Average No. of Days Inventory in Stock

The ratio evaluates the number of days it takes before inventory is sold out. The fewer

the days inventory is help before being sold, the better. FLT held its inventory for 278

Performance Analysis 9

days, 230 days, and 205 days before being sold in 2016, 2017, and 2018 respectively.

The number of days it takes to sell inventory has reduced between 2016 and 2018.

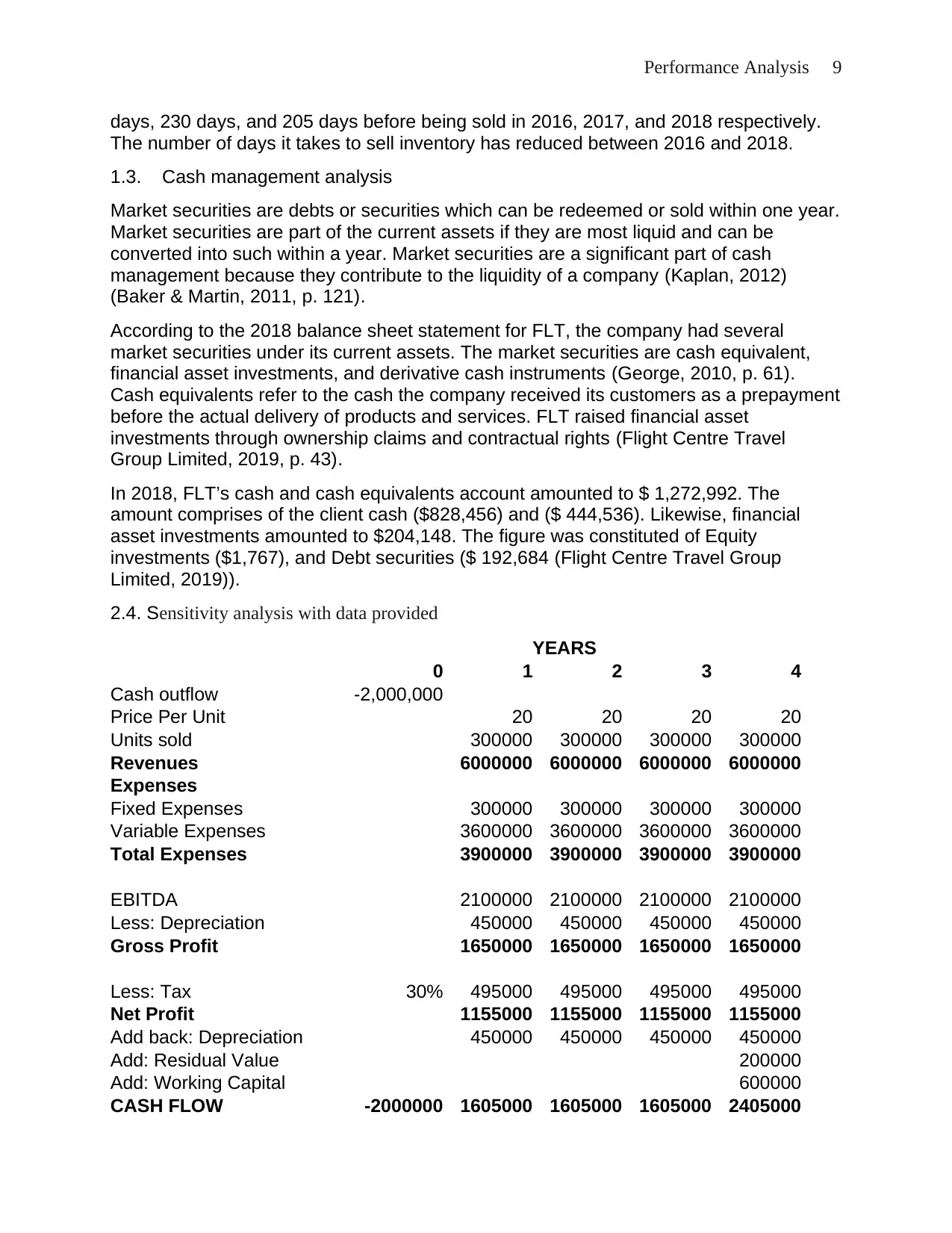

1.3. Cash management analysis

Market securities are debts or securities which can be redeemed or sold within one year.

Market securities are part of the current assets if they are most liquid and can be

converted into such within a year. Market securities are a significant part of cash

management because they contribute to the liquidity of a company (Kaplan, 2012)

(Baker & Martin, 2011, p. 121).

According to the 2018 balance sheet statement for FLT, the company had several

market securities under its current assets. The market securities are cash equivalent,

financial asset investments, and derivative cash instruments (George, 2010, p. 61).

Cash equivalents refer to the cash the company received its customers as a prepayment

before the actual delivery of products and services. FLT raised financial asset

investments through ownership claims and contractual rights (Flight Centre Travel

Group Limited, 2019, p. 43).

In 2018, FLT’s cash and cash equivalents account amounted to $ 1,272,992. The

amount comprises of the client cash ($828,456) and ($ 444,536). Likewise, financial

asset investments amounted to $204,148. The figure was constituted of Equity

investments ($1,767), and Debt securities ($ 192,684 (Flight Centre Travel Group

Limited, 2019)).

2.4. Sensitivity analysis with data provided

YEARS

0 1 2 3 4

Cash outflow -2,000,000

Price Per Unit 20 20 20 20

Units sold 300000 300000 300000 300000

Revenues 6000000 6000000 6000000 6000000

Expenses

Fixed Expenses 300000 300000 300000 300000

Variable Expenses 3600000 3600000 3600000 3600000

Total Expenses 3900000 3900000 3900000 3900000

EBITDA 2100000 2100000 2100000 2100000

Less: Depreciation 450000 450000 450000 450000

Gross Profit 1650000 1650000 1650000 1650000

Less: Tax 30% 495000 495000 495000 495000

Net Profit 1155000 1155000 1155000 1155000

Add back: Depreciation 450000 450000 450000 450000

Add: Residual Value 200000

Add: Working Capital 600000

CASH FLOW -2000000 1605000 1605000 1605000 2405000

days, 230 days, and 205 days before being sold in 2016, 2017, and 2018 respectively.

The number of days it takes to sell inventory has reduced between 2016 and 2018.

1.3. Cash management analysis

Market securities are debts or securities which can be redeemed or sold within one year.

Market securities are part of the current assets if they are most liquid and can be

converted into such within a year. Market securities are a significant part of cash

management because they contribute to the liquidity of a company (Kaplan, 2012)

(Baker & Martin, 2011, p. 121).

According to the 2018 balance sheet statement for FLT, the company had several

market securities under its current assets. The market securities are cash equivalent,

financial asset investments, and derivative cash instruments (George, 2010, p. 61).

Cash equivalents refer to the cash the company received its customers as a prepayment

before the actual delivery of products and services. FLT raised financial asset

investments through ownership claims and contractual rights (Flight Centre Travel

Group Limited, 2019, p. 43).

In 2018, FLT’s cash and cash equivalents account amounted to $ 1,272,992. The

amount comprises of the client cash ($828,456) and ($ 444,536). Likewise, financial

asset investments amounted to $204,148. The figure was constituted of Equity

investments ($1,767), and Debt securities ($ 192,684 (Flight Centre Travel Group

Limited, 2019)).

2.4. Sensitivity analysis with data provided

YEARS

0 1 2 3 4

Cash outflow -2,000,000

Price Per Unit 20 20 20 20

Units sold 300000 300000 300000 300000

Revenues 6000000 6000000 6000000 6000000

Expenses

Fixed Expenses 300000 300000 300000 300000

Variable Expenses 3600000 3600000 3600000 3600000

Total Expenses 3900000 3900000 3900000 3900000

EBITDA 2100000 2100000 2100000 2100000

Less: Depreciation 450000 450000 450000 450000

Gross Profit 1650000 1650000 1650000 1650000

Less: Tax 30% 495000 495000 495000 495000

Net Profit 1155000 1155000 1155000 1155000

Add back: Depreciation 450000 450000 450000 450000

Add: Residual Value 200000

Add: Working Capital 600000

CASH FLOW -2000000 1605000 1605000 1605000 2405000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

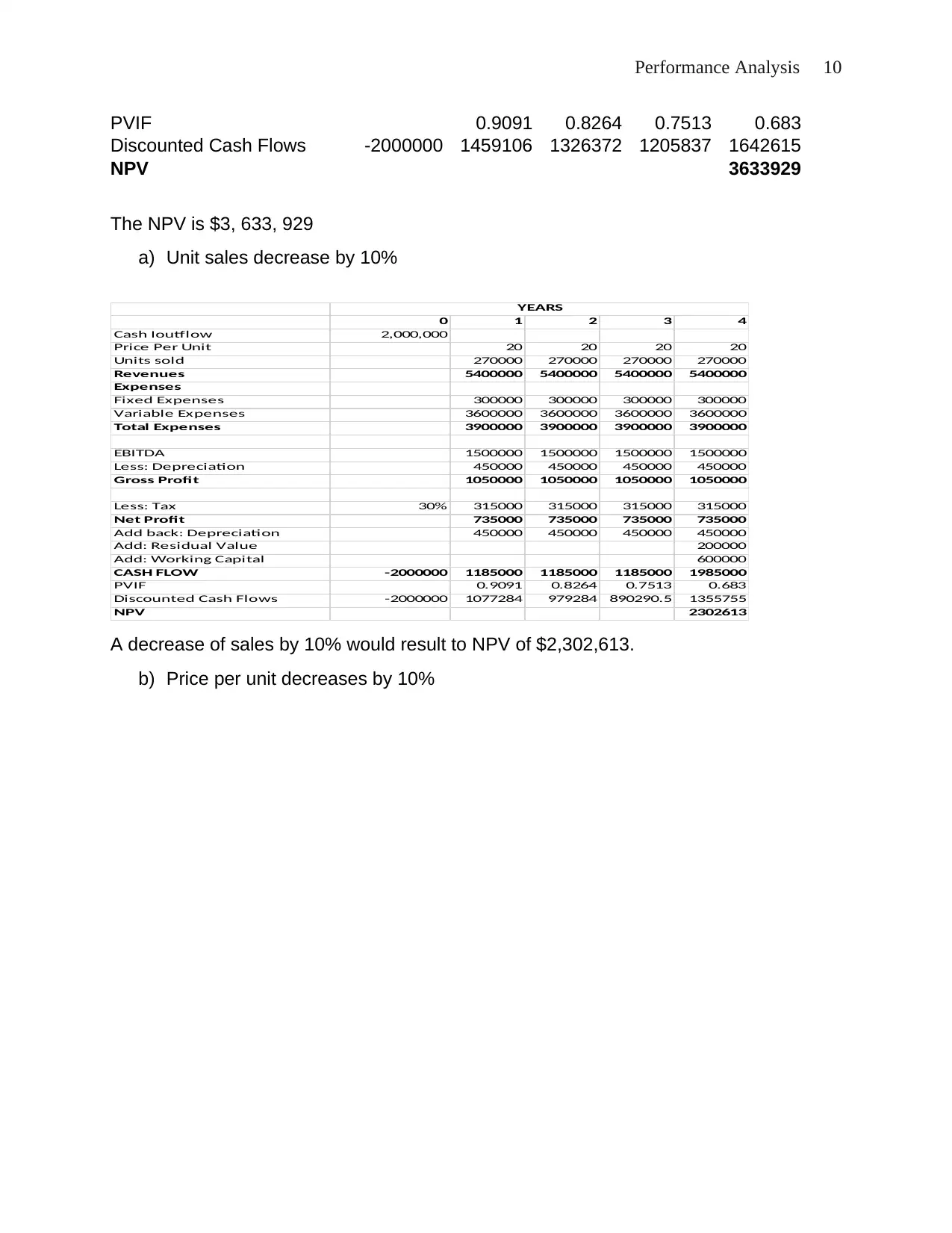

Performance Analysis 10

PVIF 0.9091 0.8264 0.7513 0.683

Discounted Cash Flows -2000000 1459106 1326372 1205837 1642615

NPV 3633929

The NPV is $3, 633, 929

a) Unit sales decrease by 10%

0 1 2 3 4

Cash Ioutflow 2,000,000

Price Per Unit 20 20 20 20

Units sold 270000 270000 270000 270000

Revenues 5400000 5400000 5400000 5400000

Expenses

Fixed Expenses 300000 300000 300000 300000

Variable Expenses 3600000 3600000 3600000 3600000

Total Expenses 3900000 3900000 3900000 3900000

EBITDA 1500000 1500000 1500000 1500000

Less: Depreciation 450000 450000 450000 450000

Gross Profit 1050000 1050000 1050000 1050000

Less: Tax 30% 315000 315000 315000 315000

Net Profit 735000 735000 735000 735000

Add back: Depreciation 450000 450000 450000 450000

Add: Residual Value 200000

Add: Working Capital 600000

CASH FLOW -2000000 1185000 1185000 1185000 1985000

PVIF 0.9091 0.8264 0.7513 0.683

Discounted Cash Flows -2000000 1077284 979284 890290.5 1355755

NPV 2302613

YEARS

A decrease of sales by 10% would result to NPV of $2,302,613.

b) Price per unit decreases by 10%

PVIF 0.9091 0.8264 0.7513 0.683

Discounted Cash Flows -2000000 1459106 1326372 1205837 1642615

NPV 3633929

The NPV is $3, 633, 929

a) Unit sales decrease by 10%

0 1 2 3 4

Cash Ioutflow 2,000,000

Price Per Unit 20 20 20 20

Units sold 270000 270000 270000 270000

Revenues 5400000 5400000 5400000 5400000

Expenses

Fixed Expenses 300000 300000 300000 300000

Variable Expenses 3600000 3600000 3600000 3600000

Total Expenses 3900000 3900000 3900000 3900000

EBITDA 1500000 1500000 1500000 1500000

Less: Depreciation 450000 450000 450000 450000

Gross Profit 1050000 1050000 1050000 1050000

Less: Tax 30% 315000 315000 315000 315000

Net Profit 735000 735000 735000 735000

Add back: Depreciation 450000 450000 450000 450000

Add: Residual Value 200000

Add: Working Capital 600000

CASH FLOW -2000000 1185000 1185000 1185000 1985000

PVIF 0.9091 0.8264 0.7513 0.683

Discounted Cash Flows -2000000 1077284 979284 890290.5 1355755

NPV 2302613

YEARS

A decrease of sales by 10% would result to NPV of $2,302,613.

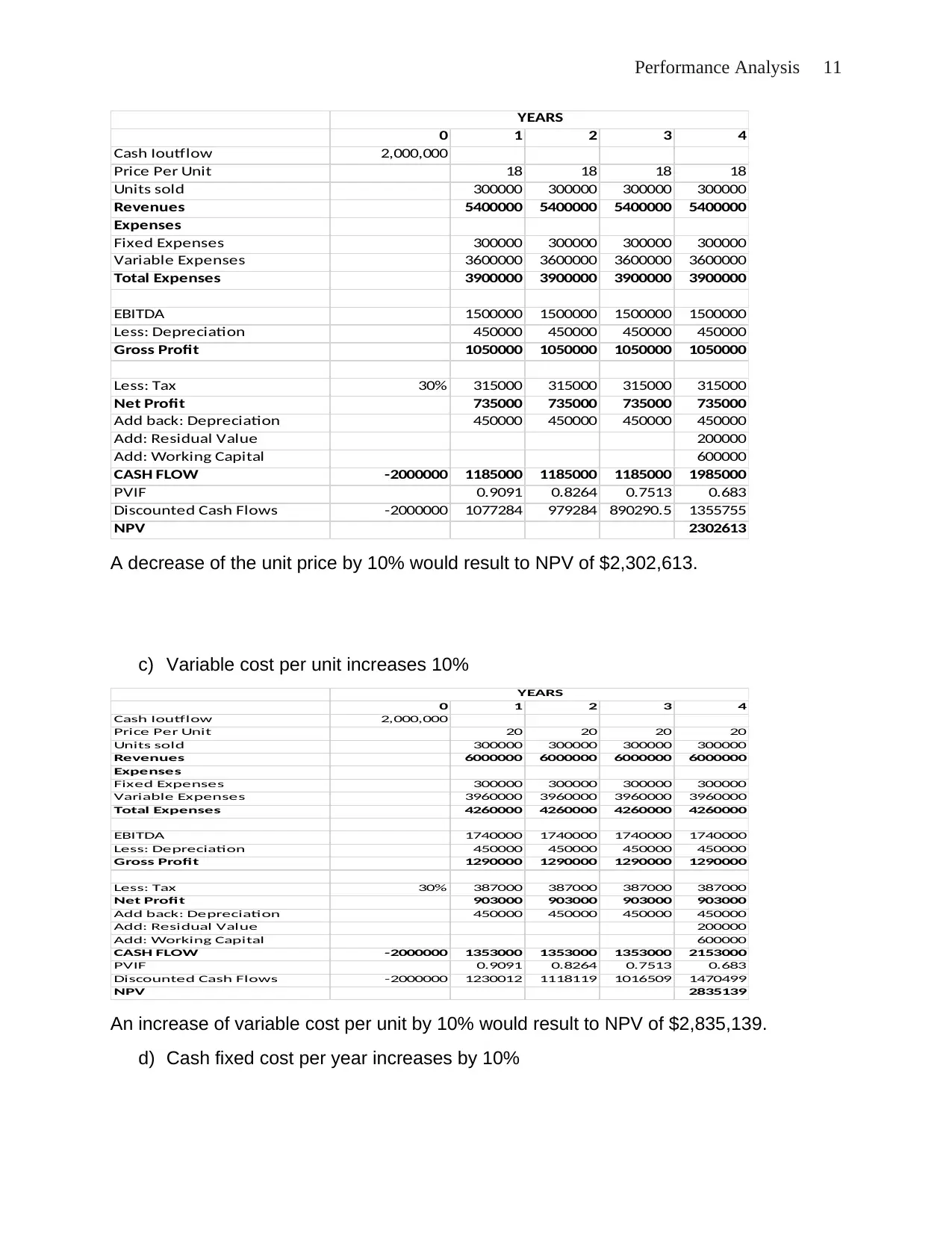

b) Price per unit decreases by 10%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance Analysis 11

0 1 2 3 4

Cash Ioutflow 2,000,000

Price Per Unit 18 18 18 18

Units sold 300000 300000 300000 300000

Revenues 5400000 5400000 5400000 5400000

Expenses

Fixed Expenses 300000 300000 300000 300000

Variable Expenses 3600000 3600000 3600000 3600000

Total Expenses 3900000 3900000 3900000 3900000

EBITDA 1500000 1500000 1500000 1500000

Less: Depreciation 450000 450000 450000 450000

Gross Profit 1050000 1050000 1050000 1050000

Less: Tax 30% 315000 315000 315000 315000

Net Profit 735000 735000 735000 735000

Add back: Depreciation 450000 450000 450000 450000

Add: Residual Value 200000

Add: Working Capital 600000

CASH FLOW -2000000 1185000 1185000 1185000 1985000

PVIF 0.9091 0.8264 0.7513 0.683

Discounted Cash Flows -2000000 1077284 979284 890290.5 1355755

NPV 2302613

YEARS

A decrease of the unit price by 10% would result to NPV of $2,302,613.

c) Variable cost per unit increases 10%

0 1 2 3 4

Cash Ioutflow 2,000,000

Price Per Unit 20 20 20 20

Units sold 300000 300000 300000 300000

Revenues 6000000 6000000 6000000 6000000

Expenses

Fixed Expenses 300000 300000 300000 300000

Variable Expenses 3960000 3960000 3960000 3960000

Total Expenses 4260000 4260000 4260000 4260000

EBITDA 1740000 1740000 1740000 1740000

Less: Depreciation 450000 450000 450000 450000

Gross Profit 1290000 1290000 1290000 1290000

Less: Tax 30% 387000 387000 387000 387000

Net Profit 903000 903000 903000 903000

Add back: Depreciation 450000 450000 450000 450000

Add: Residual Value 200000

Add: Working Capital 600000

CASH FLOW -2000000 1353000 1353000 1353000 2153000

PVIF 0.9091 0.8264 0.7513 0.683

Discounted Cash Flows -2000000 1230012 1118119 1016509 1470499

NPV 2835139

YEARS

An increase of variable cost per unit by 10% would result to NPV of $2,835,139.

d) Cash fixed cost per year increases by 10%

0 1 2 3 4

Cash Ioutflow 2,000,000

Price Per Unit 18 18 18 18

Units sold 300000 300000 300000 300000

Revenues 5400000 5400000 5400000 5400000

Expenses

Fixed Expenses 300000 300000 300000 300000

Variable Expenses 3600000 3600000 3600000 3600000

Total Expenses 3900000 3900000 3900000 3900000

EBITDA 1500000 1500000 1500000 1500000

Less: Depreciation 450000 450000 450000 450000

Gross Profit 1050000 1050000 1050000 1050000

Less: Tax 30% 315000 315000 315000 315000

Net Profit 735000 735000 735000 735000

Add back: Depreciation 450000 450000 450000 450000

Add: Residual Value 200000

Add: Working Capital 600000

CASH FLOW -2000000 1185000 1185000 1185000 1985000

PVIF 0.9091 0.8264 0.7513 0.683

Discounted Cash Flows -2000000 1077284 979284 890290.5 1355755

NPV 2302613

YEARS

A decrease of the unit price by 10% would result to NPV of $2,302,613.

c) Variable cost per unit increases 10%

0 1 2 3 4

Cash Ioutflow 2,000,000

Price Per Unit 20 20 20 20

Units sold 300000 300000 300000 300000

Revenues 6000000 6000000 6000000 6000000

Expenses

Fixed Expenses 300000 300000 300000 300000

Variable Expenses 3960000 3960000 3960000 3960000

Total Expenses 4260000 4260000 4260000 4260000

EBITDA 1740000 1740000 1740000 1740000

Less: Depreciation 450000 450000 450000 450000

Gross Profit 1290000 1290000 1290000 1290000

Less: Tax 30% 387000 387000 387000 387000

Net Profit 903000 903000 903000 903000

Add back: Depreciation 450000 450000 450000 450000

Add: Residual Value 200000

Add: Working Capital 600000

CASH FLOW -2000000 1353000 1353000 1353000 2153000

PVIF 0.9091 0.8264 0.7513 0.683

Discounted Cash Flows -2000000 1230012 1118119 1016509 1470499

NPV 2835139

YEARS

An increase of variable cost per unit by 10% would result to NPV of $2,835,139.

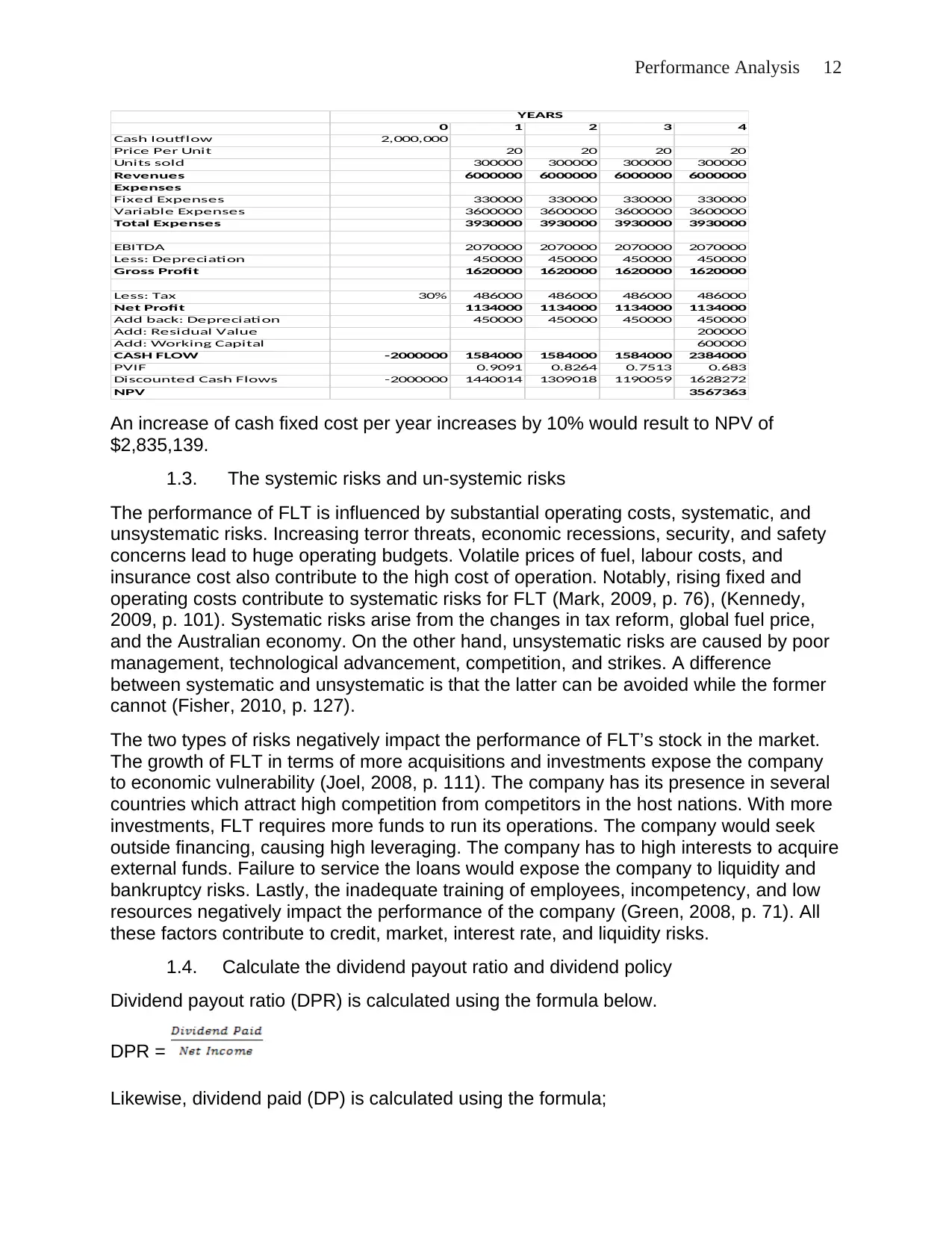

d) Cash fixed cost per year increases by 10%

Performance Analysis 12

0 1 2 3 4

Cash Ioutflow 2,000,000

Price Per Unit 20 20 20 20

Units sold 300000 300000 300000 300000

Revenues 6000000 6000000 6000000 6000000

Expenses

Fixed Expenses 330000 330000 330000 330000

Variable Expenses 3600000 3600000 3600000 3600000

Total Expenses 3930000 3930000 3930000 3930000

EBITDA 2070000 2070000 2070000 2070000

Less: Depreciation 450000 450000 450000 450000

Gross Profit 1620000 1620000 1620000 1620000

Less: Tax 30% 486000 486000 486000 486000

Net Profit 1134000 1134000 1134000 1134000

Add back: Depreciation 450000 450000 450000 450000

Add: Residual Value 200000

Add: Working Capital 600000

CASH FLOW -2000000 1584000 1584000 1584000 2384000

PVIF 0.9091 0.8264 0.7513 0.683

Discounted Cash Flows -2000000 1440014 1309018 1190059 1628272

NPV 3567363

YEARS

An increase of cash fixed cost per year increases by 10% would result to NPV of

$2,835,139.

1.3. The systemic risks and un-systemic risks

The performance of FLT is influenced by substantial operating costs, systematic, and

unsystematic risks. Increasing terror threats, economic recessions, security, and safety

concerns lead to huge operating budgets. Volatile prices of fuel, labour costs, and

insurance cost also contribute to the high cost of operation. Notably, rising fixed and

operating costs contribute to systematic risks for FLT (Mark, 2009, p. 76), (Kennedy,

2009, p. 101). Systematic risks arise from the changes in tax reform, global fuel price,

and the Australian economy. On the other hand, unsystematic risks are caused by poor

management, technological advancement, competition, and strikes. A difference

between systematic and unsystematic is that the latter can be avoided while the former

cannot (Fisher, 2010, p. 127).

The two types of risks negatively impact the performance of FLT’s stock in the market.

The growth of FLT in terms of more acquisitions and investments expose the company

to economic vulnerability (Joel, 2008, p. 111). The company has its presence in several

countries which attract high competition from competitors in the host nations. With more

investments, FLT requires more funds to run its operations. The company would seek

outside financing, causing high leveraging. The company has to high interests to acquire

external funds. Failure to service the loans would expose the company to liquidity and

bankruptcy risks. Lastly, the inadequate training of employees, incompetency, and low

resources negatively impact the performance of the company (Green, 2008, p. 71). All

these factors contribute to credit, market, interest rate, and liquidity risks.

1.4. Calculate the dividend payout ratio and dividend policy

Dividend payout ratio (DPR) is calculated using the formula below.

DPR =

Likewise, dividend paid (DP) is calculated using the formula;

0 1 2 3 4

Cash Ioutflow 2,000,000

Price Per Unit 20 20 20 20

Units sold 300000 300000 300000 300000

Revenues 6000000 6000000 6000000 6000000

Expenses

Fixed Expenses 330000 330000 330000 330000

Variable Expenses 3600000 3600000 3600000 3600000

Total Expenses 3930000 3930000 3930000 3930000

EBITDA 2070000 2070000 2070000 2070000

Less: Depreciation 450000 450000 450000 450000

Gross Profit 1620000 1620000 1620000 1620000

Less: Tax 30% 486000 486000 486000 486000

Net Profit 1134000 1134000 1134000 1134000

Add back: Depreciation 450000 450000 450000 450000

Add: Residual Value 200000

Add: Working Capital 600000

CASH FLOW -2000000 1584000 1584000 1584000 2384000

PVIF 0.9091 0.8264 0.7513 0.683

Discounted Cash Flows -2000000 1440014 1309018 1190059 1628272

NPV 3567363

YEARS

An increase of cash fixed cost per year increases by 10% would result to NPV of

$2,835,139.

1.3. The systemic risks and un-systemic risks

The performance of FLT is influenced by substantial operating costs, systematic, and

unsystematic risks. Increasing terror threats, economic recessions, security, and safety

concerns lead to huge operating budgets. Volatile prices of fuel, labour costs, and

insurance cost also contribute to the high cost of operation. Notably, rising fixed and

operating costs contribute to systematic risks for FLT (Mark, 2009, p. 76), (Kennedy,

2009, p. 101). Systematic risks arise from the changes in tax reform, global fuel price,

and the Australian economy. On the other hand, unsystematic risks are caused by poor

management, technological advancement, competition, and strikes. A difference

between systematic and unsystematic is that the latter can be avoided while the former

cannot (Fisher, 2010, p. 127).

The two types of risks negatively impact the performance of FLT’s stock in the market.

The growth of FLT in terms of more acquisitions and investments expose the company

to economic vulnerability (Joel, 2008, p. 111). The company has its presence in several

countries which attract high competition from competitors in the host nations. With more

investments, FLT requires more funds to run its operations. The company would seek

outside financing, causing high leveraging. The company has to high interests to acquire

external funds. Failure to service the loans would expose the company to liquidity and

bankruptcy risks. Lastly, the inadequate training of employees, incompetency, and low

resources negatively impact the performance of the company (Green, 2008, p. 71). All

these factors contribute to credit, market, interest rate, and liquidity risks.

1.4. Calculate the dividend payout ratio and dividend policy

Dividend payout ratio (DPR) is calculated using the formula below.

DPR =

Likewise, dividend paid (DP) is calculated using the formula;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.