FIN203 Corporate Finance: Financial Analysis and Strategy of FMG

VerifiedAdded on 2023/06/03

|9

|1523

|52

Report

AI Summary

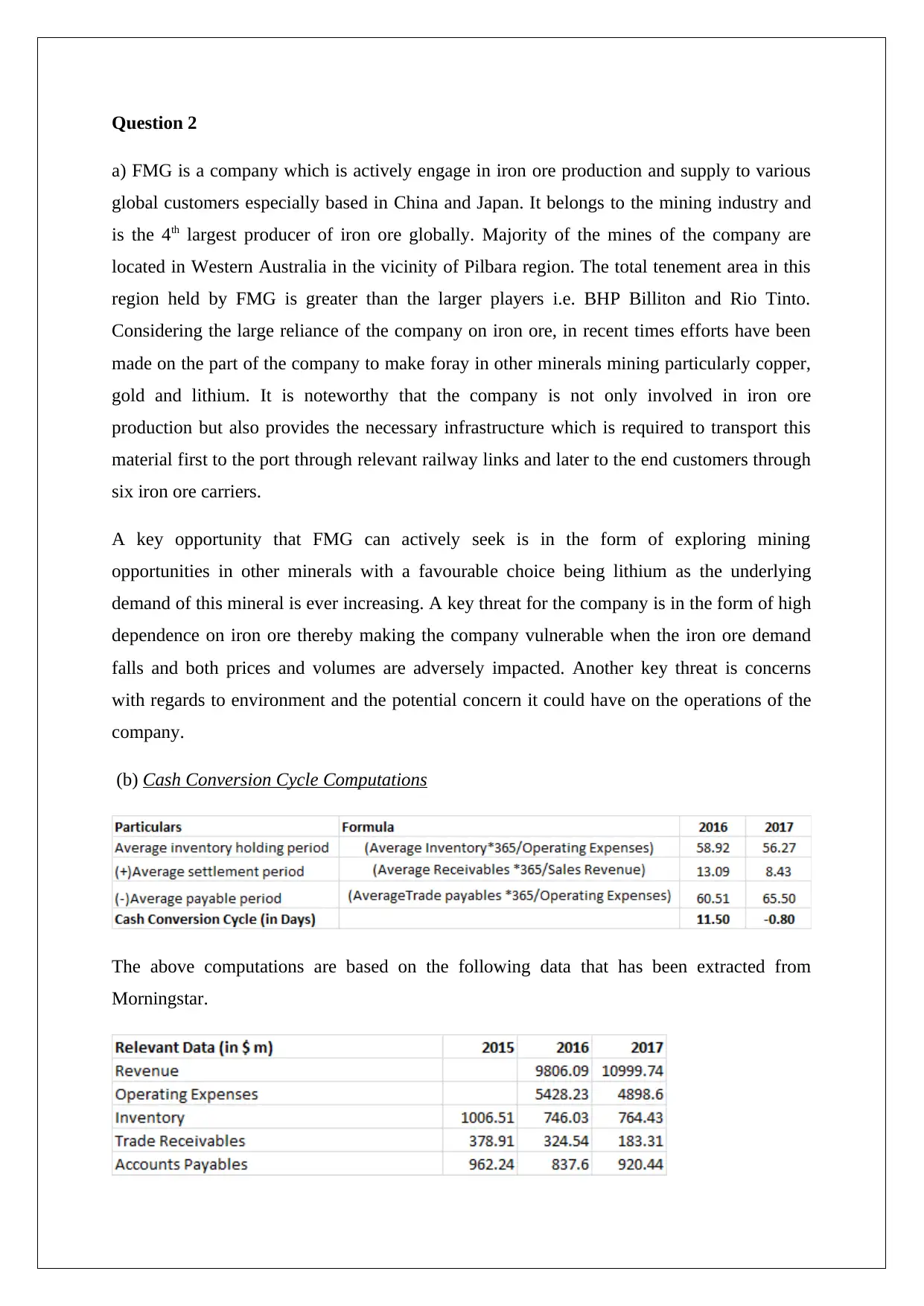

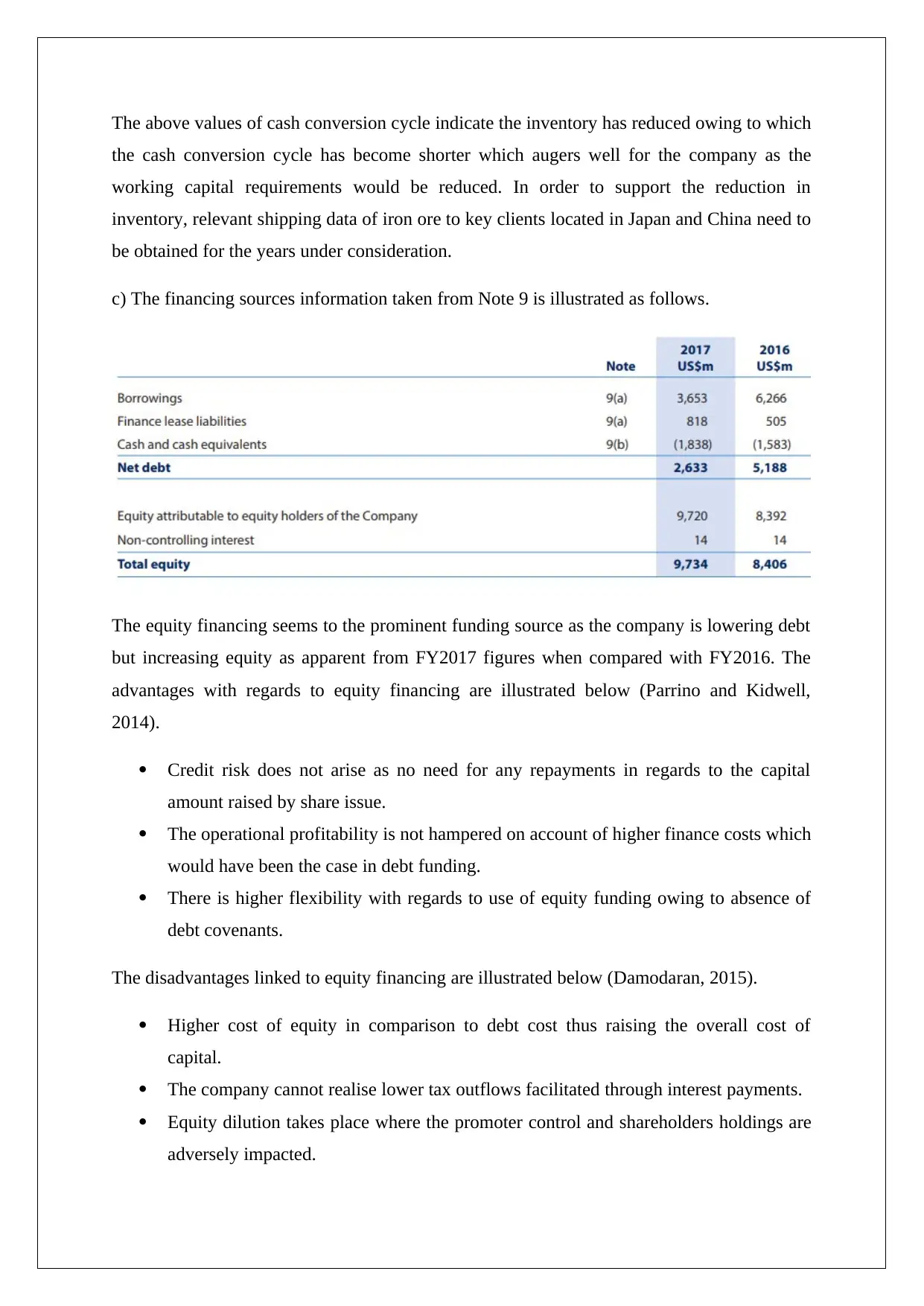

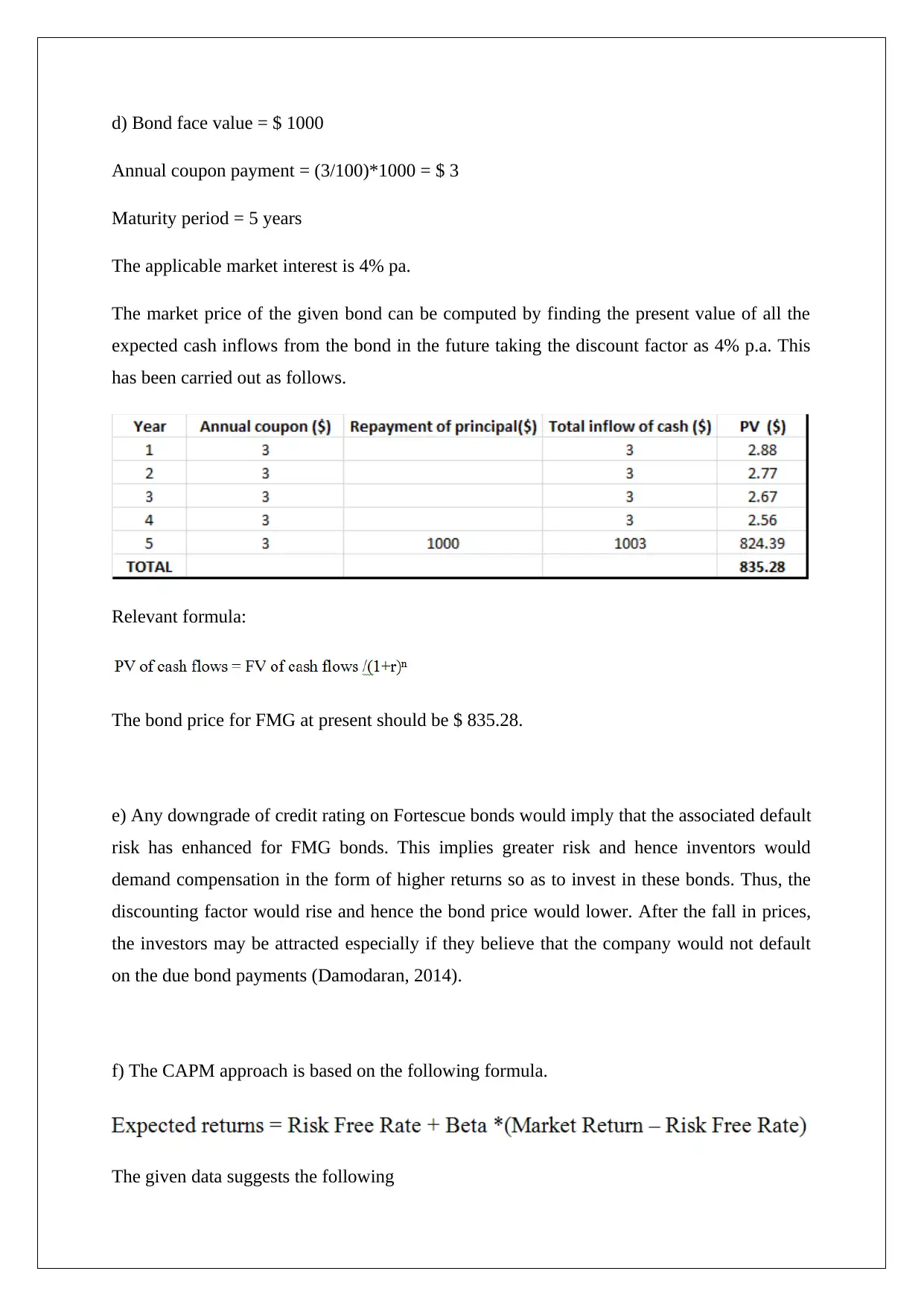

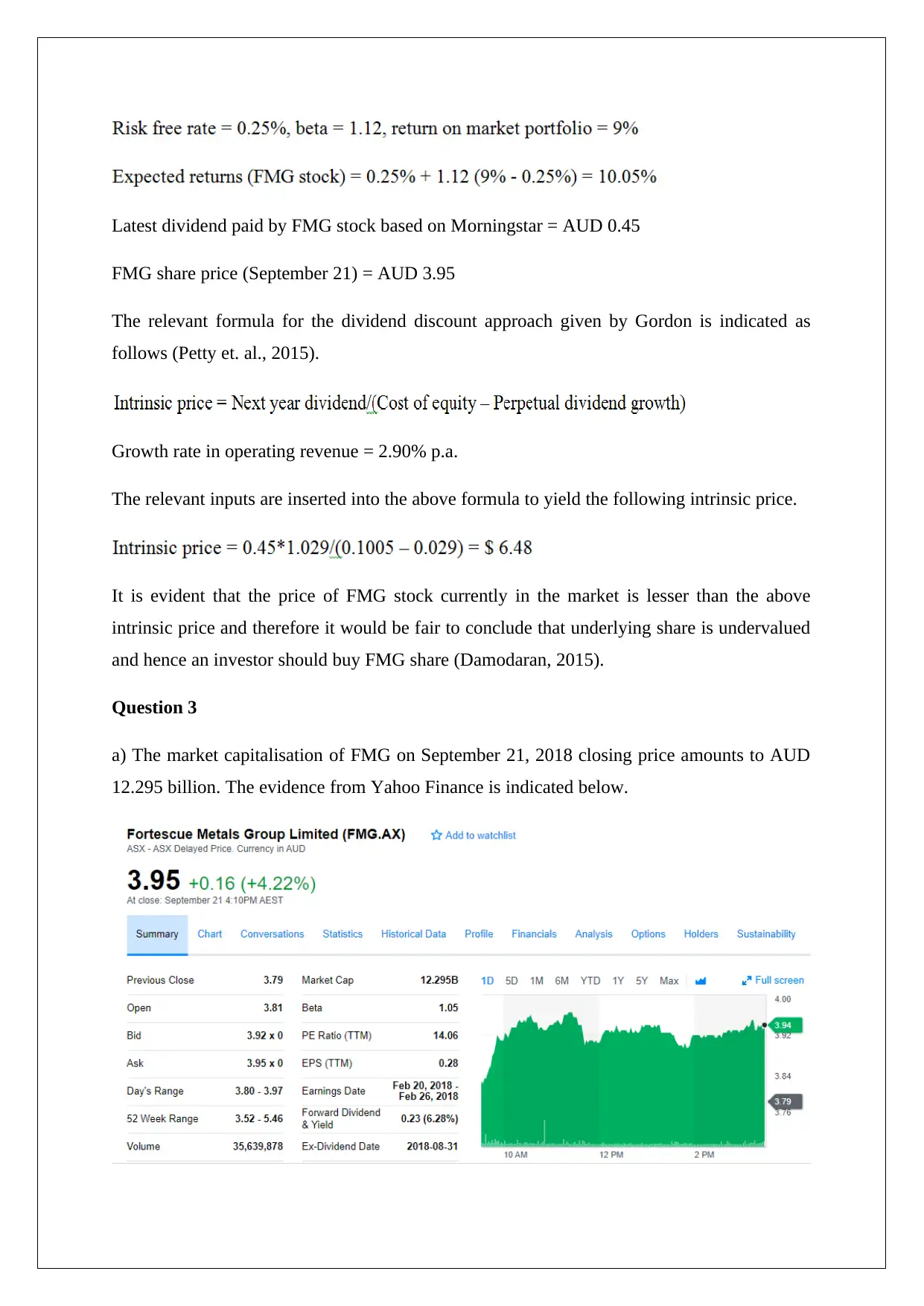

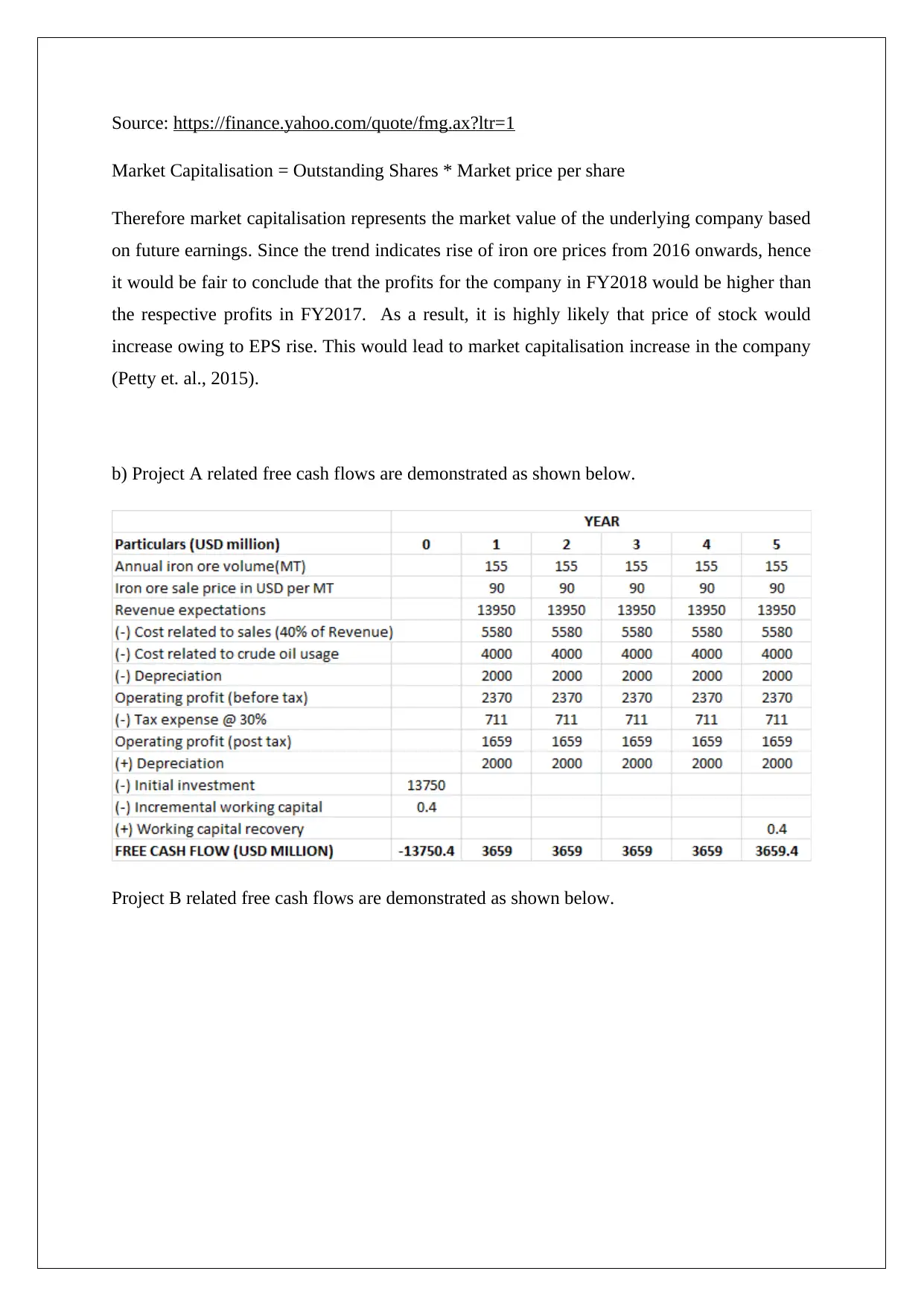

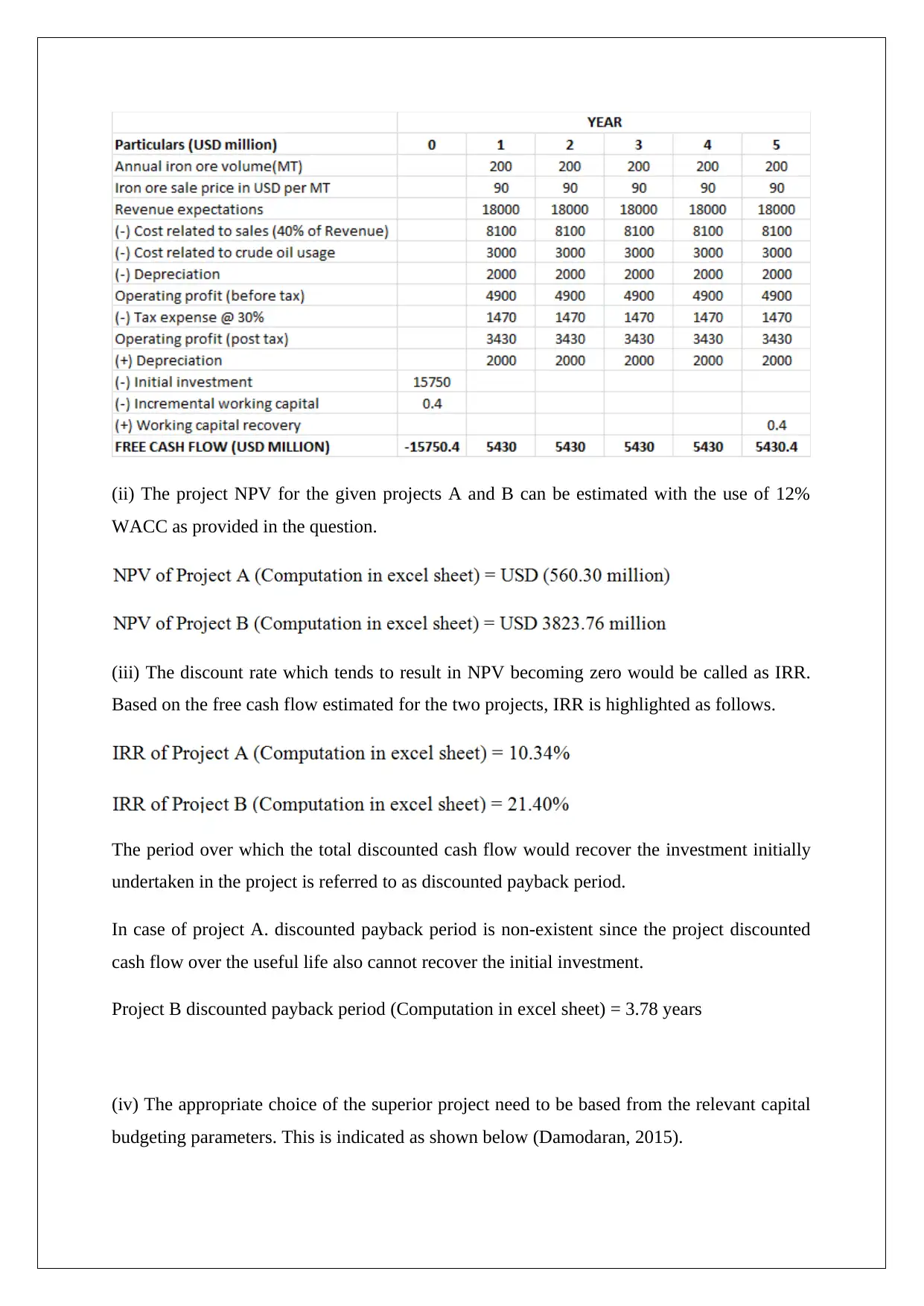

This report provides a comprehensive financial analysis of Fortescue Metals Group (FMG), a major iron ore producer. It examines FMG's business operations, focusing on its reliance on iron ore and diversification efforts into other minerals like lithium. The report includes computations of the cash conversion cycle, analysis of financing sources with a focus on equity financing, bond valuation, and the impact of credit rating downgrades. Furthermore, the report employs the CAPM and dividend discount model to assess the intrinsic value of FMG's stock. A capital budgeting exercise analyzes two projects (A and B) using NPV, IRR, and discounted payback period criteria, recommending Project B based on superior financial metrics. The analysis also considers the impact of asset sales on project selection. The document includes references to support the analysis and is intended to provide insights into FMG's financial health and investment potential. Find more solved assignments like this on Desklib.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.