FNCE 300 Assignment 3: Valuation of Common Stocks and Risk Management

VerifiedAdded on 2022/09/01

|17

|3160

|15

Homework Assignment

AI Summary

This document presents a comprehensive solution to FNCE 300 Assignment 3, focusing on key financial concepts. The assignment covers the valuation of common stocks using the dividend discount model, including calculations for present value, and analyzing the impact of growth rates and retention ratios. It delves into risk management principles, exploring confidence intervals for investments, and bond evaluation. The solution examines hedging, insurance, and diversification strategies, analyzing price variance, and the impact of hedging on various scenarios. The document also includes detailed calculations and explanations for each problem, providing a thorough understanding of the financial concepts covered in the assignment.

Running head: FNCE300

FNCE 300

Name of the Student:

Name of the University:

Author’s Note

FNCE 300

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FNCE 300

Table of Contents

Lesson 9: Valuation of Common Stocks.........................................................................................2

9.1 Dividend Discount Model......................................................................................................2

9.2 Valuation................................................................................................................................2

9.3 Equation Analysis..................................................................................................................4

9.4 Kirk’s Information Inc...........................................................................................................5

9.5 Invest Co. Inc.........................................................................................................................7

Lesson 10: Principles of Risk Management....................................................................................8

10.1 Computroids and Blazer Inc................................................................................................8

10.2 Bond Evaluation................................................................................................................12

10.3 Retail Business...................................................................................................................13

Lesson 11: Hedging, Insuring, and Diversifying...........................................................................13

11.1 Hedging..............................................................................................................................13

11.2 Annuity..............................................................................................................................14

11.3 Hedging..............................................................................................................................15

Table of Contents

Lesson 9: Valuation of Common Stocks.........................................................................................2

9.1 Dividend Discount Model......................................................................................................2

9.2 Valuation................................................................................................................................2

9.3 Equation Analysis..................................................................................................................4

9.4 Kirk’s Information Inc...........................................................................................................5

9.5 Invest Co. Inc.........................................................................................................................7

Lesson 10: Principles of Risk Management....................................................................................8

10.1 Computroids and Blazer Inc................................................................................................8

10.2 Bond Evaluation................................................................................................................12

10.3 Retail Business...................................................................................................................13

Lesson 11: Hedging, Insuring, and Diversifying...........................................................................13

11.1 Hedging..............................................................................................................................13

11.2 Annuity..............................................................................................................................14

11.3 Hedging..............................................................................................................................15

2FNCE 300

Lesson 9: Valuation of Common Stocks

9.1 Dividend Discount Model

a) Po: D1/(k-g).

1. Multiplication Effect in both the sides of the equation by (k-g) factor getting: Po(k-g)=D1.

2. Dividing both sides with Po thereby getting: (k-g) = D1/Po.

3. Now, if we add growth factor (g) in both sides: k= D1/Po+g

b) The two ways in which money can be earned from investment in shares is particularly with

the help of dividend yield and capital gain yield and the same can be well described with the help

of equation created or developed above whereby;

D1: Refers to the Dividend yield that the investors would be creating.

Po+g: Refers to the Capital Gain Yield that the company would be making.

On the other hand, the total return in the equation designed refers to the dividend and capital gain

made by the investors which can be well shown with D1+(Po+g).

9.2 Valuation

a) Price Po:

D1: 20

K: 0.15

g: 0.12

Po: D1/(K-g)

Lesson 9: Valuation of Common Stocks

9.1 Dividend Discount Model

a) Po: D1/(k-g).

1. Multiplication Effect in both the sides of the equation by (k-g) factor getting: Po(k-g)=D1.

2. Dividing both sides with Po thereby getting: (k-g) = D1/Po.

3. Now, if we add growth factor (g) in both sides: k= D1/Po+g

b) The two ways in which money can be earned from investment in shares is particularly with

the help of dividend yield and capital gain yield and the same can be well described with the help

of equation created or developed above whereby;

D1: Refers to the Dividend yield that the investors would be creating.

Po+g: Refers to the Capital Gain Yield that the company would be making.

On the other hand, the total return in the equation designed refers to the dividend and capital gain

made by the investors which can be well shown with D1+(Po+g).

9.2 Valuation

a) Price Po:

D1: 20

K: 0.15

g: 0.12

Po: D1/(K-g)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FNCE 300

Po: 20/(0.15-0.12).

Po: 666.67

b) P5 can be well calculated with the help of back calculation as follows:

D6: 20

K: 0.15

g: retention rate*return on equity.

D5: D6/(1+g)

D5: 20/(1+0.12)

D5: 17.86

P5: (D6/(k-g))

P5: (20/(0.15-0.12))

P5: 666.67

c) i) The value of the share or price at Po can be well calculated from P5 as follows:

Po: P5/(1+k)^5

Po: 666.67/(1+0.15)^5

Po: 331.45

ii) The value of share or Price at P1 can be well calculated as follows:

P1: P5/(1+k)^4

Po: 20/(0.15-0.12).

Po: 666.67

b) P5 can be well calculated with the help of back calculation as follows:

D6: 20

K: 0.15

g: retention rate*return on equity.

D5: D6/(1+g)

D5: 20/(1+0.12)

D5: 17.86

P5: (D6/(k-g))

P5: (20/(0.15-0.12))

P5: 666.67

c) i) The value of the share or price at Po can be well calculated from P5 as follows:

Po: P5/(1+k)^5

Po: 666.67/(1+0.15)^5

Po: 331.45

ii) The value of share or Price at P1 can be well calculated as follows:

P1: P5/(1+k)^4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FNCE 300

P1: 666.67/(1+0.15)^4

P1: 381.17

iii) The value of share or Price at P2 can be well calculated as follows:

P2: P5/(1+k)^3

P2: 666.67/(1+0.15)^3

P2: 438.34

d) The relationship between P2 and P1 can be well derived because if no dividends are paid in

between two point of time period then the only factor that would be remaining will be the

discount factor.

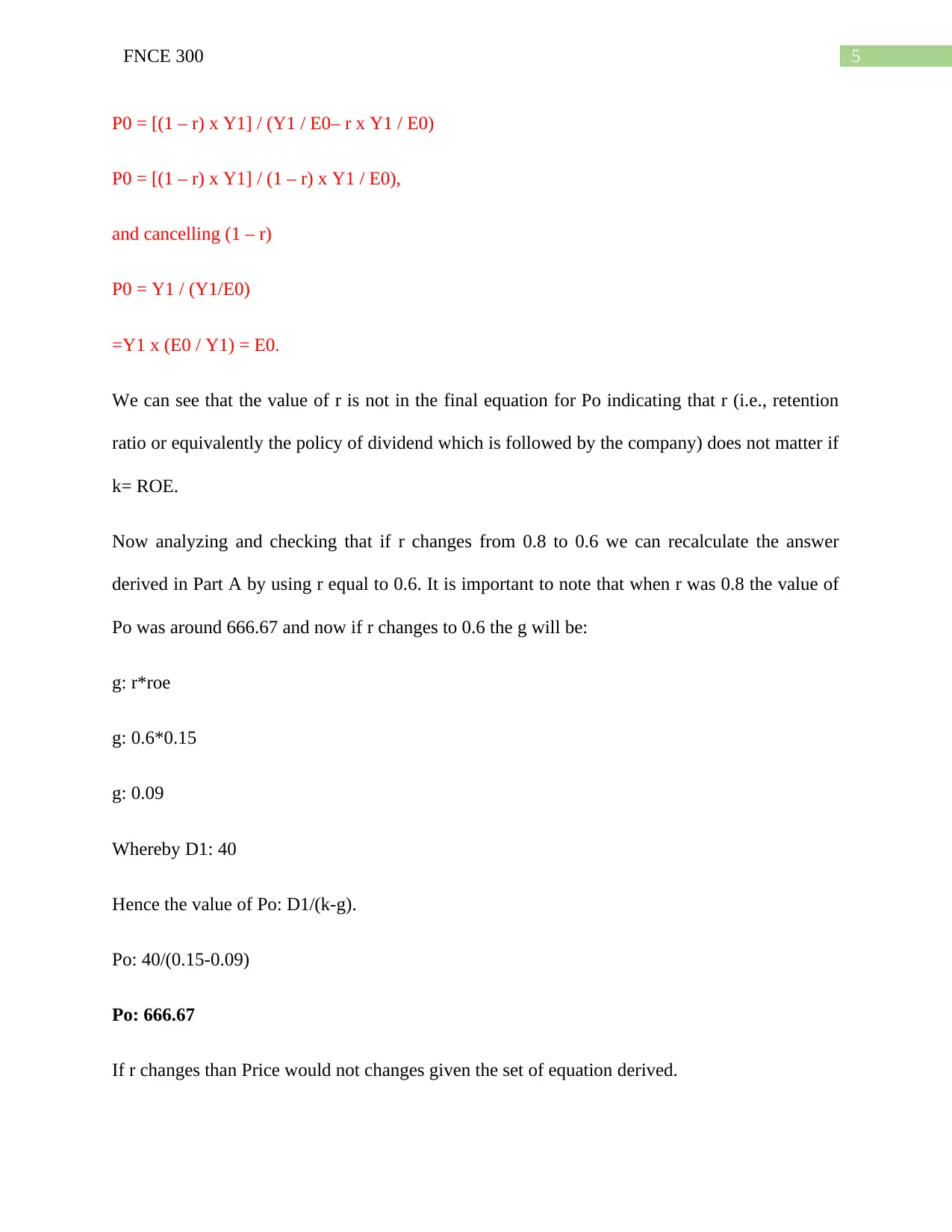

9.3 Equation Analysis

It is important to note that if K: ROE then Price level is not related to r. The same can be well

analysed as follows:

Growth rate: retention rate*return on equity

ROE: Yn/En-1.

Now Since r = (Yn-Dn)/Yn

then D1= (1 – r) x Y1 and

P0 = D1 / (k – g) . P0 = [(1 – r) x Y1] / (k – g) > P0 = [(1 – r) x Y1] / (k – g),

but, since k = ROE = Y1 / E0

P0 = [(1 – r) x Y1] / (ROE– r x ROE)

P1: 666.67/(1+0.15)^4

P1: 381.17

iii) The value of share or Price at P2 can be well calculated as follows:

P2: P5/(1+k)^3

P2: 666.67/(1+0.15)^3

P2: 438.34

d) The relationship between P2 and P1 can be well derived because if no dividends are paid in

between two point of time period then the only factor that would be remaining will be the

discount factor.

9.3 Equation Analysis

It is important to note that if K: ROE then Price level is not related to r. The same can be well

analysed as follows:

Growth rate: retention rate*return on equity

ROE: Yn/En-1.

Now Since r = (Yn-Dn)/Yn

then D1= (1 – r) x Y1 and

P0 = D1 / (k – g) . P0 = [(1 – r) x Y1] / (k – g) > P0 = [(1 – r) x Y1] / (k – g),

but, since k = ROE = Y1 / E0

P0 = [(1 – r) x Y1] / (ROE– r x ROE)

5FNCE 300

P0 = [(1 – r) x Y1] / (Y1 / E0– r x Y1 / E0)

P0 = [(1 – r) x Y1] / (1 – r) x Y1 / E0),

and cancelling (1 – r)

P0 = Y1 / (Y1/E0)

=Y1 x (E0 / Y1) = E0.

We can see that the value of r is not in the final equation for Po indicating that r (i.e., retention

ratio or equivalently the policy of dividend which is followed by the company) does not matter if

k= ROE.

Now analyzing and checking that if r changes from 0.8 to 0.6 we can recalculate the answer

derived in Part A by using r equal to 0.6. It is important to note that when r was 0.8 the value of

Po was around 666.67 and now if r changes to 0.6 the g will be:

g: r*roe

g: 0.6*0.15

g: 0.09

Whereby D1: 40

Hence the value of Po: D1/(k-g).

Po: 40/(0.15-0.09)

Po: 666.67

If r changes than Price would not changes given the set of equation derived.

P0 = [(1 – r) x Y1] / (Y1 / E0– r x Y1 / E0)

P0 = [(1 – r) x Y1] / (1 – r) x Y1 / E0),

and cancelling (1 – r)

P0 = Y1 / (Y1/E0)

=Y1 x (E0 / Y1) = E0.

We can see that the value of r is not in the final equation for Po indicating that r (i.e., retention

ratio or equivalently the policy of dividend which is followed by the company) does not matter if

k= ROE.

Now analyzing and checking that if r changes from 0.8 to 0.6 we can recalculate the answer

derived in Part A by using r equal to 0.6. It is important to note that when r was 0.8 the value of

Po was around 666.67 and now if r changes to 0.6 the g will be:

g: r*roe

g: 0.6*0.15

g: 0.09

Whereby D1: 40

Hence the value of Po: D1/(k-g).

Po: 40/(0.15-0.09)

Po: 666.67

If r changes than Price would not changes given the set of equation derived.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FNCE 300

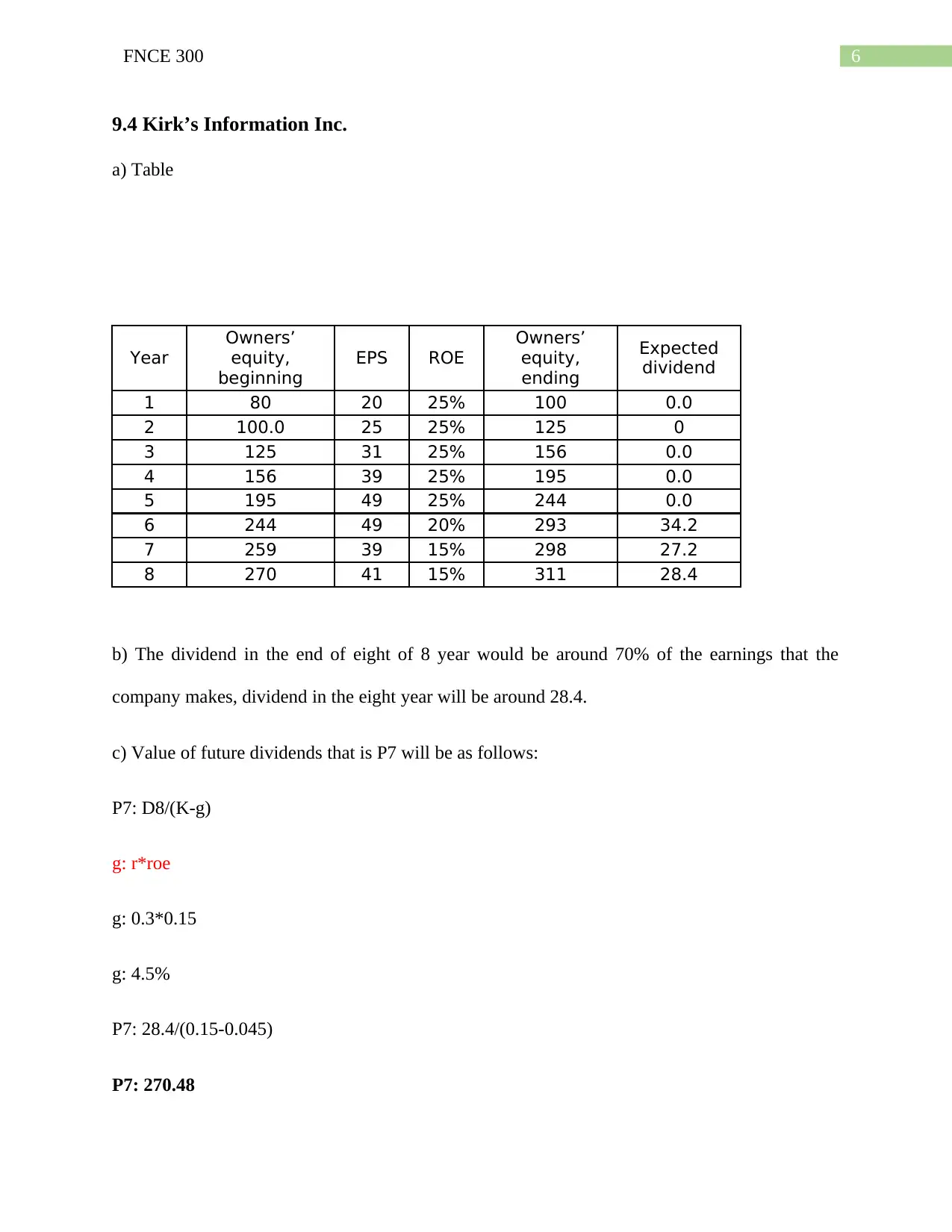

9.4 Kirk’s Information Inc.

a) Table

Year

Owners’

equity,

beginning

EPS ROE

Owners’

equity,

ending

Expected

dividend

1 80 20 25% 100 0.0

2 100.0 25 25% 125 0

3 125 31 25% 156 0.0

4 156 39 25% 195 0.0

5 195 49 25% 244 0.0

6 244 49 20% 293 34.2

7 259 39 15% 298 27.2

8 270 41 15% 311 28.4

b) The dividend in the end of eight of 8 year would be around 70% of the earnings that the

company makes, dividend in the eight year will be around 28.4.

c) Value of future dividends that is P7 will be as follows:

P7: D8/(K-g)

g: r*roe

g: 0.3*0.15

g: 4.5%

P7: 28.4/(0.15-0.045)

P7: 270.48

9.4 Kirk’s Information Inc.

a) Table

Year

Owners’

equity,

beginning

EPS ROE

Owners’

equity,

ending

Expected

dividend

1 80 20 25% 100 0.0

2 100.0 25 25% 125 0

3 125 31 25% 156 0.0

4 156 39 25% 195 0.0

5 195 49 25% 244 0.0

6 244 49 20% 293 34.2

7 259 39 15% 298 27.2

8 270 41 15% 311 28.4

b) The dividend in the end of eight of 8 year would be around 70% of the earnings that the

company makes, dividend in the eight year will be around 28.4.

c) Value of future dividends that is P7 will be as follows:

P7: D8/(K-g)

g: r*roe

g: 0.3*0.15

g: 4.5%

P7: 28.4/(0.15-0.045)

P7: 270.48

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FNCE 300

d) The present value of P7 for a single assessment at the beginning of Year 1:

PO: P7/(1+k)^7

Po: 270.48/(1+0.15)^7

Po: 101.68

e) The value of share at time of considering all possible future dividends can be well calculated

as follows:

Po: D6/(1+k)^6+D7/(1+K)^7+D8/(k-g)

Po: 34.2/(1.15)^6+27.2/(1.15)^7+28.4/(0.15-0.045).

Po: 126.66

9.5 Invest Co. Inc.

a) If dividends are paid out then the same does not changes the value of the stock. It means that

dividend policy followed by the company does not affect the share price of the company.

b) In order to determine value per share we need to find the value of the firm which is as follows:

Value of Firm: Value of Equipment-Cash Balance

Value of Firm: 900,000-100,000

Value of Firm: 800,000

Value Per Share: Value of Firm/Outstanding Shares

Value Per Share: 800,000/100,000

Value Per Share: 8

d) The present value of P7 for a single assessment at the beginning of Year 1:

PO: P7/(1+k)^7

Po: 270.48/(1+0.15)^7

Po: 101.68

e) The value of share at time of considering all possible future dividends can be well calculated

as follows:

Po: D6/(1+k)^6+D7/(1+K)^7+D8/(k-g)

Po: 34.2/(1.15)^6+27.2/(1.15)^7+28.4/(0.15-0.045).

Po: 126.66

9.5 Invest Co. Inc.

a) If dividends are paid out then the same does not changes the value of the stock. It means that

dividend policy followed by the company does not affect the share price of the company.

b) In order to determine value per share we need to find the value of the firm which is as follows:

Value of Firm: Value of Equipment-Cash Balance

Value of Firm: 900,000-100,000

Value of Firm: 800,000

Value Per Share: Value of Firm/Outstanding Shares

Value Per Share: 800,000/100,000

Value Per Share: 8

8FNCE 300

Now, if we choose to sell the share for $10 when the actual value of per share is $8 the wealth

would be increasing $2 on a per share basis.

c) If we don’t choose to participate in the buyback program then the wealth or value remains

unchanged.

d) Stock Split does not affect the value of the shares. The total number of shares will just

multiply from 100,000 to 200,000 and the value of shares will be half and the value will remain

unchanged.

e) If dividends are paid then the same does not affect the wealth of shareholders.

f) If the stated amount of purchase that the company is considering that is $100,000 for buying

equipment which will be then used for earning a return equal to the firms discount rate, then the

actual value of the firm would be increasing to $900,000 from $800,000 and the overall wealth

would also increase by $1.

Lesson 10: Principles of Risk Management

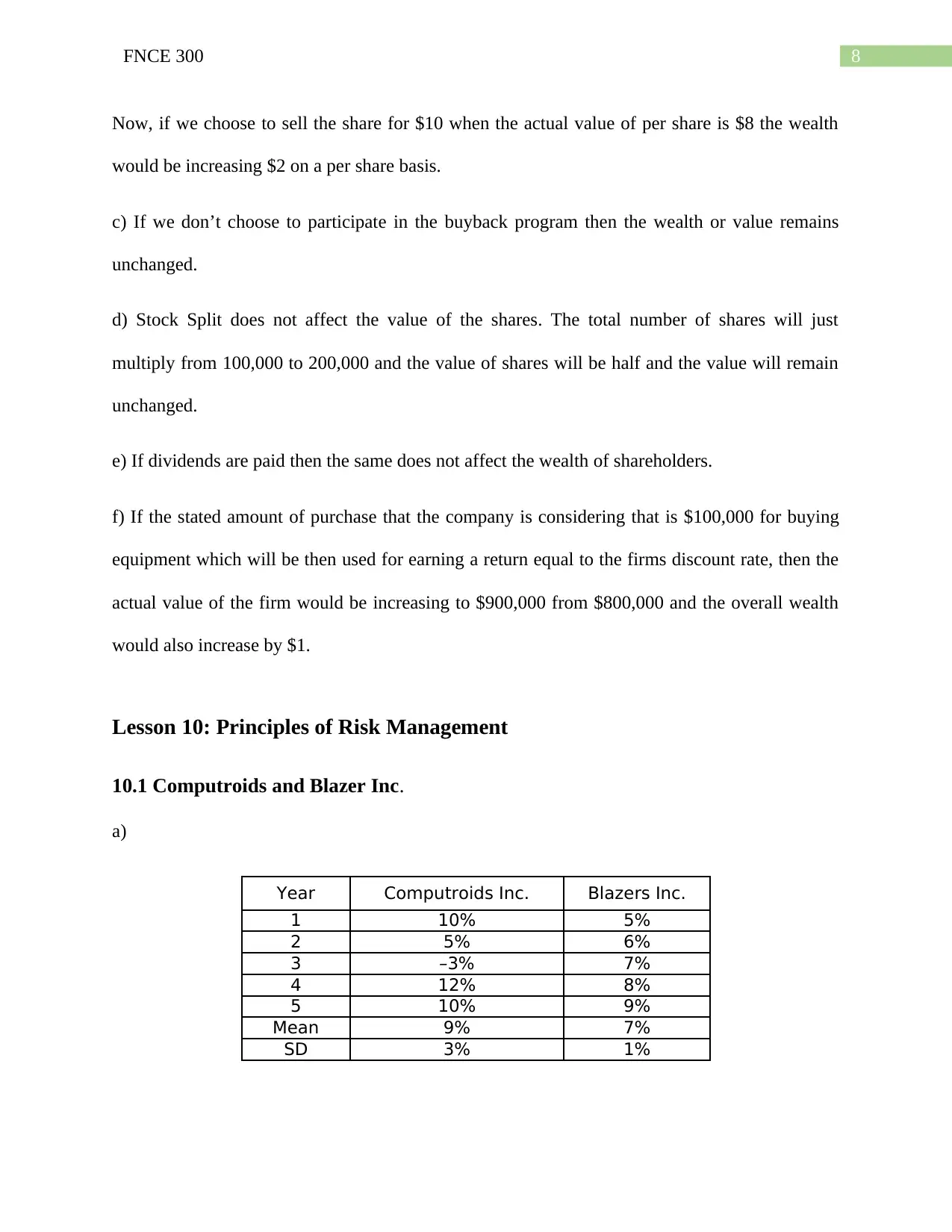

10.1 Computroids and Blazer Inc.

a)

Year Computroids Inc. Blazers Inc.

1 10% 5%

2 5% 6%

3 –3% 7%

4 12% 8%

5 10% 9%

Mean 9% 7%

SD 3% 1%

Now, if we choose to sell the share for $10 when the actual value of per share is $8 the wealth

would be increasing $2 on a per share basis.

c) If we don’t choose to participate in the buyback program then the wealth or value remains

unchanged.

d) Stock Split does not affect the value of the shares. The total number of shares will just

multiply from 100,000 to 200,000 and the value of shares will be half and the value will remain

unchanged.

e) If dividends are paid then the same does not affect the wealth of shareholders.

f) If the stated amount of purchase that the company is considering that is $100,000 for buying

equipment which will be then used for earning a return equal to the firms discount rate, then the

actual value of the firm would be increasing to $900,000 from $800,000 and the overall wealth

would also increase by $1.

Lesson 10: Principles of Risk Management

10.1 Computroids and Blazer Inc.

a)

Year Computroids Inc. Blazers Inc.

1 10% 5%

2 5% 6%

3 –3% 7%

4 12% 8%

5 10% 9%

Mean 9% 7%

SD 3% 1%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FNCE 300

b) In order to well calculate the 68% confidence interval, we would firstly calculate the top of

the examined confidence interval range with the help of adding one standard deviation with the

expected amount of return, and then accordingly calculate the bottom of the confidence interval

by subtracting one standard deviation from the expected return. For 95%, use two standard

deviations, and for 99%, use three.

Computeroids Company

In the case of 68% confidence intervals the z value is around 1. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 9%

Standard Deviation: 3%

Z Value: 1

Upper Value: 9%+(3%*1)

Upper Value: 12%

Lower Value: 9%-(3%*1)

Lower Value: 6%.

In the case of 95% confidence intervals the z value is around 2. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 9%

Standard Deviation: 3%

Z Value: 2

b) In order to well calculate the 68% confidence interval, we would firstly calculate the top of

the examined confidence interval range with the help of adding one standard deviation with the

expected amount of return, and then accordingly calculate the bottom of the confidence interval

by subtracting one standard deviation from the expected return. For 95%, use two standard

deviations, and for 99%, use three.

Computeroids Company

In the case of 68% confidence intervals the z value is around 1. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 9%

Standard Deviation: 3%

Z Value: 1

Upper Value: 9%+(3%*1)

Upper Value: 12%

Lower Value: 9%-(3%*1)

Lower Value: 6%.

In the case of 95% confidence intervals the z value is around 2. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 9%

Standard Deviation: 3%

Z Value: 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FNCE 300

Upper Value: 9%+(3%*2)

Upper Value: 15%

Lower Value: 9%-(3%*2)

Lower Value: 3%.

In the case of 99% confidence intervals the z value is around 3. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 9%

Standard Deviation: 3%

Z Value: 3

Upper Value: 9%+(3%*3)

Upper Value: 18%

Lower Value: 9%-(3%*3)

Lower Value: 0%.

Blazers Company

In the case of 68% confidence intervals the z value is around 1. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 7%

Standard Deviation: 1%

Z Value: 1

Upper Value: 9%+(3%*2)

Upper Value: 15%

Lower Value: 9%-(3%*2)

Lower Value: 3%.

In the case of 99% confidence intervals the z value is around 3. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 9%

Standard Deviation: 3%

Z Value: 3

Upper Value: 9%+(3%*3)

Upper Value: 18%

Lower Value: 9%-(3%*3)

Lower Value: 0%.

Blazers Company

In the case of 68% confidence intervals the z value is around 1. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 7%

Standard Deviation: 1%

Z Value: 1

11FNCE 300

Upper Value: 7%+(1%*1)

Upper Value: 8%

Lower Value: 7%-(1%*1)

Lower Value: 6%.

In the case of 95% confidence intervals the z value is around 2. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 7%

Standard Deviation: 1%

Z Value: 2

Upper Value: 7%+(1%*2)

Upper Value: 9%

Lower Value: 7%-(1%*2)

Lower Value: 5%.

In the case of 99% confidence intervals the z value is around 3. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 7%

Standard Deviation: 1%

Z Value: 3

Upper Value: 7%+(1%*3)

Upper Value: 7%+(1%*1)

Upper Value: 8%

Lower Value: 7%-(1%*1)

Lower Value: 6%.

In the case of 95% confidence intervals the z value is around 2. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 7%

Standard Deviation: 1%

Z Value: 2

Upper Value: 7%+(1%*2)

Upper Value: 9%

Lower Value: 7%-(1%*2)

Lower Value: 5%.

In the case of 99% confidence intervals the z value is around 3. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 7%

Standard Deviation: 1%

Z Value: 3

Upper Value: 7%+(1%*3)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.