FNCE5014 - Corporate Finance for Managers Assignment - Trimester 3

VerifiedAdded on 2022/10/19

|10

|1505

|370

Homework Assignment

AI Summary

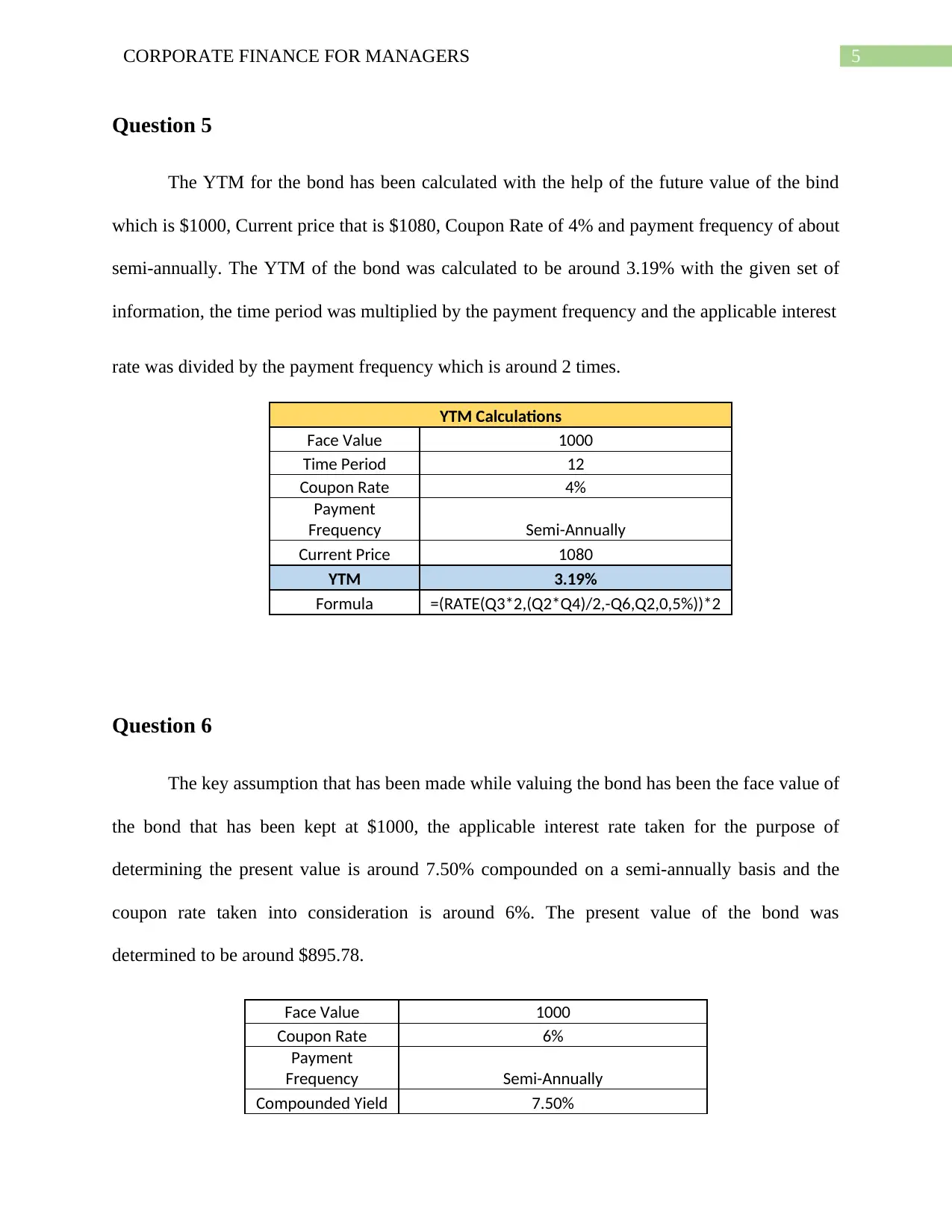

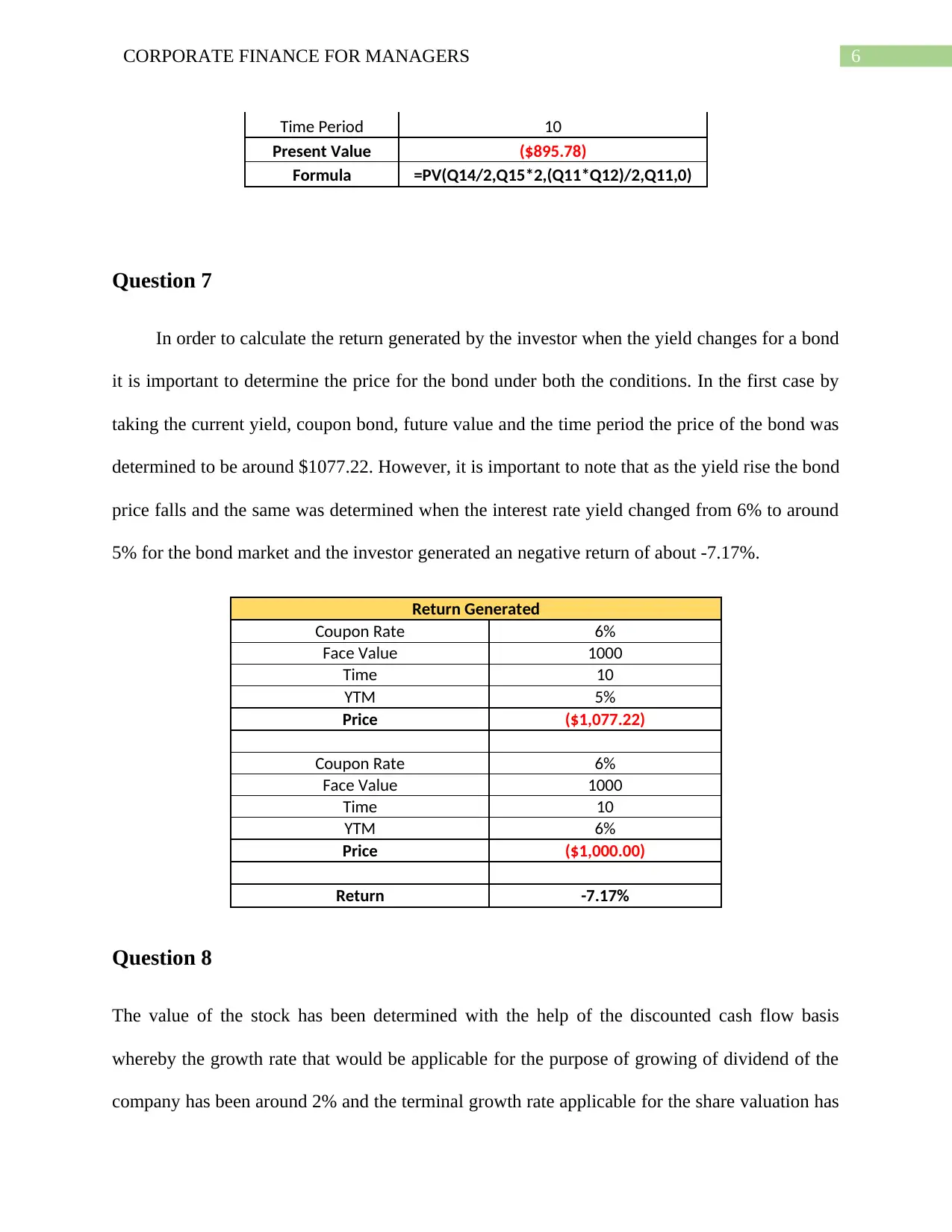

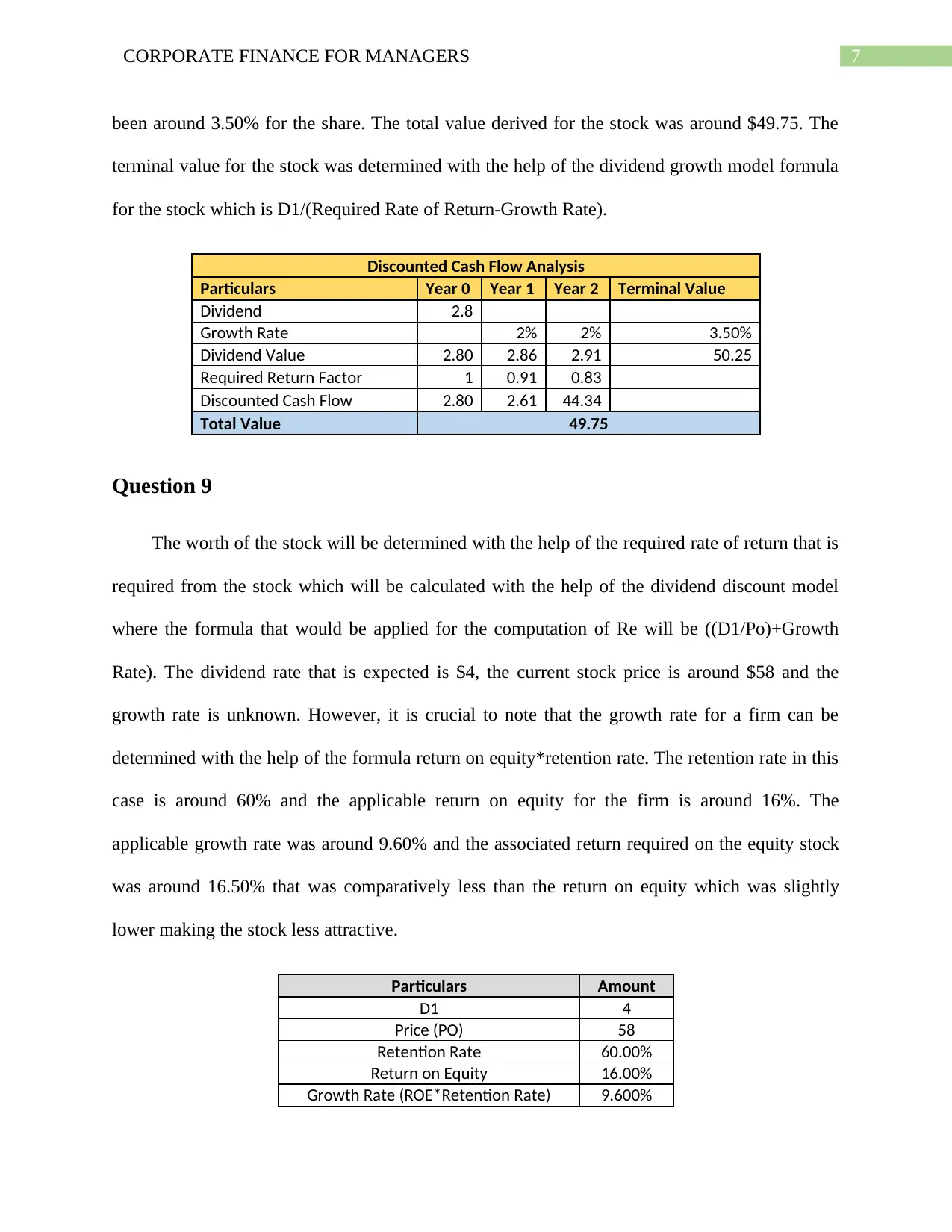

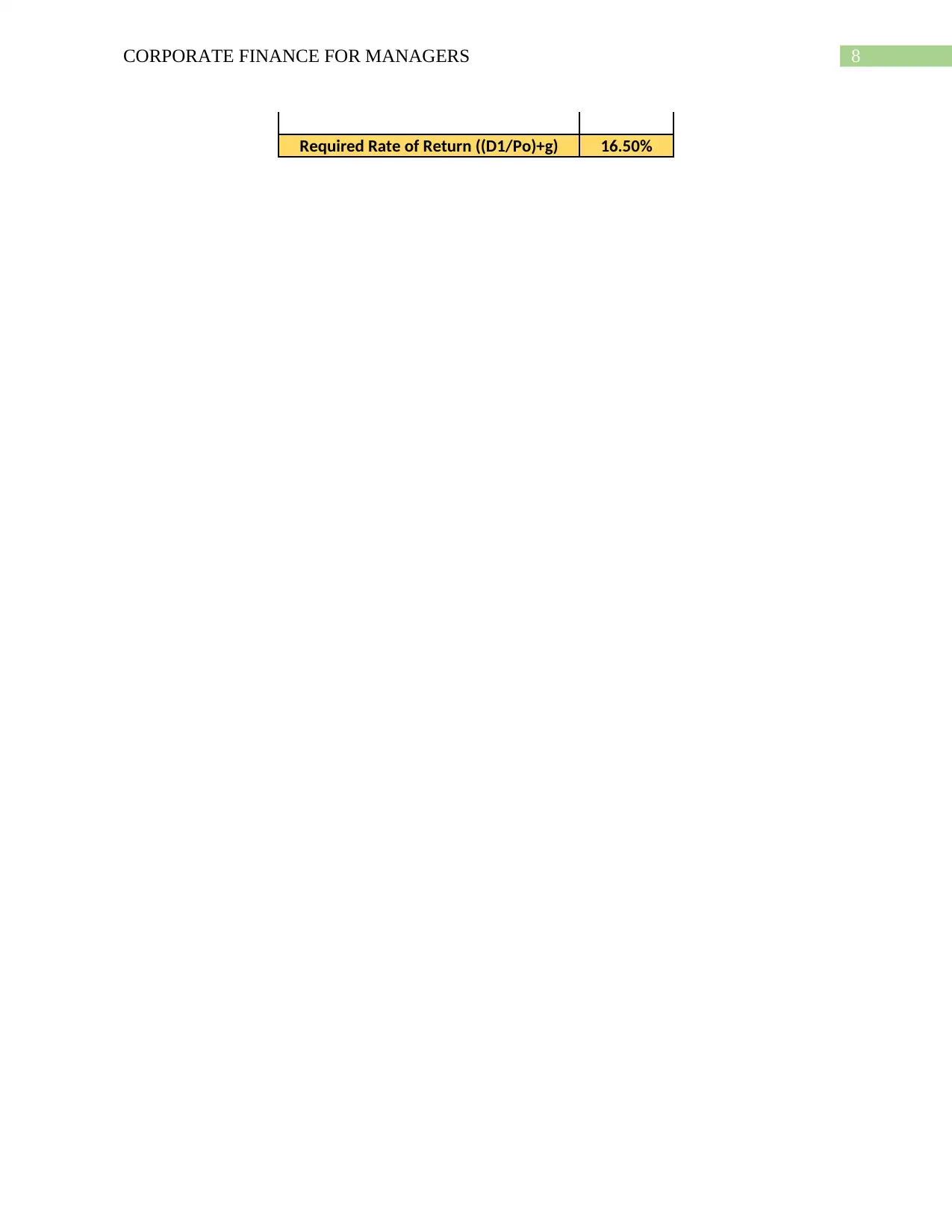

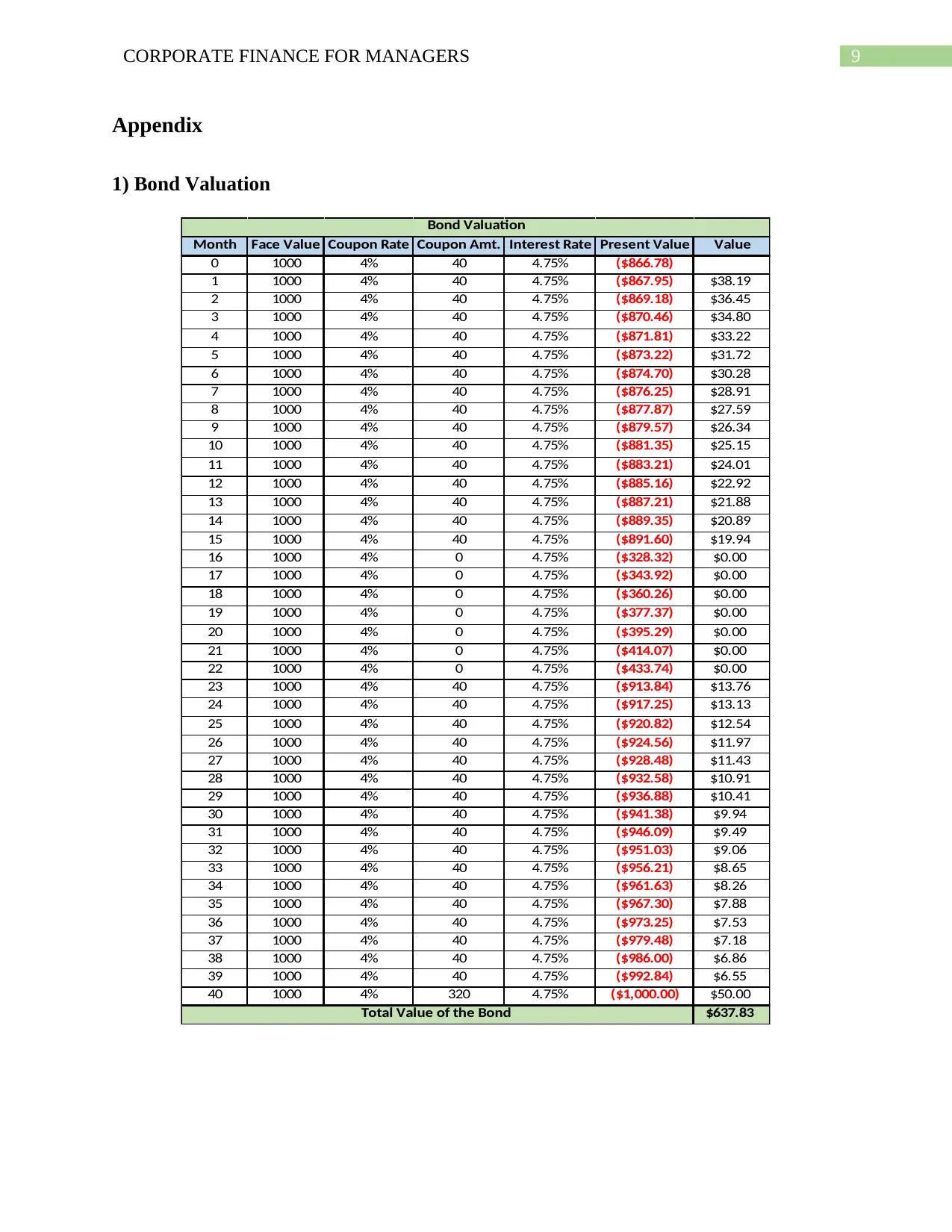

This assignment solution addresses key concepts in corporate finance, including the time value of money, bond valuation, and stock valuation. The solution begins with calculating future values under different interest rates and compounding periods. It then proceeds to present value calculations for investment options. The assignment further explores mortgage calculations, bond pricing, and yield to maturity (YTM) computations. The solution also examines the impact of yield changes on bond returns. Finally, it delves into stock valuation using discounted cash flow analysis and the dividend discount model, calculating the required rate of return and assessing the attractiveness of a stock investment. All calculations are provided with relevant formulas and values.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.