FNS40217 Certificate IV: Accounting & Budgeting Assessment

VerifiedAdded on 2023/05/31

|46

|10474

|359

Homework Assignment

AI Summary

This assignment solution covers key areas of accounting and budgeting, including preparing an adjusted trial balance, income statement, balance sheet, and statement of cash flows. It also includes financial statement analysis using ratios such as gross profit rate, net profit rate, current ratio, liquid ratio, inventory turnover rate, and average collection period. The analysis provides insights into a company's profitability, business activity, and liquidity, along with recommendations for improvement.

T-1.8.1

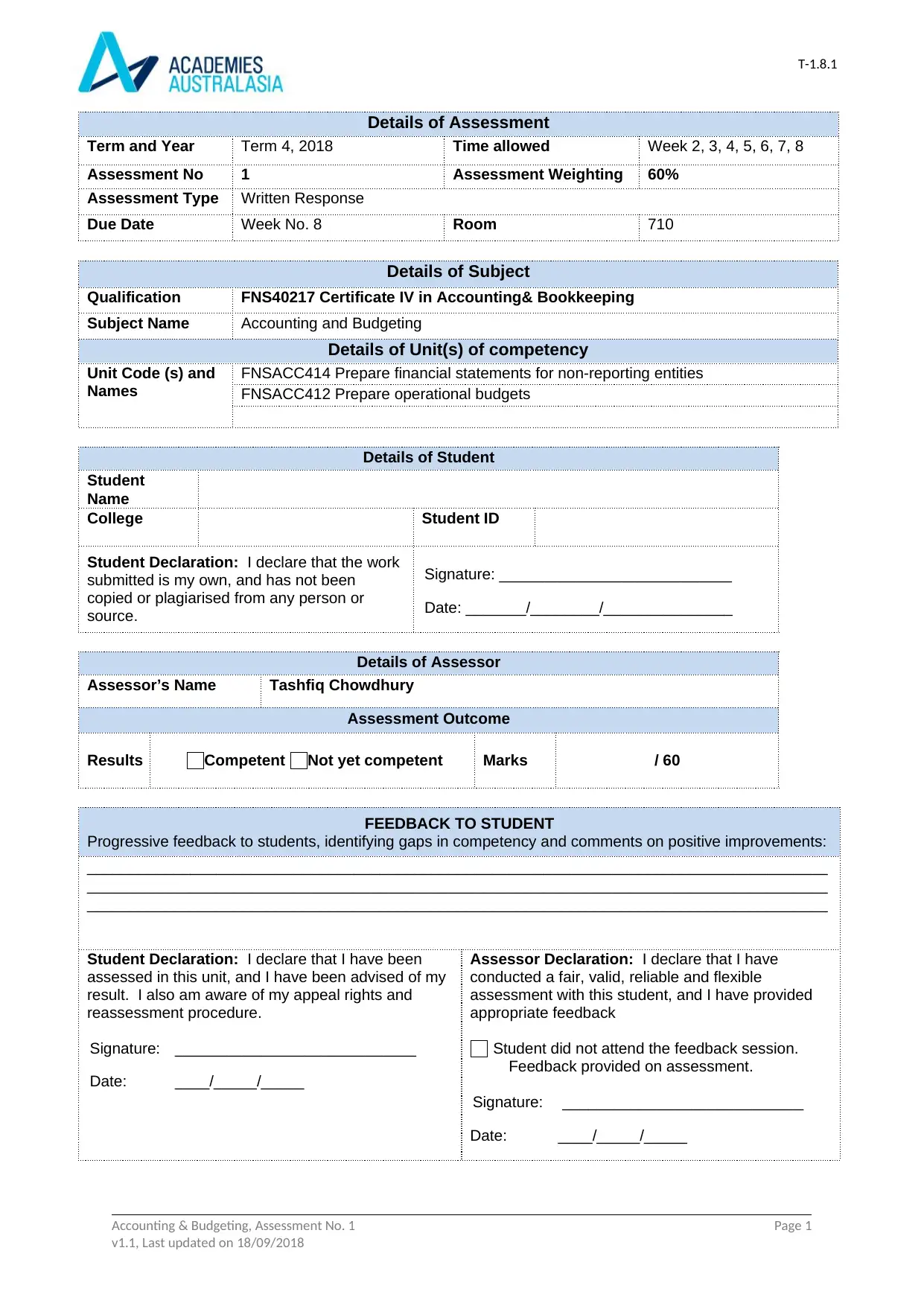

Details of Assessment

Term and Year Term 4, 2018 Time allowed Week 2, 3, 4, 5, 6, 7, 8

Assessment No 1 Assessment Weighting 60%

Assessment Type Written Response

Due Date Week No. 8 Room 710

Details of Subject

Qualification FNS40217 Certificate IV in Accounting& Bookkeeping

Subject Name Accounting and Budgeting

Details of Unit(s) of competency

Unit Code (s) and

Names

FNSACC414 Prepare financial statements for non-reporting entities

FNSACC412 Prepare operational budgets

Details of Student

Student

Name

College Student ID

Student Declaration: I declare that the work

submitted is my own, and has not been

copied or plagiarised from any person or

source.

Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name Tashfiq Chowdhury

Assessment Outcome

Results Competent Not yet competent Marks / 60

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

Student Declaration: I declare that I have been

assessed in this unit, and I have been advised of my

result. I also am aware of my appeal rights and

reassessment procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have provided

appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/_____

Accounting & Budgeting, Assessment No. 1 Page 1

v1.1, Last updated on 18/09/2018

Details of Assessment

Term and Year Term 4, 2018 Time allowed Week 2, 3, 4, 5, 6, 7, 8

Assessment No 1 Assessment Weighting 60%

Assessment Type Written Response

Due Date Week No. 8 Room 710

Details of Subject

Qualification FNS40217 Certificate IV in Accounting& Bookkeeping

Subject Name Accounting and Budgeting

Details of Unit(s) of competency

Unit Code (s) and

Names

FNSACC414 Prepare financial statements for non-reporting entities

FNSACC412 Prepare operational budgets

Details of Student

Student

Name

College Student ID

Student Declaration: I declare that the work

submitted is my own, and has not been

copied or plagiarised from any person or

source.

Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name Tashfiq Chowdhury

Assessment Outcome

Results Competent Not yet competent Marks / 60

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

Student Declaration: I declare that I have been

assessed in this unit, and I have been advised of my

result. I also am aware of my appeal rights and

reassessment procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have provided

appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/_____

Accounting & Budgeting, Assessment No. 1 Page 1

v1.1, Last updated on 18/09/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

Assessment/evidence gathering conditions

Each assessment component is recorded as either Competent (C) or Not Yet Competent (NYC). A student can only

achieve competence when all assessment components listed under “Purpose of the assessment” section are recorded

as competent. Your trainer will give you feedback after the completion of each assessment. A student who is assessed

as NYC (Not Yet Competent) is eligible for re-assessment.

Resources required for this Assessment

All documents must be created in Microsoft Word

Upon completion, submit the assessment printed copy to your trainer along with assessment

coversheet.

Refer to the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will be

provided with feedback on your work within two weeks of the assessment due date. All other feedback will be

provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspects of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment for more information (Student Handbook).

Assessment Instructions:

This is an individual task with written response. You need to prepare answers from the

materials available at elearnings or you may use any web materials.

To be assessed as competent for this unit, the student must complete all of the assessment

tasks satisfactorily.

All questions must be answered correctly in order for a student to be assessed as having

completed the task satisfactorily.

Please read through this assessment thoroughly before beginning any tasks. Ask your trainer

for clarification if you have any questions at all.

Answers must be word processed and you need to submit the hard copy of assessment to

your trainer.

Keep a copy of all of your work, as the work submitted to your assessor will not be returned to

you.

Task 1 - Accounting (2.5 Marks)

Accounting & Budgeting, Assessment No. 1 Page 2

v1.1, Last updated on 18/09/2018

Assessment/evidence gathering conditions

Each assessment component is recorded as either Competent (C) or Not Yet Competent (NYC). A student can only

achieve competence when all assessment components listed under “Purpose of the assessment” section are recorded

as competent. Your trainer will give you feedback after the completion of each assessment. A student who is assessed

as NYC (Not Yet Competent) is eligible for re-assessment.

Resources required for this Assessment

All documents must be created in Microsoft Word

Upon completion, submit the assessment printed copy to your trainer along with assessment

coversheet.

Refer to the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will be

provided with feedback on your work within two weeks of the assessment due date. All other feedback will be

provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspects of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment for more information (Student Handbook).

Assessment Instructions:

This is an individual task with written response. You need to prepare answers from the

materials available at elearnings or you may use any web materials.

To be assessed as competent for this unit, the student must complete all of the assessment

tasks satisfactorily.

All questions must be answered correctly in order for a student to be assessed as having

completed the task satisfactorily.

Please read through this assessment thoroughly before beginning any tasks. Ask your trainer

for clarification if you have any questions at all.

Answers must be word processed and you need to submit the hard copy of assessment to

your trainer.

Keep a copy of all of your work, as the work submitted to your assessor will not be returned to

you.

Task 1 - Accounting (2.5 Marks)

Accounting & Budgeting, Assessment No. 1 Page 2

v1.1, Last updated on 18/09/2018

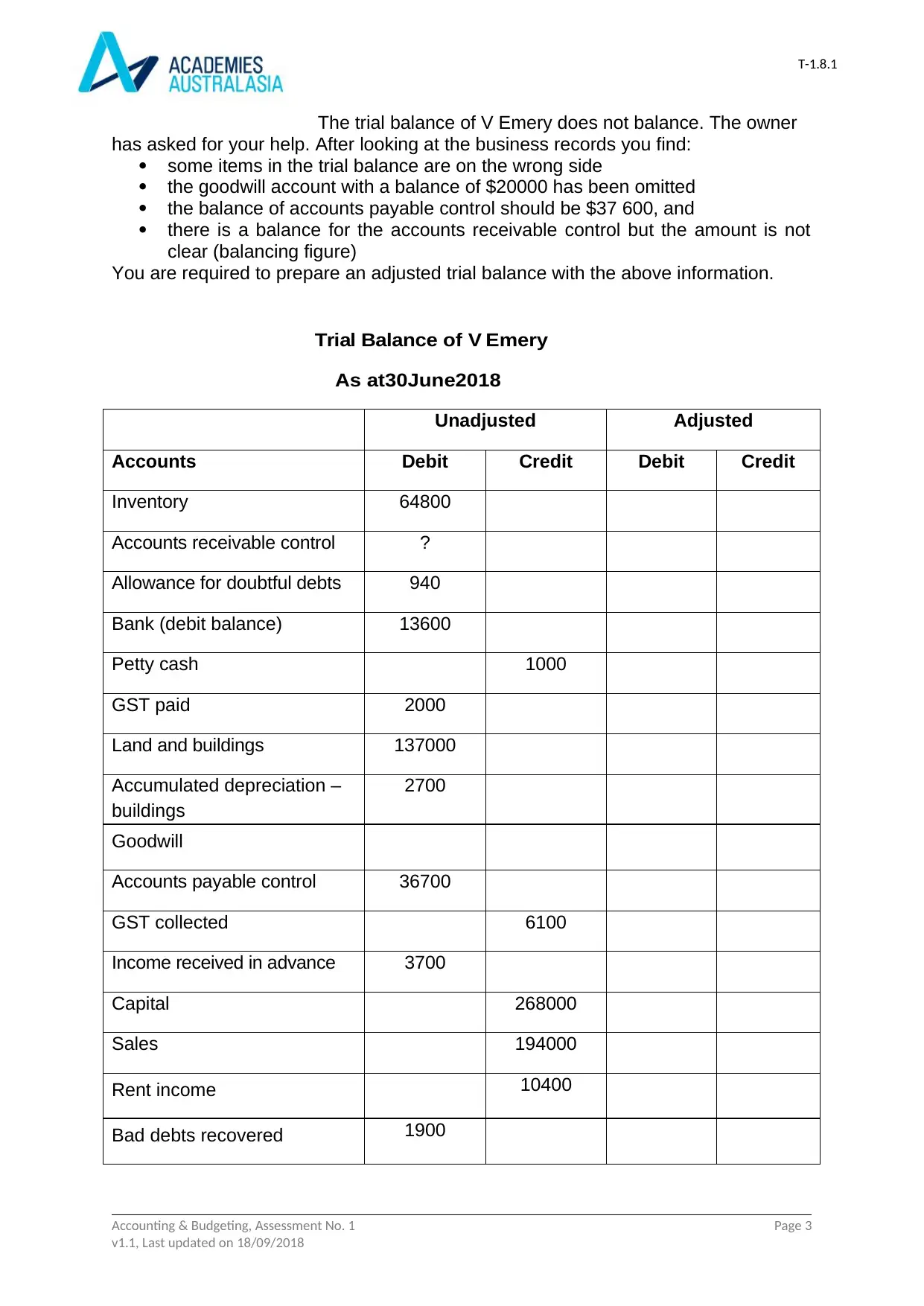

T-1.8.1

The trial balance of V Emery does not balance. The owner

has asked for your help. After looking at the business records you find:

some items in the trial balance are on the wrong side

the goodwill account with a balance of $20000 has been omitted

the balance of accounts payable control should be $37 600, and

there is a balance for the accounts receivable control but the amount is not

clear (balancing figure)

You are required to prepare an adjusted trial balance with the above information.

Trial Balance of V Emery

As at30June2018

Unadjusted Adjusted

Accounts Debit Credit Debit Credit

Inventory 64800

Accounts receivable control ?

Allowance for doubtful debts 940

Bank (debit balance) 13600

Petty cash 1000

GST paid 2000

Land and buildings 137000

Accumulated depreciation –

buildings

2700

Goodwill

Accounts payable control 36700

GST collected 6100

Income received in advance 3700

Capital 268000

Sales 194000

Rent income 10400

Bad debts recovered 1900

Accounting & Budgeting, Assessment No. 1 Page 3

v1.1, Last updated on 18/09/2018

The trial balance of V Emery does not balance. The owner

has asked for your help. After looking at the business records you find:

some items in the trial balance are on the wrong side

the goodwill account with a balance of $20000 has been omitted

the balance of accounts payable control should be $37 600, and

there is a balance for the accounts receivable control but the amount is not

clear (balancing figure)

You are required to prepare an adjusted trial balance with the above information.

Trial Balance of V Emery

As at30June2018

Unadjusted Adjusted

Accounts Debit Credit Debit Credit

Inventory 64800

Accounts receivable control ?

Allowance for doubtful debts 940

Bank (debit balance) 13600

Petty cash 1000

GST paid 2000

Land and buildings 137000

Accumulated depreciation –

buildings

2700

Goodwill

Accounts payable control 36700

GST collected 6100

Income received in advance 3700

Capital 268000

Sales 194000

Rent income 10400

Bad debts recovered 1900

Accounting & Budgeting, Assessment No. 1 Page 3

v1.1, Last updated on 18/09/2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

T-1.8.1

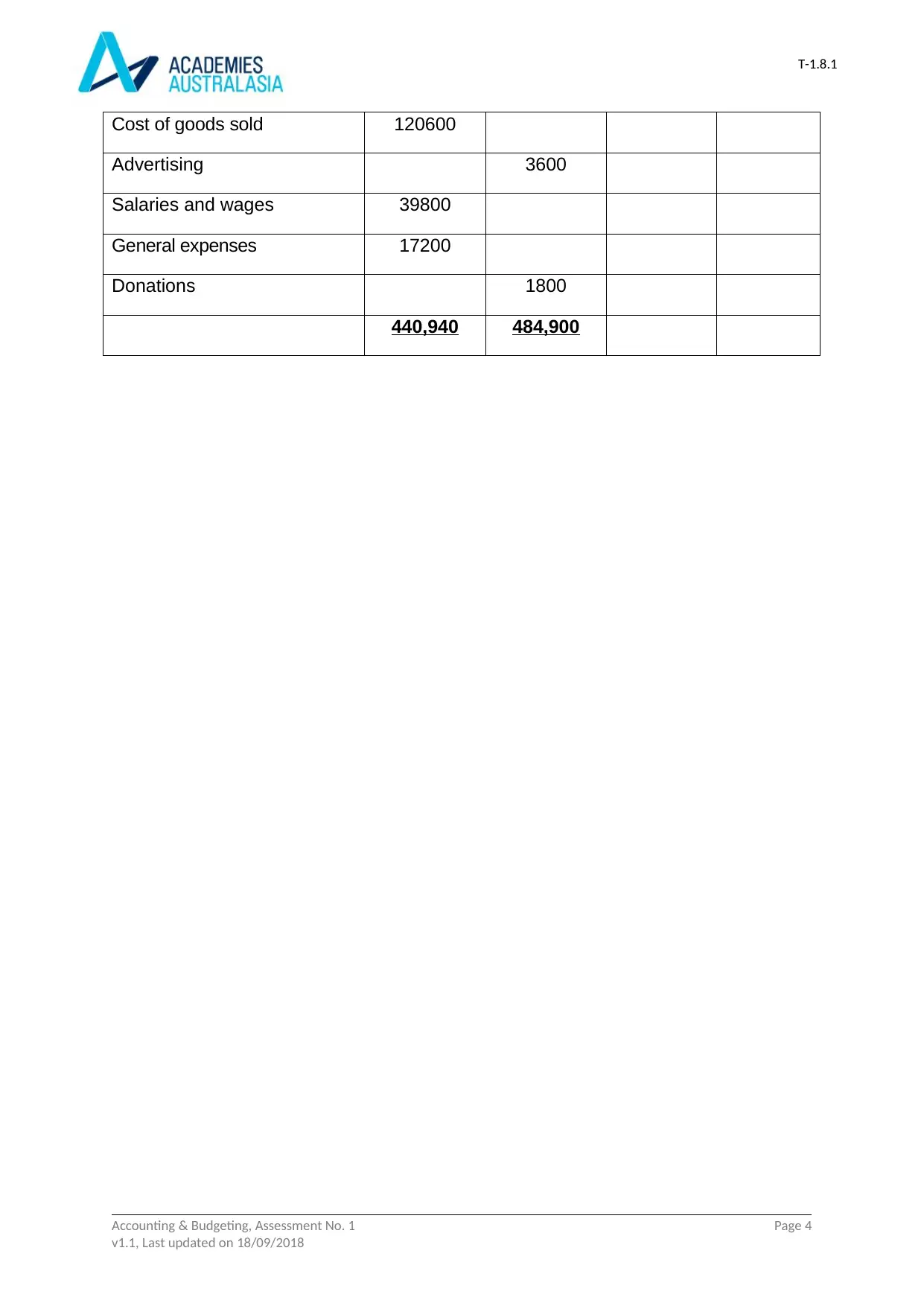

Cost of goods sold 120600

Advertising 3600

Salaries and wages 39800

General expenses 17200

Donations 1800

440,940 484,900

Accounting & Budgeting, Assessment No. 1 Page 4

v1.1, Last updated on 18/09/2018

Cost of goods sold 120600

Advertising 3600

Salaries and wages 39800

General expenses 17200

Donations 1800

440,940 484,900

Accounting & Budgeting, Assessment No. 1 Page 4

v1.1, Last updated on 18/09/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

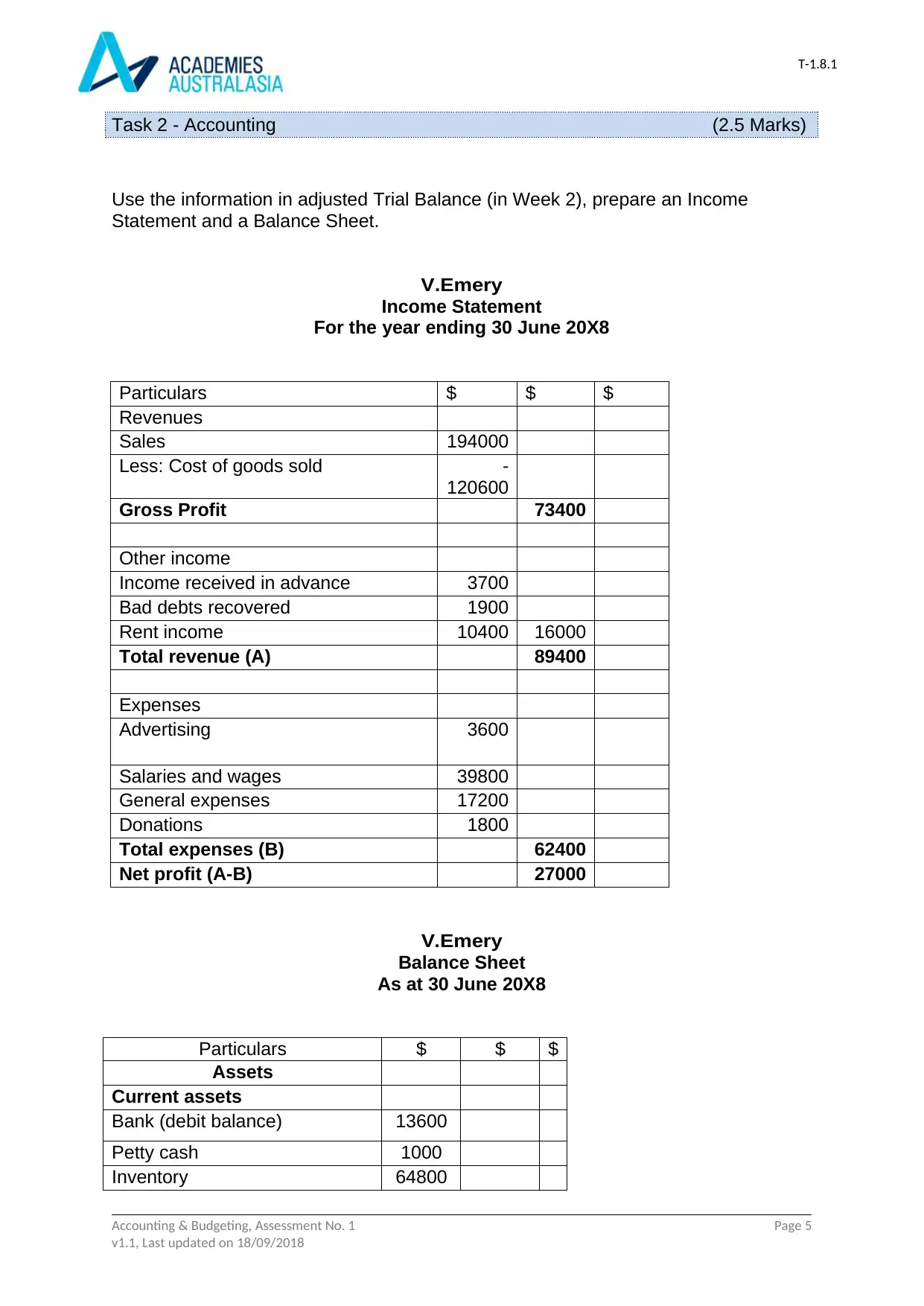

Task 2 - Accounting (2.5 Marks)

Use the information in adjusted Trial Balance (in Week 2), prepare an Income

Statement and a Balance Sheet.

V.Emery

Income Statement

For the year ending 30 June 20X8

Particulars $ $ $

Revenues

Sales 194000

Less: Cost of goods sold -

120600

Gross Profit 73400

Other income

Income received in advance 3700

Bad debts recovered 1900

Rent income 10400 16000

Total revenue (A) 89400

Expenses

Advertising 3600

Salaries and wages 39800

General expenses 17200

Donations 1800

Total expenses (B) 62400

Net profit (A-B) 27000

V.Emery

Balance Sheet

As at 30 June 20X8

Particulars $ $ $

Assets

Current assets

Bank (debit balance) 13600

Petty cash 1000

Inventory 64800

Accounting & Budgeting, Assessment No. 1 Page 5

v1.1, Last updated on 18/09/2018

Task 2 - Accounting (2.5 Marks)

Use the information in adjusted Trial Balance (in Week 2), prepare an Income

Statement and a Balance Sheet.

V.Emery

Income Statement

For the year ending 30 June 20X8

Particulars $ $ $

Revenues

Sales 194000

Less: Cost of goods sold -

120600

Gross Profit 73400

Other income

Income received in advance 3700

Bad debts recovered 1900

Rent income 10400 16000

Total revenue (A) 89400

Expenses

Advertising 3600

Salaries and wages 39800

General expenses 17200

Donations 1800

Total expenses (B) 62400

Net profit (A-B) 27000

V.Emery

Balance Sheet

As at 30 June 20X8

Particulars $ $ $

Assets

Current assets

Bank (debit balance) 13600

Petty cash 1000

Inventory 64800

Accounting & Budgeting, Assessment No. 1 Page 5

v1.1, Last updated on 18/09/2018

T-1.8.1

GST paid 2000

Goodwill 20000

Accounts receivable control 103940

20534

0

Non current assets

Land and buildings 137000

Less: accumulated depreciation -2700 13430

0

Total assets 33964

0

Liabilities and equities

Liabilities

Current liabilities

Accounts payable control 37600

GST collected 6100

Allowance for doubtful debts 940

Total liabilities 44640

Equity

Capital 268000

Net income 27000

Total equity 295000

Total liabilities and equity 339640

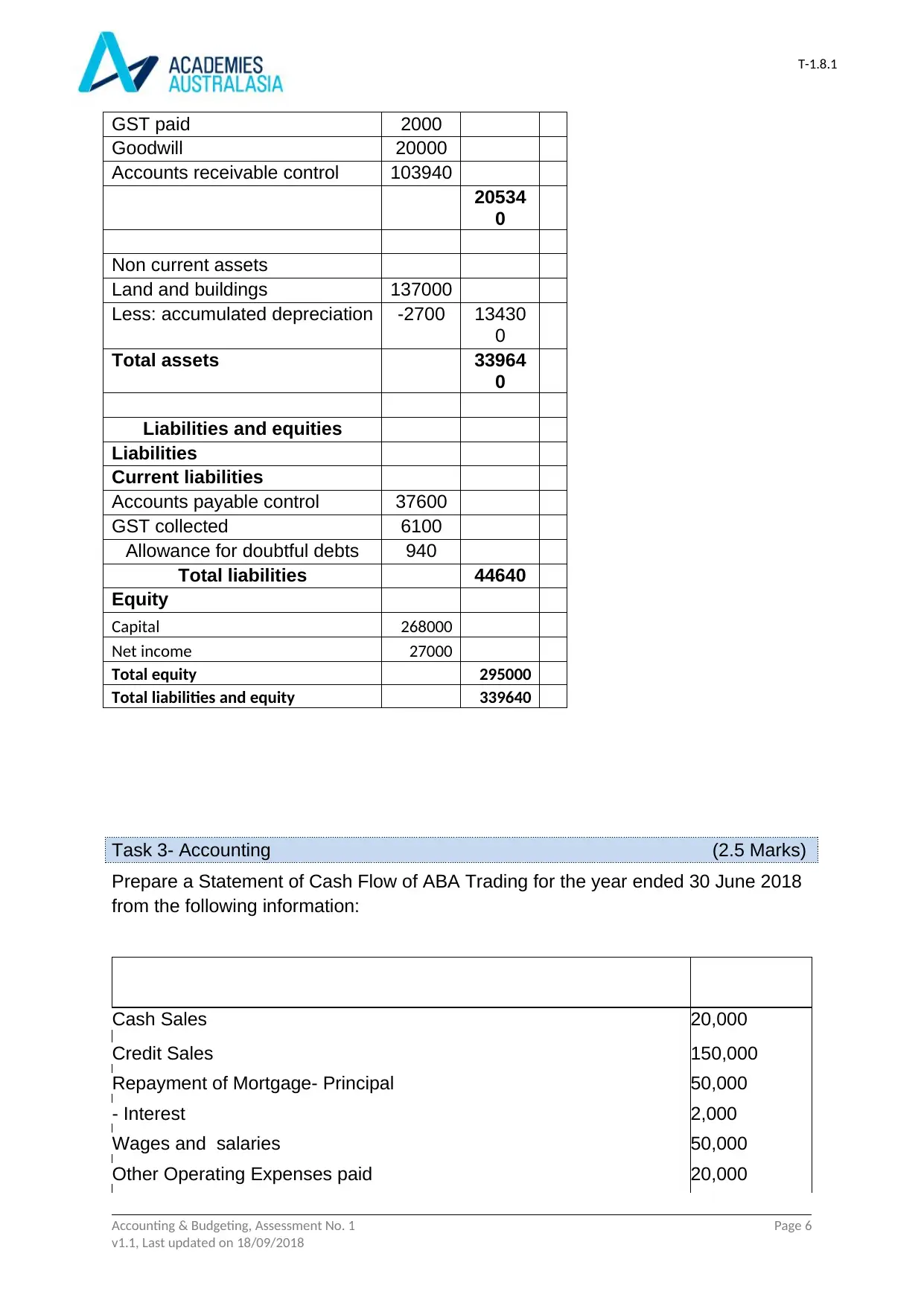

Task 3- Accounting (2.5 Marks)

Prepare a Statement of Cash Flow of ABA Trading for the year ended 30 June 2018

from the following information:

Cash Sales 20,000

Credit Sales 150,000

Repayment of Mortgage- Principal 50,000

- Interest 2,000

Wages and salaries 50,000

Other Operating Expenses paid 20,000

Accounting & Budgeting, Assessment No. 1 Page 6

v1.1, Last updated on 18/09/2018

GST paid 2000

Goodwill 20000

Accounts receivable control 103940

20534

0

Non current assets

Land and buildings 137000

Less: accumulated depreciation -2700 13430

0

Total assets 33964

0

Liabilities and equities

Liabilities

Current liabilities

Accounts payable control 37600

GST collected 6100

Allowance for doubtful debts 940

Total liabilities 44640

Equity

Capital 268000

Net income 27000

Total equity 295000

Total liabilities and equity 339640

Task 3- Accounting (2.5 Marks)

Prepare a Statement of Cash Flow of ABA Trading for the year ended 30 June 2018

from the following information:

Cash Sales 20,000

Credit Sales 150,000

Repayment of Mortgage- Principal 50,000

- Interest 2,000

Wages and salaries 50,000

Other Operating Expenses paid 20,000

Accounting & Budgeting, Assessment No. 1 Page 6

v1.1, Last updated on 18/09/2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

T-1.8.1

Payments to Accounts Payable 30,000

Discount Received 1,000

Depreciation expense 5,000

Receipts from Accounts Receivable 160,000

Dividends received on share investments 500

Proceeds from sale of Office Equipment 2,000

New Capital introduced by the owner 40,000

Bad Debts written off 3,000

Drawings by the owner 20,000

Purchase of Office Equipment 5,500

Cash at Bank 1/7/2017 5,000

Cash at Bank 30/6/2018 ?

Solution:

ABA Trading

Statement of cash flows

For the year ending 30 June 2018

Particulars $ $ $

Cash flow from operating

activities

Cash sales 20,000

Receipts from Accounts

Receivable

160,000

Payments to Accounts Payable 30,000

Wages and salaries 50,000

Other Operating Expenses paid 20,000

Cash generated from operations 80,000

Interest paid 2,000

Net cash flow from operations 78,000

Cash flow from investing

activities

Proceeds from sale of Office

Equipment

2,000

Dividends received on share

investments

500

Purchase of Office Equipment 5,500

Accounting & Budgeting, Assessment No. 1 Page 7

v1.1, Last updated on 18/09/2018

Payments to Accounts Payable 30,000

Discount Received 1,000

Depreciation expense 5,000

Receipts from Accounts Receivable 160,000

Dividends received on share investments 500

Proceeds from sale of Office Equipment 2,000

New Capital introduced by the owner 40,000

Bad Debts written off 3,000

Drawings by the owner 20,000

Purchase of Office Equipment 5,500

Cash at Bank 1/7/2017 5,000

Cash at Bank 30/6/2018 ?

Solution:

ABA Trading

Statement of cash flows

For the year ending 30 June 2018

Particulars $ $ $

Cash flow from operating

activities

Cash sales 20,000

Receipts from Accounts

Receivable

160,000

Payments to Accounts Payable 30,000

Wages and salaries 50,000

Other Operating Expenses paid 20,000

Cash generated from operations 80,000

Interest paid 2,000

Net cash flow from operations 78,000

Cash flow from investing

activities

Proceeds from sale of Office

Equipment

2,000

Dividends received on share

investments

500

Purchase of Office Equipment 5,500

Accounting & Budgeting, Assessment No. 1 Page 7

v1.1, Last updated on 18/09/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

Cash used in investing

activities

-3,000

Cash flows from financing

activities

New Capital introduced by the

owner

40,000

Repayment of Mortgage-

Principal

50,000

Drawings by the owner 20,000

Cash used in financing

activities -30,000

Net increase/decrease in cash 45,000

Add: Opening balance 5,000

Closing balance 50,000

Task 4 - Accounting (5 Marks)

Financial Statement Analysis:

You are given the following financial statements for Huffington Post Trading:

Income Statement for the year ended 30June 2018

$ $ $

Sales (all credit) 480,000

Less, Cost of Goods Sold

inventories (1/7/2017)Purchases 54,500

Goods available for sale 331,800 386,300

Less, Inventories 30/6/2018 69,500 316,800

Gross Profit 163,200

Other Income 5,000

Total Operating Income 168,200

Less, Operating Expenses 110,600

Net Profit 57,600

Balance Sheet as at 30 June 2018

$ $ $

Current Assets

Accounts Receivable 78,000

Less, Allowance for Doubtful Debts 3,000 75,000

Inventories 69,500

Prepaid Expenses 500

Accrued revenue 1,000 146,000

Non-Current Assets

Accounting & Budgeting, Assessment No. 1 Page 8

v1.1, Last updated on 18/09/2018

Cash used in investing

activities

-3,000

Cash flows from financing

activities

New Capital introduced by the

owner

40,000

Repayment of Mortgage-

Principal

50,000

Drawings by the owner 20,000

Cash used in financing

activities -30,000

Net increase/decrease in cash 45,000

Add: Opening balance 5,000

Closing balance 50,000

Task 4 - Accounting (5 Marks)

Financial Statement Analysis:

You are given the following financial statements for Huffington Post Trading:

Income Statement for the year ended 30June 2018

$ $ $

Sales (all credit) 480,000

Less, Cost of Goods Sold

inventories (1/7/2017)Purchases 54,500

Goods available for sale 331,800 386,300

Less, Inventories 30/6/2018 69,500 316,800

Gross Profit 163,200

Other Income 5,000

Total Operating Income 168,200

Less, Operating Expenses 110,600

Net Profit 57,600

Balance Sheet as at 30 June 2018

$ $ $

Current Assets

Accounts Receivable 78,000

Less, Allowance for Doubtful Debts 3,000 75,000

Inventories 69,500

Prepaid Expenses 500

Accrued revenue 1,000 146,000

Non-Current Assets

Accounting & Budgeting, Assessment No. 1 Page 8

v1.1, Last updated on 18/09/2018

T-1.8.1

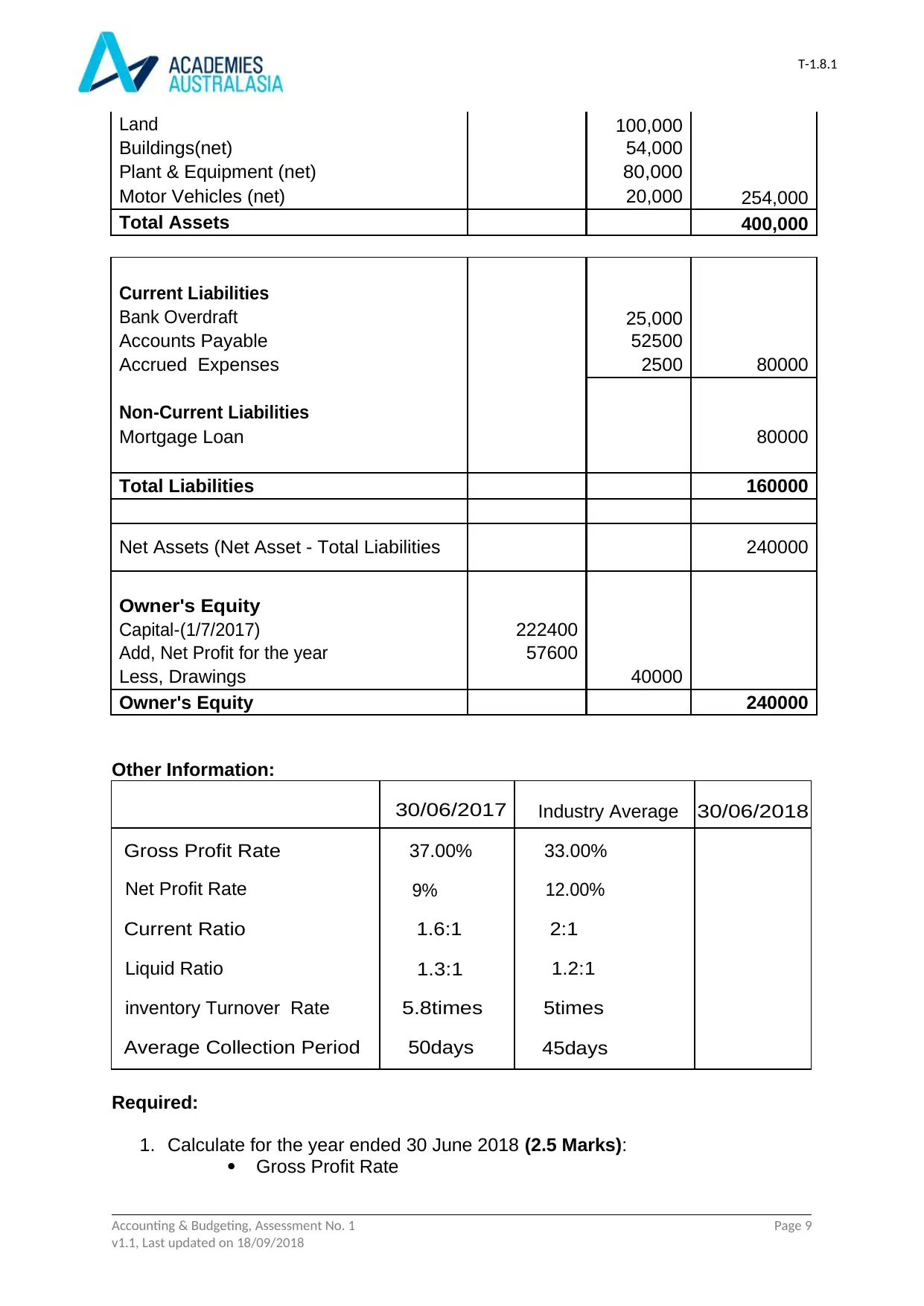

Land 100,000

Buildings(net) 54,000

Plant & Equipment (net) 80,000

Motor Vehicles (net) 20,000 254,000

Total Assets 400,000

Current Liabilities

Bank Overdraft 25,000

Accounts Payable 52500

Accrued Expenses 2500 80000

Non-Current Liabilities

Mortgage Loan 80000

Total Liabilities 160000

Net Assets (Net Asset - Total Liabilities 240000

Owner's Equity

Capital-(1/7/2017) 222400

Add, Net Profit for the year 57600

Less, Drawings 40000

Owner's Equity 240000

Other Information:

30/06/2017 Industry Average 30/06/2018

Gross Profit Rate 37.00% 33.00%

Net Profit Rate 9% 12.00%

Current Ratio 1.6:1 2:1

Liquid Ratio 1.3:1 1.2:1

inventory Turnover Rate 5.8times 5times

Average Collection Period 50days 45days

Required:

1. Calculate for the year ended 30 June 2018 (2.5 Marks):

Gross Profit Rate

Accounting & Budgeting, Assessment No. 1 Page 9

v1.1, Last updated on 18/09/2018

Land 100,000

Buildings(net) 54,000

Plant & Equipment (net) 80,000

Motor Vehicles (net) 20,000 254,000

Total Assets 400,000

Current Liabilities

Bank Overdraft 25,000

Accounts Payable 52500

Accrued Expenses 2500 80000

Non-Current Liabilities

Mortgage Loan 80000

Total Liabilities 160000

Net Assets (Net Asset - Total Liabilities 240000

Owner's Equity

Capital-(1/7/2017) 222400

Add, Net Profit for the year 57600

Less, Drawings 40000

Owner's Equity 240000

Other Information:

30/06/2017 Industry Average 30/06/2018

Gross Profit Rate 37.00% 33.00%

Net Profit Rate 9% 12.00%

Current Ratio 1.6:1 2:1

Liquid Ratio 1.3:1 1.2:1

inventory Turnover Rate 5.8times 5times

Average Collection Period 50days 45days

Required:

1. Calculate for the year ended 30 June 2018 (2.5 Marks):

Gross Profit Rate

Accounting & Budgeting, Assessment No. 1 Page 9

v1.1, Last updated on 18/09/2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

T-1.8.1

Net Profit Rate

Current Ratio

Liquid Ratio

Inventory Turnover Rate

Average Collection Period

2. Based on the ratios you have calculated and the other information given,

comment briefly on each of the following for Bowman's business (1.5 Marks):

Profitability

Business Activity

Liquidity

3. Advise the company of possible reasons for any unsatisfactory situations that

exist in relation to the business and suggest actions that may be taken to

improve them. (1 Mark)

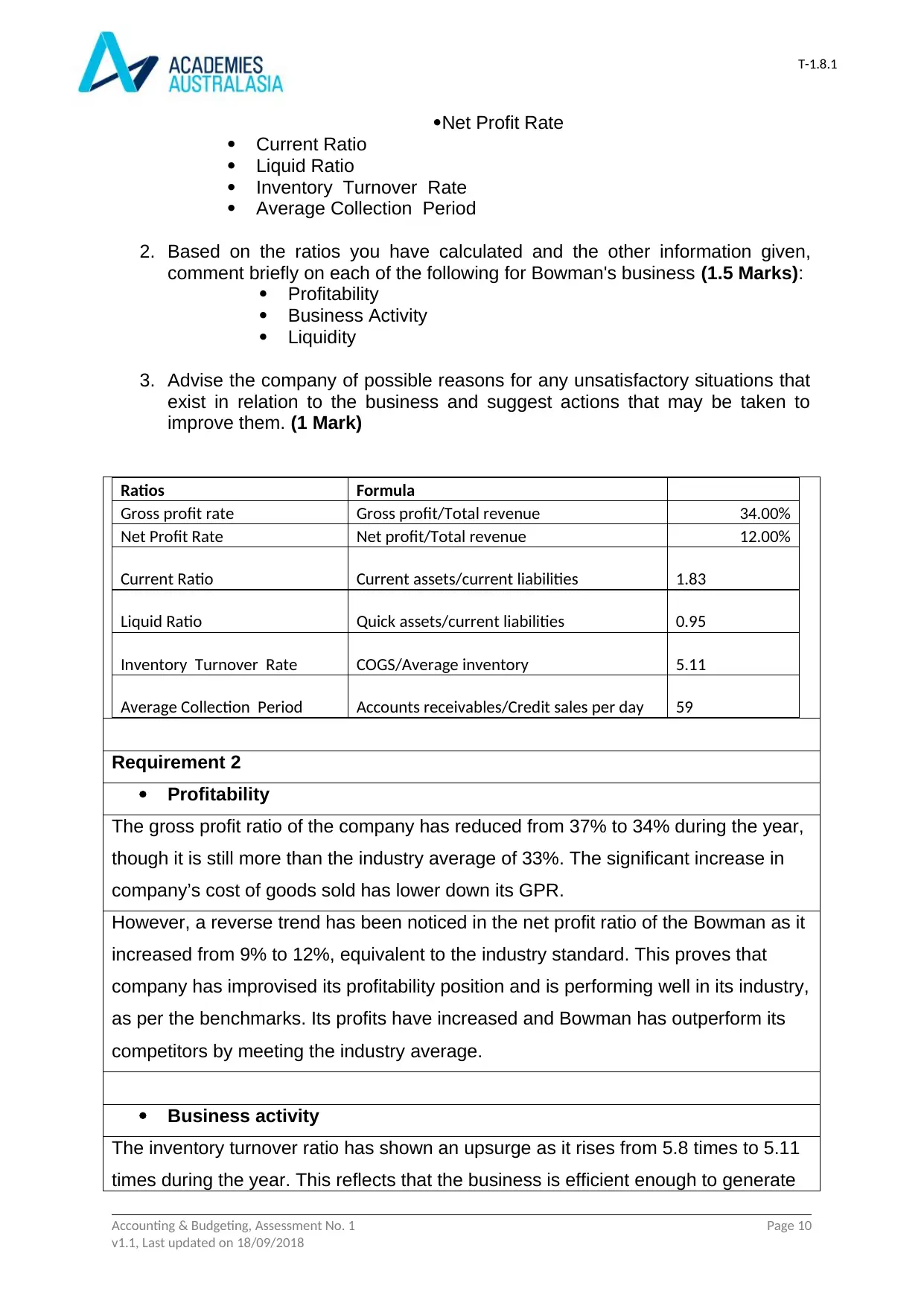

Ratios Formula

Gross profit rate Gross profit/Total revenue 34.00%

Net Profit Rate Net profit/Total revenue 12.00%

Current Ratio Current assets/current liabilities 1.83

Liquid Ratio Quick assets/current liabilities 0.95

Inventory Turnover Rate COGS/Average inventory 5.11

Average Collection Period Accounts receivables/Credit sales per day 59

Requirement 2

Profitability

The gross profit ratio of the company has reduced from 37% to 34% during the year,

though it is still more than the industry average of 33%. The significant increase in

company’s cost of goods sold has lower down its GPR.

However, a reverse trend has been noticed in the net profit ratio of the Bowman as it

increased from 9% to 12%, equivalent to the industry standard. This proves that

company has improvised its profitability position and is performing well in its industry,

as per the benchmarks. Its profits have increased and Bowman has outperform its

competitors by meeting the industry average.

Business activity

The inventory turnover ratio has shown an upsurge as it rises from 5.8 times to 5.11

times during the year. This reflects that the business is efficient enough to generate

Accounting & Budgeting, Assessment No. 1 Page 10

v1.1, Last updated on 18/09/2018

Net Profit Rate

Current Ratio

Liquid Ratio

Inventory Turnover Rate

Average Collection Period

2. Based on the ratios you have calculated and the other information given,

comment briefly on each of the following for Bowman's business (1.5 Marks):

Profitability

Business Activity

Liquidity

3. Advise the company of possible reasons for any unsatisfactory situations that

exist in relation to the business and suggest actions that may be taken to

improve them. (1 Mark)

Ratios Formula

Gross profit rate Gross profit/Total revenue 34.00%

Net Profit Rate Net profit/Total revenue 12.00%

Current Ratio Current assets/current liabilities 1.83

Liquid Ratio Quick assets/current liabilities 0.95

Inventory Turnover Rate COGS/Average inventory 5.11

Average Collection Period Accounts receivables/Credit sales per day 59

Requirement 2

Profitability

The gross profit ratio of the company has reduced from 37% to 34% during the year,

though it is still more than the industry average of 33%. The significant increase in

company’s cost of goods sold has lower down its GPR.

However, a reverse trend has been noticed in the net profit ratio of the Bowman as it

increased from 9% to 12%, equivalent to the industry standard. This proves that

company has improvised its profitability position and is performing well in its industry,

as per the benchmarks. Its profits have increased and Bowman has outperform its

competitors by meeting the industry average.

Business activity

The inventory turnover ratio has shown an upsurge as it rises from 5.8 times to 5.11

times during the year. This reflects that the business is efficient enough to generate

Accounting & Budgeting, Assessment No. 1 Page 10

v1.1, Last updated on 18/09/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

more revenues from its inventory.

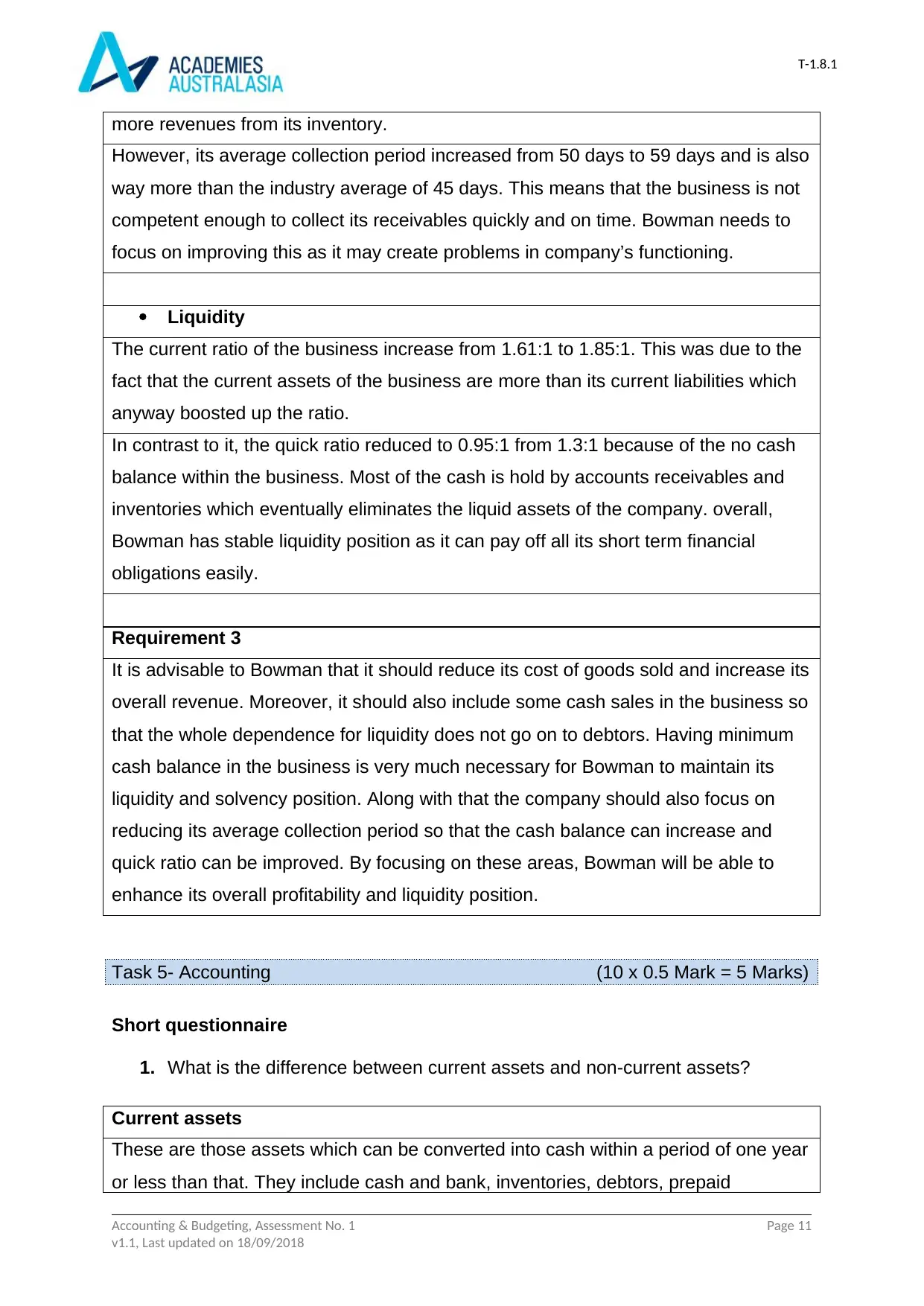

However, its average collection period increased from 50 days to 59 days and is also

way more than the industry average of 45 days. This means that the business is not

competent enough to collect its receivables quickly and on time. Bowman needs to

focus on improving this as it may create problems in company’s functioning.

Liquidity

The current ratio of the business increase from 1.61:1 to 1.85:1. This was due to the

fact that the current assets of the business are more than its current liabilities which

anyway boosted up the ratio.

In contrast to it, the quick ratio reduced to 0.95:1 from 1.3:1 because of the no cash

balance within the business. Most of the cash is hold by accounts receivables and

inventories which eventually eliminates the liquid assets of the company. overall,

Bowman has stable liquidity position as it can pay off all its short term financial

obligations easily.

Requirement 3

It is advisable to Bowman that it should reduce its cost of goods sold and increase its

overall revenue. Moreover, it should also include some cash sales in the business so

that the whole dependence for liquidity does not go on to debtors. Having minimum

cash balance in the business is very much necessary for Bowman to maintain its

liquidity and solvency position. Along with that the company should also focus on

reducing its average collection period so that the cash balance can increase and

quick ratio can be improved. By focusing on these areas, Bowman will be able to

enhance its overall profitability and liquidity position.

Task 5- Accounting (10 x 0.5 Mark = 5 Marks)

Short questionnaire

1. What is the difference between current assets and non-current assets?

Current assets

These are those assets which can be converted into cash within a period of one year

or less than that. They include cash and bank, inventories, debtors, prepaid

Accounting & Budgeting, Assessment No. 1 Page 11

v1.1, Last updated on 18/09/2018

more revenues from its inventory.

However, its average collection period increased from 50 days to 59 days and is also

way more than the industry average of 45 days. This means that the business is not

competent enough to collect its receivables quickly and on time. Bowman needs to

focus on improving this as it may create problems in company’s functioning.

Liquidity

The current ratio of the business increase from 1.61:1 to 1.85:1. This was due to the

fact that the current assets of the business are more than its current liabilities which

anyway boosted up the ratio.

In contrast to it, the quick ratio reduced to 0.95:1 from 1.3:1 because of the no cash

balance within the business. Most of the cash is hold by accounts receivables and

inventories which eventually eliminates the liquid assets of the company. overall,

Bowman has stable liquidity position as it can pay off all its short term financial

obligations easily.

Requirement 3

It is advisable to Bowman that it should reduce its cost of goods sold and increase its

overall revenue. Moreover, it should also include some cash sales in the business so

that the whole dependence for liquidity does not go on to debtors. Having minimum

cash balance in the business is very much necessary for Bowman to maintain its

liquidity and solvency position. Along with that the company should also focus on

reducing its average collection period so that the cash balance can increase and

quick ratio can be improved. By focusing on these areas, Bowman will be able to

enhance its overall profitability and liquidity position.

Task 5- Accounting (10 x 0.5 Mark = 5 Marks)

Short questionnaire

1. What is the difference between current assets and non-current assets?

Current assets

These are those assets which can be converted into cash within a period of one year

or less than that. They include cash and bank, inventories, debtors, prepaid

Accounting & Budgeting, Assessment No. 1 Page 11

v1.1, Last updated on 18/09/2018

T-1.8.1

expenses and others. All these assets provide economic benefit to the company

within a year.

Non-current assets

These assets are held by the company for more than one year and are considered

as the long term investments of the firm. They provide economic benefits to the

company for long run and require more than one year to get converted into cash. For

instance, property, plant and equipment, land, machinery, building and others.

2. Explain revenue and revenue recognition.

Revenue

In accounting terms, revenue the amount earned by a business from its operations

or activities. It is generated by the sale of goods and services to the consumers.

Revenue is also received from other sources like interest income, fees, royalties and

many more.

Revenue recognition

It is an accounting concept that focuses on specific circumstances under which the

revenue is recognized by the company. IFRS has laid down some criteria for the

same such as transfer of risks and rewards from seller to buyer, measureable

amount of revenue and cost of revenue and others.

3. What does it mean to capitalize expenditure?

Capitalization of expenditure means that it will now recorded in the balance sheet as

an asset rather than in income statement as an expense.

4. What supporting charts, diagrams or data may be useful to be presented with

the financial statements?

Charts like pie-chart reflecting the revenue of the company from different

segments, line graph showing the net profit growth, column graph reflecting the

main items like historical sales, return on equity, operating profit and others might

Accounting & Budgeting, Assessment No. 1 Page 12

v1.1, Last updated on 18/09/2018

expenses and others. All these assets provide economic benefit to the company

within a year.

Non-current assets

These assets are held by the company for more than one year and are considered

as the long term investments of the firm. They provide economic benefits to the

company for long run and require more than one year to get converted into cash. For

instance, property, plant and equipment, land, machinery, building and others.

2. Explain revenue and revenue recognition.

Revenue

In accounting terms, revenue the amount earned by a business from its operations

or activities. It is generated by the sale of goods and services to the consumers.

Revenue is also received from other sources like interest income, fees, royalties and

many more.

Revenue recognition

It is an accounting concept that focuses on specific circumstances under which the

revenue is recognized by the company. IFRS has laid down some criteria for the

same such as transfer of risks and rewards from seller to buyer, measureable

amount of revenue and cost of revenue and others.

3. What does it mean to capitalize expenditure?

Capitalization of expenditure means that it will now recorded in the balance sheet as

an asset rather than in income statement as an expense.

4. What supporting charts, diagrams or data may be useful to be presented with

the financial statements?

Charts like pie-chart reflecting the revenue of the company from different

segments, line graph showing the net profit growth, column graph reflecting the

main items like historical sales, return on equity, operating profit and others might

Accounting & Budgeting, Assessment No. 1 Page 12

v1.1, Last updated on 18/09/2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 46

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.