FNS50315 Finance & Mortgage Broking: Complex Lending Analysis

VerifiedAdded on 2024/05/17

|26

|5817

|381

Homework Assignment

AI Summary

This assignment solution for FNS50315 Finance and Mortgage Broking addresses various aspects of the broking process, including gathering client information, documenting interactions, researching complex lending solutions, identifying and managing risks, and presenting loan options. It emphasizes the importance of face-to-face interviews, maintaining client confidentiality, and establishing rapport with emotionally sensitive clients. The solution details methods for recording client information, including using loan forms and technology to manage data. It also covers researching complex broking solutions based on client needs, analyzing risks, and providing appropriate loan options while adhering to relevant legislation and ethical guidelines. The assignment further explores identifying potential client concerns before presenting loan options and preparing responses to address these concerns, ensuring transparency and accountability in the loan process.

FNS50315 Finance and Mortgage

Broking

1

Broking

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Assignment 3.........................................................................................................................................2

Assignment 4.........................................................................................................................................9

Question 1.........................................................................................................................................9

Part A.............................................................................................................................................9

Part B...........................................................................................................................................11

Part C...........................................................................................................................................12

Question 2.......................................................................................................................................13

A. Trust........................................................................................................................................13

B. Company..................................................................................................................................15

Question 3.......................................................................................................................................17

Question 4...................................................................................................................................20

Question 5...................................................................................................................................21

Question 6...................................................................................................................................23

References...........................................................................................................................................24

2

Assignment 3.........................................................................................................................................2

Assignment 4.........................................................................................................................................9

Question 1.........................................................................................................................................9

Part A.............................................................................................................................................9

Part B...........................................................................................................................................11

Part C...........................................................................................................................................12

Question 2.......................................................................................................................................13

A. Trust........................................................................................................................................13

B. Company..................................................................................................................................15

Question 3.......................................................................................................................................17

Question 4...................................................................................................................................20

Question 5...................................................................................................................................21

Question 6...................................................................................................................................23

References...........................................................................................................................................24

2

Assignment 3

Question 1: Describe how you gather the information required when establishing the

client’s complex lending requirements?

While determining the needs with regards to the lending requirements of the client, it is

important to clearly define the services to be provided to the client. In case of client seeking

the loan, the lending services will be required to be provided to the client including the

serviceability analysis, assistance in preparation and submission if loan documents and

assistance in procurement of loan. For this purpose face to face interview is conducted with

the clients in personal and questions are asked to them with regards to the lending

requirements and responses are noted. These questions include personal details, assets held

by client, liabilities and obligations due, sources and amount of income, investment and

insurance details, purpose of loan, utilisation of loan amount, etc. In case of cultural

differences with the client, the written interview form is given to the client to be filled in his

own language. The language used by the client in filling the form can be translated for

interpretation. However, the information provided by the client in any form is kept

confidential and secured so as to protect the integrity of the client under the professional

conduct.

In some cases the client faces emotive issues such as financial deficiency causing depression

or some dream project for the purpose of which loan is sought. In these cases if the loan

application is rejected, the client is seriously hurt. In case of emotionally sensitive client

assurance if loan approval is not given at the beginning and the client is helped with other

loan options for availing the loan amount. Also in these cases a rapport is established so that

the sensitive clients understand each other and communicate effectively. Throughput the

complete process of broking, regular contact with the client will be maintained so that the

client can be informed about the status of loan application and also the changes or

amendments of any required by the client can be enquired. The periodic discussions with the

client during the process will help in preventing the risks occurring due to changes in the

client requirements, legislation or any other causes.

3

Question 1: Describe how you gather the information required when establishing the

client’s complex lending requirements?

While determining the needs with regards to the lending requirements of the client, it is

important to clearly define the services to be provided to the client. In case of client seeking

the loan, the lending services will be required to be provided to the client including the

serviceability analysis, assistance in preparation and submission if loan documents and

assistance in procurement of loan. For this purpose face to face interview is conducted with

the clients in personal and questions are asked to them with regards to the lending

requirements and responses are noted. These questions include personal details, assets held

by client, liabilities and obligations due, sources and amount of income, investment and

insurance details, purpose of loan, utilisation of loan amount, etc. In case of cultural

differences with the client, the written interview form is given to the client to be filled in his

own language. The language used by the client in filling the form can be translated for

interpretation. However, the information provided by the client in any form is kept

confidential and secured so as to protect the integrity of the client under the professional

conduct.

In some cases the client faces emotive issues such as financial deficiency causing depression

or some dream project for the purpose of which loan is sought. In these cases if the loan

application is rejected, the client is seriously hurt. In case of emotionally sensitive client

assurance if loan approval is not given at the beginning and the client is helped with other

loan options for availing the loan amount. Also in these cases a rapport is established so that

the sensitive clients understand each other and communicate effectively. Throughput the

complete process of broking, regular contact with the client will be maintained so that the

client can be informed about the status of loan application and also the changes or

amendments of any required by the client can be enquired. The periodic discussions with the

client during the process will help in preventing the risks occurring due to changes in the

client requirements, legislation or any other causes.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

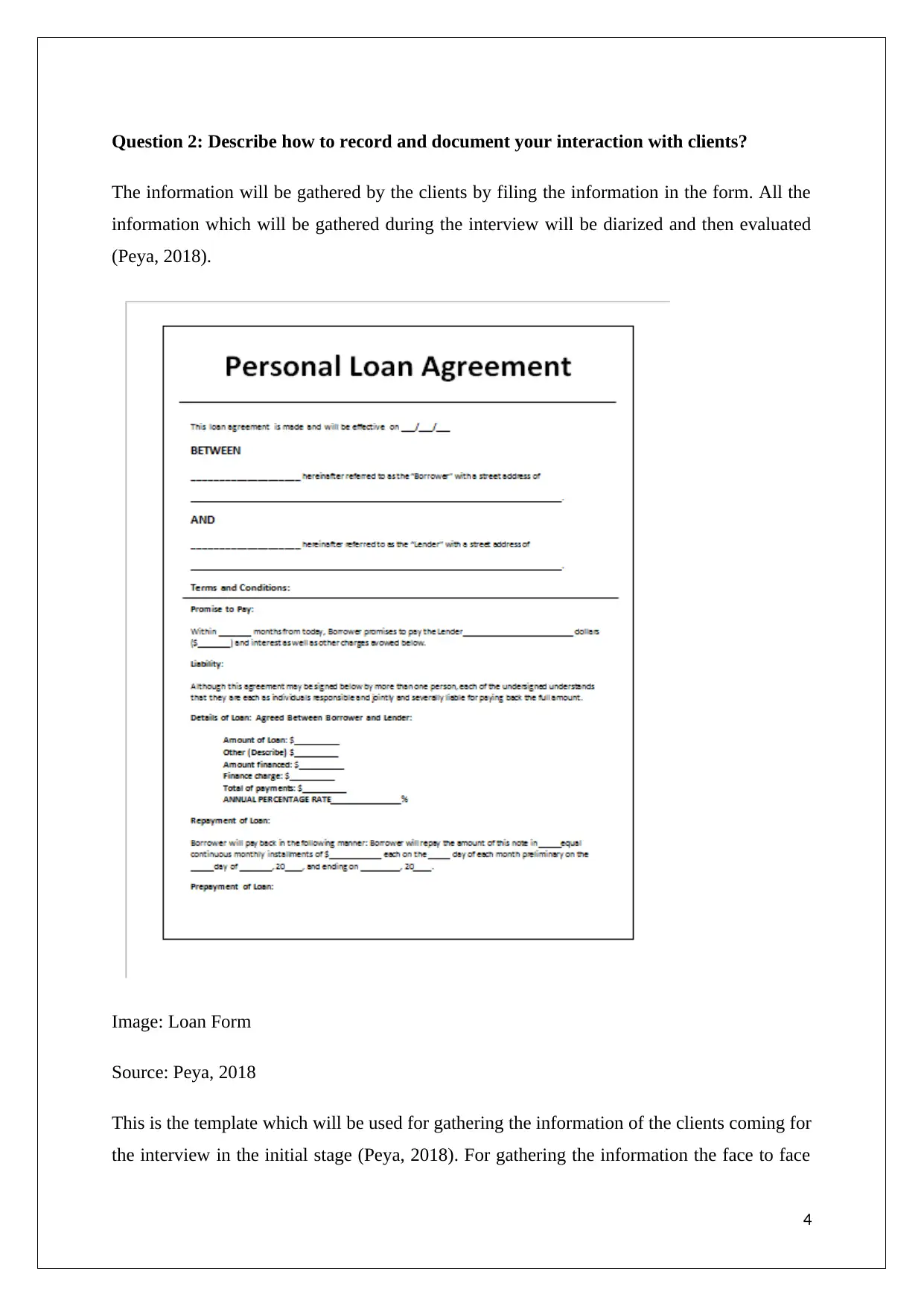

Question 2: Describe how to record and document your interaction with clients?

The information will be gathered by the clients by filing the information in the form. All the

information which will be gathered during the interview will be diarized and then evaluated

(Peya, 2018).

Image: Loan Form

Source: Peya, 2018

This is the template which will be used for gathering the information of the clients coming for

the interview in the initial stage (Peya, 2018). For gathering the information the face to face

4

The information will be gathered by the clients by filing the information in the form. All the

information which will be gathered during the interview will be diarized and then evaluated

(Peya, 2018).

Image: Loan Form

Source: Peya, 2018

This is the template which will be used for gathering the information of the clients coming for

the interview in the initial stage (Peya, 2018). For gathering the information the face to face

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

conversation will be done instead of the telephonic conversation and what all responses will

be gathered will be entered in the diary for preparing the loan agreement. The procedures that

will be followed are that first the form will be filled by the clients coming for the loan

approval and then all the information will be collected. The documents that will be gathered

before granting the loan to the clients are: the financial statements of the business, bank

statements, any current loan document, income tax returns, personal financial information,

business license and a business plan (Kiisel, 2015).

The information gathered will be recorded through the proper use of the technology through

which the data of all the clients will be at the one single place so that whenever required can

be tracked through the loan account number. The software that will be designed by the

organisation will be used to access the entire database at the proper place and the spread

sheets will be maintained of all clients. The proper loan structure will be followed and

presented to the clients according to the guidelines of the organisation. The systematic

procedure will be their which explains the exact instalments and the percentage rate at which

the loan will have to be repaid. All the documents presented for the loan will be reviewed

before granting the loan.

5

be gathered will be entered in the diary for preparing the loan agreement. The procedures that

will be followed are that first the form will be filled by the clients coming for the loan

approval and then all the information will be collected. The documents that will be gathered

before granting the loan to the clients are: the financial statements of the business, bank

statements, any current loan document, income tax returns, personal financial information,

business license and a business plan (Kiisel, 2015).

The information gathered will be recorded through the proper use of the technology through

which the data of all the clients will be at the one single place so that whenever required can

be tracked through the loan account number. The software that will be designed by the

organisation will be used to access the entire database at the proper place and the spread

sheets will be maintained of all clients. The proper loan structure will be followed and

presented to the clients according to the guidelines of the organisation. The systematic

procedure will be their which explains the exact instalments and the percentage rate at which

the loan will have to be repaid. All the documents presented for the loan will be reviewed

before granting the loan.

5

Question 3: Describe how you research and consider complex broking solutions based

on the clients’ needs?

The complex or special feature of a client situation includes the liquidity of the firm that in

how much time the loan will be repaid back. This shows that the work environments and the

situations affect the performance. The other factors that include are international purchases,

products available to the advisor and the volatility of the expected growth and the income.

The analysis of the client’s situation may include various risks some of which are allocation

of the assets, economic risks arise due to the change in the economic factors and the market

risks which can be caused due to the change in the various factors such as the economic

cycle, fixed assets, property and the stock market.

The broker needs to refer the clients to the tier 1 in case when the client who has taken the

loan from the organisation has been unable to pay back the amount taken against the

collateral. In this scenario the client will be taken to the financial advisor or the accountant

who will guide the client according to the company’s at and guidelines. The loan structures

are analysed and measured by the financial position of the client that actually the current

status of the customer who is seeking for loan is going on. The inappropriate options are

rejected on the basis of the creditworthiness that is possessed by the client seeking for the

loan. The options are analysed and checked to ensure the noncompliance through the various

acts some of which includes legislation acts, ethical guidelines that has to be followed and the

regulatory for evaluating the ability of the customer to achieve objective of the client.

6

on the clients’ needs?

The complex or special feature of a client situation includes the liquidity of the firm that in

how much time the loan will be repaid back. This shows that the work environments and the

situations affect the performance. The other factors that include are international purchases,

products available to the advisor and the volatility of the expected growth and the income.

The analysis of the client’s situation may include various risks some of which are allocation

of the assets, economic risks arise due to the change in the economic factors and the market

risks which can be caused due to the change in the various factors such as the economic

cycle, fixed assets, property and the stock market.

The broker needs to refer the clients to the tier 1 in case when the client who has taken the

loan from the organisation has been unable to pay back the amount taken against the

collateral. In this scenario the client will be taken to the financial advisor or the accountant

who will guide the client according to the company’s at and guidelines. The loan structures

are analysed and measured by the financial position of the client that actually the current

status of the customer who is seeking for loan is going on. The inappropriate options are

rejected on the basis of the creditworthiness that is possessed by the client seeking for the

loan. The options are analysed and checked to ensure the noncompliance through the various

acts some of which includes legislation acts, ethical guidelines that has to be followed and the

regulatory for evaluating the ability of the customer to achieve objective of the client.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 4: Describe and provide evidence of how you identify and manage the risk

when dealing with clients with complex loan requirements?

There are many risks which occur while dealing with the clients in the scenario. The risk has

to be identified and maintained while dealing with the clients Risk assessment is the way

through which the risk can be identified and assessed. The first step is to identify the area of

the risk then the analysis of the risk has to be done after evaluation. After all these steps the

measures has to decide by the mangers of the company for taking the appropriate decisions.

There are various tools which are used for assessing the risk one of which is the valuation

practices. This is the practice through which the value of the underlying security can be

analysed. The issues on the valuation of the underlying stock can be evaluated by these tools

which are used for the valuation practices. Assessment is the risk to provide the probability of

the risk events that impacts the risk. The clear scenario should be provided to the clients

against the risk involved while assessing the risk. The stakeholders should provide the exact

criteria for the assessment of the risk in the written form which should also include all the

information related to the investments instalments and the need through which that risk can

be controlled. The aspects which are to be taken into the consideration so that the government

and industry requirements can be coded are that the business structure should be carefully

followed and the leasing premises and the intellectual property should be entitled using the

various trademarks and the patents.

7

when dealing with clients with complex loan requirements?

There are many risks which occur while dealing with the clients in the scenario. The risk has

to be identified and maintained while dealing with the clients Risk assessment is the way

through which the risk can be identified and assessed. The first step is to identify the area of

the risk then the analysis of the risk has to be done after evaluation. After all these steps the

measures has to decide by the mangers of the company for taking the appropriate decisions.

There are various tools which are used for assessing the risk one of which is the valuation

practices. This is the practice through which the value of the underlying security can be

analysed. The issues on the valuation of the underlying stock can be evaluated by these tools

which are used for the valuation practices. Assessment is the risk to provide the probability of

the risk events that impacts the risk. The clear scenario should be provided to the clients

against the risk involved while assessing the risk. The stakeholders should provide the exact

criteria for the assessment of the risk in the written form which should also include all the

information related to the investments instalments and the need through which that risk can

be controlled. The aspects which are to be taken into the consideration so that the government

and industry requirements can be coded are that the business structure should be carefully

followed and the leasing premises and the intellectual property should be entitled using the

various trademarks and the patents.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 5: Provide an example of how you present the loan options to the client,

including an explanation of why you chose that option.

The loan option chosen have both the advantages as well as the disadvantages. The

advantages includes that the loan is provided at the less interest rates as compared with that of

the other companies with the same process (Business Queensland, 2018). The best way to

compare the loan from the other organisation is that the key factors should be considered

which includes the interest rates, tenure of the loan and the processing fees of the loan. The

disadvantage is that the long duration period which is opted by the clients seeking the high

amount of loan gets impacted. The fees charges which paid by the lender to the brokers are

also included while the calculation of the loan amount. The client will be explained about the

various relevant legislations and the regulatory guidelines and also all the policies of the

lender related to the loan. The research and the consultation which is provide to the clients is

should be taken the effectiveness into the consideration while doing the research (Business

Queensland, 2018). The proper quantitative methods should be used while doing the research

about the various plans and calculating the profitability of the plan. Consultations should be

taken from the accountants, lawyers and the financial planners so that the proper plan can be

set by the organisation which will be of benefit for both organisation as well as the clients.

Once all the evaluation has been done and the documents has been analysed then the

appropriate option should be presented to the client for the approval and then the concern are

addressed to the clients. The information related to the compliance is also provided to the

clients so that the clients are aware of all the activities that need not to be performed while the

loan process is going on (Business Queensland, 2018). The procedures should include both

internal as well as the external factors which will be added to the compliance.

8

including an explanation of why you chose that option.

The loan option chosen have both the advantages as well as the disadvantages. The

advantages includes that the loan is provided at the less interest rates as compared with that of

the other companies with the same process (Business Queensland, 2018). The best way to

compare the loan from the other organisation is that the key factors should be considered

which includes the interest rates, tenure of the loan and the processing fees of the loan. The

disadvantage is that the long duration period which is opted by the clients seeking the high

amount of loan gets impacted. The fees charges which paid by the lender to the brokers are

also included while the calculation of the loan amount. The client will be explained about the

various relevant legislations and the regulatory guidelines and also all the policies of the

lender related to the loan. The research and the consultation which is provide to the clients is

should be taken the effectiveness into the consideration while doing the research (Business

Queensland, 2018). The proper quantitative methods should be used while doing the research

about the various plans and calculating the profitability of the plan. Consultations should be

taken from the accountants, lawyers and the financial planners so that the proper plan can be

set by the organisation which will be of benefit for both organisation as well as the clients.

Once all the evaluation has been done and the documents has been analysed then the

appropriate option should be presented to the client for the approval and then the concern are

addressed to the clients. The information related to the compliance is also provided to the

clients so that the clients are aware of all the activities that need not to be performed while the

loan process is going on (Business Queensland, 2018). The procedures should include both

internal as well as the external factors which will be added to the compliance.

8

Question 6: Prior to presenting the loan options to the client did you identify any

concerns that the client may raise? What preparations were completed to respond to

these concerns?

The identification of the concerns should be done before presenting it to the client so that the

client cannot raise the issue once the proposal has been presented. Proper research should be

done for all the plans and then the most appropriate one should be considered. The materials

or the documents which are required for taking the loan should be pre-determined and

presented to the clients. The documents should include the proof that shows the credit

worthiness of the agent that is taking the loan (Yardney, 2016). The alternative

recommendations should be pre-determined by the lender that if the client does not fulfils all

the criteria so the alternative option can be given so as to attract the clients. The brochure

should be prepared by the organisation defining the regulatory acts and the guidelines for the

financers who will be financing the organisation should also be defined by the lender so that

the trust of the clients can be maintained. During the complex situations the lender should

appoint the specialist who can handle all the conflicts related to the financial issues so that the

conflicts can be decreased. The organisation should be able to identify the concerns of the

clients easily and the appropriate actions should be taken to avoid it. The process should be

clearly defined about gaining the agreement so that the proceedings can be done of the clients

(Yardney, 2016). So, the proper identification and the loan option are very much required by

the lender so that the client cannot raise the issues in the near future. The preparation of the

responses should be diarized so that the concerns can be taken into considerations and the

action can be taken accordingly. The recommendations should be designed according to the

responses and the feedbacks of the clients against the feedback provided. This whole process

brings the transparency and the accountability in the loan process of the organisation

(Yardney, 2016).

9

concerns that the client may raise? What preparations were completed to respond to

these concerns?

The identification of the concerns should be done before presenting it to the client so that the

client cannot raise the issue once the proposal has been presented. Proper research should be

done for all the plans and then the most appropriate one should be considered. The materials

or the documents which are required for taking the loan should be pre-determined and

presented to the clients. The documents should include the proof that shows the credit

worthiness of the agent that is taking the loan (Yardney, 2016). The alternative

recommendations should be pre-determined by the lender that if the client does not fulfils all

the criteria so the alternative option can be given so as to attract the clients. The brochure

should be prepared by the organisation defining the regulatory acts and the guidelines for the

financers who will be financing the organisation should also be defined by the lender so that

the trust of the clients can be maintained. During the complex situations the lender should

appoint the specialist who can handle all the conflicts related to the financial issues so that the

conflicts can be decreased. The organisation should be able to identify the concerns of the

clients easily and the appropriate actions should be taken to avoid it. The process should be

clearly defined about gaining the agreement so that the proceedings can be done of the clients

(Yardney, 2016). So, the proper identification and the loan option are very much required by

the lender so that the client cannot raise the issues in the near future. The preparation of the

responses should be diarized so that the concerns can be taken into considerations and the

action can be taken accordingly. The recommendations should be designed according to the

responses and the feedbacks of the clients against the feedback provided. This whole process

brings the transparency and the accountability in the loan process of the organisation

(Yardney, 2016).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assignment 4

Question 1

Part A

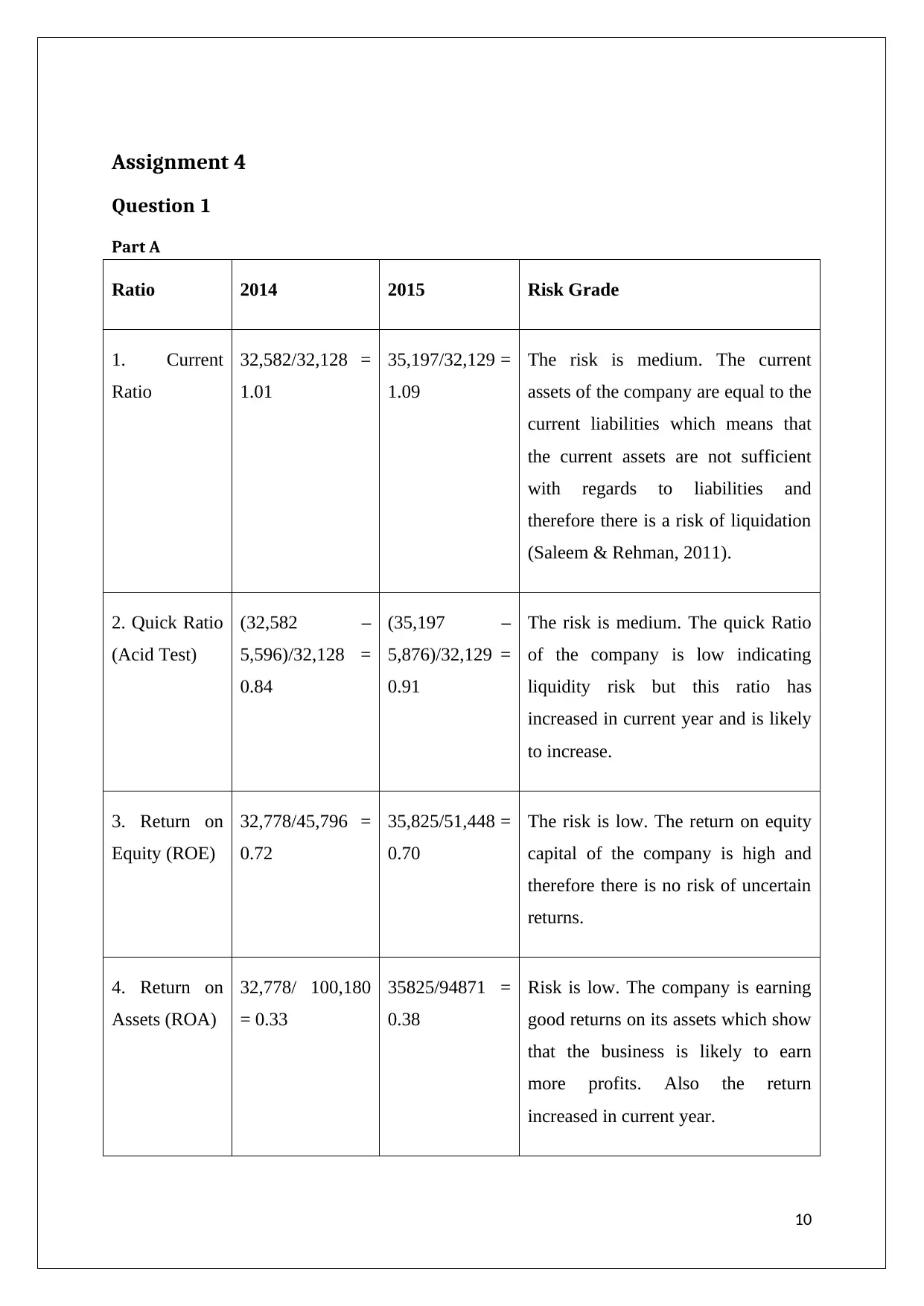

Ratio 2014 2015 Risk Grade

1. Current

Ratio

32,582/32,128 =

1.01

35,197/32,129 =

1.09

The risk is medium. The current

assets of the company are equal to the

current liabilities which means that

the current assets are not sufficient

with regards to liabilities and

therefore there is a risk of liquidation

(Saleem & Rehman, 2011).

2. Quick Ratio

(Acid Test)

(32,582 –

5,596)/32,128 =

0.84

(35,197 –

5,876)/32,129 =

0.91

The risk is medium. The quick Ratio

of the company is low indicating

liquidity risk but this ratio has

increased in current year and is likely

to increase.

3. Return on

Equity (ROE)

32,778/45,796 =

0.72

35,825/51,448 =

0.70

The risk is low. The return on equity

capital of the company is high and

therefore there is no risk of uncertain

returns.

4. Return on

Assets (ROA)

32,778/ 100,180

= 0.33

35825/94871 =

0.38

Risk is low. The company is earning

good returns on its assets which show

that the business is likely to earn

more profits. Also the return

increased in current year.

10

Question 1

Part A

Ratio 2014 2015 Risk Grade

1. Current

Ratio

32,582/32,128 =

1.01

35,197/32,129 =

1.09

The risk is medium. The current

assets of the company are equal to the

current liabilities which means that

the current assets are not sufficient

with regards to liabilities and

therefore there is a risk of liquidation

(Saleem & Rehman, 2011).

2. Quick Ratio

(Acid Test)

(32,582 –

5,596)/32,128 =

0.84

(35,197 –

5,876)/32,129 =

0.91

The risk is medium. The quick Ratio

of the company is low indicating

liquidity risk but this ratio has

increased in current year and is likely

to increase.

3. Return on

Equity (ROE)

32,778/45,796 =

0.72

35,825/51,448 =

0.70

The risk is low. The return on equity

capital of the company is high and

therefore there is no risk of uncertain

returns.

4. Return on

Assets (ROA)

32,778/ 100,180

= 0.33

35825/94871 =

0.38

Risk is low. The company is earning

good returns on its assets which show

that the business is likely to earn

more profits. Also the return

increased in current year.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

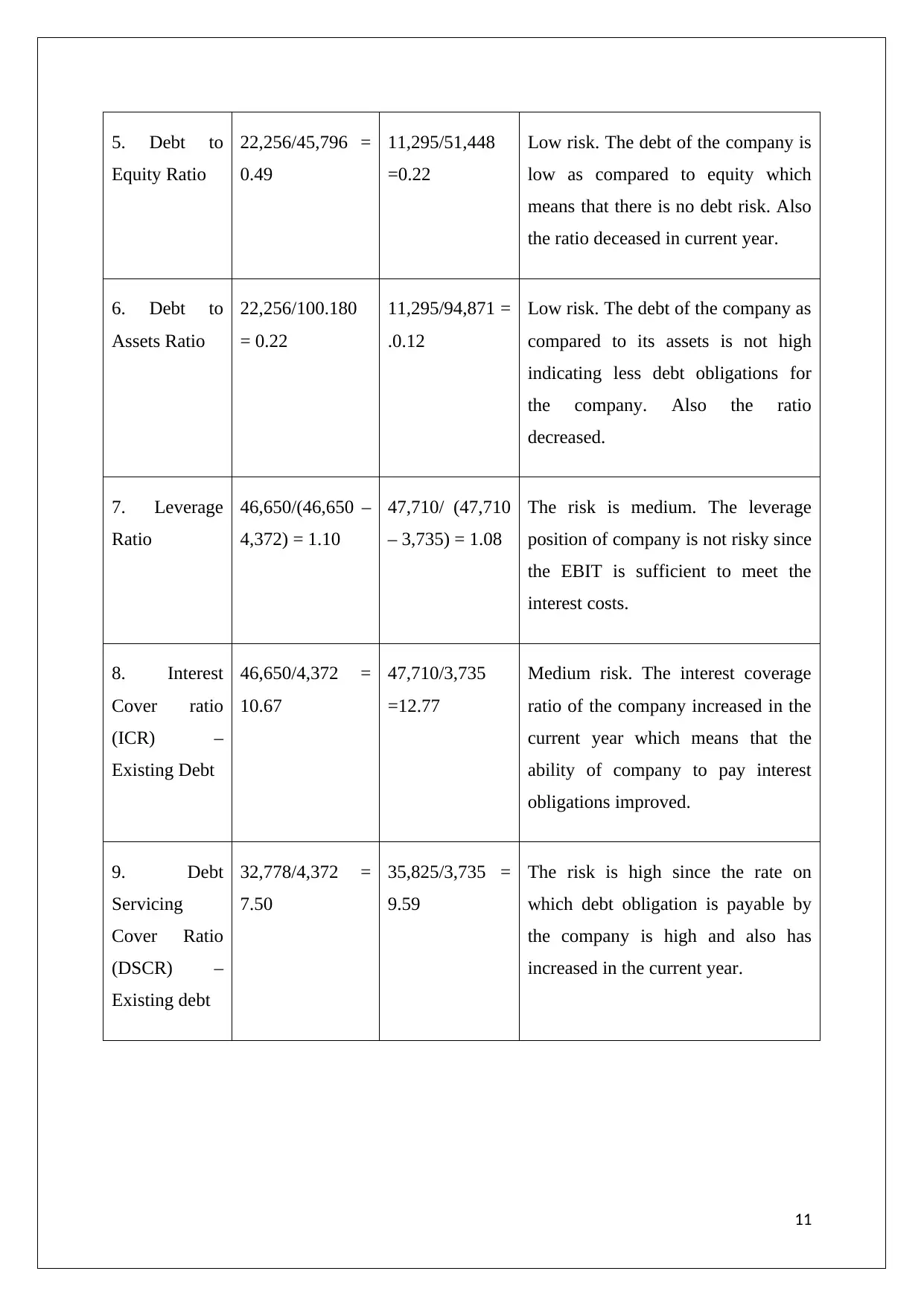

5. Debt to

Equity Ratio

22,256/45,796 =

0.49

11,295/51,448

=0.22

Low risk. The debt of the company is

low as compared to equity which

means that there is no debt risk. Also

the ratio deceased in current year.

6. Debt to

Assets Ratio

22,256/100.180

= 0.22

11,295/94,871 =

.0.12

Low risk. The debt of the company as

compared to its assets is not high

indicating less debt obligations for

the company. Also the ratio

decreased.

7. Leverage

Ratio

46,650/(46,650 –

4,372) = 1.10

47,710/ (47,710

– 3,735) = 1.08

The risk is medium. The leverage

position of company is not risky since

the EBIT is sufficient to meet the

interest costs.

8. Interest

Cover ratio

(ICR) –

Existing Debt

46,650/4,372 =

10.67

47,710/3,735

=12.77

Medium risk. The interest coverage

ratio of the company increased in the

current year which means that the

ability of company to pay interest

obligations improved.

9. Debt

Servicing

Cover Ratio

(DSCR) –

Existing debt

32,778/4,372 =

7.50

35,825/3,735 =

9.59

The risk is high since the rate on

which debt obligation is payable by

the company is high and also has

increased in the current year.

11

Equity Ratio

22,256/45,796 =

0.49

11,295/51,448

=0.22

Low risk. The debt of the company is

low as compared to equity which

means that there is no debt risk. Also

the ratio deceased in current year.

6. Debt to

Assets Ratio

22,256/100.180

= 0.22

11,295/94,871 =

.0.12

Low risk. The debt of the company as

compared to its assets is not high

indicating less debt obligations for

the company. Also the ratio

decreased.

7. Leverage

Ratio

46,650/(46,650 –

4,372) = 1.10

47,710/ (47,710

– 3,735) = 1.08

The risk is medium. The leverage

position of company is not risky since

the EBIT is sufficient to meet the

interest costs.

8. Interest

Cover ratio

(ICR) –

Existing Debt

46,650/4,372 =

10.67

47,710/3,735

=12.77

Medium risk. The interest coverage

ratio of the company increased in the

current year which means that the

ability of company to pay interest

obligations improved.

9. Debt

Servicing

Cover Ratio

(DSCR) –

Existing debt

32,778/4,372 =

7.50

35,825/3,735 =

9.59

The risk is high since the rate on

which debt obligation is payable by

the company is high and also has

increased in the current year.

11

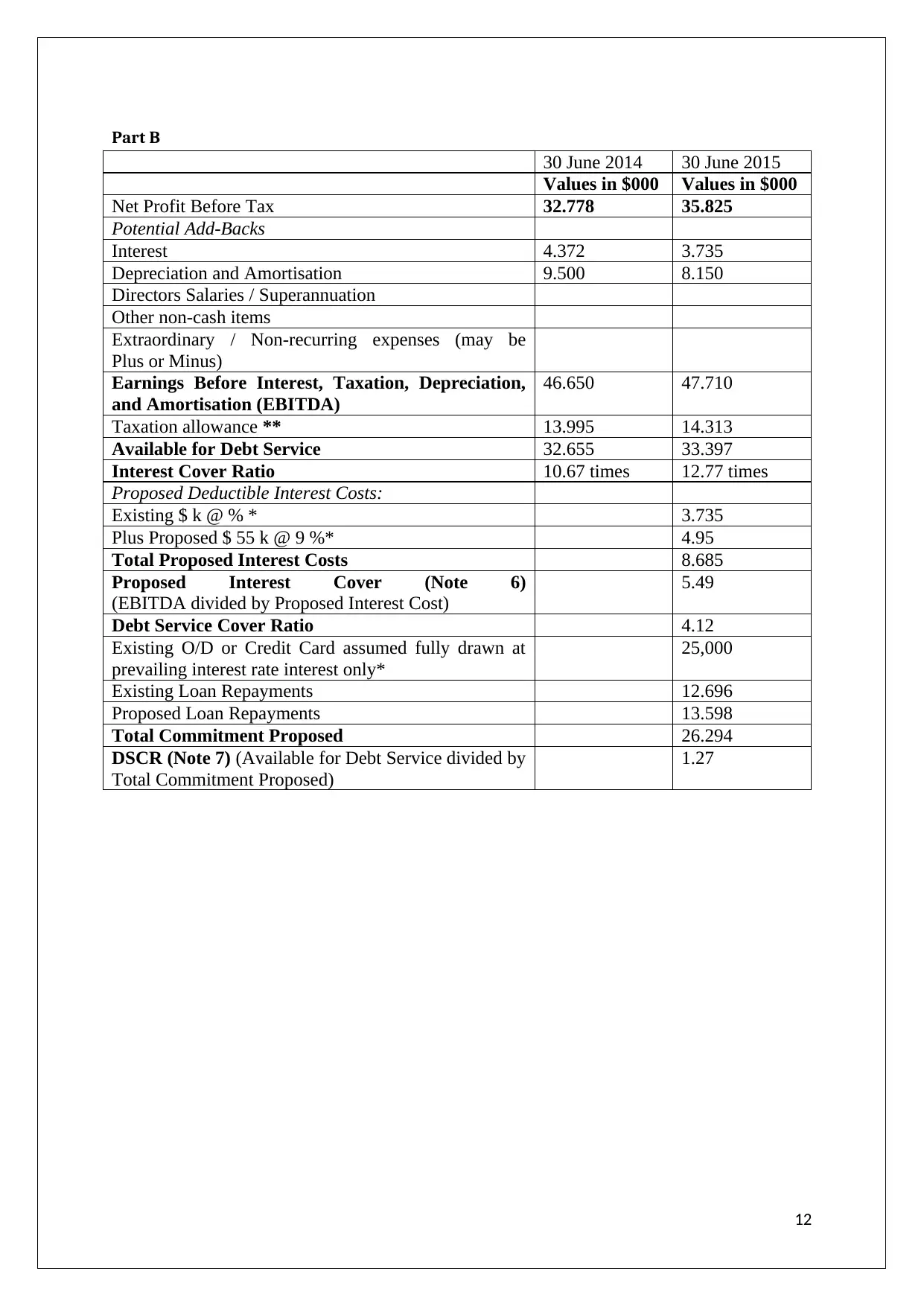

Part B

30 June 2014 30 June 2015

Values in $000 Values in $000

Net Profit Before Tax 32.778 35.825

Potential Add-Backs

Interest 4.372 3.735

Depreciation and Amortisation 9.500 8.150

Directors Salaries / Superannuation

Other non‐cash items

Extraordinary / Non-recurring expenses (may be

Plus or Minus)

Earnings Before Interest, Taxation, Depreciation,

and Amortisation (EBITDA)

46.650 47.710

Taxation allowance ** 13.995 14.313

Available for Debt Service 32.655 33.397

Interest Cover Ratio 10.67 times 12.77 times

Proposed Deductible Interest Costs:

Existing $ k @ % * 3.735

Plus Proposed $ 55 k @ 9 %* 4.95

Total Proposed Interest Costs 8.685

Proposed Interest Cover (Note 6)

(EBITDA divided by Proposed Interest Cost)

5.49

Debt Service Cover Ratio 4.12

Existing O/D or Credit Card assumed fully drawn at

prevailing interest rate interest only*

25,000

Existing Loan Repayments 12.696

Proposed Loan Repayments 13.598

Total Commitment Proposed 26.294

DSCR (Note 7) (Available for Debt Service divided by

Total Commitment Proposed)

1.27

12

30 June 2014 30 June 2015

Values in $000 Values in $000

Net Profit Before Tax 32.778 35.825

Potential Add-Backs

Interest 4.372 3.735

Depreciation and Amortisation 9.500 8.150

Directors Salaries / Superannuation

Other non‐cash items

Extraordinary / Non-recurring expenses (may be

Plus or Minus)

Earnings Before Interest, Taxation, Depreciation,

and Amortisation (EBITDA)

46.650 47.710

Taxation allowance ** 13.995 14.313

Available for Debt Service 32.655 33.397

Interest Cover Ratio 10.67 times 12.77 times

Proposed Deductible Interest Costs:

Existing $ k @ % * 3.735

Plus Proposed $ 55 k @ 9 %* 4.95

Total Proposed Interest Costs 8.685

Proposed Interest Cover (Note 6)

(EBITDA divided by Proposed Interest Cost)

5.49

Debt Service Cover Ratio 4.12

Existing O/D or Credit Card assumed fully drawn at

prevailing interest rate interest only*

25,000

Existing Loan Repayments 12.696

Proposed Loan Repayments 13.598

Total Commitment Proposed 26.294

DSCR (Note 7) (Available for Debt Service divided by

Total Commitment Proposed)

1.27

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.