FNSACC 601 Assessment 2: Capital Structure, Markets, and Economics

VerifiedAdded on 2020/03/16

|20

|4196

|89

Homework Assignment

AI Summary

This assignment solution for FNSACC 601 covers a wide range of financial concepts. It begins with defining economic problems, WACC, and capital structure, then delves into the Capital Asset Pricing Model (CAPM) and the Prudential Standard APS 110. The solution analyzes how companies make investment, financing, and dividend decisions. It identifies market structures for various products and explains financial markets and their services. The assignment further explores microeconomic principles, including reforms in Australia, and discusses key economic theories relevant to the financial services industry, such as supply-side economics, the global financial crisis, and value theory. Finally, it outlines key features of relevant legislation, statutory requirements, and industry codes of practice for the financial service industry. This comprehensive solution provides a detailed overview of essential financial concepts.

Running head: FNSACC 601

FNSACC 601

Name of the Student

Name of the University

Author Note

FNSACC 601

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ASSESSMENT 2

Assessment 1

Q1. What is an economic problem?

The economic problem – even called the central or the basic economic problem – states that an

economy's limited assets are inadequate to fulfill every human needs and wants. It expects that

human needs are boundless, however the way to fulfill human needs are scarce.

Q2. What is WACC and Leverage ratio?

The ratio among the debt and equity in the cost of capital computation should be similar as the

ratio between a company's overall debt finances and its total equity financing. This is also

known as the weighted average cost of capital, or WACC.

The organizations depend on a blend of owners' equity and debt to finance their operations. A

leverage ratio is any one of the numerous financial techniques that look at how much capital

arrives in the form of debt, or assesses the capability of a firm to meet their financial obligations.

Q3. Explain capital structure policy and Why does Capital structure matter?

Capital structure, the mixture of a firm's debt and equity, is important because it costs company

money to borrow. Capital structure also matters because of the different tax implications of debt

vs. equity and the impact of corporate taxes on a firm's profitability. Firms must be prudent in

their borrowing activities to avoid excessive risk and the possibility of financial distress or even

bankruptcy.

The capital structure policy comprises of the capital structure, financial leverage, Modigliani and

Miller's Capital Structure Theories, Bankruptcy Costs and Optimal Capital Structure, Extended

Pie Model, Observed Capital Structures and Long-Term Financing.

Assessment 1

Q1. What is an economic problem?

The economic problem – even called the central or the basic economic problem – states that an

economy's limited assets are inadequate to fulfill every human needs and wants. It expects that

human needs are boundless, however the way to fulfill human needs are scarce.

Q2. What is WACC and Leverage ratio?

The ratio among the debt and equity in the cost of capital computation should be similar as the

ratio between a company's overall debt finances and its total equity financing. This is also

known as the weighted average cost of capital, or WACC.

The organizations depend on a blend of owners' equity and debt to finance their operations. A

leverage ratio is any one of the numerous financial techniques that look at how much capital

arrives in the form of debt, or assesses the capability of a firm to meet their financial obligations.

Q3. Explain capital structure policy and Why does Capital structure matter?

Capital structure, the mixture of a firm's debt and equity, is important because it costs company

money to borrow. Capital structure also matters because of the different tax implications of debt

vs. equity and the impact of corporate taxes on a firm's profitability. Firms must be prudent in

their borrowing activities to avoid excessive risk and the possibility of financial distress or even

bankruptcy.

The capital structure policy comprises of the capital structure, financial leverage, Modigliani and

Miller's Capital Structure Theories, Bankruptcy Costs and Optimal Capital Structure, Extended

Pie Model, Observed Capital Structures and Long-Term Financing.

2ASSESSMENT 2

The capital structure of a firm does matter as it helps in the development of an effective

framework within which the company would operate their financial activities and regulate the

process of investing and gaining their capital so that effective operational activities can be

attained.

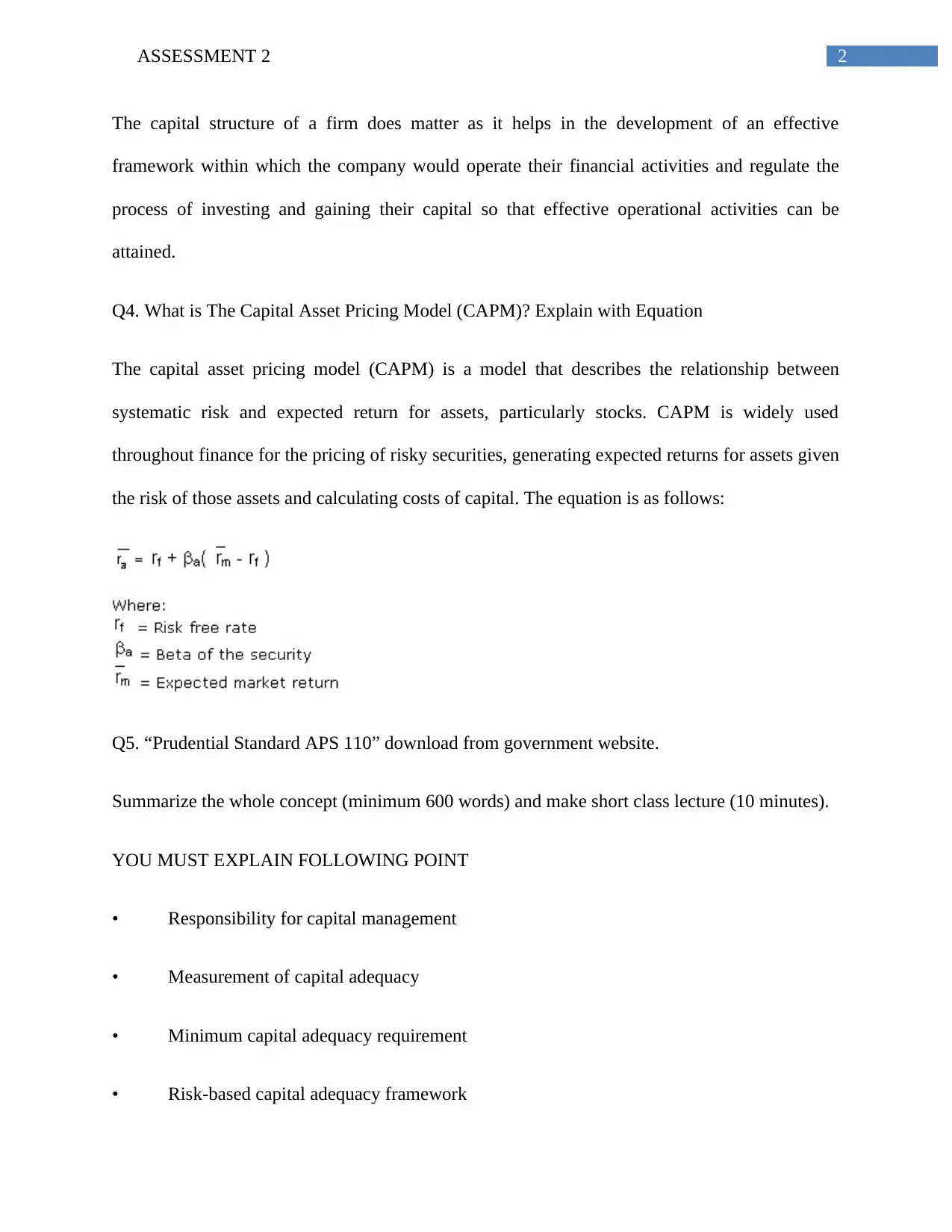

Q4. What is The Capital Asset Pricing Model (CAPM)? Explain with Equation

The capital asset pricing model (CAPM) is a model that describes the relationship between

systematic risk and expected return for assets, particularly stocks. CAPM is widely used

throughout finance for the pricing of risky securities, generating expected returns for assets given

the risk of those assets and calculating costs of capital. The equation is as follows:

Q5. “Prudential Standard APS 110” download from government website.

Summarize the whole concept (minimum 600 words) and make short class lecture (10 minutes).

YOU MUST EXPLAIN FOLLOWING POINT

• Responsibility for capital management

• Measurement of capital adequacy

• Minimum capital adequacy requirement

• Risk-based capital adequacy framework

The capital structure of a firm does matter as it helps in the development of an effective

framework within which the company would operate their financial activities and regulate the

process of investing and gaining their capital so that effective operational activities can be

attained.

Q4. What is The Capital Asset Pricing Model (CAPM)? Explain with Equation

The capital asset pricing model (CAPM) is a model that describes the relationship between

systematic risk and expected return for assets, particularly stocks. CAPM is widely used

throughout finance for the pricing of risky securities, generating expected returns for assets given

the risk of those assets and calculating costs of capital. The equation is as follows:

Q5. “Prudential Standard APS 110” download from government website.

Summarize the whole concept (minimum 600 words) and make short class lecture (10 minutes).

YOU MUST EXPLAIN FOLLOWING POINT

• Responsibility for capital management

• Measurement of capital adequacy

• Minimum capital adequacy requirement

• Risk-based capital adequacy framework

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ASSESSMENT 2

The Prudential Standard APS 110 comprises of the various concepts that are useful for the

development of the capital management of an organization. This standard is under the section

11AF of the Banking Act 1959. This standard is applicable to all the permitted deposit taking

organizations with respect to the Banking Act that is subject to paragraph 3.

It is seen that with respect to the responsibility capital management, it is seen that capital has

been looked down upon as the cornerstone of the financial strength of an ADI. It aids the

operations of ADI by giving out a cushion to absorb the losses that have not been predicted from

their actions and in the event of the issues that enables the ADI to sustain to operate in a viable

and sound manner while the issues are resolved and addressed.

The capital management requires to be an integral part of the risk management of ADI by

aligning their appetite of risk and the risk profile with its ability to gain in losses.

The board of directors of ADI has to the role to make sure that ADI maintains a degree and

quality of the capital commensurate with the amount, type and focus of risks to which ADI has

been exposed from their operations. In doing so, the board needs to have knowledge about the

changes that can be possible in the risk profile of ADI and the capital holdings.

The member of an ADI can be exposed to risks, inclusive of the contagion and reputational risk

through their relation with the other members of the group. The issues that arise in the group

members consist of the operational and financial position of ADI.

The measurement of capital adequacy can be found by explaining that APRA utilizes a tiered

method to the computation of an ADI’s adequacy of capital. It evaluates the financial strength of

ADI at three levels in order to make sure that the ADI is capitalized adequately both on a group

or an individual basis. The levels are:

The Prudential Standard APS 110 comprises of the various concepts that are useful for the

development of the capital management of an organization. This standard is under the section

11AF of the Banking Act 1959. This standard is applicable to all the permitted deposit taking

organizations with respect to the Banking Act that is subject to paragraph 3.

It is seen that with respect to the responsibility capital management, it is seen that capital has

been looked down upon as the cornerstone of the financial strength of an ADI. It aids the

operations of ADI by giving out a cushion to absorb the losses that have not been predicted from

their actions and in the event of the issues that enables the ADI to sustain to operate in a viable

and sound manner while the issues are resolved and addressed.

The capital management requires to be an integral part of the risk management of ADI by

aligning their appetite of risk and the risk profile with its ability to gain in losses.

The board of directors of ADI has to the role to make sure that ADI maintains a degree and

quality of the capital commensurate with the amount, type and focus of risks to which ADI has

been exposed from their operations. In doing so, the board needs to have knowledge about the

changes that can be possible in the risk profile of ADI and the capital holdings.

The member of an ADI can be exposed to risks, inclusive of the contagion and reputational risk

through their relation with the other members of the group. The issues that arise in the group

members consist of the operational and financial position of ADI.

The measurement of capital adequacy can be found by explaining that APRA utilizes a tiered

method to the computation of an ADI’s adequacy of capital. It evaluates the financial strength of

ADI at three levels in order to make sure that the ADI is capitalized adequately both on a group

or an individual basis. The levels are:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ASSESSMENT 2

Level 1-either:

The ADI itself or

The Extended Licensed Entity

Level 2- either

If the ADI is not a subordinate of a permitted NOHC and the ADI has subordinates in

addition to the ones that have been included in their ELE, the ADI consolidation of the

ADI and their subordinate entities other than the subsidiaries that have been non-

consolidated or

If ADI is a subordinate of a permitted NOHC, the consolidation of the imnmediate parent

NOHC of the ADI of all the immediate parent of the subsidiary entities of NOHC, other

than the non-consolidated subsidiaries, unless APRA ascertains a variant Level 2

composition for an association of comp[anise out of which ADI is a member

Level 3- the conglomerate group at the widest level

In accordance to the minimum capital adequacy requirements it is seen that APRA would

ascertain the Prudential Capital Requirements for an ADI. The PCRs explained as a

percentage of the overall risk-weighted assets, will be set by the reference to the Common

Equity Tier 1 Capital, Tier 1 Capital and Overall Capoital. The PCRs may be ascertained at

Level 1, level 2 or both. The minimum PCRs that ADI needs to maintain at all times are:

A tier 1 Capital ratio of 6%

A Common Equity Tier 1 Capital ratrio of 4.5%

Total capital. ratio of 8%.

Level 1-either:

The ADI itself or

The Extended Licensed Entity

Level 2- either

If the ADI is not a subordinate of a permitted NOHC and the ADI has subordinates in

addition to the ones that have been included in their ELE, the ADI consolidation of the

ADI and their subordinate entities other than the subsidiaries that have been non-

consolidated or

If ADI is a subordinate of a permitted NOHC, the consolidation of the imnmediate parent

NOHC of the ADI of all the immediate parent of the subsidiary entities of NOHC, other

than the non-consolidated subsidiaries, unless APRA ascertains a variant Level 2

composition for an association of comp[anise out of which ADI is a member

Level 3- the conglomerate group at the widest level

In accordance to the minimum capital adequacy requirements it is seen that APRA would

ascertain the Prudential Capital Requirements for an ADI. The PCRs explained as a

percentage of the overall risk-weighted assets, will be set by the reference to the Common

Equity Tier 1 Capital, Tier 1 Capital and Overall Capoital. The PCRs may be ascertained at

Level 1, level 2 or both. The minimum PCRs that ADI needs to maintain at all times are:

A tier 1 Capital ratio of 6%

A Common Equity Tier 1 Capital ratrio of 4.5%

Total capital. ratio of 8%.

5ASSESSMENT 2

The ADI requires to maintain a risk based capital ratios more than their PCRs at every time. The

risk based regulatory capital ratios are to be computed with respect to Attachment A.

The risk based capital adequacy ratio is consistent with Basel II and III as capital adequacy is

reliant on the risk based capital adequacy framework that has been set out in the Basel

Committee on the Banking Supervision’s Publications.

Q6. The three main decisions that companies face are given bellow.

How companies make decision?

(1) The Investment Decision

The investment decisions are undertaken by assessing the market along with the current financial

statement.

(2) The Finance Decisions

The financial decisions are undertaken by looking at the managerial finance and the decisions

associated with investment. The financial decisions are undertaken by looking at the demanders

and the suppliers of the fund, assessing the risks, the rates of interest and understanding the

financial framework of the firm. The financial decisions are undertaken by looking at the time

value of money and the risk and return trade-off.

(3). Dividend Decisions

The decisions with respect to the dividend is undertaken by gaining knowledge about the level of

profit the firm has attained in a year and the level of additional capital that is essential for the

development and expansion of the business of an organization.

The ADI requires to maintain a risk based capital ratios more than their PCRs at every time. The

risk based regulatory capital ratios are to be computed with respect to Attachment A.

The risk based capital adequacy ratio is consistent with Basel II and III as capital adequacy is

reliant on the risk based capital adequacy framework that has been set out in the Basel

Committee on the Banking Supervision’s Publications.

Q6. The three main decisions that companies face are given bellow.

How companies make decision?

(1) The Investment Decision

The investment decisions are undertaken by assessing the market along with the current financial

statement.

(2) The Finance Decisions

The financial decisions are undertaken by looking at the managerial finance and the decisions

associated with investment. The financial decisions are undertaken by looking at the demanders

and the suppliers of the fund, assessing the risks, the rates of interest and understanding the

financial framework of the firm. The financial decisions are undertaken by looking at the time

value of money and the risk and return trade-off.

(3). Dividend Decisions

The decisions with respect to the dividend is undertaken by gaining knowledge about the level of

profit the firm has attained in a year and the level of additional capital that is essential for the

development and expansion of the business of an organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ASSESSMENT 2

Q7. Research for each of the below products, identify which market structure (monopoly,

oligopoly, monopoly competition or perfect competition) each of the markets most closely

resembles, and why. The first has been done for you.

Product Example of Market

Practice

Market Structure Why?

TV Samsung Oligopoly Few participants

Price markers

Differentiated products

High barriers to entry

(significant R&D and

production costs)

Shares The ASX Monopoly One producer and no

reasonable substitute

Accounting

service

KPMG Perfect

Competition

Many buyers and sellers

Wool Independent farmers Monopolistic

Competition

Element of monopoly and

perfect competition

Cars Holder Oligopoly Few participants

Price markers

Differentiated products

High barriers to entry

Q7. Research for each of the below products, identify which market structure (monopoly,

oligopoly, monopoly competition or perfect competition) each of the markets most closely

resembles, and why. The first has been done for you.

Product Example of Market

Practice

Market Structure Why?

TV Samsung Oligopoly Few participants

Price markers

Differentiated products

High barriers to entry

(significant R&D and

production costs)

Shares The ASX Monopoly One producer and no

reasonable substitute

Accounting

service

KPMG Perfect

Competition

Many buyers and sellers

Wool Independent farmers Monopolistic

Competition

Element of monopoly and

perfect competition

Cars Holder Oligopoly Few participants

Price markers

Differentiated products

High barriers to entry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ASSESSMENT 2

Cinemas Event Cinemas Oligopoly Few participants

Price markers

Differentiated products

High barriers to entry

Q8. What is financial markets and what type of products and services they provide?

A financial market is a market in which individuals trade their financial bonds and securities,

products, and value at decreased transaction costs and at prices that replicate the supply and

demand. The securities are inclusive of the stocks and bonds, and the products include precious

metals or agricultural products.

Q9. Explain the key features of microeconomic principles and describe with example

Microeconomic Reform in Australia?

The key features of microeconomic principles are:

It is individualistic kind of economics.

It is related to the behavior of the individual economic entities like the firms, households

and markets.

It assumes the existence of full employment in the overall economy.

It assesses the economic phenomena under the assumption of ceteris paribus and

therefore is a process of partial equilibrium evaluation.

It is applicable under the market economy where price acts a core function.

Cinemas Event Cinemas Oligopoly Few participants

Price markers

Differentiated products

High barriers to entry

Q8. What is financial markets and what type of products and services they provide?

A financial market is a market in which individuals trade their financial bonds and securities,

products, and value at decreased transaction costs and at prices that replicate the supply and

demand. The securities are inclusive of the stocks and bonds, and the products include precious

metals or agricultural products.

Q9. Explain the key features of microeconomic principles and describe with example

Microeconomic Reform in Australia?

The key features of microeconomic principles are:

It is individualistic kind of economics.

It is related to the behavior of the individual economic entities like the firms, households

and markets.

It assumes the existence of full employment in the overall economy.

It assesses the economic phenomena under the assumption of ceteris paribus and

therefore is a process of partial equilibrium evaluation.

It is applicable under the market economy where price acts a core function.

8ASSESSMENT 2

It is even known that value or price theory.

Its aim has been to assess the method by which limited resources are assigned among the

alternative uses.

Its core aspects is the level of competition in the individual market.

Its fundamental variables are relative prices, supply, output, individual demand of the

singular companies and so on.

There are various microeconomic reforms that are seen in Australia and this can be explained

with the help of examples that have been given below:

Decrease in protectionism

Deregulation

IR reform

National Competition Policy

Rise in spending on capital of tertiary education

Q10. Explain key features of common economic theories that relate to the financial services

industry. Like:

(a)Supply Side Economics.

Supply side economics is a theory that is macroeconomic in nature that debates with the fact that

economic growth can be most efficiently established by reducing the level of taxes and lowering

the regulations. With respect to supply side economic, the consumers will then gain advantage

from a greater supply of services and goods at reduced prices and the level of employment will

rise.

It is even known that value or price theory.

Its aim has been to assess the method by which limited resources are assigned among the

alternative uses.

Its core aspects is the level of competition in the individual market.

Its fundamental variables are relative prices, supply, output, individual demand of the

singular companies and so on.

There are various microeconomic reforms that are seen in Australia and this can be explained

with the help of examples that have been given below:

Decrease in protectionism

Deregulation

IR reform

National Competition Policy

Rise in spending on capital of tertiary education

Q10. Explain key features of common economic theories that relate to the financial services

industry. Like:

(a)Supply Side Economics.

Supply side economics is a theory that is macroeconomic in nature that debates with the fact that

economic growth can be most efficiently established by reducing the level of taxes and lowering

the regulations. With respect to supply side economic, the consumers will then gain advantage

from a greater supply of services and goods at reduced prices and the level of employment will

rise.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ASSESSMENT 2

(b) The Global Financial Crisis

The global financial crisis is even known to be the worst financial crisis after the Great

Depression and this crisis took place due to the crisis in the mortgage market in the market of

USA and later turned into a fully developed international banking crisis with the down fall of the

investment banks globally. This crisis later was followed by economic turndown which was

known as the Great Recession. There was a massive fall in the global economy and this led to

rise in unemployment and fall in the global GDP.

(c) Value Theory

The term value theory can be used in three various ways in the philosophy. Value theory is a

catchy label that is used for the cover all the branches of the social moral and political

philosophy and the areas that would be used for the areas that are associated with the evaluative

aspect. In its shortest sense, value theory is utilized for a generally narrow area of the normative

ethical theory specifically but not exclusively of concern to the consequentialists.

Q11. Describe key features of relevant legislation, statutory requirements and industry codes of

practice for financial service industry.

The key features of relevant legislation, statutory requirements and industry codes of practice for

financial service industry are:

Legislation regulations

Source documents for regulations, legislations and policies that are precise to the provision of

financial services and products that are accessed and sourced. The key legal principles and the

organizational applications associating to the financial product and services provisions are

(b) The Global Financial Crisis

The global financial crisis is even known to be the worst financial crisis after the Great

Depression and this crisis took place due to the crisis in the mortgage market in the market of

USA and later turned into a fully developed international banking crisis with the down fall of the

investment banks globally. This crisis later was followed by economic turndown which was

known as the Great Recession. There was a massive fall in the global economy and this led to

rise in unemployment and fall in the global GDP.

(c) Value Theory

The term value theory can be used in three various ways in the philosophy. Value theory is a

catchy label that is used for the cover all the branches of the social moral and political

philosophy and the areas that would be used for the areas that are associated with the evaluative

aspect. In its shortest sense, value theory is utilized for a generally narrow area of the normative

ethical theory specifically but not exclusively of concern to the consequentialists.

Q11. Describe key features of relevant legislation, statutory requirements and industry codes of

practice for financial service industry.

The key features of relevant legislation, statutory requirements and industry codes of practice for

financial service industry are:

Legislation regulations

Source documents for regulations, legislations and policies that are precise to the provision of

financial services and products that are accessed and sourced. The key legal principles and the

organizational applications associating to the financial product and services provisions are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ASSESSMENT 2

communicated and assessed. The organizational requirements of these documents and their

impact on the working practices are recognized with respect to the procedural needs. The

procedural requirements associating to the operational components of regulations and laws and

the practice codes are executed in line with the organizational policy. The role authorities and the

limitations are recognized in the position profiles are complied with. The mechanism is created

to make sure that currency of regulatory literature is maintained.

Statutory records

It is seen that precise records are maintained and the copies of any precise agreements are

maintained in the file. The evidence with respect to present authorization, licenses and training

are maintained with respect to the legal, organizational and regulatory needs.

Industry Codes

The precise industry codes are accessed, sourced and applied to their own work with respect to

the organizational needs. The essential principles and accountabilities are translated with respect

to the industry codes of practice with own translation and application of the industry codes of the

practices confirmed and clarified as needed with the precise individuals. The effect of the codes

of practices on the working mechanism is incorporated and understood.

Q12. What do you understand by the economic and political climate change? Describe the

economic and political climate change relating to the financial services industry.

The political economy of climate change is a process that is applicable to the political economy

that looks for political and collective processes to examine the critical issues that surrounds the

decision making process on the change in climate.

communicated and assessed. The organizational requirements of these documents and their

impact on the working practices are recognized with respect to the procedural needs. The

procedural requirements associating to the operational components of regulations and laws and

the practice codes are executed in line with the organizational policy. The role authorities and the

limitations are recognized in the position profiles are complied with. The mechanism is created

to make sure that currency of regulatory literature is maintained.

Statutory records

It is seen that precise records are maintained and the copies of any precise agreements are

maintained in the file. The evidence with respect to present authorization, licenses and training

are maintained with respect to the legal, organizational and regulatory needs.

Industry Codes

The precise industry codes are accessed, sourced and applied to their own work with respect to

the organizational needs. The essential principles and accountabilities are translated with respect

to the industry codes of practice with own translation and application of the industry codes of the

practices confirmed and clarified as needed with the precise individuals. The effect of the codes

of practices on the working mechanism is incorporated and understood.

Q12. What do you understand by the economic and political climate change? Describe the

economic and political climate change relating to the financial services industry.

The political economy of climate change is a process that is applicable to the political economy

that looks for political and collective processes to examine the critical issues that surrounds the

decision making process on the change in climate.

11ASSESSMENT 2

It is seen that argumentative transformations in economic scenarios and in the political climate

could have a material impact on the business, financial scenario and outcomes of the liquidity

and activities. The business environment is attracted by various uncertainties that are political in

nature and this would sustain to have an impact in the global economy and the capital market

functioning globally. During the time of sloth economic growth or fall the customers are more

likely to reduce their expenses on the kinds of systems and products that are supplied and are

more likely to experience reduced revenues as a consequence.

Assessment 2

The Big Issues in Australian Economy

Introduction

The Australian economy is considered as one of the predominant economies in the world

and has shown impressive developments in every aspect over the years. However, in the last few

years, the economy has gone back a bit, as shown in the concerned article. There are several

reasons behind this not so impressive performance of the economy of Australia, one of the

primary one being the election and the unsure attitudes of the residents and their risk adverse

attitude. Though there are expectations regarding the economy to cope up in near future, there

are several other concerning issues, which contribute to this stagnating, condition of the country

and poses a threat to the expectations of bouncing back(Dyster and Meredith2012).

It is seen that argumentative transformations in economic scenarios and in the political climate

could have a material impact on the business, financial scenario and outcomes of the liquidity

and activities. The business environment is attracted by various uncertainties that are political in

nature and this would sustain to have an impact in the global economy and the capital market

functioning globally. During the time of sloth economic growth or fall the customers are more

likely to reduce their expenses on the kinds of systems and products that are supplied and are

more likely to experience reduced revenues as a consequence.

Assessment 2

The Big Issues in Australian Economy

Introduction

The Australian economy is considered as one of the predominant economies in the world

and has shown impressive developments in every aspect over the years. However, in the last few

years, the economy has gone back a bit, as shown in the concerned article. There are several

reasons behind this not so impressive performance of the economy of Australia, one of the

primary one being the election and the unsure attitudes of the residents and their risk adverse

attitude. Though there are expectations regarding the economy to cope up in near future, there

are several other concerning issues, which contribute to this stagnating, condition of the country

and poses a threat to the expectations of bouncing back(Dyster and Meredith2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.