FNSACC301 Financial Accounting: Processing Transactions & Reporting

VerifiedAdded on 2023/06/11

|20

|3931

|220

Homework Assignment

AI Summary

This financial accounting assignment focuses on analyzing financial transactions and extracting interim reports. It includes questions related to petty cash vouchers, security safeguards for depositing cash, key features of trial balance and balance sheets, and the accounting standard AASB 101 governing the presentation of financial statements. The assignment also covers specialized journal exercises, identifying journals for recording transactions, and entering transactions into appropriate journals. The student work also includes declaration of originality and the assessment outcome.

[Financial Accounting] – Final Exam

Details of Assessment

Term and Year T4 2017 Time allowed Week 1-8

Assessment No 3

Assessment type Assignment Assessment Weighting [30%]

Date Week 8 Room 609

Details of Subject

Qualification FNS40615 Certificate IV in Accounting

Subject Name Financial Accounting

Details of Unit(s) of competency

Unit Code FNSACC301A

BSBFIA401

Unit Title Process financial transactions and extract interim reports

Prepare financial reports

Details of Student

Student Name Student ID

College

Student Declaration: I declare that the work

submitted is my own, and has not been copied or

plagiarised from any person or source.

Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name Kaneez Selim/Ali Kauser

Assessor’s Signature Date

Assessment Outcome

Results Satisfactory Not Satisfactory

Marks/Grade / 30

Reasonable Adjustments (if

applicable)

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

_______________________________________________________________________________________________

_______________________________________________________________________________________________

_______________________________________________________________________________________________

_______________________________________________________________________________________________

____

[Financial Accounting] Page 1 QMS-AT-v2/0513

Details of Assessment

Term and Year T4 2017 Time allowed Week 1-8

Assessment No 3

Assessment type Assignment Assessment Weighting [30%]

Date Week 8 Room 609

Details of Subject

Qualification FNS40615 Certificate IV in Accounting

Subject Name Financial Accounting

Details of Unit(s) of competency

Unit Code FNSACC301A

BSBFIA401

Unit Title Process financial transactions and extract interim reports

Prepare financial reports

Details of Student

Student Name Student ID

College

Student Declaration: I declare that the work

submitted is my own, and has not been copied or

plagiarised from any person or source.

Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name Kaneez Selim/Ali Kauser

Assessor’s Signature Date

Assessment Outcome

Results Satisfactory Not Satisfactory

Marks/Grade / 30

Reasonable Adjustments (if

applicable)

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

_______________________________________________________________________________________________

_______________________________________________________________________________________________

_______________________________________________________________________________________________

_______________________________________________________________________________________________

____

[Financial Accounting] Page 1 QMS-AT-v2/0513

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

[Financial Accounting] – Final Exam

Student Declaration: I declare that I have been assessed

in this unit, and I have been advised of my result. I also

am aware of my appeal rights and reassessment

procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have conducted a

fair, valid, reliable and flexible assessment with this

student, and I have provided appropriate feedback

Signature: ____________________________

Date: ____/_____/_____

Purpose of the Assessment FNSACC301

The purpose of this assessment is to assess the student in the following learning elements

and performance criteria of the unit:

Assessment task

1: portfolio of

activities (Task

numbers)

Competent

(C)

Not yet

competent

(NYC)

Element 1: Check and verify supporting documentation

1.1 Identify, check and record information from documents 1

Element 2: Prepare and process banking and petty cash documents

2.1 Enter accurately and balance deposits and withdrawals according to

organisational procedures

2.3 Reconcile banking documentation with organisation’s financial records 3

2.4 Check, process and record petty cash claims and vouchers, and balance petty

cash book according to organisational procedures

Element 4: Prepare and post journals and batch monetary items

4.1 Prepare journals accurately and completely, and batch items within

organisational timelines

2

4.2 Match batch items precisely to initial receipt records

4.3 Ensure journals are authorised by appropriate person and process in accordance

with organisational policy and procedures

Element 5: Post journals to ledger

5.1 Post journals accurately to ledger in accordance with organisational input

standards, with transactions correctly allocated to system and accounts

Element 6: Enter data into system

6.1 Enter data accurately into system in accordance with organisational input

standards and correctly allocate transactions to system and accounts

3

6.2 Update related systems to maintain integrity of relationships between financial

systems

Element 7: Prepare deposit facility and lodge flows

7.1 Select deposit facility appropriate to banking method to be used 1

7.2 Balance batch with deposit facility without error

[Financial Accounting] Page 2 QMS-AT-v2/0513

Student Declaration: I declare that I have been assessed

in this unit, and I have been advised of my result. I also

am aware of my appeal rights and reassessment

procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have conducted a

fair, valid, reliable and flexible assessment with this

student, and I have provided appropriate feedback

Signature: ____________________________

Date: ____/_____/_____

Purpose of the Assessment FNSACC301

The purpose of this assessment is to assess the student in the following learning elements

and performance criteria of the unit:

Assessment task

1: portfolio of

activities (Task

numbers)

Competent

(C)

Not yet

competent

(NYC)

Element 1: Check and verify supporting documentation

1.1 Identify, check and record information from documents 1

Element 2: Prepare and process banking and petty cash documents

2.1 Enter accurately and balance deposits and withdrawals according to

organisational procedures

2.3 Reconcile banking documentation with organisation’s financial records 3

2.4 Check, process and record petty cash claims and vouchers, and balance petty

cash book according to organisational procedures

Element 4: Prepare and post journals and batch monetary items

4.1 Prepare journals accurately and completely, and batch items within

organisational timelines

2

4.2 Match batch items precisely to initial receipt records

4.3 Ensure journals are authorised by appropriate person and process in accordance

with organisational policy and procedures

Element 5: Post journals to ledger

5.1 Post journals accurately to ledger in accordance with organisational input

standards, with transactions correctly allocated to system and accounts

Element 6: Enter data into system

6.1 Enter data accurately into system in accordance with organisational input

standards and correctly allocate transactions to system and accounts

3

6.2 Update related systems to maintain integrity of relationships between financial

systems

Element 7: Prepare deposit facility and lodge flows

7.1 Select deposit facility appropriate to banking method to be used 1

7.2 Balance batch with deposit facility without error

[Financial Accounting] Page 2 QMS-AT-v2/0513

[Financial Accounting] – Final Exam

7.3 Take security and safety precautions appropriate to method of banking, in

accordance with organisational policy and industry and legislative requirements

1

7.4 Obtain and file proof of lodgement so that it is easily accessible and traceable 1

Element 8: Extract a trial balance and interim reports

8.2 Complete cash and credit journals and post to general ledger 2

8.3 Extract and check trial balance and prepare other required reports

Purpose of the Assessment BSBFIA401

The purpose of this assessment is to assess the student in the

following learning elements and performance criteria of the unit:

Assessment task 2: Assignment

(Task numbers)

Satisfactory (S) Not Yet Satisfactory

(NYC)

Element 1: [Maintain asset register]

1.1 Prepare a register of property, plant and equipment from fixed asset

transactions in accordance with organisational policy and procedures

5

1.2 Determine method of calculating depreciation in accordance with

organisational requirements

Element 2: [Record general journal entries for balance day adjustments]

2.1. Record depreciation of non-current assets and disposal of fixed

assets in accordance with organisational policy, procedures and

accounting requirements

2.2Adjust expense accounts and revenue accounts for prepayments

and accruals

2.3. Record bad and doubtful debts in accordance with

organizational policy, procedures and accounting requirements

2.4. Adjust ledger accounts for inventories, if required, and

transfer to final accounts

Element 3: [Prepare final general ledger accounts]

3.1 Make general journal entries for balance day adjustments in general

ledger system in accordance with organisational policy, procedures and

accounting requirements

3.2 Post revenue and expense account balances to final general ledger

accounts system

6

3.3Prepare final general ledger accounts to reflect gross and net profits

for reporting period

6

Element 4: [Prepare end of period financial reports]

4.1 Prepare revenue statement in accordance with organisational

requirements to reflect operating profit for reporting period

6

4.3 Identify and correct, or refer errors for resolution in accordance with

organisational policy and procedures

4

Assessment/evidence gathering conditions

Each assessment component is recorded as either Satisfactory (S) or Not Satisfactory (NS). A student can only achieve

competence when all assessment components listed under Purpose of the assessment section are Satisfactory. Your

trainer will give you feedback after the completion of each assessment. A student who is assessed as NS (Not

Satisfactory) is eligible for re-assessment.

Resources required for this Assessment

[Financial Accounting] Page 3 QMS-AT-v2/0513

7.3 Take security and safety precautions appropriate to method of banking, in

accordance with organisational policy and industry and legislative requirements

1

7.4 Obtain and file proof of lodgement so that it is easily accessible and traceable 1

Element 8: Extract a trial balance and interim reports

8.2 Complete cash and credit journals and post to general ledger 2

8.3 Extract and check trial balance and prepare other required reports

Purpose of the Assessment BSBFIA401

The purpose of this assessment is to assess the student in the

following learning elements and performance criteria of the unit:

Assessment task 2: Assignment

(Task numbers)

Satisfactory (S) Not Yet Satisfactory

(NYC)

Element 1: [Maintain asset register]

1.1 Prepare a register of property, plant and equipment from fixed asset

transactions in accordance with organisational policy and procedures

5

1.2 Determine method of calculating depreciation in accordance with

organisational requirements

Element 2: [Record general journal entries for balance day adjustments]

2.1. Record depreciation of non-current assets and disposal of fixed

assets in accordance with organisational policy, procedures and

accounting requirements

2.2Adjust expense accounts and revenue accounts for prepayments

and accruals

2.3. Record bad and doubtful debts in accordance with

organizational policy, procedures and accounting requirements

2.4. Adjust ledger accounts for inventories, if required, and

transfer to final accounts

Element 3: [Prepare final general ledger accounts]

3.1 Make general journal entries for balance day adjustments in general

ledger system in accordance with organisational policy, procedures and

accounting requirements

3.2 Post revenue and expense account balances to final general ledger

accounts system

6

3.3Prepare final general ledger accounts to reflect gross and net profits

for reporting period

6

Element 4: [Prepare end of period financial reports]

4.1 Prepare revenue statement in accordance with organisational

requirements to reflect operating profit for reporting period

6

4.3 Identify and correct, or refer errors for resolution in accordance with

organisational policy and procedures

4

Assessment/evidence gathering conditions

Each assessment component is recorded as either Satisfactory (S) or Not Satisfactory (NS). A student can only achieve

competence when all assessment components listed under Purpose of the assessment section are Satisfactory. Your

trainer will give you feedback after the completion of each assessment. A student who is assessed as NS (Not

Satisfactory) is eligible for re-assessment.

Resources required for this Assessment

[Financial Accounting] Page 3 QMS-AT-v2/0513

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

[Financial Accounting] – Final Exam

Upon completion, submit the assessment copy to your trainer along with assessment coversheet.

Refer to the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer, if needed

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will

be provided with feedback on your work within two weeks of the assessment due date. All other feedback will be

provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment for more information (Student handbook).

[Financial Accounting] Page 4 QMS-AT-v2/0513

Upon completion, submit the assessment copy to your trainer along with assessment coversheet.

Refer to the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer, if needed

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will

be provided with feedback on your work within two weeks of the assessment due date. All other feedback will be

provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment for more information (Student handbook).

[Financial Accounting] Page 4 QMS-AT-v2/0513

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

[Financial Accounting] – Final Exam

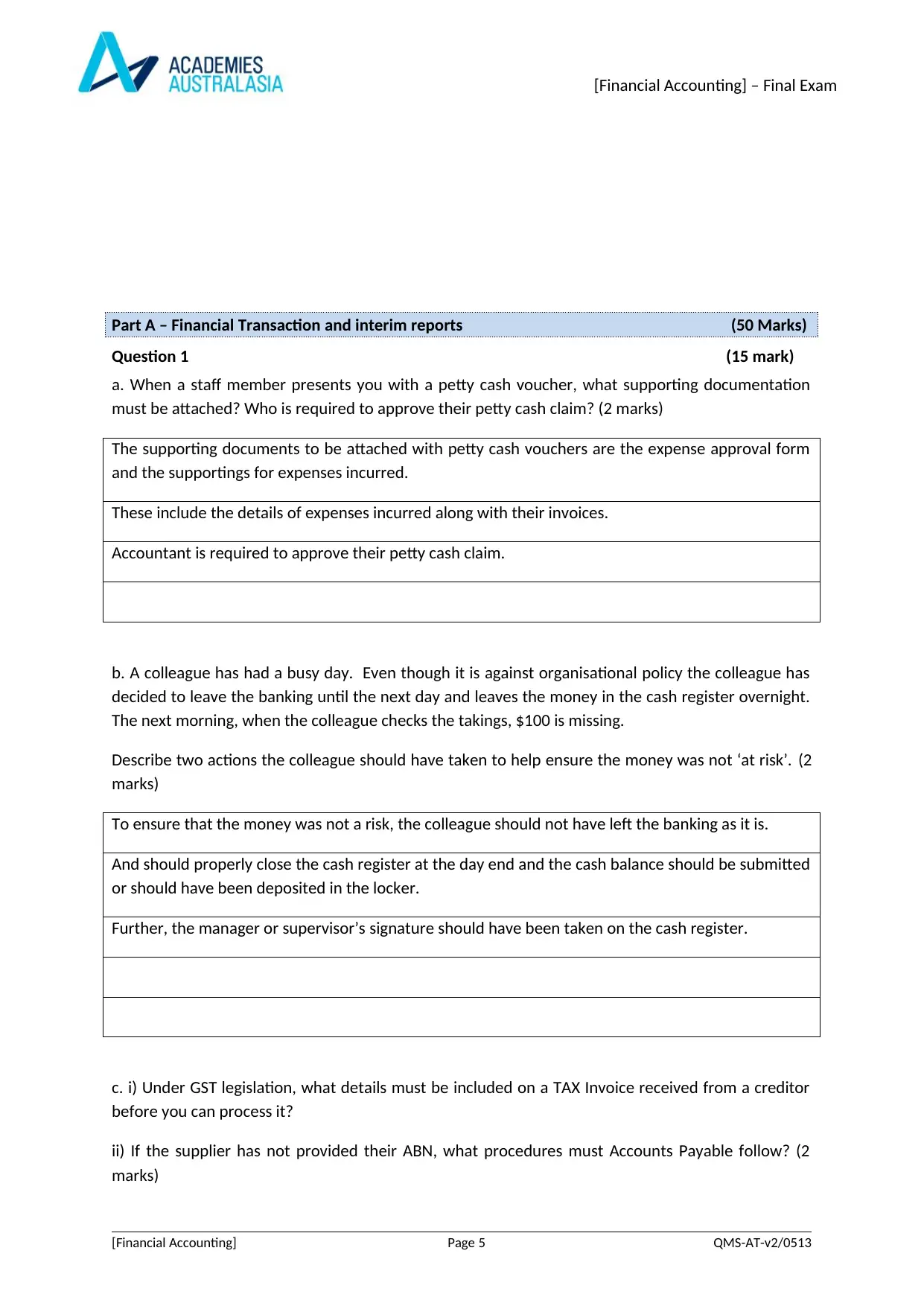

Part A – Financial Transaction and interim reports (50 Marks)

Question 1 (15 mark)

a. When a staff member presents you with a petty cash voucher, what supporting documentation

must be attached? Who is required to approve their petty cash claim? (2 marks)

The supporting documents to be attached with petty cash vouchers are the expense approval form

and the supportings for expenses incurred.

These include the details of expenses incurred along with their invoices.

Accountant is required to approve their petty cash claim.

b. A colleague has had a busy day. Even though it is against organisational policy the colleague has

decided to leave the banking until the next day and leaves the money in the cash register overnight.

The next morning, when the colleague checks the takings, $100 is missing.

Describe two actions the colleague should have taken to help ensure the money was not ‘at risk’. (2

marks)

To ensure that the money was not a risk, the colleague should not have left the banking as it is.

And should properly close the cash register at the day end and the cash balance should be submitted

or should have been deposited in the locker.

Further, the manager or supervisor’s signature should have been taken on the cash register.

c. i) Under GST legislation, what details must be included on a TAX Invoice received from a creditor

before you can process it?

ii) If the supplier has not provided their ABN, what procedures must Accounts Payable follow? (2

marks)

[Financial Accounting] Page 5 QMS-AT-v2/0513

Part A – Financial Transaction and interim reports (50 Marks)

Question 1 (15 mark)

a. When a staff member presents you with a petty cash voucher, what supporting documentation

must be attached? Who is required to approve their petty cash claim? (2 marks)

The supporting documents to be attached with petty cash vouchers are the expense approval form

and the supportings for expenses incurred.

These include the details of expenses incurred along with their invoices.

Accountant is required to approve their petty cash claim.

b. A colleague has had a busy day. Even though it is against organisational policy the colleague has

decided to leave the banking until the next day and leaves the money in the cash register overnight.

The next morning, when the colleague checks the takings, $100 is missing.

Describe two actions the colleague should have taken to help ensure the money was not ‘at risk’. (2

marks)

To ensure that the money was not a risk, the colleague should not have left the banking as it is.

And should properly close the cash register at the day end and the cash balance should be submitted

or should have been deposited in the locker.

Further, the manager or supervisor’s signature should have been taken on the cash register.

c. i) Under GST legislation, what details must be included on a TAX Invoice received from a creditor

before you can process it?

ii) If the supplier has not provided their ABN, what procedures must Accounts Payable follow? (2

marks)

[Financial Accounting] Page 5 QMS-AT-v2/0513

[Financial Accounting] – Final Exam

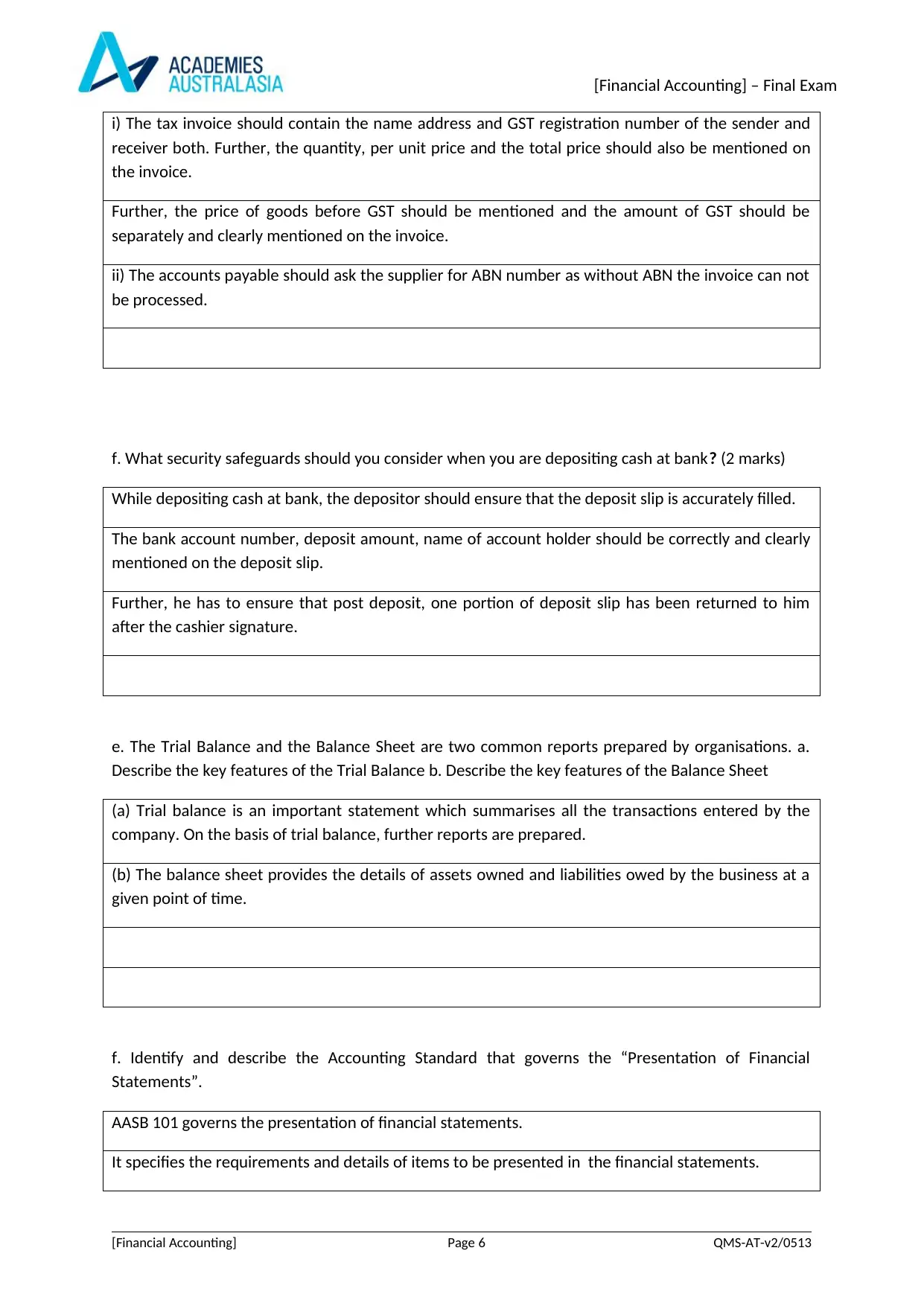

i) The tax invoice should contain the name address and GST registration number of the sender and

receiver both. Further, the quantity, per unit price and the total price should also be mentioned on

the invoice.

Further, the price of goods before GST should be mentioned and the amount of GST should be

separately and clearly mentioned on the invoice.

ii) The accounts payable should ask the supplier for ABN number as without ABN the invoice can not

be processed.

f. What security safeguards should you consider when you are depositing cash at bank? (2 marks)

While depositing cash at bank, the depositor should ensure that the deposit slip is accurately filled.

The bank account number, deposit amount, name of account holder should be correctly and clearly

mentioned on the deposit slip.

Further, he has to ensure that post deposit, one portion of deposit slip has been returned to him

after the cashier signature.

e. The Trial Balance and the Balance Sheet are two common reports prepared by organisations. a.

Describe the key features of the Trial Balance b. Describe the key features of the Balance Sheet

(a) Trial balance is an important statement which summarises all the transactions entered by the

company. On the basis of trial balance, further reports are prepared.

(b) The balance sheet provides the details of assets owned and liabilities owed by the business at a

given point of time.

f. Identify and describe the Accounting Standard that governs the “Presentation of Financial

Statements”.

AASB 101 governs the presentation of financial statements.

It specifies the requirements and details of items to be presented in the financial statements.

[Financial Accounting] Page 6 QMS-AT-v2/0513

i) The tax invoice should contain the name address and GST registration number of the sender and

receiver both. Further, the quantity, per unit price and the total price should also be mentioned on

the invoice.

Further, the price of goods before GST should be mentioned and the amount of GST should be

separately and clearly mentioned on the invoice.

ii) The accounts payable should ask the supplier for ABN number as without ABN the invoice can not

be processed.

f. What security safeguards should you consider when you are depositing cash at bank? (2 marks)

While depositing cash at bank, the depositor should ensure that the deposit slip is accurately filled.

The bank account number, deposit amount, name of account holder should be correctly and clearly

mentioned on the deposit slip.

Further, he has to ensure that post deposit, one portion of deposit slip has been returned to him

after the cashier signature.

e. The Trial Balance and the Balance Sheet are two common reports prepared by organisations. a.

Describe the key features of the Trial Balance b. Describe the key features of the Balance Sheet

(a) Trial balance is an important statement which summarises all the transactions entered by the

company. On the basis of trial balance, further reports are prepared.

(b) The balance sheet provides the details of assets owned and liabilities owed by the business at a

given point of time.

f. Identify and describe the Accounting Standard that governs the “Presentation of Financial

Statements”.

AASB 101 governs the presentation of financial statements.

It specifies the requirements and details of items to be presented in the financial statements.

[Financial Accounting] Page 6 QMS-AT-v2/0513

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

[Financial Accounting] – Final Exam

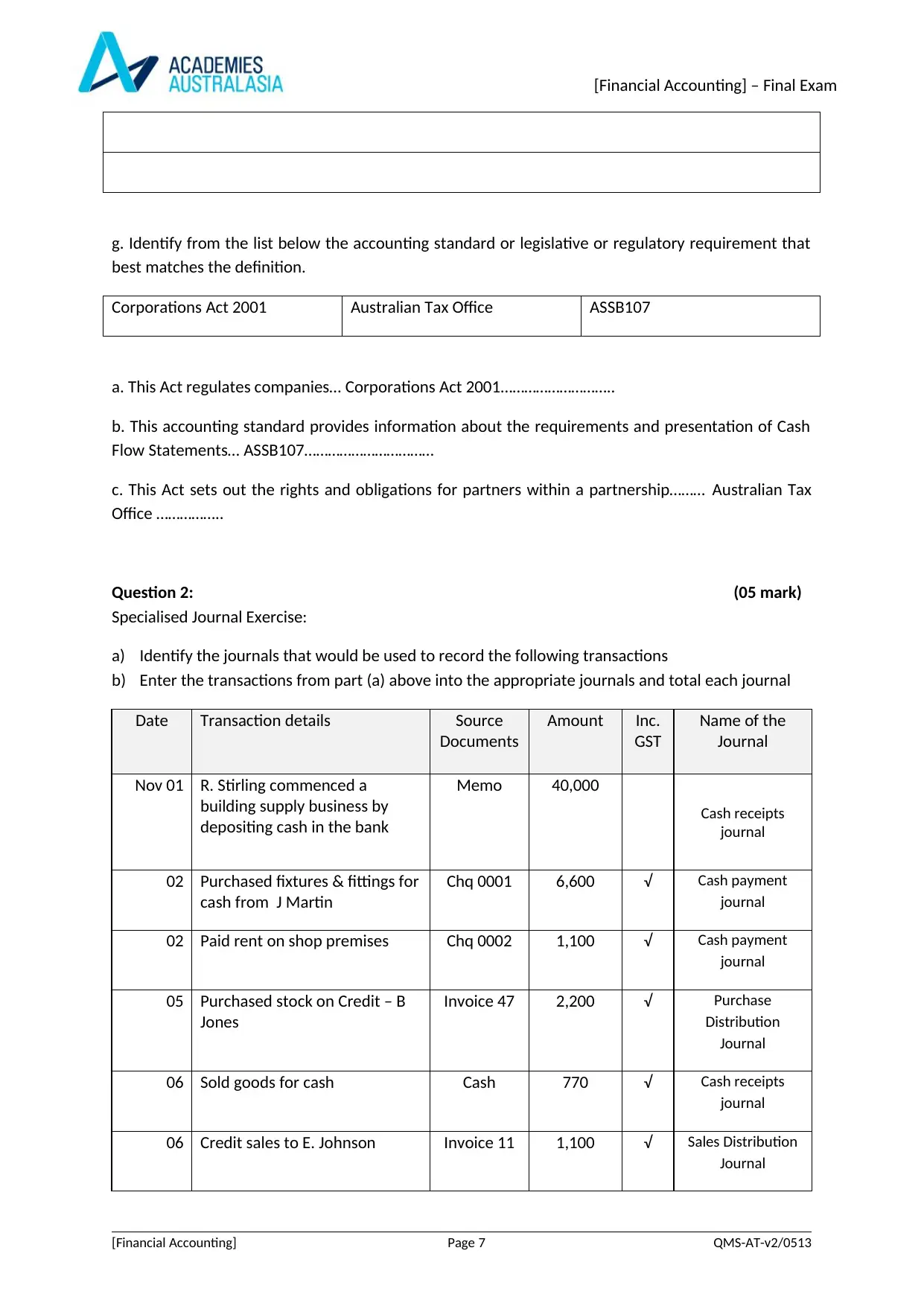

g. Identify from the list below the accounting standard or legislative or regulatory requirement that

best matches the definition.

Corporations Act 2001 Australian Tax Office ASSB107

a. This Act regulates companies… Corporations Act 2001………………………..

b. This accounting standard provides information about the requirements and presentation of Cash

Flow Statements… ASSB107……………………………

c. This Act sets out the rights and obligations for partners within a partnership……… Australian Tax

Office ……………..

Question 2: (05 mark)

Specialised Journal Exercise:

a) Identify the journals that would be used to record the following transactions

b) Enter the transactions from part (a) above into the appropriate journals and total each journal

Date Transaction details Source

Documents

Amount Inc.

GST

Name of the

Journal

Nov 01 R. Stirling commenced a

building supply business by

depositing cash in the bank

Memo 40,000

Cash receipts

journal

02 Purchased fixtures & fittings for

cash from J Martin

Chq 0001 6,600 √ Cash payment

journal

02 Paid rent on shop premises Chq 0002 1,100 √ Cash payment

journal

05 Purchased stock on Credit – B

Jones

Invoice 47 2,200 √ Purchase

Distribution

Journal

06 Sold goods for cash Cash 770 √ Cash receipts

journal

06 Credit sales to E. Johnson Invoice 11 1,100 √ Sales Distribution

Journal

[Financial Accounting] Page 7 QMS-AT-v2/0513

g. Identify from the list below the accounting standard or legislative or regulatory requirement that

best matches the definition.

Corporations Act 2001 Australian Tax Office ASSB107

a. This Act regulates companies… Corporations Act 2001………………………..

b. This accounting standard provides information about the requirements and presentation of Cash

Flow Statements… ASSB107……………………………

c. This Act sets out the rights and obligations for partners within a partnership……… Australian Tax

Office ……………..

Question 2: (05 mark)

Specialised Journal Exercise:

a) Identify the journals that would be used to record the following transactions

b) Enter the transactions from part (a) above into the appropriate journals and total each journal

Date Transaction details Source

Documents

Amount Inc.

GST

Name of the

Journal

Nov 01 R. Stirling commenced a

building supply business by

depositing cash in the bank

Memo 40,000

Cash receipts

journal

02 Purchased fixtures & fittings for

cash from J Martin

Chq 0001 6,600 √ Cash payment

journal

02 Paid rent on shop premises Chq 0002 1,100 √ Cash payment

journal

05 Purchased stock on Credit – B

Jones

Invoice 47 2,200 √ Purchase

Distribution

Journal

06 Sold goods for cash Cash 770 √ Cash receipts

journal

06 Credit sales to E. Johnson Invoice 11 1,100 √ Sales Distribution

Journal

[Financial Accounting] Page 7 QMS-AT-v2/0513

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

[Financial Accounting] – Final Exam

09 Paid wages Chq 0003 650 Cash payment

journal

09 Sold goods to F Black Invoice 12 704 √ Sales Distribution

Journal

10 Cash sales Cash 2,750 √ Cash receipts

journal

13 Paid television advertising Chq 0004 2,420 √ Cash payment

journal

14 Cash sales Cash 1,320 √ Cash receipts

journal

14 Sales to E. Thomson Invoice 13 550 √ Sales Distribution

Journal

16 Sales to D Brown Invoice 14 825 √ Sales Distribution

Journal

16 Purchases from P. Plummer Invoice 687 792 √ Purchase

Distribution

Journal

17 Cash purchases Chq 0005 1,650 √ Cash payment

journal

17 Paid wages Chq 0006 450 Cash payment

journal

21 Cash purchases Chq 0007 1,265 √ Cash payment

journal

21 Cash sales Cash 2,200 √ Cash receipts

journal

25 Credit sales to E. Green Invoice 15 880 √ Sales Distribution

Journal

27 Received cash from F Black for

payment of account in full

Receipt 01 704 Cash receipts

journal

28 Paid bank interest Chq 0008 250 Cash payment

journal

[Financial Accounting] Page 8 QMS-AT-v2/0513

09 Paid wages Chq 0003 650 Cash payment

journal

09 Sold goods to F Black Invoice 12 704 √ Sales Distribution

Journal

10 Cash sales Cash 2,750 √ Cash receipts

journal

13 Paid television advertising Chq 0004 2,420 √ Cash payment

journal

14 Cash sales Cash 1,320 √ Cash receipts

journal

14 Sales to E. Thomson Invoice 13 550 √ Sales Distribution

Journal

16 Sales to D Brown Invoice 14 825 √ Sales Distribution

Journal

16 Purchases from P. Plummer Invoice 687 792 √ Purchase

Distribution

Journal

17 Cash purchases Chq 0005 1,650 √ Cash payment

journal

17 Paid wages Chq 0006 450 Cash payment

journal

21 Cash purchases Chq 0007 1,265 √ Cash payment

journal

21 Cash sales Cash 2,200 √ Cash receipts

journal

25 Credit sales to E. Green Invoice 15 880 √ Sales Distribution

Journal

27 Received cash from F Black for

payment of account in full

Receipt 01 704 Cash receipts

journal

28 Paid bank interest Chq 0008 250 Cash payment

journal

[Financial Accounting] Page 8 QMS-AT-v2/0513

[Financial Accounting] – Final Exam

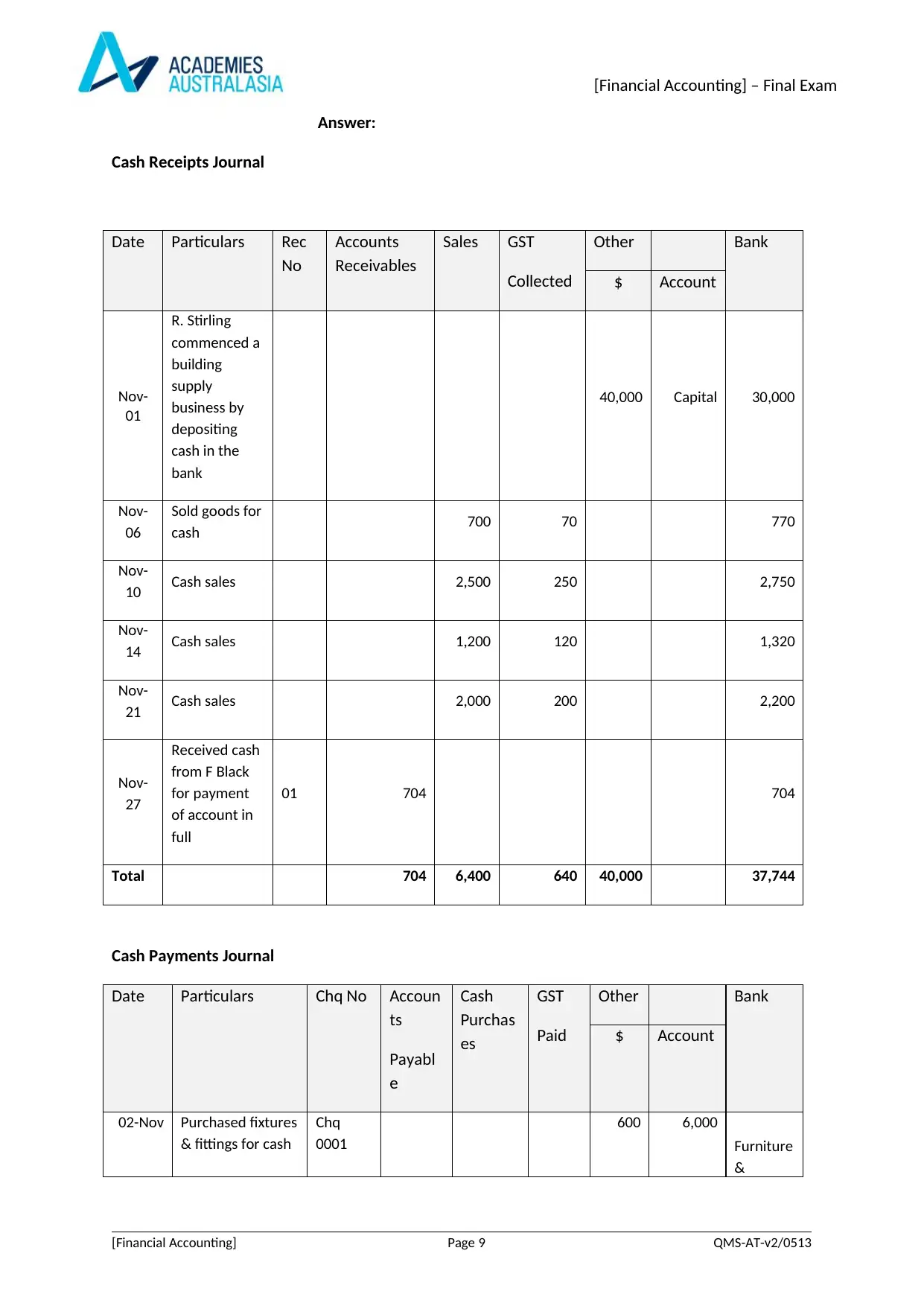

Answer:

Cash Receipts Journal

Date Particulars Rec

No

Accounts

Receivables

Sales GST

Collected

Other Bank

$ Account

Nov-

01

R. Stirling

commenced a

building

supply

business by

depositing

cash in the

bank

40,000 Capital 30,000

Nov-

06

Sold goods for

cash 700 70 770

Nov-

10 Cash sales 2,500 250 2,750

Nov-

14 Cash sales 1,200 120 1,320

Nov-

21 Cash sales 2,000 200 2,200

Nov-

27

Received cash

from F Black

for payment

of account in

full

01 704 704

Total 704 6,400 640 40,000 37,744

Cash Payments Journal

Date Particulars Chq No Accoun

ts

Payabl

e

Cash

Purchas

es

GST

Paid

Other Bank

$ Account

02-Nov Purchased fixtures

& fittings for cash

Chq

0001

600 6,000

Furniture

&

[Financial Accounting] Page 9 QMS-AT-v2/0513

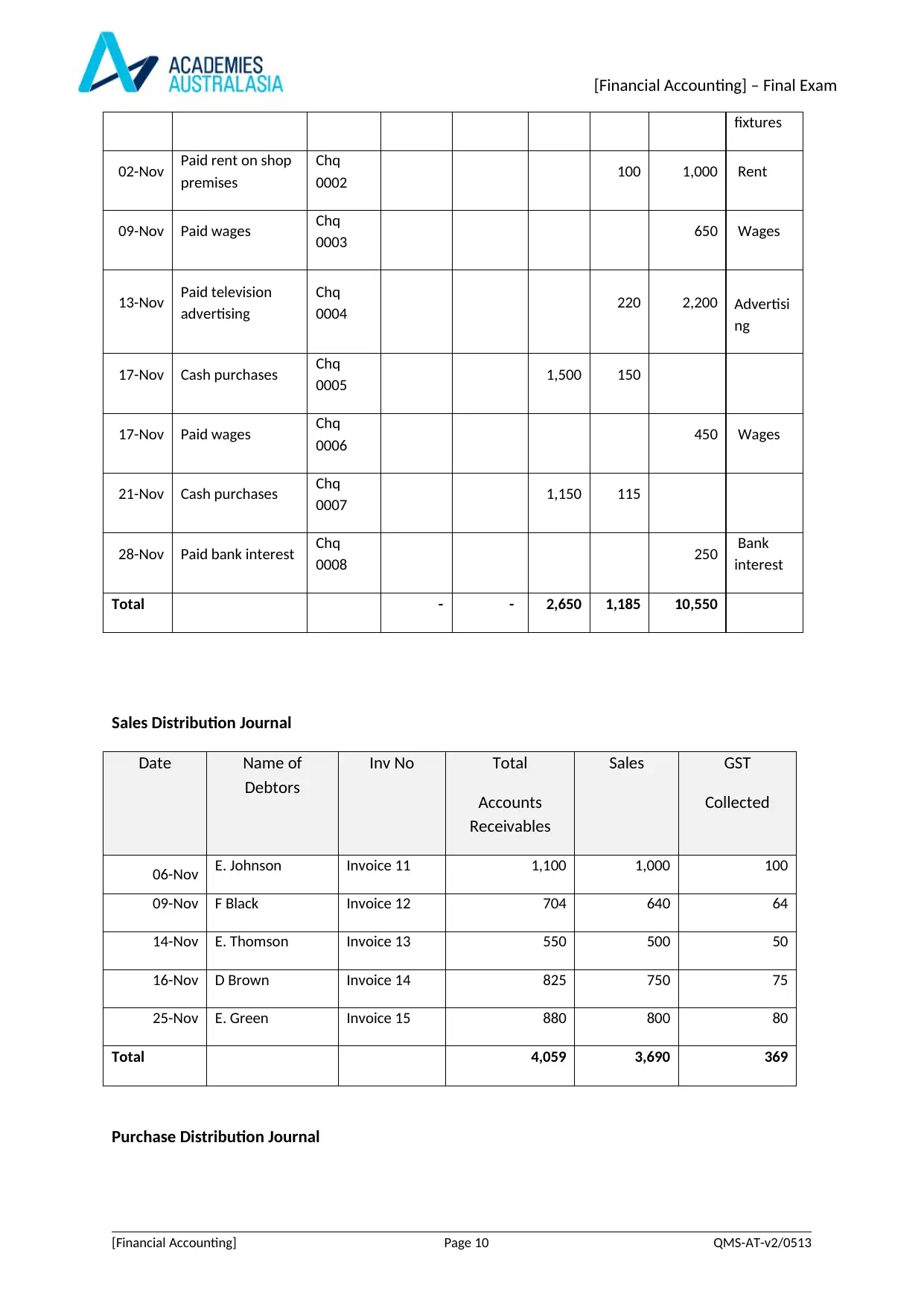

Answer:

Cash Receipts Journal

Date Particulars Rec

No

Accounts

Receivables

Sales GST

Collected

Other Bank

$ Account

Nov-

01

R. Stirling

commenced a

building

supply

business by

depositing

cash in the

bank

40,000 Capital 30,000

Nov-

06

Sold goods for

cash 700 70 770

Nov-

10 Cash sales 2,500 250 2,750

Nov-

14 Cash sales 1,200 120 1,320

Nov-

21 Cash sales 2,000 200 2,200

Nov-

27

Received cash

from F Black

for payment

of account in

full

01 704 704

Total 704 6,400 640 40,000 37,744

Cash Payments Journal

Date Particulars Chq No Accoun

ts

Payabl

e

Cash

Purchas

es

GST

Paid

Other Bank

$ Account

02-Nov Purchased fixtures

& fittings for cash

Chq

0001

600 6,000

Furniture

&

[Financial Accounting] Page 9 QMS-AT-v2/0513

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

[Financial Accounting] – Final Exam

fixtures

02-Nov Paid rent on shop

premises

Chq

0002 100 1,000 Rent

09-Nov Paid wages Chq

0003 650 Wages

13-Nov Paid television

advertising

Chq

0004 220 2,200 Advertisi

ng

17-Nov Cash purchases Chq

0005 1,500 150

17-Nov Paid wages Chq

0006 450 Wages

21-Nov Cash purchases Chq

0007 1,150 115

28-Nov Paid bank interest Chq

0008 250 Bank

interest

Total - - 2,650 1,185 10,550

Sales Distribution Journal

Date Name of

Debtors

Inv No Total

Accounts

Receivables

Sales GST

Collected

06-Nov E. Johnson Invoice 11 1,100 1,000 100

09-Nov F Black Invoice 12 704 640 64

14-Nov E. Thomson Invoice 13 550 500 50

16-Nov D Brown Invoice 14 825 750 75

25-Nov E. Green Invoice 15 880 800 80

Total 4,059 3,690 369

Purchase Distribution Journal

[Financial Accounting] Page 10 QMS-AT-v2/0513

fixtures

02-Nov Paid rent on shop

premises

Chq

0002 100 1,000 Rent

09-Nov Paid wages Chq

0003 650 Wages

13-Nov Paid television

advertising

Chq

0004 220 2,200 Advertisi

ng

17-Nov Cash purchases Chq

0005 1,500 150

17-Nov Paid wages Chq

0006 450 Wages

21-Nov Cash purchases Chq

0007 1,150 115

28-Nov Paid bank interest Chq

0008 250 Bank

interest

Total - - 2,650 1,185 10,550

Sales Distribution Journal

Date Name of

Debtors

Inv No Total

Accounts

Receivables

Sales GST

Collected

06-Nov E. Johnson Invoice 11 1,100 1,000 100

09-Nov F Black Invoice 12 704 640 64

14-Nov E. Thomson Invoice 13 550 500 50

16-Nov D Brown Invoice 14 825 750 75

25-Nov E. Green Invoice 15 880 800 80

Total 4,059 3,690 369

Purchase Distribution Journal

[Financial Accounting] Page 10 QMS-AT-v2/0513

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

[Financial Accounting] – Final Exam

Date Name of

Creditors

Inv No Total

Accounts Payables

Purchases GST

Paid

05-Nov B Jones Invoice 47 2,200 2,000 200

16-Nov P. Plummer Invoice

687 792 720 72

Total 2,992 2,720 272

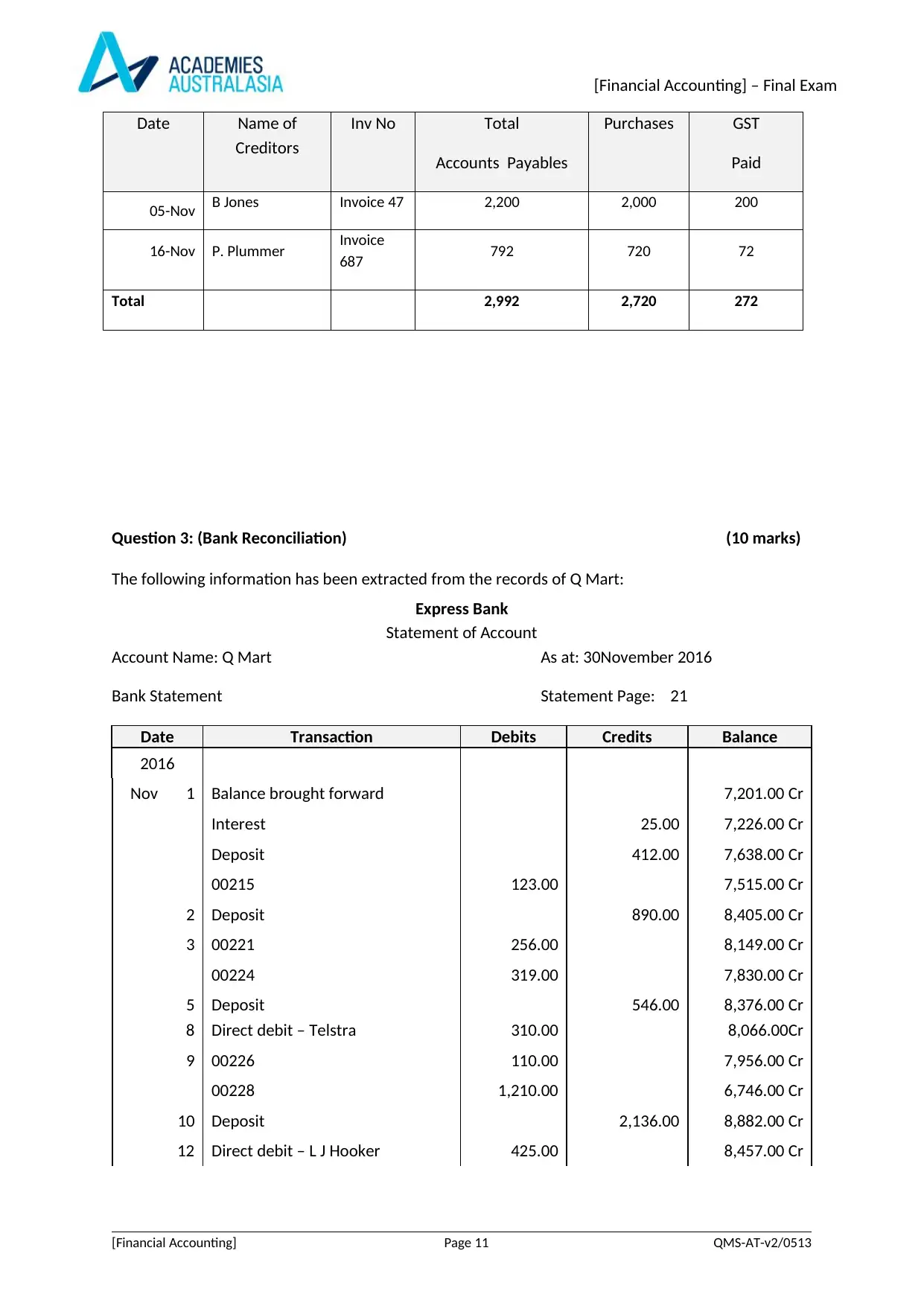

Question 3: (Bank Reconciliation) (10 marks)

The following information has been extracted from the records of Q Mart:

Express Bank

Statement of Account

Account Name: Q Mart As at: 30November 2016

Bank Statement Statement Page: 21

Date Transaction Debits Credits Balance

2016

Nov 1 Balance brought forward 7,201.00 Cr

Interest 25.00 7,226.00 Cr

Deposit 412.00 7,638.00 Cr

00215 123.00 7,515.00 Cr

2 Deposit 890.00 8,405.00 Cr

3 00221 256.00 8,149.00 Cr

00224 319.00 7,830.00 Cr

5

8

Deposit

Direct debit – Telstra 310.00

546.00 8,376.00 Cr

8,066.00Cr

9 00226 110.00 7,956.00 Cr

00228 1,210.00 6,746.00 Cr

10 Deposit 2,136.00 8,882.00 Cr

12 Direct debit – L J Hooker 425.00 8,457.00 Cr

[Financial Accounting] Page 11 QMS-AT-v2/0513

Date Name of

Creditors

Inv No Total

Accounts Payables

Purchases GST

Paid

05-Nov B Jones Invoice 47 2,200 2,000 200

16-Nov P. Plummer Invoice

687 792 720 72

Total 2,992 2,720 272

Question 3: (Bank Reconciliation) (10 marks)

The following information has been extracted from the records of Q Mart:

Express Bank

Statement of Account

Account Name: Q Mart As at: 30November 2016

Bank Statement Statement Page: 21

Date Transaction Debits Credits Balance

2016

Nov 1 Balance brought forward 7,201.00 Cr

Interest 25.00 7,226.00 Cr

Deposit 412.00 7,638.00 Cr

00215 123.00 7,515.00 Cr

2 Deposit 890.00 8,405.00 Cr

3 00221 256.00 8,149.00 Cr

00224 319.00 7,830.00 Cr

5

8

Deposit

Direct debit – Telstra 310.00

546.00 8,376.00 Cr

8,066.00Cr

9 00226 110.00 7,956.00 Cr

00228 1,210.00 6,746.00 Cr

10 Deposit 2,136.00 8,882.00 Cr

12 Direct debit – L J Hooker 425.00 8,457.00 Cr

[Financial Accounting] Page 11 QMS-AT-v2/0513

[Financial Accounting] – Final Exam

15 Deposit 520.00 8,977.00 Cr

00227 110.00 8,867.00 Cr

19 00229 350.00 8,517.00 Cr

00225 460.00 8,057.00 Cr

22 Deposit 356.00 8,413.00 Cr

Dishonour 120.00 8,293.00 Cr

Dishonour fee 10.00 8,283.00 Cr

23 Deposit 130.00 8,413.00 Cr

25 Dividend BHP 125.00 8,538.00 Cr

29 Deposit 500.00 9,038.00 Cr

30 00232 750.00 8,288.00 Cr

Bank charges 15.00 8,273.00 Cr

Closing balance 8,273.00 Cr

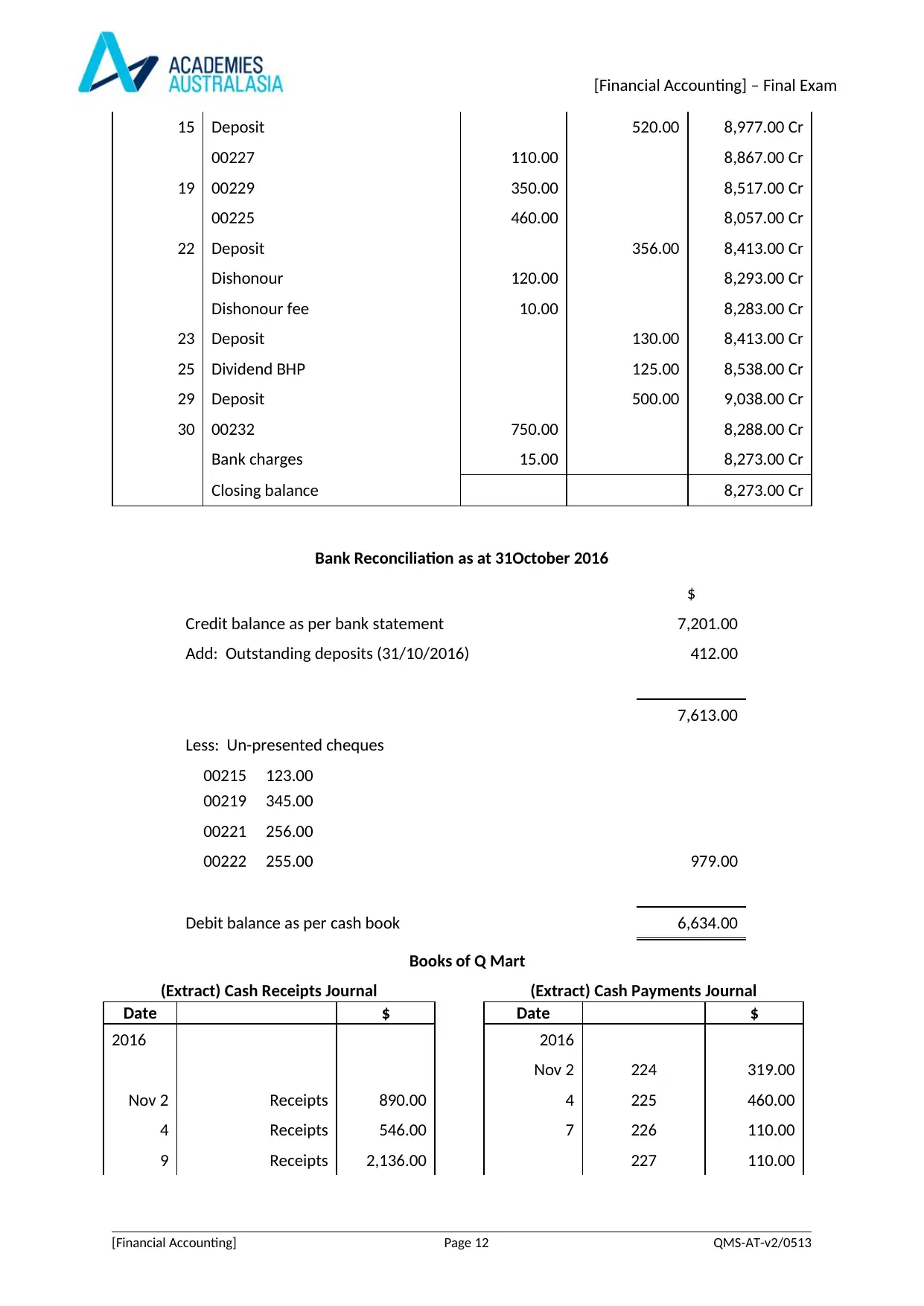

Bank Reconciliation as at 31October 2016

$

Credit balance as per bank statement 7,201.00

Add: Outstanding deposits (31/10/2016) 412.00

7,613.00

Less: Un-presented cheques

00215 123.00

00219 345.00

00221 256.00

00222 255.00 979.00

Debit balance as per cash book 6,634.00

Books of Q Mart

(Extract) Cash Receipts Journal (Extract) Cash Payments Journal

Date $ Date $

2016 2016

Nov 2 224 319.00

Nov 2 Receipts 890.00 4 225 460.00

4 Receipts 546.00 7 226 110.00

9 Receipts 2,136.00 227 110.00

[Financial Accounting] Page 12 QMS-AT-v2/0513

15 Deposit 520.00 8,977.00 Cr

00227 110.00 8,867.00 Cr

19 00229 350.00 8,517.00 Cr

00225 460.00 8,057.00 Cr

22 Deposit 356.00 8,413.00 Cr

Dishonour 120.00 8,293.00 Cr

Dishonour fee 10.00 8,283.00 Cr

23 Deposit 130.00 8,413.00 Cr

25 Dividend BHP 125.00 8,538.00 Cr

29 Deposit 500.00 9,038.00 Cr

30 00232 750.00 8,288.00 Cr

Bank charges 15.00 8,273.00 Cr

Closing balance 8,273.00 Cr

Bank Reconciliation as at 31October 2016

$

Credit balance as per bank statement 7,201.00

Add: Outstanding deposits (31/10/2016) 412.00

7,613.00

Less: Un-presented cheques

00215 123.00

00219 345.00

00221 256.00

00222 255.00 979.00

Debit balance as per cash book 6,634.00

Books of Q Mart

(Extract) Cash Receipts Journal (Extract) Cash Payments Journal

Date $ Date $

2016 2016

Nov 2 224 319.00

Nov 2 Receipts 890.00 4 225 460.00

4 Receipts 546.00 7 226 110.00

9 Receipts 2,136.00 227 110.00

[Financial Accounting] Page 12 QMS-AT-v2/0513

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.