Processing Financial Transactions and Reports: FNSACC301A Assignment

VerifiedAdded on 2020/04/21

|16

|4292

|78

Practical Assignment

AI Summary

This assignment, FNSACC301A, focuses on processing financial transactions and extracting interim reports using MYOB AccountRight. The assessment is divided into two parts: a written/oral section with questions on verifying documentation, bank reconciliations, petty cash systems, invoices, journals, data entry, deposit facilities, and trial balances; and a practical exercise. The practical part involves simulating a retail stationery shop, 'Office Supplies Shop,' where the student is required to perform tasks such as setting up company information, recording sales orders and tax invoices, processing customer payments, creating sales adjustment notes, managing purchase orders, paying bills, and preparing a trial balance. The assignment emphasizes the accurate recording of financial data, adherence to organizational procedures, and the generation of financial reports. The provided solution demonstrates how to complete these tasks within the MYOB AccountRight software, including creating customer and supplier cards, and making journal entries.

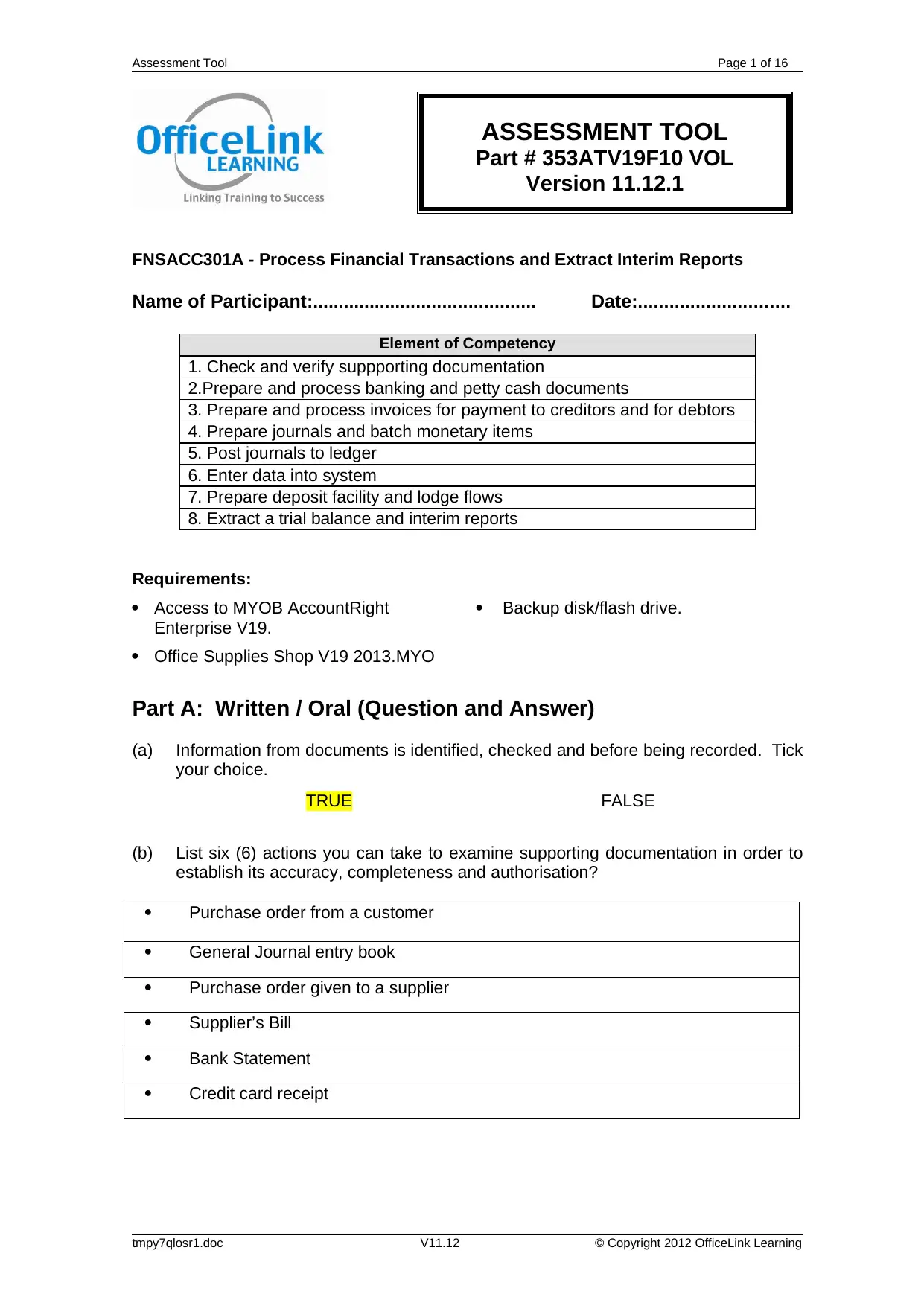

Assessment Tool Page 1 of 16

FNSACC301A - Process Financial Transactions and Extract Interim Reports

Name of Participant:........................................... Date:.............................

Element of Competency

1. Check and verify suppporting documentation

2.Prepare and process banking and petty cash documents

3. Prepare and process invoices for payment to creditors and for debtors

4. Prepare journals and batch monetary items

5. Post journals to ledger

6. Enter data into system

7. Prepare deposit facility and lodge flows

8. Extract a trial balance and interim reports

Requirements:

Access to MYOB AccountRight

Enterprise V19.

Backup disk/flash drive.

Office Supplies Shop V19 2013.MYO

Part A: Written / Oral (Question and Answer)

(a) Information from documents is identified, checked and before being recorded. Tick

your choice.

TRUE FALSE

(b) List six (6) actions you can take to examine supporting documentation in order to

establish its accuracy, completeness and authorisation?

Purchase order from a customer

General Journal entry book

Purchase order given to a supplier

Supplier’s Bill

Bank Statement

Credit card receipt

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

ASSESSMENT TOOL

Part # 353ATV19F10 VOL

Version 11.12.1

FNSACC301A - Process Financial Transactions and Extract Interim Reports

Name of Participant:........................................... Date:.............................

Element of Competency

1. Check and verify suppporting documentation

2.Prepare and process banking and petty cash documents

3. Prepare and process invoices for payment to creditors and for debtors

4. Prepare journals and batch monetary items

5. Post journals to ledger

6. Enter data into system

7. Prepare deposit facility and lodge flows

8. Extract a trial balance and interim reports

Requirements:

Access to MYOB AccountRight

Enterprise V19.

Backup disk/flash drive.

Office Supplies Shop V19 2013.MYO

Part A: Written / Oral (Question and Answer)

(a) Information from documents is identified, checked and before being recorded. Tick

your choice.

TRUE FALSE

(b) List six (6) actions you can take to examine supporting documentation in order to

establish its accuracy, completeness and authorisation?

Purchase order from a customer

General Journal entry book

Purchase order given to a supplier

Supplier’s Bill

Bank Statement

Credit card receipt

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

ASSESSMENT TOOL

Part # 353ATV19F10 VOL

Version 11.12.1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Tool Page 2 of 16

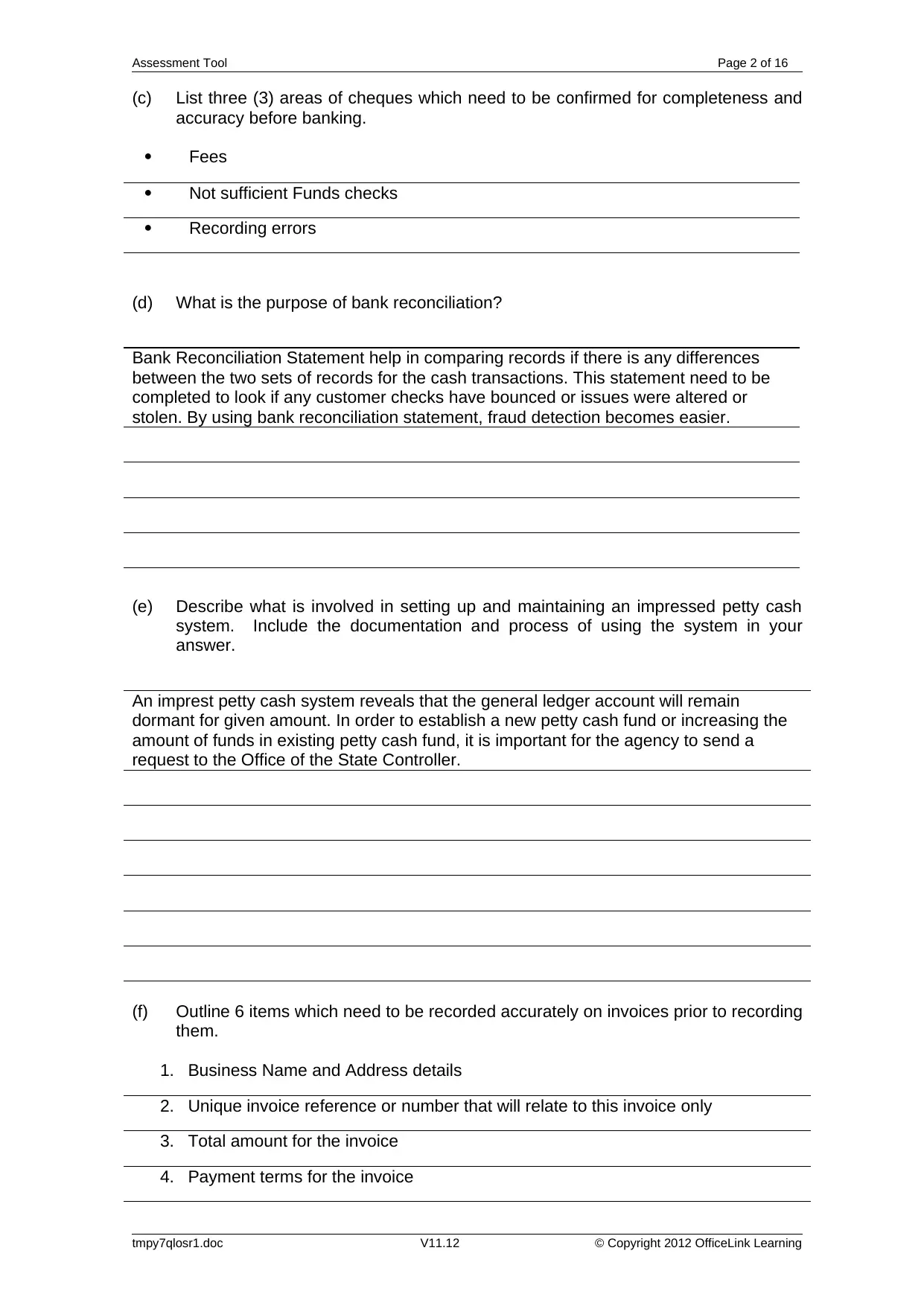

(c) List three (3) areas of cheques which need to be confirmed for completeness and

accuracy before banking.

Fees

Not sufficient Funds checks

Recording errors

(d) What is the purpose of bank reconciliation?

Bank Reconciliation Statement help in comparing records if there is any differences

between the two sets of records for the cash transactions. This statement need to be

completed to look if any customer checks have bounced or issues were altered or

stolen. By using bank reconciliation statement, fraud detection becomes easier.

(e) Describe what is involved in setting up and maintaining an impressed petty cash

system. Include the documentation and process of using the system in your

answer.

An imprest petty cash system reveals that the general ledger account will remain

dormant for given amount. In order to establish a new petty cash fund or increasing the

amount of funds in existing petty cash fund, it is important for the agency to send a

request to the Office of the State Controller.

(f) Outline 6 items which need to be recorded accurately on invoices prior to recording

them.

1. Business Name and Address details

2. Unique invoice reference or number that will relate to this invoice only

3. Total amount for the invoice

4. Payment terms for the invoice

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

(c) List three (3) areas of cheques which need to be confirmed for completeness and

accuracy before banking.

Fees

Not sufficient Funds checks

Recording errors

(d) What is the purpose of bank reconciliation?

Bank Reconciliation Statement help in comparing records if there is any differences

between the two sets of records for the cash transactions. This statement need to be

completed to look if any customer checks have bounced or issues were altered or

stolen. By using bank reconciliation statement, fraud detection becomes easier.

(e) Describe what is involved in setting up and maintaining an impressed petty cash

system. Include the documentation and process of using the system in your

answer.

An imprest petty cash system reveals that the general ledger account will remain

dormant for given amount. In order to establish a new petty cash fund or increasing the

amount of funds in existing petty cash fund, it is important for the agency to send a

request to the Office of the State Controller.

(f) Outline 6 items which need to be recorded accurately on invoices prior to recording

them.

1. Business Name and Address details

2. Unique invoice reference or number that will relate to this invoice only

3. Total amount for the invoice

4. Payment terms for the invoice

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

Assessment Tool Page 3 of 16

5. Customer Purchase Order Number

6. List of products or services

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

5. Customer Purchase Order Number

6. List of products or services

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assessment Tool Page 4 of 16

(g) Once invoices are accurately recorded the documentation needs to be filed for

auditing purposes. Tick your choice.

TRUE FALSE

(h) From the list below, indicate your choices about preparing and posting journals in

order for the journals to be prepared accurately and completely. Tick your choices.

Batched into organisational

timelines

Allocated to appropriate accounts

Authorised before being entered May require tax codes to allocate

GST accurately

Computerised batches match

source documents

Posted to the ledger within

organisational timeframes

(i) When entering data into accounting systems/applications, what actions can you do

to ensure the transactions are accurate and in accordance with organisational

procedures to ensure that you maintain the integrity of relationships between

different financial systems/applications.

Many actions can be taken that can help in maintaining high level of accuracy. The first

action is supporting as well as training the staff members when implementing any new

software program. The second action is preparing checklist that can be used for

maintaining high level of accuracy. The third actions are involving in cross references for

sourcing documents. For instance- Checking Totals of GST. The fourth action is data

testing and data comparison with reports.

(j) A deposit facility could be the ‘un-deposited’ funds account. Tick your choice.

YES NO

(k) List three methods of payment which customers could use with a deposit facility?

1. Credit Card

2. Debit Card

3. Cheque

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

(g) Once invoices are accurately recorded the documentation needs to be filed for

auditing purposes. Tick your choice.

TRUE FALSE

(h) From the list below, indicate your choices about preparing and posting journals in

order for the journals to be prepared accurately and completely. Tick your choices.

Batched into organisational

timelines

Allocated to appropriate accounts

Authorised before being entered May require tax codes to allocate

GST accurately

Computerised batches match

source documents

Posted to the ledger within

organisational timeframes

(i) When entering data into accounting systems/applications, what actions can you do

to ensure the transactions are accurate and in accordance with organisational

procedures to ensure that you maintain the integrity of relationships between

different financial systems/applications.

Many actions can be taken that can help in maintaining high level of accuracy. The first

action is supporting as well as training the staff members when implementing any new

software program. The second action is preparing checklist that can be used for

maintaining high level of accuracy. The third actions are involving in cross references for

sourcing documents. For instance- Checking Totals of GST. The fourth action is data

testing and data comparison with reports.

(j) A deposit facility could be the ‘un-deposited’ funds account. Tick your choice.

YES NO

(k) List three methods of payment which customers could use with a deposit facility?

1. Credit Card

2. Debit Card

3. Cheque

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Tool Page 5 of 16

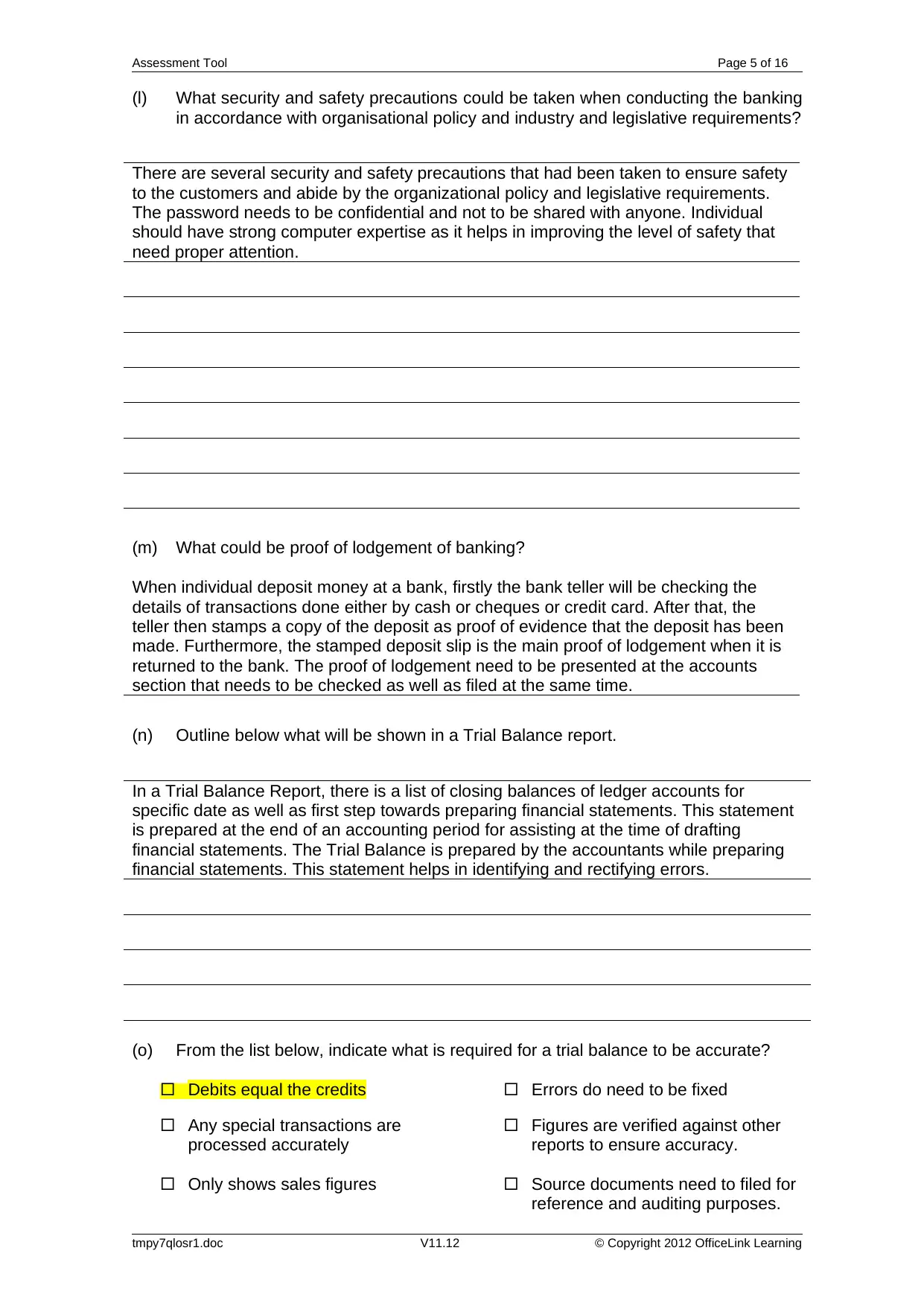

(l) What security and safety precautions could be taken when conducting the banking

in accordance with organisational policy and industry and legislative requirements?

There are several security and safety precautions that had been taken to ensure safety

to the customers and abide by the organizational policy and legislative requirements.

The password needs to be confidential and not to be shared with anyone. Individual

should have strong computer expertise as it helps in improving the level of safety that

need proper attention.

(m) What could be proof of lodgement of banking?

When individual deposit money at a bank, firstly the bank teller will be checking the

details of transactions done either by cash or cheques or credit card. After that, the

teller then stamps a copy of the deposit as proof of evidence that the deposit has been

made. Furthermore, the stamped deposit slip is the main proof of lodgement when it is

returned to the bank. The proof of lodgement need to be presented at the accounts

section that needs to be checked as well as filed at the same time.

(n) Outline below what will be shown in a Trial Balance report.

In a Trial Balance Report, there is a list of closing balances of ledger accounts for

specific date as well as first step towards preparing financial statements. This statement

is prepared at the end of an accounting period for assisting at the time of drafting

financial statements. The Trial Balance is prepared by the accountants while preparing

financial statements. This statement helps in identifying and rectifying errors.

(o) From the list below, indicate what is required for a trial balance to be accurate?

Debits equal the credits Errors do need to be fixed

Any special transactions are

processed accurately

Figures are verified against other

reports to ensure accuracy.

Only shows sales figures Source documents need to filed for

reference and auditing purposes.

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

(l) What security and safety precautions could be taken when conducting the banking

in accordance with organisational policy and industry and legislative requirements?

There are several security and safety precautions that had been taken to ensure safety

to the customers and abide by the organizational policy and legislative requirements.

The password needs to be confidential and not to be shared with anyone. Individual

should have strong computer expertise as it helps in improving the level of safety that

need proper attention.

(m) What could be proof of lodgement of banking?

When individual deposit money at a bank, firstly the bank teller will be checking the

details of transactions done either by cash or cheques or credit card. After that, the

teller then stamps a copy of the deposit as proof of evidence that the deposit has been

made. Furthermore, the stamped deposit slip is the main proof of lodgement when it is

returned to the bank. The proof of lodgement need to be presented at the accounts

section that needs to be checked as well as filed at the same time.

(n) Outline below what will be shown in a Trial Balance report.

In a Trial Balance Report, there is a list of closing balances of ledger accounts for

specific date as well as first step towards preparing financial statements. This statement

is prepared at the end of an accounting period for assisting at the time of drafting

financial statements. The Trial Balance is prepared by the accountants while preparing

financial statements. This statement helps in identifying and rectifying errors.

(o) From the list below, indicate what is required for a trial balance to be accurate?

Debits equal the credits Errors do need to be fixed

Any special transactions are

processed accurately

Figures are verified against other

reports to ensure accuracy.

Only shows sales figures Source documents need to filed for

reference and auditing purposes.

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

Assessment Tool Page 6 of 16

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assessment Tool Page 7 of 16

Part B: Practical Exercise / Evidence

This practical exercise will consolidate your skills and knowledge to Process Financial

Transactions and Reports in AccountRight. You will simulate that you own retail shop

which sells stationery.

Use the instructions in the previous units to assist you in completing the consolidation

exercise.

Assessment Details

Office Supplies Shop is owned by Richard Herbert, it

is a retail shop.

In this data file you will be working in July 2012.

Extract from Office Supply Shop Procedures Manual

Procedures

All supporting documentation is to be checked against computerized entries. The

supporting documentation must be authorized by Richard Herbert. Then it is to be filed

in the Accounts filing cabinet.

Banking Deposits & Receipts

All customer receipts or deposits must be entered into the undeposited funds account.

The bank deposits will then be processed into the Cheque Account. Two copies of the

Bank Deposit report must be taken to the bank and be stamped. A stamped copy must

be returned in the office and filed in cabinet.

All customer cheques need to be checked for correctness before they are processed.

Account Reconciliations

Reconciliations of the Cheque Account must be conducted upon receipt of the Bank

Statement.

The Petty Cash Account must be reconciled each time that a reimbursement cheque is

drawn.

Copies of the Reconciliation Reports must be stored with their source documents in arch

lever folders in the Accounts department.

Petty Cash

All entries over $20 must be authorized by Richard otherwise the Bookkeeper can

authorize and process the transactions. Vouchers are to be completed only when

money is reimbursed to the purchaser.

Journal Entries

All journals must be authorised by Richard with his initials in the memo field. Entries are

to be batched together and recorded at the end of month or end of quarter

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

Part B: Practical Exercise / Evidence

This practical exercise will consolidate your skills and knowledge to Process Financial

Transactions and Reports in AccountRight. You will simulate that you own retail shop

which sells stationery.

Use the instructions in the previous units to assist you in completing the consolidation

exercise.

Assessment Details

Office Supplies Shop is owned by Richard Herbert, it

is a retail shop.

In this data file you will be working in July 2012.

Extract from Office Supply Shop Procedures Manual

Procedures

All supporting documentation is to be checked against computerized entries. The

supporting documentation must be authorized by Richard Herbert. Then it is to be filed

in the Accounts filing cabinet.

Banking Deposits & Receipts

All customer receipts or deposits must be entered into the undeposited funds account.

The bank deposits will then be processed into the Cheque Account. Two copies of the

Bank Deposit report must be taken to the bank and be stamped. A stamped copy must

be returned in the office and filed in cabinet.

All customer cheques need to be checked for correctness before they are processed.

Account Reconciliations

Reconciliations of the Cheque Account must be conducted upon receipt of the Bank

Statement.

The Petty Cash Account must be reconciled each time that a reimbursement cheque is

drawn.

Copies of the Reconciliation Reports must be stored with their source documents in arch

lever folders in the Accounts department.

Petty Cash

All entries over $20 must be authorized by Richard otherwise the Bookkeeper can

authorize and process the transactions. Vouchers are to be completed only when

money is reimbursed to the purchaser.

Journal Entries

All journals must be authorised by Richard with his initials in the memo field. Entries are

to be batched together and recorded at the end of month or end of quarter

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Tool Page 8 of 16

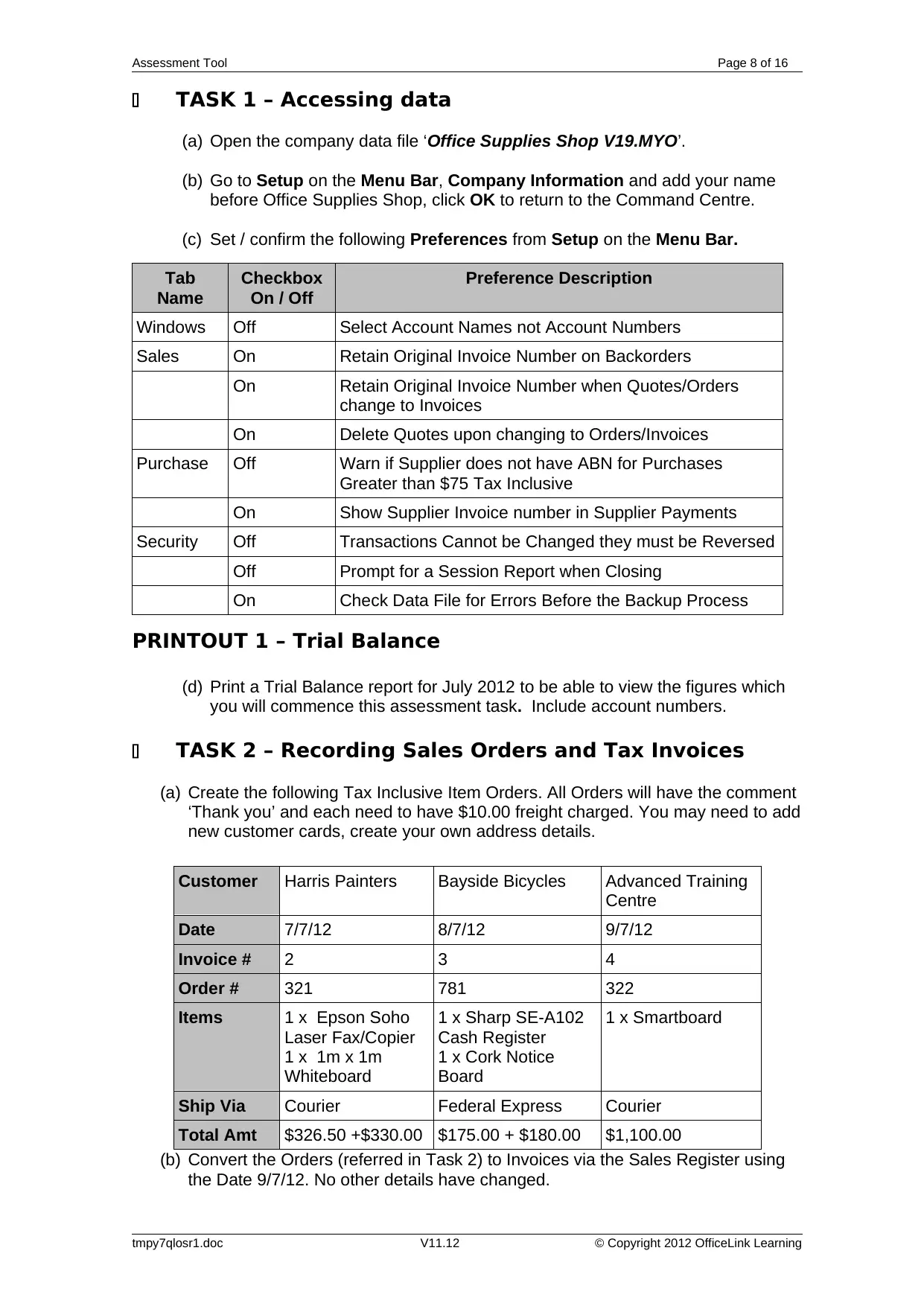

TASK 1 – Accessing data

(a) Open the company data file ‘Office Supplies Shop V19.MYO’.

(b) Go to Setup on the Menu Bar, Company Information and add your name

before Office Supplies Shop, click OK to return to the Command Centre.

(c) Set / confirm the following Preferences from Setup on the Menu Bar.

Tab

Name

Checkbox

On / Off

Preference Description

Windows Off Select Account Names not Account Numbers

Sales On Retain Original Invoice Number on Backorders

On Retain Original Invoice Number when Quotes/Orders

change to Invoices

On Delete Quotes upon changing to Orders/Invoices

Purchase Off Warn if Supplier does not have ABN for Purchases

Greater than $75 Tax Inclusive

On Show Supplier Invoice number in Supplier Payments

Security Off Transactions Cannot be Changed they must be Reversed

Off Prompt for a Session Report when Closing

On Check Data File for Errors Before the Backup Process

PRINTOUT 1 – Trial Balance

(d) Print a Trial Balance report for July 2012 to be able to view the figures which

you will commence this assessment task. Include account numbers.

TASK 2 – Recording Sales Orders and Tax Invoices

(a) Create the following Tax Inclusive Item Orders. All Orders will have the comment

‘Thank you’ and each need to have $10.00 freight charged. You may need to add

new customer cards, create your own address details.

(b) Convert the Orders (referred in Task 2) to Invoices via the Sales Register using

the Date 9/7/12. No other details have changed.

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

Customer Harris Painters Bayside Bicycles Advanced Training

Centre

Date 7/7/12 8/7/12 9/7/12

Invoice # 2 3 4

Order # 321 781 322

Items 1 x Epson Soho

Laser Fax/Copier

1 x 1m x 1m

Whiteboard

1 x Sharp SE-A102

Cash Register

1 x Cork Notice

Board

1 x Smartboard

Ship Via Courier Federal Express Courier

Total Amt $326.50 +$330.00 $175.00 + $180.00 $1,100.00

TASK 1 – Accessing data

(a) Open the company data file ‘Office Supplies Shop V19.MYO’.

(b) Go to Setup on the Menu Bar, Company Information and add your name

before Office Supplies Shop, click OK to return to the Command Centre.

(c) Set / confirm the following Preferences from Setup on the Menu Bar.

Tab

Name

Checkbox

On / Off

Preference Description

Windows Off Select Account Names not Account Numbers

Sales On Retain Original Invoice Number on Backorders

On Retain Original Invoice Number when Quotes/Orders

change to Invoices

On Delete Quotes upon changing to Orders/Invoices

Purchase Off Warn if Supplier does not have ABN for Purchases

Greater than $75 Tax Inclusive

On Show Supplier Invoice number in Supplier Payments

Security Off Transactions Cannot be Changed they must be Reversed

Off Prompt for a Session Report when Closing

On Check Data File for Errors Before the Backup Process

PRINTOUT 1 – Trial Balance

(d) Print a Trial Balance report for July 2012 to be able to view the figures which

you will commence this assessment task. Include account numbers.

TASK 2 – Recording Sales Orders and Tax Invoices

(a) Create the following Tax Inclusive Item Orders. All Orders will have the comment

‘Thank you’ and each need to have $10.00 freight charged. You may need to add

new customer cards, create your own address details.

(b) Convert the Orders (referred in Task 2) to Invoices via the Sales Register using

the Date 9/7/12. No other details have changed.

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

Customer Harris Painters Bayside Bicycles Advanced Training

Centre

Date 7/7/12 8/7/12 9/7/12

Invoice # 2 3 4

Order # 321 781 322

Items 1 x Epson Soho

Laser Fax/Copier

1 x 1m x 1m

Whiteboard

1 x Sharp SE-A102

Cash Register

1 x Cork Notice

Board

1 x Smartboard

Ship Via Courier Federal Express Courier

Total Amt $326.50 +$330.00 $175.00 + $180.00 $1,100.00

Assessment Tool Page 9 of 16

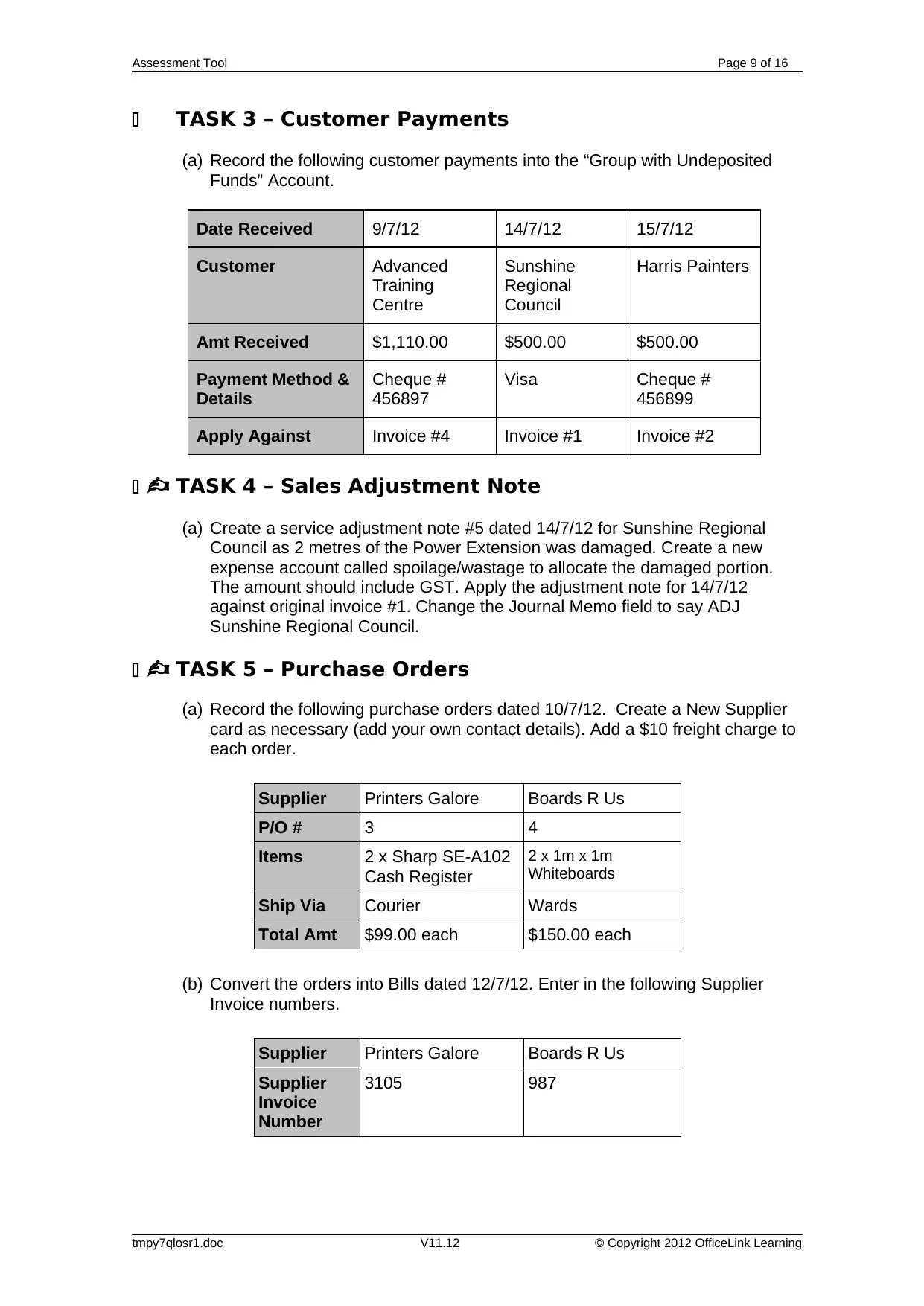

TASK 3 – Customer Payments

(a) Record the following customer payments into the “Group with Undeposited

Funds” Account.

Date Received 9/7/12 14/7/12 15/7/12

Customer Advanced

Training

Centre

Sunshine

Regional

Council

Harris Painters

Amt Received $1,110.00 $500.00 $500.00

Payment Method &

Details

Cheque #

456897

Visa Cheque #

456899

Apply Against Invoice #4 Invoice #1 Invoice #2

TASK 4 – Sales Adjustment Note

(a) Create a service adjustment note #5 dated 14/7/12 for Sunshine Regional

Council as 2 metres of the Power Extension was damaged. Create a new

expense account called spoilage/wastage to allocate the damaged portion.

The amount should include GST. Apply the adjustment note for 14/7/12

against original invoice #1. Change the Journal Memo field to say ADJ

Sunshine Regional Council.

TASK 5 – Purchase Orders

(a) Record the following purchase orders dated 10/7/12. Create a New Supplier

card as necessary (add your own contact details). Add a $10 freight charge to

each order.

(b) Convert the orders into Bills dated 12/7/12. Enter in the following Supplier

Invoice numbers.

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

Supplier Printers Galore Boards R Us

P/O # 3 4

Items 2 x Sharp SE-A102

Cash Register

2 x 1m x 1m

Whiteboards

Ship Via Courier Wards

Total Amt $99.00 each $150.00 each

Supplier Printers Galore Boards R Us

Supplier

Invoice

Number

3105 987

TASK 3 – Customer Payments

(a) Record the following customer payments into the “Group with Undeposited

Funds” Account.

Date Received 9/7/12 14/7/12 15/7/12

Customer Advanced

Training

Centre

Sunshine

Regional

Council

Harris Painters

Amt Received $1,110.00 $500.00 $500.00

Payment Method &

Details

Cheque #

456897

Visa Cheque #

456899

Apply Against Invoice #4 Invoice #1 Invoice #2

TASK 4 – Sales Adjustment Note

(a) Create a service adjustment note #5 dated 14/7/12 for Sunshine Regional

Council as 2 metres of the Power Extension was damaged. Create a new

expense account called spoilage/wastage to allocate the damaged portion.

The amount should include GST. Apply the adjustment note for 14/7/12

against original invoice #1. Change the Journal Memo field to say ADJ

Sunshine Regional Council.

TASK 5 – Purchase Orders

(a) Record the following purchase orders dated 10/7/12. Create a New Supplier

card as necessary (add your own contact details). Add a $10 freight charge to

each order.

(b) Convert the orders into Bills dated 12/7/12. Enter in the following Supplier

Invoice numbers.

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

Supplier Printers Galore Boards R Us

P/O # 3 4

Items 2 x Sharp SE-A102

Cash Register

2 x 1m x 1m

Whiteboards

Ship Via Courier Wards

Total Amt $99.00 each $150.00 each

Supplier Printers Galore Boards R Us

Supplier

Invoice

Number

3105 987

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assessment Tool Page 10 of 16

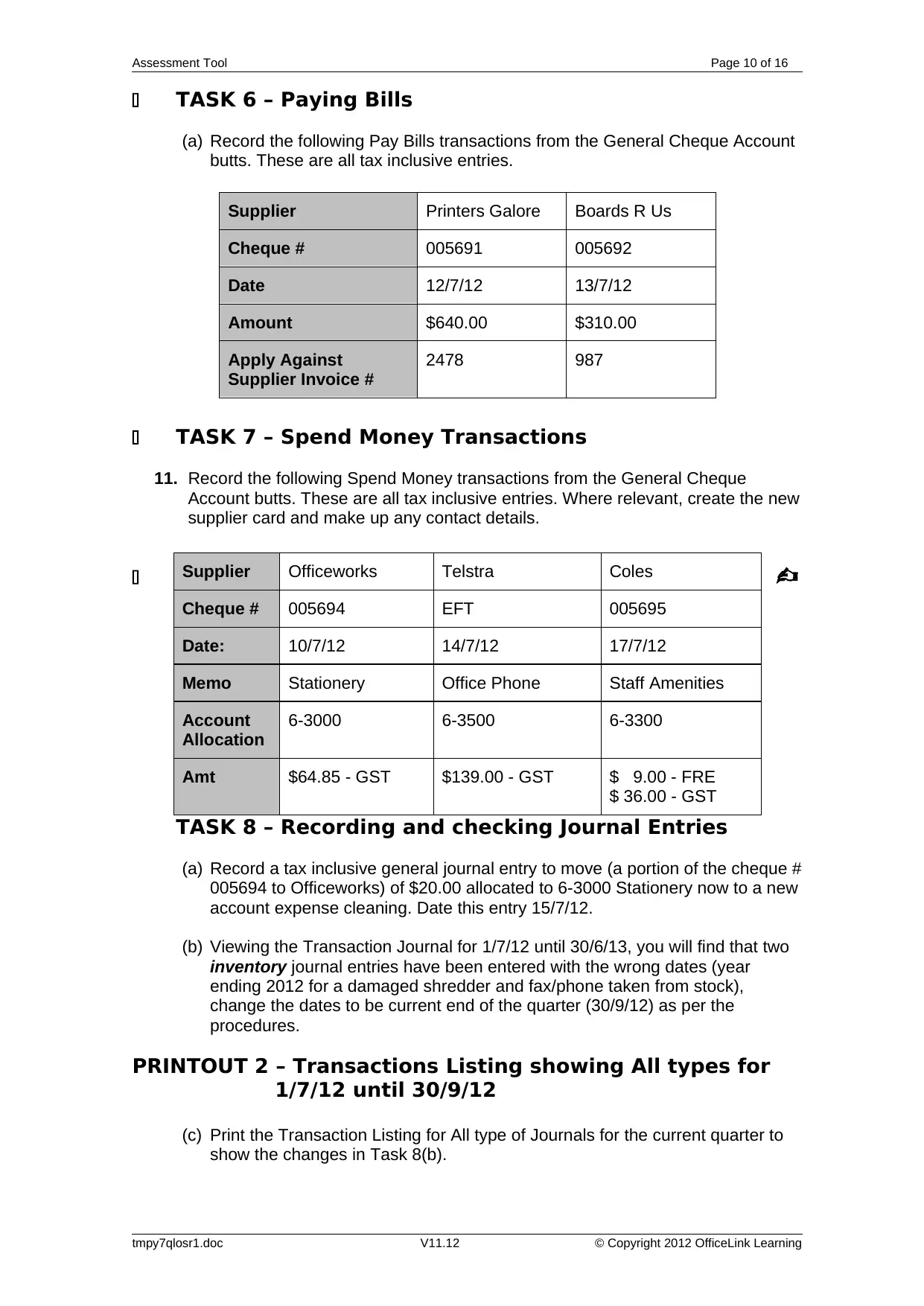

TASK 6 – Paying Bills

(a) Record the following Pay Bills transactions from the General Cheque Account

butts. These are all tax inclusive entries.

TASK 7 – Spend Money Transactions

11. Record the following Spend Money transactions from the General Cheque

Account butts. These are all tax inclusive entries. Where relevant, create the new

supplier card and make up any contact details.

TASK 8 – Recording and checking Journal Entries

(a) Record a tax inclusive general journal entry to move (a portion of the cheque #

005694 to Officeworks) of $20.00 allocated to 6-3000 Stationery now to a new

account expense cleaning. Date this entry 15/7/12.

(b) Viewing the Transaction Journal for 1/7/12 until 30/6/13, you will find that two

inventory journal entries have been entered with the wrong dates (year

ending 2012 for a damaged shredder and fax/phone taken from stock),

change the dates to be current end of the quarter (30/9/12) as per the

procedures.

PRINTOUT 2 – Transactions Listing showing All types for

1/7/12 until 30/9/12

(c) Print the Transaction Listing for All type of Journals for the current quarter to

show the changes in Task 8(b).

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

Supplier Printers Galore Boards R Us

Cheque # 005691 005692

Date 12/7/12 13/7/12

Amount $640.00 $310.00

Apply Against

Supplier Invoice #

2478 987

Supplier Officeworks Telstra Coles

Cheque # 005694 EFT 005695

Date: 10/7/12 14/7/12 17/7/12

Memo Stationery Office Phone Staff Amenities

Account

Allocation

6-3000 6-3500 6-3300

Amt $64.85 - GST $139.00 - GST $ 9.00 - FRE

$ 36.00 - GST

TASK 6 – Paying Bills

(a) Record the following Pay Bills transactions from the General Cheque Account

butts. These are all tax inclusive entries.

TASK 7 – Spend Money Transactions

11. Record the following Spend Money transactions from the General Cheque

Account butts. These are all tax inclusive entries. Where relevant, create the new

supplier card and make up any contact details.

TASK 8 – Recording and checking Journal Entries

(a) Record a tax inclusive general journal entry to move (a portion of the cheque #

005694 to Officeworks) of $20.00 allocated to 6-3000 Stationery now to a new

account expense cleaning. Date this entry 15/7/12.

(b) Viewing the Transaction Journal for 1/7/12 until 30/6/13, you will find that two

inventory journal entries have been entered with the wrong dates (year

ending 2012 for a damaged shredder and fax/phone taken from stock),

change the dates to be current end of the quarter (30/9/12) as per the

procedures.

PRINTOUT 2 – Transactions Listing showing All types for

1/7/12 until 30/9/12

(c) Print the Transaction Listing for All type of Journals for the current quarter to

show the changes in Task 8(b).

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

Supplier Printers Galore Boards R Us

Cheque # 005691 005692

Date 12/7/12 13/7/12

Amount $640.00 $310.00

Apply Against

Supplier Invoice #

2478 987

Supplier Officeworks Telstra Coles

Cheque # 005694 EFT 005695

Date: 10/7/12 14/7/12 17/7/12

Memo Stationery Office Phone Staff Amenities

Account

Allocation

6-3000 6-3500 6-3300

Amt $64.85 - GST $139.00 - GST $ 9.00 - FRE

$ 36.00 - GST

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Tool Page 11 of 16

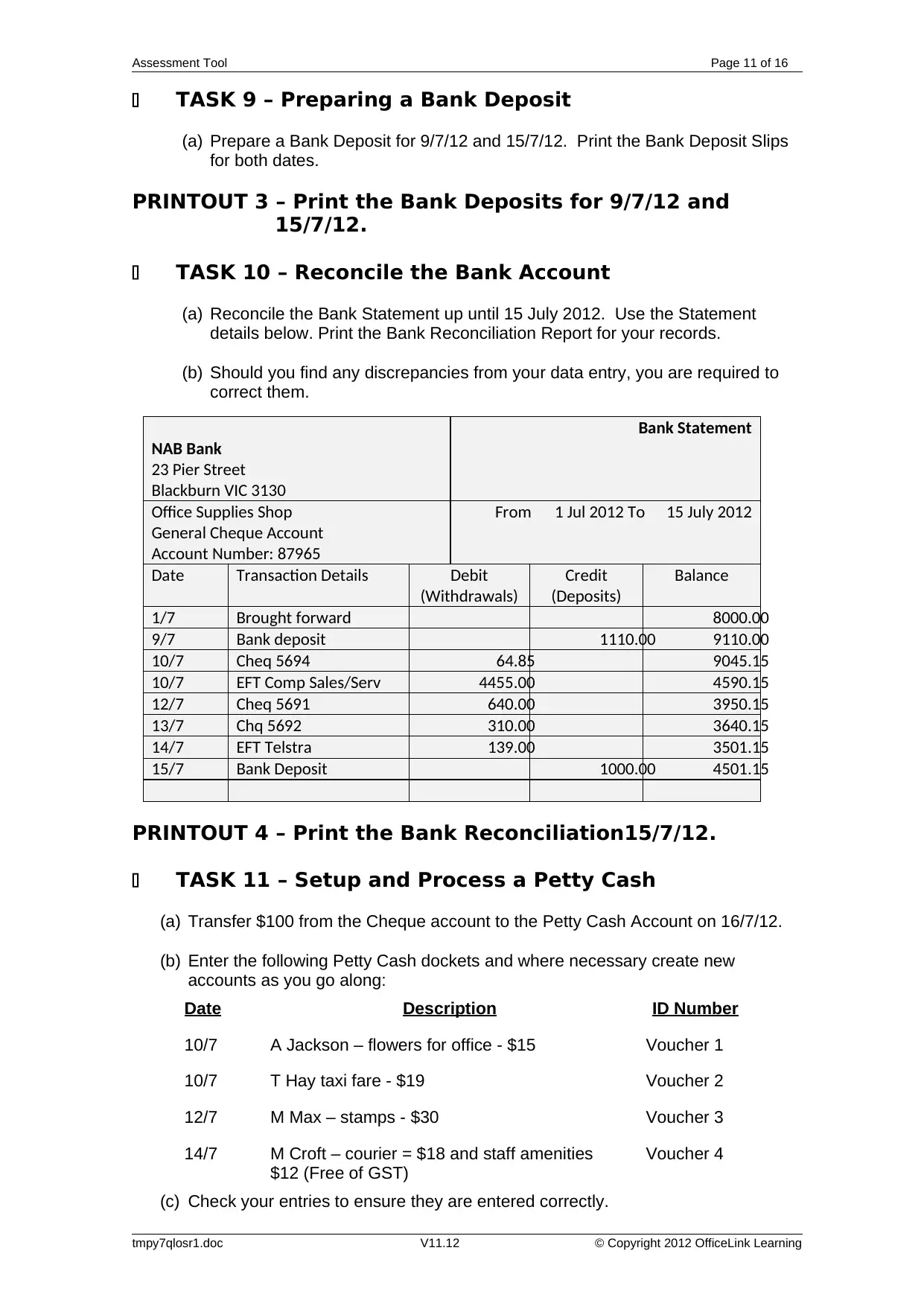

TASK 9 – Preparing a Bank Deposit

(a) Prepare a Bank Deposit for 9/7/12 and 15/7/12. Print the Bank Deposit Slips

for both dates.

PRINTOUT 3 – Print the Bank Deposits for 9/7/12 and

15/7/12.

TASK 10 – Reconcile the Bank Account

(a) Reconcile the Bank Statement up until 15 July 2012. Use the Statement

details below. Print the Bank Reconciliation Report for your records.

(b) Should you find any discrepancies from your data entry, you are required to

correct them.

NAB Bank

23 Pier Street

Blackburn VIC 3130

Bank Statement

Office Supplies Shop

General Cheque Account

Account Number: 87965

From 1 Jul 2012 To 15 July 2012

Date Transaction Details Debit

(Withdrawals)

Credit

(Deposits)

Balance

1/7 Brought forward 8000.00

9/7 Bank deposit 1110.00 9110.00

10/7 Cheq 5694 64.85 9045.15

10/7 EFT Comp Sales/Serv 4455.00 4590.15

12/7 Cheq 5691 640.00 3950.15

13/7 Chq 5692 310.00 3640.15

14/7 EFT Telstra 139.00 3501.15

15/7 Bank Deposit 1000.00 4501.15

PRINTOUT 4 – Print the Bank Reconciliation15/7/12.

TASK 11 – Setup and Process a Petty Cash

(a) Transfer $100 from the Cheque account to the Petty Cash Account on 16/7/12.

(b) Enter the following Petty Cash dockets and where necessary create new

accounts as you go along:

Date Description ID Number

10/7 A Jackson – flowers for office - $15 Voucher 1

10/7 T Hay taxi fare - $19 Voucher 2

12/7 M Max – stamps - $30 Voucher 3

14/7 M Croft – courier = $18 and staff amenities

$12 (Free of GST)

Voucher 4

(c) Check your entries to ensure they are entered correctly.

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

TASK 9 – Preparing a Bank Deposit

(a) Prepare a Bank Deposit for 9/7/12 and 15/7/12. Print the Bank Deposit Slips

for both dates.

PRINTOUT 3 – Print the Bank Deposits for 9/7/12 and

15/7/12.

TASK 10 – Reconcile the Bank Account

(a) Reconcile the Bank Statement up until 15 July 2012. Use the Statement

details below. Print the Bank Reconciliation Report for your records.

(b) Should you find any discrepancies from your data entry, you are required to

correct them.

NAB Bank

23 Pier Street

Blackburn VIC 3130

Bank Statement

Office Supplies Shop

General Cheque Account

Account Number: 87965

From 1 Jul 2012 To 15 July 2012

Date Transaction Details Debit

(Withdrawals)

Credit

(Deposits)

Balance

1/7 Brought forward 8000.00

9/7 Bank deposit 1110.00 9110.00

10/7 Cheq 5694 64.85 9045.15

10/7 EFT Comp Sales/Serv 4455.00 4590.15

12/7 Cheq 5691 640.00 3950.15

13/7 Chq 5692 310.00 3640.15

14/7 EFT Telstra 139.00 3501.15

15/7 Bank Deposit 1000.00 4501.15

PRINTOUT 4 – Print the Bank Reconciliation15/7/12.

TASK 11 – Setup and Process a Petty Cash

(a) Transfer $100 from the Cheque account to the Petty Cash Account on 16/7/12.

(b) Enter the following Petty Cash dockets and where necessary create new

accounts as you go along:

Date Description ID Number

10/7 A Jackson – flowers for office - $15 Voucher 1

10/7 T Hay taxi fare - $19 Voucher 2

12/7 M Max – stamps - $30 Voucher 3

14/7 M Croft – courier = $18 and staff amenities

$12 (Free of GST)

Voucher 4

(c) Check your entries to ensure they are entered correctly.

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

Assessment Tool Page 12 of 16

(d) On 16/7/12 and using Spend Money, record an EFT transfer to reimburse the

account for the total of the 4 vouchers you have just entered.

(e) Reconcile the Petty Cash Account to ensure that it balances to $100 on 16/7.

Print the Reconciliation Report.

PRINTOUT 5 – Print the Bank Reconciliation16/7/12 for the

Petty Cash Account.

TASK 12 – Printing Reports

(a) Print the following reports:

PRINTOUT 6 – Print the Profit & Loss Report (Accrual)

from 1/7/12 to 30/9/12 including account

numbers.

PRINTOUT 7 – Print the Standard Balance Sheet as at

September this year.

PRINTOUT 8 – Print the Transaction Listing of All entries from 1/7/12 to

30/9/12.

PRINTOUT 9 – Print the Prepare the GST Detailed Cash Report for the period

1/7/12 to 30/9/12.

PRINTOUT 10 – Print the Trial Balance to 30/9/12.

TASK 13 – Finalising the project

(a) Back up your data file.

(b) Ensure you have saved all your reports as PDF files, named according to the

instructions.

(c) Submit this assessment, printouts and back up to your Supervisor/Coach/Trainer for

assessment. It is recommended that you attach your printouts in numerical order.

Congratulations you have completed this project.

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

(d) On 16/7/12 and using Spend Money, record an EFT transfer to reimburse the

account for the total of the 4 vouchers you have just entered.

(e) Reconcile the Petty Cash Account to ensure that it balances to $100 on 16/7.

Print the Reconciliation Report.

PRINTOUT 5 – Print the Bank Reconciliation16/7/12 for the

Petty Cash Account.

TASK 12 – Printing Reports

(a) Print the following reports:

PRINTOUT 6 – Print the Profit & Loss Report (Accrual)

from 1/7/12 to 30/9/12 including account

numbers.

PRINTOUT 7 – Print the Standard Balance Sheet as at

September this year.

PRINTOUT 8 – Print the Transaction Listing of All entries from 1/7/12 to

30/9/12.

PRINTOUT 9 – Print the Prepare the GST Detailed Cash Report for the period

1/7/12 to 30/9/12.

PRINTOUT 10 – Print the Trial Balance to 30/9/12.

TASK 13 – Finalising the project

(a) Back up your data file.

(b) Ensure you have saved all your reports as PDF files, named according to the

instructions.

(c) Submit this assessment, printouts and back up to your Supervisor/Coach/Trainer for

assessment. It is recommended that you attach your printouts in numerical order.

Congratulations you have completed this project.

tmpy7qlosr1.doc V11.12 © Copyright 2012 OfficeLink Learning

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.