FNSACC404 Assessment 1: Written and Practical Questions

VerifiedAdded on 2020/04/15

|65

|9879

|83

Homework Assignment

AI Summary

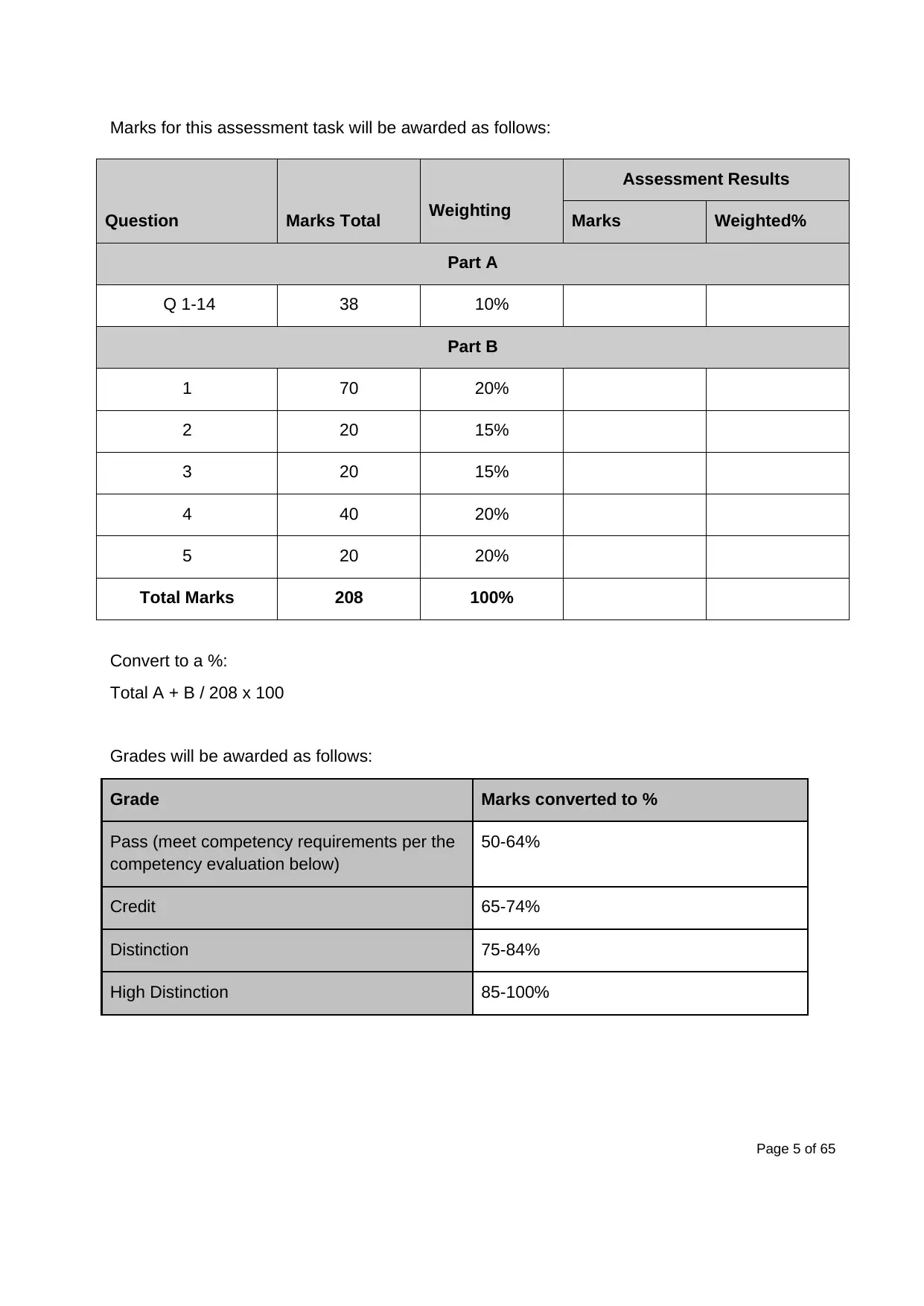

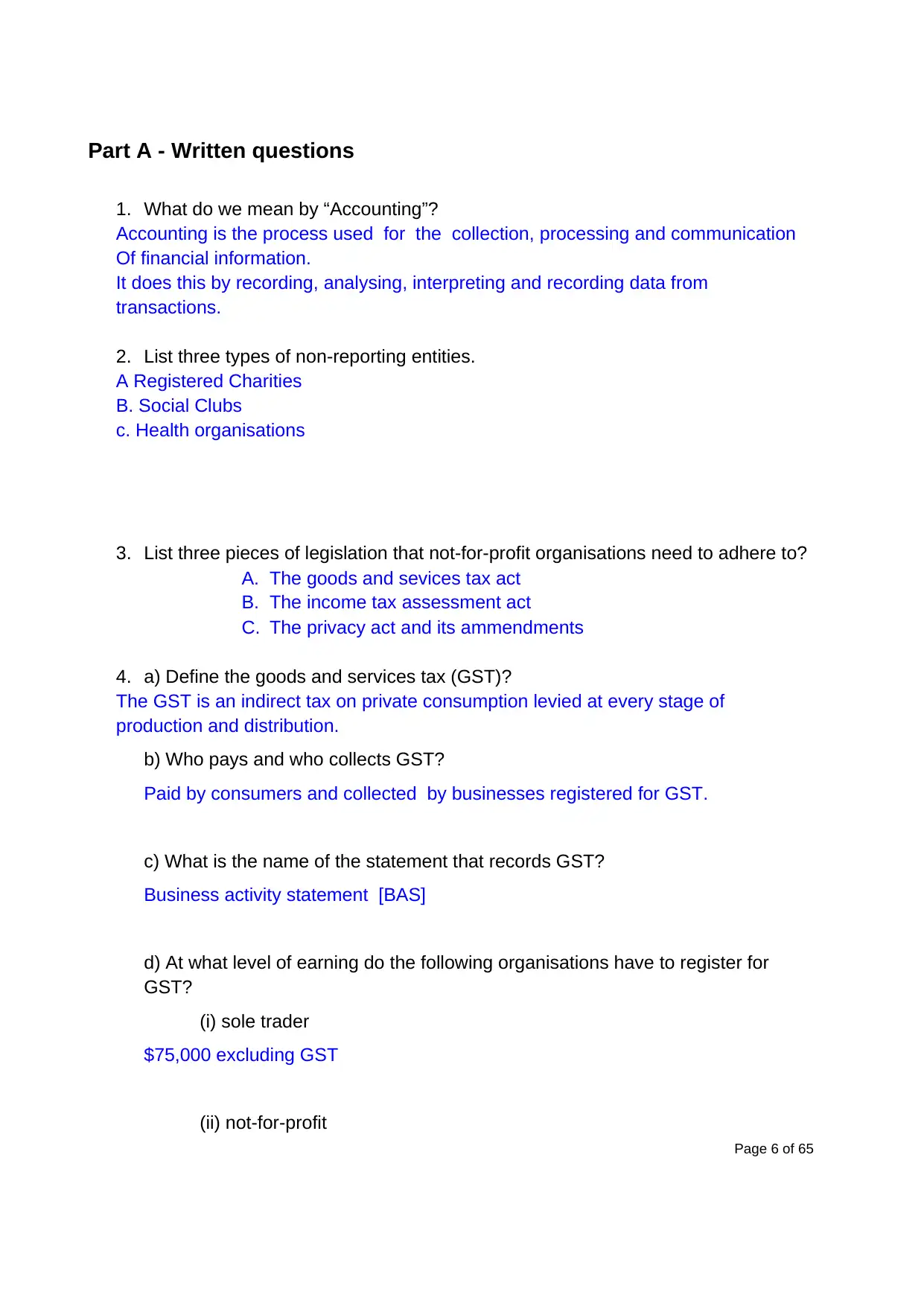

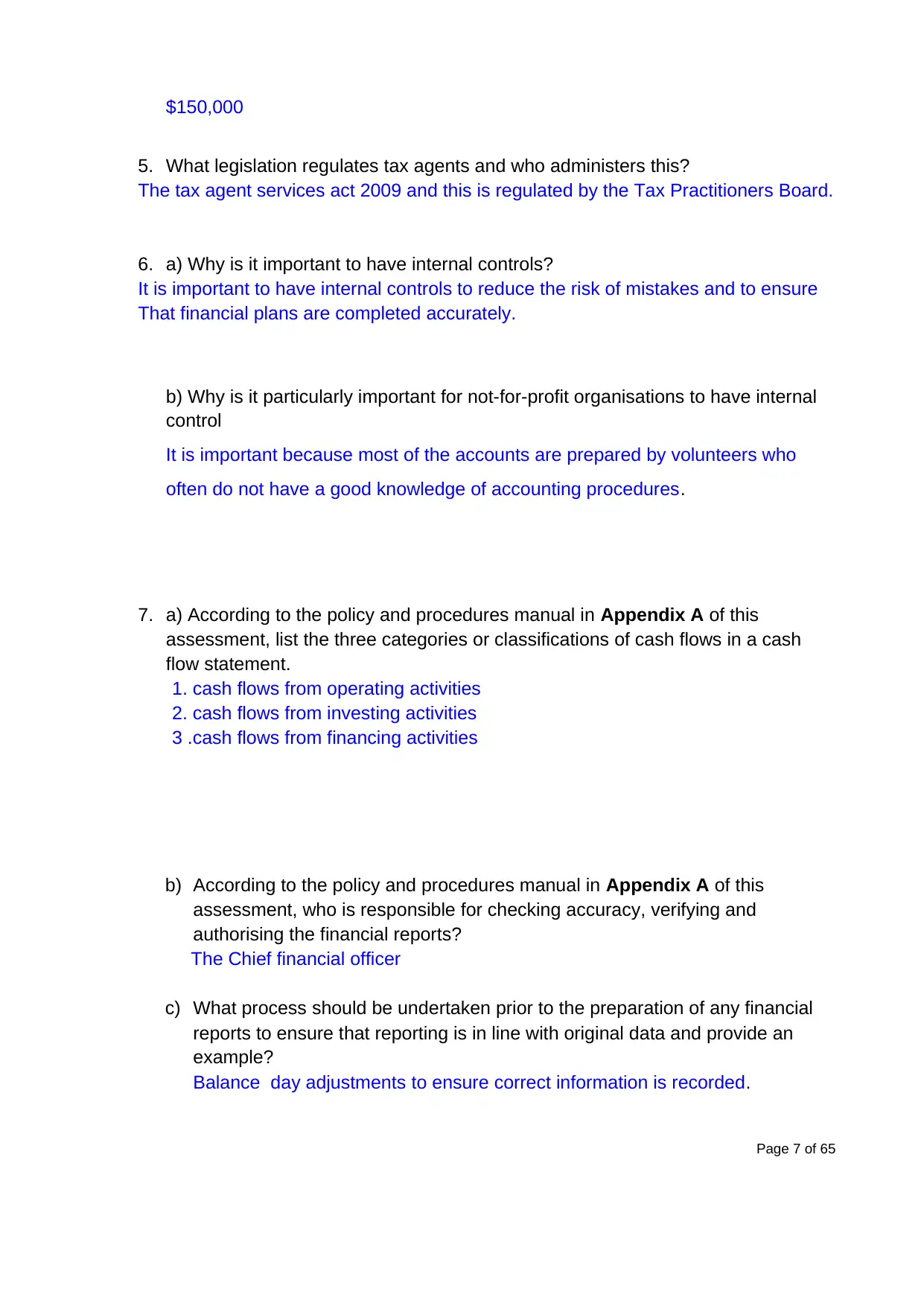

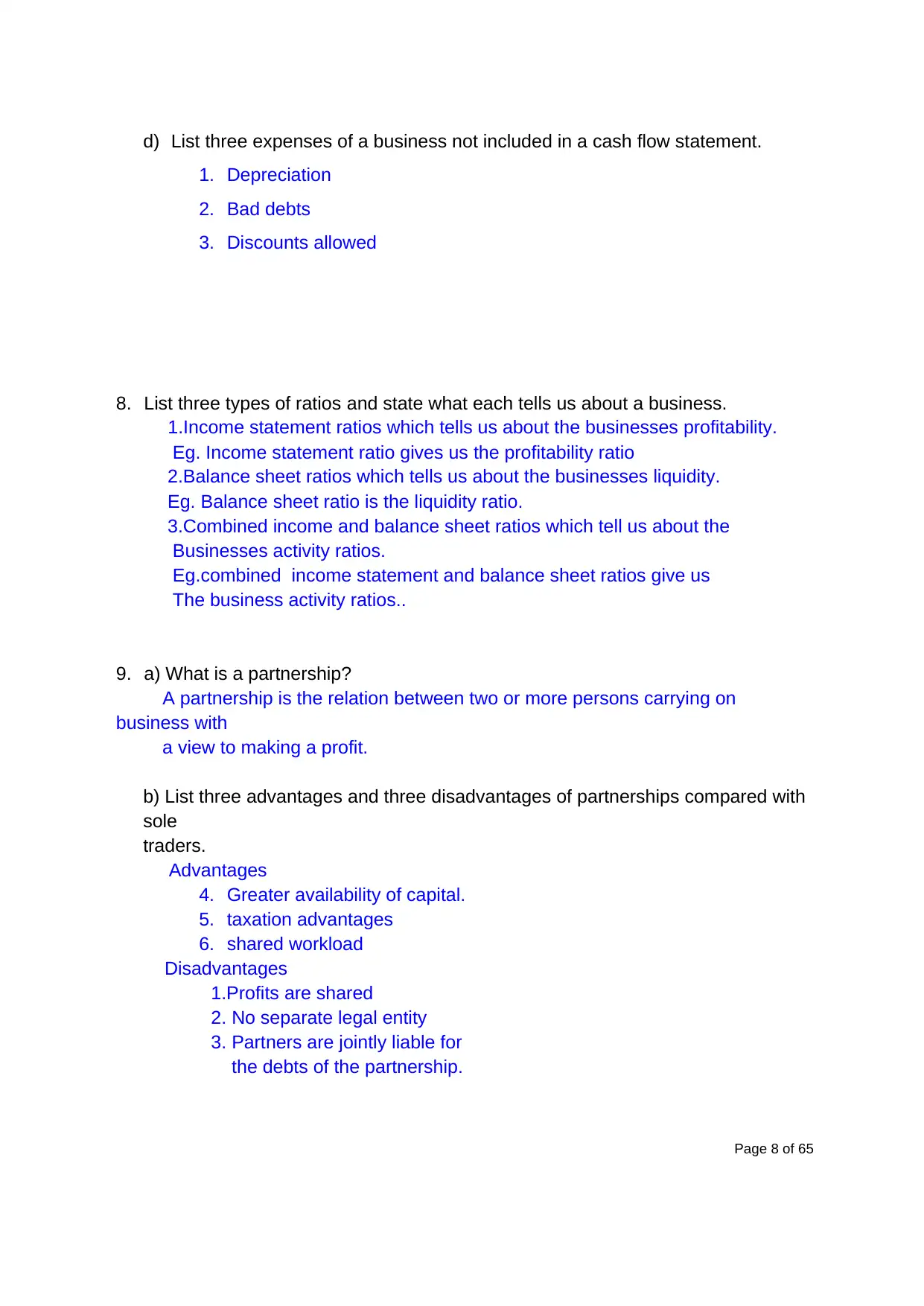

This document presents the complete solution for FNSACC404 Assessment 1, focusing on preparing financial statements for non-reporting entities. The assessment is divided into two parts: Part A comprises written questions covering accounting principles, types of non-reporting entities, relevant legislation, internal controls, cash flow statements, financial ratios, partnerships, not-for-profit organizations, depreciation methods, and the characteristics of non-reporting entities. Part B consists of practical questions, including incomplete records, cash flow statement preparation, and the creation of financial statements based on provided data, such as Income Statements and Balance Sheets. The solution includes the calculation of opening capital, completion of ledger accounts for sales, purchases, and wages, as well as the preparation of Dianna Gordon’s Income Statement and Balance Sheet. It also involves the creation of a Cash Flow Statement for M Sellars, determining which figures to include based on provided data. The solution demonstrates a comprehensive understanding of financial statement preparation and the specific requirements for non-reporting entities.

1 out of 65

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.