FNSACC408 - Business Systems: Bookkeeper Induction Guide and Tasks

VerifiedAdded on 2022/11/13

|10

|3100

|304

Portfolio

AI Summary

This portfolio assignment presents a comprehensive bookkeeper induction guide, designed to assist new bookkeepers in understanding their roles and responsibilities within an organization. The guide details the functions of bookkeeping, including maintaining books of accounts, managing payroll, and preparing financial records using various software like Sage, Xero, Excel, and MYOB. It outlines the roles of other staff members, such as accounting professionals and tax advisors, emphasizing the importance of adhering to accounting standards, ethical codes, and relevant legislation like the Goods and Services Tax Act, Privacy Act, and Corporations Act. The guide also explores internal and external support pathways, including financial accountants, the TPB, ASIC, and the tax office, and covers legislation, regulations, industry standards, and organizational requirements. Furthermore, it addresses finance code of practice, ethical guidelines, activities outside the bookkeeper's scope, necessary tasks, available publications, communication, and reporting requirements, as well as performance review and management processes. The document also provides insights into the software programs utilized, access restrictions, and other resources available to bookkeepers.

Assessment Number 1

Your Name

File Name: Your Name FNSACC408 AT1 Attempt 1

File Name Marking Criteria: Your Name FNSACC408 AT1 MCriteria Attempt 1

Task 1: Bookkeeper Induction Guide

1. Functions of jobs and processes

As per the requirement of the organization, the management of the company

requires new bookkeepers so that the accounting process can be smoothly

undertaken by the business. In respect of the business, the main function of a

bookkeeper which can be identified are listed below in details:

a. The primary function which can be identified for a bookkeeper is related to the

process of maintaining the books of accounts for the business. The books of

accounts are maintained under the supervision of the financial accountant,

b. The bookkeeper also needs to make entries in the books of accounts and

make adjustments as and when required in the same.

c. In addition to this, the book keepers would also be responsible for the payroll

system which is established in the business.

d. The bookkeeper prepares the financial records by posting different

transactions in the books of accounts or accounting software by referring to

source documents such as invoices, customer receipts, notes and memo.

e. The bookkeeper also has the responsibility of maintaining different day books

and general ledger accounts such as cash book, sales day book, purchase

day books.

2. Roles and responsibilities the existing staff

The other staff member who are also engaged in the business are responsible

for different departments which can be associated with the operational

process. In addition to this, the staff members also include accounting

professionals, tax advisors, senior managers who have to comply with

different requirements of the law. The roles and responsibilities of the other

staff members of the business are listed below in details:

a. The accounting professionals needs to adhere to conceptual framework which

is set by IASB while preparing the financial statements and in addition to this

also adhere to relevant accounting standards which are applicable to the

business.

b. The employees and senior staff members needs to ensure that the ethical

code of conduct is followed by the business and ethical standards like APES

110 are followed while conducting the operations of the business.

c. In terms of taxation requirements, the tax advisors and professionals needs to

check with the regulations which are brought about by Australia Tax Office

and Tax Practitioners Board. In addition to this, the agents and tax

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 1

Your Name

File Name: Your Name FNSACC408 AT1 Attempt 1

File Name Marking Criteria: Your Name FNSACC408 AT1 MCriteria Attempt 1

Task 1: Bookkeeper Induction Guide

1. Functions of jobs and processes

As per the requirement of the organization, the management of the company

requires new bookkeepers so that the accounting process can be smoothly

undertaken by the business. In respect of the business, the main function of a

bookkeeper which can be identified are listed below in details:

a. The primary function which can be identified for a bookkeeper is related to the

process of maintaining the books of accounts for the business. The books of

accounts are maintained under the supervision of the financial accountant,

b. The bookkeeper also needs to make entries in the books of accounts and

make adjustments as and when required in the same.

c. In addition to this, the book keepers would also be responsible for the payroll

system which is established in the business.

d. The bookkeeper prepares the financial records by posting different

transactions in the books of accounts or accounting software by referring to

source documents such as invoices, customer receipts, notes and memo.

e. The bookkeeper also has the responsibility of maintaining different day books

and general ledger accounts such as cash book, sales day book, purchase

day books.

2. Roles and responsibilities the existing staff

The other staff member who are also engaged in the business are responsible

for different departments which can be associated with the operational

process. In addition to this, the staff members also include accounting

professionals, tax advisors, senior managers who have to comply with

different requirements of the law. The roles and responsibilities of the other

staff members of the business are listed below in details:

a. The accounting professionals needs to adhere to conceptual framework which

is set by IASB while preparing the financial statements and in addition to this

also adhere to relevant accounting standards which are applicable to the

business.

b. The employees and senior staff members needs to ensure that the ethical

code of conduct is followed by the business and ethical standards like APES

110 are followed while conducting the operations of the business.

c. In terms of taxation requirements, the tax advisors and professionals needs to

check with the regulations which are brought about by Australia Tax Office

and Tax Practitioners Board. In addition to this, the agents and tax

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

professional also needs to follow the regulations which have been brought

about in Tax Agent Service Act 2009 and comply with the same.

3. Networking and support pathways available

The accounting and financial reporting process of the business is under the financial

accountant and the bookkeepers who help him to manage different transactions of

the business (Abdul-Rahamon & Adejare, 2014). The bookkeepers are at the lowest

level of hierarchy and the internal support pathways for the bookkeepers is from the

financial accountant who prepares the financial statements at the ends of the period.

On the other hand, external support pathways for the bookkeepers would be from

the TPB, ASIC and the tax office. These external support pathways often provide

guidance to the bookkeeper in case any situation arises in the business or even in

case of any confusion.

4. Legislation, regulations, industry standards and organisation requirements

There is certain legislation which needs to be followed by a business while following

a reporting framework for presentation of financial information of the business. Some

of the common regulations which a business needs to adhere while reporting

important financial information of the business (Green, 2014). Some of the

regulations which the management of the company needs to adhere to are listed

below in details: Goods and Services Tax) Act 1999: The business needs to adhere to goods

and service tax of 1999 as indirect taxes would be applicable to the business

and therefore proper records needs to be maintained so that how much GST

is paid or payable can be tracked. Retention of financial records: The financial records of a business needs to be

maintained for future use or for comparison between past and present

performance. Privacy Act 1988: The privacy act of 1988 states that the information of the

employees and customers needs to be protected and their privacy should not

be affected in any manner. Corporations Act: The corporation act provides the framework which needs to

be followed by a business for ensuring that the business follows all relevant

rules and regulations while conducting the operations of the business.

The regulations which are set by the management of the company for the company

are listed below in details: The employees should adhere to all the rules and regulations which are set

out in the Corporation Act 2001 The employees would be also be held liable

for any fines if there is a violation in compliance with the regulations.

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 2

about in Tax Agent Service Act 2009 and comply with the same.

3. Networking and support pathways available

The accounting and financial reporting process of the business is under the financial

accountant and the bookkeepers who help him to manage different transactions of

the business (Abdul-Rahamon & Adejare, 2014). The bookkeepers are at the lowest

level of hierarchy and the internal support pathways for the bookkeepers is from the

financial accountant who prepares the financial statements at the ends of the period.

On the other hand, external support pathways for the bookkeepers would be from

the TPB, ASIC and the tax office. These external support pathways often provide

guidance to the bookkeeper in case any situation arises in the business or even in

case of any confusion.

4. Legislation, regulations, industry standards and organisation requirements

There is certain legislation which needs to be followed by a business while following

a reporting framework for presentation of financial information of the business. Some

of the common regulations which a business needs to adhere while reporting

important financial information of the business (Green, 2014). Some of the

regulations which the management of the company needs to adhere to are listed

below in details: Goods and Services Tax) Act 1999: The business needs to adhere to goods

and service tax of 1999 as indirect taxes would be applicable to the business

and therefore proper records needs to be maintained so that how much GST

is paid or payable can be tracked. Retention of financial records: The financial records of a business needs to be

maintained for future use or for comparison between past and present

performance. Privacy Act 1988: The privacy act of 1988 states that the information of the

employees and customers needs to be protected and their privacy should not

be affected in any manner. Corporations Act: The corporation act provides the framework which needs to

be followed by a business for ensuring that the business follows all relevant

rules and regulations while conducting the operations of the business.

The regulations which are set by the management of the company for the company

are listed below in details: The employees should adhere to all the rules and regulations which are set

out in the Corporation Act 2001 The employees would be also be held liable

for any fines if there is a violation in compliance with the regulations.

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 2

The management of the company needs to implement the ethical codes of

APES 110 so that the employees follow the same for maintaining code of

conduct in the operation of the business.

The industry standards which the company needs to adhere to related to the

reporting framework which is used by the business should be same so that

transparency can be maintained in the organization. In addition to this, the function

of bookkeeping is closely associated with the process of reporting and therefore

such a standard need to be maintained by the business.

Organisational Requirements

The company needs to formulate appropriate strategic plans so that a level of

transparency is maintained in the operations and reporting. The reporting framework

which is used by the business needs to be transparent so that the stakeholders are

aware of the activities of the business. The strategic plans help the management to

make decisions relating to the business and also the reports which needs to be

prepared by the business.

The business also needs to prepare operational plan for smooth operations of the

business and effective reporting for all the financial information of the business. The

operation plan sets the timeline which needs to be followed for presenting the

financial information of the business in an effective manner.

The plan and procedure manual provide a guide as to how the transactions needs to

be presented in the books of accounts and what exactly is expected from the

financial accounting department. It also sets the process by which the books of

accounts are prepared by the bookkeepers and then reviewed by the financial

accountant.

5. Finance Code of Practice and ethical guidelines

The code of professional conduct which every finance professional is expected to

adhere to is set out in TPB websites. In addition to this, the company also needs to

adhere to rules and regulations which are set out by accounting standards (Code

obligations | TPB. 2019). In addition to this, the business also needs to be consistent

with the accounting policies and principles which are followed by the business.

The ethical standard which needs to be followed by businesses for managing the

operations of the business and the same are listed below in details: Honesty and integrity Independence Confidentiality Competence Other responsibilities.

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 3

APES 110 so that the employees follow the same for maintaining code of

conduct in the operation of the business.

The industry standards which the company needs to adhere to related to the

reporting framework which is used by the business should be same so that

transparency can be maintained in the organization. In addition to this, the function

of bookkeeping is closely associated with the process of reporting and therefore

such a standard need to be maintained by the business.

Organisational Requirements

The company needs to formulate appropriate strategic plans so that a level of

transparency is maintained in the operations and reporting. The reporting framework

which is used by the business needs to be transparent so that the stakeholders are

aware of the activities of the business. The strategic plans help the management to

make decisions relating to the business and also the reports which needs to be

prepared by the business.

The business also needs to prepare operational plan for smooth operations of the

business and effective reporting for all the financial information of the business. The

operation plan sets the timeline which needs to be followed for presenting the

financial information of the business in an effective manner.

The plan and procedure manual provide a guide as to how the transactions needs to

be presented in the books of accounts and what exactly is expected from the

financial accounting department. It also sets the process by which the books of

accounts are prepared by the bookkeepers and then reviewed by the financial

accountant.

5. Finance Code of Practice and ethical guidelines

The code of professional conduct which every finance professional is expected to

adhere to is set out in TPB websites. In addition to this, the company also needs to

adhere to rules and regulations which are set out by accounting standards (Code

obligations | TPB. 2019). In addition to this, the business also needs to be consistent

with the accounting policies and principles which are followed by the business.

The ethical standard which needs to be followed by businesses for managing the

operations of the business and the same are listed below in details: Honesty and integrity Independence Confidentiality Competence Other responsibilities.

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6. Dealing with activities that are not within the scope of the bookkeeper and

who is to perform these duties

In a business organization, the bookkeeper also needs to perform certain duties

which are not within the scope of his work but the same needs to be performed as

per the requirement of the business (Sangster, 2015). Some of these activities are

listed below in details:

Function Role of Bookkeeper Person Responsible

Assistance in Internal

Audit

Preparation of the process

of internal audit and

providing any assistance

to the internal auditor

Internal Auditor.

Training new recruits Training and guiding new

recruits to handle

accounting software and

also manual books of

accounts

Human Resource

Manager

Preparation of Business

Plan

Development and

formulation of strategies in

a business plan

Operational Manager

7. Activities and tasks required to be completed

The activities and task which is required to be completed by the management of the

company are listed below in details: The primary function which can be identified for a bookkeeper is related to the

process of maintaining the books of accounts for the business. The bookkeeper also needs to make entries in the books of accounts so that

financial statements and different ledger accounts are up to dated. The Bookkeeper would also have the task to make any changes on the

financial statements in case of any errors or rectification.

8. Software programs that are utilised and any access restrictions required

The different software which can be used by the business for maintaining the

financial accounts of the business are listed below in details: Sage: This has become one of the most popular accounting software which

is being used by businesses. Sage Peachtree is used in most of the small

businesses. The main restriction associated with the same is that the software

offers limited format and cannot be customised for different business use. It

has poor customer service and is often considered time consuming. Xero: Xero is a cloud-based accounting software based out of New Zealand

and it is popular due to the various reports which it can produce. The main

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 4

who is to perform these duties

In a business organization, the bookkeeper also needs to perform certain duties

which are not within the scope of his work but the same needs to be performed as

per the requirement of the business (Sangster, 2015). Some of these activities are

listed below in details:

Function Role of Bookkeeper Person Responsible

Assistance in Internal

Audit

Preparation of the process

of internal audit and

providing any assistance

to the internal auditor

Internal Auditor.

Training new recruits Training and guiding new

recruits to handle

accounting software and

also manual books of

accounts

Human Resource

Manager

Preparation of Business

Plan

Development and

formulation of strategies in

a business plan

Operational Manager

7. Activities and tasks required to be completed

The activities and task which is required to be completed by the management of the

company are listed below in details: The primary function which can be identified for a bookkeeper is related to the

process of maintaining the books of accounts for the business. The bookkeeper also needs to make entries in the books of accounts so that

financial statements and different ledger accounts are up to dated. The Bookkeeper would also have the task to make any changes on the

financial statements in case of any errors or rectification.

8. Software programs that are utilised and any access restrictions required

The different software which can be used by the business for maintaining the

financial accounts of the business are listed below in details: Sage: This has become one of the most popular accounting software which

is being used by businesses. Sage Peachtree is used in most of the small

businesses. The main restriction associated with the same is that the software

offers limited format and cannot be customised for different business use. It

has poor customer service and is often considered time consuming. Xero: Xero is a cloud-based accounting software based out of New Zealand

and it is popular due to the various reports which it can produce. The main

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

restriction associated with the XERO software is that it is quite costly and it is

not a good option in case of numerous transactions. Excel Software: The excel software is the most commonly used software for

accounting and it is used to create spreadsheets for recording financial

information. The main restriction associated with the same is that the other

accounting software are much more advanced than this and offers more

options. MYOB Software: This is also one of the software which is used by

businesses for recording financial transactions of a business. The major

restrictions associated with the same is that the software is not user friendly

and it can get complex.

9. Publications and other resources available

The publications and other resources which needs to be available to the bookkeeper

are listed below in details: Ledger accounts which is maintained by the business. TPB guidelines needs to be followed by the business. Fair Work Australia regulations needs to be followed as per ATO guidelines ASIC guidelines

10. Communication and reporting requirements within the organisation

The bookkeeper would be needing different ledger book accounts for preparing the

general ledgers and the financial statements of the business (Boyns, Edwards &

Nikitin, 2013). The main use of the ledger accounts is to ensure that transactions are

genuinely entered or not and also the process facilitates double entry system of

accounting. The ledger accounts also ensure that the main books of accounts are

followed and financial statements are prepared on the basis of the same. The

debtors and creditors report provide important information relating to the credit sales

and credit purchases. The credit sales and purchases are important as they have

direct impact on the profitability of the business. The bookkeeper also would be

requiring information relating to inventory and cash. The inventory and cash

information are also considered to be important while at the same time it is used for

preparing the balance sheet of the business.

11. Performance review and management processes

The management of the company needs to undertake regular review of the financial

performance of the business and also ensure that all the guidelines are being

followed by the staff members. In addition to this, review also needs to be made on

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 5

not a good option in case of numerous transactions. Excel Software: The excel software is the most commonly used software for

accounting and it is used to create spreadsheets for recording financial

information. The main restriction associated with the same is that the other

accounting software are much more advanced than this and offers more

options. MYOB Software: This is also one of the software which is used by

businesses for recording financial transactions of a business. The major

restrictions associated with the same is that the software is not user friendly

and it can get complex.

9. Publications and other resources available

The publications and other resources which needs to be available to the bookkeeper

are listed below in details: Ledger accounts which is maintained by the business. TPB guidelines needs to be followed by the business. Fair Work Australia regulations needs to be followed as per ATO guidelines ASIC guidelines

10. Communication and reporting requirements within the organisation

The bookkeeper would be needing different ledger book accounts for preparing the

general ledgers and the financial statements of the business (Boyns, Edwards &

Nikitin, 2013). The main use of the ledger accounts is to ensure that transactions are

genuinely entered or not and also the process facilitates double entry system of

accounting. The ledger accounts also ensure that the main books of accounts are

followed and financial statements are prepared on the basis of the same. The

debtors and creditors report provide important information relating to the credit sales

and credit purchases. The credit sales and purchases are important as they have

direct impact on the profitability of the business. The bookkeeper also would be

requiring information relating to inventory and cash. The inventory and cash

information are also considered to be important while at the same time it is used for

preparing the balance sheet of the business.

11. Performance review and management processes

The management of the company needs to undertake regular review of the financial

performance of the business and also ensure that all the guidelines are being

followed by the staff members. In addition to this, review also needs to be made on

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 5

the financial reports which is prepared by the business and ensure that the same are

showing accurate view of the financial position of the business. The review can be

done in monthly basis or quarterly basis depending on the decisions of the

management of the company. Th review of performance would be involving use of

different tools such as budgeting and standard costing for ascertaining the

performance of the business. In addition to this, the non-financial performance of the

business would be reviewed on the basis of certain indicators such as employee

turnover, satisfaction of the employees, efficiency level in operations and support

departments.

Task 2: Peer Review Survey

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 6

showing accurate view of the financial position of the business. The review can be

done in monthly basis or quarterly basis depending on the decisions of the

management of the company. Th review of performance would be involving use of

different tools such as budgeting and standard costing for ascertaining the

performance of the business. In addition to this, the non-financial performance of the

business would be reviewed on the basis of certain indicators such as employee

turnover, satisfaction of the employees, efficiency level in operations and support

departments.

Task 2: Peer Review Survey

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

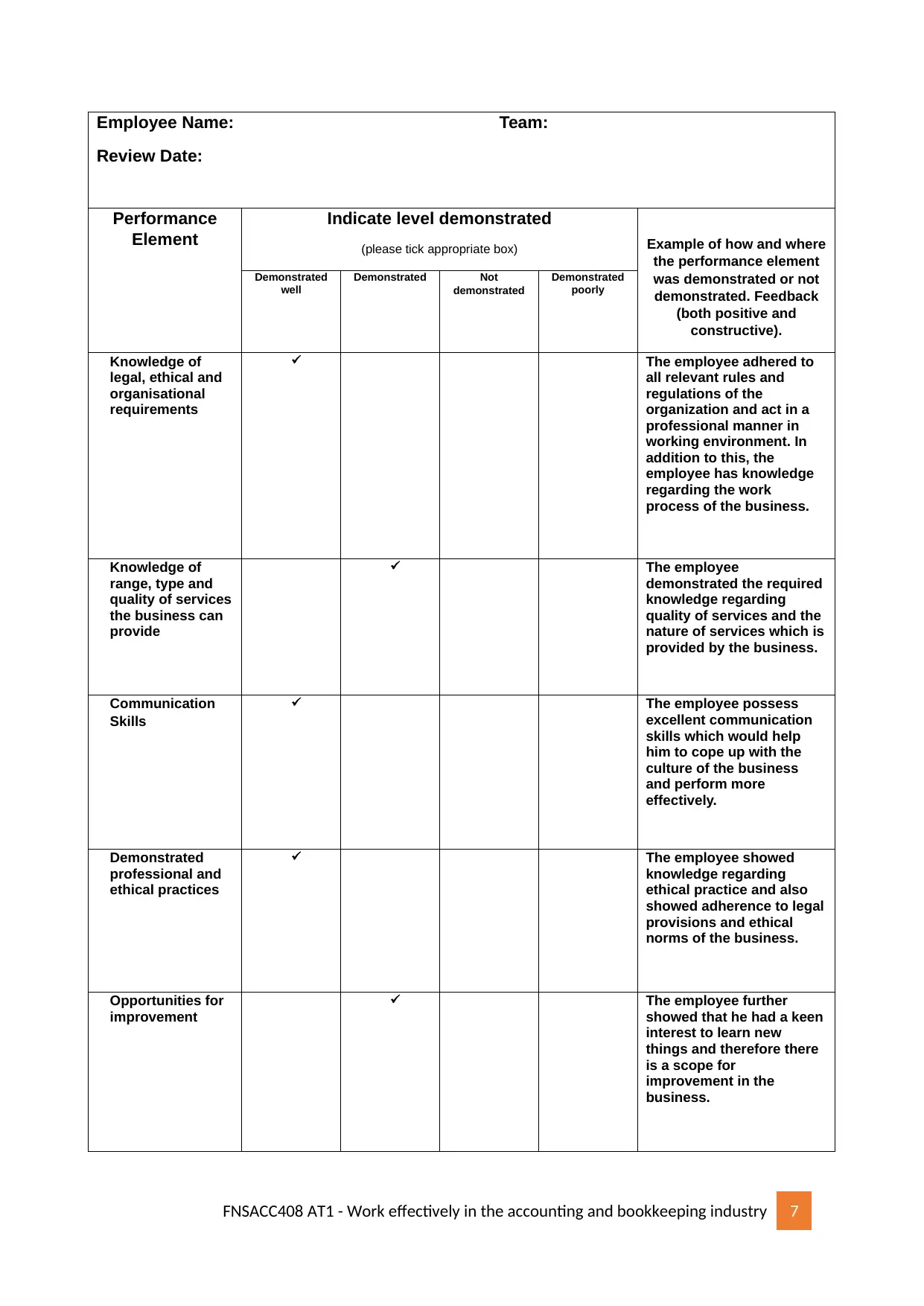

Employee Name: Team:

Review Date:

Performance

Element

Indicate level demonstrated

(please tick appropriate box) Example of how and where

the performance element

was demonstrated or not

demonstrated. Feedback

(both positive and

constructive).

Demonstrated

well

Demonstrated Not

demonstrated

Demonstrated

poorly

Knowledge of

legal, ethical and

organisational

requirements

The employee adhered to

all relevant rules and

regulations of the

organization and act in a

professional manner in

working environment. In

addition to this, the

employee has knowledge

regarding the work

process of the business.

Knowledge of

range, type and

quality of services

the business can

provide

The employee

demonstrated the required

knowledge regarding

quality of services and the

nature of services which is

provided by the business.

Communication

Skills

The employee possess

excellent communication

skills which would help

him to cope up with the

culture of the business

and perform more

effectively.

Demonstrated

professional and

ethical practices

The employee showed

knowledge regarding

ethical practice and also

showed adherence to legal

provisions and ethical

norms of the business.

Opportunities for

improvement

The employee further

showed that he had a keen

interest to learn new

things and therefore there

is a scope for

improvement in the

business.

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 7

Review Date:

Performance

Element

Indicate level demonstrated

(please tick appropriate box) Example of how and where

the performance element

was demonstrated or not

demonstrated. Feedback

(both positive and

constructive).

Demonstrated

well

Demonstrated Not

demonstrated

Demonstrated

poorly

Knowledge of

legal, ethical and

organisational

requirements

The employee adhered to

all relevant rules and

regulations of the

organization and act in a

professional manner in

working environment. In

addition to this, the

employee has knowledge

regarding the work

process of the business.

Knowledge of

range, type and

quality of services

the business can

provide

The employee

demonstrated the required

knowledge regarding

quality of services and the

nature of services which is

provided by the business.

Communication

Skills

The employee possess

excellent communication

skills which would help

him to cope up with the

culture of the business

and perform more

effectively.

Demonstrated

professional and

ethical practices

The employee showed

knowledge regarding

ethical practice and also

showed adherence to legal

provisions and ethical

norms of the business.

Opportunities for

improvement

The employee further

showed that he had a keen

interest to learn new

things and therefore there

is a scope for

improvement in the

business.

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 3: BAS Lodgement Instructions

1. Gather required information

The bookkeeper needs to gather relevant information for the purpose of forming the

financial statements of the business. Some of the information which needs to be

collected by the Bookkeeper are listed below in details: Purchase invoices: The purchases are handled by the purchase department

and therefore purchases invoices would be required Sales invoices: The sales of the business depend on the sales department of

the company and invoices are prepared according to such conditions. The

information of such sales department needs to be presented so that the same

can be appropriately presented in the books of accounts. Payroll information and PAYG Summaries: The payroll information and PAYG

information also needs to be provided to the bookkeeper for preparation of the

financial statements. Cash Records: Another major source of information for a business is the cash

statements which is prepared by the business showing cash transactions of

the business.

2. Manage client discussions

The first step in managing the information which is provided by the client and

understand the nature of the business of the clients so that appropriate services can

be provided to the clients. The agent needs to take all the familiar steps in

familiarizing the nature of the business of the client. The agent would also needs to

discuss with the client regarding the services which the agent would be providing.

Another manner of showing that the business is dedicated towards the needs of the

client is by conducting regular meeting and discussing with the client regarding any

changes in the nature of the business.

3. Prepare documents for compliance

The management of the company also needs to prepare documents for compliance

which would help the business to keep track of the reports which is required to be

prepared such as BAS, Payroll, P&L, Balance Sheet, Cash Flow, Bank

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 8

1. Gather required information

The bookkeeper needs to gather relevant information for the purpose of forming the

financial statements of the business. Some of the information which needs to be

collected by the Bookkeeper are listed below in details: Purchase invoices: The purchases are handled by the purchase department

and therefore purchases invoices would be required Sales invoices: The sales of the business depend on the sales department of

the company and invoices are prepared according to such conditions. The

information of such sales department needs to be presented so that the same

can be appropriately presented in the books of accounts. Payroll information and PAYG Summaries: The payroll information and PAYG

information also needs to be provided to the bookkeeper for preparation of the

financial statements. Cash Records: Another major source of information for a business is the cash

statements which is prepared by the business showing cash transactions of

the business.

2. Manage client discussions

The first step in managing the information which is provided by the client and

understand the nature of the business of the clients so that appropriate services can

be provided to the clients. The agent needs to take all the familiar steps in

familiarizing the nature of the business of the client. The agent would also needs to

discuss with the client regarding the services which the agent would be providing.

Another manner of showing that the business is dedicated towards the needs of the

client is by conducting regular meeting and discussing with the client regarding any

changes in the nature of the business.

3. Prepare documents for compliance

The management of the company also needs to prepare documents for compliance

which would help the business to keep track of the reports which is required to be

prepared such as BAS, Payroll, P&L, Balance Sheet, Cash Flow, Bank

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 8

reconciliations. The business also needs to comply with all rules and regulations of

the business

4. Meet timeline for compliance and implementation

The business also needs to consider the timeline for the project and therefore

conduct the operations of the business according so that the business is able to

meet the deadline which is set out by the clients or the management of the company.

The deadline of regulatory bodies also needs to be considered of ATO, ASIC.

5. Access support if issues arise in the preparation

The management of the company can access support from parties such as

accountants and financial advisors regarding the different reports which is required

to be prepared by the business. Plus, external support can also be taken from TPB

and financial accounting bodies. The accounting bodies can provide a clear view

regarding any doubts which is faced by the business while conducting the

operations. This would ensure that proper accounting practices is followed in the

business.

6. Monitor and review procedures including processes for improvements

The management of the company also needs to follow the following processes for

monitoring the processes for improvements: Familiarise with the organisations Policies and Procedures, specifically relevant

to bookkeeping and accounting activities Be familiar with the organisations Continuous Improvement Policy and

Procedures Attend professional body workshops and seminars Complete regular professional development events

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 9

the business

4. Meet timeline for compliance and implementation

The business also needs to consider the timeline for the project and therefore

conduct the operations of the business according so that the business is able to

meet the deadline which is set out by the clients or the management of the company.

The deadline of regulatory bodies also needs to be considered of ATO, ASIC.

5. Access support if issues arise in the preparation

The management of the company can access support from parties such as

accountants and financial advisors regarding the different reports which is required

to be prepared by the business. Plus, external support can also be taken from TPB

and financial accounting bodies. The accounting bodies can provide a clear view

regarding any doubts which is faced by the business while conducting the

operations. This would ensure that proper accounting practices is followed in the

business.

6. Monitor and review procedures including processes for improvements

The management of the company also needs to follow the following processes for

monitoring the processes for improvements: Familiarise with the organisations Policies and Procedures, specifically relevant

to bookkeeping and accounting activities Be familiar with the organisations Continuous Improvement Policy and

Procedures Attend professional body workshops and seminars Complete regular professional development events

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Abdul-Rahamon, O. A., & Adejare, A. T. (2014). The analysis of the impact of

accounting records keeping on the performance of the small scale

enterprises. International Journal of Academic Research in Business

and Social Sciences, 4(1), 1-17.

Boyns, T., Edwards, J. R., & Nikitin, M. (2013). The birth of industrial

accounting in France and Britain. Routledge.

Code obligations | TPB. (2019). Tpb.gov.au. Retrieved 25 July 2019, from

https://www.tpb.gov.au/code-obligations

Green, W. L. (2014). History and Survey of Accountancy (RLE Accounting).

Routledge.

Sangster, A. (2015). The genesis of double entry bookkeeping. The Accounting

Review, 91(1), 299-315.

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 1

0

Abdul-Rahamon, O. A., & Adejare, A. T. (2014). The analysis of the impact of

accounting records keeping on the performance of the small scale

enterprises. International Journal of Academic Research in Business

and Social Sciences, 4(1), 1-17.

Boyns, T., Edwards, J. R., & Nikitin, M. (2013). The birth of industrial

accounting in France and Britain. Routledge.

Code obligations | TPB. (2019). Tpb.gov.au. Retrieved 25 July 2019, from

https://www.tpb.gov.au/code-obligations

Green, W. L. (2014). History and Survey of Accountancy (RLE Accounting).

Routledge.

Sangster, A. (2015). The genesis of double entry bookkeeping. The Accounting

Review, 91(1), 299-315.

FNSACC408 AT1 - Work effectively in the accounting and bookkeeping industry 1

0

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.