FNSACC412: Prepare Operational Budgets - Assessment 3 with Template

VerifiedAdded on 2023/06/10

|12

|1437

|397

Homework Assignment

AI Summary

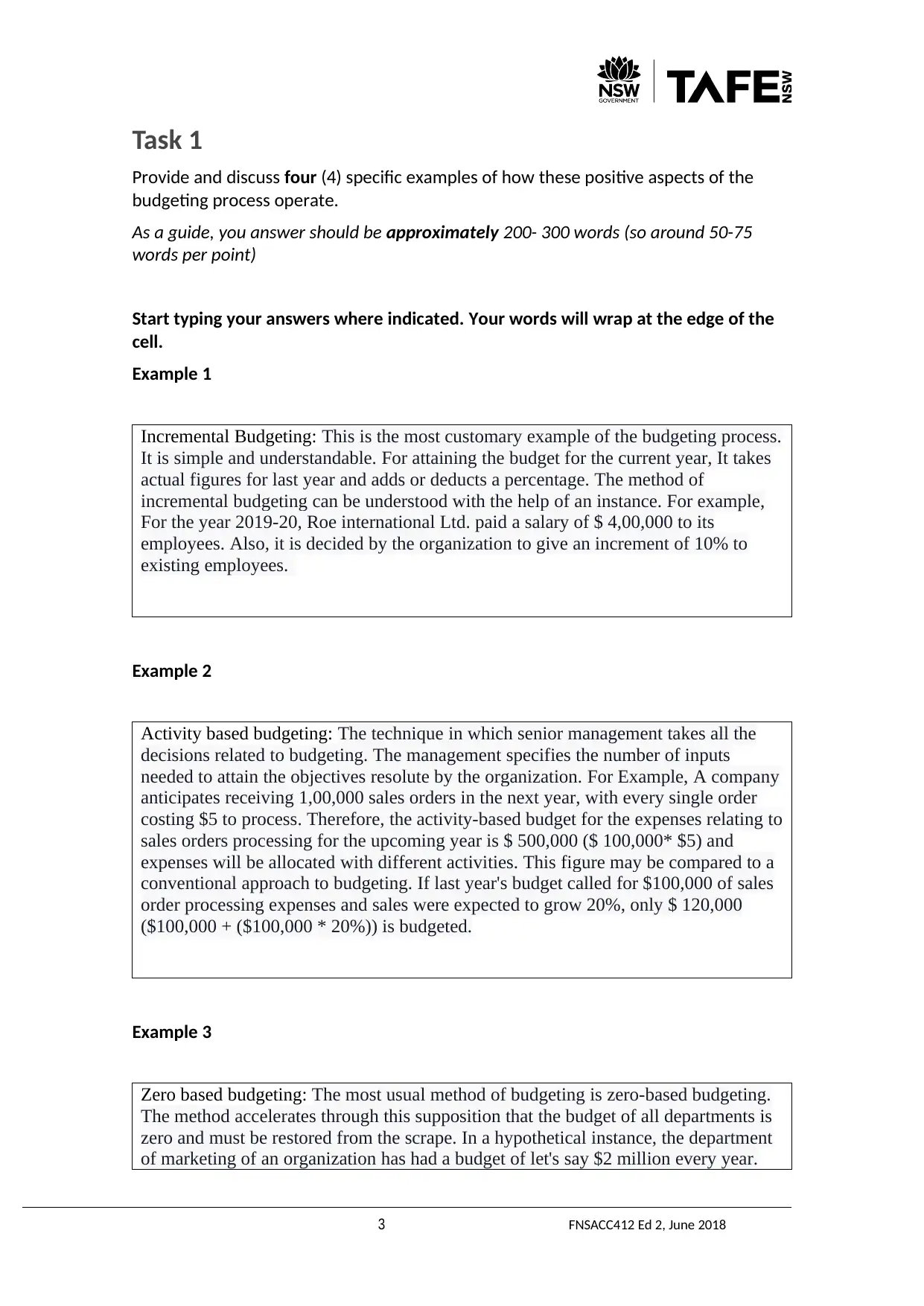

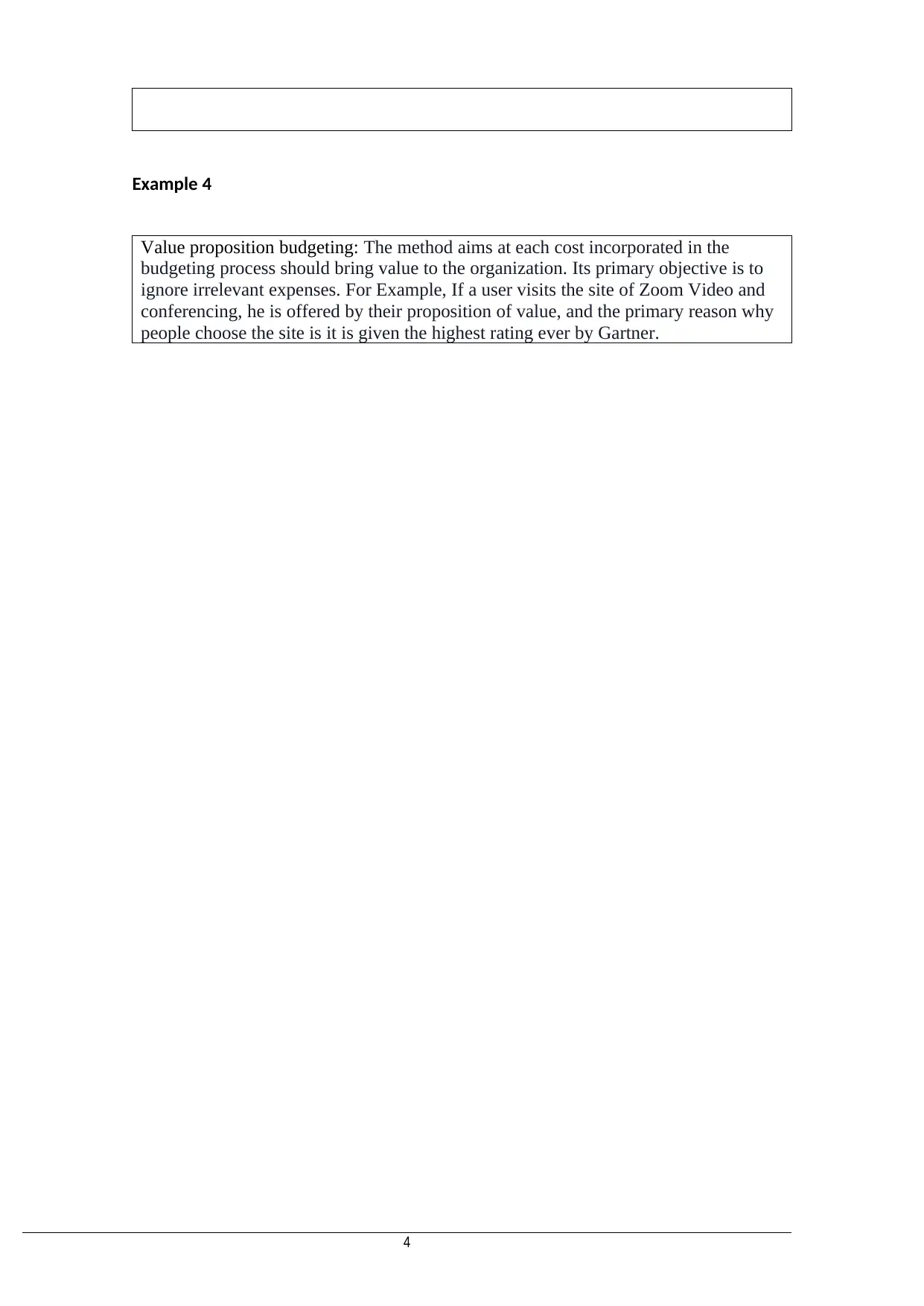

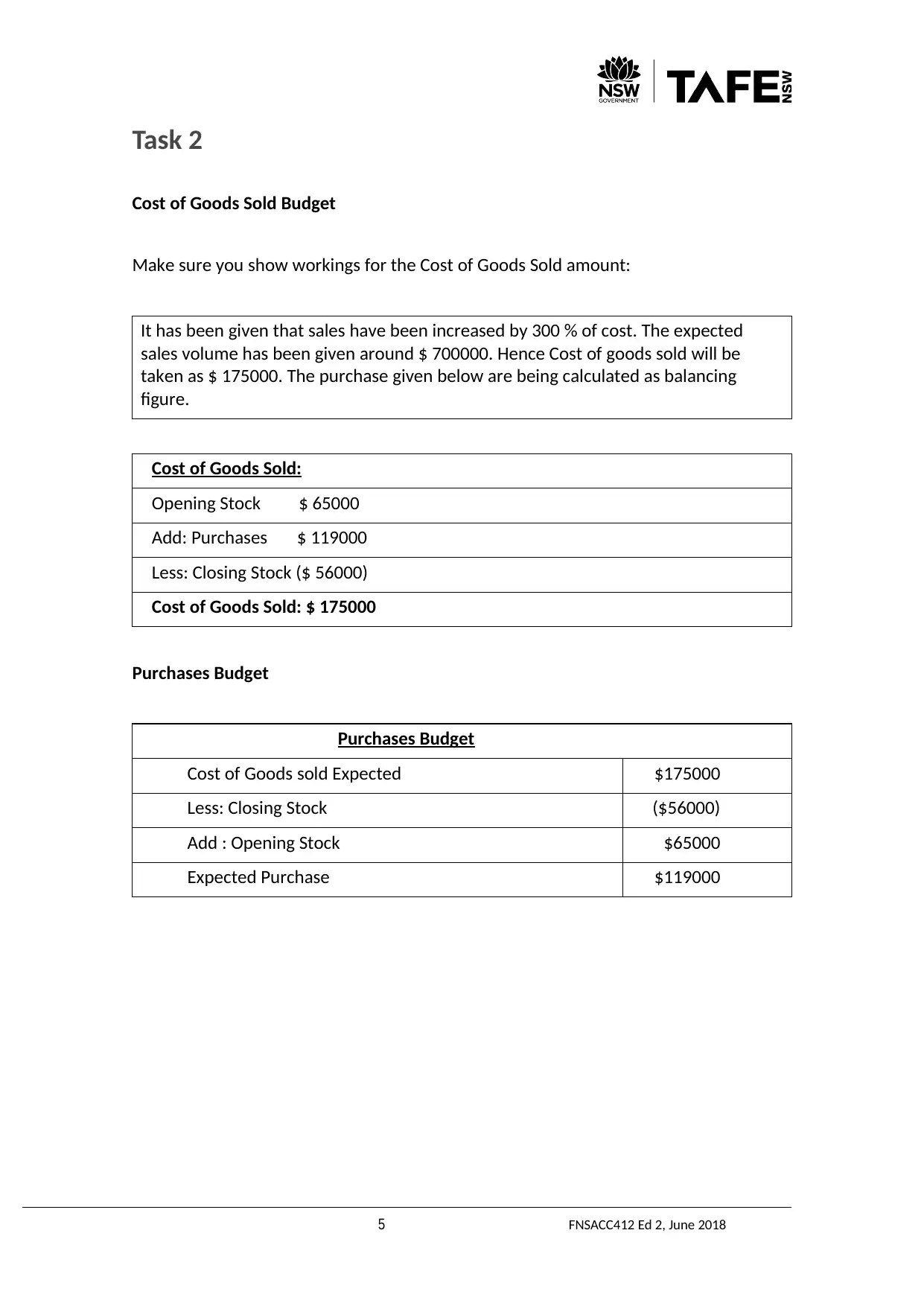

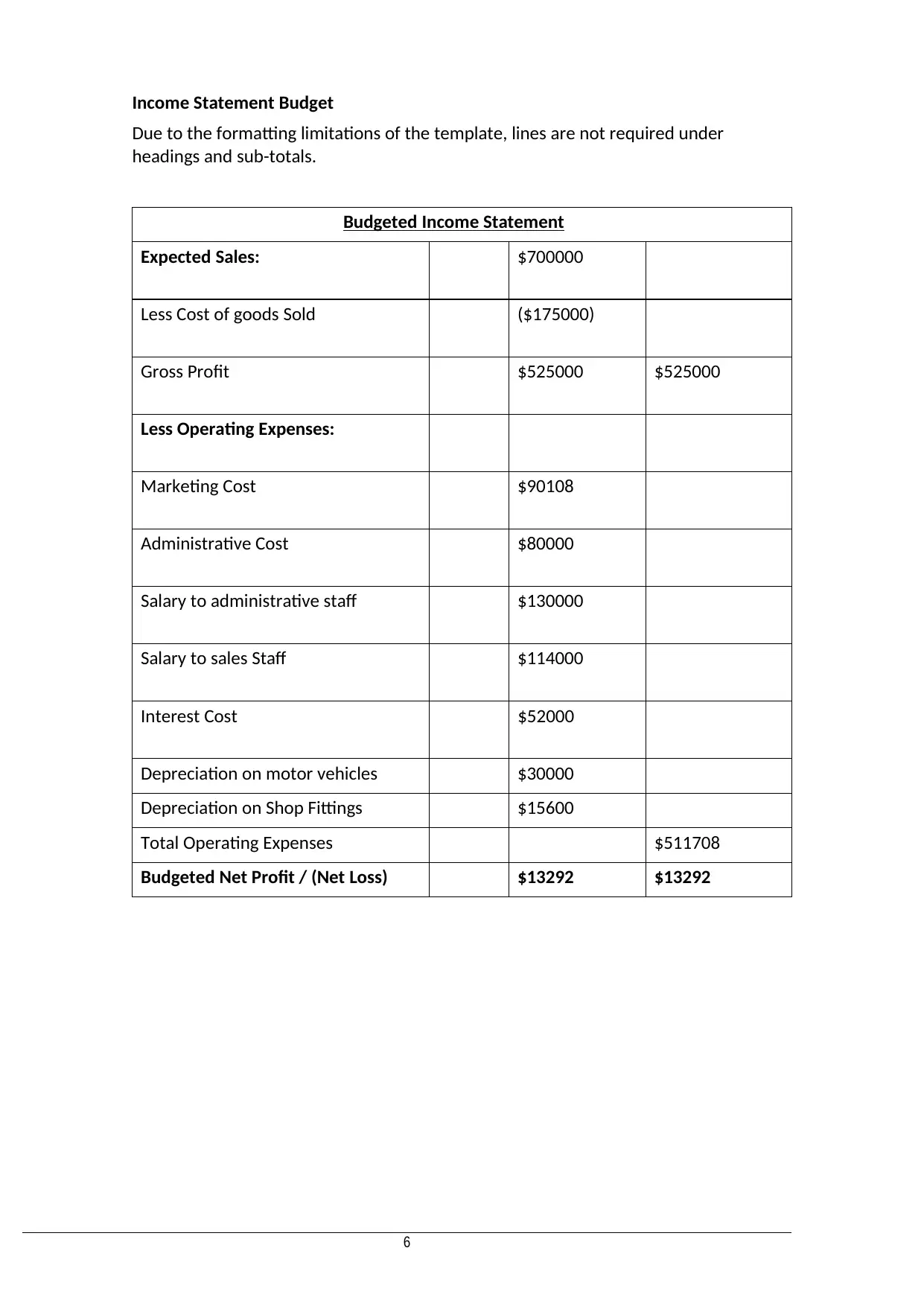

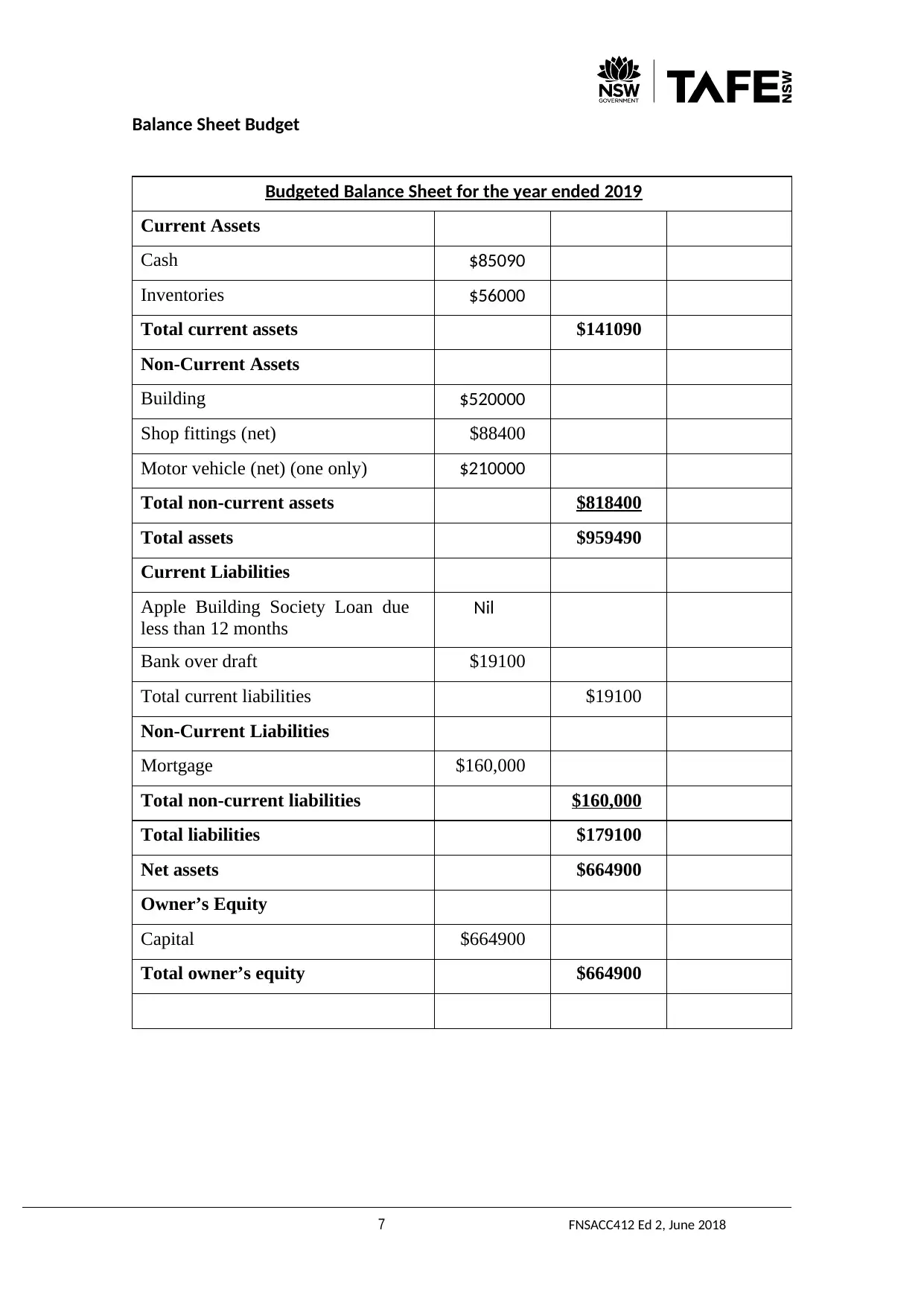

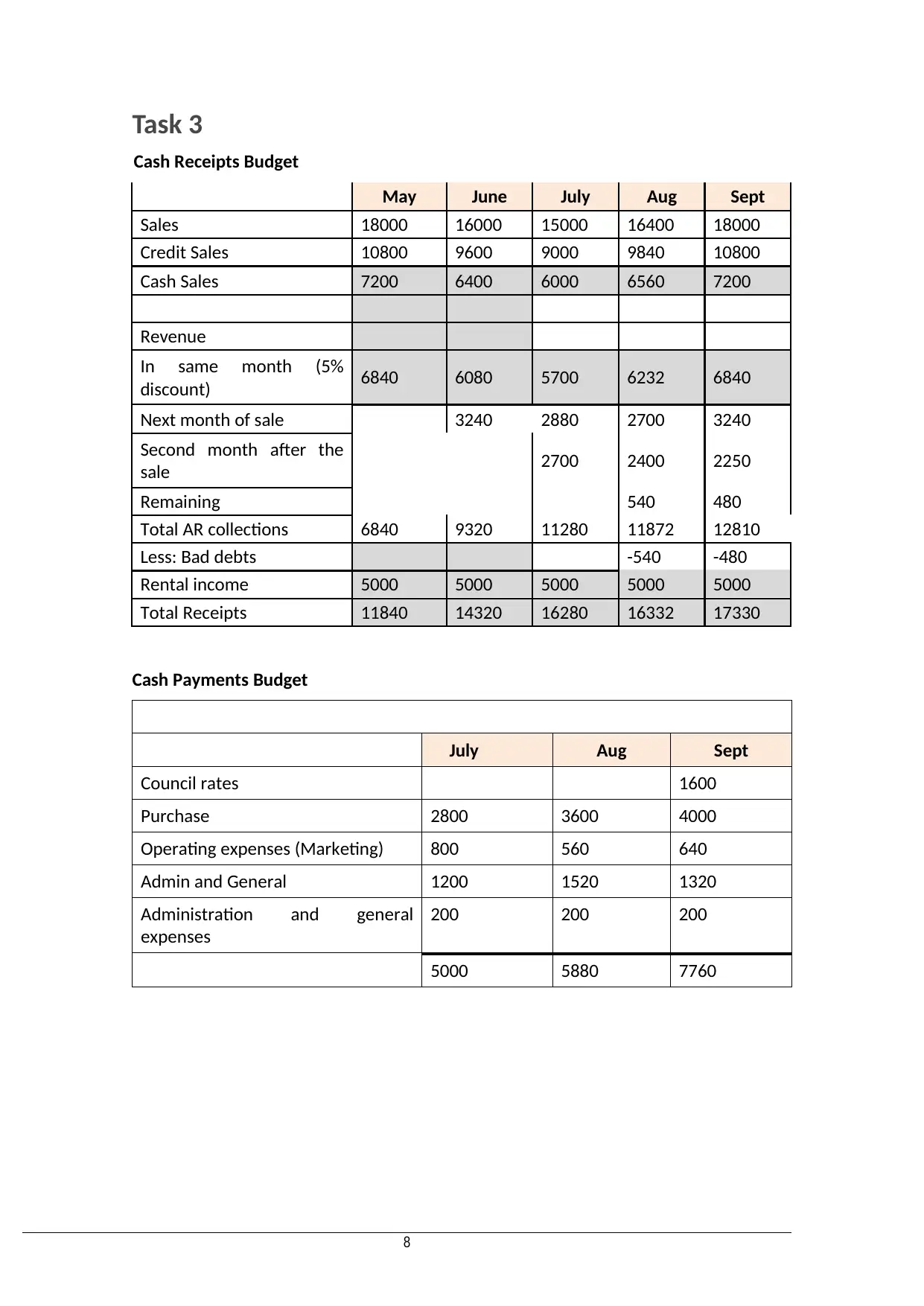

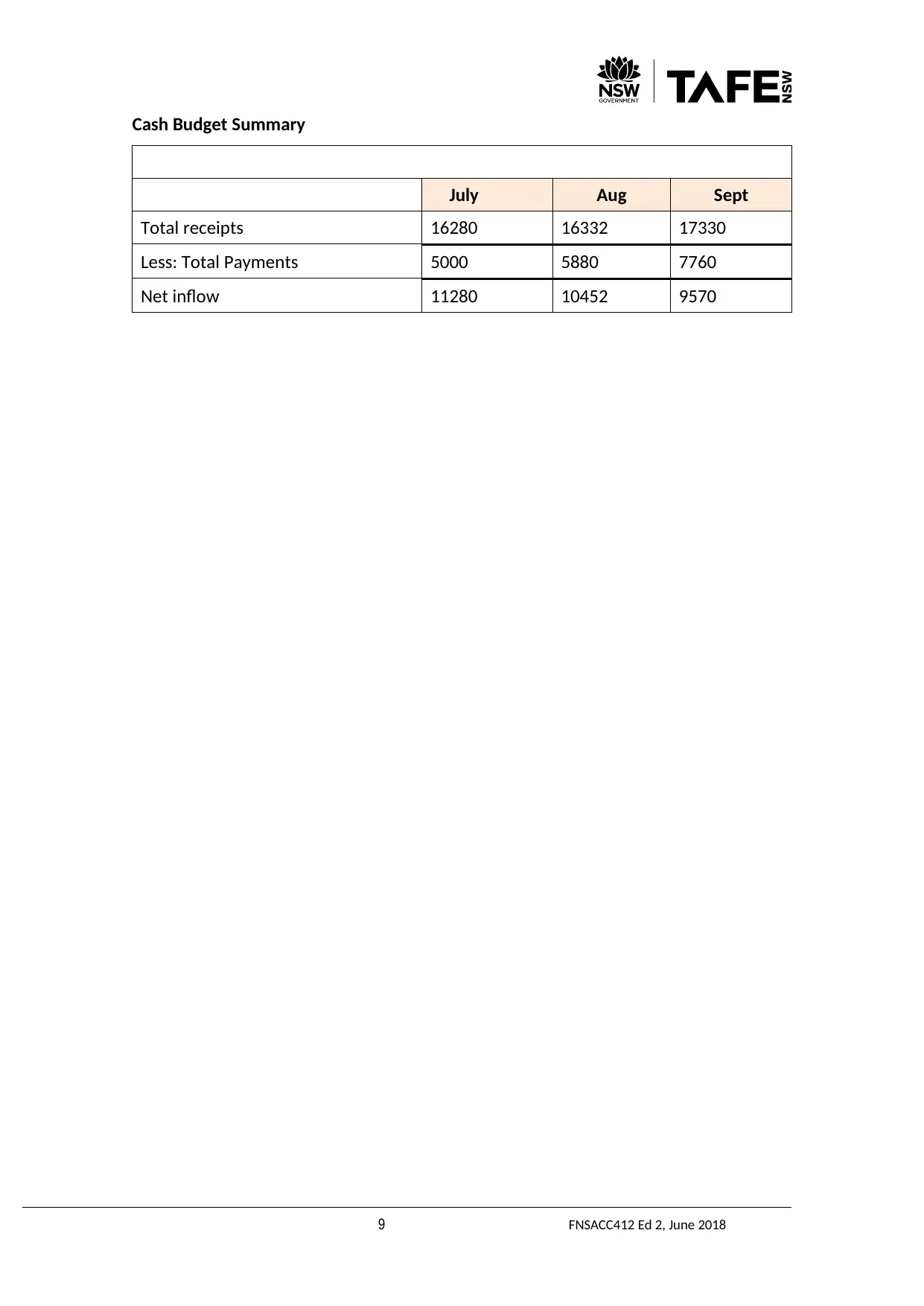

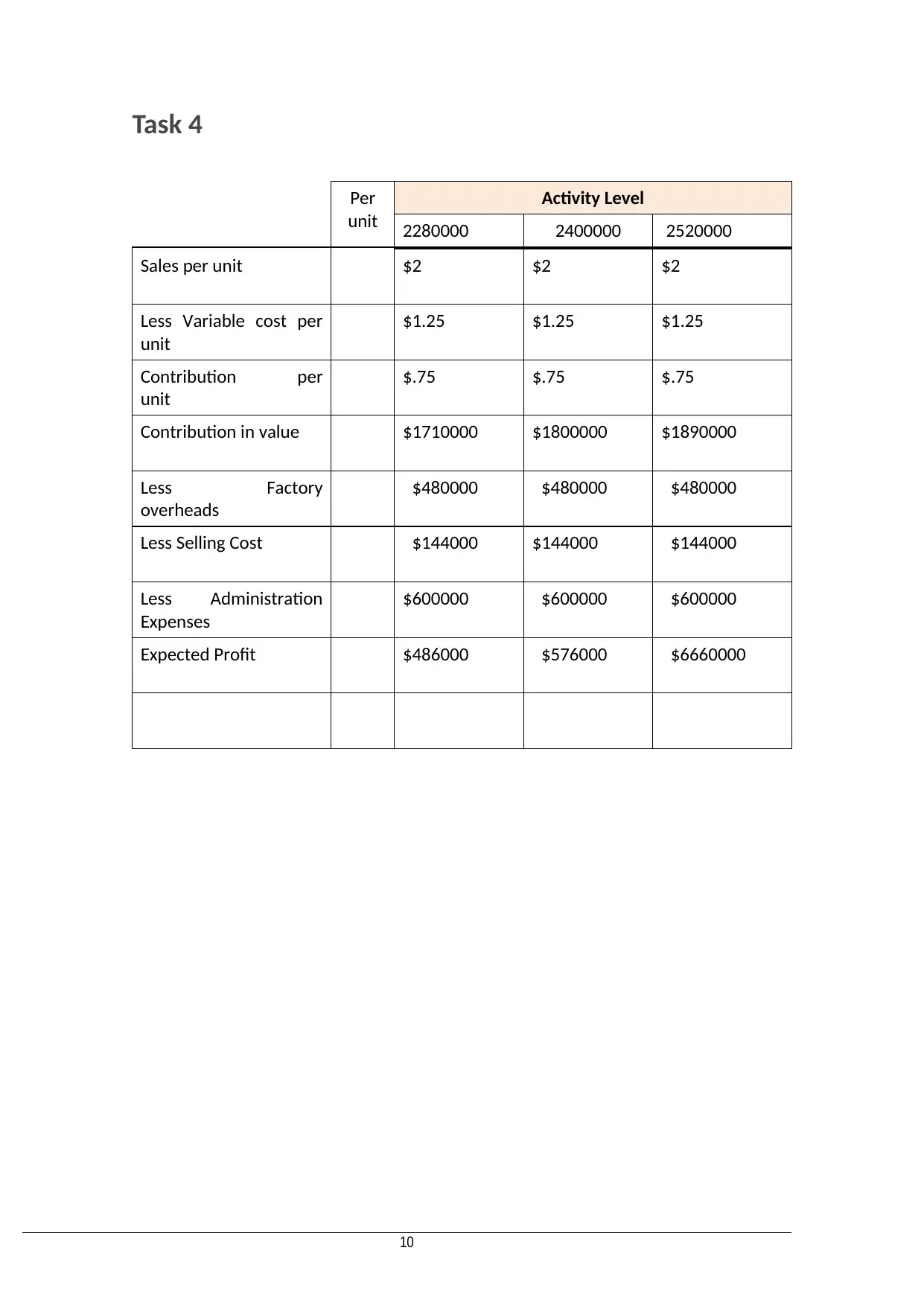

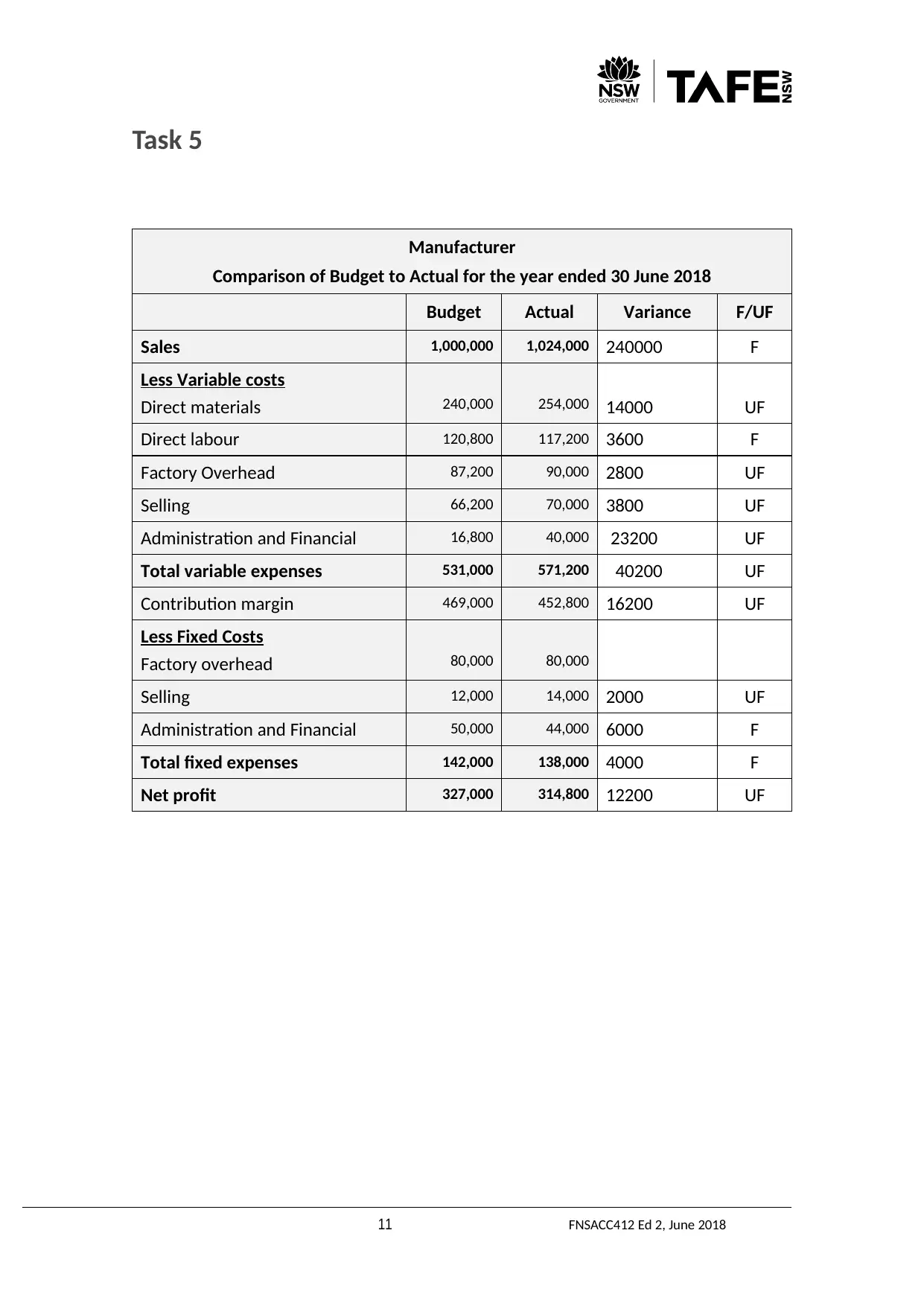

This document provides a comprehensive solution to FNSACC412 Assessment 3, which focuses on preparing operational budgets. The solution includes detailed explanations and calculations for various tasks, including incremental budgeting, activity-based budgeting, and zero-based budgeting. It covers the preparation of a Cost of Goods Sold budget, a Purchases Budget, an Income Statement Budget, and a Balance Sheet Budget. Furthermore, the solution includes a Cash Receipts Budget, a Cash Payments Budget, and a Cash Budget Summary. It also addresses flexible budgeting and performance reporting, with a comparison of budget to actual figures. The document concludes with references to relevant academic sources. Desklib is a valuable resource for students seeking similar solved assignments and study materials.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.