FNSACC501 - Assessment 2: Financial and Business Performance Report

VerifiedAdded on 2020/11/12

|17

|3816

|184

Report

AI Summary

This report, a solution to FNSACC501 Assessment 2, delves into providing financial and business performance information. It covers various aspects, including the treatment of business expenses under tax legislation, allowances for businesses managed by trusts, and the concept of forecast returns. The report also analyzes adherence to financial policies by Not-for-Profit (NFP) organizations, repayment amounts, and business performance objectives. It explores the concept of General Purpose Financial Report Users (GPFRU), state and territory charges, and tax calculations on land. Furthermore, it examines practices for businesses paying Commonwealth taxes, financial information sought by clients, and different financial options. The report includes variance analysis of forecast returns, a quarterly financial management questionnaire, and file notes addressing financial issues. It also discusses the role of a financial manager in preparing Business Activity Statements (BAS) and assessing Goods and Services Tax (GST).

FNSACC501-Provide

Financial and Business

Performance Information

(Assessment 2)

Financial and Business

Performance Information

(Assessment 2)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Part 1................................................................................................................................................3

1. Treatment of Business Expenses in regard to Tax Legislation................................................3

2. Allowance provided to businesses managed on behalf of a trust............................................3

3. Concept of Forecast Returns and Set-Up ................................................................................3

4. Adherence to Financial Policies by NFP Sector Organisations based on their statutory

returns..........................................................................................................................................3

5. Repayment amounts and current balance for XYZ..................................................................3

6. Four categories that client’s business performance objectives can be set up as......................4

7.Concept of GPFRU and its potential users...............................................................................4

8. Type of clients that can expect state and territory charges......................................................4

9. Calculating the amount of taxes and charges on land..............................................................5

10. Practices that businesses who pay Commonwealth taxes must adopt...................................5

TASK 2............................................................................................................................................5

1....................................................................................................................................................5

2....................................................................................................................................................5

3....................................................................................................................................................6

4....................................................................................................................................................6

5....................................................................................................................................................6

6....................................................................................................................................................6

7....................................................................................................................................................8

8....................................................................................................................................................8

9....................................................................................................................................................8

10..................................................................................................................................................9

11..................................................................................................................................................9

12..................................................................................................................................................9

13................................................................................................................................................10

14................................................................................................................................................10

15................................................................................................................................................11

16................................................................................................................................................11

Part 1................................................................................................................................................3

1. Treatment of Business Expenses in regard to Tax Legislation................................................3

2. Allowance provided to businesses managed on behalf of a trust............................................3

3. Concept of Forecast Returns and Set-Up ................................................................................3

4. Adherence to Financial Policies by NFP Sector Organisations based on their statutory

returns..........................................................................................................................................3

5. Repayment amounts and current balance for XYZ..................................................................3

6. Four categories that client’s business performance objectives can be set up as......................4

7.Concept of GPFRU and its potential users...............................................................................4

8. Type of clients that can expect state and territory charges......................................................4

9. Calculating the amount of taxes and charges on land..............................................................5

10. Practices that businesses who pay Commonwealth taxes must adopt...................................5

TASK 2............................................................................................................................................5

1....................................................................................................................................................5

2....................................................................................................................................................5

3....................................................................................................................................................6

4....................................................................................................................................................6

5....................................................................................................................................................6

6....................................................................................................................................................6

7....................................................................................................................................................8

8....................................................................................................................................................8

9....................................................................................................................................................8

10..................................................................................................................................................9

11..................................................................................................................................................9

12..................................................................................................................................................9

13................................................................................................................................................10

14................................................................................................................................................10

15................................................................................................................................................11

16................................................................................................................................................11

17................................................................................................................................................11

18................................................................................................................................................12

19................................................................................................................................................12

20................................................................................................................................................13

21................................................................................................................................................13

REFERENCES..............................................................................................................................14

18................................................................................................................................................12

19................................................................................................................................................12

20................................................................................................................................................13

21................................................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 1

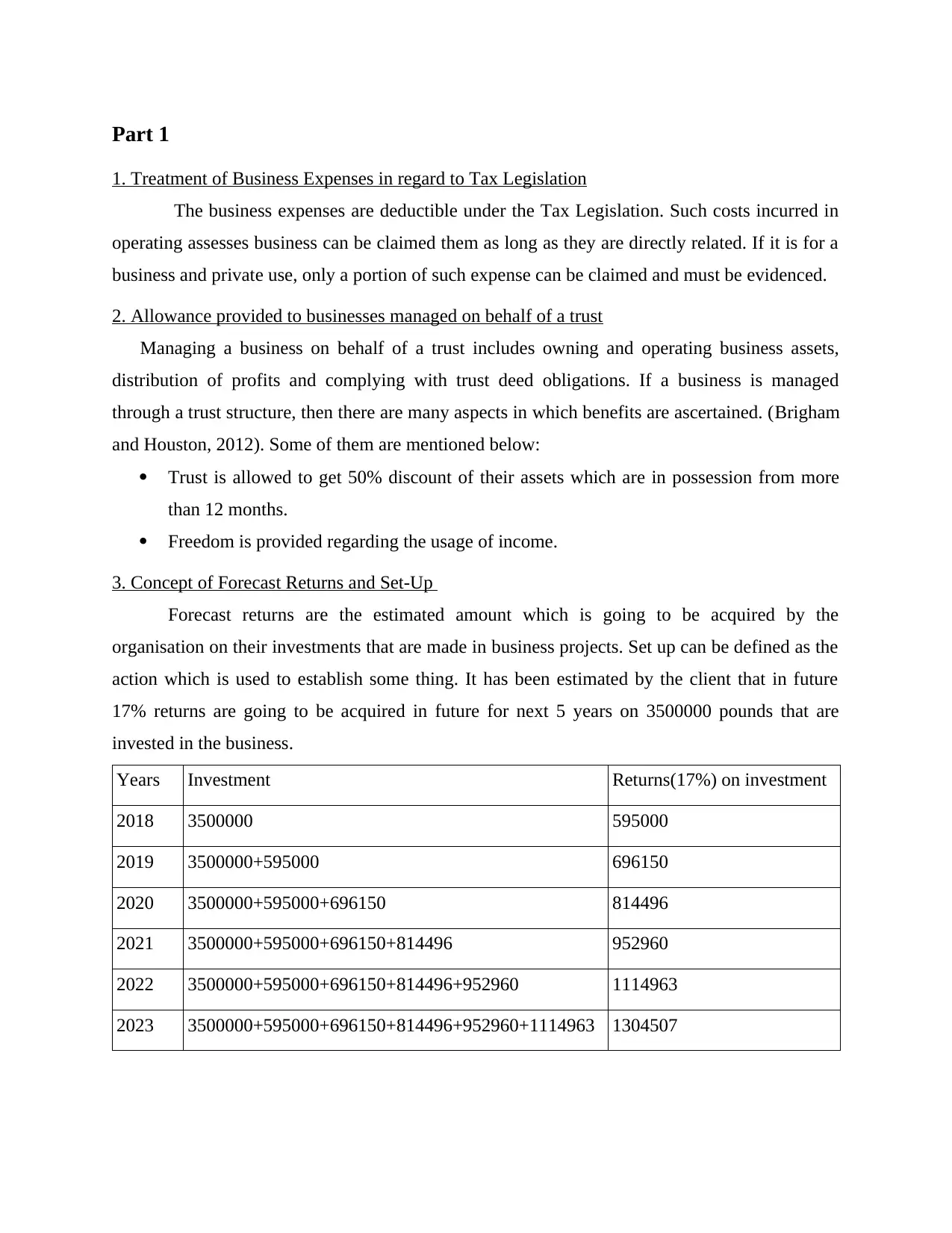

1. Treatment of Business Expenses in regard to Tax Legislation

The business expenses are deductible under the Tax Legislation. Such costs incurred in

operating assesses business can be claimed them as long as they are directly related. If it is for a

business and private use, only a portion of such expense can be claimed and must be evidenced.

2. Allowance provided to businesses managed on behalf of a trust

Managing a business on behalf of a trust includes owning and operating business assets,

distribution of profits and complying with trust deed obligations. If a business is managed

through a trust structure, then there are many aspects in which benefits are ascertained. (Brigham

and Houston, 2012). Some of them are mentioned below:

Trust is allowed to get 50% discount of their assets which are in possession from more

than 12 months.

Freedom is provided regarding the usage of income.

3. Concept of Forecast Returns and Set-Up

Forecast returns are the estimated amount which is going to be acquired by the

organisation on their investments that are made in business projects. Set up can be defined as the

action which is used to establish some thing. It has been estimated by the client that in future

17% returns are going to be acquired in future for next 5 years on 3500000 pounds that are

invested in the business.

Years Investment Returns(17%) on investment

2018 3500000 595000

2019 3500000+595000 696150

2020 3500000+595000+696150 814496

2021 3500000+595000+696150+814496 952960

2022 3500000+595000+696150+814496+952960 1114963

2023 3500000+595000+696150+814496+952960+1114963 1304507

1. Treatment of Business Expenses in regard to Tax Legislation

The business expenses are deductible under the Tax Legislation. Such costs incurred in

operating assesses business can be claimed them as long as they are directly related. If it is for a

business and private use, only a portion of such expense can be claimed and must be evidenced.

2. Allowance provided to businesses managed on behalf of a trust

Managing a business on behalf of a trust includes owning and operating business assets,

distribution of profits and complying with trust deed obligations. If a business is managed

through a trust structure, then there are many aspects in which benefits are ascertained. (Brigham

and Houston, 2012). Some of them are mentioned below:

Trust is allowed to get 50% discount of their assets which are in possession from more

than 12 months.

Freedom is provided regarding the usage of income.

3. Concept of Forecast Returns and Set-Up

Forecast returns are the estimated amount which is going to be acquired by the

organisation on their investments that are made in business projects. Set up can be defined as the

action which is used to establish some thing. It has been estimated by the client that in future

17% returns are going to be acquired in future for next 5 years on 3500000 pounds that are

invested in the business.

Years Investment Returns(17%) on investment

2018 3500000 595000

2019 3500000+595000 696150

2020 3500000+595000+696150 814496

2021 3500000+595000+696150+814496 952960

2022 3500000+595000+696150+814496+952960 1114963

2023 3500000+595000+696150+814496+952960+1114963 1304507

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

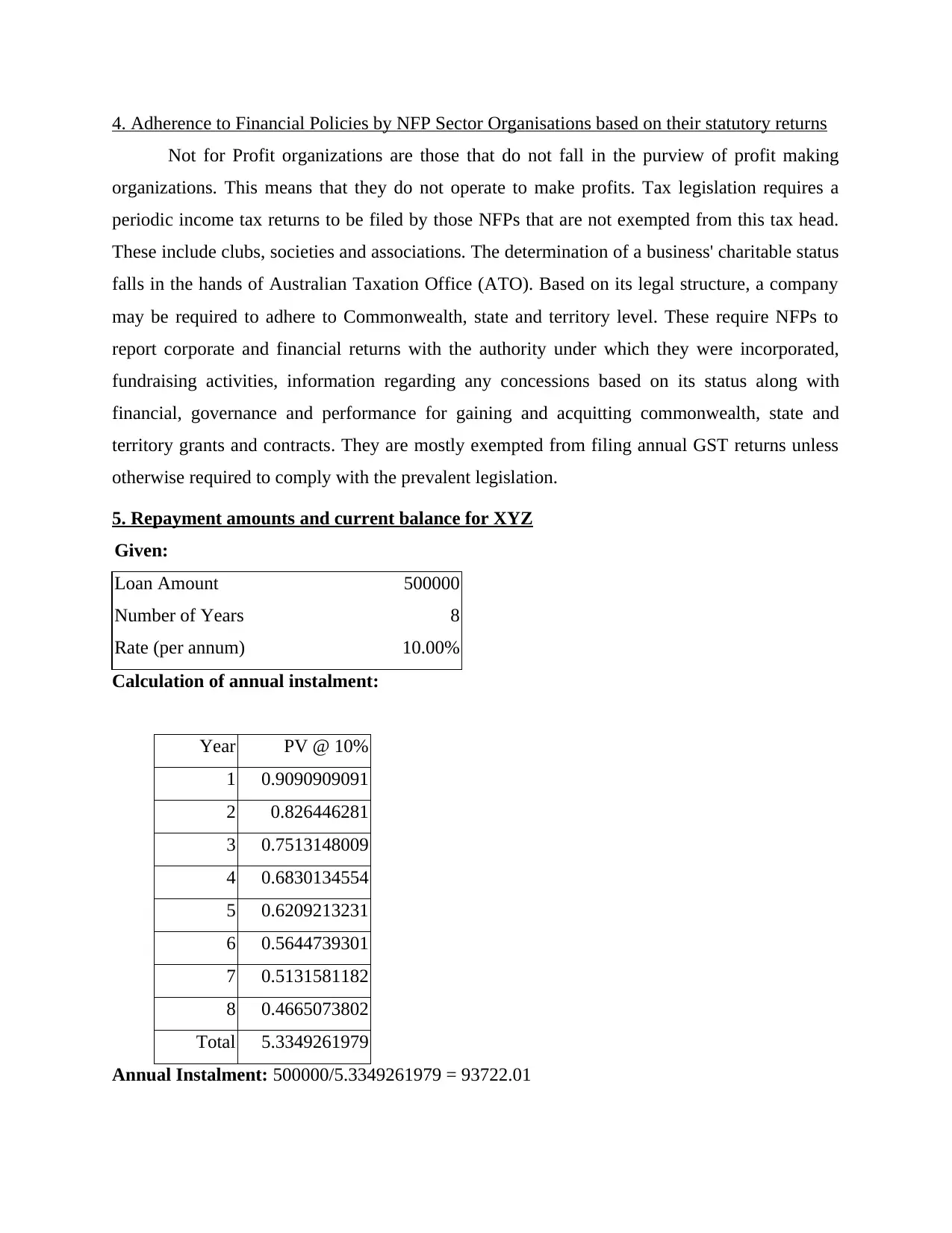

4. Adherence to Financial Policies by NFP Sector Organisations based on their statutory returns

Not for Profit organizations are those that do not fall in the purview of profit making

organizations. This means that they do not operate to make profits. Tax legislation requires a

periodic income tax returns to be filed by those NFPs that are not exempted from this tax head.

These include clubs, societies and associations. The determination of a business' charitable status

falls in the hands of Australian Taxation Office (ATO). Based on its legal structure, a company

may be required to adhere to Commonwealth, state and territory level. These require NFPs to

report corporate and financial returns with the authority under which they were incorporated,

fundraising activities, information regarding any concessions based on its status along with

financial, governance and performance for gaining and acquitting commonwealth, state and

territory grants and contracts. They are mostly exempted from filing annual GST returns unless

otherwise required to comply with the prevalent legislation.

5. Repayment amounts and current balance for XYZ

Given:

Loan Amount 500000

Number of Years 8

Rate (per annum) 10.00%

Calculation of annual instalment:

Year PV @ 10%

1 0.9090909091

2 0.826446281

3 0.7513148009

4 0.6830134554

5 0.6209213231

6 0.5644739301

7 0.5131581182

8 0.4665073802

Total 5.3349261979

Annual Instalment: 500000/5.3349261979 = 93722.01

Not for Profit organizations are those that do not fall in the purview of profit making

organizations. This means that they do not operate to make profits. Tax legislation requires a

periodic income tax returns to be filed by those NFPs that are not exempted from this tax head.

These include clubs, societies and associations. The determination of a business' charitable status

falls in the hands of Australian Taxation Office (ATO). Based on its legal structure, a company

may be required to adhere to Commonwealth, state and territory level. These require NFPs to

report corporate and financial returns with the authority under which they were incorporated,

fundraising activities, information regarding any concessions based on its status along with

financial, governance and performance for gaining and acquitting commonwealth, state and

territory grants and contracts. They are mostly exempted from filing annual GST returns unless

otherwise required to comply with the prevalent legislation.

5. Repayment amounts and current balance for XYZ

Given:

Loan Amount 500000

Number of Years 8

Rate (per annum) 10.00%

Calculation of annual instalment:

Year PV @ 10%

1 0.9090909091

2 0.826446281

3 0.7513148009

4 0.6830134554

5 0.6209213231

6 0.5644739301

7 0.5131581182

8 0.4665073802

Total 5.3349261979

Annual Instalment: 500000/5.3349261979 = 93722.01

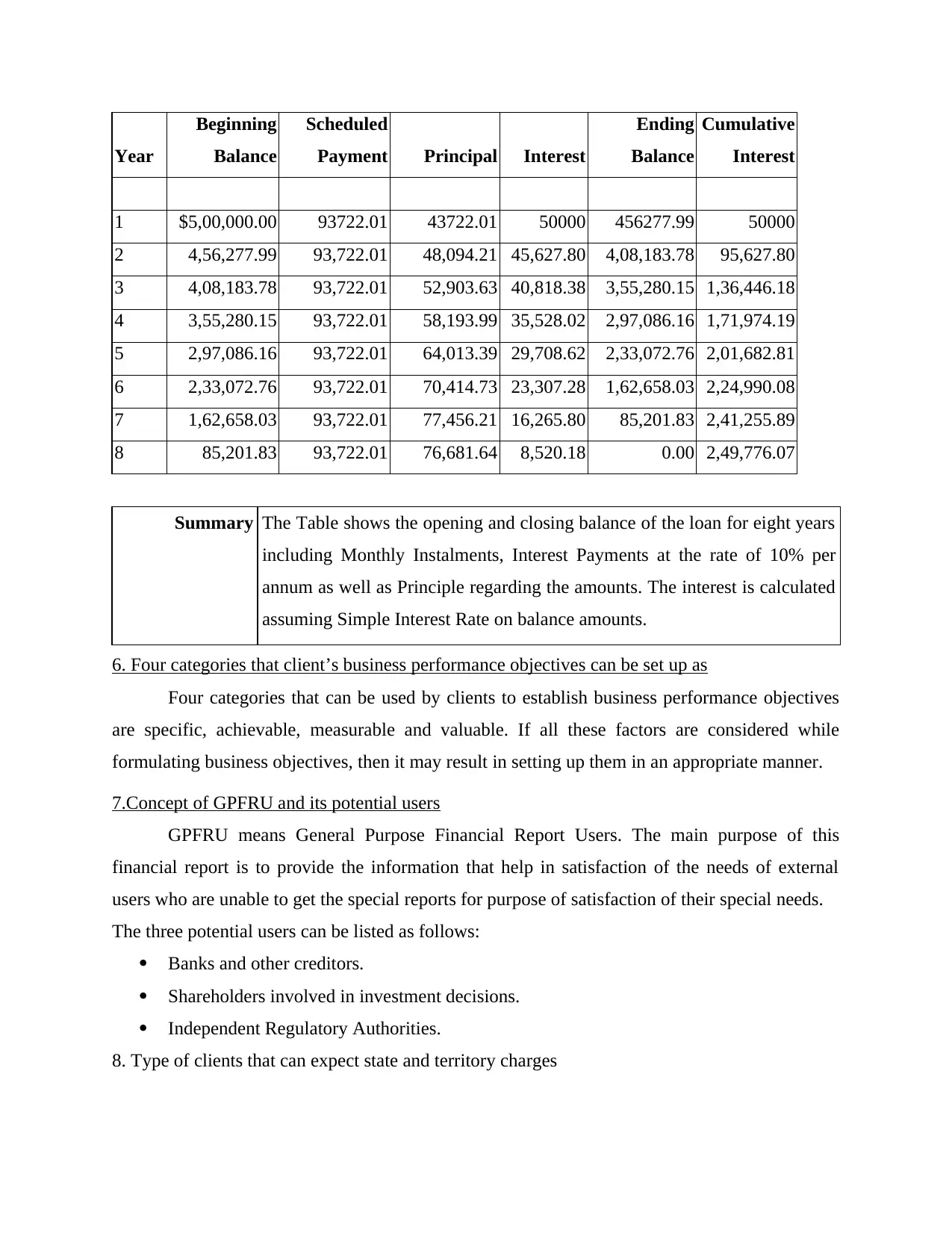

Year

Beginning

Balance

Scheduled

Payment Principal Interest

Ending

Balance

Cumulative

Interest

1 $5,00,000.00 93722.01 43722.01 50000 456277.99 50000

2 4,56,277.99 93,722.01 48,094.21 45,627.80 4,08,183.78 95,627.80

3 4,08,183.78 93,722.01 52,903.63 40,818.38 3,55,280.15 1,36,446.18

4 3,55,280.15 93,722.01 58,193.99 35,528.02 2,97,086.16 1,71,974.19

5 2,97,086.16 93,722.01 64,013.39 29,708.62 2,33,072.76 2,01,682.81

6 2,33,072.76 93,722.01 70,414.73 23,307.28 1,62,658.03 2,24,990.08

7 1,62,658.03 93,722.01 77,456.21 16,265.80 85,201.83 2,41,255.89

8 85,201.83 93,722.01 76,681.64 8,520.18 0.00 2,49,776.07

Summary The Table shows the opening and closing balance of the loan for eight years

including Monthly Instalments, Interest Payments at the rate of 10% per

annum as well as Principle regarding the amounts. The interest is calculated

assuming Simple Interest Rate on balance amounts.

6. Four categories that client’s business performance objectives can be set up as

Four categories that can be used by clients to establish business performance objectives

are specific, achievable, measurable and valuable. If all these factors are considered while

formulating business objectives, then it may result in setting up them in an appropriate manner.

7.Concept of GPFRU and its potential users

GPFRU means General Purpose Financial Report Users. The main purpose of this

financial report is to provide the information that help in satisfaction of the needs of external

users who are unable to get the special reports for purpose of satisfaction of their special needs.

The three potential users can be listed as follows:

Banks and other creditors.

Shareholders involved in investment decisions.

Independent Regulatory Authorities.

8. Type of clients that can expect state and territory charges

Beginning

Balance

Scheduled

Payment Principal Interest

Ending

Balance

Cumulative

Interest

1 $5,00,000.00 93722.01 43722.01 50000 456277.99 50000

2 4,56,277.99 93,722.01 48,094.21 45,627.80 4,08,183.78 95,627.80

3 4,08,183.78 93,722.01 52,903.63 40,818.38 3,55,280.15 1,36,446.18

4 3,55,280.15 93,722.01 58,193.99 35,528.02 2,97,086.16 1,71,974.19

5 2,97,086.16 93,722.01 64,013.39 29,708.62 2,33,072.76 2,01,682.81

6 2,33,072.76 93,722.01 70,414.73 23,307.28 1,62,658.03 2,24,990.08

7 1,62,658.03 93,722.01 77,456.21 16,265.80 85,201.83 2,41,255.89

8 85,201.83 93,722.01 76,681.64 8,520.18 0.00 2,49,776.07

Summary The Table shows the opening and closing balance of the loan for eight years

including Monthly Instalments, Interest Payments at the rate of 10% per

annum as well as Principle regarding the amounts. The interest is calculated

assuming Simple Interest Rate on balance amounts.

6. Four categories that client’s business performance objectives can be set up as

Four categories that can be used by clients to establish business performance objectives

are specific, achievable, measurable and valuable. If all these factors are considered while

formulating business objectives, then it may result in setting up them in an appropriate manner.

7.Concept of GPFRU and its potential users

GPFRU means General Purpose Financial Report Users. The main purpose of this

financial report is to provide the information that help in satisfaction of the needs of external

users who are unable to get the special reports for purpose of satisfaction of their special needs.

The three potential users can be listed as follows:

Banks and other creditors.

Shareholders involved in investment decisions.

Independent Regulatory Authorities.

8. Type of clients that can expect state and territory charges

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

According to Australian taxation office and Office of Fair trading, clients which can expect

state and territory charges includes fundraisers. These fundraisers can be non-profit organisations

or the organisations engaged in lottery businesses. These businesses also include charitable

collections, fundraising lotteries, gaming activities etc.

9. Calculating the amount of taxes and charges on land

A client is liable to pay annual tax and charges on the land held by them based on its

worth. This is calculated based on different state and territory offices based on their related

criteria implemented in that area. ATO and other relevant websites provide accurate annual tax

amounts by multiplying land value with the tax rates.

For example: The tax is calculated on the total value of land which is exceed the limit of

land tax threshold. General threshold: $100plus1.6% of land value above the threshold, up to the

premium threshold.

10. Practices that businesses who pay Commonwealth taxes must adopt

Businesses falling under the legislation of Commonwealth Taxes must keep track of its

transactions by maintaining a record of receipts and other related evidences regarding sales and

purchase. This includes tax invoices, wage and salary records and GST related documents. Any

purchase, sale or repairing of capital assets such as buildings, office equipment should be

recorded duly. Every business activity's statements, income tax and FBT returns as well as

employee related information on superannuation, etc. must be duly kept in the documents of the

business entity. Such records must be maintained for at least five years either manually or on a

software in a language that is easily understandable (Chandra, 2011).

TASK 2

1.

a. Ans. Financial information sought, Size, Current information

b. Ans. Sole traders are specialist who has special skills and expertise in particular field and

normally runs small businesses a specific industry. Sole traders normally have inadequate time in

framing, preparing and analysing business data or information. They need normal advice and

help in preparation of balance sheet or financial statements, managing business loans and

state and territory charges includes fundraisers. These fundraisers can be non-profit organisations

or the organisations engaged in lottery businesses. These businesses also include charitable

collections, fundraising lotteries, gaming activities etc.

9. Calculating the amount of taxes and charges on land

A client is liable to pay annual tax and charges on the land held by them based on its

worth. This is calculated based on different state and territory offices based on their related

criteria implemented in that area. ATO and other relevant websites provide accurate annual tax

amounts by multiplying land value with the tax rates.

For example: The tax is calculated on the total value of land which is exceed the limit of

land tax threshold. General threshold: $100plus1.6% of land value above the threshold, up to the

premium threshold.

10. Practices that businesses who pay Commonwealth taxes must adopt

Businesses falling under the legislation of Commonwealth Taxes must keep track of its

transactions by maintaining a record of receipts and other related evidences regarding sales and

purchase. This includes tax invoices, wage and salary records and GST related documents. Any

purchase, sale or repairing of capital assets such as buildings, office equipment should be

recorded duly. Every business activity's statements, income tax and FBT returns as well as

employee related information on superannuation, etc. must be duly kept in the documents of the

business entity. Such records must be maintained for at least five years either manually or on a

software in a language that is easily understandable (Chandra, 2011).

TASK 2

1.

a. Ans. Financial information sought, Size, Current information

b. Ans. Sole traders are specialist who has special skills and expertise in particular field and

normally runs small businesses a specific industry. Sole traders normally have inadequate time in

framing, preparing and analysing business data or information. They need normal advice and

help in preparation of balance sheet or financial statements, managing business loans and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

overdraft, baking activities, various tax forms and returns, bank reconciling statement and

indicator to changes in various legislation including changes in taxation policies

2.

Ans. Under financial services sectors and industry client and group of client repeatedly

approached for information on a wide range of financial and business issues. Following are the

different type of financial options available for client to solve such financial and business issues:

Different types of financial options may include:

Funding alternatives

Long-term investments

Purchases

Adjustment of borrowings

Asset liquidation

Cost of capital

Sources of finance

Cost recoveries

Debt and equity

Dividends

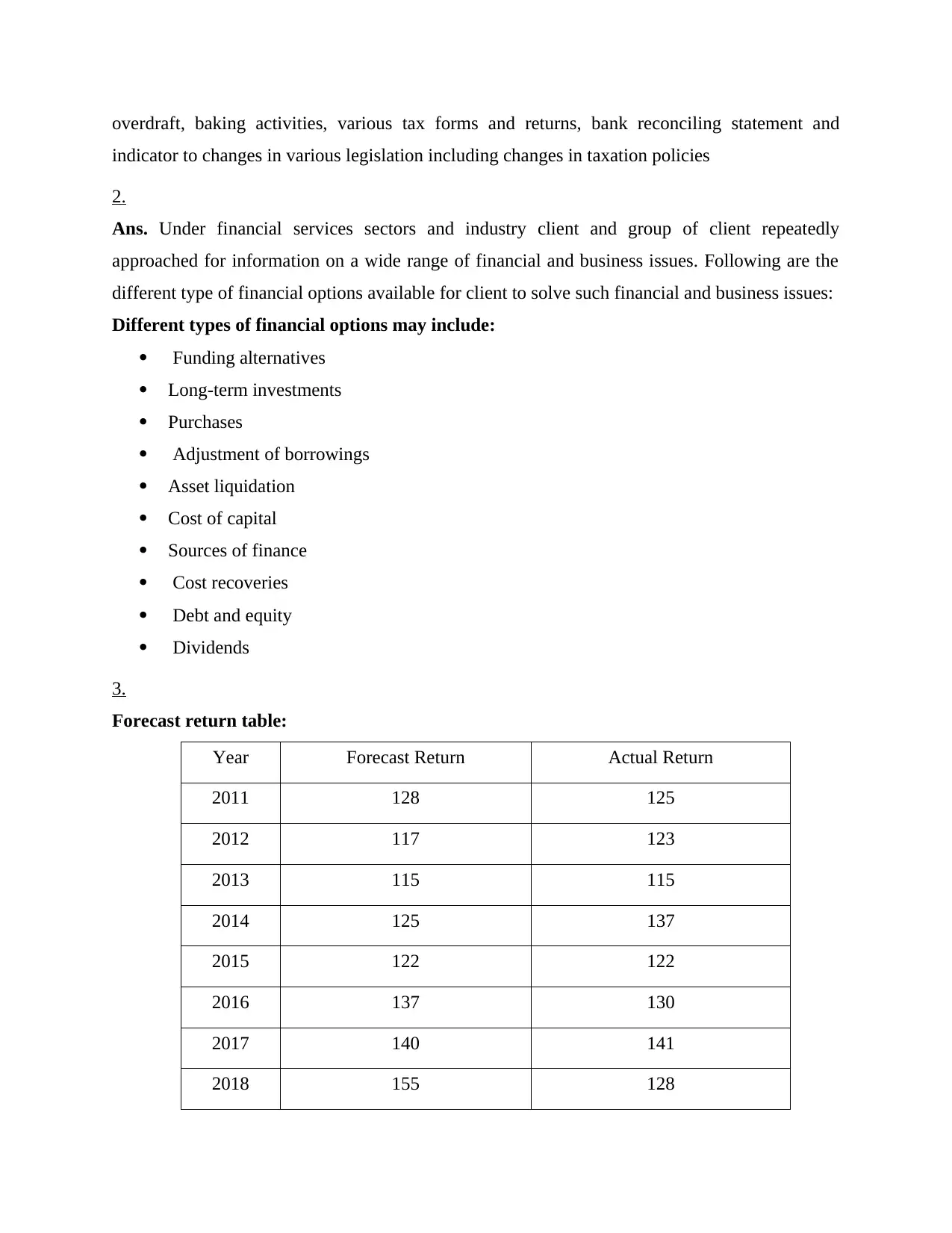

3.

Forecast return table:

Year Forecast Return Actual Return

2011 128 125

2012 117 123

2013 115 115

2014 125 137

2015 122 122

2016 137 130

2017 140 141

2018 155 128

indicator to changes in various legislation including changes in taxation policies

2.

Ans. Under financial services sectors and industry client and group of client repeatedly

approached for information on a wide range of financial and business issues. Following are the

different type of financial options available for client to solve such financial and business issues:

Different types of financial options may include:

Funding alternatives

Long-term investments

Purchases

Adjustment of borrowings

Asset liquidation

Cost of capital

Sources of finance

Cost recoveries

Debt and equity

Dividends

3.

Forecast return table:

Year Forecast Return Actual Return

2011 128 125

2012 117 123

2013 115 115

2014 125 137

2015 122 122

2016 137 130

2017 140 141

2018 155 128

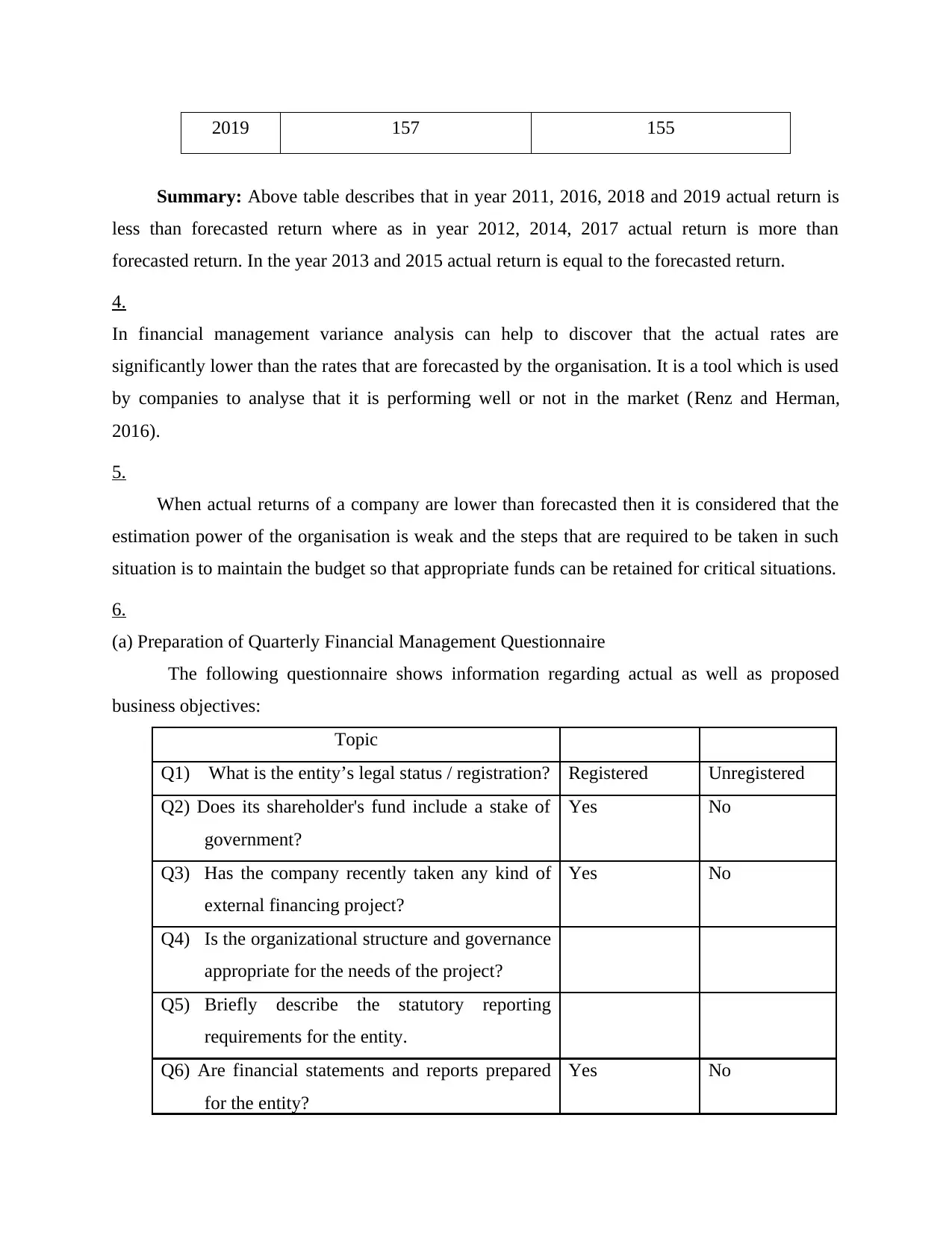

2019 157 155

Summary: Above table describes that in year 2011, 2016, 2018 and 2019 actual return is

less than forecasted return where as in year 2012, 2014, 2017 actual return is more than

forecasted return. In the year 2013 and 2015 actual return is equal to the forecasted return.

4.

In financial management variance analysis can help to discover that the actual rates are

significantly lower than the rates that are forecasted by the organisation. It is a tool which is used

by companies to analyse that it is performing well or not in the market (Renz and Herman,

2016).

5.

When actual returns of a company are lower than forecasted then it is considered that the

estimation power of the organisation is weak and the steps that are required to be taken in such

situation is to maintain the budget so that appropriate funds can be retained for critical situations.

6.

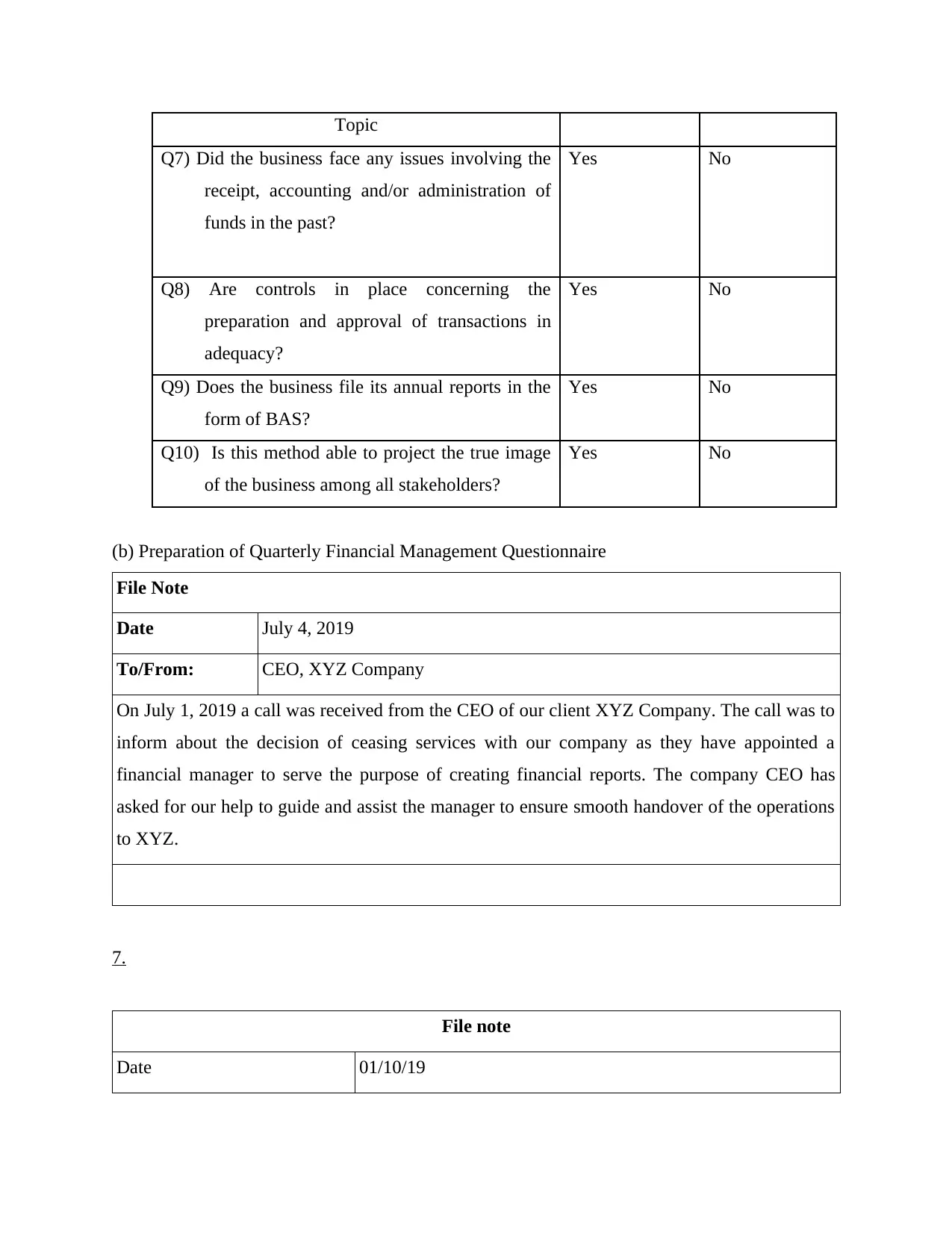

(a) Preparation of Quarterly Financial Management Questionnaire

The following questionnaire shows information regarding actual as well as proposed

business objectives:

Topic

Q1) What is the entity’s legal status / registration? Registered Unregistered

Q2) Does its shareholder's fund include a stake of

government?

Yes No

Q3) Has the company recently taken any kind of

external financing project?

Yes No

Q4) Is the organizational structure and governance

appropriate for the needs of the project?

Q5) Briefly describe the statutory reporting

requirements for the entity.

Q6) Are financial statements and reports prepared

for the entity?

Yes No

Summary: Above table describes that in year 2011, 2016, 2018 and 2019 actual return is

less than forecasted return where as in year 2012, 2014, 2017 actual return is more than

forecasted return. In the year 2013 and 2015 actual return is equal to the forecasted return.

4.

In financial management variance analysis can help to discover that the actual rates are

significantly lower than the rates that are forecasted by the organisation. It is a tool which is used

by companies to analyse that it is performing well or not in the market (Renz and Herman,

2016).

5.

When actual returns of a company are lower than forecasted then it is considered that the

estimation power of the organisation is weak and the steps that are required to be taken in such

situation is to maintain the budget so that appropriate funds can be retained for critical situations.

6.

(a) Preparation of Quarterly Financial Management Questionnaire

The following questionnaire shows information regarding actual as well as proposed

business objectives:

Topic

Q1) What is the entity’s legal status / registration? Registered Unregistered

Q2) Does its shareholder's fund include a stake of

government?

Yes No

Q3) Has the company recently taken any kind of

external financing project?

Yes No

Q4) Is the organizational structure and governance

appropriate for the needs of the project?

Q5) Briefly describe the statutory reporting

requirements for the entity.

Q6) Are financial statements and reports prepared

for the entity?

Yes No

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

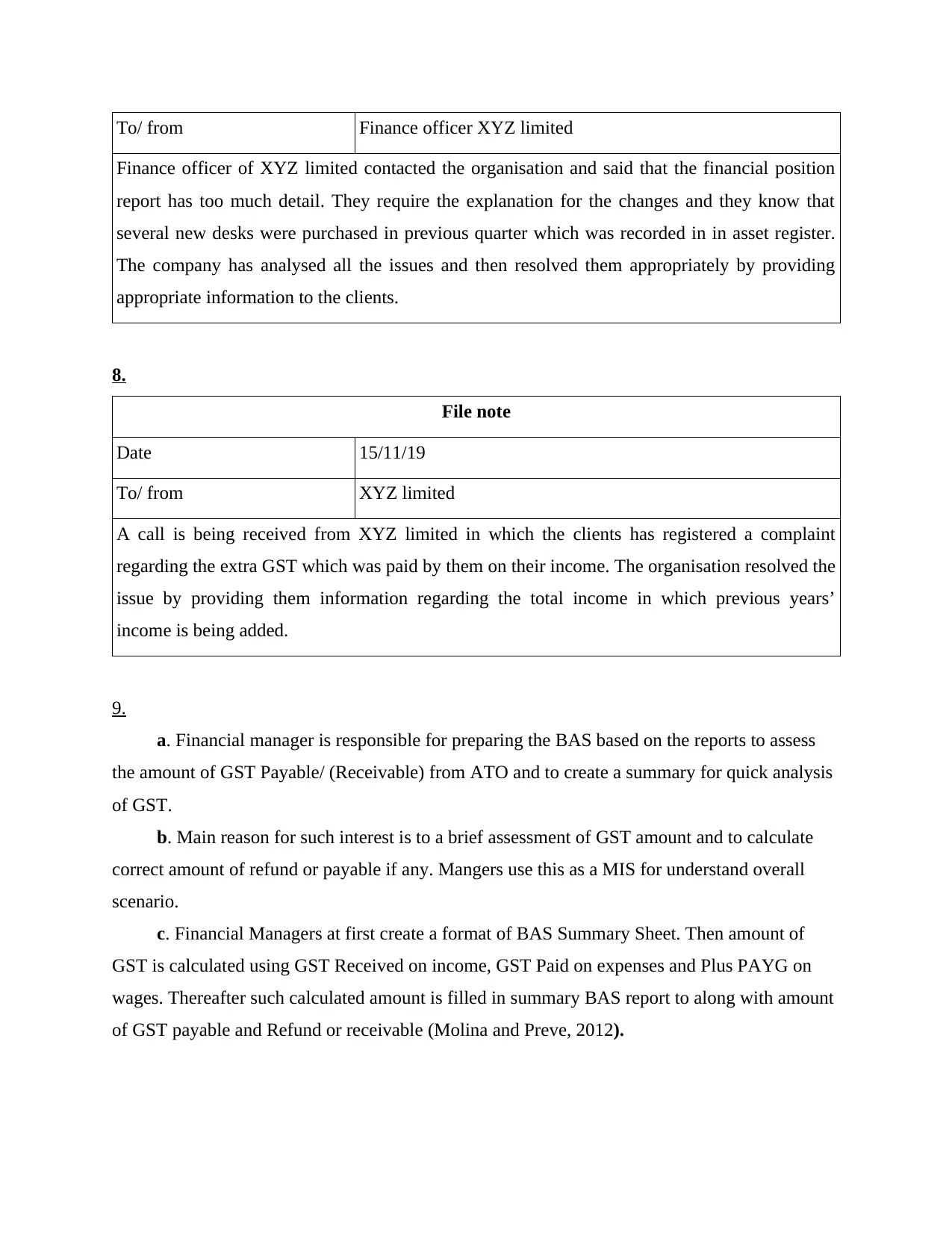

Topic

Q7) Did the business face any issues involving the

receipt, accounting and/or administration of

funds in the past?

Yes No

Q8) Are controls in place concerning the

preparation and approval of transactions in

adequacy?

Yes No

Q9) Does the business file its annual reports in the

form of BAS?

Yes No

Q10) Is this method able to project the true image

of the business among all stakeholders?

Yes No

(b) Preparation of Quarterly Financial Management Questionnaire

File Note

Date July 4, 2019

To/From: CEO, XYZ Company

On July 1, 2019 a call was received from the CEO of our client XYZ Company. The call was to

inform about the decision of ceasing services with our company as they have appointed a

financial manager to serve the purpose of creating financial reports. The company CEO has

asked for our help to guide and assist the manager to ensure smooth handover of the operations

to XYZ.

7.

File note

Date 01/10/19

Q7) Did the business face any issues involving the

receipt, accounting and/or administration of

funds in the past?

Yes No

Q8) Are controls in place concerning the

preparation and approval of transactions in

adequacy?

Yes No

Q9) Does the business file its annual reports in the

form of BAS?

Yes No

Q10) Is this method able to project the true image

of the business among all stakeholders?

Yes No

(b) Preparation of Quarterly Financial Management Questionnaire

File Note

Date July 4, 2019

To/From: CEO, XYZ Company

On July 1, 2019 a call was received from the CEO of our client XYZ Company. The call was to

inform about the decision of ceasing services with our company as they have appointed a

financial manager to serve the purpose of creating financial reports. The company CEO has

asked for our help to guide and assist the manager to ensure smooth handover of the operations

to XYZ.

7.

File note

Date 01/10/19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To/ from Finance officer XYZ limited

Finance officer of XYZ limited contacted the organisation and said that the financial position

report has too much detail. They require the explanation for the changes and they know that

several new desks were purchased in previous quarter which was recorded in in asset register.

The company has analysed all the issues and then resolved them appropriately by providing

appropriate information to the clients.

8.

File note

Date 15/11/19

To/ from XYZ limited

A call is being received from XYZ limited in which the clients has registered a complaint

regarding the extra GST which was paid by them on their income. The organisation resolved the

issue by providing them information regarding the total income in which previous years’

income is being added.

9.

a. Financial manager is responsible for preparing the BAS based on the reports to assess

the amount of GST Payable/ (Receivable) from ATO and to create a summary for quick analysis

of GST.

b. Main reason for such interest is to a brief assessment of GST amount and to calculate

correct amount of refund or payable if any. Mangers use this as a MIS for understand overall

scenario.

c. Financial Managers at first create a format of BAS Summary Sheet. Then amount of

GST is calculated using GST Received on income, GST Paid on expenses and Plus PAYG on

wages. Thereafter such calculated amount is filled in summary BAS report to along with amount

of GST payable and Refund or receivable (Molina and Preve, 2012).

Finance officer of XYZ limited contacted the organisation and said that the financial position

report has too much detail. They require the explanation for the changes and they know that

several new desks were purchased in previous quarter which was recorded in in asset register.

The company has analysed all the issues and then resolved them appropriately by providing

appropriate information to the clients.

8.

File note

Date 15/11/19

To/ from XYZ limited

A call is being received from XYZ limited in which the clients has registered a complaint

regarding the extra GST which was paid by them on their income. The organisation resolved the

issue by providing them information regarding the total income in which previous years’

income is being added.

9.

a. Financial manager is responsible for preparing the BAS based on the reports to assess

the amount of GST Payable/ (Receivable) from ATO and to create a summary for quick analysis

of GST.

b. Main reason for such interest is to a brief assessment of GST amount and to calculate

correct amount of refund or payable if any. Mangers use this as a MIS for understand overall

scenario.

c. Financial Managers at first create a format of BAS Summary Sheet. Then amount of

GST is calculated using GST Received on income, GST Paid on expenses and Plus PAYG on

wages. Thereafter such calculated amount is filled in summary BAS report to along with amount

of GST payable and Refund or receivable (Molina and Preve, 2012).

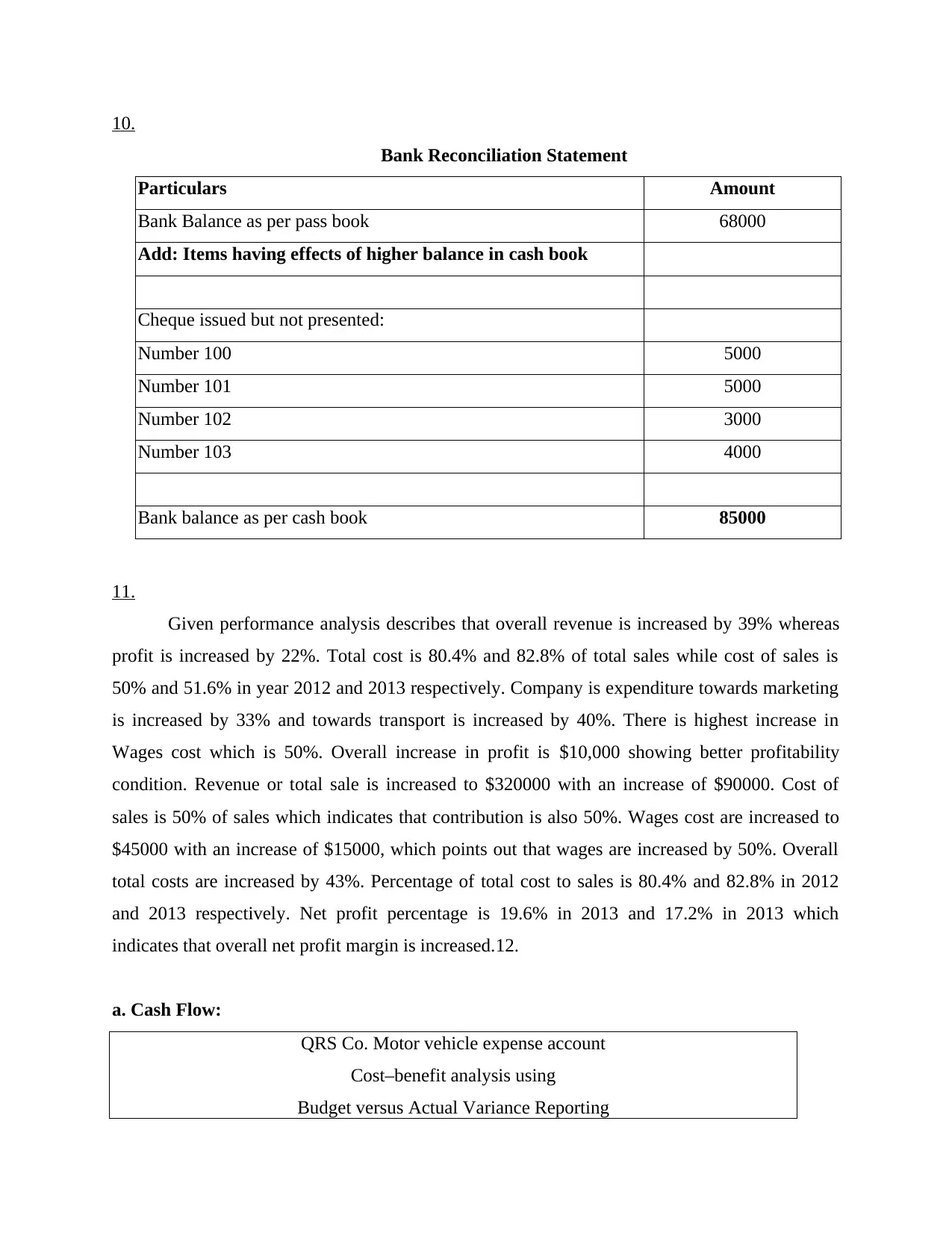

10.

Bank Reconciliation Statement

Particulars Amount

Bank Balance as per pass book 68000

Add: Items having effects of higher balance in cash book

Cheque issued but not presented:

Number 100 5000

Number 101 5000

Number 102 3000

Number 103 4000

Bank balance as per cash book 85000

11.

Given performance analysis describes that overall revenue is increased by 39% whereas

profit is increased by 22%. Total cost is 80.4% and 82.8% of total sales while cost of sales is

50% and 51.6% in year 2012 and 2013 respectively. Company is expenditure towards marketing

is increased by 33% and towards transport is increased by 40%. There is highest increase in

Wages cost which is 50%. Overall increase in profit is $10,000 showing better profitability

condition. Revenue or total sale is increased to $320000 with an increase of $90000. Cost of

sales is 50% of sales which indicates that contribution is also 50%. Wages cost are increased to

$45000 with an increase of $15000, which points out that wages are increased by 50%. Overall

total costs are increased by 43%. Percentage of total cost to sales is 80.4% and 82.8% in 2012

and 2013 respectively. Net profit percentage is 19.6% in 2013 and 17.2% in 2013 which

indicates that overall net profit margin is increased.12.

a. Cash Flow:

QRS Co. Motor vehicle expense account

Cost–benefit analysis using

Budget versus Actual Variance Reporting

Bank Reconciliation Statement

Particulars Amount

Bank Balance as per pass book 68000

Add: Items having effects of higher balance in cash book

Cheque issued but not presented:

Number 100 5000

Number 101 5000

Number 102 3000

Number 103 4000

Bank balance as per cash book 85000

11.

Given performance analysis describes that overall revenue is increased by 39% whereas

profit is increased by 22%. Total cost is 80.4% and 82.8% of total sales while cost of sales is

50% and 51.6% in year 2012 and 2013 respectively. Company is expenditure towards marketing

is increased by 33% and towards transport is increased by 40%. There is highest increase in

Wages cost which is 50%. Overall increase in profit is $10,000 showing better profitability

condition. Revenue or total sale is increased to $320000 with an increase of $90000. Cost of

sales is 50% of sales which indicates that contribution is also 50%. Wages cost are increased to

$45000 with an increase of $15000, which points out that wages are increased by 50%. Overall

total costs are increased by 43%. Percentage of total cost to sales is 80.4% and 82.8% in 2012

and 2013 respectively. Net profit percentage is 19.6% in 2013 and 17.2% in 2013 which

indicates that overall net profit margin is increased.12.

a. Cash Flow:

QRS Co. Motor vehicle expense account

Cost–benefit analysis using

Budget versus Actual Variance Reporting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.