FNSACC502 Diploma of Accounting: Income Tax Returns - Task 1

VerifiedAdded on 2023/06/10

|20

|4625

|77

Homework Assignment

AI Summary

This document presents a solution to an assessment task for the FNSACC502 unit, which focuses on preparing income tax returns for individuals. The assessment includes questions related to defining assessable income according to the Income Tax Assessment Act 1997, providing examples of ordinary and statutory income, describing different types of audits conducted by the ATO, outlining the key differences between residents and non-residents for tax purposes, explaining the exhaustive tests of residence for individuals as per Section 6(1) of the ITAA 1936, detailing the core principles of the Tax Agent Services Act 2009, providing examples of conflict management arrangements for tax practitioners, addressing ethical dilemmas faced by tax practitioners, specifying the record-keeping requirements for taxpayers, and determining correct lodgment dates for various scenarios. The solution also includes student and assessor declarations, assessment conditions, and references to relevant legislation and resources.

Assessment Cover Sheet

Assessment Week One Details

Term and Year Term 1 2018

Assessment Type Portfolio of activities

Due Date Class Room

Student Name:

Student ID No:

Date:

Qualification : FNS50215 Diploma of Accounting

Unit Code: FNSACC502

Unit Title: Prepare income tax returns for individuals

Assessor’s Name Ada DU

Student Declaration: I declare that this

work has been completed by me honestly

and with integrity. I understand that the Elite

Education Vocation Institute’s Student

Assessment, Reassessment and Repeating

Units of Competency Guidelines apply to

these assessment tasks.

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have

provided appropriate feedback.

Name: Name: Ada DU

Signature: Signature:

Date: Date:

Student was absent from the feedback

session.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

Assessment Week One Details

Term and Year Term 1 2018

Assessment Type Portfolio of activities

Due Date Class Room

Student Name:

Student ID No:

Date:

Qualification : FNS50215 Diploma of Accounting

Unit Code: FNSACC502

Unit Title: Prepare income tax returns for individuals

Assessor’s Name Ada DU

Student Declaration: I declare that this

work has been completed by me honestly

and with integrity. I understand that the Elite

Education Vocation Institute’s Student

Assessment, Reassessment and Repeating

Units of Competency Guidelines apply to

these assessment tasks.

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have

provided appropriate feedback.

Name: Name: Ada DU

Signature: Signature:

Date: Date:

Student was absent from the feedback

session.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment/evidence gathering conditions

Each assessment component is recorded as either Satisfactory (S) or Not Yet Satisfactory

(NYS). A student can only achieve competence when all assessment components listed

under procedures and specifications of the assessment section are Satisfactory. Your trainer

will give you feedback after the completion of each assessment. A student who is assessed as

NYS is eligible for re-assessment. Should the student fail to submit the assessment, a result

outcome of Did Not Submit (DNS) will be recorded.

Principles of Assessment

Based on Clauses 1.8 – 1.12 from the Australian Standards Quality Assurance’s (ASQA)

Standards for Registered Training Organizations (RTO) 2015, the learner would be assessed

based on the following principles:

Fairness - (1) the individual learner’s needs are considered in the assessment process, (2)

where appropriate, reasonable adjustments are applied by the RTO to take into

account the individual leaner’s needs and, (3) the RTO informs the leaner about the

assessment process, and provides the learner with the opportunity to challenge the

result of the assessment and be reassessed if necessary.

Flexibility – assessment is flexible to the individual learner by; (1) reflecting the learner’s

needs, (2) assessing competencies held by the learner no matter how or where they

have been acquired and, (3) the unit of competency and associated assessment

requirements, and the individual.

Validity – (1) requires that assessment against the unit/s of competency and the associated

assessment requirements covers the broad range of skills and knowledge, (2)

assessment of knowledge and skills is integrated with their practical application, (3)

assessment to be based on evidence that demonstrates tat a leaner could

demonstrate these skills and knowledge in other similar situations and, (4)

judgement of competence is based on evidence of learner performance that is

aligned to the unit/s of competency and associated assessment requirements.

Reliability – evidence presented for assessment is consistently interpreted and assessment

results are comparable irrespective of the assessor conducting the assessment

Rules of Evidence

Validity – the assessor is assured that the learner has the skills, knowledge and attributes,

as described in the module of unit of competency and associated assessment

requirements.

Sufficiency – the assessor is assured that the quality, quantity and relevance of the

assessment evidence enables a judgement to be made of a learner’s competency.

Authenticity – the assessor is assured that the evidence presented for assessment is the

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

Each assessment component is recorded as either Satisfactory (S) or Not Yet Satisfactory

(NYS). A student can only achieve competence when all assessment components listed

under procedures and specifications of the assessment section are Satisfactory. Your trainer

will give you feedback after the completion of each assessment. A student who is assessed as

NYS is eligible for re-assessment. Should the student fail to submit the assessment, a result

outcome of Did Not Submit (DNS) will be recorded.

Principles of Assessment

Based on Clauses 1.8 – 1.12 from the Australian Standards Quality Assurance’s (ASQA)

Standards for Registered Training Organizations (RTO) 2015, the learner would be assessed

based on the following principles:

Fairness - (1) the individual learner’s needs are considered in the assessment process, (2)

where appropriate, reasonable adjustments are applied by the RTO to take into

account the individual leaner’s needs and, (3) the RTO informs the leaner about the

assessment process, and provides the learner with the opportunity to challenge the

result of the assessment and be reassessed if necessary.

Flexibility – assessment is flexible to the individual learner by; (1) reflecting the learner’s

needs, (2) assessing competencies held by the learner no matter how or where they

have been acquired and, (3) the unit of competency and associated assessment

requirements, and the individual.

Validity – (1) requires that assessment against the unit/s of competency and the associated

assessment requirements covers the broad range of skills and knowledge, (2)

assessment of knowledge and skills is integrated with their practical application, (3)

assessment to be based on evidence that demonstrates tat a leaner could

demonstrate these skills and knowledge in other similar situations and, (4)

judgement of competence is based on evidence of learner performance that is

aligned to the unit/s of competency and associated assessment requirements.

Reliability – evidence presented for assessment is consistently interpreted and assessment

results are comparable irrespective of the assessor conducting the assessment

Rules of Evidence

Validity – the assessor is assured that the learner has the skills, knowledge and attributes,

as described in the module of unit of competency and associated assessment

requirements.

Sufficiency – the assessor is assured that the quality, quantity and relevance of the

assessment evidence enables a judgement to be made of a learner’s competency.

Authenticity – the assessor is assured that the evidence presented for assessment is the

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

learner’s own work. This would mean that any form of plagiarism or copying of

other’s work may not be permitted and would be deemed strictly as a ‘Not Yet

Competent’ grading.

Currency – the assessor is assured that the assessment evidence demonstrates current

competency. This requires the assessment evidence to be from the present or the

very recent past.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

other’s work may not be permitted and would be deemed strictly as a ‘Not Yet

Competent’ grading.

Currency – the assessor is assured that the assessment evidence demonstrates current

competency. This requires the assessment evidence to be from the present or the

very recent past.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Resources required for this Assessment

All documents must be created using Microsoft Office suites i.e., MS Word, Excel,

PowerPoint

Upon completion, submit the assessment via the student learning management system to

your trainer along with the completed assessment coversheet.

Refer the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment is to be completed according to the instructions given by your assessor.

Students are allowed to take this assessment home.

Feedback on each task will be provided to enable you to determine how your work could

be improved. You will be provided with feedback on your work within 2 weeks of the

assessment due date.

Should you not answer the questions correctly, you will be given feedback on the results

and your gaps in knowledge. You will be given another opportunity to demonstrate your

knowledge and skills to be deemed competent for this unit of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from

your assessor.

Please refer to the College re-assessment and re-enrolment policy for more information.

Procedures and Specifications of the Assessment

To complete the unit requirements safely and effectively, the individual must:

Define international marketing

Identify international trade patterns

Explain international trade policies and agreements

Identify legislative requirements

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

All documents must be created using Microsoft Office suites i.e., MS Word, Excel,

PowerPoint

Upon completion, submit the assessment via the student learning management system to

your trainer along with the completed assessment coversheet.

Refer the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment is to be completed according to the instructions given by your assessor.

Students are allowed to take this assessment home.

Feedback on each task will be provided to enable you to determine how your work could

be improved. You will be provided with feedback on your work within 2 weeks of the

assessment due date.

Should you not answer the questions correctly, you will be given feedback on the results

and your gaps in knowledge. You will be given another opportunity to demonstrate your

knowledge and skills to be deemed competent for this unit of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from

your assessor.

Please refer to the College re-assessment and re-enrolment policy for more information.

Procedures and Specifications of the Assessment

To complete the unit requirements safely and effectively, the individual must:

Define international marketing

Identify international trade patterns

Explain international trade policies and agreements

Identify legislative requirements

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment 1

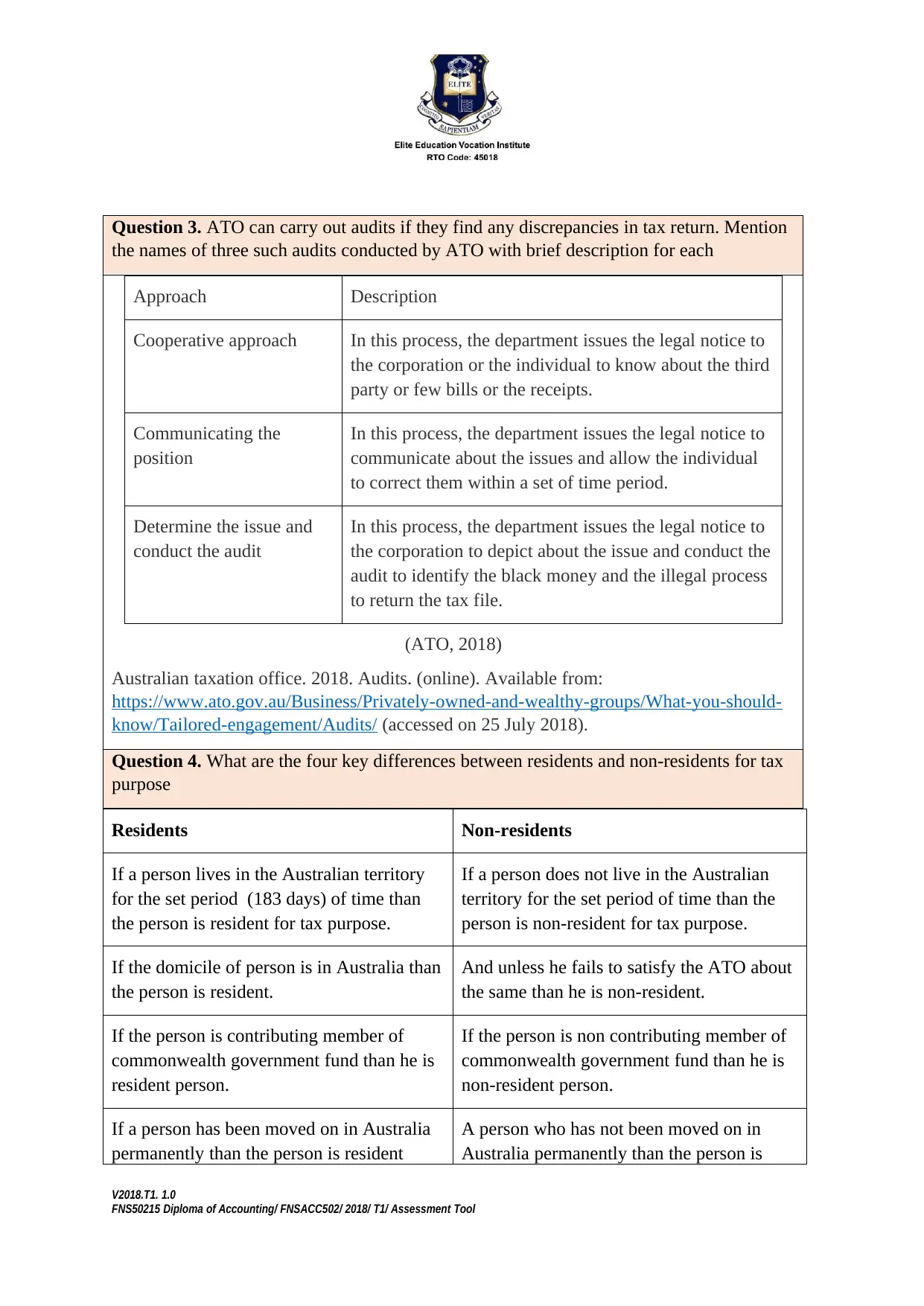

Question1. Define assessable income as per Income Tax Assessment Act 1997

Income tax assessment act, 1997 is an act of Australian parliament. It is among one of the

statutes under which income tax is calculated by the business. It is the total income which

is earned by an individual or the corporate within a tax year (Commonwealth consolidated

acts, 2018)

Question2. Give two examples of ordinary income and statutory income

Ordinary income Statutory income

1. Salaries 2. Net capital

gain

3. Commissions and

bonuses

4. Refund from

tax

authorities

(Tax administration, 2018)

Tax administration. 2018. Income tax. (online). Available from:

https://www.jamaicatax.gov.jm/income-tax2 (accessed on 25 July 2018).

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

Question1. Define assessable income as per Income Tax Assessment Act 1997

Income tax assessment act, 1997 is an act of Australian parliament. It is among one of the

statutes under which income tax is calculated by the business. It is the total income which

is earned by an individual or the corporate within a tax year (Commonwealth consolidated

acts, 2018)

Question2. Give two examples of ordinary income and statutory income

Ordinary income Statutory income

1. Salaries 2. Net capital

gain

3. Commissions and

bonuses

4. Refund from

tax

authorities

(Tax administration, 2018)

Tax administration. 2018. Income tax. (online). Available from:

https://www.jamaicatax.gov.jm/income-tax2 (accessed on 25 July 2018).

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

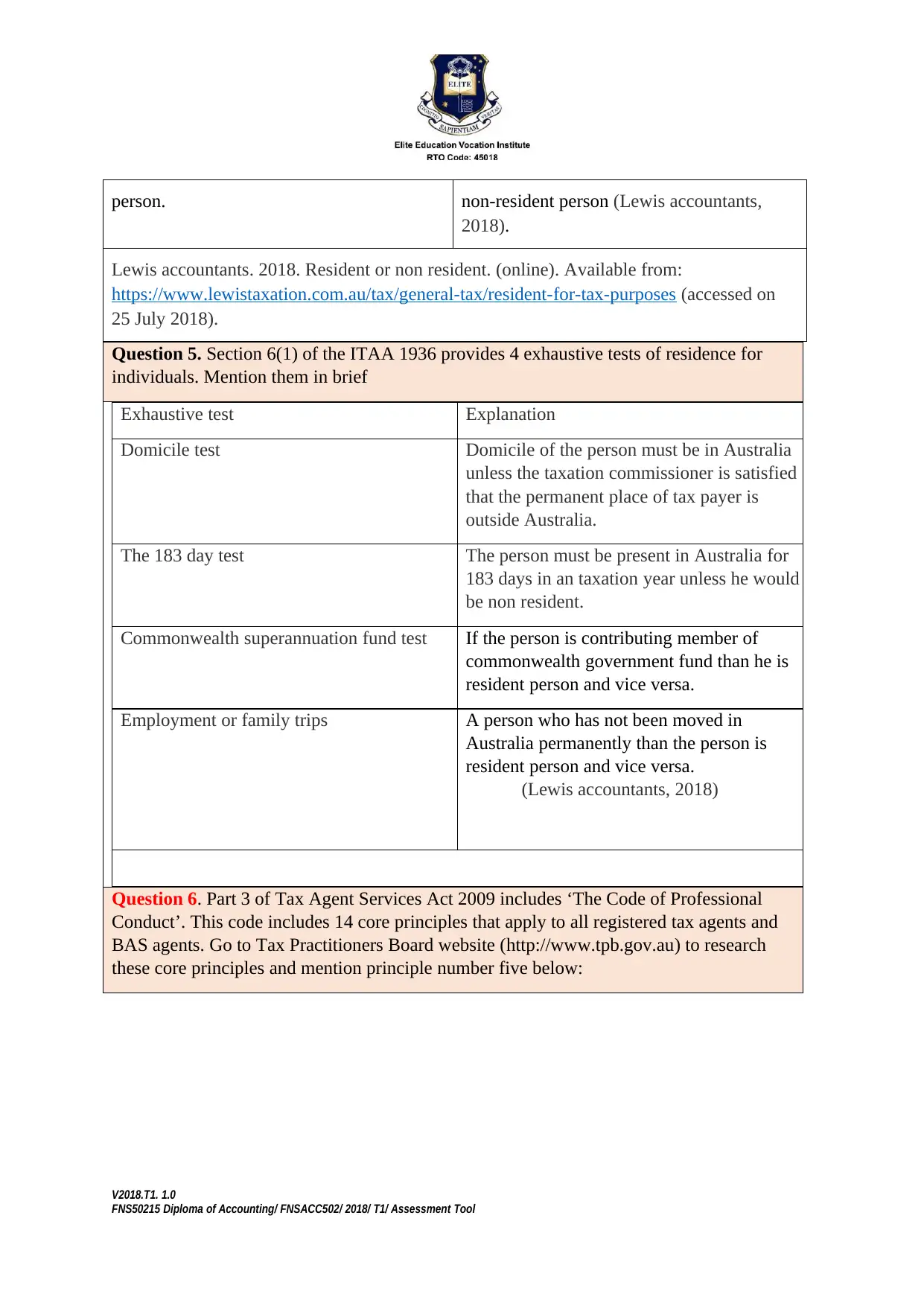

Question 3. ATO can carry out audits if they find any discrepancies in tax return. Mention

the names of three such audits conducted by ATO with brief description for each

Approach Description

Cooperative approach In this process, the department issues the legal notice to

the corporation or the individual to know about the third

party or few bills or the receipts.

Communicating the

position

In this process, the department issues the legal notice to

communicate about the issues and allow the individual

to correct them within a set of time period.

Determine the issue and

conduct the audit

In this process, the department issues the legal notice to

the corporation to depict about the issue and conduct the

audit to identify the black money and the illegal process

to return the tax file.

(ATO, 2018)

Australian taxation office. 2018. Audits. (online). Available from:

https://www.ato.gov.au/Business/Privately-owned-and-wealthy-groups/What-you-should-

know/Tailored-engagement/Audits/ (accessed on 25 July 2018).

Question 4. What are the four key differences between residents and non-residents for tax

purpose

Residents Non-residents

If a person lives in the Australian territory

for the set period (183 days) of time than

the person is resident for tax purpose.

If a person does not live in the Australian

territory for the set period of time than the

person is non-resident for tax purpose.

If the domicile of person is in Australia than

the person is resident.

And unless he fails to satisfy the ATO about

the same than he is non-resident.

If the person is contributing member of

commonwealth government fund than he is

resident person.

If the person is non contributing member of

commonwealth government fund than he is

non-resident person.

If a person has been moved on in Australia

permanently than the person is resident

A person who has not been moved on in

Australia permanently than the person is

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

the names of three such audits conducted by ATO with brief description for each

Approach Description

Cooperative approach In this process, the department issues the legal notice to

the corporation or the individual to know about the third

party or few bills or the receipts.

Communicating the

position

In this process, the department issues the legal notice to

communicate about the issues and allow the individual

to correct them within a set of time period.

Determine the issue and

conduct the audit

In this process, the department issues the legal notice to

the corporation to depict about the issue and conduct the

audit to identify the black money and the illegal process

to return the tax file.

(ATO, 2018)

Australian taxation office. 2018. Audits. (online). Available from:

https://www.ato.gov.au/Business/Privately-owned-and-wealthy-groups/What-you-should-

know/Tailored-engagement/Audits/ (accessed on 25 July 2018).

Question 4. What are the four key differences between residents and non-residents for tax

purpose

Residents Non-residents

If a person lives in the Australian territory

for the set period (183 days) of time than

the person is resident for tax purpose.

If a person does not live in the Australian

territory for the set period of time than the

person is non-resident for tax purpose.

If the domicile of person is in Australia than

the person is resident.

And unless he fails to satisfy the ATO about

the same than he is non-resident.

If the person is contributing member of

commonwealth government fund than he is

resident person.

If the person is non contributing member of

commonwealth government fund than he is

non-resident person.

If a person has been moved on in Australia

permanently than the person is resident

A person who has not been moved on in

Australia permanently than the person is

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

person. non-resident person (Lewis accountants,

2018).

Lewis accountants. 2018. Resident or non resident. (online). Available from:

https://www.lewistaxation.com.au/tax/general-tax/resident-for-tax-purposes (accessed on

25 July 2018).

Question 5. Section 6(1) of the ITAA 1936 provides 4 exhaustive tests of residence for

individuals. Mention them in brief

Exhaustive test Explanation

Domicile test Domicile of the person must be in Australia

unless the taxation commissioner is satisfied

that the permanent place of tax payer is

outside Australia.

The 183 day test The person must be present in Australia for

183 days in an taxation year unless he would

be non resident.

Commonwealth superannuation fund test If the person is contributing member of

commonwealth government fund than he is

resident person and vice versa.

Employment or family trips A person who has not been moved in

Australia permanently than the person is

resident person and vice versa.

(Lewis accountants, 2018)

Question 6. Part 3 of Tax Agent Services Act 2009 includes ‘The Code of Professional

Conduct’. This code includes 14 core principles that apply to all registered tax agents and

BAS agents. Go to Tax Practitioners Board website (http://www.tpb.gov.au) to research

these core principles and mention principle number five below:

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

2018).

Lewis accountants. 2018. Resident or non resident. (online). Available from:

https://www.lewistaxation.com.au/tax/general-tax/resident-for-tax-purposes (accessed on

25 July 2018).

Question 5. Section 6(1) of the ITAA 1936 provides 4 exhaustive tests of residence for

individuals. Mention them in brief

Exhaustive test Explanation

Domicile test Domicile of the person must be in Australia

unless the taxation commissioner is satisfied

that the permanent place of tax payer is

outside Australia.

The 183 day test The person must be present in Australia for

183 days in an taxation year unless he would

be non resident.

Commonwealth superannuation fund test If the person is contributing member of

commonwealth government fund than he is

resident person and vice versa.

Employment or family trips A person who has not been moved in

Australia permanently than the person is

resident person and vice versa.

(Lewis accountants, 2018)

Question 6. Part 3 of Tax Agent Services Act 2009 includes ‘The Code of Professional

Conduct’. This code includes 14 core principles that apply to all registered tax agents and

BAS agents. Go to Tax Practitioners Board website (http://www.tpb.gov.au) to research

these core principles and mention principle number five below:

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The principle five of Code of Professional Conduct states that the person should have made

suitable arrangements for managing the conflicts of interest that arises from the activities

done by him or her, when registered as a tax agent or BAS agent. Different types of

situations are laid down by the principle in which such conflicts can arise and the

arrangements for managing the same is been done by the agent.

Question 7. Give two examples of “adequate and effective conflict management

arrangements” that you as a “tax practitioner” can apply in your workplace

Integrating the internal control measures and disclosing the conflicts can help in

managing them easily.

Maintenance of appropriate records and documents that represents each and every details

of the policies and procedure formed in relation with the conflict manager, by tax

practitioner. Update regarding the same is also necessary.

Question 8. John, a tax practitioner is requested by his client, Daniel to include some

fictitious expenses in his tax return to reduce the tax liability. John knows that the expenses

were not incurred by Daniel and if he includes them in the tax return, then Principle no. 1

(honesty and integrity) of ‘The Code of Professional Conduct’ will be violated. But at the

same time John does not want to lose Daniel as client. How John can communicate his

professional obligations to Daniel?

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

suitable arrangements for managing the conflicts of interest that arises from the activities

done by him or her, when registered as a tax agent or BAS agent. Different types of

situations are laid down by the principle in which such conflicts can arise and the

arrangements for managing the same is been done by the agent.

Question 7. Give two examples of “adequate and effective conflict management

arrangements” that you as a “tax practitioner” can apply in your workplace

Integrating the internal control measures and disclosing the conflicts can help in

managing them easily.

Maintenance of appropriate records and documents that represents each and every details

of the policies and procedure formed in relation with the conflict manager, by tax

practitioner. Update regarding the same is also necessary.

Question 8. John, a tax practitioner is requested by his client, Daniel to include some

fictitious expenses in his tax return to reduce the tax liability. John knows that the expenses

were not incurred by Daniel and if he includes them in the tax return, then Principle no. 1

(honesty and integrity) of ‘The Code of Professional Conduct’ will be violated. But at the

same time John does not want to lose Daniel as client. How John can communicate his

professional obligations to Daniel?

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

John must follow the fourth principle of code of professional conduct which states that the

John must act in the best interest of his client i.e. Daniel without breaching the provisions of

Law. As a tax practitioner, he is obliged to fulfil the requirements of his clients within the

scale of law. Since John has the knowledge that the deduction claimed by the client is not in

line with law and if he allows Daniel to get the benefit of deduction, it will amount to breach

of first and foremost principle of professional code of conduct which relates to honesty and

Integrity. So he must advise the client that it will be a wrongful act to claim the deduction.

Question 9. For how long the taxpayers need to keep evidence/record for income tax

purpose? Mention the relevant legal provision (name of act and section) for this rule.

Generally the tax payers are required to keep their evidences for the period of five years from

the date of filing of the return and in case of the deduction claimed, the evidence shall be kept

for around 5 years from the last claim for the declined value (Australian Tax Office, 2018).

Australian Tax Office, (2018) Keeping your tax records [Online] Available from

https://www.ato.gov.au/Individuals/Income-and-deductions/In-detail/Keeping-your-tax-

records/ [Accessed on 25th July 2018]

Question 10. Mention the correct lodgment date for the following scenarios

Scenario Lodgeme

nt date

Income tax return for all individuals and trusts where one or more prior year

income tax returns were outstanding as at 30 June.

31st

October

2018

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

John must act in the best interest of his client i.e. Daniel without breaching the provisions of

Law. As a tax practitioner, he is obliged to fulfil the requirements of his clients within the

scale of law. Since John has the knowledge that the deduction claimed by the client is not in

line with law and if he allows Daniel to get the benefit of deduction, it will amount to breach

of first and foremost principle of professional code of conduct which relates to honesty and

Integrity. So he must advise the client that it will be a wrongful act to claim the deduction.

Question 9. For how long the taxpayers need to keep evidence/record for income tax

purpose? Mention the relevant legal provision (name of act and section) for this rule.

Generally the tax payers are required to keep their evidences for the period of five years from

the date of filing of the return and in case of the deduction claimed, the evidence shall be kept

for around 5 years from the last claim for the declined value (Australian Tax Office, 2018).

Australian Tax Office, (2018) Keeping your tax records [Online] Available from

https://www.ato.gov.au/Individuals/Income-and-deductions/In-detail/Keeping-your-tax-

records/ [Accessed on 25th July 2018]

Question 10. Mention the correct lodgment date for the following scenarios

Scenario Lodgeme

nt date

Income tax return for all individuals and trusts where one or more prior year

income tax returns were outstanding as at 30 June.

31st

October

2018

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxpayers who lodge their own return using e-tax or Tax Pack 31st

October

2018

Income tax return for individuals and trusts which were tax level 6 (tax

payable of $20,000 or more on last tax assessment) as per latest year lodge

Business Activity Statement for first quarter 28th April

Business Activity Statement for second quarter 28th July

Business Activity Statement for third quarter 28th October

Business Activity Statement for fourth quarter 28th February

Australian Tax Office, (2018) Quarterly reporting [Online] Available from

https://www.ato.gov.au/Business/Business-activity-statements-(BAS)/Lodging-

and-paying-your-BAS/Due-dates-for-lodging-and-paying-your-BAS/ [Accessed

on 25th July 2018]

31st

March

2019

Question 11. Mention the name of five records/documents that can be kept by taxpayers as

evidence.

The five records that are to be kept by the tax payers as evidence are as follows

1. The document of the payments the tax payer has received.

2. Any document regarding the gifts, donations and contributions (Australian Tax

Office, 2018).

3. The papers regarding the acquisition and disposal of assets if any shall also be kept.

4. The expenses related to the payments that have been received.

5. The previous year returns in order to have a comparative analysis.

Australian Tax Office, (2018) Types of records you should keep [Online] Available from

https://www.ato.gov.au/Individuals/Income-and-deductions/In-detail/Keeping-your-tax-

records/?page=1#Types_of_records_you_should_keep [Accessed on 25th July 2018]

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

October

2018

Income tax return for individuals and trusts which were tax level 6 (tax

payable of $20,000 or more on last tax assessment) as per latest year lodge

Business Activity Statement for first quarter 28th April

Business Activity Statement for second quarter 28th July

Business Activity Statement for third quarter 28th October

Business Activity Statement for fourth quarter 28th February

Australian Tax Office, (2018) Quarterly reporting [Online] Available from

https://www.ato.gov.au/Business/Business-activity-statements-(BAS)/Lodging-

and-paying-your-BAS/Due-dates-for-lodging-and-paying-your-BAS/ [Accessed

on 25th July 2018]

31st

March

2019

Question 11. Mention the name of five records/documents that can be kept by taxpayers as

evidence.

The five records that are to be kept by the tax payers as evidence are as follows

1. The document of the payments the tax payer has received.

2. Any document regarding the gifts, donations and contributions (Australian Tax

Office, 2018).

3. The papers regarding the acquisition and disposal of assets if any shall also be kept.

4. The expenses related to the payments that have been received.

5. The previous year returns in order to have a comparative analysis.

Australian Tax Office, (2018) Types of records you should keep [Online] Available from

https://www.ato.gov.au/Individuals/Income-and-deductions/In-detail/Keeping-your-tax-

records/?page=1#Types_of_records_you_should_keep [Accessed on 25th July 2018]

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 12. What information must be included in a Tax Invoice for taxable supplies

of more than $1000?

The information that must be included in a Tax invoice for the taxable supplies exceeding

more than $1000 are the following the documents.

1. The documents shall consist of a tax invoice at first place.

2. The identity of the seller must be recorded separately.

3. The seller’s Australian Business number must be present on the invoice number.

4. The date shall also be included.

5. The quantity and the price of the items sold shall also be mentioned (Australian Tax

Office, 2018).

6. The amount of the GST if payable can be shown separately.

7. All the taxable sales shall be determined.

Apart from the normal documents the additional documents are

1. The identity number if the buyer or the Australian Business number.

2. The e invoice in a PDF format to a customer.

Australian Tax Office, (2018) Requirements of Tax invoices [Online] Available from

https://www.ato.gov.au/Business/GST/Issuing-tax-invoices/#SalesOf1000OrMore

[Accessed on 25th July 2018]

Question 13. As per tax law, mention five types of taxpayers who must lodge their tax

return.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

of more than $1000?

The information that must be included in a Tax invoice for the taxable supplies exceeding

more than $1000 are the following the documents.

1. The documents shall consist of a tax invoice at first place.

2. The identity of the seller must be recorded separately.

3. The seller’s Australian Business number must be present on the invoice number.

4. The date shall also be included.

5. The quantity and the price of the items sold shall also be mentioned (Australian Tax

Office, 2018).

6. The amount of the GST if payable can be shown separately.

7. All the taxable sales shall be determined.

Apart from the normal documents the additional documents are

1. The identity number if the buyer or the Australian Business number.

2. The e invoice in a PDF format to a customer.

Australian Tax Office, (2018) Requirements of Tax invoices [Online] Available from

https://www.ato.gov.au/Business/GST/Issuing-tax-invoices/#SalesOf1000OrMore

[Accessed on 25th July 2018]

Question 13. As per tax law, mention five types of taxpayers who must lodge their tax

return.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

The five types of the tax payers who must lodge their returns normally are as follows

(Australian Tax Office, 2018).

Individuals

Trusts and Associations

Companies and super funds

Partnership firms

Consolidated groups

Australian Tax Office, (2018) Tax returns by client type [Online] Available from

https://www.ato.gov.au/Tax-professionals/Prepare-and-lodge/Tax-agent-lodgment-

program/Tax-returns-by-client-type/ [Accessed on 25th July 2018]

Question 14 How much assessable income was derived by each of the following

taxpayers?

Scenario Assessable income

Kelly's net wages were $1 350. Her

employer had deducted $380 tax.

Assessable income: $ 1350

Alan received net wages of $50 300 and

bank interest of $400 over the year. His

employer deducted $19 700 tax.

Assessable income: $ 50300+ $ 400= $

50700

Karl received a net salary of $41 800 over

the year plus $120 bank interest. He also

was paid a gross salary of $2 000 for a part-

time job he had during the year. The tax

deducted from his full-time job was $13 600

and $600 was deducted from his part time

wages.

Assessable income: $ 41800+ $ 120+

$2000= $ 43920

Fiona runs a small business that had $36

000 in sales during the year. Her net profit

was calculated by deducting $22 000 of

expenses.

Net profit= Sales – Expenses

=$ 36000- $ 22000

=$ 14000= Assessable Income

Question 15. Advise whether the following are assessable income, statutory income,

exempt income or non-assessable income.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

(Australian Tax Office, 2018).

Individuals

Trusts and Associations

Companies and super funds

Partnership firms

Consolidated groups

Australian Tax Office, (2018) Tax returns by client type [Online] Available from

https://www.ato.gov.au/Tax-professionals/Prepare-and-lodge/Tax-agent-lodgment-

program/Tax-returns-by-client-type/ [Accessed on 25th July 2018]

Question 14 How much assessable income was derived by each of the following

taxpayers?

Scenario Assessable income

Kelly's net wages were $1 350. Her

employer had deducted $380 tax.

Assessable income: $ 1350

Alan received net wages of $50 300 and

bank interest of $400 over the year. His

employer deducted $19 700 tax.

Assessable income: $ 50300+ $ 400= $

50700

Karl received a net salary of $41 800 over

the year plus $120 bank interest. He also

was paid a gross salary of $2 000 for a part-

time job he had during the year. The tax

deducted from his full-time job was $13 600

and $600 was deducted from his part time

wages.

Assessable income: $ 41800+ $ 120+

$2000= $ 43920

Fiona runs a small business that had $36

000 in sales during the year. Her net profit

was calculated by deducting $22 000 of

expenses.

Net profit= Sales – Expenses

=$ 36000- $ 22000

=$ 14000= Assessable Income

Question 15. Advise whether the following are assessable income, statutory income,

exempt income or non-assessable income.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC502/ 2018/ T1/ Assessment Tool

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.