FNSACC502 Assignment Solution: Medicare Levy and Tax Calculation

VerifiedAdded on 2023/06/15

|31

|8252

|295

Homework Assignment

AI Summary

This assignment solution for FNSACC502 covers various aspects of Australian taxation, including the calculation of Medicare Levy for different family scenarios based on their taxable incomes and dependent children. It addresses tax calculations for individuals with reportable fringe benefits, PAYG tax installments, and dividend income. The solution also delves into calculating taxable income from both Australian and foreign sources, considering factors like foreign tax offsets and reportable fringe benefits. Furthermore, it tackles capital gains tax calculations, comparing indexed cost base and discount methods for asset disposals, and partial main residence exemptions. The assignment provides detailed computations and explanations for each scenario, offering a comprehensive understanding of the relevant tax principles and their practical application. Desklib provides more solved assignments like these to help students.

Units Covered: FNSACC502

The following questions are based on the material in Chapter 1:

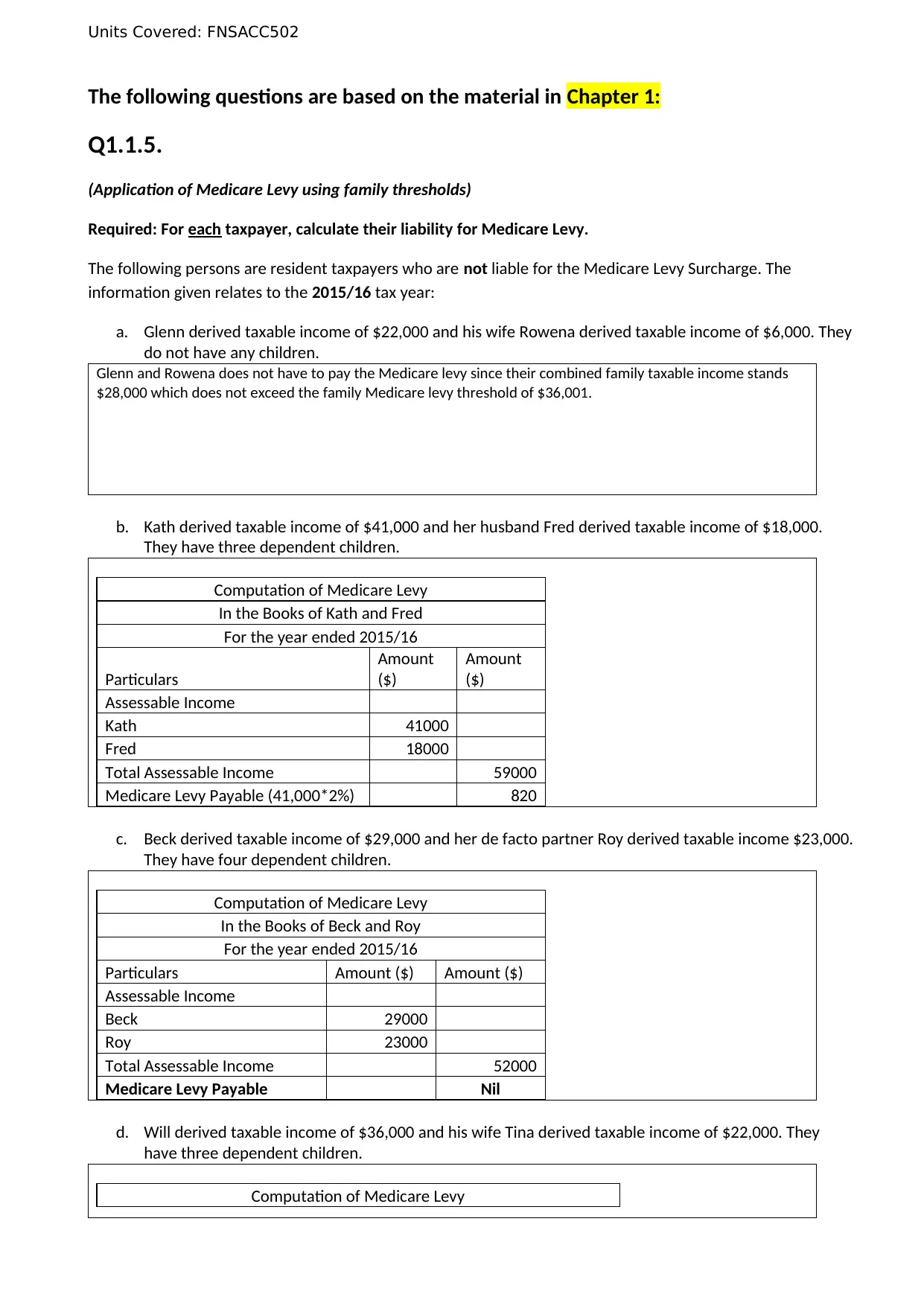

Q1.1.5.

(Application of Medicare Levy using family thresholds)

Required: For each taxpayer, calculate their liability for Medicare Levy.

The following persons are resident taxpayers who are not liable for the Medicare Levy Surcharge. The

information given relates to the 2015/16 tax year:

a. Glenn derived taxable income of $22,000 and his wife Rowena derived taxable income of $6,000. They

do not have any children.

Glenn and Rowena does not have to pay the Medicare levy since their combined family taxable income stands

$28,000 which does not exceed the family Medicare levy threshold of $36,001.

b. Kath derived taxable income of $41,000 and her husband Fred derived taxable income of $18,000.

They have three dependent children.

Computation of Medicare Levy

In the Books of Kath and Fred

For the year ended 2015/16

Particulars

Amount

($)

Amount

($)

Assessable Income

Kath 41000

Fred 18000

Total Assessable Income 59000

Medicare Levy Payable (41,000*2%) 820

c. Beck derived taxable income of $29,000 and her de facto partner Roy derived taxable income $23,000.

They have four dependent children.

Computation of Medicare Levy

In the Books of Beck and Roy

For the year ended 2015/16

Particulars Amount ($) Amount ($)

Assessable Income

Beck 29000

Roy 23000

Total Assessable Income 52000

Medicare Levy Payable Nil

d. Will derived taxable income of $36,000 and his wife Tina derived taxable income of $22,000. They

have three dependent children.

Computation of Medicare Levy

The following questions are based on the material in Chapter 1:

Q1.1.5.

(Application of Medicare Levy using family thresholds)

Required: For each taxpayer, calculate their liability for Medicare Levy.

The following persons are resident taxpayers who are not liable for the Medicare Levy Surcharge. The

information given relates to the 2015/16 tax year:

a. Glenn derived taxable income of $22,000 and his wife Rowena derived taxable income of $6,000. They

do not have any children.

Glenn and Rowena does not have to pay the Medicare levy since their combined family taxable income stands

$28,000 which does not exceed the family Medicare levy threshold of $36,001.

b. Kath derived taxable income of $41,000 and her husband Fred derived taxable income of $18,000.

They have three dependent children.

Computation of Medicare Levy

In the Books of Kath and Fred

For the year ended 2015/16

Particulars

Amount

($)

Amount

($)

Assessable Income

Kath 41000

Fred 18000

Total Assessable Income 59000

Medicare Levy Payable (41,000*2%) 820

c. Beck derived taxable income of $29,000 and her de facto partner Roy derived taxable income $23,000.

They have four dependent children.

Computation of Medicare Levy

In the Books of Beck and Roy

For the year ended 2015/16

Particulars Amount ($) Amount ($)

Assessable Income

Beck 29000

Roy 23000

Total Assessable Income 52000

Medicare Levy Payable Nil

d. Will derived taxable income of $36,000 and his wife Tina derived taxable income of $22,000. They

have three dependent children.

Computation of Medicare Levy

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC502

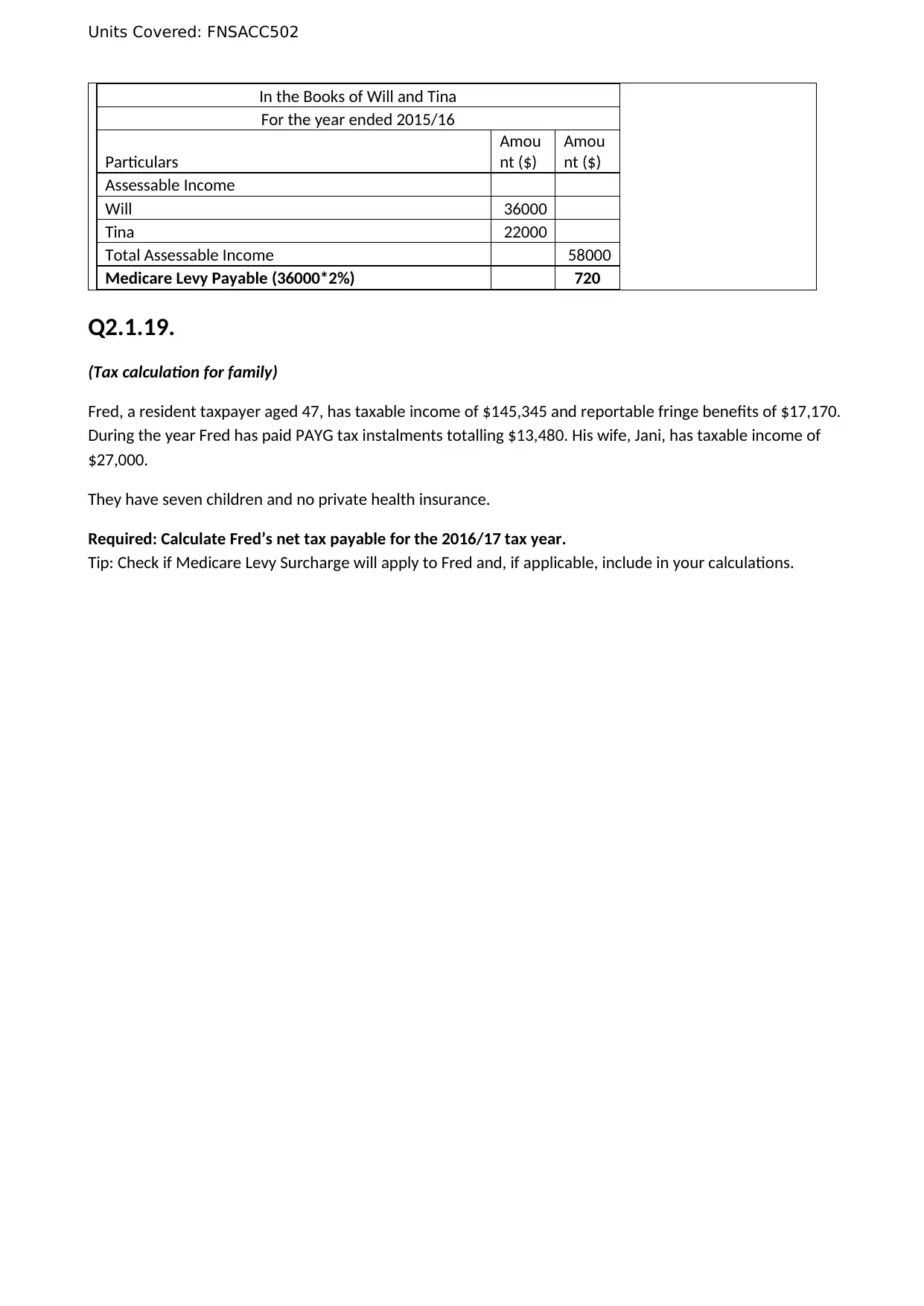

In the Books of Will and Tina

For the year ended 2015/16

Particulars

Amou

nt ($)

Amou

nt ($)

Assessable Income

Will 36000

Tina 22000

Total Assessable Income 58000

Medicare Levy Payable (36000*2%) 720

Q2.1.19.

(Tax calculation for family)

Fred, a resident taxpayer aged 47, has taxable income of $145,345 and reportable fringe benefits of $17,170.

During the year Fred has paid PAYG tax instalments totalling $13,480. His wife, Jani, has taxable income of

$27,000.

They have seven children and no private health insurance.

Required: Calculate Fred’s net tax payable for the 2016/17 tax year.

Tip: Check if Medicare Levy Surcharge will apply to Fred and, if applicable, include in your calculations.

In the Books of Will and Tina

For the year ended 2015/16

Particulars

Amou

nt ($)

Amou

nt ($)

Assessable Income

Will 36000

Tina 22000

Total Assessable Income 58000

Medicare Levy Payable (36000*2%) 720

Q2.1.19.

(Tax calculation for family)

Fred, a resident taxpayer aged 47, has taxable income of $145,345 and reportable fringe benefits of $17,170.

During the year Fred has paid PAYG tax instalments totalling $13,480. His wife, Jani, has taxable income of

$27,000.

They have seven children and no private health insurance.

Required: Calculate Fred’s net tax payable for the 2016/17 tax year.

Tip: Check if Medicare Levy Surcharge will apply to Fred and, if applicable, include in your calculations.

Units Covered: FNSACC502

The following questions are based on the material in Chapter 2:

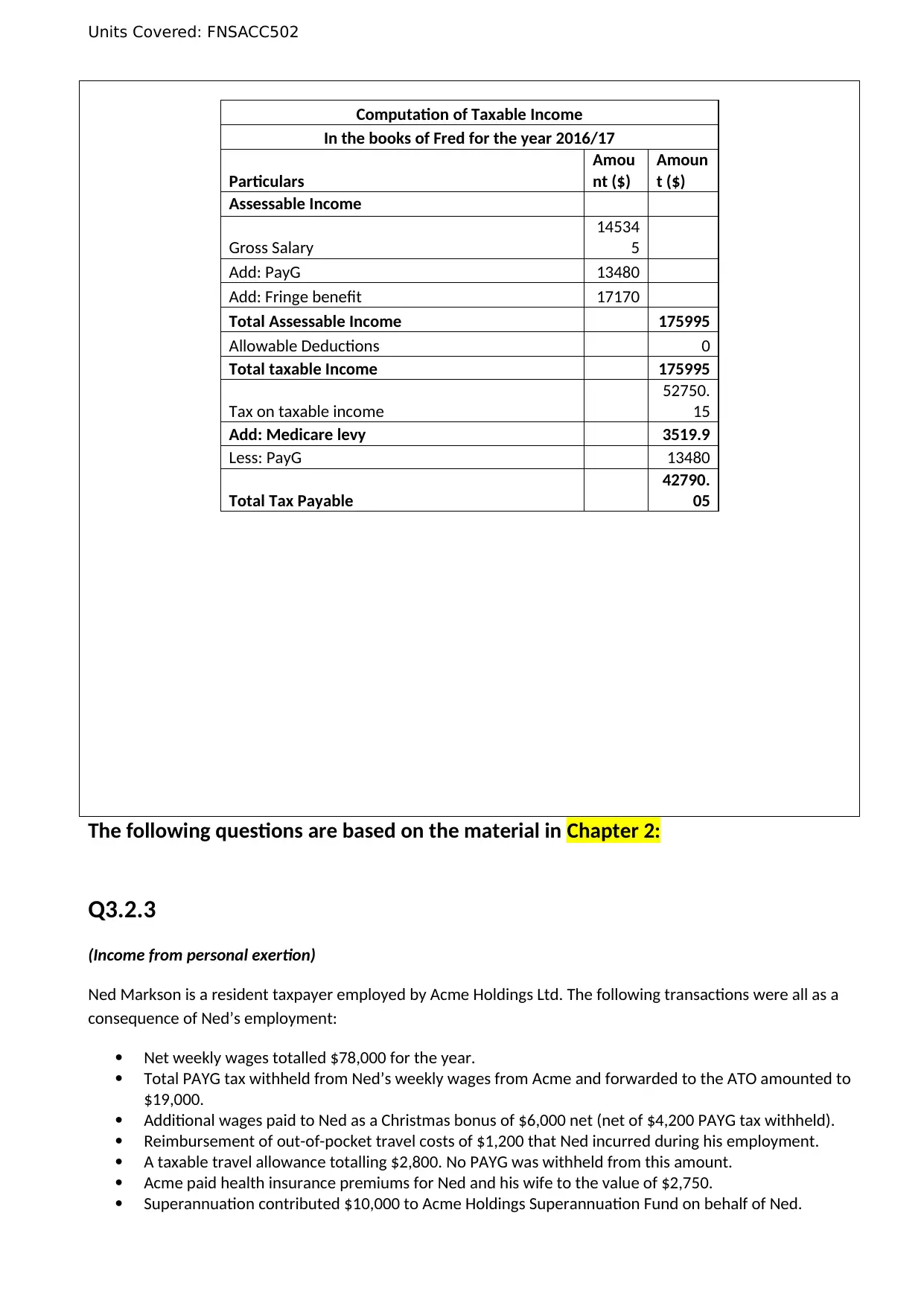

Q3.2.3

(Income from personal exertion)

Ned Markson is a resident taxpayer employed by Acme Holdings Ltd. The following transactions were all as a

consequence of Ned’s employment:

Net weekly wages totalled $78,000 for the year.

Total PAYG tax withheld from Ned’s weekly wages from Acme and forwarded to the ATO amounted to

$19,000.

Additional wages paid to Ned as a Christmas bonus of $6,000 net (net of $4,200 PAYG tax withheld).

Reimbursement of out-of-pocket travel costs of $1,200 that Ned incurred during his employment.

A taxable travel allowance totalling $2,800. No PAYG was withheld from this amount.

Acme paid health insurance premiums for Ned and his wife to the value of $2,750.

Superannuation contributed $10,000 to Acme Holdings Superannuation Fund on behalf of Ned.

Computation of Taxable Income

In the books of Fred for the year 2016/17

Particulars

Amou

nt ($)

Amoun

t ($)

Assessable Income

Gross Salary

14534

5

Add: PayG 13480

Add: Fringe benefit 17170

Total Assessable Income 175995

Allowable Deductions 0

Total taxable Income 175995

Tax on taxable income

52750.

15

Add: Medicare levy 3519.9

Less: PayG 13480

Total Tax Payable

42790.

05

The following questions are based on the material in Chapter 2:

Q3.2.3

(Income from personal exertion)

Ned Markson is a resident taxpayer employed by Acme Holdings Ltd. The following transactions were all as a

consequence of Ned’s employment:

Net weekly wages totalled $78,000 for the year.

Total PAYG tax withheld from Ned’s weekly wages from Acme and forwarded to the ATO amounted to

$19,000.

Additional wages paid to Ned as a Christmas bonus of $6,000 net (net of $4,200 PAYG tax withheld).

Reimbursement of out-of-pocket travel costs of $1,200 that Ned incurred during his employment.

A taxable travel allowance totalling $2,800. No PAYG was withheld from this amount.

Acme paid health insurance premiums for Ned and his wife to the value of $2,750.

Superannuation contributed $10,000 to Acme Holdings Superannuation Fund on behalf of Ned.

Computation of Taxable Income

In the books of Fred for the year 2016/17

Particulars

Amou

nt ($)

Amoun

t ($)

Assessable Income

Gross Salary

14534

5

Add: PayG 13480

Add: Fringe benefit 17170

Total Assessable Income 175995

Allowable Deductions 0

Total taxable Income 175995

Tax on taxable income

52750.

15

Add: Medicare levy 3519.9

Less: PayG 13480

Total Tax Payable

42790.

05

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Units Covered: FNSACC502

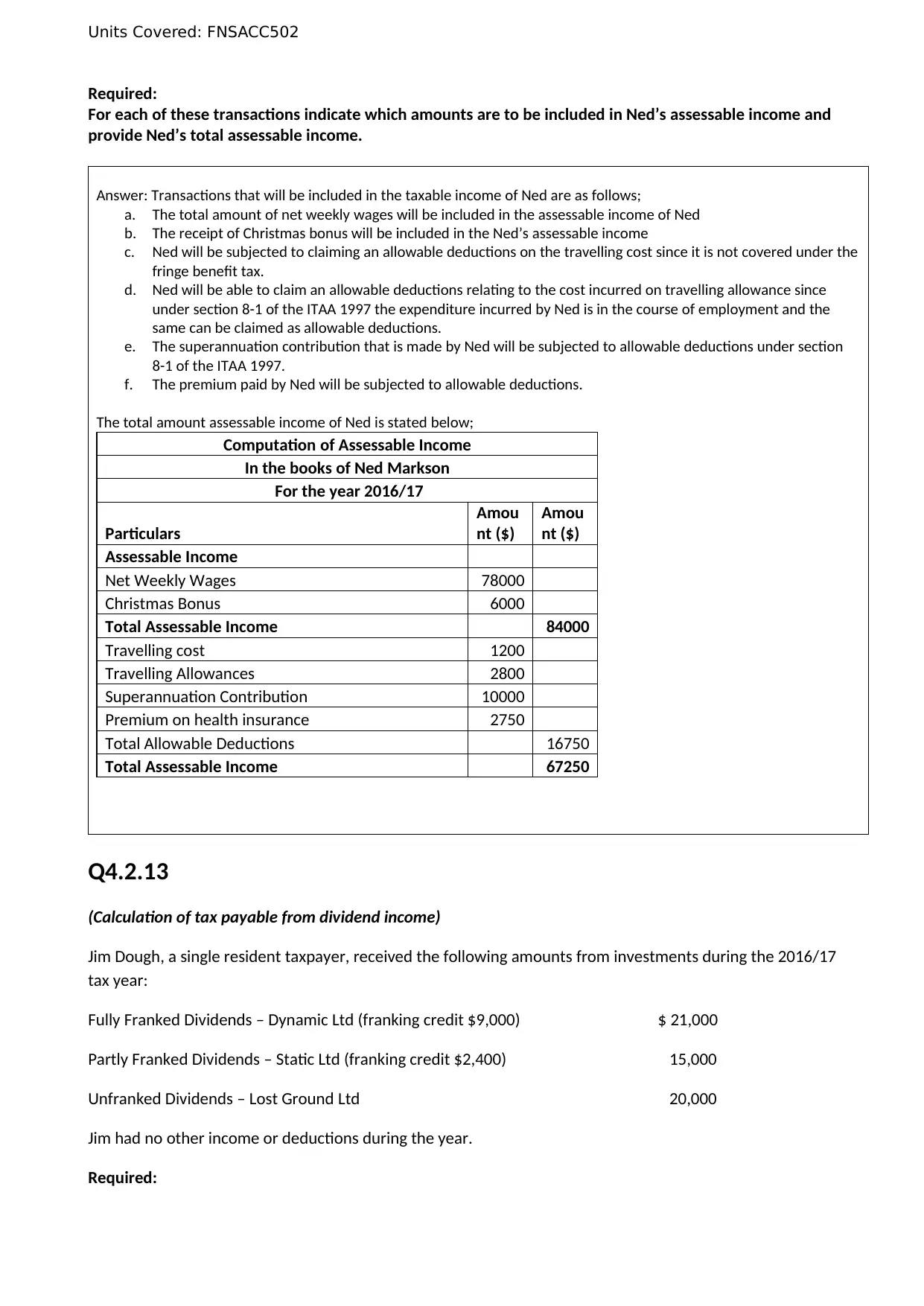

Required:

For each of these transactions indicate which amounts are to be included in Ned’s assessable income and

provide Ned’s total assessable income.

Answer: Transactions that will be included in the taxable income of Ned are as follows;

a. The total amount of net weekly wages will be included in the assessable income of Ned

b. The receipt of Christmas bonus will be included in the Ned’s assessable income

c. Ned will be subjected to claiming an allowable deductions on the travelling cost since it is not covered under the

fringe benefit tax.

d. Ned will be able to claim an allowable deductions relating to the cost incurred on travelling allowance since

under section 8-1 of the ITAA 1997 the expenditure incurred by Ned is in the course of employment and the

same can be claimed as allowable deductions.

e. The superannuation contribution that is made by Ned will be subjected to allowable deductions under section

8-1 of the ITAA 1997.

f. The premium paid by Ned will be subjected to allowable deductions.

The total amount assessable income of Ned is stated below;

Computation of Assessable Income

In the books of Ned Markson

For the year 2016/17

Particulars

Amou

nt ($)

Amou

nt ($)

Assessable Income

Net Weekly Wages 78000

Christmas Bonus 6000

Total Assessable Income 84000

Travelling cost 1200

Travelling Allowances 2800

Superannuation Contribution 10000

Premium on health insurance 2750

Total Allowable Deductions 16750

Total Assessable Income 67250

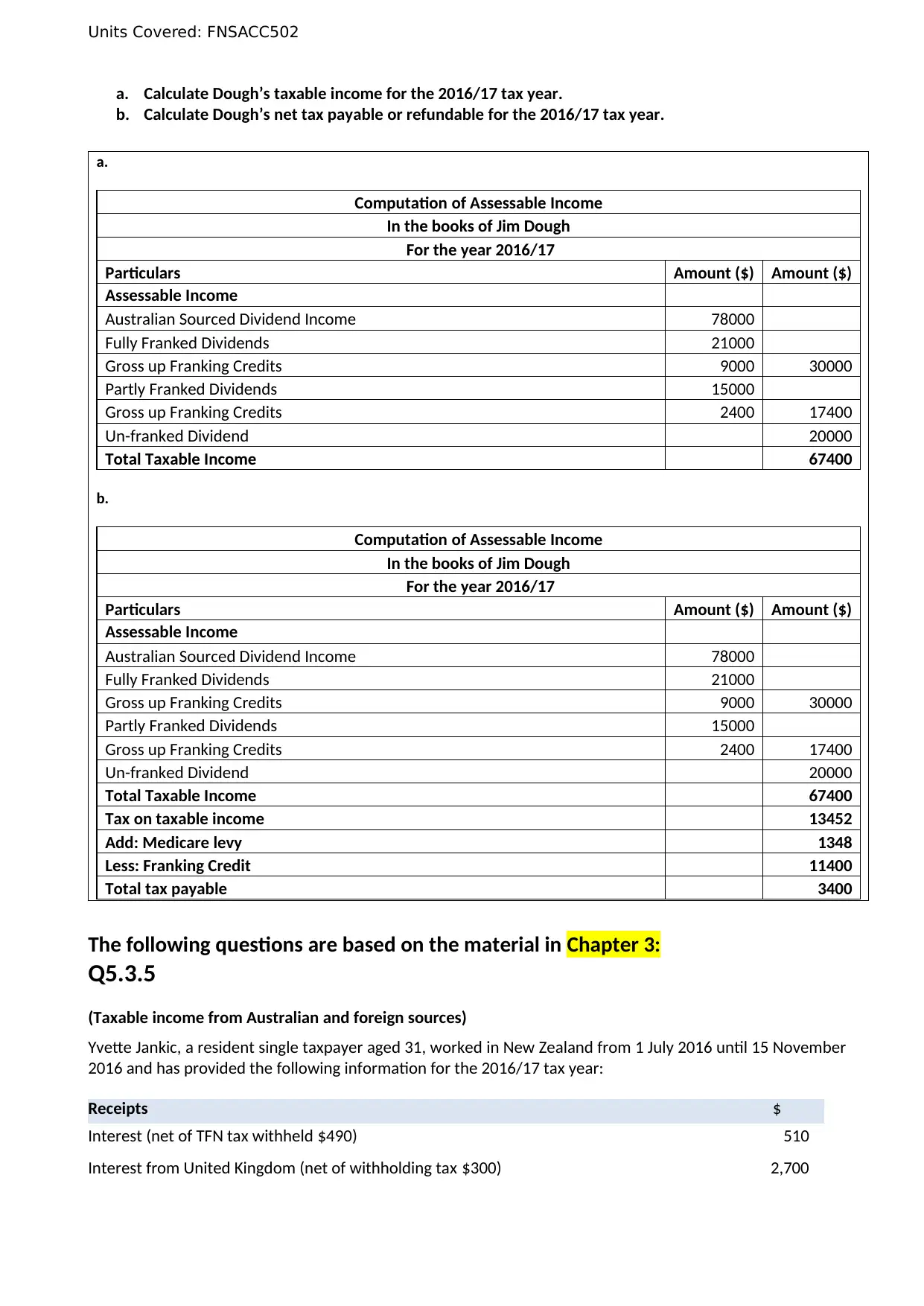

Q4.2.13

(Calculation of tax payable from dividend income)

Jim Dough, a single resident taxpayer, received the following amounts from investments during the 2016/17

tax year:

Fully Franked Dividends – Dynamic Ltd (franking credit $9,000) $ 21,000

Partly Franked Dividends – Static Ltd (franking credit $2,400) 15,000

Unfranked Dividends – Lost Ground Ltd 20,000

Jim had no other income or deductions during the year.

Required:

Required:

For each of these transactions indicate which amounts are to be included in Ned’s assessable income and

provide Ned’s total assessable income.

Answer: Transactions that will be included in the taxable income of Ned are as follows;

a. The total amount of net weekly wages will be included in the assessable income of Ned

b. The receipt of Christmas bonus will be included in the Ned’s assessable income

c. Ned will be subjected to claiming an allowable deductions on the travelling cost since it is not covered under the

fringe benefit tax.

d. Ned will be able to claim an allowable deductions relating to the cost incurred on travelling allowance since

under section 8-1 of the ITAA 1997 the expenditure incurred by Ned is in the course of employment and the

same can be claimed as allowable deductions.

e. The superannuation contribution that is made by Ned will be subjected to allowable deductions under section

8-1 of the ITAA 1997.

f. The premium paid by Ned will be subjected to allowable deductions.

The total amount assessable income of Ned is stated below;

Computation of Assessable Income

In the books of Ned Markson

For the year 2016/17

Particulars

Amou

nt ($)

Amou

nt ($)

Assessable Income

Net Weekly Wages 78000

Christmas Bonus 6000

Total Assessable Income 84000

Travelling cost 1200

Travelling Allowances 2800

Superannuation Contribution 10000

Premium on health insurance 2750

Total Allowable Deductions 16750

Total Assessable Income 67250

Q4.2.13

(Calculation of tax payable from dividend income)

Jim Dough, a single resident taxpayer, received the following amounts from investments during the 2016/17

tax year:

Fully Franked Dividends – Dynamic Ltd (franking credit $9,000) $ 21,000

Partly Franked Dividends – Static Ltd (franking credit $2,400) 15,000

Unfranked Dividends – Lost Ground Ltd 20,000

Jim had no other income or deductions during the year.

Required:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC502

a. Calculate Dough’s taxable income for the 2016/17 tax year.

b. Calculate Dough’s net tax payable or refundable for the 2016/17 tax year.

a.

Computation of Assessable Income

In the books of Jim Dough

For the year 2016/17

Particulars Amount ($) Amount ($)

Assessable Income

Australian Sourced Dividend Income 78000

Fully Franked Dividends 21000

Gross up Franking Credits 9000 30000

Partly Franked Dividends 15000

Gross up Franking Credits 2400 17400

Un-franked Dividend 20000

Total Taxable Income 67400

b.

Computation of Assessable Income

In the books of Jim Dough

For the year 2016/17

Particulars Amount ($) Amount ($)

Assessable Income

Australian Sourced Dividend Income 78000

Fully Franked Dividends 21000

Gross up Franking Credits 9000 30000

Partly Franked Dividends 15000

Gross up Franking Credits 2400 17400

Un-franked Dividend 20000

Total Taxable Income 67400

Tax on taxable income 13452

Add: Medicare levy 1348

Less: Franking Credit 11400

Total tax payable 3400

The following questions are based on the material in Chapter 3:

Q5.3.5

(Taxable income from Australian and foreign sources)

Yvette Jankic, a resident single taxpayer aged 31, worked in New Zealand from 1 July 2016 until 15 November

2016 and has provided the following information for the 2016/17 tax year:

Receipts $

Interest (net of TFN tax withheld $490) 510

Interest from United Kingdom (net of withholding tax $300) 2,700

a. Calculate Dough’s taxable income for the 2016/17 tax year.

b. Calculate Dough’s net tax payable or refundable for the 2016/17 tax year.

a.

Computation of Assessable Income

In the books of Jim Dough

For the year 2016/17

Particulars Amount ($) Amount ($)

Assessable Income

Australian Sourced Dividend Income 78000

Fully Franked Dividends 21000

Gross up Franking Credits 9000 30000

Partly Franked Dividends 15000

Gross up Franking Credits 2400 17400

Un-franked Dividend 20000

Total Taxable Income 67400

b.

Computation of Assessable Income

In the books of Jim Dough

For the year 2016/17

Particulars Amount ($) Amount ($)

Assessable Income

Australian Sourced Dividend Income 78000

Fully Franked Dividends 21000

Gross up Franking Credits 9000 30000

Partly Franked Dividends 15000

Gross up Franking Credits 2400 17400

Un-franked Dividend 20000

Total Taxable Income 67400

Tax on taxable income 13452

Add: Medicare levy 1348

Less: Franking Credit 11400

Total tax payable 3400

The following questions are based on the material in Chapter 3:

Q5.3.5

(Taxable income from Australian and foreign sources)

Yvette Jankic, a resident single taxpayer aged 31, worked in New Zealand from 1 July 2016 until 15 November

2016 and has provided the following information for the 2016/17 tax year:

Receipts $

Interest (net of TFN tax withheld $490) 510

Interest from United Kingdom (net of withholding tax $300) 2,700

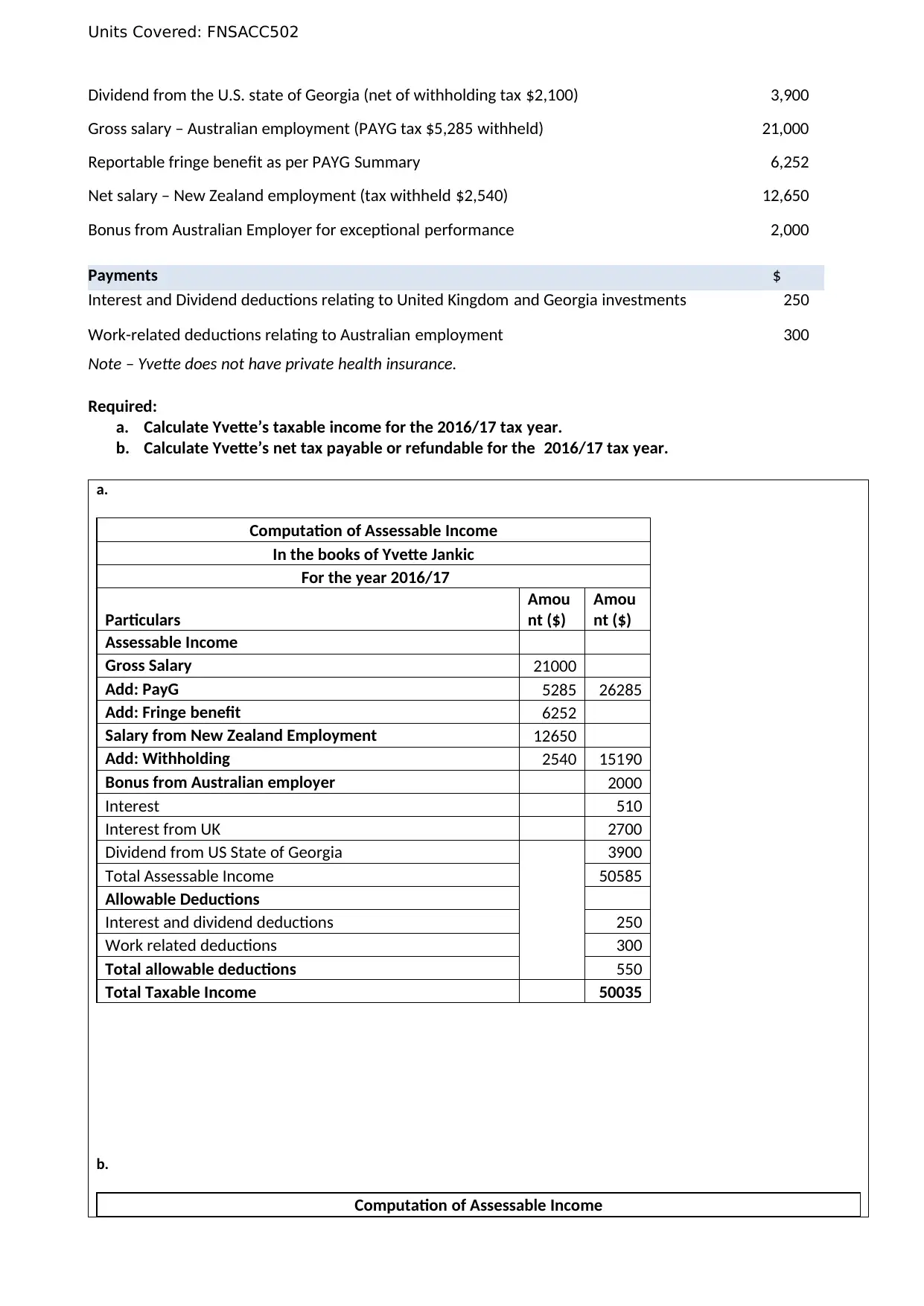

Units Covered: FNSACC502

Dividend from the U.S. state of Georgia (net of withholding tax $2,100) 3,900

Gross salary – Australian employment (PAYG tax $5,285 withheld) 21,000

Reportable fringe benefit as per PAYG Summary 6,252

Net salary – New Zealand employment (tax withheld $2,540) 12,650

Bonus from Australian Employer for exceptional performance 2,000

Payments $

Interest and Dividend deductions relating to United Kingdom and Georgia investments 250

Work-related deductions relating to Australian employment 300

Note – Yvette does not have private health insurance.

Required:

a. Calculate Yvette’s taxable income for the 2016/17 tax year.

b. Calculate Yvette’s net tax payable or refundable for the 2016/17 tax year.

a.

Computation of Assessable Income

In the books of Yvette Jankic

For the year 2016/17

Particulars

Amou

nt ($)

Amou

nt ($)

Assessable Income

Gross Salary 21000

Add: PayG 5285 26285

Add: Fringe benefit 6252

Salary from New Zealand Employment 12650

Add: Withholding 2540 15190

Bonus from Australian employer 2000

Interest 510

Interest from UK 2700

Dividend from US State of Georgia 3900

Total Assessable Income 50585

Allowable Deductions

Interest and dividend deductions 250

Work related deductions 300

Total allowable deductions 550

Total Taxable Income 50035

b.

Computation of Assessable Income

Dividend from the U.S. state of Georgia (net of withholding tax $2,100) 3,900

Gross salary – Australian employment (PAYG tax $5,285 withheld) 21,000

Reportable fringe benefit as per PAYG Summary 6,252

Net salary – New Zealand employment (tax withheld $2,540) 12,650

Bonus from Australian Employer for exceptional performance 2,000

Payments $

Interest and Dividend deductions relating to United Kingdom and Georgia investments 250

Work-related deductions relating to Australian employment 300

Note – Yvette does not have private health insurance.

Required:

a. Calculate Yvette’s taxable income for the 2016/17 tax year.

b. Calculate Yvette’s net tax payable or refundable for the 2016/17 tax year.

a.

Computation of Assessable Income

In the books of Yvette Jankic

For the year 2016/17

Particulars

Amou

nt ($)

Amou

nt ($)

Assessable Income

Gross Salary 21000

Add: PayG 5285 26285

Add: Fringe benefit 6252

Salary from New Zealand Employment 12650

Add: Withholding 2540 15190

Bonus from Australian employer 2000

Interest 510

Interest from UK 2700

Dividend from US State of Georgia 3900

Total Assessable Income 50585

Allowable Deductions

Interest and dividend deductions 250

Work related deductions 300

Total allowable deductions 550

Total Taxable Income 50035

b.

Computation of Assessable Income

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

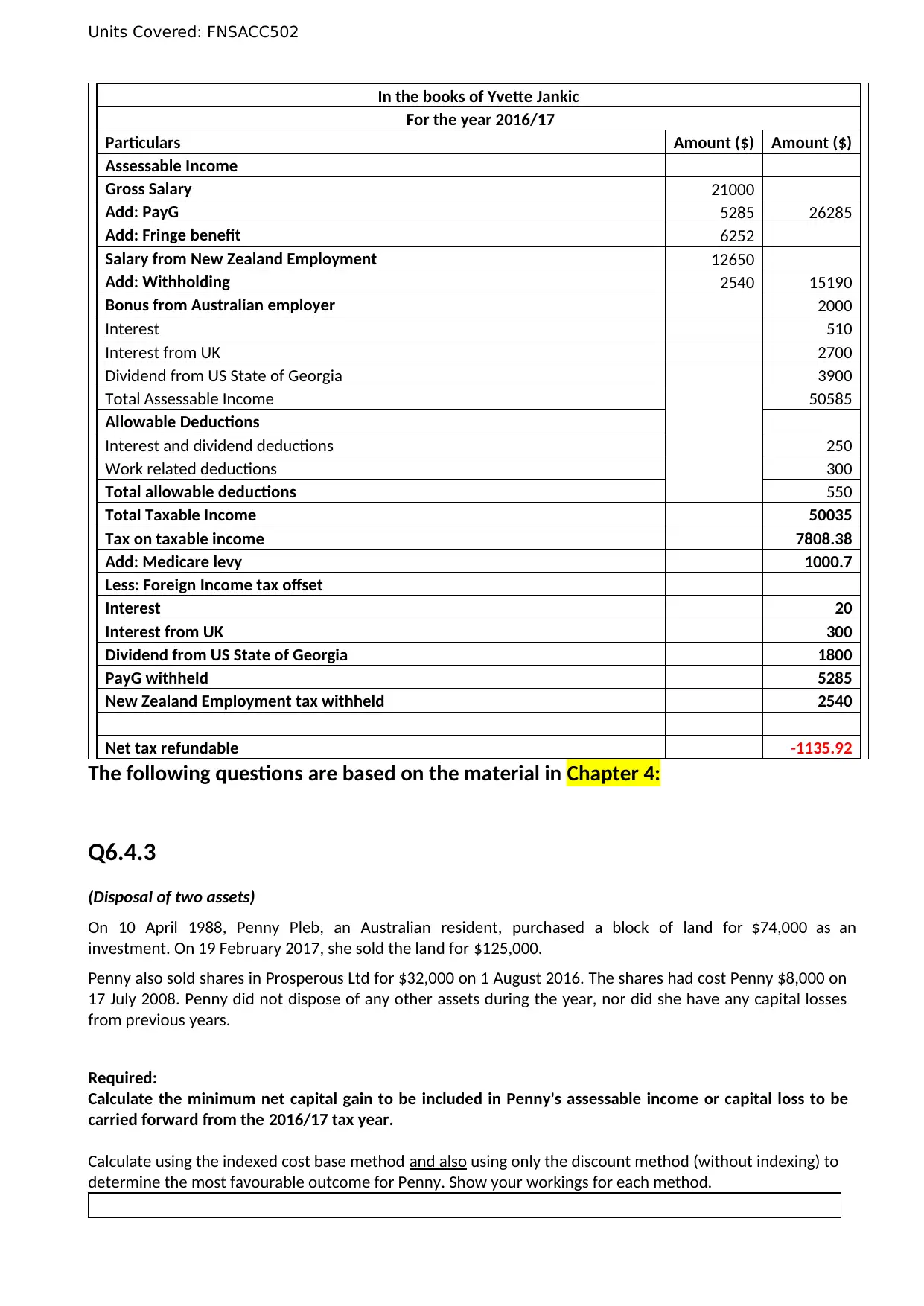

Units Covered: FNSACC502

In the books of Yvette Jankic

For the year 2016/17

Particulars Amount ($) Amount ($)

Assessable Income

Gross Salary 21000

Add: PayG 5285 26285

Add: Fringe benefit 6252

Salary from New Zealand Employment 12650

Add: Withholding 2540 15190

Bonus from Australian employer 2000

Interest 510

Interest from UK 2700

Dividend from US State of Georgia 3900

Total Assessable Income 50585

Allowable Deductions

Interest and dividend deductions 250

Work related deductions 300

Total allowable deductions 550

Total Taxable Income 50035

Tax on taxable income 7808.38

Add: Medicare levy 1000.7

Less: Foreign Income tax offset

Interest 20

Interest from UK 300

Dividend from US State of Georgia 1800

PayG withheld 5285

New Zealand Employment tax withheld 2540

Net tax refundable -1135.92

The following questions are based on the material in Chapter 4:

Q6.4.3

(Disposal of two assets)

On 10 April 1988, Penny Pleb, an Australian resident, purchased a block of land for $74,000 as an

investment. On 19 February 2017, she sold the land for $125,000.

Penny also sold shares in Prosperous Ltd for $32,000 on 1 August 2016. The shares had cost Penny $8,000 on

17 July 2008. Penny did not dispose of any other assets during the year, nor did she have any capital losses

from previous years.

Required:

Calculate the minimum net capital gain to be included in Penny's assessable income or capital loss to be

carried forward from the 2016/17 tax year.

Calculate using the indexed cost base method and also using only the discount method (without indexing) to

determine the most favourable outcome for Penny. Show your workings for each method.

In the books of Yvette Jankic

For the year 2016/17

Particulars Amount ($) Amount ($)

Assessable Income

Gross Salary 21000

Add: PayG 5285 26285

Add: Fringe benefit 6252

Salary from New Zealand Employment 12650

Add: Withholding 2540 15190

Bonus from Australian employer 2000

Interest 510

Interest from UK 2700

Dividend from US State of Georgia 3900

Total Assessable Income 50585

Allowable Deductions

Interest and dividend deductions 250

Work related deductions 300

Total allowable deductions 550

Total Taxable Income 50035

Tax on taxable income 7808.38

Add: Medicare levy 1000.7

Less: Foreign Income tax offset

Interest 20

Interest from UK 300

Dividend from US State of Georgia 1800

PayG withheld 5285

New Zealand Employment tax withheld 2540

Net tax refundable -1135.92

The following questions are based on the material in Chapter 4:

Q6.4.3

(Disposal of two assets)

On 10 April 1988, Penny Pleb, an Australian resident, purchased a block of land for $74,000 as an

investment. On 19 February 2017, she sold the land for $125,000.

Penny also sold shares in Prosperous Ltd for $32,000 on 1 August 2016. The shares had cost Penny $8,000 on

17 July 2008. Penny did not dispose of any other assets during the year, nor did she have any capital losses

from previous years.

Required:

Calculate the minimum net capital gain to be included in Penny's assessable income or capital loss to be

carried forward from the 2016/17 tax year.

Calculate using the indexed cost base method and also using only the discount method (without indexing) to

determine the most favourable outcome for Penny. Show your workings for each method.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC502

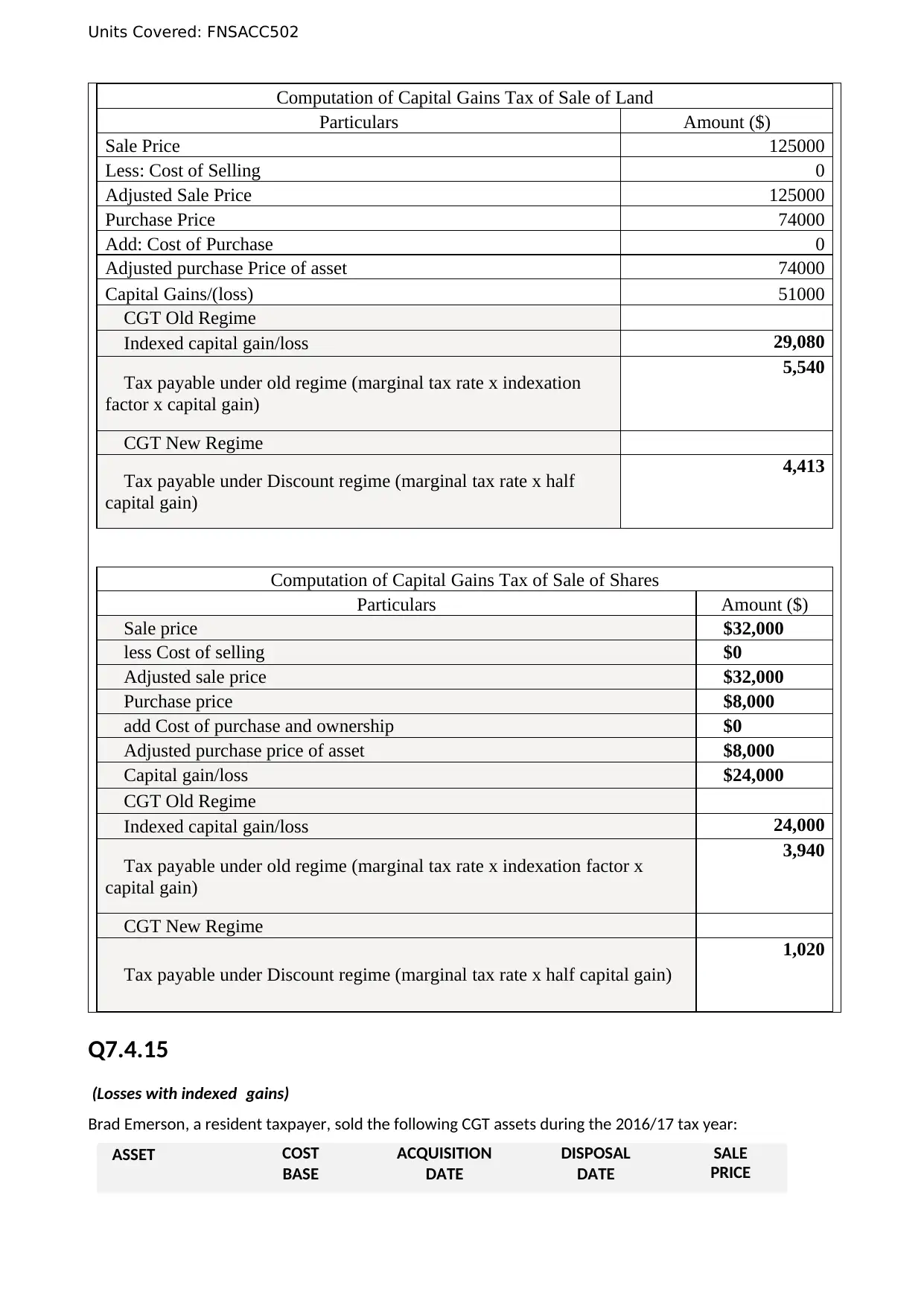

Computation of Capital Gains Tax of Sale of Land

Particulars Amount ($)

Sale Price 125000

Less: Cost of Selling 0

Adjusted Sale Price 125000

Purchase Price 74000

Add: Cost of Purchase 0

Adjusted purchase Price of asset 74000

Capital Gains/(loss) 51000

CGT Old Regime

Indexed capital gain/loss 29,080

Tax payable under old regime (marginal tax rate x indexation

factor x capital gain)

5,540

CGT New Regime

Tax payable under Discount regime (marginal tax rate x half

capital gain)

4,413

Computation of Capital Gains Tax of Sale of Shares

Particulars Amount ($)

Sale price $32,000

less Cost of selling $0

Adjusted sale price $32,000

Purchase price $8,000

add Cost of purchase and ownership $0

Adjusted purchase price of asset $8,000

Capital gain/loss $24,000

CGT Old Regime

Indexed capital gain/loss 24,000

Tax payable under old regime (marginal tax rate x indexation factor x

capital gain)

3,940

CGT New Regime

Tax payable under Discount regime (marginal tax rate x half capital gain)

1,020

Q7.4.15

(Losses with indexed gains)

Brad Emerson, a resident taxpayer, sold the following CGT assets during the 2016/17 tax year:

ASSET COST

BASE

ACQUISITION

DATE

DISPOSAL

DATE

SALE

PRICE

Computation of Capital Gains Tax of Sale of Land

Particulars Amount ($)

Sale Price 125000

Less: Cost of Selling 0

Adjusted Sale Price 125000

Purchase Price 74000

Add: Cost of Purchase 0

Adjusted purchase Price of asset 74000

Capital Gains/(loss) 51000

CGT Old Regime

Indexed capital gain/loss 29,080

Tax payable under old regime (marginal tax rate x indexation

factor x capital gain)

5,540

CGT New Regime

Tax payable under Discount regime (marginal tax rate x half

capital gain)

4,413

Computation of Capital Gains Tax of Sale of Shares

Particulars Amount ($)

Sale price $32,000

less Cost of selling $0

Adjusted sale price $32,000

Purchase price $8,000

add Cost of purchase and ownership $0

Adjusted purchase price of asset $8,000

Capital gain/loss $24,000

CGT Old Regime

Indexed capital gain/loss 24,000

Tax payable under old regime (marginal tax rate x indexation factor x

capital gain)

3,940

CGT New Regime

Tax payable under Discount regime (marginal tax rate x half capital gain)

1,020

Q7.4.15

(Losses with indexed gains)

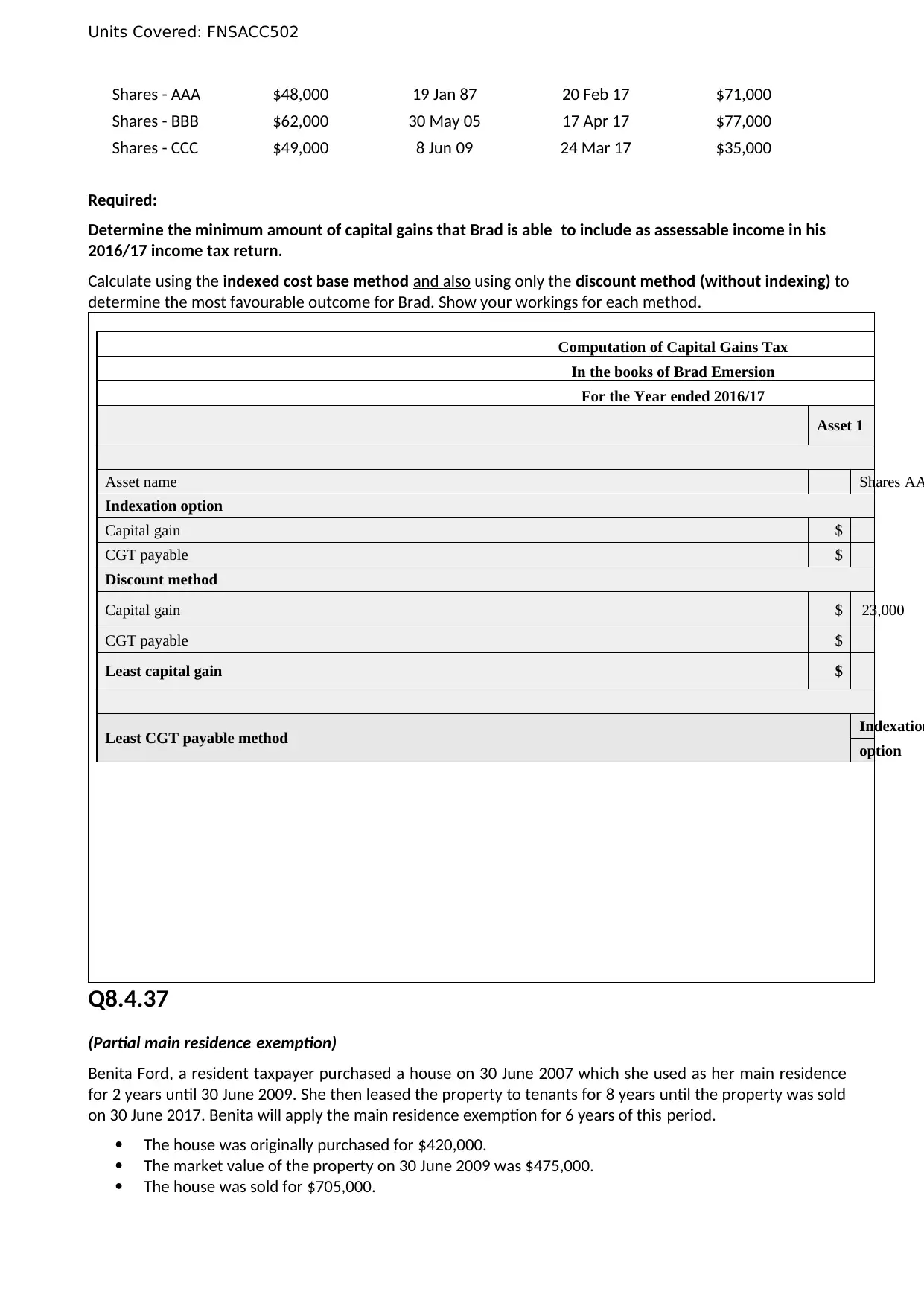

Brad Emerson, a resident taxpayer, sold the following CGT assets during the 2016/17 tax year:

ASSET COST

BASE

ACQUISITION

DATE

DISPOSAL

DATE

SALE

PRICE

Units Covered: FNSACC502

Shares - AAA $48,000 19 Jan 87 20 Feb 17 $71,000

Shares - BBB $62,000 30 May 05 17 Apr 17 $77,000

Shares - CCC $49,000 8 Jun 09 24 Mar 17 $35,000

Required:

Determine the minimum amount of capital gains that Brad is able to include as assessable income in his

2016/17 income tax return.

Calculate using the indexed cost base method and also using only the discount method (without indexing) to

determine the most favourable outcome for Brad. Show your workings for each method.

Computation of Capital Gains Tax

In the books of Brad Emersion

For the Year ended 2016/17

Asset 1

Asset name Shares AA

Indexation option

Capital gain $

CGT payable $

Discount method

Capital gain $ 23,000

CGT payable $

Least capital gain $

Least CGT payable method Indexation

option

Q8.4.37

(Partial main residence exemption)

Benita Ford, a resident taxpayer purchased a house on 30 June 2007 which she used as her main residence

for 2 years until 30 June 2009. She then leased the property to tenants for 8 years until the property was sold

on 30 June 2017. Benita will apply the main residence exemption for 6 years of this period.

The house was originally purchased for $420,000.

The market value of the property on 30 June 2009 was $475,000.

The house was sold for $705,000.

Shares - AAA $48,000 19 Jan 87 20 Feb 17 $71,000

Shares - BBB $62,000 30 May 05 17 Apr 17 $77,000

Shares - CCC $49,000 8 Jun 09 24 Mar 17 $35,000

Required:

Determine the minimum amount of capital gains that Brad is able to include as assessable income in his

2016/17 income tax return.

Calculate using the indexed cost base method and also using only the discount method (without indexing) to

determine the most favourable outcome for Brad. Show your workings for each method.

Computation of Capital Gains Tax

In the books of Brad Emersion

For the Year ended 2016/17

Asset 1

Asset name Shares AA

Indexation option

Capital gain $

CGT payable $

Discount method

Capital gain $ 23,000

CGT payable $

Least capital gain $

Least CGT payable method Indexation

option

Q8.4.37

(Partial main residence exemption)

Benita Ford, a resident taxpayer purchased a house on 30 June 2007 which she used as her main residence

for 2 years until 30 June 2009. She then leased the property to tenants for 8 years until the property was sold

on 30 June 2017. Benita will apply the main residence exemption for 6 years of this period.

The house was originally purchased for $420,000.

The market value of the property on 30 June 2009 was $475,000.

The house was sold for $705,000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Units Covered: FNSACC502

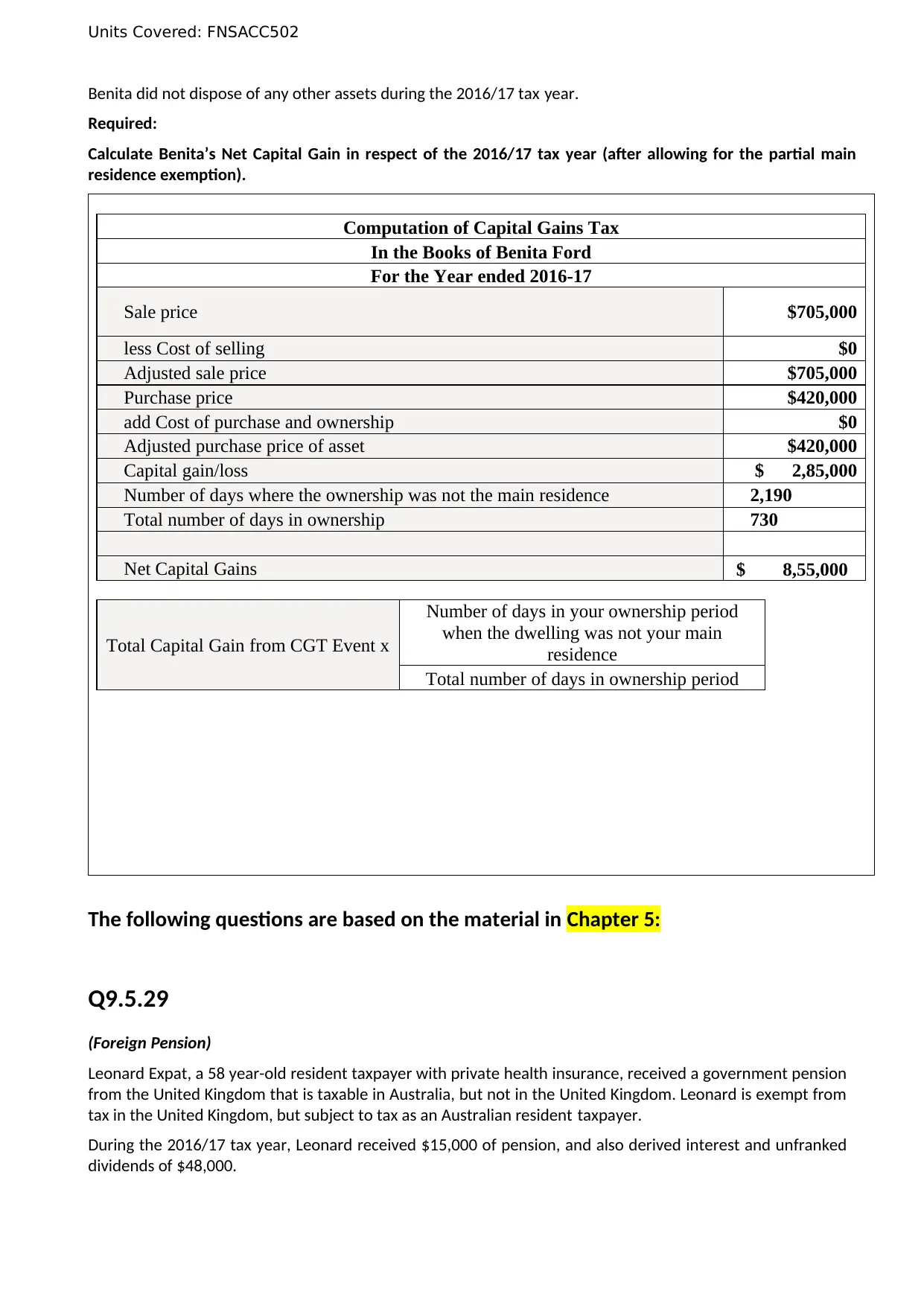

Benita did not dispose of any other assets during the 2016/17 tax year.

Required:

Calculate Benita’s Net Capital Gain in respect of the 2016/17 tax year (after allowing for the partial main

residence exemption).

Computation of Capital Gains Tax

In the Books of Benita Ford

For the Year ended 2016-17

Sale price $705,000

less Cost of selling $0

Adjusted sale price $705,000

Purchase price $420,000

add Cost of purchase and ownership $0

Adjusted purchase price of asset $420,000

Capital gain/loss $ 2,85,000

Number of days where the ownership was not the main residence 2,190

Total number of days in ownership 730

Net Capital Gains $ 8,55,000

Total Capital Gain from CGT Event x

Number of days in your ownership period

when the dwelling was not your main

residence

Total number of days in ownership period

The following questions are based on the material in Chapter 5:

Q9.5.29

(Foreign Pension)

Leonard Expat, a 58 year-old resident taxpayer with private health insurance, received a government pension

from the United Kingdom that is taxable in Australia, but not in the United Kingdom. Leonard is exempt from

tax in the United Kingdom, but subject to tax as an Australian resident taxpayer.

During the 2016/17 tax year, Leonard received $15,000 of pension, and also derived interest and unfranked

dividends of $48,000.

Benita did not dispose of any other assets during the 2016/17 tax year.

Required:

Calculate Benita’s Net Capital Gain in respect of the 2016/17 tax year (after allowing for the partial main

residence exemption).

Computation of Capital Gains Tax

In the Books of Benita Ford

For the Year ended 2016-17

Sale price $705,000

less Cost of selling $0

Adjusted sale price $705,000

Purchase price $420,000

add Cost of purchase and ownership $0

Adjusted purchase price of asset $420,000

Capital gain/loss $ 2,85,000

Number of days where the ownership was not the main residence 2,190

Total number of days in ownership 730

Net Capital Gains $ 8,55,000

Total Capital Gain from CGT Event x

Number of days in your ownership period

when the dwelling was not your main

residence

Total number of days in ownership period

The following questions are based on the material in Chapter 5:

Q9.5.29

(Foreign Pension)

Leonard Expat, a 58 year-old resident taxpayer with private health insurance, received a government pension

from the United Kingdom that is taxable in Australia, but not in the United Kingdom. Leonard is exempt from

tax in the United Kingdom, but subject to tax as an Australian resident taxpayer.

During the 2016/17 tax year, Leonard received $15,000 of pension, and also derived interest and unfranked

dividends of $48,000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC502

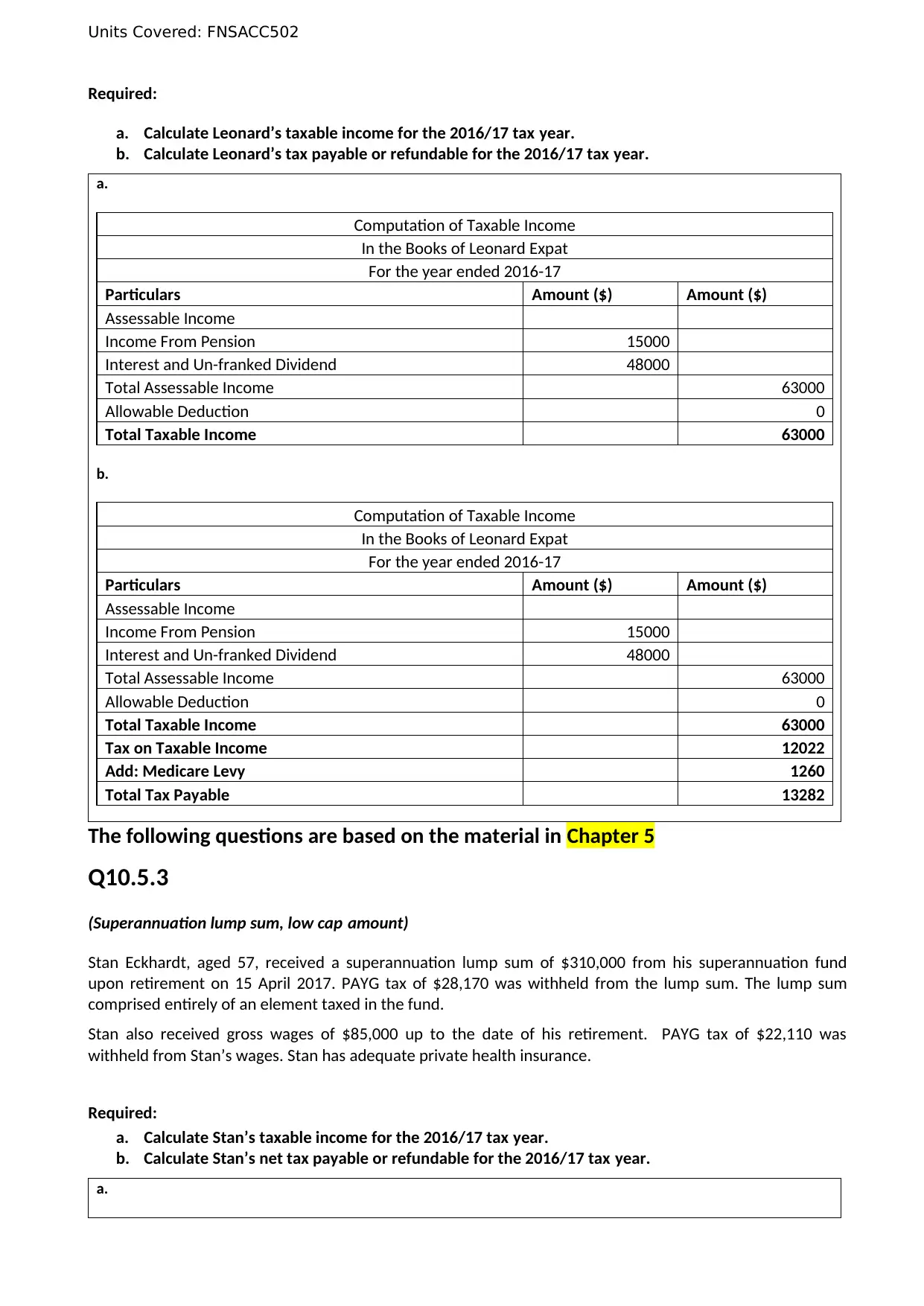

Required:

a. Calculate Leonard’s taxable income for the 2016/17 tax year.

b. Calculate Leonard’s tax payable or refundable for the 2016/17 tax year.

a.

Computation of Taxable Income

In the Books of Leonard Expat

For the year ended 2016-17

Particulars Amount ($) Amount ($)

Assessable Income

Income From Pension 15000

Interest and Un-franked Dividend 48000

Total Assessable Income 63000

Allowable Deduction 0

Total Taxable Income 63000

b.

Computation of Taxable Income

In the Books of Leonard Expat

For the year ended 2016-17

Particulars Amount ($) Amount ($)

Assessable Income

Income From Pension 15000

Interest and Un-franked Dividend 48000

Total Assessable Income 63000

Allowable Deduction 0

Total Taxable Income 63000

Tax on Taxable Income 12022

Add: Medicare Levy 1260

Total Tax Payable 13282

The following questions are based on the material in Chapter 5

Q10.5.3

(Superannuation lump sum, low cap amount)

Stan Eckhardt, aged 57, received a superannuation lump sum of $310,000 from his superannuation fund

upon retirement on 15 April 2017. PAYG tax of $28,170 was withheld from the lump sum. The lump sum

comprised entirely of an element taxed in the fund.

Stan also received gross wages of $85,000 up to the date of his retirement. PAYG tax of $22,110 was

withheld from Stan’s wages. Stan has adequate private health insurance.

Required:

a. Calculate Stan’s taxable income for the 2016/17 tax year.

b. Calculate Stan’s net tax payable or refundable for the 2016/17 tax year.

a.

Required:

a. Calculate Leonard’s taxable income for the 2016/17 tax year.

b. Calculate Leonard’s tax payable or refundable for the 2016/17 tax year.

a.

Computation of Taxable Income

In the Books of Leonard Expat

For the year ended 2016-17

Particulars Amount ($) Amount ($)

Assessable Income

Income From Pension 15000

Interest and Un-franked Dividend 48000

Total Assessable Income 63000

Allowable Deduction 0

Total Taxable Income 63000

b.

Computation of Taxable Income

In the Books of Leonard Expat

For the year ended 2016-17

Particulars Amount ($) Amount ($)

Assessable Income

Income From Pension 15000

Interest and Un-franked Dividend 48000

Total Assessable Income 63000

Allowable Deduction 0

Total Taxable Income 63000

Tax on Taxable Income 12022

Add: Medicare Levy 1260

Total Tax Payable 13282

The following questions are based on the material in Chapter 5

Q10.5.3

(Superannuation lump sum, low cap amount)

Stan Eckhardt, aged 57, received a superannuation lump sum of $310,000 from his superannuation fund

upon retirement on 15 April 2017. PAYG tax of $28,170 was withheld from the lump sum. The lump sum

comprised entirely of an element taxed in the fund.

Stan also received gross wages of $85,000 up to the date of his retirement. PAYG tax of $22,110 was

withheld from Stan’s wages. Stan has adequate private health insurance.

Required:

a. Calculate Stan’s taxable income for the 2016/17 tax year.

b. Calculate Stan’s net tax payable or refundable for the 2016/17 tax year.

a.

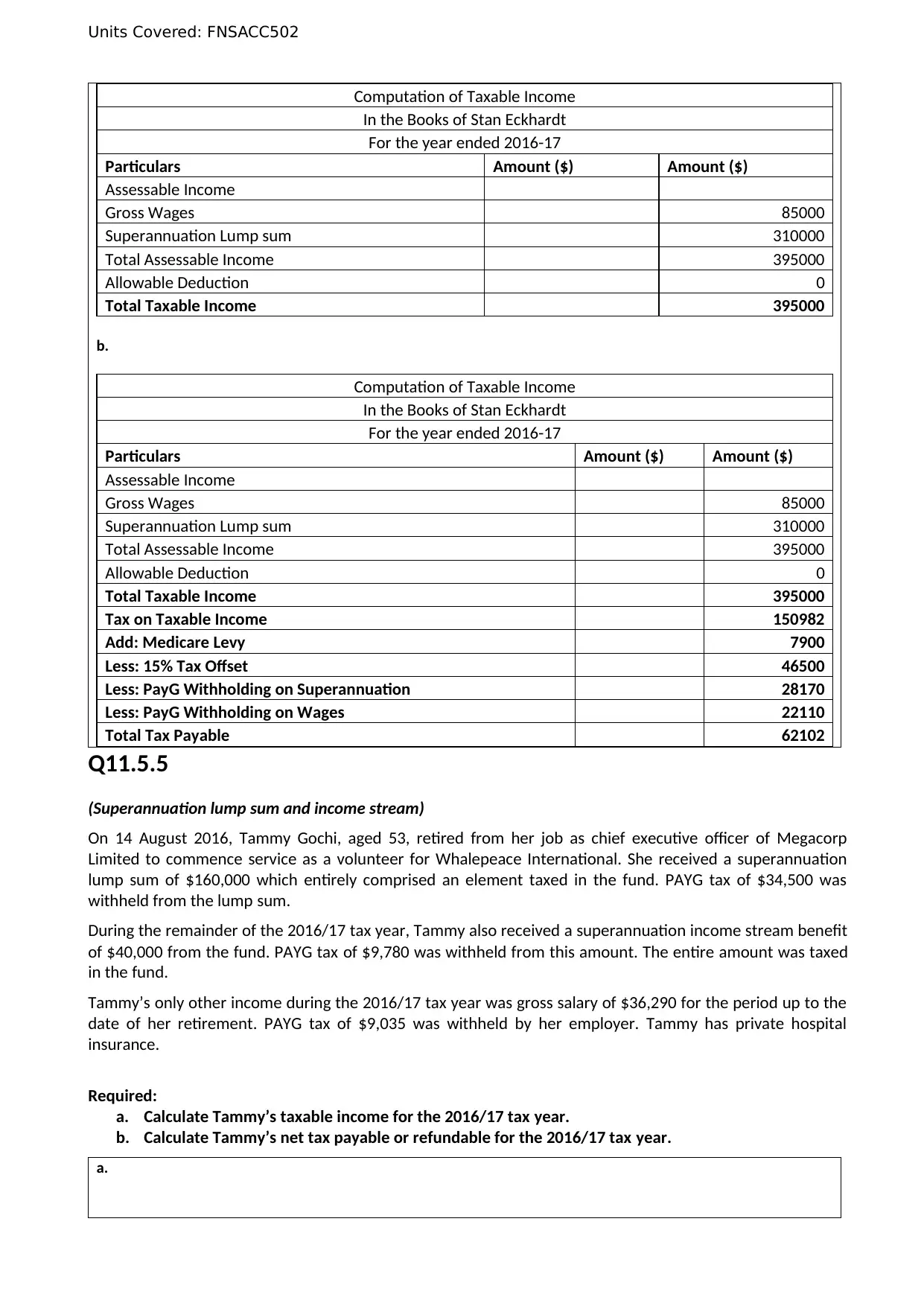

Units Covered: FNSACC502

Computation of Taxable Income

In the Books of Stan Eckhardt

For the year ended 2016-17

Particulars Amount ($) Amount ($)

Assessable Income

Gross Wages 85000

Superannuation Lump sum 310000

Total Assessable Income 395000

Allowable Deduction 0

Total Taxable Income 395000

b.

Computation of Taxable Income

In the Books of Stan Eckhardt

For the year ended 2016-17

Particulars Amount ($) Amount ($)

Assessable Income

Gross Wages 85000

Superannuation Lump sum 310000

Total Assessable Income 395000

Allowable Deduction 0

Total Taxable Income 395000

Tax on Taxable Income 150982

Add: Medicare Levy 7900

Less: 15% Tax Offset 46500

Less: PayG Withholding on Superannuation 28170

Less: PayG Withholding on Wages 22110

Total Tax Payable 62102

Q11.5.5

(Superannuation lump sum and income stream)

On 14 August 2016, Tammy Gochi, aged 53, retired from her job as chief executive officer of Megacorp

Limited to commence service as a volunteer for Whalepeace International. She received a superannuation

lump sum of $160,000 which entirely comprised an element taxed in the fund. PAYG tax of $34,500 was

withheld from the lump sum.

During the remainder of the 2016/17 tax year, Tammy also received a superannuation income stream benefit

of $40,000 from the fund. PAYG tax of $9,780 was withheld from this amount. The entire amount was taxed

in the fund.

Tammy’s only other income during the 2016/17 tax year was gross salary of $36,290 for the period up to the

date of her retirement. PAYG tax of $9,035 was withheld by her employer. Tammy has private hospital

insurance.

Required:

a. Calculate Tammy’s taxable income for the 2016/17 tax year.

b. Calculate Tammy’s net tax payable or refundable for the 2016/17 tax year.

a.

Computation of Taxable Income

In the Books of Stan Eckhardt

For the year ended 2016-17

Particulars Amount ($) Amount ($)

Assessable Income

Gross Wages 85000

Superannuation Lump sum 310000

Total Assessable Income 395000

Allowable Deduction 0

Total Taxable Income 395000

b.

Computation of Taxable Income

In the Books of Stan Eckhardt

For the year ended 2016-17

Particulars Amount ($) Amount ($)

Assessable Income

Gross Wages 85000

Superannuation Lump sum 310000

Total Assessable Income 395000

Allowable Deduction 0

Total Taxable Income 395000

Tax on Taxable Income 150982

Add: Medicare Levy 7900

Less: 15% Tax Offset 46500

Less: PayG Withholding on Superannuation 28170

Less: PayG Withholding on Wages 22110

Total Tax Payable 62102

Q11.5.5

(Superannuation lump sum and income stream)

On 14 August 2016, Tammy Gochi, aged 53, retired from her job as chief executive officer of Megacorp

Limited to commence service as a volunteer for Whalepeace International. She received a superannuation

lump sum of $160,000 which entirely comprised an element taxed in the fund. PAYG tax of $34,500 was

withheld from the lump sum.

During the remainder of the 2016/17 tax year, Tammy also received a superannuation income stream benefit

of $40,000 from the fund. PAYG tax of $9,780 was withheld from this amount. The entire amount was taxed

in the fund.

Tammy’s only other income during the 2016/17 tax year was gross salary of $36,290 for the period up to the

date of her retirement. PAYG tax of $9,035 was withheld by her employer. Tammy has private hospital

insurance.

Required:

a. Calculate Tammy’s taxable income for the 2016/17 tax year.

b. Calculate Tammy’s net tax payable or refundable for the 2016/17 tax year.

a.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 31

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.