FNSACC507 - Sydney Metro College: Management Accounting Assignment

VerifiedAdded on 2023/06/04

|26

|2345

|357

Homework Assignment

AI Summary

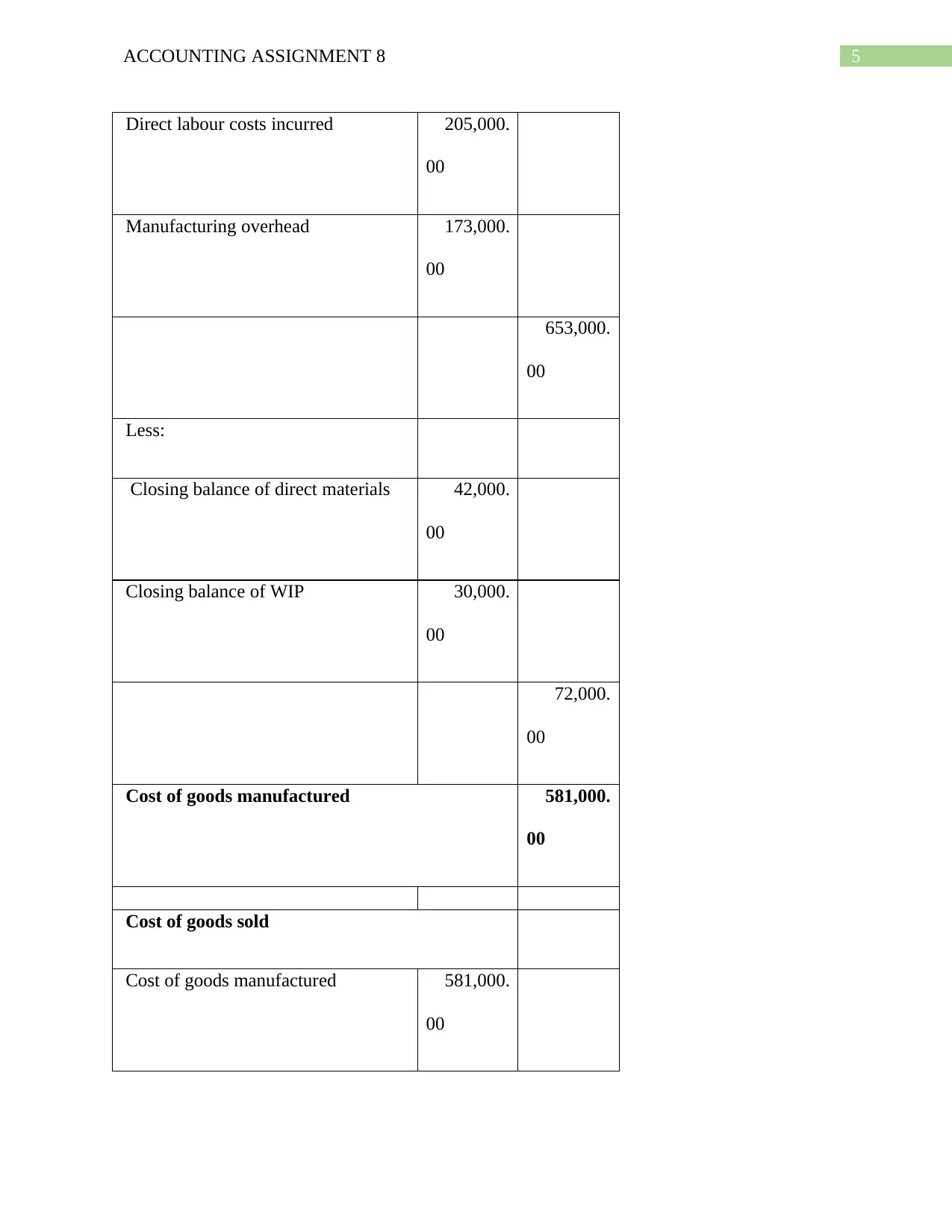

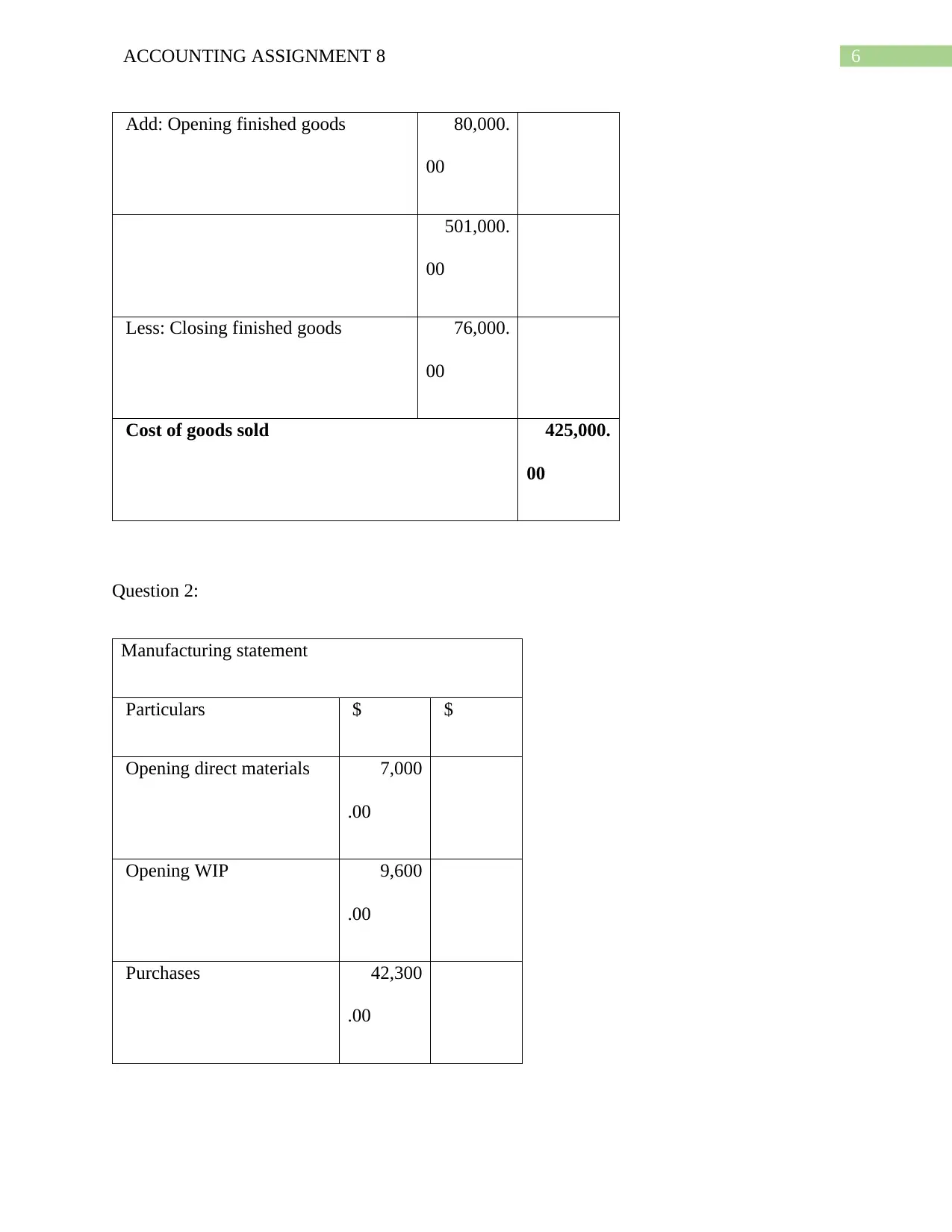

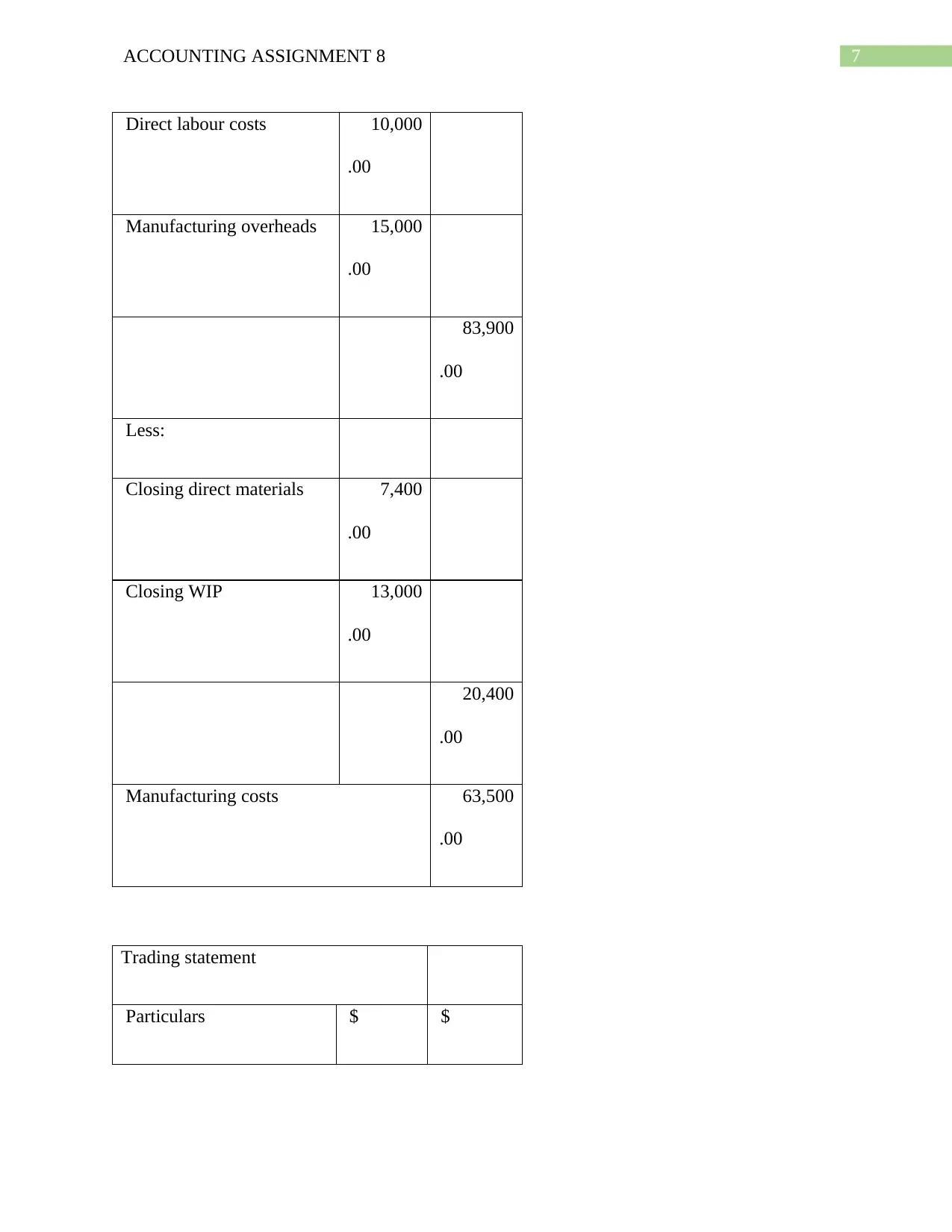

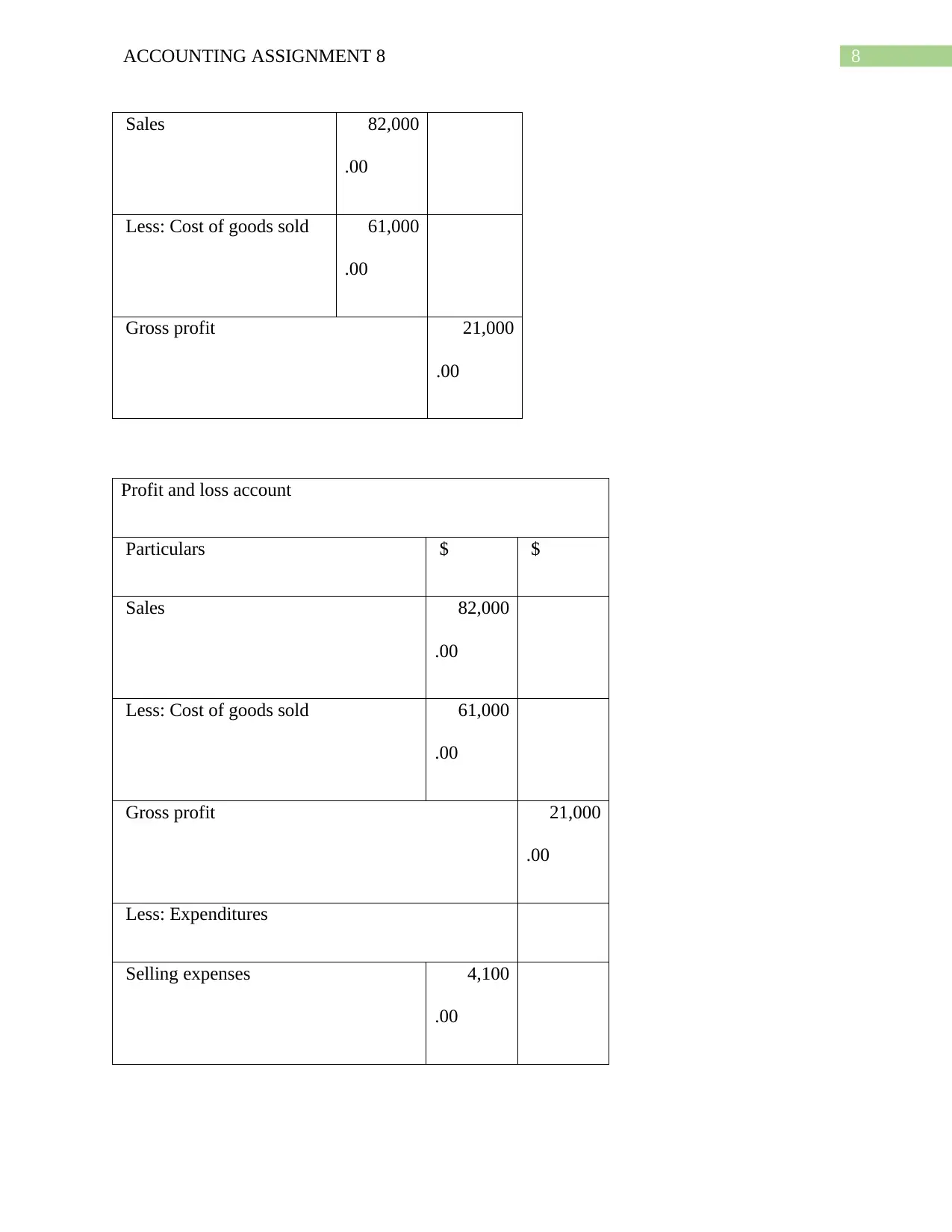

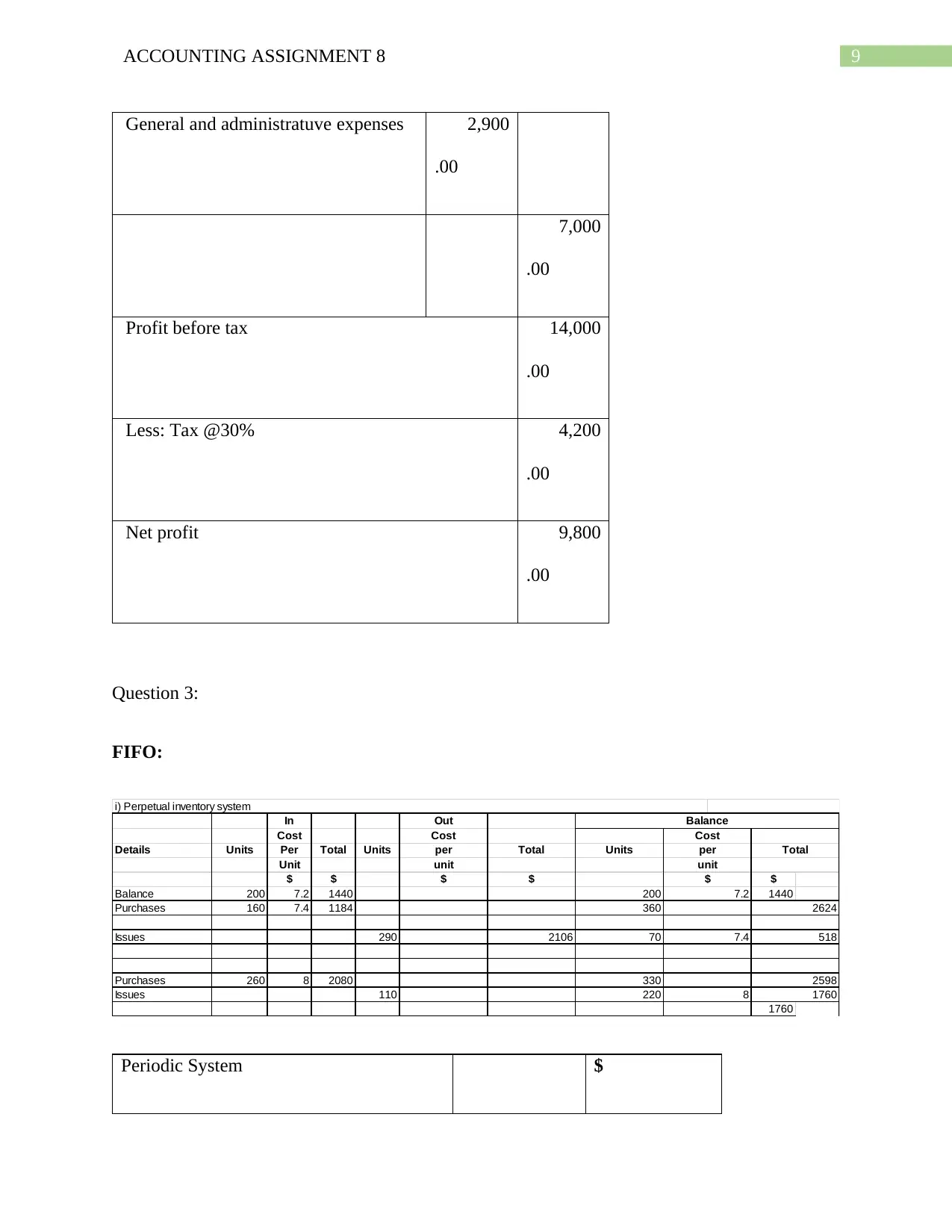

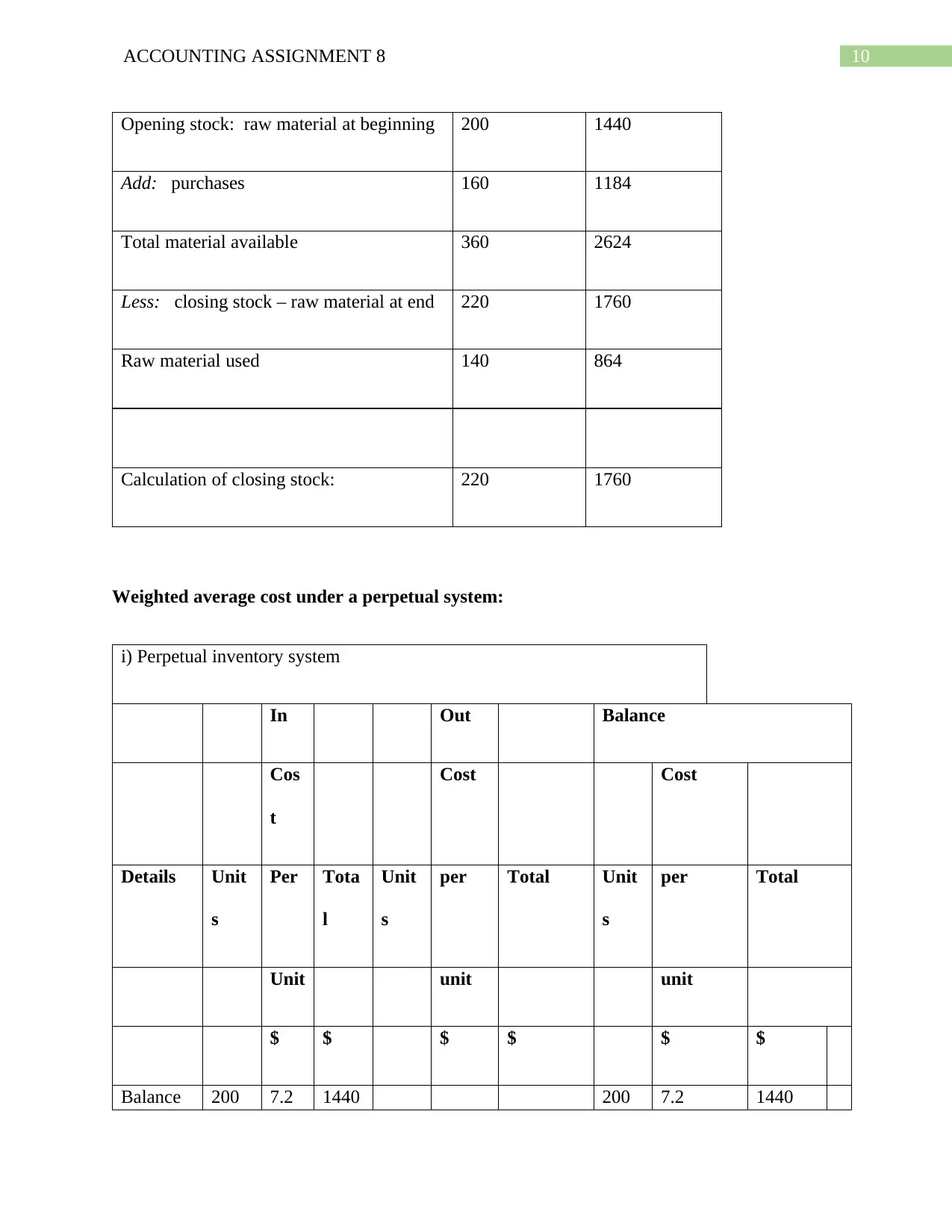

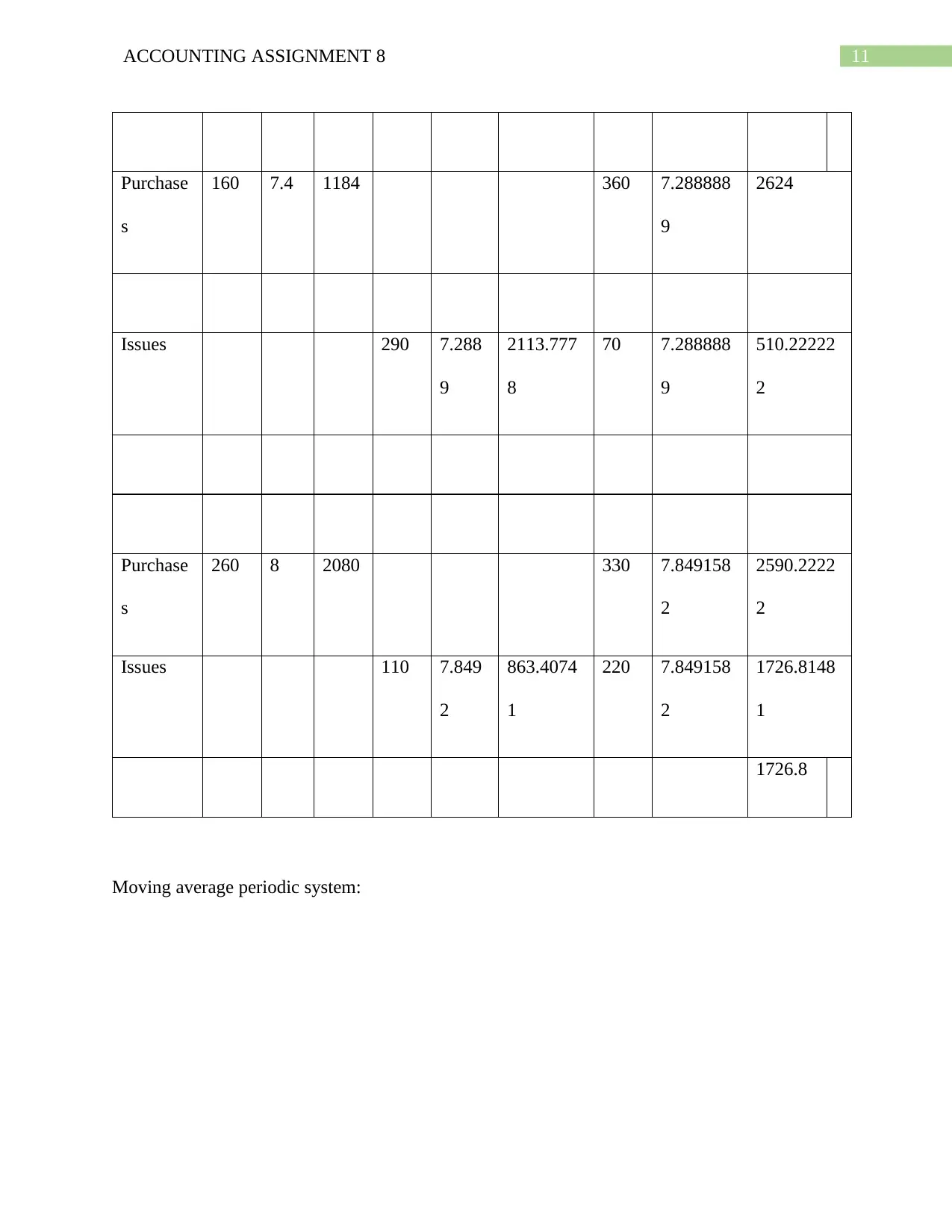

This assignment solution covers various aspects of management accounting, including cost accounting systems, manufacturing statements, inventory valuation methods (FIFO and weighted average), journal entries, variance analysis, budgeting, and break-even point calculations. It addresses tasks such as calculating the cost of goods manufactured and sold, preparing manufacturing and trading statements, analyzing variances in expenditures, and determining break-even points for sales and production. The document also includes practical applications with numerical examples and journal entries to demonstrate accounting principles and techniques relevant to manufacturing and service industries.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.