FNSACC507 - Management Accounting Information: A Detailed Analysis

VerifiedAdded on 2023/06/12

|12

|2834

|120

Case Study

AI Summary

This case study solution provides a comprehensive analysis of management accounting information, covering topics such as cost data gathering, budget preparation, variance analysis, and factory overhead allocation. It includes detailed calculations of revenue and expense variances, an analysis of controllable and non-controllable variances, and journal entries for material issues and purchase returns. The solution also addresses the calculation of factory overhead recovery rates and provides short answers to questions related to accounting principles, legislation, and performance analysis. Furthermore, it contains written activities that discuss budgetary control, financial data recording, the relationship between variance analysis and costing system integrity, and budget preparation principles. Desklib offers this document to aid students in their studies, alongside a wealth of other solved assignments and study resources.

Case study 4.2

Task 1

Management could gather cost data by identification and establishment of the system for

gathering operating data. This data can be recorded by using a systematically coded data. Such

data should be classified appropriately as per policies of the organization and must be accurate

and reliable.

Budget preparer could get cost data for the budget from all sections of the organization by asking

for cost information advice. In addition to gathering, cost data budget preparer should use the

proper structure for preparation of budgets.

Task 2

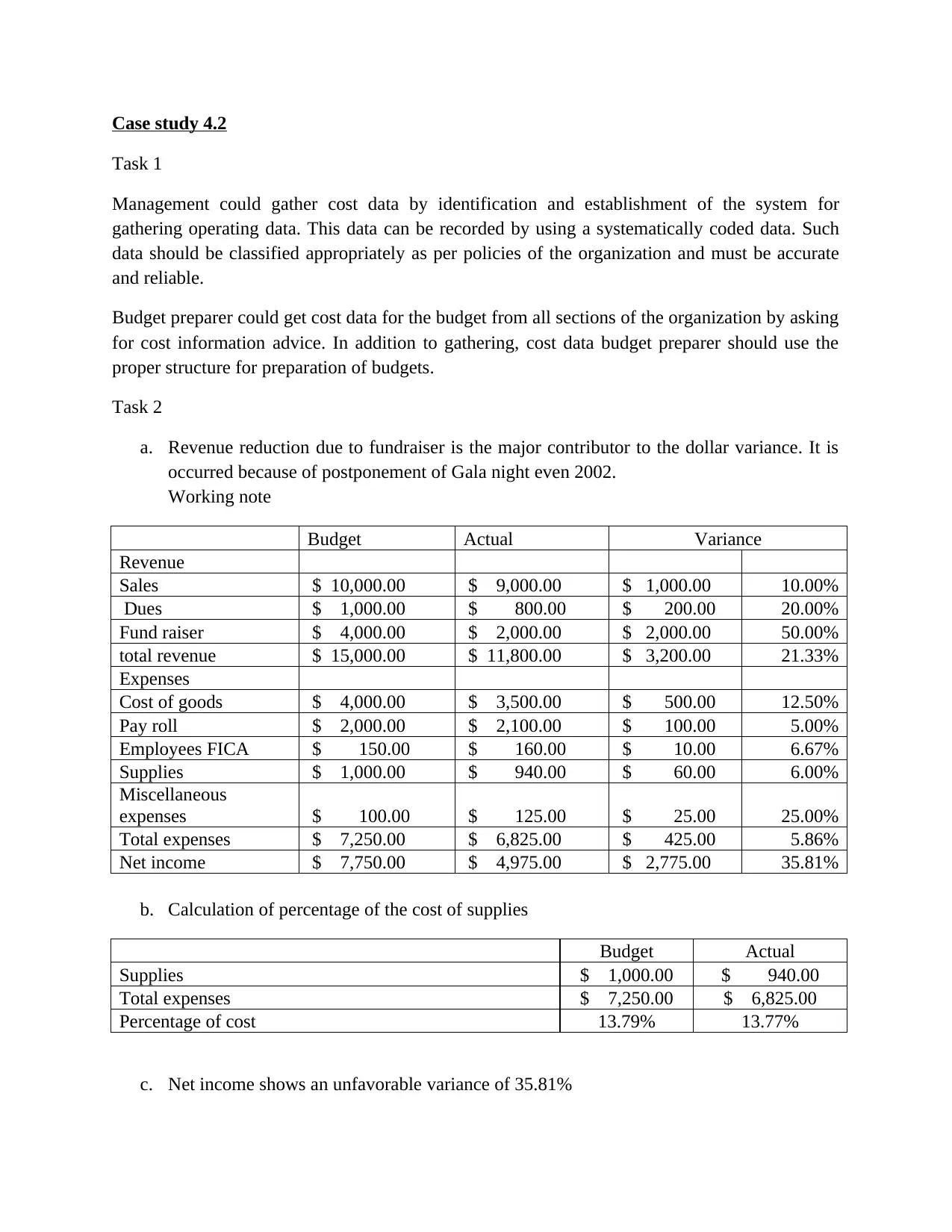

a. Revenue reduction due to fundraiser is the major contributor to the dollar variance. It is

occurred because of postponement of Gala night even 2002.

Working note

Budget Actual Variance

Revenue

Sales $ 10,000.00 $ 9,000.00 $ 1,000.00 10.00%

Dues $ 1,000.00 $ 800.00 $ 200.00 20.00%

Fund raiser $ 4,000.00 $ 2,000.00 $ 2,000.00 50.00%

total revenue $ 15,000.00 $ 11,800.00 $ 3,200.00 21.33%

Expenses

Cost of goods $ 4,000.00 $ 3,500.00 $ 500.00 12.50%

Pay roll $ 2,000.00 $ 2,100.00 $ 100.00 5.00%

Employees FICA $ 150.00 $ 160.00 $ 10.00 6.67%

Supplies $ 1,000.00 $ 940.00 $ 60.00 6.00%

Miscellaneous

expenses $ 100.00 $ 125.00 $ 25.00 25.00%

Total expenses $ 7,250.00 $ 6,825.00 $ 425.00 5.86%

Net income $ 7,750.00 $ 4,975.00 $ 2,775.00 35.81%

b. Calculation of percentage of the cost of supplies

Budget Actual

Supplies $ 1,000.00 $ 940.00

Total expenses $ 7,250.00 $ 6,825.00

Percentage of cost 13.79% 13.77%

c. Net income shows an unfavorable variance of 35.81%

Task 1

Management could gather cost data by identification and establishment of the system for

gathering operating data. This data can be recorded by using a systematically coded data. Such

data should be classified appropriately as per policies of the organization and must be accurate

and reliable.

Budget preparer could get cost data for the budget from all sections of the organization by asking

for cost information advice. In addition to gathering, cost data budget preparer should use the

proper structure for preparation of budgets.

Task 2

a. Revenue reduction due to fundraiser is the major contributor to the dollar variance. It is

occurred because of postponement of Gala night even 2002.

Working note

Budget Actual Variance

Revenue

Sales $ 10,000.00 $ 9,000.00 $ 1,000.00 10.00%

Dues $ 1,000.00 $ 800.00 $ 200.00 20.00%

Fund raiser $ 4,000.00 $ 2,000.00 $ 2,000.00 50.00%

total revenue $ 15,000.00 $ 11,800.00 $ 3,200.00 21.33%

Expenses

Cost of goods $ 4,000.00 $ 3,500.00 $ 500.00 12.50%

Pay roll $ 2,000.00 $ 2,100.00 $ 100.00 5.00%

Employees FICA $ 150.00 $ 160.00 $ 10.00 6.67%

Supplies $ 1,000.00 $ 940.00 $ 60.00 6.00%

Miscellaneous

expenses $ 100.00 $ 125.00 $ 25.00 25.00%

Total expenses $ 7,250.00 $ 6,825.00 $ 425.00 5.86%

Net income $ 7,750.00 $ 4,975.00 $ 2,775.00 35.81%

b. Calculation of percentage of the cost of supplies

Budget Actual

Supplies $ 1,000.00 $ 940.00

Total expenses $ 7,250.00 $ 6,825.00

Percentage of cost 13.79% 13.77%

c. Net income shows an unfavorable variance of 35.81%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

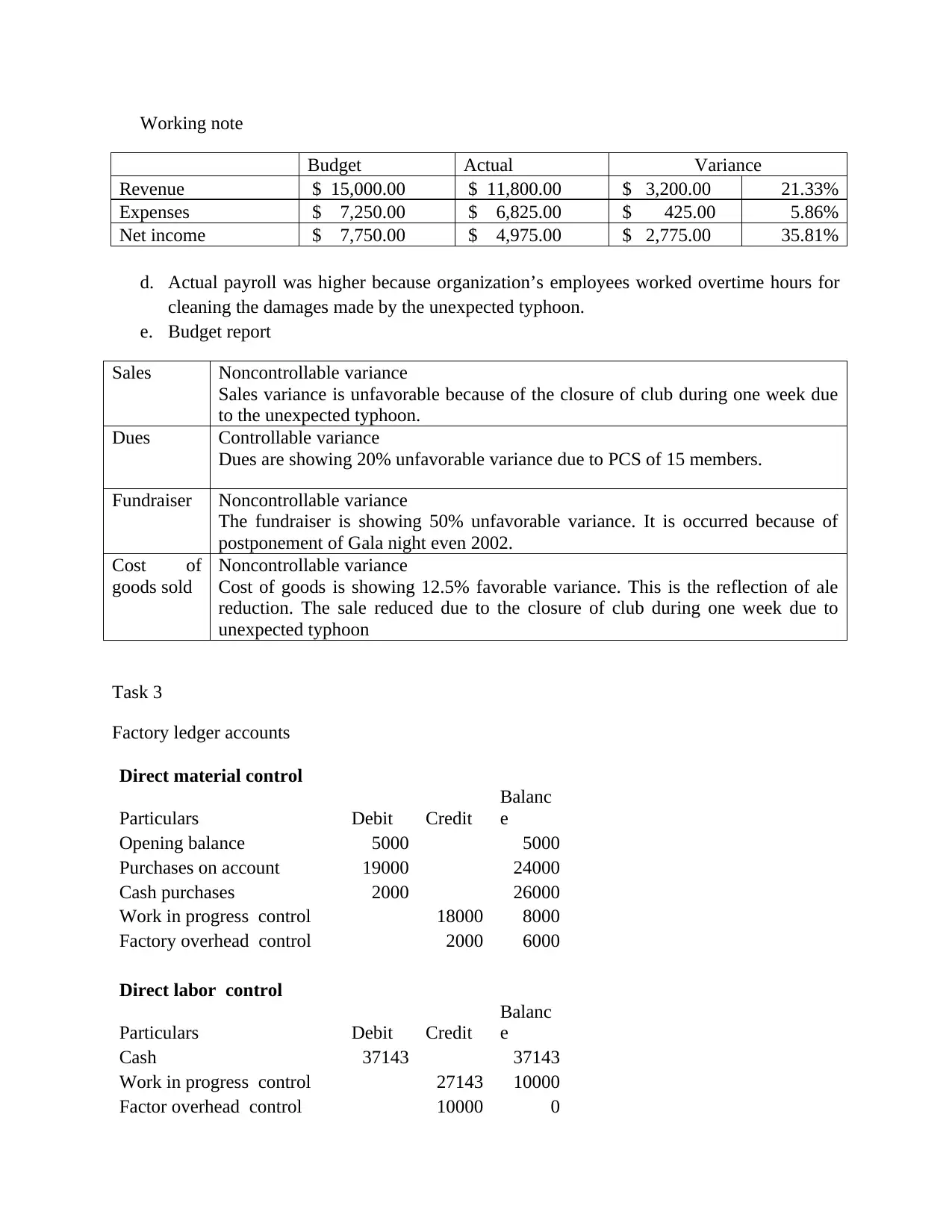

Working note

Budget Actual Variance

Revenue $ 15,000.00 $ 11,800.00 $ 3,200.00 21.33%

Expenses $ 7,250.00 $ 6,825.00 $ 425.00 5.86%

Net income $ 7,750.00 $ 4,975.00 $ 2,775.00 35.81%

d. Actual payroll was higher because organization’s employees worked overtime hours for

cleaning the damages made by the unexpected typhoon.

e. Budget report

Sales Noncontrollable variance

Sales variance is unfavorable because of the closure of club during one week due

to the unexpected typhoon.

Dues Controllable variance

Dues are showing 20% unfavorable variance due to PCS of 15 members.

Fundraiser Noncontrollable variance

The fundraiser is showing 50% unfavorable variance. It is occurred because of

postponement of Gala night even 2002.

Cost of

goods sold

Noncontrollable variance

Cost of goods is showing 12.5% favorable variance. This is the reflection of ale

reduction. The sale reduced due to the closure of club during one week due to

unexpected typhoon

Task 3

Factory ledger accounts

Direct material control

Particulars Debit Credit

Balanc

e

Opening balance 5000 5000

Purchases on account 19000 24000

Cash purchases 2000 26000

Work in progress control 18000 8000

Factory overhead control 2000 6000

Direct labor control

Particulars Debit Credit

Balanc

e

Cash 37143 37143

Work in progress control 27143 10000

Factor overhead control 10000 0

Budget Actual Variance

Revenue $ 15,000.00 $ 11,800.00 $ 3,200.00 21.33%

Expenses $ 7,250.00 $ 6,825.00 $ 425.00 5.86%

Net income $ 7,750.00 $ 4,975.00 $ 2,775.00 35.81%

d. Actual payroll was higher because organization’s employees worked overtime hours for

cleaning the damages made by the unexpected typhoon.

e. Budget report

Sales Noncontrollable variance

Sales variance is unfavorable because of the closure of club during one week due

to the unexpected typhoon.

Dues Controllable variance

Dues are showing 20% unfavorable variance due to PCS of 15 members.

Fundraiser Noncontrollable variance

The fundraiser is showing 50% unfavorable variance. It is occurred because of

postponement of Gala night even 2002.

Cost of

goods sold

Noncontrollable variance

Cost of goods is showing 12.5% favorable variance. This is the reflection of ale

reduction. The sale reduced due to the closure of club during one week due to

unexpected typhoon

Task 3

Factory ledger accounts

Direct material control

Particulars Debit Credit

Balanc

e

Opening balance 5000 5000

Purchases on account 19000 24000

Cash purchases 2000 26000

Work in progress control 18000 8000

Factory overhead control 2000 6000

Direct labor control

Particulars Debit Credit

Balanc

e

Cash 37143 37143

Work in progress control 27143 10000

Factor overhead control 10000 0

Factory overhead control

Particulars Debit Credit

Balanc

e

Direct material control 2000 2000

Direct labor control 10000 12000

Depreciation 3600 15600

Insurance 600 16200

Rent 2800 19000

Work in progress control 19000 0

Work in progress control

Particulars Debit Credit

Balanc

e

Opening balance 15200 15200

Direct material control 18000 33200

Direct labor control 27143 60343

Factory overhead control 19000 79343

Finished goods control 62000 17343

Abnormal loss 6143 11200

Finished goods control

Particulars Debit Credit

Balanc

e

Opening balance 15000 15000

Work in progress control 62000 77000

Cost of goods sold 68000 9000

Manufacturing statement

Direct materials used 18000

Direct manufacturing labor 27143

Manufacturing overhead costs:

Indirect manufacturing labor 10000

Indirect material 2000

Depreciation - plant 3600

Factory insurance 600

Factory rent 2800

Total Manufacturing overhead costs 19000

Manufacturing costs incurring during the month 64143

Beginning work-in-progress inventory 15200

Particulars Debit Credit

Balanc

e

Direct material control 2000 2000

Direct labor control 10000 12000

Depreciation 3600 15600

Insurance 600 16200

Rent 2800 19000

Work in progress control 19000 0

Work in progress control

Particulars Debit Credit

Balanc

e

Opening balance 15200 15200

Direct material control 18000 33200

Direct labor control 27143 60343

Factory overhead control 19000 79343

Finished goods control 62000 17343

Abnormal loss 6143 11200

Finished goods control

Particulars Debit Credit

Balanc

e

Opening balance 15000 15000

Work in progress control 62000 77000

Cost of goods sold 68000 9000

Manufacturing statement

Direct materials used 18000

Direct manufacturing labor 27143

Manufacturing overhead costs:

Indirect manufacturing labor 10000

Indirect material 2000

Depreciation - plant 3600

Factory insurance 600

Factory rent 2800

Total Manufacturing overhead costs 19000

Manufacturing costs incurring during the month 64143

Beginning work-in-progress inventory 15200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

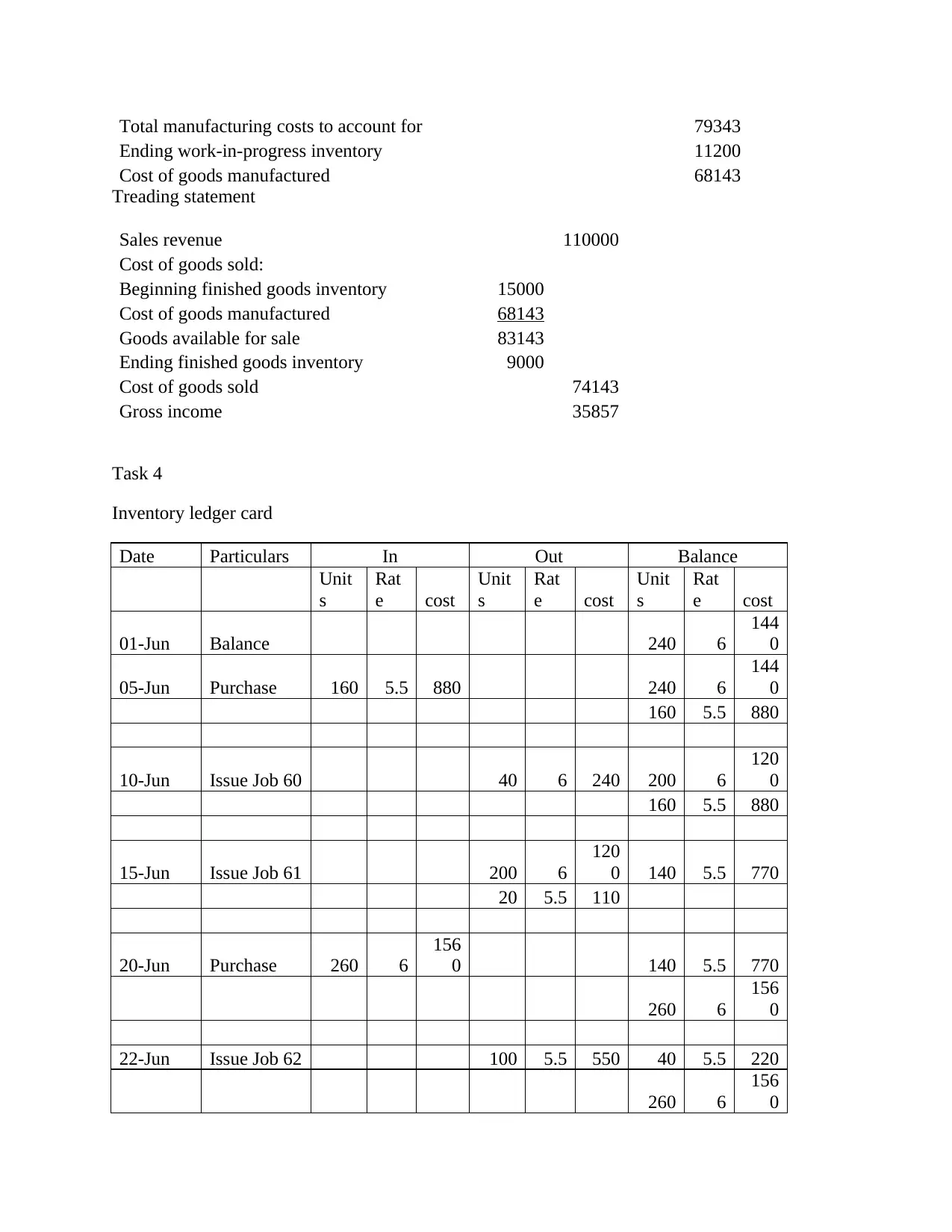

Total manufacturing costs to account for 79343

Ending work-in-progress inventory 11200

Cost of goods manufactured 68143

Treading statement

Sales revenue 110000

Cost of goods sold:

Beginning finished goods inventory 15000

Cost of goods manufactured 68143

Goods available for sale 83143

Ending finished goods inventory 9000

Cost of goods sold 74143

Gross income 35857

Task 4

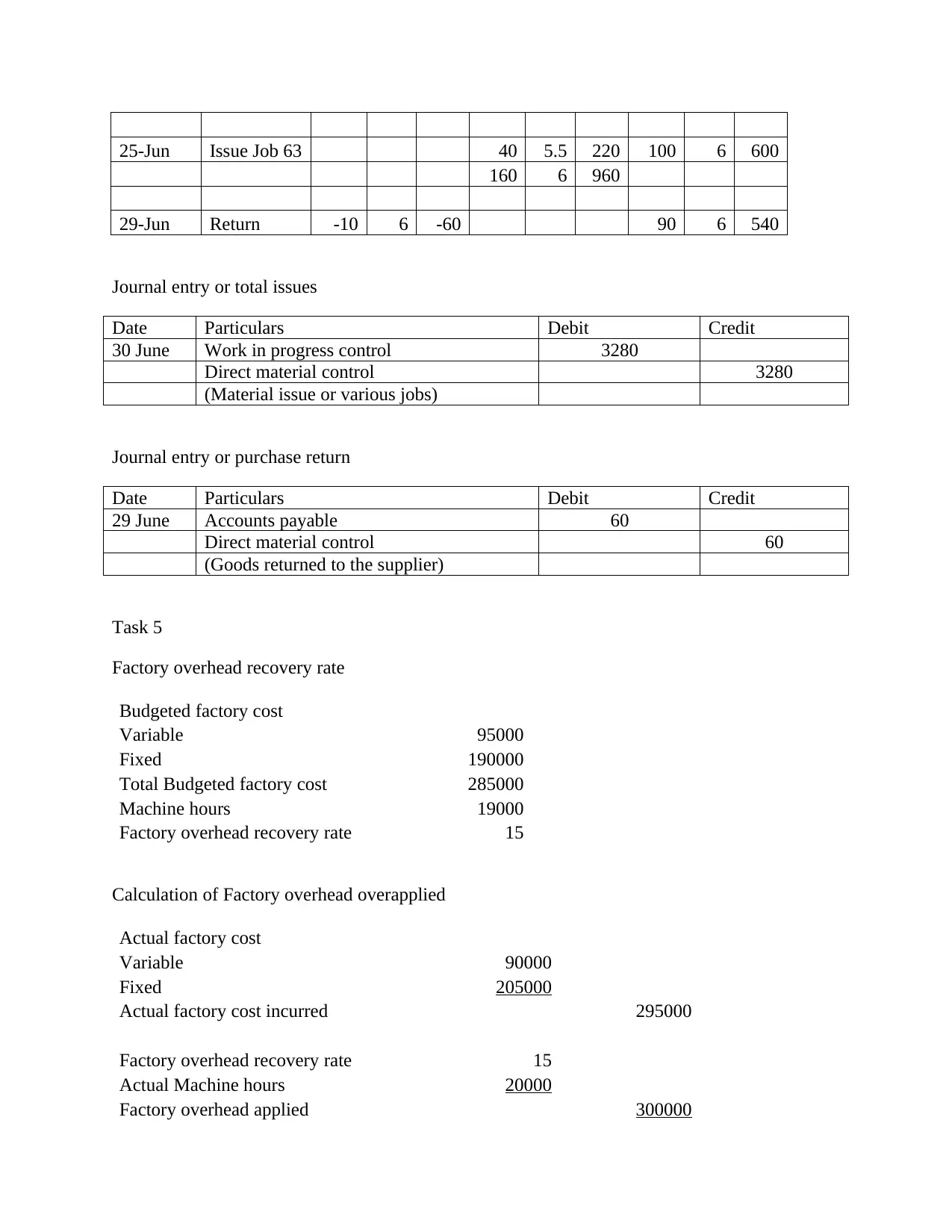

Inventory ledger card

Date Particulars In Out Balance

Unit

s

Rat

e cost

Unit

s

Rat

e cost

Unit

s

Rat

e cost

01-Jun Balance 240 6

144

0

05-Jun Purchase 160 5.5 880 240 6

144

0

160 5.5 880

10-Jun Issue Job 60 40 6 240 200 6

120

0

160 5.5 880

15-Jun Issue Job 61 200 6

120

0 140 5.5 770

20 5.5 110

20-Jun Purchase 260 6

156

0 140 5.5 770

260 6

156

0

22-Jun Issue Job 62 100 5.5 550 40 5.5 220

260 6

156

0

Ending work-in-progress inventory 11200

Cost of goods manufactured 68143

Treading statement

Sales revenue 110000

Cost of goods sold:

Beginning finished goods inventory 15000

Cost of goods manufactured 68143

Goods available for sale 83143

Ending finished goods inventory 9000

Cost of goods sold 74143

Gross income 35857

Task 4

Inventory ledger card

Date Particulars In Out Balance

Unit

s

Rat

e cost

Unit

s

Rat

e cost

Unit

s

Rat

e cost

01-Jun Balance 240 6

144

0

05-Jun Purchase 160 5.5 880 240 6

144

0

160 5.5 880

10-Jun Issue Job 60 40 6 240 200 6

120

0

160 5.5 880

15-Jun Issue Job 61 200 6

120

0 140 5.5 770

20 5.5 110

20-Jun Purchase 260 6

156

0 140 5.5 770

260 6

156

0

22-Jun Issue Job 62 100 5.5 550 40 5.5 220

260 6

156

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25-Jun Issue Job 63 40 5.5 220 100 6 600

160 6 960

29-Jun Return -10 6 -60 90 6 540

Journal entry or total issues

Date Particulars Debit Credit

30 June Work in progress control 3280

Direct material control 3280

(Material issue or various jobs)

Journal entry or purchase return

Date Particulars Debit Credit

29 June Accounts payable 60

Direct material control 60

(Goods returned to the supplier)

Task 5

Factory overhead recovery rate

Budgeted factory cost

Variable 95000

Fixed 190000

Total Budgeted factory cost 285000

Machine hours 19000

Factory overhead recovery rate 15

Calculation of Factory overhead overapplied

Actual factory cost

Variable 90000

Fixed 205000

Actual factory cost incurred 295000

Factory overhead recovery rate 15

Actual Machine hours 20000

Factory overhead applied 300000

160 6 960

29-Jun Return -10 6 -60 90 6 540

Journal entry or total issues

Date Particulars Debit Credit

30 June Work in progress control 3280

Direct material control 3280

(Material issue or various jobs)

Journal entry or purchase return

Date Particulars Debit Credit

29 June Accounts payable 60

Direct material control 60

(Goods returned to the supplier)

Task 5

Factory overhead recovery rate

Budgeted factory cost

Variable 95000

Fixed 190000

Total Budgeted factory cost 285000

Machine hours 19000

Factory overhead recovery rate 15

Calculation of Factory overhead overapplied

Actual factory cost

Variable 90000

Fixed 205000

Actual factory cost incurred 295000

Factory overhead recovery rate 15

Actual Machine hours 20000

Factory overhead applied 300000

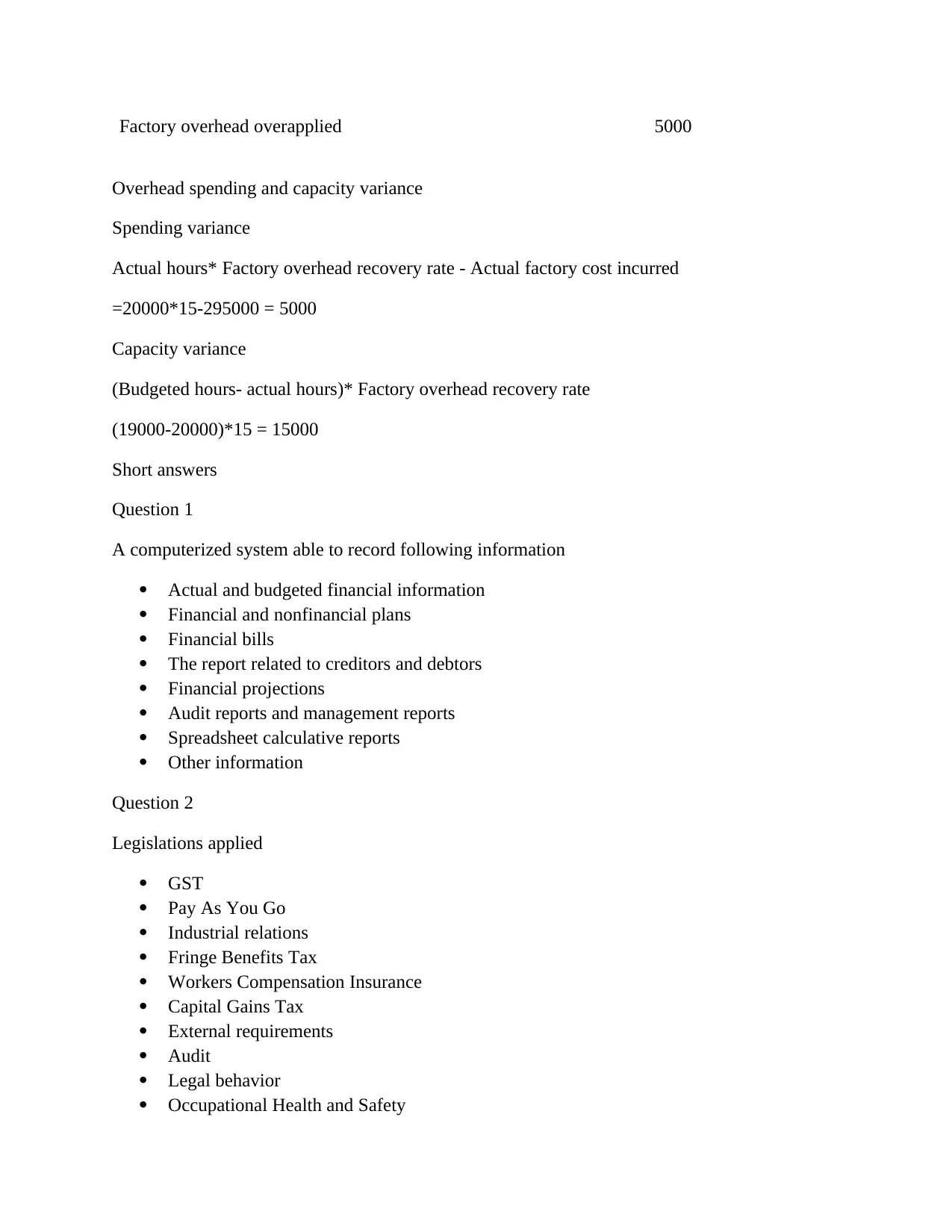

Factory overhead overapplied 5000

Overhead spending and capacity variance

Spending variance

Actual hours* Factory overhead recovery rate - Actual factory cost incurred

=20000*15-295000 = 5000

Capacity variance

(Budgeted hours- actual hours)* Factory overhead recovery rate

(19000-20000)*15 = 15000

Short answers

Question 1

A computerized system able to record following information

Actual and budgeted financial information

Financial and nonfinancial plans

Financial bills

The report related to creditors and debtors

Financial projections

Audit reports and management reports

Spreadsheet calculative reports

Other information

Question 2

Legislations applied

GST

Pay As You Go

Industrial relations

Fringe Benefits Tax

Workers Compensation Insurance

Capital Gains Tax

External requirements

Audit

Legal behavior

Occupational Health and Safety

Overhead spending and capacity variance

Spending variance

Actual hours* Factory overhead recovery rate - Actual factory cost incurred

=20000*15-295000 = 5000

Capacity variance

(Budgeted hours- actual hours)* Factory overhead recovery rate

(19000-20000)*15 = 15000

Short answers

Question 1

A computerized system able to record following information

Actual and budgeted financial information

Financial and nonfinancial plans

Financial bills

The report related to creditors and debtors

Financial projections

Audit reports and management reports

Spreadsheet calculative reports

Other information

Question 2

Legislations applied

GST

Pay As You Go

Industrial relations

Fringe Benefits Tax

Workers Compensation Insurance

Capital Gains Tax

External requirements

Audit

Legal behavior

Occupational Health and Safety

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

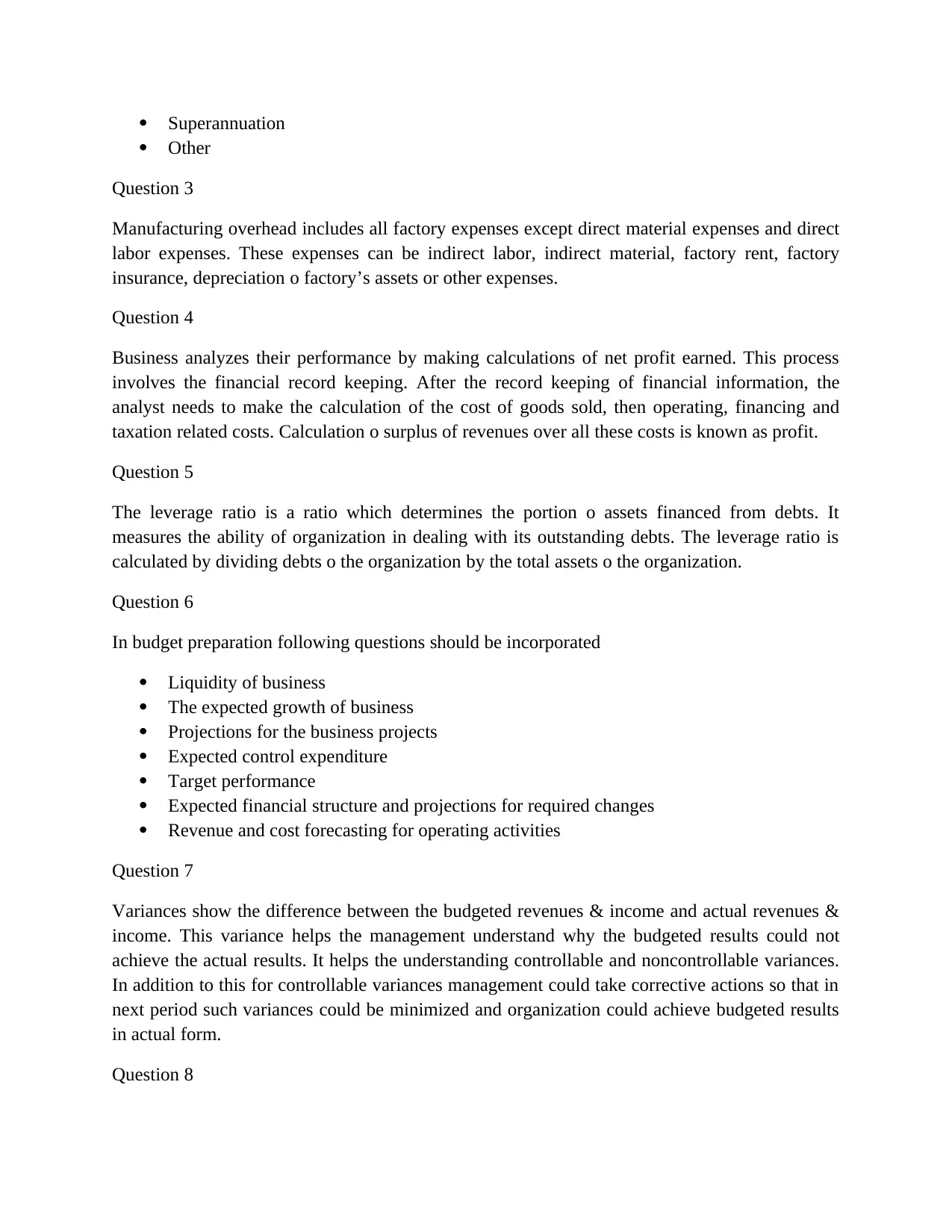

Superannuation

Other

Question 3

Manufacturing overhead includes all factory expenses except direct material expenses and direct

labor expenses. These expenses can be indirect labor, indirect material, factory rent, factory

insurance, depreciation o factory’s assets or other expenses.

Question 4

Business analyzes their performance by making calculations of net profit earned. This process

involves the financial record keeping. After the record keeping of financial information, the

analyst needs to make the calculation of the cost of goods sold, then operating, financing and

taxation related costs. Calculation o surplus of revenues over all these costs is known as profit.

Question 5

The leverage ratio is a ratio which determines the portion o assets financed from debts. It

measures the ability of organization in dealing with its outstanding debts. The leverage ratio is

calculated by dividing debts o the organization by the total assets o the organization.

Question 6

In budget preparation following questions should be incorporated

Liquidity of business

The expected growth of business

Projections for the business projects

Expected control expenditure

Target performance

Expected financial structure and projections for required changes

Revenue and cost forecasting for operating activities

Question 7

Variances show the difference between the budgeted revenues & income and actual revenues &

income. This variance helps the management understand why the budgeted results could not

achieve the actual results. It helps the understanding controllable and noncontrollable variances.

In addition to this for controllable variances management could take corrective actions so that in

next period such variances could be minimized and organization could achieve budgeted results

in actual form.

Question 8

Other

Question 3

Manufacturing overhead includes all factory expenses except direct material expenses and direct

labor expenses. These expenses can be indirect labor, indirect material, factory rent, factory

insurance, depreciation o factory’s assets or other expenses.

Question 4

Business analyzes their performance by making calculations of net profit earned. This process

involves the financial record keeping. After the record keeping of financial information, the

analyst needs to make the calculation of the cost of goods sold, then operating, financing and

taxation related costs. Calculation o surplus of revenues over all these costs is known as profit.

Question 5

The leverage ratio is a ratio which determines the portion o assets financed from debts. It

measures the ability of organization in dealing with its outstanding debts. The leverage ratio is

calculated by dividing debts o the organization by the total assets o the organization.

Question 6

In budget preparation following questions should be incorporated

Liquidity of business

The expected growth of business

Projections for the business projects

Expected control expenditure

Target performance

Expected financial structure and projections for required changes

Revenue and cost forecasting for operating activities

Question 7

Variances show the difference between the budgeted revenues & income and actual revenues &

income. This variance helps the management understand why the budgeted results could not

achieve the actual results. It helps the understanding controllable and noncontrollable variances.

In addition to this for controllable variances management could take corrective actions so that in

next period such variances could be minimized and organization could achieve budgeted results

in actual form.

Question 8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

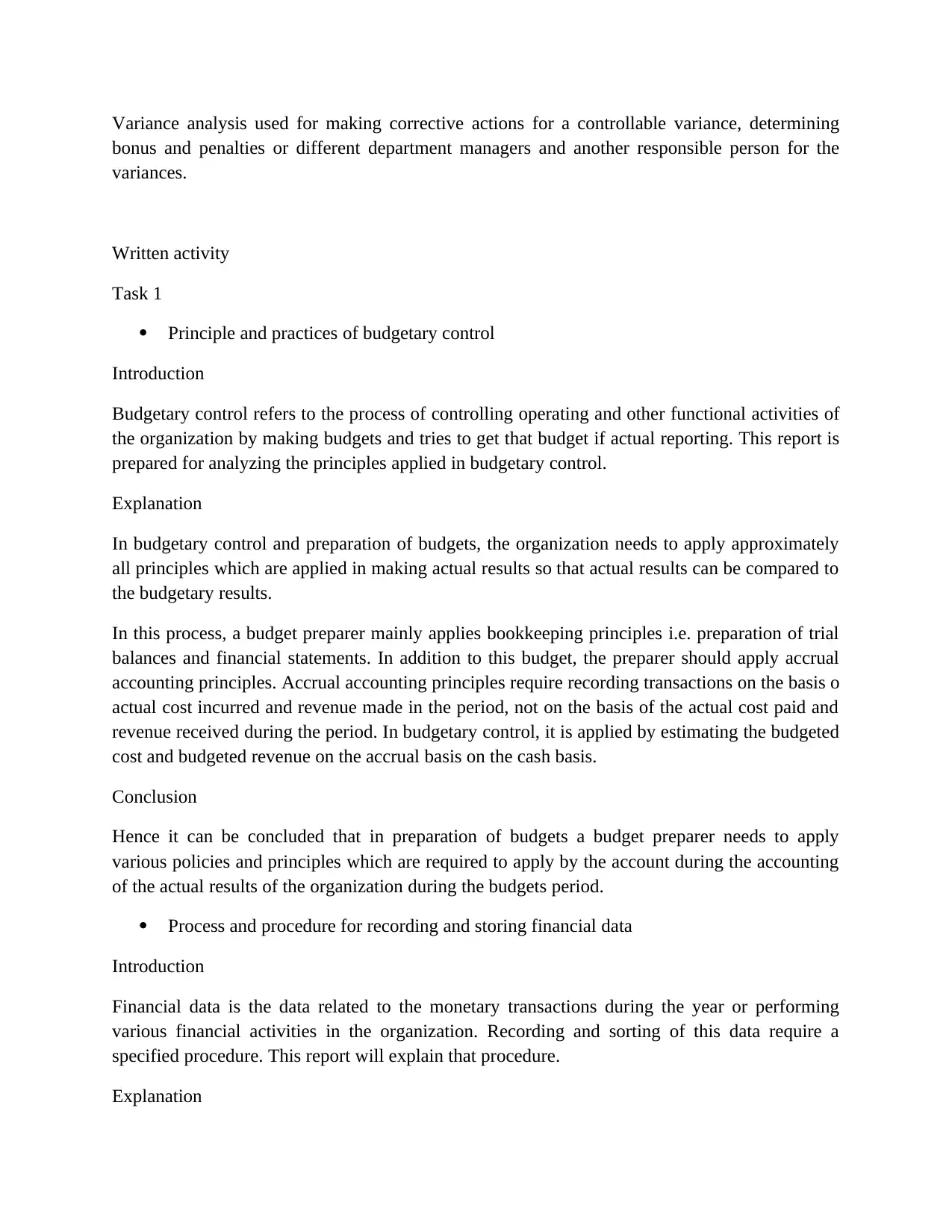

Variance analysis used for making corrective actions for a controllable variance, determining

bonus and penalties or different department managers and another responsible person for the

variances.

Written activity

Task 1

Principle and practices of budgetary control

Introduction

Budgetary control refers to the process of controlling operating and other functional activities of

the organization by making budgets and tries to get that budget if actual reporting. This report is

prepared for analyzing the principles applied in budgetary control.

Explanation

In budgetary control and preparation of budgets, the organization needs to apply approximately

all principles which are applied in making actual results so that actual results can be compared to

the budgetary results.

In this process, a budget preparer mainly applies bookkeeping principles i.e. preparation of trial

balances and financial statements. In addition to this budget, the preparer should apply accrual

accounting principles. Accrual accounting principles require recording transactions on the basis o

actual cost incurred and revenue made in the period, not on the basis of the actual cost paid and

revenue received during the period. In budgetary control, it is applied by estimating the budgeted

cost and budgeted revenue on the accrual basis on the cash basis.

Conclusion

Hence it can be concluded that in preparation of budgets a budget preparer needs to apply

various policies and principles which are required to apply by the account during the accounting

of the actual results of the organization during the budgets period.

Process and procedure for recording and storing financial data

Introduction

Financial data is the data related to the monetary transactions during the year or performing

various financial activities in the organization. Recording and sorting of this data require a

specified procedure. This report will explain that procedure.

Explanation

bonus and penalties or different department managers and another responsible person for the

variances.

Written activity

Task 1

Principle and practices of budgetary control

Introduction

Budgetary control refers to the process of controlling operating and other functional activities of

the organization by making budgets and tries to get that budget if actual reporting. This report is

prepared for analyzing the principles applied in budgetary control.

Explanation

In budgetary control and preparation of budgets, the organization needs to apply approximately

all principles which are applied in making actual results so that actual results can be compared to

the budgetary results.

In this process, a budget preparer mainly applies bookkeeping principles i.e. preparation of trial

balances and financial statements. In addition to this budget, the preparer should apply accrual

accounting principles. Accrual accounting principles require recording transactions on the basis o

actual cost incurred and revenue made in the period, not on the basis of the actual cost paid and

revenue received during the period. In budgetary control, it is applied by estimating the budgeted

cost and budgeted revenue on the accrual basis on the cash basis.

Conclusion

Hence it can be concluded that in preparation of budgets a budget preparer needs to apply

various policies and principles which are required to apply by the account during the accounting

of the actual results of the organization during the budgets period.

Process and procedure for recording and storing financial data

Introduction

Financial data is the data related to the monetary transactions during the year or performing

various financial activities in the organization. Recording and sorting of this data require a

specified procedure. This report will explain that procedure.

Explanation

Financial data needs to record by the bookkeeper in the form of journal entries. Journal entries

are the primary recording of the financial data. These journal entries posted to the various ledger

accounts. In ledger accounts, various journal entries regarding each transaction sorted for

calculation of closing accounts balances. Ater the ledger accounts a bookkeeper needs to prepare

trial balance for checking arithmetic accuracy and recording adjusting entries. The adjusted

account balance from the trial balance transferred to the financial statements for estimating the

financial position and performance.

Conclusion

The above discussion concludes that financial transactions record in journal entries and ledger

accounts. On the other hand, these are sorted in the trial balance, statements of financial position

and statement of financial performance.

The relationship between variance analysis and costing system integrity

Introduction

The integrity of the system defines the function performed in such a manner so that such

performed by without impairing them and degraded the standard of that system. The variance

analysis is an analysis defined the cost required to be controlled. Variance analysis is related to

the costs system integrity.

Explanation

Variances show the difference between the budgeted revenues & income and actual revenues &

income. This variance helps the management understand why the budgeted results could not

achieve the actual results. It helps the understanding controllable and noncontrollable variances.

In addition to this for controllable variances management could take corrective actions so that in

next period such variances could be minimized and organization could achieve budgeted results

in actual form.

Variance analysis used for making corrective actions for a controllable variance, determining

bonus and penalties or different department managers and another responsible person for the

variances.

Cost system integrity means that costing function performance should be in a manner so that

such costing data should not impair and degraded the costing standards. Variance analysis helps

to active this integrity of the costing system.

Conclusion

Hence it can be concluded that variance analysis is related to the costs system integrity. In

addition to this variance analysis controlled the degradation of the costing data.

are the primary recording of the financial data. These journal entries posted to the various ledger

accounts. In ledger accounts, various journal entries regarding each transaction sorted for

calculation of closing accounts balances. Ater the ledger accounts a bookkeeper needs to prepare

trial balance for checking arithmetic accuracy and recording adjusting entries. The adjusted

account balance from the trial balance transferred to the financial statements for estimating the

financial position and performance.

Conclusion

The above discussion concludes that financial transactions record in journal entries and ledger

accounts. On the other hand, these are sorted in the trial balance, statements of financial position

and statement of financial performance.

The relationship between variance analysis and costing system integrity

Introduction

The integrity of the system defines the function performed in such a manner so that such

performed by without impairing them and degraded the standard of that system. The variance

analysis is an analysis defined the cost required to be controlled. Variance analysis is related to

the costs system integrity.

Explanation

Variances show the difference between the budgeted revenues & income and actual revenues &

income. This variance helps the management understand why the budgeted results could not

achieve the actual results. It helps the understanding controllable and noncontrollable variances.

In addition to this for controllable variances management could take corrective actions so that in

next period such variances could be minimized and organization could achieve budgeted results

in actual form.

Variance analysis used for making corrective actions for a controllable variance, determining

bonus and penalties or different department managers and another responsible person for the

variances.

Cost system integrity means that costing function performance should be in a manner so that

such costing data should not impair and degraded the costing standards. Variance analysis helps

to active this integrity of the costing system.

Conclusion

Hence it can be concluded that variance analysis is related to the costs system integrity. In

addition to this variance analysis controlled the degradation of the costing data.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Principles and practices of the budget preparation

Introduction

Budgetary control refers to the process of controlling operating and other functional activities of

the organization by making budgets and tries to get that budget if actual reporting. This report is

prepared for analyzing the principles applied in budgetary control.

Explanation

In budgetary control and preparation of budgets, the organization needs to apply approximately

all principles which are applied in making actual results so that actual results can be compared to

the budgetary results.

In this process, a budget preparer mainly applies bookkeeping principles i.e. preparation of trial

balances and financial statements. In addition to this budget, the preparer should apply accrual

accounting principles. Accrual accounting principles require recording transactions on the basis o

actual cost incurred and revenue made in the period, not on the basis of the actual cost paid and

revenue received during the period. In budgetary control, it is applied by estimating the budgeted

cost and budgeted revenue on the accrual basis on the cash basis.

In addition to this, some other acts which need to consider during budget preparation are,

Timeline budget drafting

The format of each budget

Users of such budget

The responsible person for budget preparation

Conclusion

Hence it can be concluded that in preparation of budgets a budget preparer needs to apply

various policies and principles which are required to apply by the account during the accounting

of the actual results of the organization during the budgets period.

Key management information requirements

Introduction

Key management refers to the top management of the organization. Key management takes

various crucial decisions for the organization on the basis of information provided to them. The

information provides to the key management is very important. This discussion will explain the

requirements needs to adhere to the information provided to key management.

Explanation

The information provided to key management needs to adhere following requirements,

Introduction

Budgetary control refers to the process of controlling operating and other functional activities of

the organization by making budgets and tries to get that budget if actual reporting. This report is

prepared for analyzing the principles applied in budgetary control.

Explanation

In budgetary control and preparation of budgets, the organization needs to apply approximately

all principles which are applied in making actual results so that actual results can be compared to

the budgetary results.

In this process, a budget preparer mainly applies bookkeeping principles i.e. preparation of trial

balances and financial statements. In addition to this budget, the preparer should apply accrual

accounting principles. Accrual accounting principles require recording transactions on the basis o

actual cost incurred and revenue made in the period, not on the basis of the actual cost paid and

revenue received during the period. In budgetary control, it is applied by estimating the budgeted

cost and budgeted revenue on the accrual basis on the cash basis.

In addition to this, some other acts which need to consider during budget preparation are,

Timeline budget drafting

The format of each budget

Users of such budget

The responsible person for budget preparation

Conclusion

Hence it can be concluded that in preparation of budgets a budget preparer needs to apply

various policies and principles which are required to apply by the account during the accounting

of the actual results of the organization during the budgets period.

Key management information requirements

Introduction

Key management refers to the top management of the organization. Key management takes

various crucial decisions for the organization on the basis of information provided to them. The

information provides to the key management is very important. This discussion will explain the

requirements needs to adhere to the information provided to key management.

Explanation

The information provided to key management needs to adhere following requirements,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Complete: The information provided to the key management should be complete and should not

escape any relevant act regarding the performance and position of the organization.

Relevant: Key management personnel has various tasks related to the organization. Hence

information provides to them must be relevant for the purposes they asked for. It should not

include irrelevant information far away from the purpose o the information required.

Timely: The information is relevant for a specific time the lapse o that time information becomes

irrelevant or the decision-making purposes. Hence information provided to the key management

should be provided to them timely.

Accurate: Accurate is the crucial aspect of information. If key management provides with a

timely, complete and relevant information but not accurate information the results from decision

making may go in wrong directions. Hence the information should be accurate.

Key features of organizational policies and procedures as they apply to costing system

Costing data recording and processing requires various stapes that starts with data collections,

continues with data input, data processing and ends with making output. The policies and

procedures need to adhere the internal control policies so that costing system could generate air

output. Somme policies which can apply to costing system are followed,

a. Input controls: The costing system should have some input controls. These controls

should ensure the accuracy, completeness, relevance, and validity of the input provided to

the costing system.

b. Processing control: The costing system should have some process controls. These

controls should ensure the accuracy, and validity of the process performed for the costing

system.

c. Output control: The costing system should have some output controls. These controls

should ensure the format, reports, and content of the output provided to the costing

system.

Costing behavior patterns for the different cost elements of a product or service

In the costing system are three types of costs i.e. fixed costs, variable costs and mixed costs.

Fixed costs are the costs that remain same at each level of output this cost cannot change by the

change of the level of output. Per unit fixed costs goes reduce for per unit of output increased.

Variable costs are the costs that do not remain same at each level of output this cost change by

the change of the level of output. Per unit variable costs remain same for per unit of output

increased or decreased. Mixed costs are the costs which have features of each cost type i.e. fixed

as well as variable.

escape any relevant act regarding the performance and position of the organization.

Relevant: Key management personnel has various tasks related to the organization. Hence

information provides to them must be relevant for the purposes they asked for. It should not

include irrelevant information far away from the purpose o the information required.

Timely: The information is relevant for a specific time the lapse o that time information becomes

irrelevant or the decision-making purposes. Hence information provided to the key management

should be provided to them timely.

Accurate: Accurate is the crucial aspect of information. If key management provides with a

timely, complete and relevant information but not accurate information the results from decision

making may go in wrong directions. Hence the information should be accurate.

Key features of organizational policies and procedures as they apply to costing system

Costing data recording and processing requires various stapes that starts with data collections,

continues with data input, data processing and ends with making output. The policies and

procedures need to adhere the internal control policies so that costing system could generate air

output. Somme policies which can apply to costing system are followed,

a. Input controls: The costing system should have some input controls. These controls

should ensure the accuracy, completeness, relevance, and validity of the input provided to

the costing system.

b. Processing control: The costing system should have some process controls. These

controls should ensure the accuracy, and validity of the process performed for the costing

system.

c. Output control: The costing system should have some output controls. These controls

should ensure the format, reports, and content of the output provided to the costing

system.

Costing behavior patterns for the different cost elements of a product or service

In the costing system are three types of costs i.e. fixed costs, variable costs and mixed costs.

Fixed costs are the costs that remain same at each level of output this cost cannot change by the

change of the level of output. Per unit fixed costs goes reduce for per unit of output increased.

Variable costs are the costs that do not remain same at each level of output this cost change by

the change of the level of output. Per unit variable costs remain same for per unit of output

increased or decreased. Mixed costs are the costs which have features of each cost type i.e. fixed

as well as variable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.