Provide Management Accounting Information: Assessment Workbook W

VerifiedAdded on 2020/04/21

|44

|8213

|100

Homework Assignment

AI Summary

This assessment workbook addresses the unit of competency FNSACC507, focusing on providing management accounting information. The workbook includes a variety of questions and exercises covering key concepts such as the three main functions of management, differences in cost accounting systems between manufacturing and service organizations, the distinction between cost and cost drivers, and the calculation of costs and markups. It also delves into the management and safeguarding of inventory and materials, including system procedures for storage, purchasing, and stock issuance. The assessment includes written questions, exercises, and a case study designed to test the student's understanding of these concepts and their ability to apply them to real-world scenarios. The workbook provides detailed solutions and calculations related to financial statements and inventory management. The student demonstrates an understanding of cost accounting principles, financial analysis, and inventory management practices.

Provide Management Accounting Information

This course is based on the nationally recognised unit of competency:

● FNSACC507 Provide Management Accounting Information

It covers the skills and knowledge required to prepare, document and

manage budgets and forecasts, and encompasses forecasting estimates

and monitoring budgeted outcomes.

ASSESSMENT WORKBOOK

Participant Name:

Learner ID/Username:

This course is based on the nationally recognised unit of competency:

● FNSACC507 Provide Management Accounting Information

It covers the skills and knowledge required to prepare, document and

manage budgets and forecasts, and encompasses forecasting estimates

and monitoring budgeted outcomes.

ASSESSMENT WORKBOOK

Participant Name:

Learner ID/Username:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Workbook W: Provide Management Accounting Information

Assessment Workbook W

Provide Management Accounting Information

V1.0

Produced 1 February 2016

Copyright © 2016

All rights reserved. No part of this publication maybe reproduced or distributed in any form or by

any means, or stored in a database or retrieval system other than pursuant to the terms of the

Copyright Act 1968 (Commonwealth).

Date Summary of Modifications

Made

Version

1/02/16 Version 1 produced following

assessment validation

V1.0

Page 1

Assessment Workbook W

Provide Management Accounting Information

V1.0

Produced 1 February 2016

Copyright © 2016

All rights reserved. No part of this publication maybe reproduced or distributed in any form or by

any means, or stored in a database or retrieval system other than pursuant to the terms of the

Copyright Act 1968 (Commonwealth).

Date Summary of Modifications

Made

Version

1/02/16 Version 1 produced following

assessment validation

V1.0

Page 1

Assessment Workbook W: Provide Management Accounting Information

Page 2

Page 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assessment Workbook W: Provide Management Accounting Information

Getting Started

Instructions

There is one (1) workbook for this unit and it contains one (1) assessment

made up of:

● Written Questions – A set of generic questions testing the student’s

general knowledge and understanding of the general theory behind

the unit.

● Exercises - A set of exercises to test the student’s knowledge,

analytical skills in problem solving and performing numerical

calculations.

● Case Study – A hypothetical exercise to test the student’s knowledge,

analytical skills in problem solving and performing numerical

calculations.

The following questions are divided into the following categories.

The first part of the assessment covers generic underpinning knowledge of

tax law and concepts. These questions are all in a short answer format. The

longer questions requiring creative thought processes are covered in the

second part of the assessment and the case study and involve the

calculation of tax transactions. You must answer all questions using your

own words. However you may reference your learner guide, the PMBOK

guide and other online or hard copy resources to complete this

assessment.

The second part of the assessment covers exercises relating to the

calculation and processing of taxation information. Ideally you should be

able to answer these questions based on the processes that are currently

in place in your workplace. If this is not the case, then answer the

questions based on processes that should be implemented in your

workplace.

The final part of the assessment is based on a case study involving the

completion of a tax return for an individual.

Requirements for satisfactory completion

Page 3

Getting Started

Instructions

There is one (1) workbook for this unit and it contains one (1) assessment

made up of:

● Written Questions – A set of generic questions testing the student’s

general knowledge and understanding of the general theory behind

the unit.

● Exercises - A set of exercises to test the student’s knowledge,

analytical skills in problem solving and performing numerical

calculations.

● Case Study – A hypothetical exercise to test the student’s knowledge,

analytical skills in problem solving and performing numerical

calculations.

The following questions are divided into the following categories.

The first part of the assessment covers generic underpinning knowledge of

tax law and concepts. These questions are all in a short answer format. The

longer questions requiring creative thought processes are covered in the

second part of the assessment and the case study and involve the

calculation of tax transactions. You must answer all questions using your

own words. However you may reference your learner guide, the PMBOK

guide and other online or hard copy resources to complete this

assessment.

The second part of the assessment covers exercises relating to the

calculation and processing of taxation information. Ideally you should be

able to answer these questions based on the processes that are currently

in place in your workplace. If this is not the case, then answer the

questions based on processes that should be implemented in your

workplace.

The final part of the assessment is based on a case study involving the

completion of a tax return for an individual.

Requirements for satisfactory completion

Page 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Workbook W: Provide Management Accounting Information

For a ‘satisfactory’ result for each component of this workbook, all tasks

must be addressed to a ‘satisfactory’ standard. It is important you;

1. Provide responses using complete sentences, making direct

reference to the question.

2. Specifically address all parts of the question providing examples

where appropriate.

Competency Based Assessment

Competency based assessment focuses on whether you are able to

perform the task to the standard expected in the workplace. It relies on

you providing evidence that supports your claim of competence. This

evidence is in the form of your completion of the assessments set for each

unit.

Once you have submitted your completed assessments, your instructor will

assess your submission to determine your competence. To be deemed

competent in each course, you are required to achieve a satisfactory result

for all of the assessment components that make up that unit. Where a ‘not

yet satisfactory’ judgement is made, you will be given guidance on steps to

take to improve your performance and provided the opportunity to re-

submit evidence to demonstrate competence. Once a ‘satisfactory’

judgement has been made on all components for a unit, you will be

deemed ‘competent’ in that unit.

Submission

Only submit your workbook once all activities inside are complete. Should

you have any questions regarding your assessments, or not understand

what is required for you to complete your assessment, please feel free to

ask your instructor.

Keep your answers succinct and make sure you are answering the

question. Re-read the question after you have drafted up your response

just to be sure you have covered all that is needed.

Your final assessment result will either be ‘Competent’ or ‘Not Yet

Competent’.

When submitting your assessments please ensure that

1. All assessment tasks within the workbook have been completed

Page 4

For a ‘satisfactory’ result for each component of this workbook, all tasks

must be addressed to a ‘satisfactory’ standard. It is important you;

1. Provide responses using complete sentences, making direct

reference to the question.

2. Specifically address all parts of the question providing examples

where appropriate.

Competency Based Assessment

Competency based assessment focuses on whether you are able to

perform the task to the standard expected in the workplace. It relies on

you providing evidence that supports your claim of competence. This

evidence is in the form of your completion of the assessments set for each

unit.

Once you have submitted your completed assessments, your instructor will

assess your submission to determine your competence. To be deemed

competent in each course, you are required to achieve a satisfactory result

for all of the assessment components that make up that unit. Where a ‘not

yet satisfactory’ judgement is made, you will be given guidance on steps to

take to improve your performance and provided the opportunity to re-

submit evidence to demonstrate competence. Once a ‘satisfactory’

judgement has been made on all components for a unit, you will be

deemed ‘competent’ in that unit.

Submission

Only submit your workbook once all activities inside are complete. Should

you have any questions regarding your assessments, or not understand

what is required for you to complete your assessment, please feel free to

ask your instructor.

Keep your answers succinct and make sure you are answering the

question. Re-read the question after you have drafted up your response

just to be sure you have covered all that is needed.

Your final assessment result will either be ‘Competent’ or ‘Not Yet

Competent’.

When submitting your assessments please ensure that

1. All assessment tasks within the workbook have been completed

Page 4

Assessment Workbook W: Provide Management Accounting Information

2. You have proof read your assessment

Candidate Declaration

Submission of this workbook means you agree to abide by the terms of the

candidate declaration below.

By submitting this work, I declare that:

● I have been advised of the assessment requirements, have been

made aware of my rights and responsibilities as an assessment

candidate, and choose to be assessed at this time.

● I am aware that there is a limit to the number of submissions that I

can make for each assessment and I am submitting all documents

required to complete this Assessment Workbook.

● I have organised and named the files I am submitting according to

the instructions provided and I am aware that my assessor will not

assess work that cannot be clearly identified and may request the

work be resubmitted according to the correct process.

● This work is my own and contains no material written by another

person except where due reference is made. I am aware that a false

declaration may lead to the withdrawal of a qualification or

statement of attainment.

● I am aware that there is a policy of checking the validity of

qualifications that I submit as evidence as well as the

qualifications/evidence of parties who verify my performance or

observable skills. I give my consent to contact these parties for

verification purposes.

Page 5

2. You have proof read your assessment

Candidate Declaration

Submission of this workbook means you agree to abide by the terms of the

candidate declaration below.

By submitting this work, I declare that:

● I have been advised of the assessment requirements, have been

made aware of my rights and responsibilities as an assessment

candidate, and choose to be assessed at this time.

● I am aware that there is a limit to the number of submissions that I

can make for each assessment and I am submitting all documents

required to complete this Assessment Workbook.

● I have organised and named the files I am submitting according to

the instructions provided and I am aware that my assessor will not

assess work that cannot be clearly identified and may request the

work be resubmitted according to the correct process.

● This work is my own and contains no material written by another

person except where due reference is made. I am aware that a false

declaration may lead to the withdrawal of a qualification or

statement of attainment.

● I am aware that there is a policy of checking the validity of

qualifications that I submit as evidence as well as the

qualifications/evidence of parties who verify my performance or

observable skills. I give my consent to contact these parties for

verification purposes.

Page 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assessment Workbook W: Provide Management Accounting Information

Written Questions

Instructions

The following assessment is divided into three (3) categories.

The first part of the assessment covers generic underpinning knowledge of

the principles and application of management accounting and concepts.

These questions are all in a short answer format. The longer questions

requiring creative thought processes are covered in the second part of the

assessment and the case study. You must answer all questions using

your own words.However you may reference your learner guide, and

other online or hard copy resources to complete this assessment.

The second part of the assessment covers exercises relating to the

management, application and accounting for costs in a manufacturing or

service industry. Ideally you should be able to answer these questions

based on the processes that are currently in place in your workplace. If this

is not the case, then answer the questions based on processes that should

be implemented in your workplace.

The final part of the assessment is based on a case study involving the

management of financial information and monitoring performance in an

organisation.

Questions

WQ1: List the three (3) main functions of management.

The three main functions of management are as follows:

Planning – planning is one of the main functions of management.

The planning is done by the management in order to facilitate

smooth running of the organization. The management of a

particular organization adopts the method of planning in order to

establish a particular goal and then finding out the most suitable

method of achieving that goal.

Organizing – the function of organizing is exercised by the

management in order to designate tasks and responsibilities to the

individual or groups of employees that have the required skill or

knowledge that is required to complete the assigned task. The

function of organizing specifically deals with the leadership control

that exists within an organization.

Staffing – the third major function of the management deals with

the human resources that is required by an organization. The

Page 6

Written Questions

Instructions

The following assessment is divided into three (3) categories.

The first part of the assessment covers generic underpinning knowledge of

the principles and application of management accounting and concepts.

These questions are all in a short answer format. The longer questions

requiring creative thought processes are covered in the second part of the

assessment and the case study. You must answer all questions using

your own words.However you may reference your learner guide, and

other online or hard copy resources to complete this assessment.

The second part of the assessment covers exercises relating to the

management, application and accounting for costs in a manufacturing or

service industry. Ideally you should be able to answer these questions

based on the processes that are currently in place in your workplace. If this

is not the case, then answer the questions based on processes that should

be implemented in your workplace.

The final part of the assessment is based on a case study involving the

management of financial information and monitoring performance in an

organisation.

Questions

WQ1: List the three (3) main functions of management.

The three main functions of management are as follows:

Planning – planning is one of the main functions of management.

The planning is done by the management in order to facilitate

smooth running of the organization. The management of a

particular organization adopts the method of planning in order to

establish a particular goal and then finding out the most suitable

method of achieving that goal.

Organizing – the function of organizing is exercised by the

management in order to designate tasks and responsibilities to the

individual or groups of employees that have the required skill or

knowledge that is required to complete the assigned task. The

function of organizing specifically deals with the leadership control

that exists within an organization.

Staffing – the third major function of the management deals with

the human resources that is required by an organization. The

Page 6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Workbook W: Provide Management Accounting Information

function of staffing essentially deals with the recruitment and other

needs of the organization related to staff or personnel. The function

of staffing also involves activities like training, transfer and

promotion of the staff inside an organization.

WQ2: Explain how cost accounting systems differ between manufacturing

and service organisations.

The cost accounting system for a manufacturing organization differs from

a service organization in many aspects. The output produced in a

manufacturing organization is a tangible good that is its cost can be

measured in terms of quantity produced, but in case of a service

industry, the output is always intangible in nature that is its cost cannot

be calculated in terms of quantity produced , therefore a particular cost

allocation method is adopted in order to measure the cost of service.

Another major difference between the cost accounting system in a

manufacturing and service organization pertains to the area of labor. In a

manufacturing organization the entire process of production can be

automated thus depending on a technology intensive workforce than

manual workforce but in an service organization the entire workforce is

generally manual labor intensive that is the process of serving a

particular customer cannot be automated. Therefore the cost of

employing a specific technology can be easily calculates in a

manufacturing organization but in case of a service organization the cost

of manual labor has to be calculated by following a complex system of

cost allocation. In some cases the cost of service is calculated by certain

pre determined percentages.

Page 7

function of staffing essentially deals with the recruitment and other

needs of the organization related to staff or personnel. The function

of staffing also involves activities like training, transfer and

promotion of the staff inside an organization.

WQ2: Explain how cost accounting systems differ between manufacturing

and service organisations.

The cost accounting system for a manufacturing organization differs from

a service organization in many aspects. The output produced in a

manufacturing organization is a tangible good that is its cost can be

measured in terms of quantity produced, but in case of a service

industry, the output is always intangible in nature that is its cost cannot

be calculated in terms of quantity produced , therefore a particular cost

allocation method is adopted in order to measure the cost of service.

Another major difference between the cost accounting system in a

manufacturing and service organization pertains to the area of labor. In a

manufacturing organization the entire process of production can be

automated thus depending on a technology intensive workforce than

manual workforce but in an service organization the entire workforce is

generally manual labor intensive that is the process of serving a

particular customer cannot be automated. Therefore the cost of

employing a specific technology can be easily calculates in a

manufacturing organization but in case of a service organization the cost

of manual labor has to be calculated by following a complex system of

cost allocation. In some cases the cost of service is calculated by certain

pre determined percentages.

Page 7

Assessment Workbook W: Provide Management Accounting Information

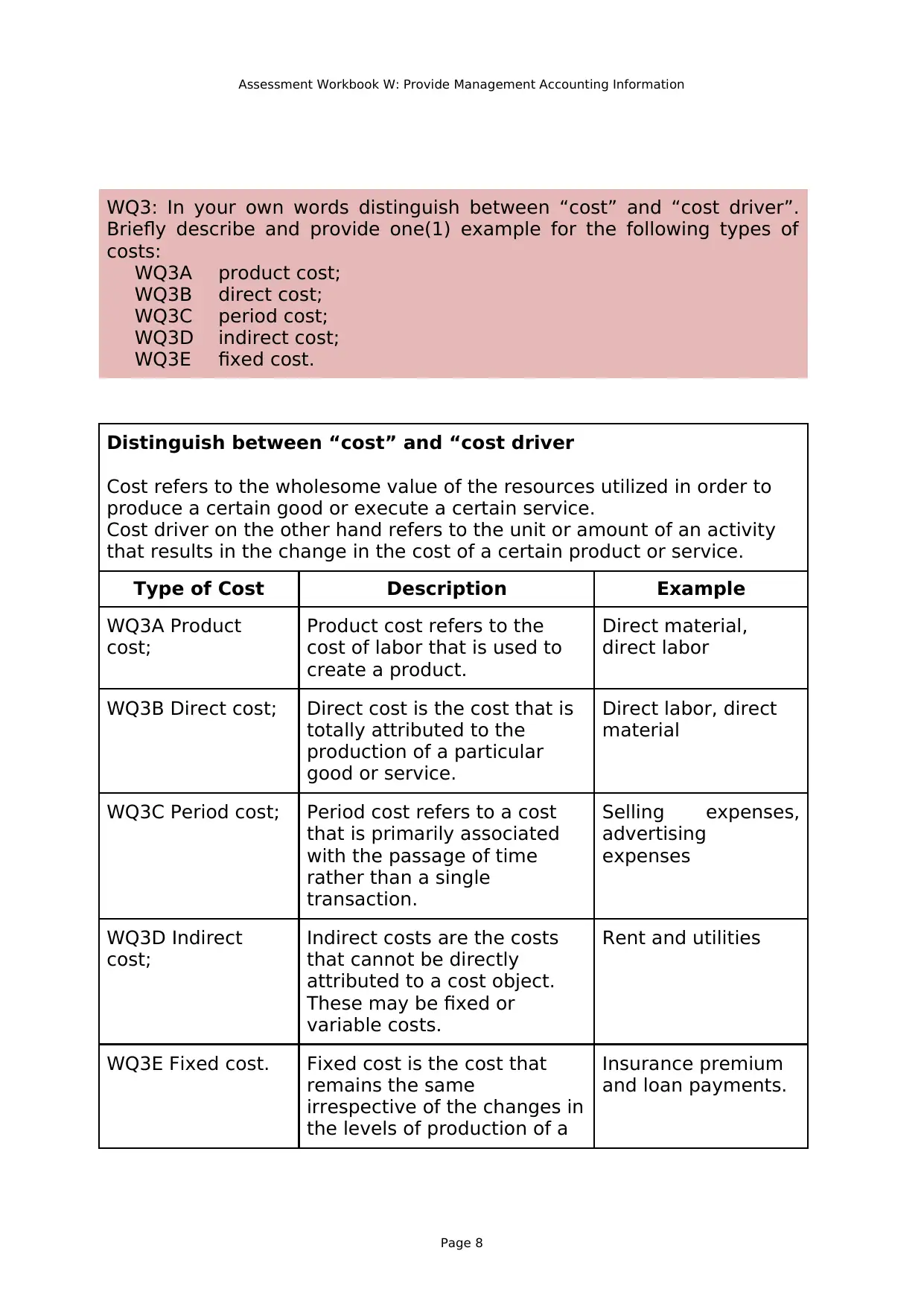

WQ3: In your own words distinguish between “cost” and “cost driver”.

Briefly describe and provide one(1) example for the following types of

costs:

WQ3A product cost;

WQ3B direct cost;

WQ3C period cost;

WQ3D indirect cost;

WQ3E fixed cost.

Distinguish between “cost” and “cost driver

Cost refers to the wholesome value of the resources utilized in order to

produce a certain good or execute a certain service.

Cost driver on the other hand refers to the unit or amount of an activity

that results in the change in the cost of a certain product or service.

Type of Cost Description Example

WQ3A Product

cost;

Product cost refers to the

cost of labor that is used to

create a product.

Direct material,

direct labor

WQ3B Direct cost; Direct cost is the cost that is

totally attributed to the

production of a particular

good or service.

Direct labor, direct

material

WQ3C Period cost; Period cost refers to a cost

that is primarily associated

with the passage of time

rather than a single

transaction.

Selling expenses,

advertising

expenses

WQ3D Indirect

cost;

Indirect costs are the costs

that cannot be directly

attributed to a cost object.

These may be fixed or

variable costs.

Rent and utilities

WQ3E Fixed cost. Fixed cost is the cost that

remains the same

irrespective of the changes in

the levels of production of a

Insurance premium

and loan payments.

Page 8

WQ3: In your own words distinguish between “cost” and “cost driver”.

Briefly describe and provide one(1) example for the following types of

costs:

WQ3A product cost;

WQ3B direct cost;

WQ3C period cost;

WQ3D indirect cost;

WQ3E fixed cost.

Distinguish between “cost” and “cost driver

Cost refers to the wholesome value of the resources utilized in order to

produce a certain good or execute a certain service.

Cost driver on the other hand refers to the unit or amount of an activity

that results in the change in the cost of a certain product or service.

Type of Cost Description Example

WQ3A Product

cost;

Product cost refers to the

cost of labor that is used to

create a product.

Direct material,

direct labor

WQ3B Direct cost; Direct cost is the cost that is

totally attributed to the

production of a particular

good or service.

Direct labor, direct

material

WQ3C Period cost; Period cost refers to a cost

that is primarily associated

with the passage of time

rather than a single

transaction.

Selling expenses,

advertising

expenses

WQ3D Indirect

cost;

Indirect costs are the costs

that cannot be directly

attributed to a cost object.

These may be fixed or

variable costs.

Rent and utilities

WQ3E Fixed cost. Fixed cost is the cost that

remains the same

irrespective of the changes in

the levels of production of a

Insurance premium

and loan payments.

Page 8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assessment Workbook W: Provide Management Accounting Information

particular product.

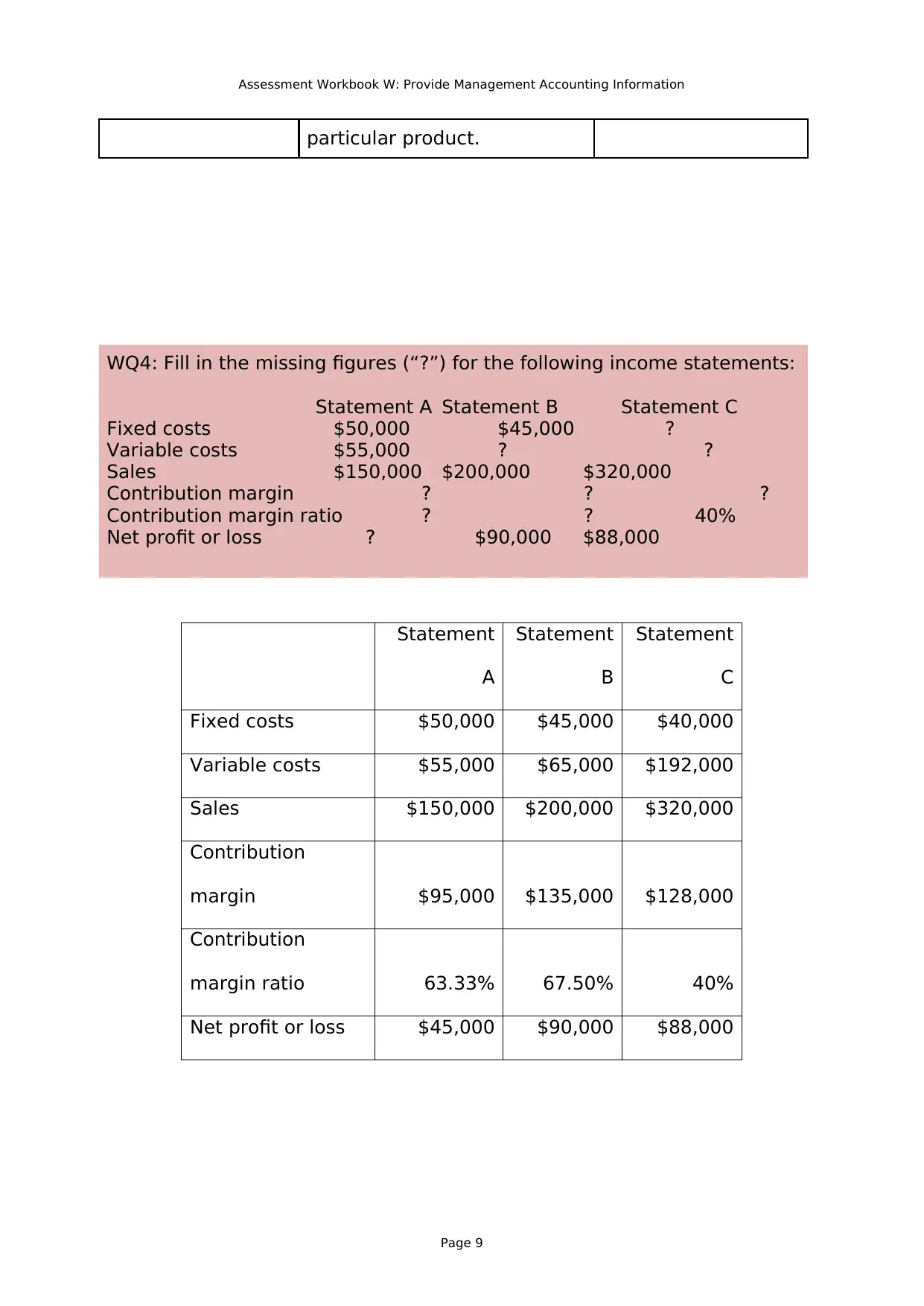

WQ4: Fill in the missing figures (“?”) for the following income statements:

Statement A Statement B Statement C

Fixed costs $50,000 $45,000 ?

Variable costs $55,000 ? ?

Sales $150,000 $200,000 $320,000

Contribution margin ? ? ?

Contribution margin ratio ? ? 40%

Net profit or loss ? $90,000 $88,000

Statement

A

Statement

B

Statement

C

Fixed costs $50,000 $45,000 $40,000

Variable costs $55,000 $65,000 $192,000

Sales $150,000 $200,000 $320,000

Contribution

margin $95,000 $135,000 $128,000

Contribution

margin ratio 63.33% 67.50% 40%

Net profit or loss $45,000 $90,000 $88,000

Page 9

particular product.

WQ4: Fill in the missing figures (“?”) for the following income statements:

Statement A Statement B Statement C

Fixed costs $50,000 $45,000 ?

Variable costs $55,000 ? ?

Sales $150,000 $200,000 $320,000

Contribution margin ? ? ?

Contribution margin ratio ? ? 40%

Net profit or loss ? $90,000 $88,000

Statement

A

Statement

B

Statement

C

Fixed costs $50,000 $45,000 $40,000

Variable costs $55,000 $65,000 $192,000

Sales $150,000 $200,000 $320,000

Contribution

margin $95,000 $135,000 $128,000

Contribution

margin ratio 63.33% 67.50% 40%

Net profit or loss $45,000 $90,000 $88,000

Page 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Workbook W: Provide Management Accounting Information

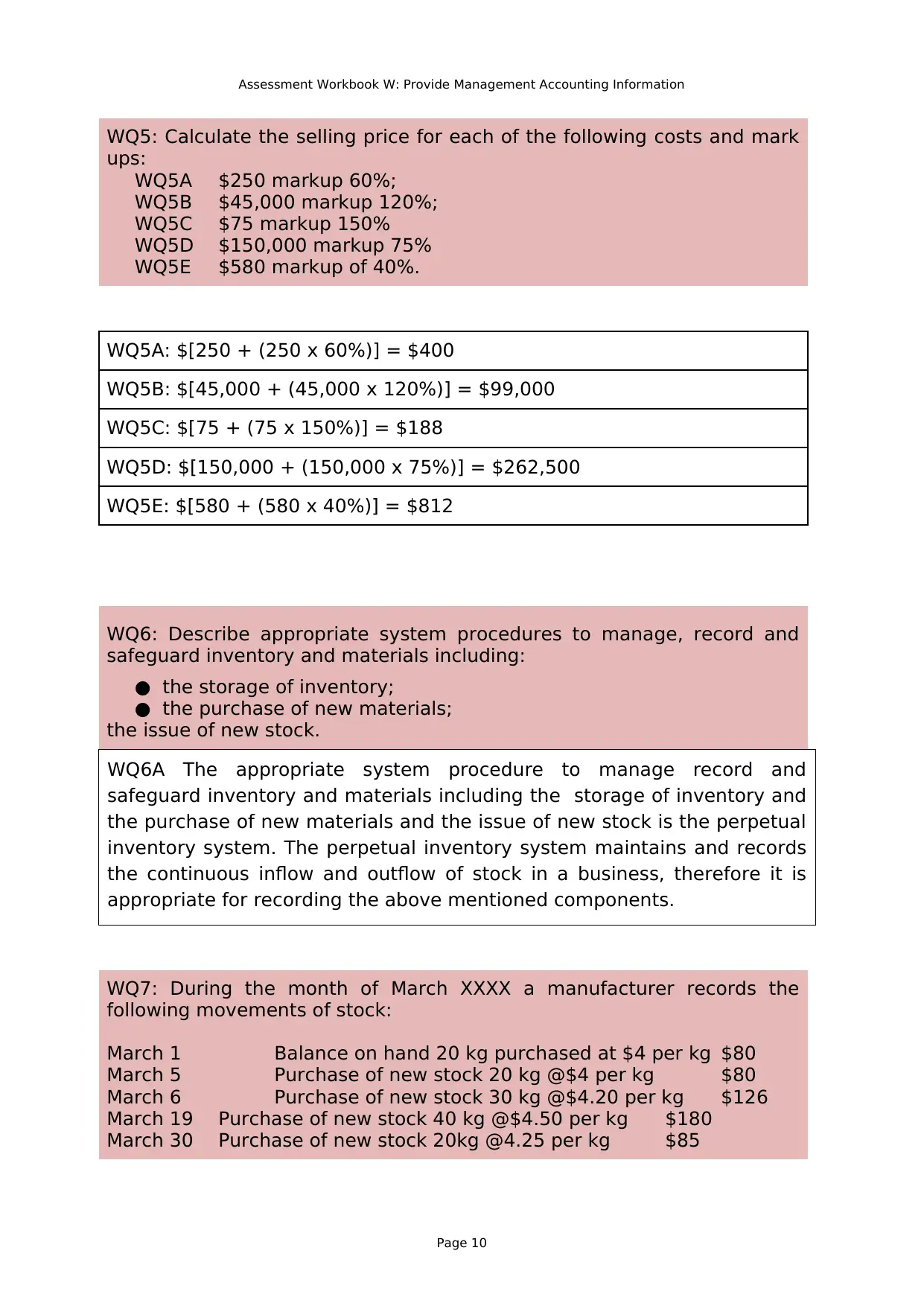

WQ5: Calculate the selling price for each of the following costs and mark

ups:

WQ5A $250 markup 60%;

WQ5B $45,000 markup 120%;

WQ5C $75 markup 150%

WQ5D $150,000 markup 75%

WQ5E $580 markup of 40%.

WQ5A: $[250 + (250 x 60%)] = $400

WQ5B: $[45,000 + (45,000 x 120%)] = $99,000

WQ5C: $[75 + (75 x 150%)] = $188

WQ5D: $[150,000 + (150,000 x 75%)] = $262,500

WQ5E: $[580 + (580 x 40%)] = $812

WQ6: Describe appropriate system procedures to manage, record and

safeguard inventory and materials including:

● the storage of inventory;

● the purchase of new materials;

the issue of new stock.

WQ6A The appropriate system procedure to manage record and

safeguard inventory and materials including the storage of inventory and

the purchase of new materials and the issue of new stock is the perpetual

inventory system. The perpetual inventory system maintains and records

the continuous inflow and outflow of stock in a business, therefore it is

appropriate for recording the above mentioned components.

WQ7: During the month of March XXXX a manufacturer records the

following movements of stock:

March 1 Balance on hand 20 kg purchased at $4 per kg $80

March 5 Purchase of new stock 20 kg @$4 per kg $80

March 6 Purchase of new stock 30 kg @$4.20 per kg $126

March 19 Purchase of new stock 40 kg @$4.50 per kg $180

March 30 Purchase of new stock 20kg @4.25 per kg $85

Page 10

WQ5: Calculate the selling price for each of the following costs and mark

ups:

WQ5A $250 markup 60%;

WQ5B $45,000 markup 120%;

WQ5C $75 markup 150%

WQ5D $150,000 markup 75%

WQ5E $580 markup of 40%.

WQ5A: $[250 + (250 x 60%)] = $400

WQ5B: $[45,000 + (45,000 x 120%)] = $99,000

WQ5C: $[75 + (75 x 150%)] = $188

WQ5D: $[150,000 + (150,000 x 75%)] = $262,500

WQ5E: $[580 + (580 x 40%)] = $812

WQ6: Describe appropriate system procedures to manage, record and

safeguard inventory and materials including:

● the storage of inventory;

● the purchase of new materials;

the issue of new stock.

WQ6A The appropriate system procedure to manage record and

safeguard inventory and materials including the storage of inventory and

the purchase of new materials and the issue of new stock is the perpetual

inventory system. The perpetual inventory system maintains and records

the continuous inflow and outflow of stock in a business, therefore it is

appropriate for recording the above mentioned components.

WQ7: During the month of March XXXX a manufacturer records the

following movements of stock:

March 1 Balance on hand 20 kg purchased at $4 per kg $80

March 5 Purchase of new stock 20 kg @$4 per kg $80

March 6 Purchase of new stock 30 kg @$4.20 per kg $126

March 19 Purchase of new stock 40 kg @$4.50 per kg $180

March 30 Purchase of new stock 20kg @4.25 per kg $85

Page 10

Assessment Workbook W: Provide Management Accounting Information

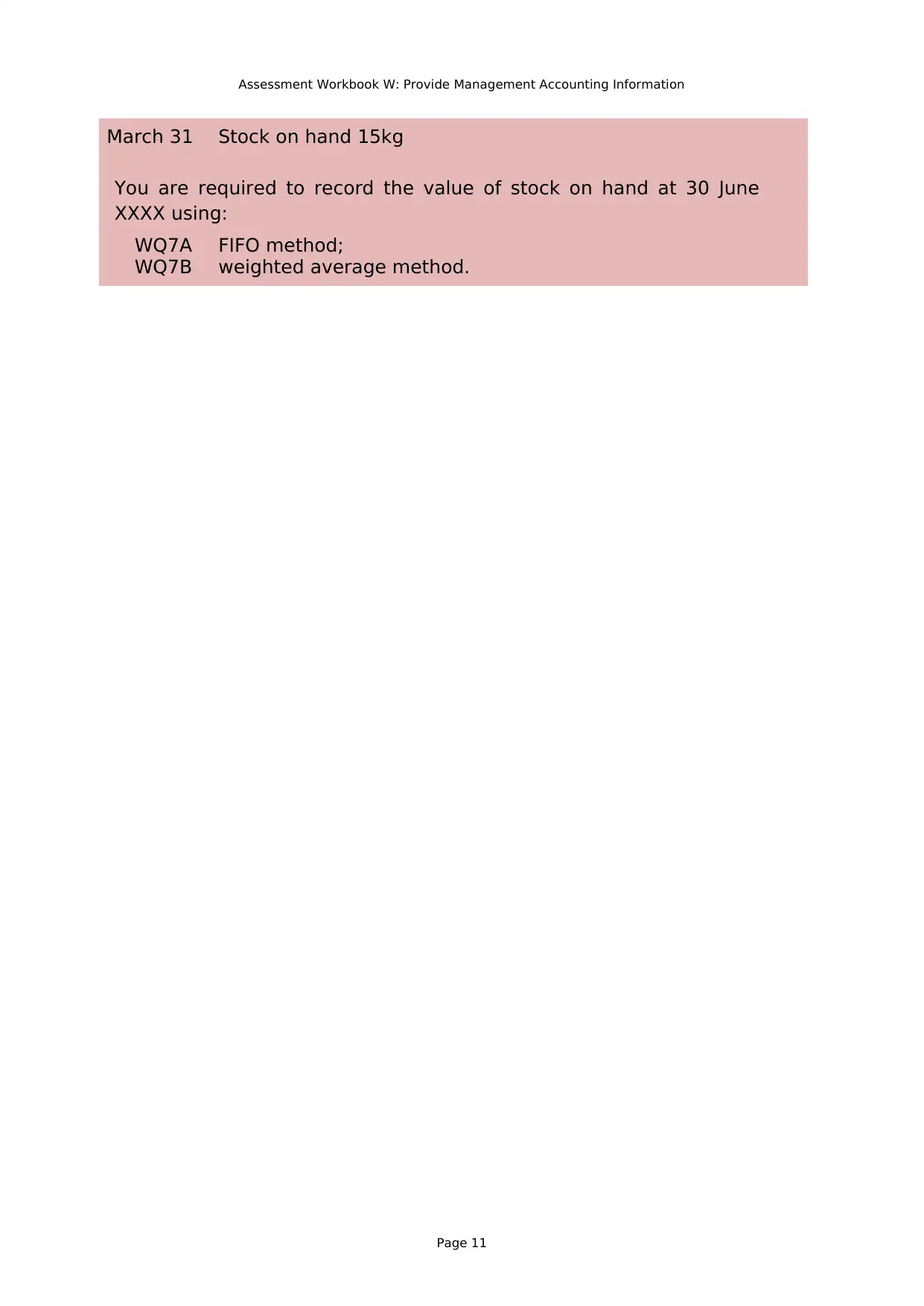

March 31 Stock on hand 15kg

You are required to record the value of stock on hand at 30 June

XXXX using:

WQ7A FIFO method;

WQ7B weighted average method.

Page 11

March 31 Stock on hand 15kg

You are required to record the value of stock on hand at 30 June

XXXX using:

WQ7A FIFO method;

WQ7B weighted average method.

Page 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 44

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.