FNSACC507: Assessment Workbook for Management Accounting Information

VerifiedAdded on 2023/06/03

|14

|4414

|262

Homework Assignment

AI Summary

This document is a comprehensive assessment workbook for the FNSACC507 unit, focusing on providing management accounting information. It includes two assessments: short answer questions and a project. The short answer questions cover topics like the differences between manual and computerized accounting systems, identifying and establishing systems for cost data generation, classifying and checking data, and the importance of organizational policies. The project involves analyzing cost reports and budgets, calculating variances, and reviewing costing system integrity. The workbook also includes questions on analyzing financial statements, consulting staff for cost information, the importance of clear report structures, and ensuring report accuracy. The provided answers demonstrate an understanding of gathering and recording operating and cost data, analyzing data and assigning costs, preparing cost reports and budgets, and analyzing variances and reviewing costing system integrity, all crucial aspects of management accounting. The assessment also covers the importance of accurate and timely reports, and the analysis of cost behavior within an organization.

Assessment Workbook – FNSACC507 1 | P a g e Version 3.0

Assessment Workbook: FNSACC507

Provide management accounting

information

Assessment Workbook: FNSACC507

Provide management accounting

information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Version control

Version No. Date Dept. Change

1.0 03/05/2016 Training Original

2.0 12/08/2016 Training Moodle updates

3.0 15/09/2016 Training Moodle updates and changed title from Instructor

Workbook to Trainer Guide

Copyright Statement

© Copyright National Training

Disclaimer

All rights reserved. No part of this publication may be reproduced or transmitted

in any form or by any means, electronic or mechanical, including photocopying,

scanning, recording, or any information storage retrieval system without

permission in writing from National Training. No patent liability is assumed with

respect to the use of information used herein.

While every effort has been taken in the preparation of this publication, the

publisher and authors assume no responsibility for errors or omissions. Neither is

any liability assumed for damages resulting from the use of information contained

herein.

Assessment Workbook – FNSACC507 2 | P a g e Version 3.0

Version No. Date Dept. Change

1.0 03/05/2016 Training Original

2.0 12/08/2016 Training Moodle updates

3.0 15/09/2016 Training Moodle updates and changed title from Instructor

Workbook to Trainer Guide

Copyright Statement

© Copyright National Training

Disclaimer

All rights reserved. No part of this publication may be reproduced or transmitted

in any form or by any means, electronic or mechanical, including photocopying,

scanning, recording, or any information storage retrieval system without

permission in writing from National Training. No patent liability is assumed with

respect to the use of information used herein.

While every effort has been taken in the preparation of this publication, the

publisher and authors assume no responsibility for errors or omissions. Neither is

any liability assumed for damages resulting from the use of information contained

herein.

Assessment Workbook – FNSACC507 2 | P a g e Version 3.0

Contents

Assessment 1: Short Answer Questions 4

Question 1A...................................................................................................................................4

Question 1B...................................................................................................................................4

Question 2A...................................................................................................................................4

Question 2B...................................................................................................................................4

Question 3A...................................................................................................................................4

Question 3B...................................................................................................................................5

Question 4.....................................................................................................................................5

Question 5.....................................................................................................................................6

Question 6.....................................................................................................................................6

Question 7.....................................................................................................................................7

Question 8.....................................................................................................................................7

Question 9.....................................................................................................................................8

Question 10...................................................................................................................................8

Question 11...................................................................................................................................8

Question 12...................................................................................................................................8

Question 13...................................................................................................................................9

Question 14...................................................................................................................................9

Question 15...................................................................................................................................9

Question 16...................................................................................................................................9

Assessment 2: Project 9

Project.........................................................................................................................................10

Question 1...................................................................................................................................10

Question 2...................................................................................................................................11

Question 3A.................................................................................................................................11

Question 3B.................................................................................................................................11

Assessment Workbook – FNSACC507 3 | P a g e Version 3.0

Assessment 1: Short Answer Questions 4

Question 1A...................................................................................................................................4

Question 1B...................................................................................................................................4

Question 2A...................................................................................................................................4

Question 2B...................................................................................................................................4

Question 3A...................................................................................................................................4

Question 3B...................................................................................................................................5

Question 4.....................................................................................................................................5

Question 5.....................................................................................................................................6

Question 6.....................................................................................................................................6

Question 7.....................................................................................................................................7

Question 8.....................................................................................................................................7

Question 9.....................................................................................................................................8

Question 10...................................................................................................................................8

Question 11...................................................................................................................................8

Question 12...................................................................................................................................8

Question 13...................................................................................................................................9

Question 14...................................................................................................................................9

Question 15...................................................................................................................................9

Question 16...................................................................................................................................9

Assessment 2: Project 9

Project.........................................................................................................................................10

Question 1...................................................................................................................................10

Question 2...................................................................................................................................11

Question 3A.................................................................................................................................11

Question 3B.................................................................................................................................11

Assessment Workbook – FNSACC507 3 | P a g e Version 3.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assessment 1: Short Answer Questions

The objective of this section is to demonstrate 1.0 Gather and record operating and cost data

Question 1A

What are the differences between manual and computerised systems when entering final

transactions?

The main difference among the manual and computerized system is easiness to backup the

accounts. In case of fire and other mishap, all the transactions could be saved and backed up in

computerized accounting but it cannot happen with the manual accounting unless the other copies of

the transaction have been saved at other place (Tsanakas and Millossovich, 2016).

Question 1B

Describe how do you Identify and establish systems to generate operating cost data?

The identification of the operating cost data is done on the basis of business’s nature in order

to maintain the records, transactions, easily accessibility and the information which could be utilized

in the accounting system. a system must be established by the organization through focusing on the

accounting process which focuses on the data collection, recording of the data, journalize the data,

posit the ledger entries, make the trail balance and financial statement of the organization (Ward,

2012) .

Question 2A

Explain the process to which you would classify and check data in preparation for processing.

In order to classify the financial data, the nature of the cost is recognized firstlysuch as the

direct cost, indirect cost, variable cost, fixed cost etc so that the treatment of each cost must be done

accordingly. Mainly the data is classified into 3 categories which are as follows:

Direct Material

Direct labour

Overheads

Question 2B

As an accountant of an organisation, explain why it is important to refer to the organisational

policies and procedures while classifying and coding data?

Organizational policies and procedure of the organizations are different to other organziation’s

policies. The policies reflect the belief and phisloshy of the organization. And thus, it becomes

imprtnat for the accountant to follow that process so that the right conclusion could be reached and

the deatials support could be reached to each of the department (Palicka, 2011).

The objective of this section is to demonstrate 2.0 Analyse data and assign costs

Question 3A

Why do organisations need accurate and timely reports and what financial information is required to

manage the organisation’s finances?

Assessment Workbook – FNSACC507 4 | P a g e Version 3.0

The objective of this section is to demonstrate 1.0 Gather and record operating and cost data

Question 1A

What are the differences between manual and computerised systems when entering final

transactions?

The main difference among the manual and computerized system is easiness to backup the

accounts. In case of fire and other mishap, all the transactions could be saved and backed up in

computerized accounting but it cannot happen with the manual accounting unless the other copies of

the transaction have been saved at other place (Tsanakas and Millossovich, 2016).

Question 1B

Describe how do you Identify and establish systems to generate operating cost data?

The identification of the operating cost data is done on the basis of business’s nature in order

to maintain the records, transactions, easily accessibility and the information which could be utilized

in the accounting system. a system must be established by the organization through focusing on the

accounting process which focuses on the data collection, recording of the data, journalize the data,

posit the ledger entries, make the trail balance and financial statement of the organization (Ward,

2012) .

Question 2A

Explain the process to which you would classify and check data in preparation for processing.

In order to classify the financial data, the nature of the cost is recognized firstlysuch as the

direct cost, indirect cost, variable cost, fixed cost etc so that the treatment of each cost must be done

accordingly. Mainly the data is classified into 3 categories which are as follows:

Direct Material

Direct labour

Overheads

Question 2B

As an accountant of an organisation, explain why it is important to refer to the organisational

policies and procedures while classifying and coding data?

Organizational policies and procedure of the organizations are different to other organziation’s

policies. The policies reflect the belief and phisloshy of the organization. And thus, it becomes

imprtnat for the accountant to follow that process so that the right conclusion could be reached and

the deatials support could be reached to each of the department (Palicka, 2011).

The objective of this section is to demonstrate 2.0 Analyse data and assign costs

Question 3A

Why do organisations need accurate and timely reports and what financial information is required to

manage the organisation’s finances?

Assessment Workbook – FNSACC507 4 | P a g e Version 3.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

An up to date, accurate and timely report in an organization make sure that the financial

informnation is ccurate and the informnation has been used in proper way in the business. It

monitors the business outcome in the regular basis, makes comparison among the forecast and

actual result, identifies the area where extra expenses are incurred and fulfil the stuatory and

taxation obligation of the business. It makes it easier for the business and the stakeholders to make

better decision in reagards to the business and its activities (Moles, Parrino and Kidwekk, 2011).

Question 3B

Explain how you would analyse costs and what cost behaviour characteristics can be identified in

organisational reports.

Cost analysis referes to the measurnent of the coston the basis of its nature and the behaviour.

Mostly, the cost occurred in the business is either manufacturing cost or the overheads. The cost

which is directly related to the production process in the direct manufacturing vost and rest all the

cost falls in the category of overheads.

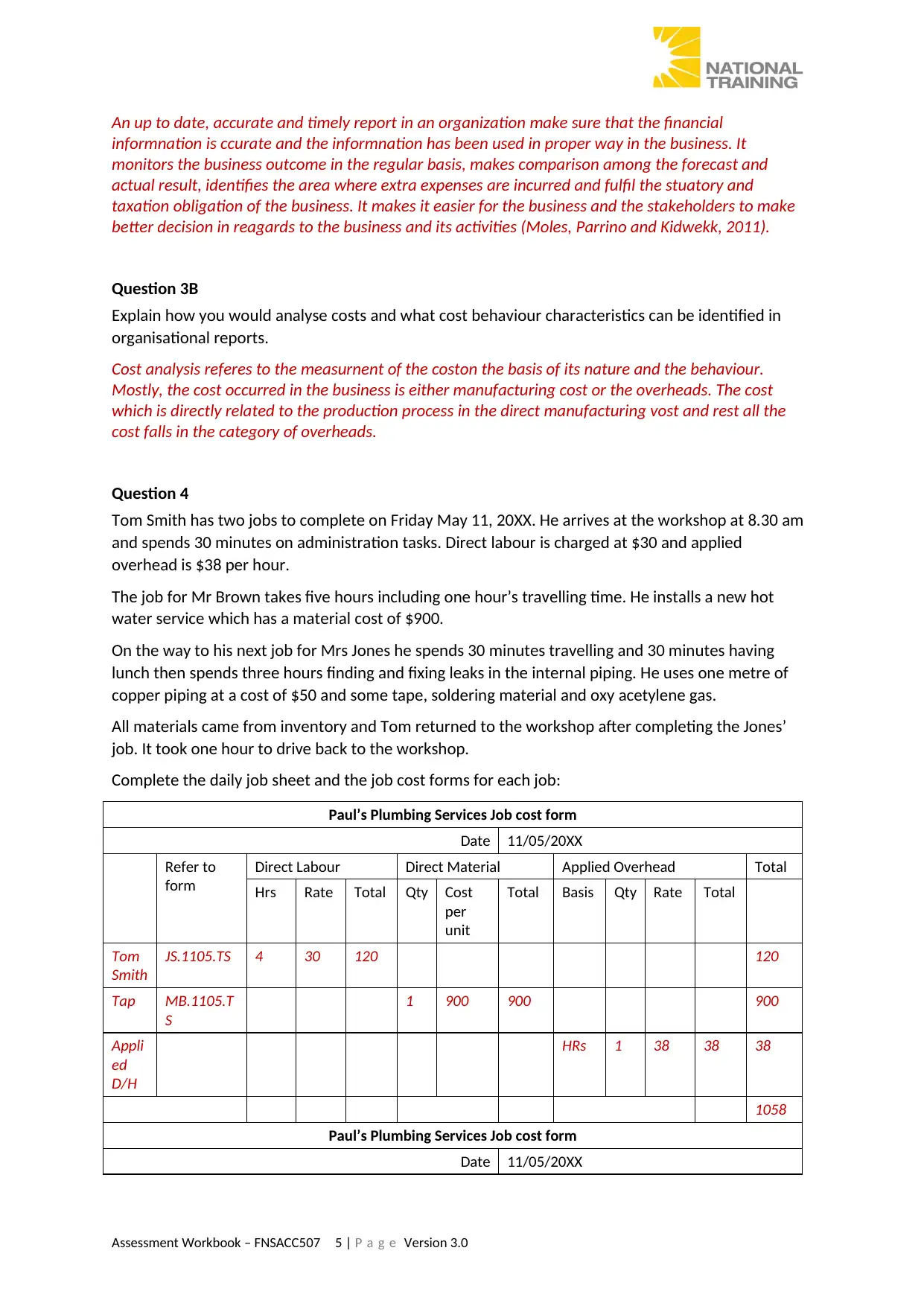

Question 4

Tom Smith has two jobs to complete on Friday May 11, 20XX. He arrives at the workshop at 8.30 am

and spends 30 minutes on administration tasks. Direct labour is charged at $30 and applied

overhead is $38 per hour.

The job for Mr Brown takes five hours including one hour’s travelling time. He installs a new hot

water service which has a material cost of $900.

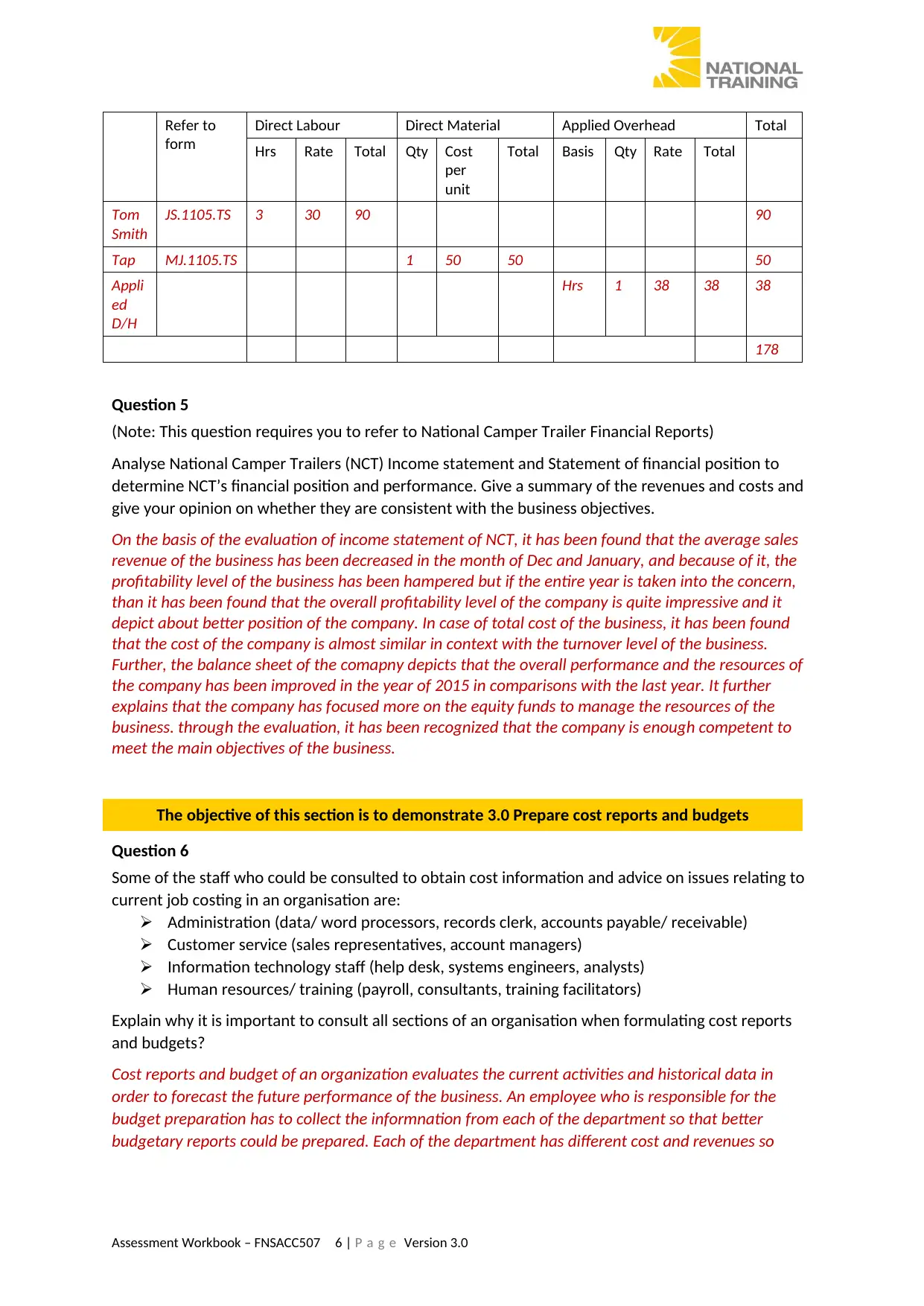

On the way to his next job for Mrs Jones he spends 30 minutes travelling and 30 minutes having

lunch then spends three hours finding and fixing leaks in the internal piping. He uses one metre of

copper piping at a cost of $50 and some tape, soldering material and oxy acetylene gas.

All materials came from inventory and Tom returned to the workshop after completing the Jones’

job. It took one hour to drive back to the workshop.

Complete the daily job sheet and the job cost forms for each job:

Paul’s Plumbing Services Job cost form

Date 11/05/20XX

Refer to

form

Direct Labour Direct Material Applied Overhead Total

Hrs Rate Total Qty Cost

per

unit

Total Basis Qty Rate Total

Tom

Smith

JS.1105.TS 4 30 120 120

Tap MB.1105.T

S

1 900 900 900

Appli

ed

D/H

HRs 1 38 38 38

1058

Paul’s Plumbing Services Job cost form

Date 11/05/20XX

Assessment Workbook – FNSACC507 5 | P a g e Version 3.0

informnation is ccurate and the informnation has been used in proper way in the business. It

monitors the business outcome in the regular basis, makes comparison among the forecast and

actual result, identifies the area where extra expenses are incurred and fulfil the stuatory and

taxation obligation of the business. It makes it easier for the business and the stakeholders to make

better decision in reagards to the business and its activities (Moles, Parrino and Kidwekk, 2011).

Question 3B

Explain how you would analyse costs and what cost behaviour characteristics can be identified in

organisational reports.

Cost analysis referes to the measurnent of the coston the basis of its nature and the behaviour.

Mostly, the cost occurred in the business is either manufacturing cost or the overheads. The cost

which is directly related to the production process in the direct manufacturing vost and rest all the

cost falls in the category of overheads.

Question 4

Tom Smith has two jobs to complete on Friday May 11, 20XX. He arrives at the workshop at 8.30 am

and spends 30 minutes on administration tasks. Direct labour is charged at $30 and applied

overhead is $38 per hour.

The job for Mr Brown takes five hours including one hour’s travelling time. He installs a new hot

water service which has a material cost of $900.

On the way to his next job for Mrs Jones he spends 30 minutes travelling and 30 minutes having

lunch then spends three hours finding and fixing leaks in the internal piping. He uses one metre of

copper piping at a cost of $50 and some tape, soldering material and oxy acetylene gas.

All materials came from inventory and Tom returned to the workshop after completing the Jones’

job. It took one hour to drive back to the workshop.

Complete the daily job sheet and the job cost forms for each job:

Paul’s Plumbing Services Job cost form

Date 11/05/20XX

Refer to

form

Direct Labour Direct Material Applied Overhead Total

Hrs Rate Total Qty Cost

per

unit

Total Basis Qty Rate Total

Tom

Smith

JS.1105.TS 4 30 120 120

Tap MB.1105.T

S

1 900 900 900

Appli

ed

D/H

HRs 1 38 38 38

1058

Paul’s Plumbing Services Job cost form

Date 11/05/20XX

Assessment Workbook – FNSACC507 5 | P a g e Version 3.0

Refer to

form

Direct Labour Direct Material Applied Overhead Total

Hrs Rate Total Qty Cost

per

unit

Total Basis Qty Rate Total

Tom

Smith

JS.1105.TS 3 30 90 90

Tap MJ.1105.TS 1 50 50 50

Appli

ed

D/H

Hrs 1 38 38 38

178

Question 5

(Note: This question requires you to refer to National Camper Trailer Financial Reports)

Analyse National Camper Trailers (NCT) Income statement and Statement of financial position to

determine NCT’s financial position and performance. Give a summary of the revenues and costs and

give your opinion on whether they are consistent with the business objectives.

On the basis of the evaluation of income statement of NCT, it has been found that the average sales

revenue of the business has been decreased in the month of Dec and January, and because of it, the

profitability level of the business has been hampered but if the entire year is taken into the concern,

than it has been found that the overall profitability level of the company is quite impressive and it

depict about better position of the company. In case of total cost of the business, it has been found

that the cost of the company is almost similar in context with the turnover level of the business.

Further, the balance sheet of the comapny depicts that the overall performance and the resources of

the company has been improved in the year of 2015 in comparisons with the last year. It further

explains that the company has focused more on the equity funds to manage the resources of the

business. through the evaluation, it has been recognized that the company is enough competent to

meet the main objectives of the business.

The objective of this section is to demonstrate 3.0 Prepare cost reports and budgets

Question 6

Some of the staff who could be consulted to obtain cost information and advice on issues relating to

current job costing in an organisation are:

Administration (data/ word processors, records clerk, accounts payable/ receivable)

Customer service (sales representatives, account managers)

Information technology staff (help desk, systems engineers, analysts)

Human resources/ training (payroll, consultants, training facilitators)

Explain why it is important to consult all sections of an organisation when formulating cost reports

and budgets?

Cost reports and budget of an organization evaluates the current activities and historical data in

order to forecast the future performance of the business. An employee who is responsible for the

budget preparation has to collect the informnation from each of the department so that better

budgetary reports could be prepared. Each of the department has different cost and revenues so

Assessment Workbook – FNSACC507 6 | P a g e Version 3.0

form

Direct Labour Direct Material Applied Overhead Total

Hrs Rate Total Qty Cost

per

unit

Total Basis Qty Rate Total

Tom

Smith

JS.1105.TS 3 30 90 90

Tap MJ.1105.TS 1 50 50 50

Appli

ed

D/H

Hrs 1 38 38 38

178

Question 5

(Note: This question requires you to refer to National Camper Trailer Financial Reports)

Analyse National Camper Trailers (NCT) Income statement and Statement of financial position to

determine NCT’s financial position and performance. Give a summary of the revenues and costs and

give your opinion on whether they are consistent with the business objectives.

On the basis of the evaluation of income statement of NCT, it has been found that the average sales

revenue of the business has been decreased in the month of Dec and January, and because of it, the

profitability level of the business has been hampered but if the entire year is taken into the concern,

than it has been found that the overall profitability level of the company is quite impressive and it

depict about better position of the company. In case of total cost of the business, it has been found

that the cost of the company is almost similar in context with the turnover level of the business.

Further, the balance sheet of the comapny depicts that the overall performance and the resources of

the company has been improved in the year of 2015 in comparisons with the last year. It further

explains that the company has focused more on the equity funds to manage the resources of the

business. through the evaluation, it has been recognized that the company is enough competent to

meet the main objectives of the business.

The objective of this section is to demonstrate 3.0 Prepare cost reports and budgets

Question 6

Some of the staff who could be consulted to obtain cost information and advice on issues relating to

current job costing in an organisation are:

Administration (data/ word processors, records clerk, accounts payable/ receivable)

Customer service (sales representatives, account managers)

Information technology staff (help desk, systems engineers, analysts)

Human resources/ training (payroll, consultants, training facilitators)

Explain why it is important to consult all sections of an organisation when formulating cost reports

and budgets?

Cost reports and budget of an organization evaluates the current activities and historical data in

order to forecast the future performance of the business. An employee who is responsible for the

budget preparation has to collect the informnation from each of the department so that better

budgetary reports could be prepared. Each of the department has different cost and revenues so

Assessment Workbook – FNSACC507 6 | P a g e Version 3.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

infromnation and data collection from each of the department in necessary in the business (Krantz,

2016).

Question 7

Why is it essential for budgets and reports to be presented in a clear structure and format that

complies with management information requirements and organisational procedures?

a budget helps the organization and the internal stakeholders of the business to pull together its

commitment, projects, plans, cost and a good procedure plan in order to meet the common goal of

the business. A clear structure and a better format could only help the organization and its

stakeholders to undertand the future forecasting so that they could make the staregies accordingly

and meet the cmmon goals and objectives of the business. if an the management informnation and

the proper process of organization would be complied along with the budegtory reports than it would

make it easier for the managers of the organization to make better decision (Lumby and Jones,

2007).

The objective of this section is to demonstrate

4.0 Analyse variances and review costing system integrity

Question 8

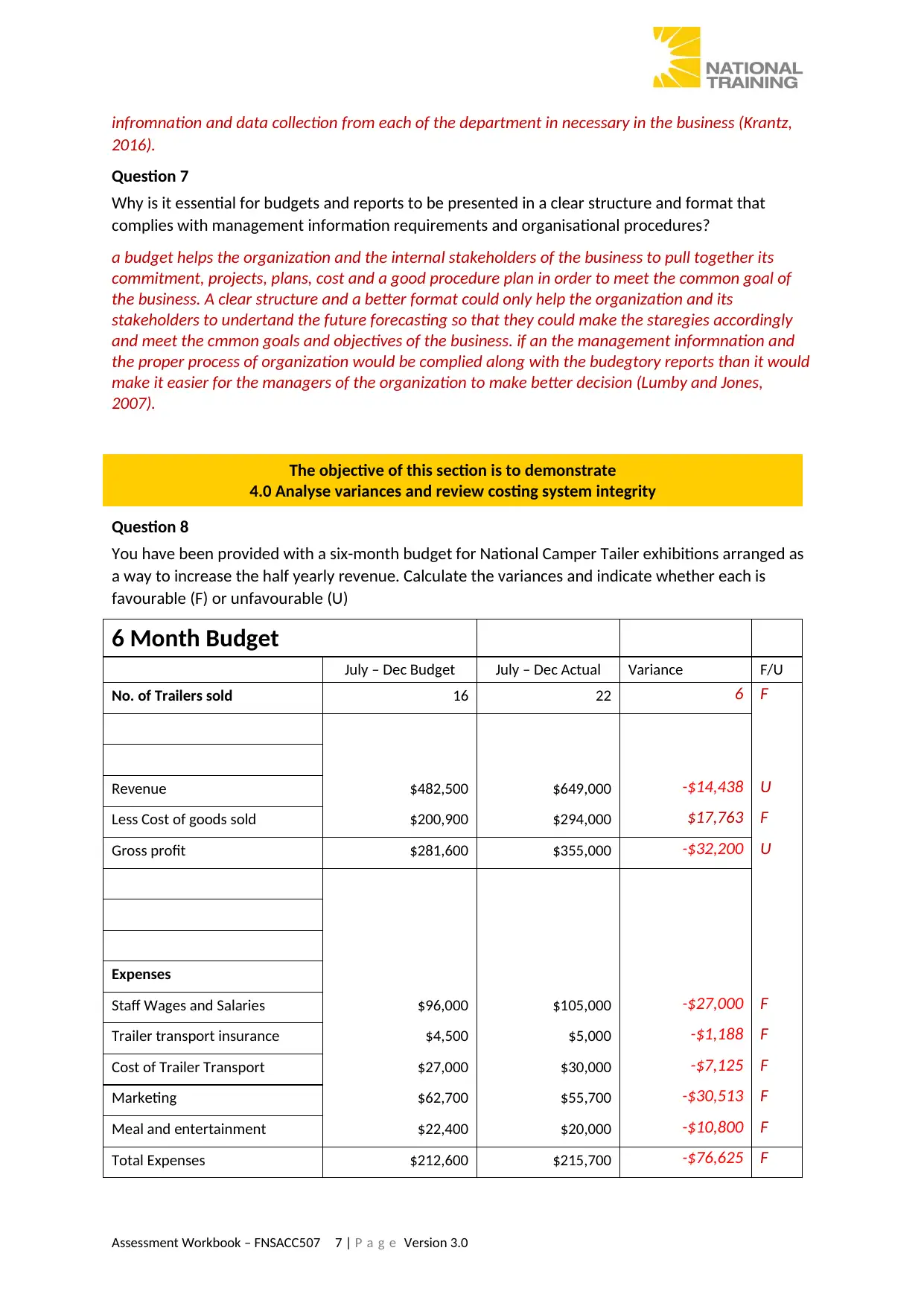

You have been provided with a six-month budget for National Camper Tailer exhibitions arranged as

a way to increase the half yearly revenue. Calculate the variances and indicate whether each is

favourable (F) or unfavourable (U)

6 Month Budget

July – Dec Budget July – Dec Actual Variance F/U

No. of Trailers sold 16 22 6 F

Revenue $482,500 $649,000 -$14,438 U

Less Cost of goods sold $200,900 $294,000 $17,763 F

Gross profit $281,600 $355,000 -$32,200 U

Expenses

Staff Wages and Salaries $96,000 $105,000 -$27,000 F

Trailer transport insurance $4,500 $5,000 -$1,188 F

Cost of Trailer Transport $27,000 $30,000 -$7,125 F

Marketing $62,700 $55,700 -$30,513 F

Meal and entertainment $22,400 $20,000 -$10,800 F

Total Expenses $212,600 $215,700 -$76,625 F

Assessment Workbook – FNSACC507 7 | P a g e Version 3.0

2016).

Question 7

Why is it essential for budgets and reports to be presented in a clear structure and format that

complies with management information requirements and organisational procedures?

a budget helps the organization and the internal stakeholders of the business to pull together its

commitment, projects, plans, cost and a good procedure plan in order to meet the common goal of

the business. A clear structure and a better format could only help the organization and its

stakeholders to undertand the future forecasting so that they could make the staregies accordingly

and meet the cmmon goals and objectives of the business. if an the management informnation and

the proper process of organization would be complied along with the budegtory reports than it would

make it easier for the managers of the organization to make better decision (Lumby and Jones,

2007).

The objective of this section is to demonstrate

4.0 Analyse variances and review costing system integrity

Question 8

You have been provided with a six-month budget for National Camper Tailer exhibitions arranged as

a way to increase the half yearly revenue. Calculate the variances and indicate whether each is

favourable (F) or unfavourable (U)

6 Month Budget

July – Dec Budget July – Dec Actual Variance F/U

No. of Trailers sold 16 22 6 F

Revenue $482,500 $649,000 -$14,438 U

Less Cost of goods sold $200,900 $294,000 $17,763 F

Gross profit $281,600 $355,000 -$32,200 U

Expenses

Staff Wages and Salaries $96,000 $105,000 -$27,000 F

Trailer transport insurance $4,500 $5,000 -$1,188 F

Cost of Trailer Transport $27,000 $30,000 -$7,125 F

Marketing $62,700 $55,700 -$30,513 F

Meal and entertainment $22,400 $20,000 -$10,800 F

Total Expenses $212,600 $215,700 -$76,625 F

Assessment Workbook – FNSACC507 7 | P a g e Version 3.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Profit $69,000 $139,300 $44,425 F

Question 9

From the variance analysis in question 8, comment on the effectiveness of NCT’s Cost Assignment

processes.

On the basis of the above calculations, it has been found that the revenue of the company

has been unfavourable but along with that, the cost level of the organization has been managed by

the business because of that the total expenses worth $ 76,625 has been lower than the estimated

expenses. It explains that the cost management o f the organization is quite effective and because of

that only, the net profit of the organization has been $ 44,425 higher than the estimated profit level

(Elton, Gruber, Brown and Goetzmann, 2009).

Question 10

How do you ensure reports are accurate, comprehensive and comply with management information

requirements and organisational practices?

In order to ensure that the reports of the organization are accurate and it complies all the required

information of the organization, it is important for the managers to identify the errors in the

recording of the transaction, manage the discrepancies in the sales invoice, supply invoice, bank

changes, payment and deposits etc. Along with that, it is also important to double check all the

invoices and receipt of the business so that the accurate reports could be prepared (Lord, 2007).

Along with that, the proper accounting standards must also be followed while preparing the reports.

The objective of this section is to demonstrate

FNSACC507 Provide management accounting information

Question 11

Identify and describe the cost behaviour characteristics for the different cost elements of a product

or service.

Cost behaviour characteristics define the nature and the reason behind incurring the cost. Mainly the

cost element of a business could be direct labour hour, total sales units, number of space used etc.

Total sales units: this is used in the business in order to examine the total COGS of each of the unit. It

defines about total units which have been sold in the business.

Direct labour hours: this is used in the business in order to examine per head labour cost. It defines

about total working hours in the business.

Number of space used: this is used in the business in order to identify the rent, electricity etc. It

defines that how much space is used by each of the unit in the business (Kaplan and Atkinson, 2015).

Question 12

Describe the principles of double entry book keeping and accrual based accounting

Double entry book keeping explains that each financial transaction impacts on two or more than two

financial elements. Thus it is important to recognize both the element and record the transaction

accordingly. The equation of double accounting system is as follows:

Assessment Workbook – FNSACC507 8 | P a g e Version 3.0

Question 9

From the variance analysis in question 8, comment on the effectiveness of NCT’s Cost Assignment

processes.

On the basis of the above calculations, it has been found that the revenue of the company

has been unfavourable but along with that, the cost level of the organization has been managed by

the business because of that the total expenses worth $ 76,625 has been lower than the estimated

expenses. It explains that the cost management o f the organization is quite effective and because of

that only, the net profit of the organization has been $ 44,425 higher than the estimated profit level

(Elton, Gruber, Brown and Goetzmann, 2009).

Question 10

How do you ensure reports are accurate, comprehensive and comply with management information

requirements and organisational practices?

In order to ensure that the reports of the organization are accurate and it complies all the required

information of the organization, it is important for the managers to identify the errors in the

recording of the transaction, manage the discrepancies in the sales invoice, supply invoice, bank

changes, payment and deposits etc. Along with that, it is also important to double check all the

invoices and receipt of the business so that the accurate reports could be prepared (Lord, 2007).

Along with that, the proper accounting standards must also be followed while preparing the reports.

The objective of this section is to demonstrate

FNSACC507 Provide management accounting information

Question 11

Identify and describe the cost behaviour characteristics for the different cost elements of a product

or service.

Cost behaviour characteristics define the nature and the reason behind incurring the cost. Mainly the

cost element of a business could be direct labour hour, total sales units, number of space used etc.

Total sales units: this is used in the business in order to examine the total COGS of each of the unit. It

defines about total units which have been sold in the business.

Direct labour hours: this is used in the business in order to examine per head labour cost. It defines

about total working hours in the business.

Number of space used: this is used in the business in order to identify the rent, electricity etc. It

defines that how much space is used by each of the unit in the business (Kaplan and Atkinson, 2015).

Question 12

Describe the principles of double entry book keeping and accrual based accounting

Double entry book keeping explains that each financial transaction impacts on two or more than two

financial elements. Thus it is important to recognize both the element and record the transaction

accordingly. The equation of double accounting system is as follows:

Assessment Workbook – FNSACC507 8 | P a g e Version 3.0

Assets = liabilities + equity (Madura, 2014)

Accrual accounting method describes that an organization must record the transaction in the period it has

incurred rather than the period in which the payment has been done or the amount has been recovered by

the business.

Question 13

Explain the key processes and procedures for recording and securely storing cash transactions

Cash transaction involves each of the cash transaction in which either cash has been paid or received

by the business. Usually, the cash transactions are recorded after measuring and evaluating the

cheques, money orders, money deposits, credit card sales, payment from the debtors, proceeds from

sales etc. Each of the documents is processed in a particular manner to evaluate the cash level of the

business. In order to secure each of the cash transaction, the computerized according is better option

in front of the business because in that case, the transaction could be protected through password

(Schlichting, 2013).

Question 14

Identify and explain the key principles and practices of preparing a budget.

A budget is a formal internal statement which is prepared in order to identify the future revenue and

expenses of business. A budget preparer has to collect the information from each of the department

in order to assure the performance of the business and make the future strategies of the business so

that the common goal of the business could be achieved. the total cost, manufacturing cost, labour

cost, manufacture overhead etc are evaluated and the flexible budget, operating budget, cash

budget, revenue budget are prepared to meet the goals of the business (Lee and Lee, 2006).

Question 15

Explain the relevance of Australian Standard: Record Management to maintaining management

accounting information.

“Record management accounting standard” acts as a code of practice to set the benchmark in order

to collect and record of the financial information. The main focus of this accounting standard is to set

a principle to record the management system, design and implement the record management

system, training in records management, monitoring of management system etc. This accounting

standard makes it very easy for the business to record and manage the financial transaction and

other information (Lumby and Jones, 2007).

Question 16

Explain the relevance of organisational policy and procedures as they apply to costing systems

Organizational policy and process play a crucial role in every business. It defines about the culture and the

philosophy of organization. It becomes important for each of the business and its employees to

understand the process of the business and meet the common goal of the business. Each of the business

defines the different process and role to each of the employees which becomes important to manage

overall performance of the business (Lee and Lee, 2006).

Assessment 2: Project

The objective of this section is to demonstrate

FNSACC507 Provide management accounting information

Assessment Workbook – FNSACC507 9 | P a g e Version 3.0

Accrual accounting method describes that an organization must record the transaction in the period it has

incurred rather than the period in which the payment has been done or the amount has been recovered by

the business.

Question 13

Explain the key processes and procedures for recording and securely storing cash transactions

Cash transaction involves each of the cash transaction in which either cash has been paid or received

by the business. Usually, the cash transactions are recorded after measuring and evaluating the

cheques, money orders, money deposits, credit card sales, payment from the debtors, proceeds from

sales etc. Each of the documents is processed in a particular manner to evaluate the cash level of the

business. In order to secure each of the cash transaction, the computerized according is better option

in front of the business because in that case, the transaction could be protected through password

(Schlichting, 2013).

Question 14

Identify and explain the key principles and practices of preparing a budget.

A budget is a formal internal statement which is prepared in order to identify the future revenue and

expenses of business. A budget preparer has to collect the information from each of the department

in order to assure the performance of the business and make the future strategies of the business so

that the common goal of the business could be achieved. the total cost, manufacturing cost, labour

cost, manufacture overhead etc are evaluated and the flexible budget, operating budget, cash

budget, revenue budget are prepared to meet the goals of the business (Lee and Lee, 2006).

Question 15

Explain the relevance of Australian Standard: Record Management to maintaining management

accounting information.

“Record management accounting standard” acts as a code of practice to set the benchmark in order

to collect and record of the financial information. The main focus of this accounting standard is to set

a principle to record the management system, design and implement the record management

system, training in records management, monitoring of management system etc. This accounting

standard makes it very easy for the business to record and manage the financial transaction and

other information (Lumby and Jones, 2007).

Question 16

Explain the relevance of organisational policy and procedures as they apply to costing systems

Organizational policy and process play a crucial role in every business. It defines about the culture and the

philosophy of organization. It becomes important for each of the business and its employees to

understand the process of the business and meet the common goal of the business. Each of the business

defines the different process and role to each of the employees which becomes important to manage

overall performance of the business (Lee and Lee, 2006).

Assessment 2: Project

The objective of this section is to demonstrate

FNSACC507 Provide management accounting information

Assessment Workbook – FNSACC507 9 | P a g e Version 3.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Project

ABC company is a transport and logistics company that provides storage and delivery services. You

are the accountant of ABC and one of your responsibilities is to oversee the budget process. The

company has 5 departments which are Human Resources, Finance, Sales and marketing, Operations,

Administration and Customer service

Some of the ABC’s company’s policy and procedures that apply to costing are as follows:

All accounts are maintained in a chart of accounts which has identification codes as follows

Assets (1,000 – 1999), liabilities= (2000 – 2999), owners’ equity = (3000 – 3999), revenue =

(4000 – 4999), cost of goods sold = (5000 – 5999), expenses = (6000 – 6999).

Before a journal entry is processed the data entry officer should

o Identify the requirements of the journal entries to be entered

o Select the accounts that should be adjusted in the chart of accounts

o Prepare the entry

o The budget prepared yearly is a fixed budget and should be prepared using a

template format provided by the management.

The total cost for wages and salaries in the budget in the Sales and Marketing department has

increased dramatically in the last two years. The management has requested you to investigate the

methods of allocating the wages costs

You are the accountant of ABC and you are responsible for preparation and overseeing the budget

process.

Question 1

Systematically code the following chart of accounts in accordance with the organisation policies and

procedures

Account Code

E.g. Cash at bank - 1010

*since cash at bank is an asset the account code has to begin with 1…)

a. Accounts Payable - 2010

b. Owner’s capital account - 3000

c. Revenue from distributions - 4000

d. GST Payable - 2020

e. Marketing expenses - 6010

f. Delivery Truck -1050

g. Inventory - 1020

h. Wages and salaries - 6020

i. Telephone expenses - 6030

j. Short Term Loan from ANZ bank - 2030

k. Buildings - 1040

l. interest expense - 6040

Assessment Workbook – FNSACC507 10 | P a g e Version 3.0

ABC company is a transport and logistics company that provides storage and delivery services. You

are the accountant of ABC and one of your responsibilities is to oversee the budget process. The

company has 5 departments which are Human Resources, Finance, Sales and marketing, Operations,

Administration and Customer service

Some of the ABC’s company’s policy and procedures that apply to costing are as follows:

All accounts are maintained in a chart of accounts which has identification codes as follows

Assets (1,000 – 1999), liabilities= (2000 – 2999), owners’ equity = (3000 – 3999), revenue =

(4000 – 4999), cost of goods sold = (5000 – 5999), expenses = (6000 – 6999).

Before a journal entry is processed the data entry officer should

o Identify the requirements of the journal entries to be entered

o Select the accounts that should be adjusted in the chart of accounts

o Prepare the entry

o The budget prepared yearly is a fixed budget and should be prepared using a

template format provided by the management.

The total cost for wages and salaries in the budget in the Sales and Marketing department has

increased dramatically in the last two years. The management has requested you to investigate the

methods of allocating the wages costs

You are the accountant of ABC and you are responsible for preparation and overseeing the budget

process.

Question 1

Systematically code the following chart of accounts in accordance with the organisation policies and

procedures

Account Code

E.g. Cash at bank - 1010

*since cash at bank is an asset the account code has to begin with 1…)

a. Accounts Payable - 2010

b. Owner’s capital account - 3000

c. Revenue from distributions - 4000

d. GST Payable - 2020

e. Marketing expenses - 6010

f. Delivery Truck -1050

g. Inventory - 1020

h. Wages and salaries - 6020

i. Telephone expenses - 6030

j. Short Term Loan from ANZ bank - 2030

k. Buildings - 1040

l. interest expense - 6040

Assessment Workbook – FNSACC507 10 | P a g e Version 3.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 2

Explain where you would obtain cost information while investigating the drivers of the dramatic

Increase in wages and salaries? Why this is important in a budget preparation?

In order to identify and evaluate the information about the drastic changes in the wages and salaries

of the business, the labour rate of the market and the requirement of the labour hours would be

studied. It would be identified that whether the more labour hours are required in the business

because of that the labour rate and salaries are getting higher drastically or the labour rate in the

market has been improved (Horngren, 2009).

Evaluation on the reasons behind drastic changes in the wages and salaries of the business is

important to prepare the budgetary reports because on the basis of that only, better budgetary

reports could be prepared and the strategies could be decided by the business on the basis of that

only.

Question 3A

Explain how you would:

Ensure structure and format of the budget you prepare are clear and comply with ABC’s

management information requirements and organisational practices?’

In order to identify and evaluate the case study of ABC, it has been found that the following budgets

must be prepared by the business in a sequence to complying the management information

requirement and the culture and practices of the organization:

Firstly, the business must identify and evaluated all the information from the different department of

the business and prepared the material purchase budget (Lord, 2007).

Further, the material required budget, cost of goods sold budget, sales budget and production

overhead and manufacturing overhead budgeted is prepared after linking the information from each

of the budget (Higgins, 2012).

The information has been identified about the wages and salaries increment and it has also been

context while preparing the budgetary reports.

Question 3B

Check the budget is accurate and comprehensive and complies with ABC’s management information

requirements and organisational practices?

The budget is an obligation which represents about the projected income and the expenses of the

business. Each organization or group has to assure that the proper format and structure has been

followed of budgetary reports so that a better report could be prepared and it could help the

management to make better decisions. In order to assure that whether the management information

has been followed in the business or not, the process of the reports must be monitored and it has

been evaluated that:

The proper information has been collected about the expenses and revenue of the business.

All the departments have provided the relevant information about the revenue and the expense.

Seasonal operations have been taken into the concern.

The historical data and the current market performance have been measured (Gapenski, 2008).

The accounting policies and the organizational procedures have been followed.

Assessment Workbook – FNSACC507 11 | P a g e Version 3.0

Explain where you would obtain cost information while investigating the drivers of the dramatic

Increase in wages and salaries? Why this is important in a budget preparation?

In order to identify and evaluate the information about the drastic changes in the wages and salaries

of the business, the labour rate of the market and the requirement of the labour hours would be

studied. It would be identified that whether the more labour hours are required in the business

because of that the labour rate and salaries are getting higher drastically or the labour rate in the

market has been improved (Horngren, 2009).

Evaluation on the reasons behind drastic changes in the wages and salaries of the business is

important to prepare the budgetary reports because on the basis of that only, better budgetary

reports could be prepared and the strategies could be decided by the business on the basis of that

only.

Question 3A

Explain how you would:

Ensure structure and format of the budget you prepare are clear and comply with ABC’s

management information requirements and organisational practices?’

In order to identify and evaluate the case study of ABC, it has been found that the following budgets

must be prepared by the business in a sequence to complying the management information

requirement and the culture and practices of the organization:

Firstly, the business must identify and evaluated all the information from the different department of

the business and prepared the material purchase budget (Lord, 2007).

Further, the material required budget, cost of goods sold budget, sales budget and production

overhead and manufacturing overhead budgeted is prepared after linking the information from each

of the budget (Higgins, 2012).

The information has been identified about the wages and salaries increment and it has also been

context while preparing the budgetary reports.

Question 3B

Check the budget is accurate and comprehensive and complies with ABC’s management information

requirements and organisational practices?

The budget is an obligation which represents about the projected income and the expenses of the

business. Each organization or group has to assure that the proper format and structure has been

followed of budgetary reports so that a better report could be prepared and it could help the

management to make better decisions. In order to assure that whether the management information

has been followed in the business or not, the process of the reports must be monitored and it has

been evaluated that:

The proper information has been collected about the expenses and revenue of the business.

All the departments have provided the relevant information about the revenue and the expense.

Seasonal operations have been taken into the concern.

The historical data and the current market performance have been measured (Gapenski, 2008).

The accounting policies and the organizational procedures have been followed.

Assessment Workbook – FNSACC507 11 | P a g e Version 3.0

the wages and salaries increment rate has been studied and the improvement have been seen

accordingly (Hillier, Grinblatt and Titman, 2011).

Assessment Workbook – FNSACC507 12 | P a g e Version 3.0

accordingly (Hillier, Grinblatt and Titman, 2011).

Assessment Workbook – FNSACC507 12 | P a g e Version 3.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.