FNSACC601 & FNSACC603: Tax Calculations, Trust & Partnership Income

VerifiedAdded on 2023/06/15

|29

|5493

|117

Homework Assignment

AI Summary

This assignment provides solutions to various taxation questions covering individual income tax calculations, trust income distributions, and partnership income allocations. It addresses scenarios involving prescribed persons, inter vivos trusts, and partnership agreements. The assignment includes calculations for assessable income, tax payable by trustees and individuals, and reconciliation of taxable income for companies. Additionally, it covers franking account preparation, average income calculations for primary producers, and assessable contributions to superannuation funds. The document also touches on income attributable to club members. Desklib offers this assignment as a study resource, providing students with access to solved assignments and past papers to aid their learning.

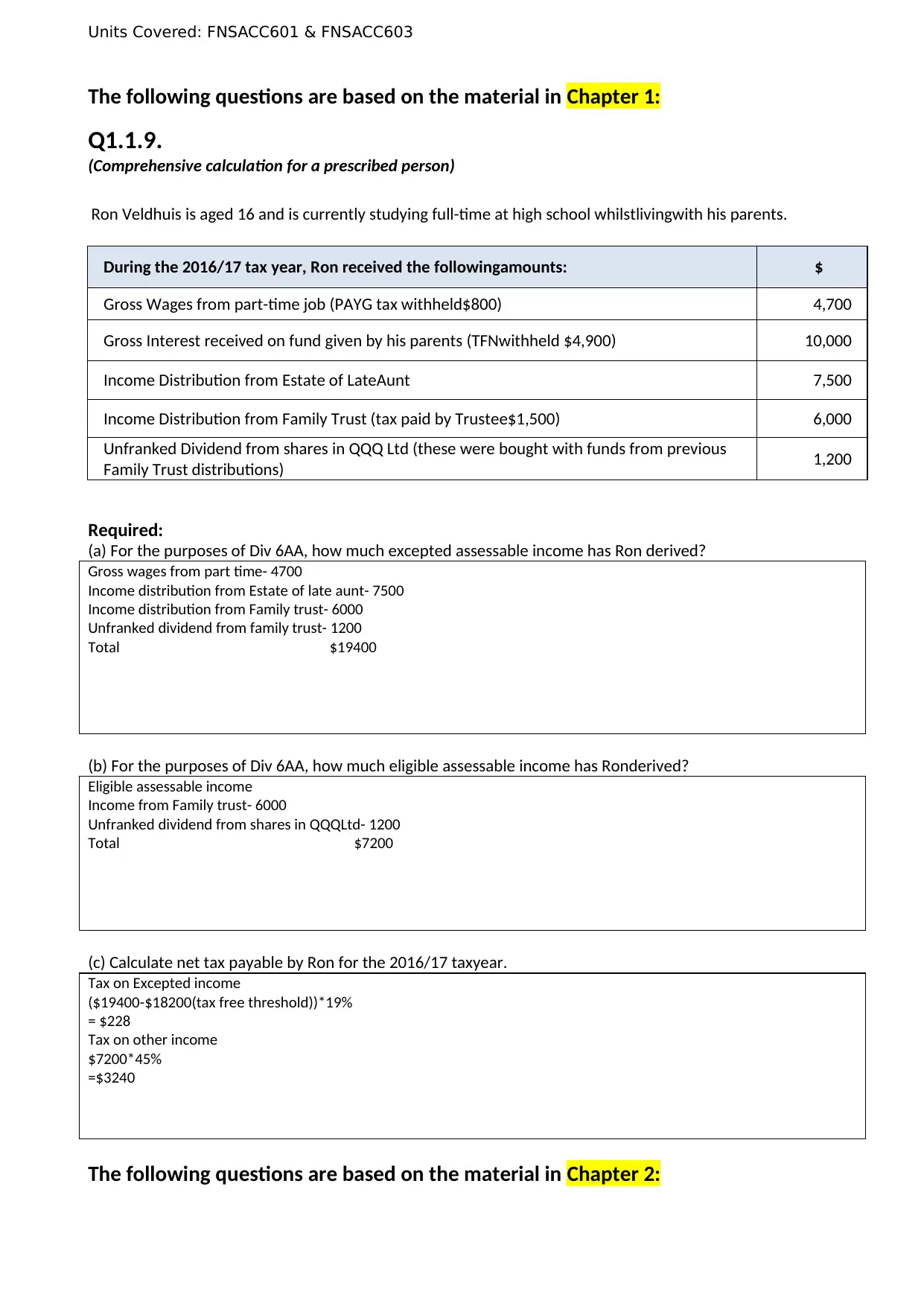

Units Covered: FNSACC601 & FNSACC603

The following questions are based on the material in Chapter 1:

Q1.1.9.

(Comprehensive calculation for a prescribed person)

Ron Veldhuis is aged 16 and is currently studying full-time at high school whilstlivingwith his parents.

During the 2016/17 tax year, Ron received the followingamounts: $

Gross Wages from part-time job (PAYG tax withheld$800) 4,700

Gross Interest received on fund given by his parents (TFNwithheld $4,900) 10,000

Income Distribution from Estate of LateAunt 7,500

Income Distribution from Family Trust (tax paid by Trustee$1,500) 6,000

Unfranked Dividend from shares in QQQ Ltd (these were bought with funds from previous

Family Trust distributions) 1,200

Required:

(a) For the purposes of Div 6AA, how much excepted assessable income has Ron derived?

Gross wages from part time- 4700

Income distribution from Estate of late aunt- 7500

Income distribution from Family trust- 6000

Unfranked dividend from family trust- 1200

Total $19400

(b) For the purposes of Div 6AA, how much eligible assessable income has Ronderived?

Eligible assessable income

Income from Family trust- 6000

Unfranked dividend from shares in QQQLtd- 1200

Total $7200

(c) Calculate net tax payable by Ron for the 2016/17 taxyear.

Tax on Excepted income

($19400-$18200(tax free threshold))*19%

= $228

Tax on other income

$7200*45%

=$3240

The following questions are based on the material in Chapter 2:

The following questions are based on the material in Chapter 1:

Q1.1.9.

(Comprehensive calculation for a prescribed person)

Ron Veldhuis is aged 16 and is currently studying full-time at high school whilstlivingwith his parents.

During the 2016/17 tax year, Ron received the followingamounts: $

Gross Wages from part-time job (PAYG tax withheld$800) 4,700

Gross Interest received on fund given by his parents (TFNwithheld $4,900) 10,000

Income Distribution from Estate of LateAunt 7,500

Income Distribution from Family Trust (tax paid by Trustee$1,500) 6,000

Unfranked Dividend from shares in QQQ Ltd (these were bought with funds from previous

Family Trust distributions) 1,200

Required:

(a) For the purposes of Div 6AA, how much excepted assessable income has Ron derived?

Gross wages from part time- 4700

Income distribution from Estate of late aunt- 7500

Income distribution from Family trust- 6000

Unfranked dividend from family trust- 1200

Total $19400

(b) For the purposes of Div 6AA, how much eligible assessable income has Ronderived?

Eligible assessable income

Income from Family trust- 6000

Unfranked dividend from shares in QQQLtd- 1200

Total $7200

(c) Calculate net tax payable by Ron for the 2016/17 taxyear.

Tax on Excepted income

($19400-$18200(tax free threshold))*19%

= $228

Tax on other income

$7200*45%

=$3240

The following questions are based on the material in Chapter 2:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC601 & FNSACC603

Q2.2.15

(Comprehensive, inter vivostrust)

The Alberts Family Trust, an inter vivos trust, had the followingbeneficiaries:

Candy (aged 45; entitled to 40% of trustincome)

Dandy (aged 30; bankrupt; entitled to 35% of trustincome)

Landy (aged 17; entitled to 20% of trustincome)

The remainder of each year's income was to be retained or distributed at the Trustee'sdiscretion.

During the 2016/17 tax year trust income was $195,000.

A discretionary amountof$7,000 was paid to Landy (this amount was in addition to Landy’s entitlement under

the TrustDeed).

The trust also had losses of $15,000 in the 2015/16 tax year. These were to be met out of the trustincome.

Landy also received interest of $38,000 during the 2016/17 tax year from investments given to him by

hisparents.

Landy is single and is not covered by private healthinsurance.

Required:

a. Complete the following table (covering all beneficiaries)nominating:

Name of theBENEFICIARY

Whether or not the beneficiary is PRESENTLYENTITLED

Whether or not the beneficiary is under a LEGALDISABILITY

WHO IS ASSESSED on eachamount

Which sections of the Act apply to make the incomeassessable

The amount retained ordistributed.

Beneficiary Presently

entitled?

(Yes/No)

Legal

disability?

(Yes/No)

Who is assessed?

(Beneficiary or

Trustee)

Section(s)

Applicable

Amount $

Candy No No Trustee Section 97 72000

Dandy No Yes Beneficiary Section 97 63000

Landy No Yes Beneficiary Section 97 43000

Balance

Total $178000

b. Calculate tax payable by the trustee on behalf of Dandy, Landy and the balance of trust net income.

Q2.2.15

(Comprehensive, inter vivostrust)

The Alberts Family Trust, an inter vivos trust, had the followingbeneficiaries:

Candy (aged 45; entitled to 40% of trustincome)

Dandy (aged 30; bankrupt; entitled to 35% of trustincome)

Landy (aged 17; entitled to 20% of trustincome)

The remainder of each year's income was to be retained or distributed at the Trustee'sdiscretion.

During the 2016/17 tax year trust income was $195,000.

A discretionary amountof$7,000 was paid to Landy (this amount was in addition to Landy’s entitlement under

the TrustDeed).

The trust also had losses of $15,000 in the 2015/16 tax year. These were to be met out of the trustincome.

Landy also received interest of $38,000 during the 2016/17 tax year from investments given to him by

hisparents.

Landy is single and is not covered by private healthinsurance.

Required:

a. Complete the following table (covering all beneficiaries)nominating:

Name of theBENEFICIARY

Whether or not the beneficiary is PRESENTLYENTITLED

Whether or not the beneficiary is under a LEGALDISABILITY

WHO IS ASSESSED on eachamount

Which sections of the Act apply to make the incomeassessable

The amount retained ordistributed.

Beneficiary Presently

entitled?

(Yes/No)

Legal

disability?

(Yes/No)

Who is assessed?

(Beneficiary or

Trustee)

Section(s)

Applicable

Amount $

Candy No No Trustee Section 97 72000

Dandy No Yes Beneficiary Section 97 63000

Landy No Yes Beneficiary Section 97 43000

Balance

Total $178000

b. Calculate tax payable by the trustee on behalf of Dandy, Landy and the balance of trust net income.

Units Covered: FNSACC601 & FNSACC603

Tax payable by Trustee on behalf of Dandy:

Assessable income*45%

72000*45%= $32400

Tax payable by Trustee on behalf of Landy:

Assessable income

Income from trust- 43000

Total assessable income- $43000

Assessable income*45%

= $43000*45%

= $19350

Tax payable by Trustee on balance of trust net income:

Assessable income

Balance of trust income- 2000

Assessable income*45%

= $2000*45%

= $900

c. Calculate tax payable byLandy (only).

Assessable income

Income from trust- 43000

Income from investments- 38000

Total assessable income- $81000

Assessable income*45%

= $81000*45%

= $36450

The following questions are based on the material in Chapter 3:

Tax payable by Trustee on behalf of Dandy:

Assessable income*45%

72000*45%= $32400

Tax payable by Trustee on behalf of Landy:

Assessable income

Income from trust- 43000

Total assessable income- $43000

Assessable income*45%

= $43000*45%

= $19350

Tax payable by Trustee on balance of trust net income:

Assessable income

Balance of trust income- 2000

Assessable income*45%

= $2000*45%

= $900

c. Calculate tax payable byLandy (only).

Assessable income

Income from trust- 43000

Income from investments- 38000

Total assessable income- $81000

Assessable income*45%

= $81000*45%

= $36450

The following questions are based on the material in Chapter 3:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Units Covered: FNSACC601 & FNSACC603

Q3.3.3

(Allocation of Partnership Net Income)

Sue, Prue, Lou and Emmet operate a transport company in the ratio 4:3:2:1.

Their assessable income for the 2016/17 tax year amounted to $780,000 while they had $300,000 of

deductions.

Their partnership agreement states that all profits and losses are to be shared in the ratio 4:3:2:1 after

adjusting for partner’s salaries, travel allowances and interest on capital.

The following data was extracted from their financial records:

Interest on Capital

Sue $ 12,000

Prue 15,000

Lou 5,000

Emmet 3,000

Partner’s Salaries

Sue 65,000

Prue 50,000

Emmet 20,000

Travel Allowances

Sue 4,000

Emmet 6,000

Required:

Based on the above information, complete the table calculating each partner’s share of partnership net

income under the terms of the partnership agreement.

Sue Prue Lou Emmet Total $

Interest on capital 12000 15000 5000 3000 35000

Partners’ salaries 65000 50000 20000 135000

Travel allowances 4000 6000 10000

Share of Adjusted Net Income 109091 81819 54545 27273 300000

Total $ 190091 146819 104545 83273 480000

Q3.3.3

(Allocation of Partnership Net Income)

Sue, Prue, Lou and Emmet operate a transport company in the ratio 4:3:2:1.

Their assessable income for the 2016/17 tax year amounted to $780,000 while they had $300,000 of

deductions.

Their partnership agreement states that all profits and losses are to be shared in the ratio 4:3:2:1 after

adjusting for partner’s salaries, travel allowances and interest on capital.

The following data was extracted from their financial records:

Interest on Capital

Sue $ 12,000

Prue 15,000

Lou 5,000

Emmet 3,000

Partner’s Salaries

Sue 65,000

Prue 50,000

Emmet 20,000

Travel Allowances

Sue 4,000

Emmet 6,000

Required:

Based on the above information, complete the table calculating each partner’s share of partnership net

income under the terms of the partnership agreement.

Sue Prue Lou Emmet Total $

Interest on capital 12000 15000 5000 3000 35000

Partners’ salaries 65000 50000 20000 135000

Travel allowances 4000 6000 10000

Share of Adjusted Net Income 109091 81819 54545 27273 300000

Total $ 190091 146819 104545 83273 480000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC601 & FNSACC603

The following questions are based on the material in Chapter 4:

Q4.4.21

(Reconciliation of taxableincome)

Trash Converters Limited, a small business entity, has prepared an income statement for2016/17:

$ $

GROSSPROFIT 1,624,000

Add: OTHERINCOME

UnfrankedDividend 2,300

Fully Franked Dividends (company tax rate 30%) 7,700

Net Dividends from Spain - note1 32,000

Gain on Sale of Shares - note2 2,000 44,000

TOTAL OPERATING INCOME 1,668,000

EXPENSES

Depreciation - note 3 34,000

Fringe BenefitsTax 48,000

Payroll Tax 46,900

Superannuation - note4 75,000

PAYG Instalments Paid - note5 92,000

Other DeductibleExpenditure 965,000 1,260,900

NETPROFIT 407,100

Note 1 The dividends from Spain have had $8,000 of tax withheld.

Note 2 Shares sold during the year were acquired in 1984 as an investment.

Note 3 Decline in value deduction is calculated as $28,000.

Note 4 Superannuation includes an amount of $30,000 paid to a director's spouse. This

$30,000 amount is deemed to be excessive.

Note 5 All of the PAYG tax instalments relate to the current year.

Required:

a. Complete the table reconciling net profit with taxable income for the 2016/17 taxyear.

b. Calculate net tax payable by the company for the 2016/17 taxyear. (For the purpose of this exercise,

assume a 27.5% small business entity company income tax rate, as per chapter 4.3 of your textbook).

The following questions are based on the material in Chapter 4:

Q4.4.21

(Reconciliation of taxableincome)

Trash Converters Limited, a small business entity, has prepared an income statement for2016/17:

$ $

GROSSPROFIT 1,624,000

Add: OTHERINCOME

UnfrankedDividend 2,300

Fully Franked Dividends (company tax rate 30%) 7,700

Net Dividends from Spain - note1 32,000

Gain on Sale of Shares - note2 2,000 44,000

TOTAL OPERATING INCOME 1,668,000

EXPENSES

Depreciation - note 3 34,000

Fringe BenefitsTax 48,000

Payroll Tax 46,900

Superannuation - note4 75,000

PAYG Instalments Paid - note5 92,000

Other DeductibleExpenditure 965,000 1,260,900

NETPROFIT 407,100

Note 1 The dividends from Spain have had $8,000 of tax withheld.

Note 2 Shares sold during the year were acquired in 1984 as an investment.

Note 3 Decline in value deduction is calculated as $28,000.

Note 4 Superannuation includes an amount of $30,000 paid to a director's spouse. This

$30,000 amount is deemed to be excessive.

Note 5 All of the PAYG tax instalments relate to the current year.

Required:

a. Complete the table reconciling net profit with taxable income for the 2016/17 taxyear.

b. Calculate net tax payable by the company for the 2016/17 taxyear. (For the purpose of this exercise,

assume a 27.5% small business entity company income tax rate, as per chapter 4.3 of your textbook).

Units Covered: FNSACC601 & FNSACC603

4 a. and 4 b.

$ $

Net Profit per income statement $407100

Add:

Franking Credits $3300

Foreign Tax – Spain $8000

Accounting Depreciation $34000

Superannuation $45000

PAYG instalments $92000 $182300

$224800

Less:

Decline in Value $28000

Accounting Gain on Shares $2000 $30000

Taxable Income $194800

Tax on Taxable Income 53570 $53570

Less:

Franking Tax Offset $2310

PAYG Instalments $17000

Foreign Income Tax Offset – tax paid $8000 $27310

Tax Payable 26260 $26260

References

https://www.ato.gov.au/Print-publications/Guide-to-capital-gains-tax-

2012-13/?page=8

4 a. and 4 b.

$ $

Net Profit per income statement $407100

Add:

Franking Credits $3300

Foreign Tax – Spain $8000

Accounting Depreciation $34000

Superannuation $45000

PAYG instalments $92000 $182300

$224800

Less:

Decline in Value $28000

Accounting Gain on Shares $2000 $30000

Taxable Income $194800

Tax on Taxable Income 53570 $53570

Less:

Franking Tax Offset $2310

PAYG Instalments $17000

Foreign Income Tax Offset – tax paid $8000 $27310

Tax Payable 26260 $26260

References

https://www.ato.gov.au/Print-publications/Guide-to-capital-gains-tax-

2012-13/?page=8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Units Covered: FNSACC601 & FNSACC603

Q5.4.27

(FrankingAccount)

Rudimentary Pty Ltd, a corporate tax entity, has the following transactions for the 2016/17 taxyear:

Date Transaction $

30/06/16 Balance Nil

15/10/16 PAYG InstalmentPaid 14,000

15/12/16 2015/16 Tax RefundReceived 9,500

12/03/17 Fully Franked DividendReceived 3,500

08/05/17 Fully Franked DividendPaid 7,000

Note – the benchmark franking percentage is100%.

Required: Prepare the franking account for the 2016/17 taxyear.

Date Transaction Debit Credit Balance

(state if DR or CR)

1/7/16 Opening Balance 0

15/10/16 PAYG Instalment paid 14000 14000

15/12/16 2015/16 Tax refund 9500 4500

12/03/17 Full franked dividend received 3500 8000

08/05/17 Fully Franked dividend paid 7000 1000

Reference

https://www.ato.gov.au/Business/Imputation/Paying-dividends-and-

other-distributions/Franking-account/

Q5.4.27

(FrankingAccount)

Rudimentary Pty Ltd, a corporate tax entity, has the following transactions for the 2016/17 taxyear:

Date Transaction $

30/06/16 Balance Nil

15/10/16 PAYG InstalmentPaid 14,000

15/12/16 2015/16 Tax RefundReceived 9,500

12/03/17 Fully Franked DividendReceived 3,500

08/05/17 Fully Franked DividendPaid 7,000

Note – the benchmark franking percentage is100%.

Required: Prepare the franking account for the 2016/17 taxyear.

Date Transaction Debit Credit Balance

(state if DR or CR)

1/7/16 Opening Balance 0

15/10/16 PAYG Instalment paid 14000 14000

15/12/16 2015/16 Tax refund 9500 4500

12/03/17 Full franked dividend received 3500 8000

08/05/17 Fully Franked dividend paid 7000 1000

Reference

https://www.ato.gov.au/Business/Imputation/Paying-dividends-and-

other-distributions/Franking-account/

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC601 & FNSACC603

The following questions are based on the material in Chapter 5:

Q6.5.1

(AverageIncome)

Ernie Wombat is a primary producer who commenced business in 2011/12. The following data relates to

Ernie’s first 6 years oftrading:

Year AssessableIncome Deductions

2011/12 $32,000 $15,000

2012/13 35,000 20,000

2013/14 31,000 39,000

2014/15 42,000 21,000

2015/16 45,000 22,000

2016/17 51,000 25,000

All assessable income and deductions are from primaryproduction.

The deductions do not include any amounts that may be deductible for losses of previousyears.

Required:

a. Calculate Ernie’s taxable income for each taxyear.

b. Calculate Ernie’s average income for each taxyear.

Year Taxable Income Average Income Notes (if any)

2011/12 17000 8500

2012/13 15000 16000

2013/14 -8000 3500

2014/15 21000 10500

2015/16 23000 22000

2016/17 26000 24500

The following questions are based on the material in Chapter 5:

Q6.5.1

(AverageIncome)

Ernie Wombat is a primary producer who commenced business in 2011/12. The following data relates to

Ernie’s first 6 years oftrading:

Year AssessableIncome Deductions

2011/12 $32,000 $15,000

2012/13 35,000 20,000

2013/14 31,000 39,000

2014/15 42,000 21,000

2015/16 45,000 22,000

2016/17 51,000 25,000

All assessable income and deductions are from primaryproduction.

The deductions do not include any amounts that may be deductible for losses of previousyears.

Required:

a. Calculate Ernie’s taxable income for each taxyear.

b. Calculate Ernie’s average income for each taxyear.

Year Taxable Income Average Income Notes (if any)

2011/12 17000 8500

2012/13 15000 16000

2013/14 -8000 3500

2014/15 21000 10500

2015/16 23000 22000

2016/17 26000 24500

Units Covered: FNSACC601 & FNSACC603

Q7.5.5.

(Tax calculation under averaging)

Rikki Teabridge had the following income during the 2016/17 taxyear:

Net Business Income from Primary Production $ 35,000

Gross Wages from part-time job at local supermarket $20,000

Rikki’s average income was$20,000.

Rikki had no other assessable income ordeductions.

PAYG tax of $2,000 was withheld from Rikki’swages.

Rikki is covered by adequate private healthinsurance.

Required:

Complete the following statement showing Rikki’s tax payable for the 2016/17 taxyearincluding any

averagingadjustment.

Notes/Workings (if any)

Tax on Average Income

Tax on $ 20000*19% $3800

Comparison of Tax Rate 30%

Gross Averaging Amount

Tax on $ @ ordinary rates 55000*32.5% $17875

Tax on $ @ comparison rates 55000*30% $16500

$17187.5

Averaging Component $17187.5

Averaging Adjustment Tax Offset $2000

Tax Payable Calculation

Tax on $ $21675

Less Averaging Tax Offset $28

Less Low Income Tax Offset $1375

Add Medicare Levy $358

Less PAYG Withheld $2000

= Tax Payable $17914

Q8.5.9

Q7.5.5.

(Tax calculation under averaging)

Rikki Teabridge had the following income during the 2016/17 taxyear:

Net Business Income from Primary Production $ 35,000

Gross Wages from part-time job at local supermarket $20,000

Rikki’s average income was$20,000.

Rikki had no other assessable income ordeductions.

PAYG tax of $2,000 was withheld from Rikki’swages.

Rikki is covered by adequate private healthinsurance.

Required:

Complete the following statement showing Rikki’s tax payable for the 2016/17 taxyearincluding any

averagingadjustment.

Notes/Workings (if any)

Tax on Average Income

Tax on $ 20000*19% $3800

Comparison of Tax Rate 30%

Gross Averaging Amount

Tax on $ @ ordinary rates 55000*32.5% $17875

Tax on $ @ comparison rates 55000*30% $16500

$17187.5

Averaging Component $17187.5

Averaging Adjustment Tax Offset $2000

Tax Payable Calculation

Tax on $ $21675

Less Averaging Tax Offset $28

Less Low Income Tax Offset $1375

Add Medicare Levy $358

Less PAYG Withheld $2000

= Tax Payable $17914

Q8.5.9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Units Covered: FNSACC601 & FNSACC603

(Trading account, average cost)

Clyde Wishbone breeds and sells sheep. During the 2016/17 year records disclosed the following:

Quantity Value ($)

Sheep on Hand – 30 June2016 8,200 47,900

Purchases 500 9,200

NaturalIncrease 2,900

Sales 4,300 92,400

Rations 100

Deaths 300

Clyde chooses to use the prescribed value for natural increase and average cost for rations and closingstock.

Required:

Prepare the average cost calculations and the trading account for the 2016/17 taxyear.

Average Cost Calculations

Qty. of Sheep $

Opening Stock 8200 $47900

Purchases 500 $9200

Natural Increase @ prescribed value 2900 $2895

Total 11600 $59995

Average Cost of one sheep $5.17

Average Costof Rations Qty Sheep for rations 100 $5.17

Average Cost of Closing Stock Qty Sheep at Closing Stock $21.48

Sheep Trading Account

Qty. $ Qty. $

Opening Stock 8200 47900 Sales 4300 92400

Purchases 500 9200 Rations 100 517

Natural Increase 2900 2895 Deaths 300 1551

Gross Profit 182685 Closing Stock 6900 148212

Total Total 242680

The following questions are based on the material in Chapter 6:

Q9.6.3.

(Assessablecontributions)

(Trading account, average cost)

Clyde Wishbone breeds and sells sheep. During the 2016/17 year records disclosed the following:

Quantity Value ($)

Sheep on Hand – 30 June2016 8,200 47,900

Purchases 500 9,200

NaturalIncrease 2,900

Sales 4,300 92,400

Rations 100

Deaths 300

Clyde chooses to use the prescribed value for natural increase and average cost for rations and closingstock.

Required:

Prepare the average cost calculations and the trading account for the 2016/17 taxyear.

Average Cost Calculations

Qty. of Sheep $

Opening Stock 8200 $47900

Purchases 500 $9200

Natural Increase @ prescribed value 2900 $2895

Total 11600 $59995

Average Cost of one sheep $5.17

Average Costof Rations Qty Sheep for rations 100 $5.17

Average Cost of Closing Stock Qty Sheep at Closing Stock $21.48

Sheep Trading Account

Qty. $ Qty. $

Opening Stock 8200 47900 Sales 4300 92400

Purchases 500 9200 Rations 100 517

Natural Increase 2900 2895 Deaths 300 1551

Gross Profit 182685 Closing Stock 6900 148212

Total Total 242680

The following questions are based on the material in Chapter 6:

Q9.6.3.

(Assessablecontributions)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC601 & FNSACC603

The Spotless Superannuation Fund is a complying superannuation fund. The fund received the following

contributions:

July 2016 Contributions from contributing employer relatingto2015/16 $27,800

Sep2016 Superannuation Guarantee Shortfall received from ATO 11,400

Oct2016 Contributions from employer relating to Sept 2016 quarter 34,500

Jan2017 Contributions from employer relating to Dec 2016 quarter 36,100

Apr 2017 Contributions from employer relating to March 2017 quarter 27,450

July 2017 Contributions from employer relating to June 2017 quarter 19,320

All of the above amounts related to members who have supplied their TFN.

There was a further $8,340 of superannuation accrued and payable by the contributing employer in relation

to 2016/17 but not yet received by the fund.

Required:

Calculate the fund’s assessable income from contributions for the2016/17 taxyear.

Contributions from contributing employer relatingto2015/16- 27800

Superannuation Guarantee Shortfall received from ATO- 11400

Contributions from employer relating to Sept 2016 quarter-34500

Contributions from employer relating to Dec 2016 quarter-36100

Contributions from employer relating to March 2017 quarter-27450

Contributions from employer relating to June 2017 quarter-19320

Total 156570

Less: accrued 8340

= 148230

Q10.6.5

(Assessable income, ordinaryincome)

The Blowhard Superannuation Fund, a complying fund, received the following amounts during the 2016/17 tax

year:

Unfranked Dividends from listed companies $12,450

The Spotless Superannuation Fund is a complying superannuation fund. The fund received the following

contributions:

July 2016 Contributions from contributing employer relatingto2015/16 $27,800

Sep2016 Superannuation Guarantee Shortfall received from ATO 11,400

Oct2016 Contributions from employer relating to Sept 2016 quarter 34,500

Jan2017 Contributions from employer relating to Dec 2016 quarter 36,100

Apr 2017 Contributions from employer relating to March 2017 quarter 27,450

July 2017 Contributions from employer relating to June 2017 quarter 19,320

All of the above amounts related to members who have supplied their TFN.

There was a further $8,340 of superannuation accrued and payable by the contributing employer in relation

to 2016/17 but not yet received by the fund.

Required:

Calculate the fund’s assessable income from contributions for the2016/17 taxyear.

Contributions from contributing employer relatingto2015/16- 27800

Superannuation Guarantee Shortfall received from ATO- 11400

Contributions from employer relating to Sept 2016 quarter-34500

Contributions from employer relating to Dec 2016 quarter-36100

Contributions from employer relating to March 2017 quarter-27450

Contributions from employer relating to June 2017 quarter-19320

Total 156570

Less: accrued 8340

= 148230

Q10.6.5

(Assessable income, ordinaryincome)

The Blowhard Superannuation Fund, a complying fund, received the following amounts during the 2016/17 tax

year:

Unfranked Dividends from listed companies $12,450

Units Covered: FNSACC601 & FNSACC603

Franked Dividends from listed companies (Fullyfranked. Company Tax rate 30%) 20,300

Interest from cash managementaccount 8,250

Proceeds from redemption of term deposits (includes principalof$50,000) 59,400

Interest from at-call deposit (net of $4,900 TFN taxwithheld) 5,100

Interest from investments segregated to meet the payment of current income

stream benefits

35,000

Required:

Calculate the fund’s assessable income from investments for the2016/17 taxyear.

Unfranked Dividends from listed companies-12450

Franked Dividends from listed companies-20300

Interest from cash managementaccount-8250

Proceeds from redemption of term deposits-59400

Interest from at-call deposit-5100

Interest from investments-35000

Total= 140500

The following questions are based on the material in Chapter 7:

Q11.7.3

(Calculation of income attributable to members)

Dockside Rowers Club disclosed the following data for the 2016/17 financialyear:

DaysOpen 361

Financialmembers 900

Franked Dividends from listed companies (Fullyfranked. Company Tax rate 30%) 20,300

Interest from cash managementaccount 8,250

Proceeds from redemption of term deposits (includes principalof$50,000) 59,400

Interest from at-call deposit (net of $4,900 TFN taxwithheld) 5,100

Interest from investments segregated to meet the payment of current income

stream benefits

35,000

Required:

Calculate the fund’s assessable income from investments for the2016/17 taxyear.

Unfranked Dividends from listed companies-12450

Franked Dividends from listed companies-20300

Interest from cash managementaccount-8250

Proceeds from redemption of term deposits-59400

Interest from at-call deposit-5100

Interest from investments-35000

Total= 140500

The following questions are based on the material in Chapter 7:

Q11.7.3

(Calculation of income attributable to members)

Dockside Rowers Club disclosed the following data for the 2016/17 financialyear:

DaysOpen 361

Financialmembers 900

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.