Queensford College: FNSACC607 Evaluate Business Performance Project

VerifiedAdded on 2023/01/04

|24

|4298

|47

Project

AI Summary

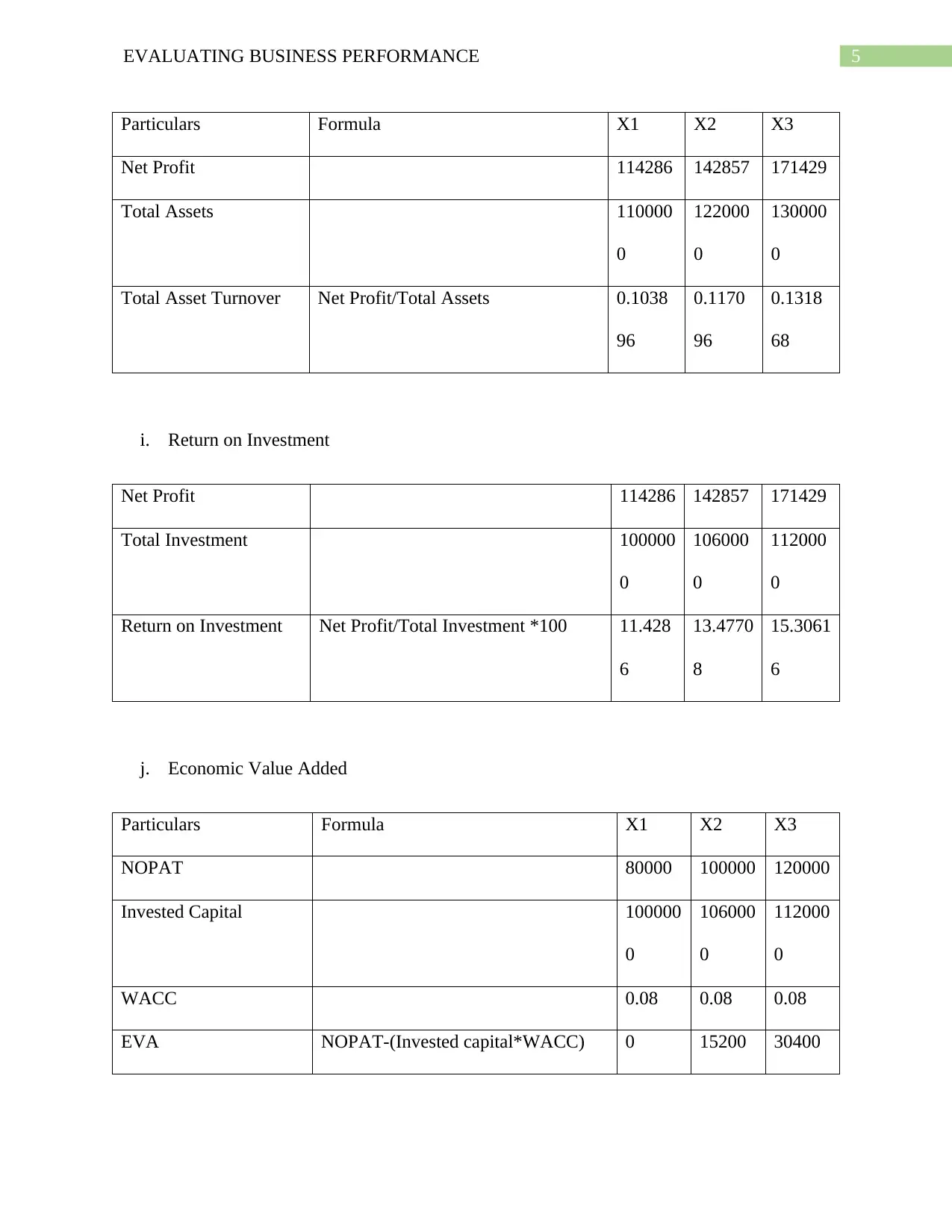

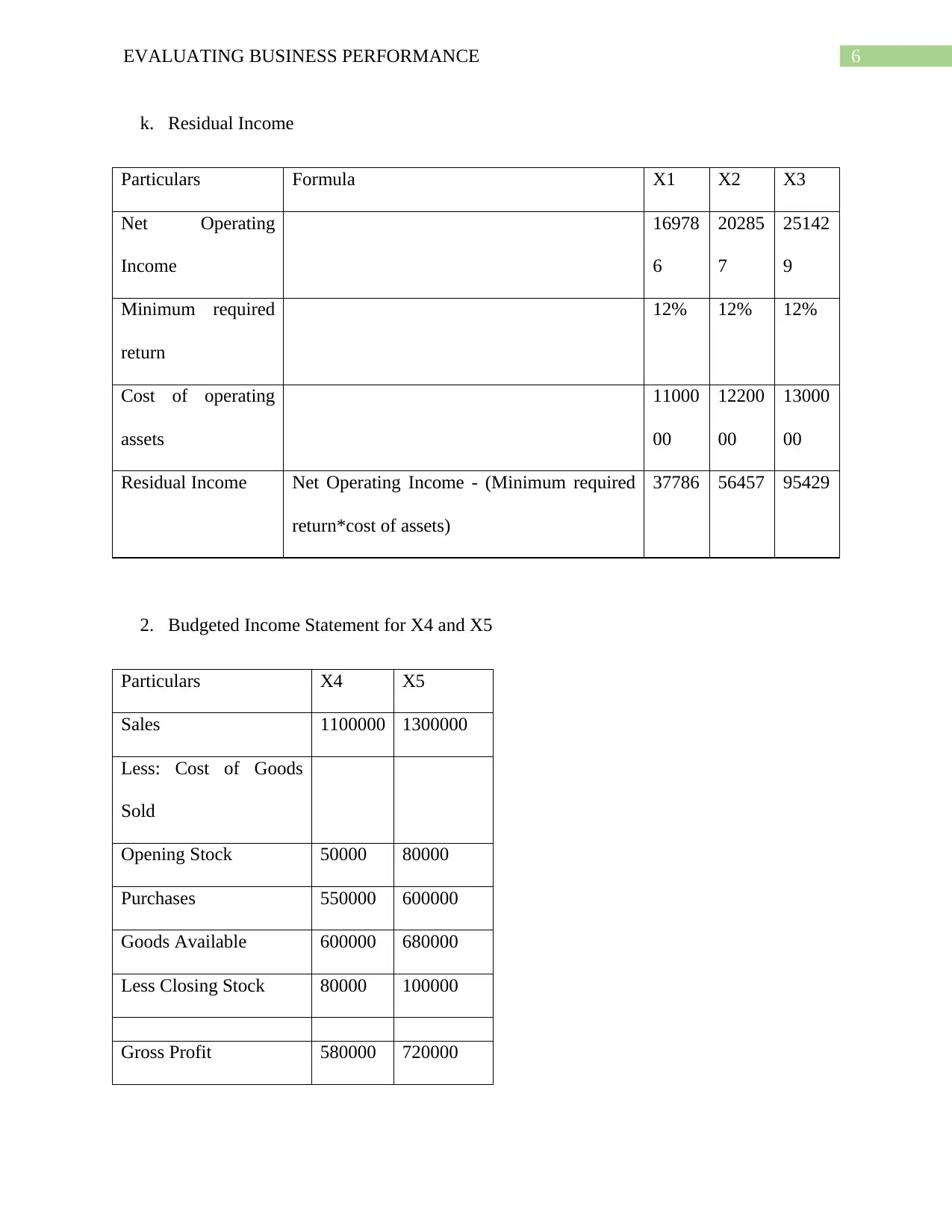

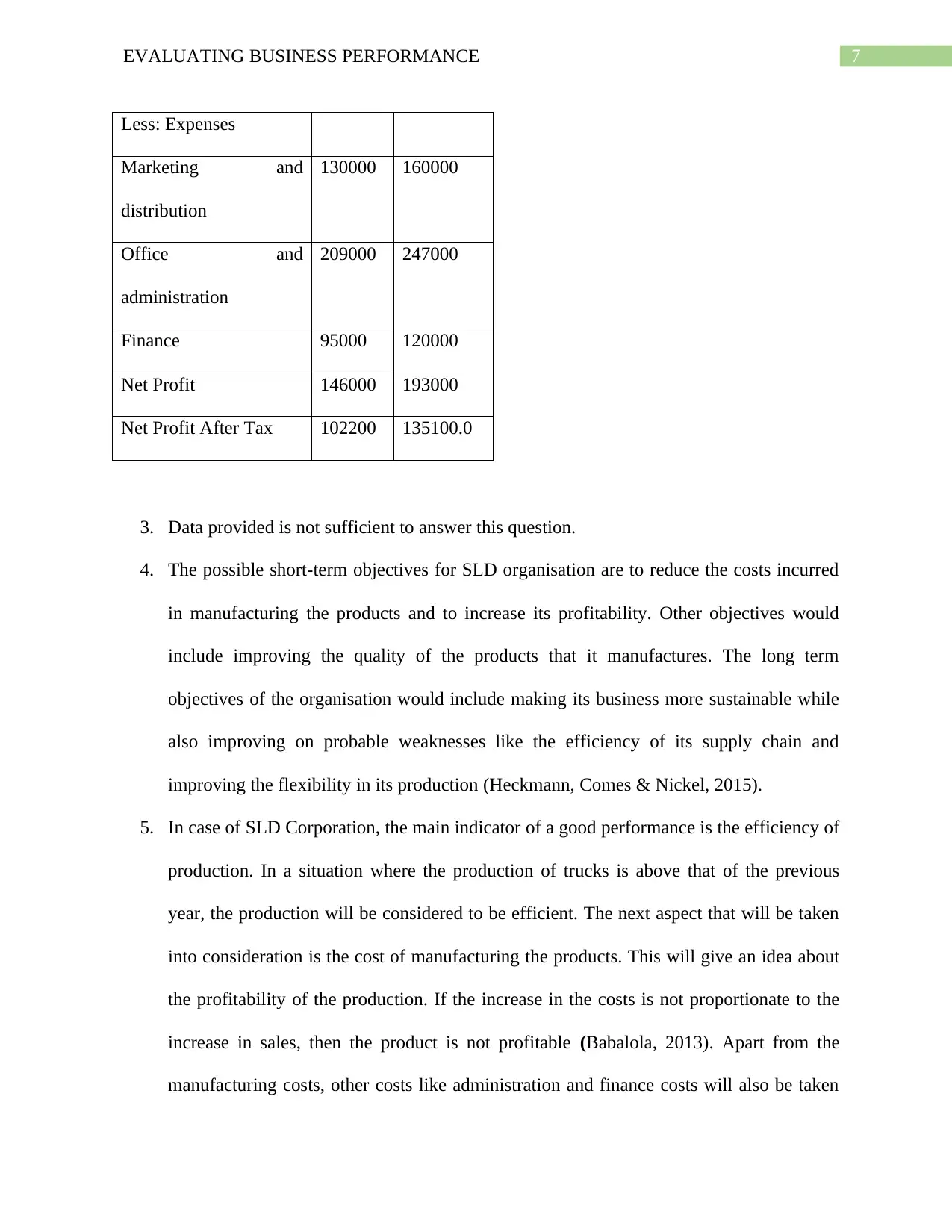

This assignment evaluates business performance through a case study and written activities. It begins with the calculation and interpretation of various financial ratios, including gross profit, net profit, liquid, accounts receivable, inventory turnover, return on equity, debt to equity, total asset turnover, return on investment, economic value added, and residual income. The analysis extends to budgeting, short-term and long-term objectives, and performance indicators for SLD Corporation, including strategies for employee engagement, customer satisfaction, and the implementation of a balanced scorecard. The project explores benchmarking, factors influencing performance measurement systems, employee rewards, communication strategies, and capital investment decisions. Additionally, the assignment includes a ratio analysis of C Juice, a SWOT analysis, and a course of action, providing a comprehensive overview of business performance evaluation.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

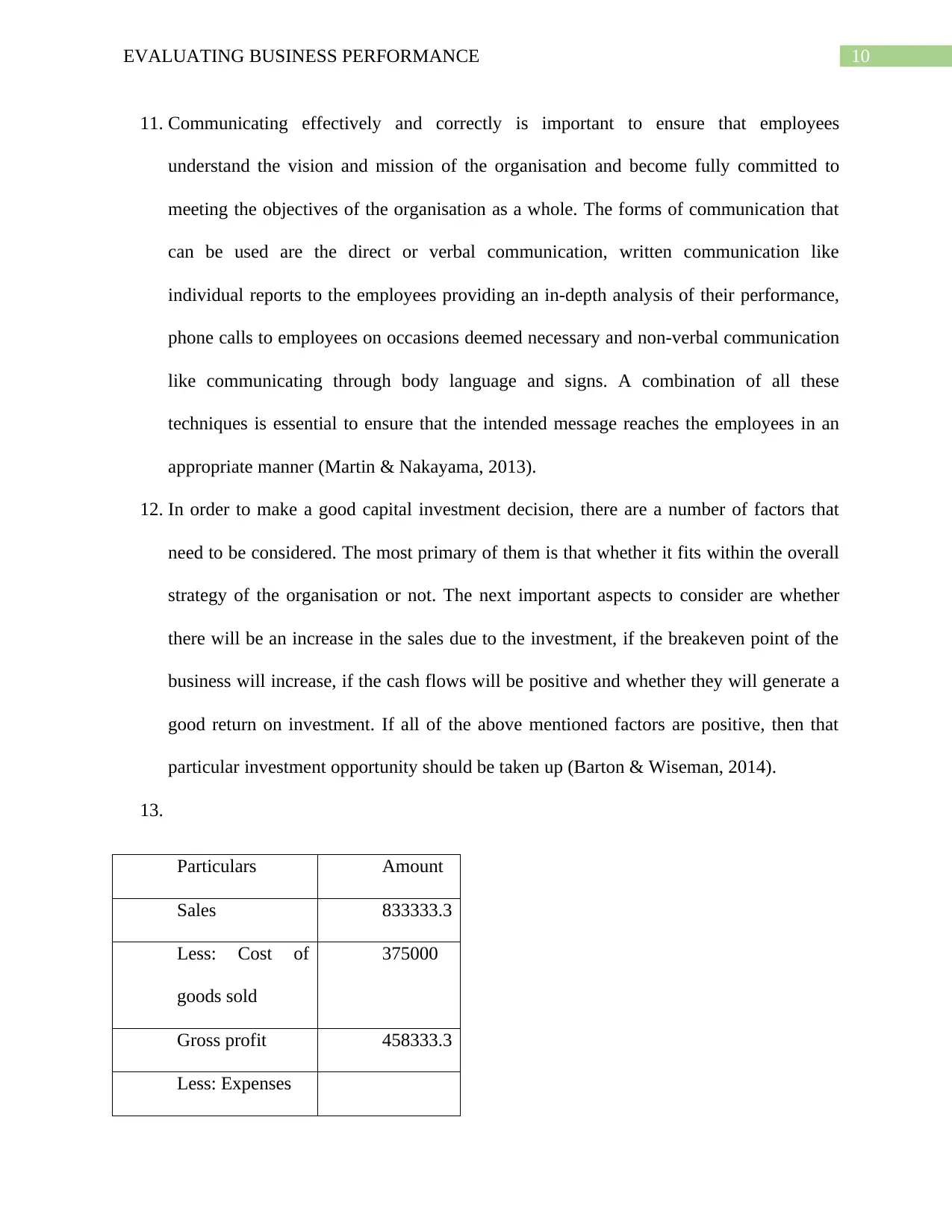

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.