FNSASICU503, FNSFPL502, FNSFPL503 Financial Planning Module 3 Solution

VerifiedAdded on 2023/06/14

|20

|4486

|90

Homework Assignment

AI Summary

This assignment solution focuses on superannuation fundamentals, covering topics relevant to the FNSASICU503, FNSFPL502, and FNSFPL503 units within a Diploma of Financial Planning Module 3. It addresses key concepts such as market-linked funds, defined benefit funds, bring-forward rules for non-concessional contributions, work tests for superannuation contributions based on age, salary sacrificing strategies, and the benefits of salary sacrificing for employees. The assignment includes detailed explanations and examples to illustrate these concepts, providing a comprehensive overview of superannuation principles and their practical application in financial planning scenarios. Desklib offers this assignment as part of its collection of solved assignments and study resources for students.

DFP Module 3 Assignment 1807

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Diploma of Financial Planning

Module 3 Assignment

Submission Instructions:

Key steps that must be followed:

1. Please complete the Declaration of Authenticity at the bottom of this page.

2. Once you have completed all parts of the assessment and saved it (e.g. to your

desktop computer), login to the Monarch Learning Management System (LMS) to

submit your assessment.

3. In the LMS, click on the file ”Submit DFP Module 3 Assignment” in the Module 3

section of your course and upload your assessment file/s by following the prompts.

4. Please be sure to click “Continue” after clicking “submit”. This ensures your assessor

receives notification – very important!

Click here to go to the Monarch LMS

Declaration of Authenticity*

I certify that the attached material is my original work. No other person’s work has been used without due

acknowledgement. I understand that the work submitted may be reproduced and/or communicated for the purpose of

detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by the

above student declaration.

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Diploma of Financial Planning

Module 3 Assignment

Submission Instructions:

Key steps that must be followed:

1. Please complete the Declaration of Authenticity at the bottom of this page.

2. Once you have completed all parts of the assessment and saved it (e.g. to your

desktop computer), login to the Monarch Learning Management System (LMS) to

submit your assessment.

3. In the LMS, click on the file ”Submit DFP Module 3 Assignment” in the Module 3

section of your course and upload your assessment file/s by following the prompts.

4. Please be sure to click “Continue” after clicking “submit”. This ensures your assessor

receives notification – very important!

Click here to go to the Monarch LMS

Declaration of Authenticity*

I certify that the attached material is my original work. No other person’s work has been used without due

acknowledgement. I understand that the work submitted may be reproduced and/or communicated for the purpose of

detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by the

above student declaration.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP Module 3 Assignment 1807

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Important assessment information

Aims of this assessment

This assessment covers the fundamentals of superannuation. It covers rules around contributing

to superannuation such as the work test, as well as contribution limits (both concessional and

non-concessional). Salary sacrifice strategies are addressed, as are the differences around a

superannuation fund in accumulation phase versus pension phase. Tax consequences across

contributions to super, money held within the accumulation phase, and lump sum withdrawal of

benefits (inclusive of pension payments) is also explored. SMSFs are addressed including

important tests such as the sole purpose test, and in-house asset test. The use of business real

property including in-specie contributions into superannuation is also addressed in the context of

SMSF strategies.

Marking and feedback

This assignment contains 4 assessment activities each containing specific instructions.

This particular assessment forms part of your overall assessment for the following units of

competency:

FNSASICU503

FNSFPL502

FNSFPL503

If you are enrolled in SMSF units, the following units are also applicable.

FNSSMS501

FNSSMS505

FNSSMS601

FNSSMS602

FNSSMS603

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with

specified educational standards under the Australian Qualifications Framework.

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Important assessment information

Aims of this assessment

This assessment covers the fundamentals of superannuation. It covers rules around contributing

to superannuation such as the work test, as well as contribution limits (both concessional and

non-concessional). Salary sacrifice strategies are addressed, as are the differences around a

superannuation fund in accumulation phase versus pension phase. Tax consequences across

contributions to super, money held within the accumulation phase, and lump sum withdrawal of

benefits (inclusive of pension payments) is also explored. SMSFs are addressed including

important tests such as the sole purpose test, and in-house asset test. The use of business real

property including in-specie contributions into superannuation is also addressed in the context of

SMSF strategies.

Marking and feedback

This assignment contains 4 assessment activities each containing specific instructions.

This particular assessment forms part of your overall assessment for the following units of

competency:

FNSASICU503

FNSFPL502

FNSFPL503

If you are enrolled in SMSF units, the following units are also applicable.

FNSSMS501

FNSSMS505

FNSSMS601

FNSSMS602

FNSSMS603

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with

specified educational standards under the Australian Qualifications Framework.

DFP Module 3 Assignment 1807

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s with

limited serious errors in fact or application. If incorrect information is contained in an answer, it

must be fundamentally outweighed by the accurate information provided. This will be assessed

against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from a

legislative perspective, or are incorrectly applied. Answers that omit to provide a response to any

significant issue (where multiple issues must be addressed in a question) may also be deemed

not-yet-competent. Answers that have faulty reasoning, a poor standard of expression or include

plagiarism may also be deemed not-yet-competent. Please note, additional information regarding

Monarch’s plagiarism policy is contained in the Student Information Guide which can be found

here: http://www.monarch.edu.au/student-info/

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be

given one more opportunity to re-submit the assessment after consultation with your Trainer/

Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your grade book in the

Monarch LMS says “NYC” after you have received an email from your assessor advising your

assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas

deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting

competency after resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our

Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter

areas raised in the question in full as part of the response.

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s with

limited serious errors in fact or application. If incorrect information is contained in an answer, it

must be fundamentally outweighed by the accurate information provided. This will be assessed

against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from a

legislative perspective, or are incorrectly applied. Answers that omit to provide a response to any

significant issue (where multiple issues must be addressed in a question) may also be deemed

not-yet-competent. Answers that have faulty reasoning, a poor standard of expression or include

plagiarism may also be deemed not-yet-competent. Please note, additional information regarding

Monarch’s plagiarism policy is contained in the Student Information Guide which can be found

here: http://www.monarch.edu.au/student-info/

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be

given one more opportunity to re-submit the assessment after consultation with your Trainer/

Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your grade book in the

Monarch LMS says “NYC” after you have received an email from your assessor advising your

assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas

deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting

competency after resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our

Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter

areas raised in the question in full as part of the response.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DFP Module 3 Assignment 1807

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Skill based questions:

Where you are asked to write as though you are speaking to a client, your answers must show

your ability to:

understand your client’s concerns/perspective/views

show empathy

display a professional response

explain ideas clearly and simply so your client can understand the issues

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to

assist you

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Skill based questions:

Where you are asked to write as though you are speaking to a client, your answers must show

your ability to:

understand your client’s concerns/perspective/views

show empathy

display a professional response

explain ideas clearly and simply so your client can understand the issues

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to

assist you

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP Module 3 Assignment 1807

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 10 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 2-3 hours

Assessment Activity 1

Short Answer

Superannuation

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 10 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 2-3 hours

Assessment Activity 1

Short Answer

Superannuation

DFP Module 3 Assignment 1807

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

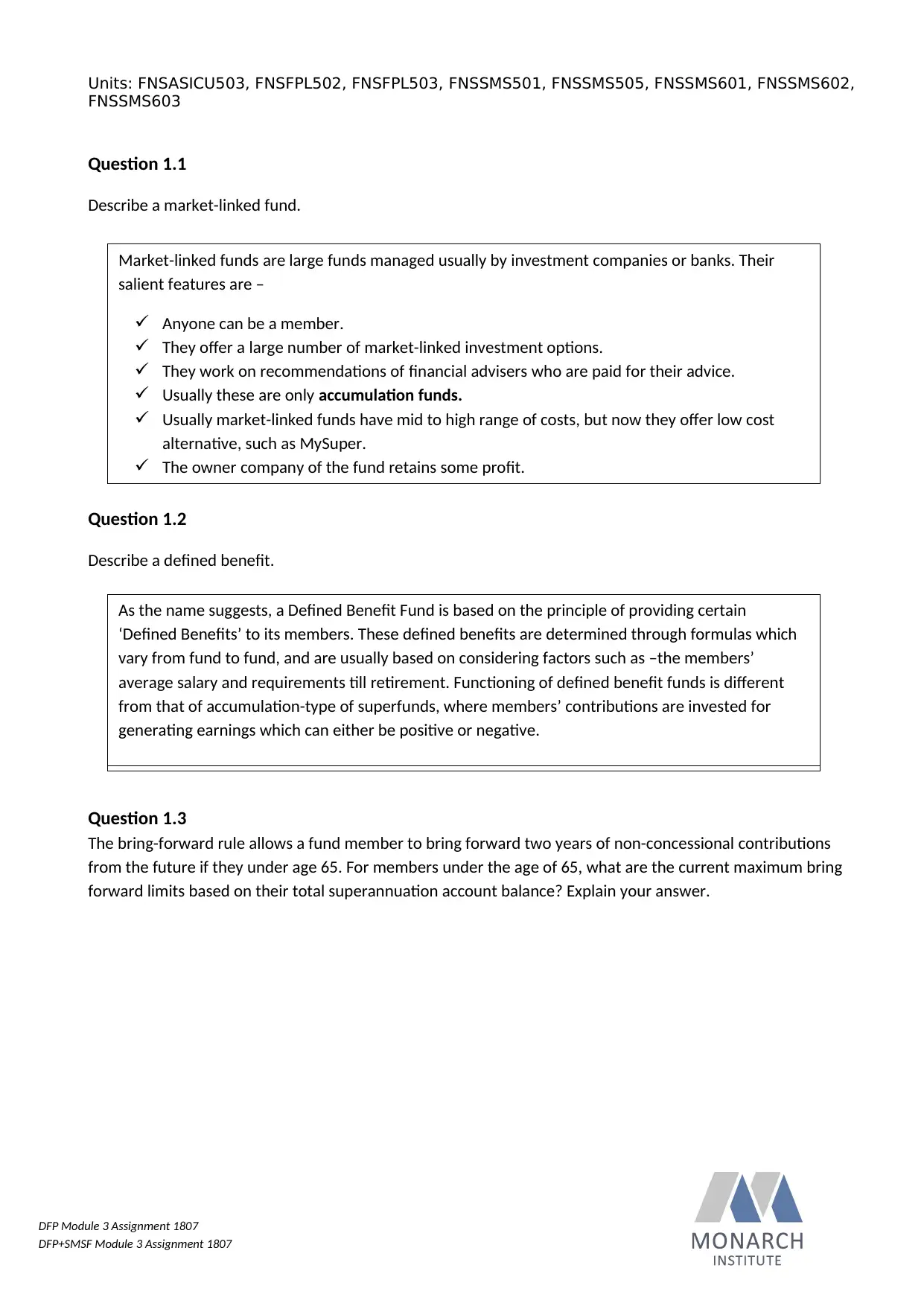

Question 1.1

Describe a market-linked fund.

Question 1.2

Describe a defined benefit.

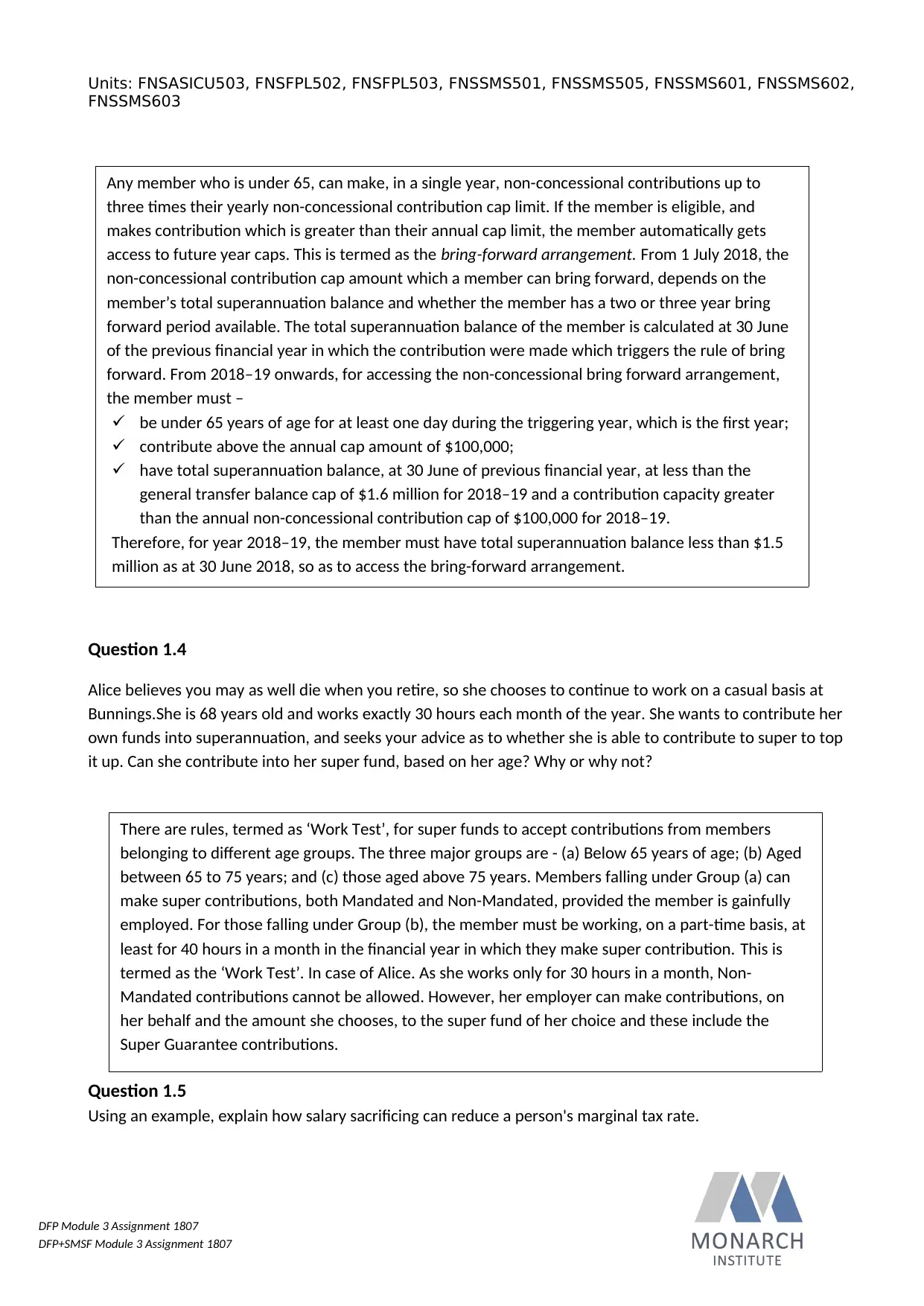

Question 1.3

The bring-forward rule allows a fund member to bring forward two years of non-concessional contributions

from the future if they under age 65. For members under the age of 65, what are the current maximum bring

forward limits based on their total superannuation account balance? Explain your answer.

Market-linked funds are large funds managed usually by investment companies or banks. Their

salient features are –

Anyone can be a member.

They offer a large number of market-linked investment options.

They work on recommendations of financial advisers who are paid for their advice.

Usually these are only accumulation funds.

Usually market-linked funds have mid to high range of costs, but now they offer low cost

alternative, such as MySuper.

The owner company of the fund retains some profit.

As the name suggests, a Defined Benefit Fund is based on the principle of providing certain

‘Defined Benefits’ to its members. These defined benefits are determined through formulas which

vary from fund to fund, and are usually based on considering factors such as –the members’

average salary and requirements till retirement. Functioning of defined benefit funds is different

from that of accumulation-type of superfunds, where members’ contributions are invested for

generating earnings which can either be positive or negative.

As the name suggests, a Defined Benefit Fund is based on the principle of providing certain

‘Defined Benefits’ to its members. These defined benefits are determined through formulas which

vary from fund to fund, and are usually based on considering factors such as –the members’

average salary and requirements till retirement. Functioning of defined benefit funds is different

from that of accumulation-type of superfunds, where members’ contributions are invested for

generating earnings which can either be positive or negative.

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Question 1.1

Describe a market-linked fund.

Question 1.2

Describe a defined benefit.

Question 1.3

The bring-forward rule allows a fund member to bring forward two years of non-concessional contributions

from the future if they under age 65. For members under the age of 65, what are the current maximum bring

forward limits based on their total superannuation account balance? Explain your answer.

Market-linked funds are large funds managed usually by investment companies or banks. Their

salient features are –

Anyone can be a member.

They offer a large number of market-linked investment options.

They work on recommendations of financial advisers who are paid for their advice.

Usually these are only accumulation funds.

Usually market-linked funds have mid to high range of costs, but now they offer low cost

alternative, such as MySuper.

The owner company of the fund retains some profit.

As the name suggests, a Defined Benefit Fund is based on the principle of providing certain

‘Defined Benefits’ to its members. These defined benefits are determined through formulas which

vary from fund to fund, and are usually based on considering factors such as –the members’

average salary and requirements till retirement. Functioning of defined benefit funds is different

from that of accumulation-type of superfunds, where members’ contributions are invested for

generating earnings which can either be positive or negative.

As the name suggests, a Defined Benefit Fund is based on the principle of providing certain

‘Defined Benefits’ to its members. These defined benefits are determined through formulas which

vary from fund to fund, and are usually based on considering factors such as –the members’

average salary and requirements till retirement. Functioning of defined benefit funds is different

from that of accumulation-type of superfunds, where members’ contributions are invested for

generating earnings which can either be positive or negative.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DFP Module 3 Assignment 1807

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Question 1.4

Alice believes you may as well die when you retire, so she chooses to continue to work on a casual basis at

Bunnings.She is 68 years old and works exactly 30 hours each month of the year. She wants to contribute her

own funds into superannuation, and seeks your advice as to whether she is able to contribute to super to top

it up. Can she contribute into her super fund, based on her age? Why or why not?

Question 1.5

Using an example, explain how salary sacrificing can reduce a person's marginal tax rate.

There are rules, termed as ‘Work Test’, for super funds to accept contributions from members

belonging to different age groups. The three major groups are - (a) Below 65 years of age; (b) Aged

between 65 to 75 years; and (c) those aged above 75 years. Members falling under Group (a) can

make super contributions, both Mandated and Non-Mandated, provided the member is gainfully

employed. For those falling under Group (b), the member must be working, on a part-time basis, at

least for 40 hours in a month in the financial year in which they make super contribution. This is

termed as the ‘Work Test’. In case of Alice. As she works only for 30 hours in a month, Non-

Mandated contributions cannot be allowed. However, her employer can make contributions, on

her behalf and the amount she chooses, to the super fund of her choice and these include the

Super Guarantee contributions.

Any member who is under 65, can make, in a single year, non-concessional contributions up to

three times their yearly non-concessional contribution cap limit. If the member is eligible, and

makes contribution which is greater than their annual cap limit, the member automatically gets

access to future year caps. This is termed as the bring-forward arrangement. From 1 July 2018, the

non-concessional contribution cap amount which a member can bring forward, depends on the

member’s total superannuation balance and whether the member has a two or three year bring

forward period available. The total superannuation balance of the member is calculated at 30 June

of the previous financial year in which the contribution were made which triggers the rule of bring

forward. From 2018–19 onwards, for accessing the non-concessional bring forward arrangement,

the member must –

be under 65 years of age for at least one day during the triggering year, which is the first year;

contribute above the annual cap amount of $100,000;

have total superannuation balance, at 30 June of previous financial year, at less than the

general transfer balance cap of $1.6 million for 2018–19 and a contribution capacity greater

than the annual non-concessional contribution cap of $100,000 for 2018–19.

Therefore, for year 2018–19, the member must have total superannuation balance less than $1.5

million as at 30 June 2018, so as to access the bring-forward arrangement.

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Question 1.4

Alice believes you may as well die when you retire, so she chooses to continue to work on a casual basis at

Bunnings.She is 68 years old and works exactly 30 hours each month of the year. She wants to contribute her

own funds into superannuation, and seeks your advice as to whether she is able to contribute to super to top

it up. Can she contribute into her super fund, based on her age? Why or why not?

Question 1.5

Using an example, explain how salary sacrificing can reduce a person's marginal tax rate.

There are rules, termed as ‘Work Test’, for super funds to accept contributions from members

belonging to different age groups. The three major groups are - (a) Below 65 years of age; (b) Aged

between 65 to 75 years; and (c) those aged above 75 years. Members falling under Group (a) can

make super contributions, both Mandated and Non-Mandated, provided the member is gainfully

employed. For those falling under Group (b), the member must be working, on a part-time basis, at

least for 40 hours in a month in the financial year in which they make super contribution. This is

termed as the ‘Work Test’. In case of Alice. As she works only for 30 hours in a month, Non-

Mandated contributions cannot be allowed. However, her employer can make contributions, on

her behalf and the amount she chooses, to the super fund of her choice and these include the

Super Guarantee contributions.

Any member who is under 65, can make, in a single year, non-concessional contributions up to

three times their yearly non-concessional contribution cap limit. If the member is eligible, and

makes contribution which is greater than their annual cap limit, the member automatically gets

access to future year caps. This is termed as the bring-forward arrangement. From 1 July 2018, the

non-concessional contribution cap amount which a member can bring forward, depends on the

member’s total superannuation balance and whether the member has a two or three year bring

forward period available. The total superannuation balance of the member is calculated at 30 June

of the previous financial year in which the contribution were made which triggers the rule of bring

forward. From 2018–19 onwards, for accessing the non-concessional bring forward arrangement,

the member must –

be under 65 years of age for at least one day during the triggering year, which is the first year;

contribute above the annual cap amount of $100,000;

have total superannuation balance, at 30 June of previous financial year, at less than the

general transfer balance cap of $1.6 million for 2018–19 and a contribution capacity greater

than the annual non-concessional contribution cap of $100,000 for 2018–19.

Therefore, for year 2018–19, the member must have total superannuation balance less than $1.5

million as at 30 June 2018, so as to access the bring-forward arrangement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP Module 3 Assignment 1807

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

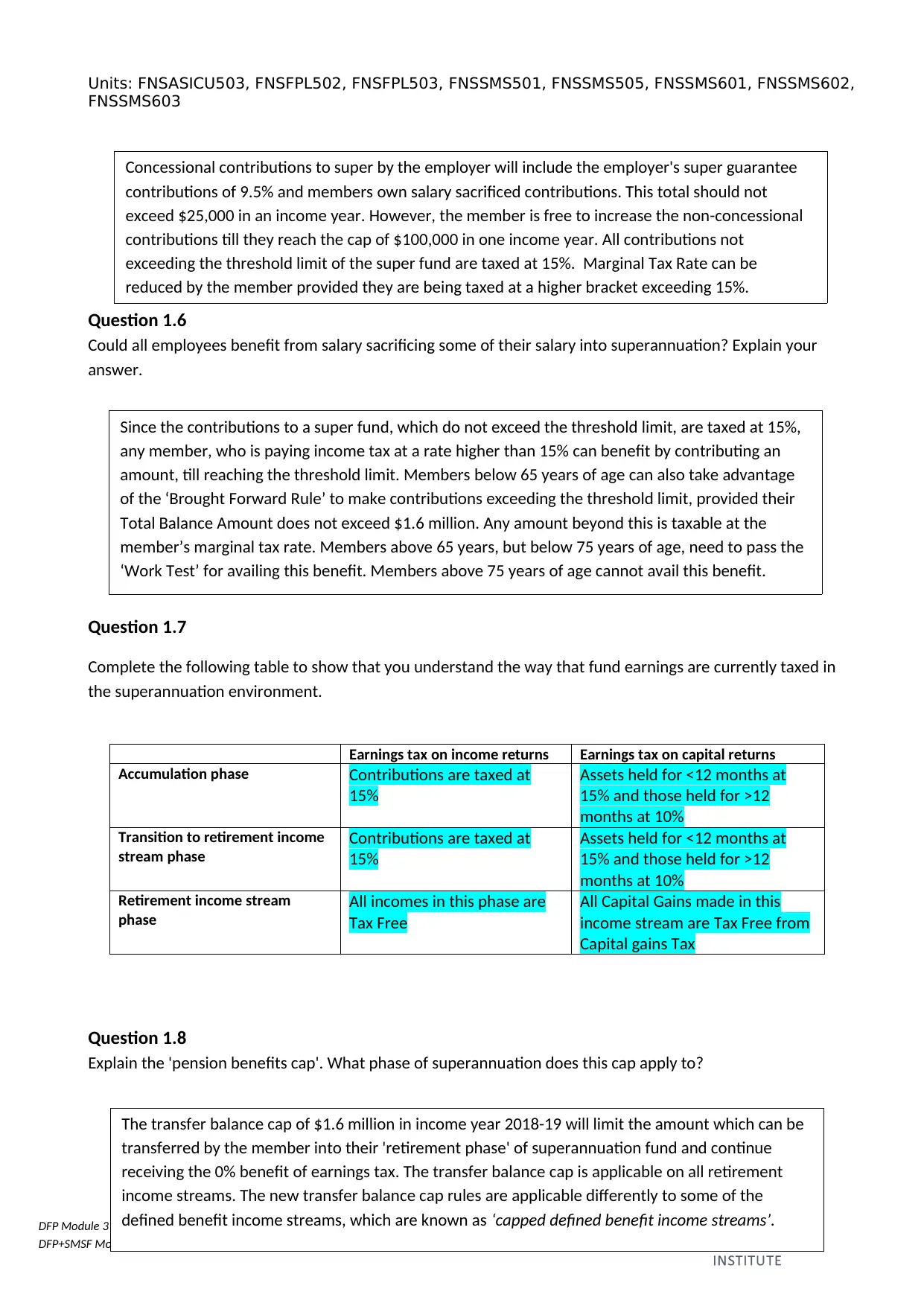

Question 1.6

Could all employees benefit from salary sacrificing some of their salary into superannuation? Explain your

answer.

Question 1.7

Complete the following table to show that you understand the way that fund earnings are currently taxed in

the superannuation environment.

Earnings tax on income returns Earnings tax on capital returns

Accumulation phase Contributions are taxed at

15%

Assets held for <12 months at

15% and those held for >12

months at 10%

Transition to retirement income

stream phase

Contributions are taxed at

15%

Assets held for <12 months at

15% and those held for >12

months at 10%

Retirement income stream

phase

All incomes in this phase are

Tax Free

All Capital Gains made in this

income stream are Tax Free from

Capital gains Tax

Question 1.8

Explain the 'pension benefits cap'. What phase of superannuation does this cap apply to?

Concessional contributions to super by the employer will include the employer's super guarantee

contributions of 9.5% and members own salary sacrificed contributions. This total should not

exceed $25,000 in an income year. However, the member is free to increase the non-concessional

contributions till they reach the cap of $100,000 in one income year. All contributions not

exceeding the threshold limit of the super fund are taxed at 15%. Marginal Tax Rate can be

reduced by the member provided they are being taxed at a higher bracket exceeding 15%.

The transfer balance cap of $1.6 million in income year 2018-19 will limit the amount which can be

transferred by the member into their 'retirement phase' of superannuation fund and continue

receiving the 0% benefit of earnings tax. The transfer balance cap is applicable on all retirement

income streams. The new transfer balance cap rules are applicable differently to some of the

defined benefit income streams, which are known as ‘capped defined benefit income streams’.

Since the contributions to a super fund, which do not exceed the threshold limit, are taxed at 15%,

any member, who is paying income tax at a rate higher than 15% can benefit by contributing an

amount, till reaching the threshold limit. Members below 65 years of age can also take advantage

of the ‘Brought Forward Rule’ to make contributions exceeding the threshold limit, provided their

Total Balance Amount does not exceed $1.6 million. Any amount beyond this is taxable at the

member’s marginal tax rate. Members above 65 years, but below 75 years of age, need to pass the

‘Work Test’ for availing this benefit. Members above 75 years of age cannot avail this benefit.

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Question 1.6

Could all employees benefit from salary sacrificing some of their salary into superannuation? Explain your

answer.

Question 1.7

Complete the following table to show that you understand the way that fund earnings are currently taxed in

the superannuation environment.

Earnings tax on income returns Earnings tax on capital returns

Accumulation phase Contributions are taxed at

15%

Assets held for <12 months at

15% and those held for >12

months at 10%

Transition to retirement income

stream phase

Contributions are taxed at

15%

Assets held for <12 months at

15% and those held for >12

months at 10%

Retirement income stream

phase

All incomes in this phase are

Tax Free

All Capital Gains made in this

income stream are Tax Free from

Capital gains Tax

Question 1.8

Explain the 'pension benefits cap'. What phase of superannuation does this cap apply to?

Concessional contributions to super by the employer will include the employer's super guarantee

contributions of 9.5% and members own salary sacrificed contributions. This total should not

exceed $25,000 in an income year. However, the member is free to increase the non-concessional

contributions till they reach the cap of $100,000 in one income year. All contributions not

exceeding the threshold limit of the super fund are taxed at 15%. Marginal Tax Rate can be

reduced by the member provided they are being taxed at a higher bracket exceeding 15%.

The transfer balance cap of $1.6 million in income year 2018-19 will limit the amount which can be

transferred by the member into their 'retirement phase' of superannuation fund and continue

receiving the 0% benefit of earnings tax. The transfer balance cap is applicable on all retirement

income streams. The new transfer balance cap rules are applicable differently to some of the

defined benefit income streams, which are known as ‘capped defined benefit income streams’.

Since the contributions to a super fund, which do not exceed the threshold limit, are taxed at 15%,

any member, who is paying income tax at a rate higher than 15% can benefit by contributing an

amount, till reaching the threshold limit. Members below 65 years of age can also take advantage

of the ‘Brought Forward Rule’ to make contributions exceeding the threshold limit, provided their

Total Balance Amount does not exceed $1.6 million. Any amount beyond this is taxable at the

member’s marginal tax rate. Members above 65 years, but below 75 years of age, need to pass the

‘Work Test’ for availing this benefit. Members above 75 years of age cannot avail this benefit.

DFP Module 3 Assignment 1807

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Question 1.9

Your clients are Mr and Mrs Jones. They are in their mid-50's and they are planning for their retirement in 10

years’ time. Mr Jones has a much higher superannuation balance than Mrs Jones and the pension benefits cap

is a concern for him in the future.

Explain the concept of 'contributions splitting' and how it could help Mr and Mrs Jones plan for the future.

Question 1.10

Nicholas pays tax at a marginal tax rate (MTR) of 37% plus the Medicare Levy of 2%. What is the benefit of

receiving fully franked dividends in his SMSF compared with receiving fully franked dividends in his own

personal name?

The contribution splitting rules will allow Mr. and Mrs. Jones to split certain concessional

contributions within their respective super accounts. As Mr. Jones has a higher income compared

to Mrs. Jones, he can contribute to Mrs. Jones’ Super Fund under the Non-concessional

contribution category. This will mean that both will have enough super for drawing pension after

their retirement. On making eligible contributions to Mrs. Jones’ super account, Mr. Jones can

claim a tax offset, to a maximum of $540 every year on the contributions which he makes to his

spouse’s super fund. However, Mr. Jones cannot claim the tax offset if Mrs. Jones’ income exceeds

$13,800. To claim this tax offset, if applicable, all Mr. Jones need to do is to claim the amount of the

tax offset in his tax return.

If the fully franked dividend payments are received by Nicholas directly into his SMSF account and

provided this contribution to his SMSF account is within the Total Balance Amount Cap, then this

will be treated as earning at the hands of the SMSF. SMSF earnings are taxed at maximum tax rate

of 15% as compared to the 37% marginal tax rate (plus 2% Medical Levy) which Nicholas will pay if

he gets the fully franked dividends in his personal name. Thus he will be saving close to 22% on tax

liability.

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Question 1.9

Your clients are Mr and Mrs Jones. They are in their mid-50's and they are planning for their retirement in 10

years’ time. Mr Jones has a much higher superannuation balance than Mrs Jones and the pension benefits cap

is a concern for him in the future.

Explain the concept of 'contributions splitting' and how it could help Mr and Mrs Jones plan for the future.

Question 1.10

Nicholas pays tax at a marginal tax rate (MTR) of 37% plus the Medicare Levy of 2%. What is the benefit of

receiving fully franked dividends in his SMSF compared with receiving fully franked dividends in his own

personal name?

The contribution splitting rules will allow Mr. and Mrs. Jones to split certain concessional

contributions within their respective super accounts. As Mr. Jones has a higher income compared

to Mrs. Jones, he can contribute to Mrs. Jones’ Super Fund under the Non-concessional

contribution category. This will mean that both will have enough super for drawing pension after

their retirement. On making eligible contributions to Mrs. Jones’ super account, Mr. Jones can

claim a tax offset, to a maximum of $540 every year on the contributions which he makes to his

spouse’s super fund. However, Mr. Jones cannot claim the tax offset if Mrs. Jones’ income exceeds

$13,800. To claim this tax offset, if applicable, all Mr. Jones need to do is to claim the amount of the

tax offset in his tax return.

If the fully franked dividend payments are received by Nicholas directly into his SMSF account and

provided this contribution to his SMSF account is within the Total Balance Amount Cap, then this

will be treated as earning at the hands of the SMSF. SMSF earnings are taxed at maximum tax rate

of 15% as compared to the 37% marginal tax rate (plus 2% Medical Levy) which Nicholas will pay if

he gets the fully franked dividends in his personal name. Thus he will be saving close to 22% on tax

liability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DFP Module 3 Assignment 1807

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Assessment Activity 2

Case Study

Superannuation

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all of the following questions.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 2-3 hours

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Assessment Activity 2

Case Study

Superannuation

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all of the following questions.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 2-3 hours

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP Module 3 Assignment 1807

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

DFP Module 3 Assignment 1807

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Question 2.1

Lisa is 59 years old and has permanently retired from the workforce. She has come to your office to seek

advice in regards to her superannuation. Lisa has $350,000 in her superannuation accumulation fund which

comprises $70,000 as a tax free component and $280,000 as a taxable component (from a taxed source). Lisa

is planning to go on an extended overseas holiday with her daughter and would like to spend a year in Paris.

She has a few questions she wants you to clarify.

Provide a clear explanation to Lisa for each of the following.

a. Can Lisa access her tax free component first as she wishes to use the $70,000 towards her trip and would

rather keep the remaining $280,000 invested?

b. How much of the total $350,000 can Lisa access as a lump sum withdrawal from her superannuation

accumulation fund, without having to pay any tax at all on that withdrawal?

c. At what age can Lisa access all her funds tax free?

DFP+SMSF Module 3 Assignment 1807

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Question 2.1

Lisa is 59 years old and has permanently retired from the workforce. She has come to your office to seek

advice in regards to her superannuation. Lisa has $350,000 in her superannuation accumulation fund which

comprises $70,000 as a tax free component and $280,000 as a taxable component (from a taxed source). Lisa

is planning to go on an extended overseas holiday with her daughter and would like to spend a year in Paris.

She has a few questions she wants you to clarify.

Provide a clear explanation to Lisa for each of the following.

a. Can Lisa access her tax free component first as she wishes to use the $70,000 towards her trip and would

rather keep the remaining $280,000 invested?

b. How much of the total $350,000 can Lisa access as a lump sum withdrawal from her superannuation

accumulation fund, without having to pay any tax at all on that withdrawal?

c. At what age can Lisa access all her funds tax free?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.