FNSR2101 Introduction to Insurance: Comprehensive Assignment Solution

VerifiedAdded on 2022/10/07

|14

|3135

|21

Homework Assignment

AI Summary

This assignment solution provides a comprehensive overview of key concepts in Introduction to Insurance, covering various aspects such as identifying insurable and non-insurable risks, including scenarios like rusting structures, genetic defects, and obsolescence of computers. It explores the advantages of insurance in society, detailing its role in protecting wealth, removing social evils, and providing security. The solution delves into physical hazards in fast-food industries and the concept of reinsurance, offering examples of how insurance companies share risks and increase capacity. It further analyzes contract breaches, ownership issues, and the role of alarm systems in insurance claims, as well as the importance of disclosing material facts. The assignment also addresses mortgage loans, industrial property policies, and standard mortgage clauses. The document provides detailed answers to various questions related to insurance, including the application of statutory conditions, loss payee relationships, and policy termination provisions. The solution also explores the Insurance Bureau of Canada and its services.

Running head: INTRODUCTION INSURANCE

Introduction Insurance

Name of the student:

Name of the university:

Author notes:

Introduction Insurance

Name of the student:

Name of the university:

Author notes:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

INTRODUCTION INSURANCE

Table of Contents

Part1...........................................................................................................................................2

Answer to question1...............................................................................................................2

Answer to question 2..............................................................................................................3

Answer to question 3..............................................................................................................4

Answer to question 4..............................................................................................................5

Part 2..........................................................................................................................................5

Answer to question no 5:........................................................................................................5

Answer to question no 6:........................................................................................................6

Answer to question 7:.............................................................................................................6

Answer to question 8:.............................................................................................................6

Part 3..........................................................................................................................................7

Answer to question 9:.............................................................................................................7

Answer to question 10:...............................................................................................................8

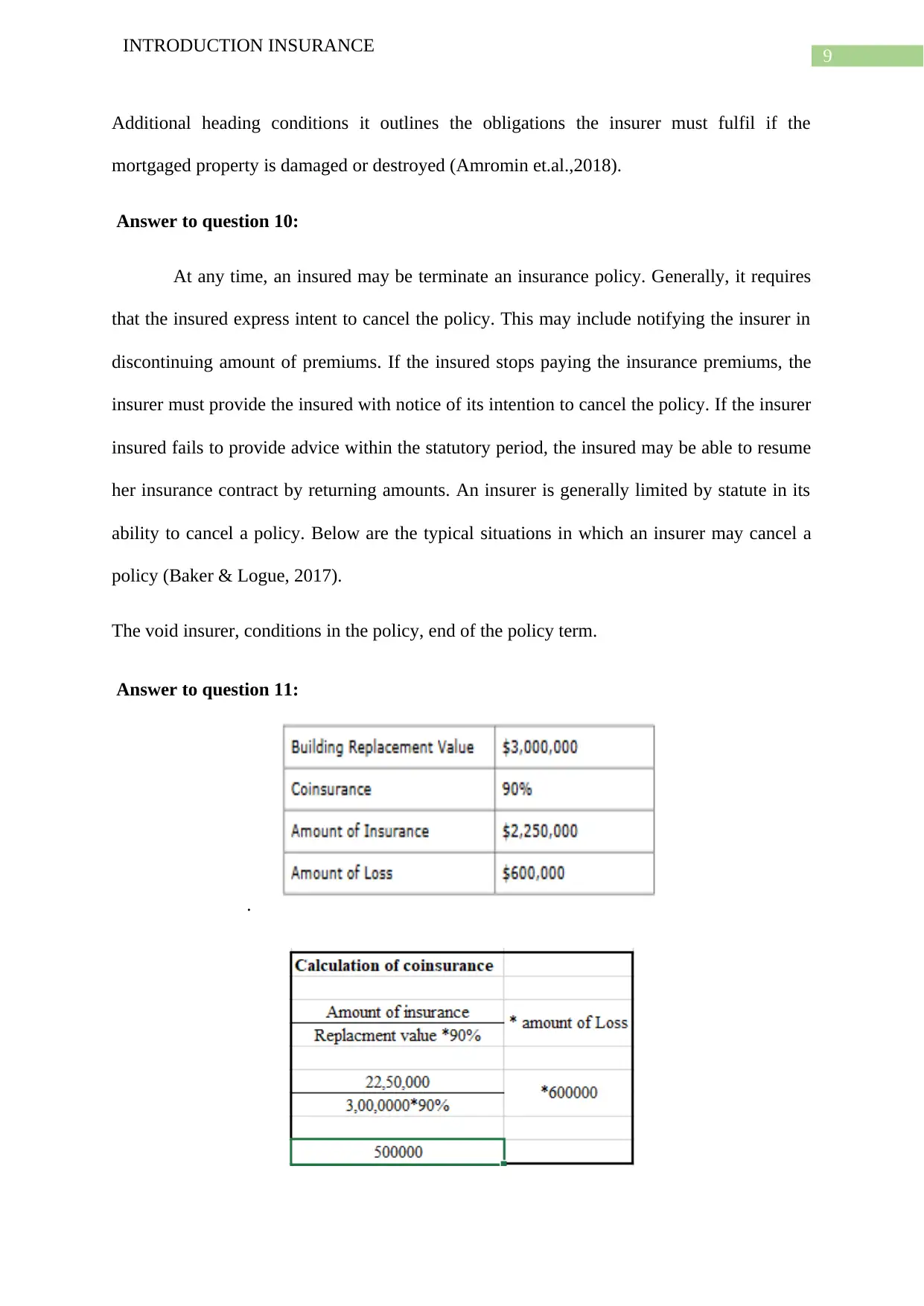

Answer to question 11:...........................................................................................................8

Answer to question 12:...........................................................................................................9

Reference:..................................................................................................................................9

INTRODUCTION INSURANCE

Table of Contents

Part1...........................................................................................................................................2

Answer to question1...............................................................................................................2

Answer to question 2..............................................................................................................3

Answer to question 3..............................................................................................................4

Answer to question 4..............................................................................................................5

Part 2..........................................................................................................................................5

Answer to question no 5:........................................................................................................5

Answer to question no 6:........................................................................................................6

Answer to question 7:.............................................................................................................6

Answer to question 8:.............................................................................................................6

Part 3..........................................................................................................................................7

Answer to question 9:.............................................................................................................7

Answer to question 10:...............................................................................................................8

Answer to question 11:...........................................................................................................8

Answer to question 12:...........................................................................................................9

Reference:..................................................................................................................................9

2

INTRODUCTION INSURANCE

Part1.

Answer to question1.

An insured event generally occurs when an insurer is required to pay a claim. But

sometimes it is considered as a risk to the insurance company if the company needs to pay an

amount, which is more than the claimed value. For example, concerning life insurance policy,

the insurance risk is like the possibility of insured party will die before his premiums amount

is equal or exceed the benefits of death.

Here, providing some scenarios which indicating whether or not any insurable Risk is

existing.

a) In case of Rusting of an unprotected structure: Generally the insurance company do

not cover any insurance relating to rusting for an unprotected structure.

Reason: Rust is generally considered under normal wear and tear of an instrument. So

there is no certain incident relating to insurance risk for an insurance company.

However, if rust is due to an incident and repair was done correctly or any water

damage that occurred due to floods or hurricane winds or waters then its need to

check the comprehensive insurance policy.

b) The Genetic defect affects 9 out of 10 newborn males: Usually, an insurance

company may face a situation of insurance risk that may occur due to an uncertain

death of a deceased person, who is suffering some genetic disorders.

Reason: According to the new implicated laws in Canada, an insurance company

needs to cover insurance policies for those peoples who are suffering any genetic

disorders. So in that case insurance company may need to pay some certain amount of

claim to the insurer in case of uncertain death.

INTRODUCTION INSURANCE

Part1.

Answer to question1.

An insured event generally occurs when an insurer is required to pay a claim. But

sometimes it is considered as a risk to the insurance company if the company needs to pay an

amount, which is more than the claimed value. For example, concerning life insurance policy,

the insurance risk is like the possibility of insured party will die before his premiums amount

is equal or exceed the benefits of death.

Here, providing some scenarios which indicating whether or not any insurable Risk is

existing.

a) In case of Rusting of an unprotected structure: Generally the insurance company do

not cover any insurance relating to rusting for an unprotected structure.

Reason: Rust is generally considered under normal wear and tear of an instrument. So

there is no certain incident relating to insurance risk for an insurance company.

However, if rust is due to an incident and repair was done correctly or any water

damage that occurred due to floods or hurricane winds or waters then its need to

check the comprehensive insurance policy.

b) The Genetic defect affects 9 out of 10 newborn males: Usually, an insurance

company may face a situation of insurance risk that may occur due to an uncertain

death of a deceased person, who is suffering some genetic disorders.

Reason: According to the new implicated laws in Canada, an insurance company

needs to cover insurance policies for those peoples who are suffering any genetic

disorders. So in that case insurance company may need to pay some certain amount of

claim to the insurer in case of uncertain death.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

INTRODUCTION INSURANCE

c) Developing of Cancer: For the purpose of developing the condition of a cancer

patients can be done through the chemotherapy, and such therapy is also covered

under insurance policy. So in such situation the insurance company may face a

situation of insurance risk.

Reason: During the period of chemotherapy the patients may collapsed due to

unconditional event, in such situation if the patient not paid the insured amount as

premium then it’s consider as insurance risk to the company as they have to pay the

claimed amount to the insurer in that moment.

d) Eventual Obsolescence of a personal computer: The personal property generally

covered under insurance policy. In case of personal computer, it’s also covered with

such policy and for such normally calculated premium amount needs to be paid by the

insurer. As it covered under the policy the insurance company may face some

situation of insurance risk.

Reason: In case the insured property obsolescence the insurance company have to

pay the claimed amount. But sometime the company faced the situation of insurance

risk if the amount of claim is more than the amount paid as premium.

e) Losing money at the casino: Losing money in casino is one type of gambling and

there are some certain policy which is called gambling insurance. Therefore in case of

gambling the insurance company may face a situation of insurance risk.

Reason: In case the losing amount in casino is more than the amount of premium paid

for this gambling, the insurance company faced the situation of insurance risk.

Answer to question 2.

In today’s society the insurance consider as one of the important elements to secure

any functions performed by human towards the society. Such advantages are given below;

INTRODUCTION INSURANCE

c) Developing of Cancer: For the purpose of developing the condition of a cancer

patients can be done through the chemotherapy, and such therapy is also covered

under insurance policy. So in such situation the insurance company may face a

situation of insurance risk.

Reason: During the period of chemotherapy the patients may collapsed due to

unconditional event, in such situation if the patient not paid the insured amount as

premium then it’s consider as insurance risk to the company as they have to pay the

claimed amount to the insurer in that moment.

d) Eventual Obsolescence of a personal computer: The personal property generally

covered under insurance policy. In case of personal computer, it’s also covered with

such policy and for such normally calculated premium amount needs to be paid by the

insurer. As it covered under the policy the insurance company may face some

situation of insurance risk.

Reason: In case the insured property obsolescence the insurance company have to

pay the claimed amount. But sometime the company faced the situation of insurance

risk if the amount of claim is more than the amount paid as premium.

e) Losing money at the casino: Losing money in casino is one type of gambling and

there are some certain policy which is called gambling insurance. Therefore in case of

gambling the insurance company may face a situation of insurance risk.

Reason: In case the losing amount in casino is more than the amount of premium paid

for this gambling, the insurance company faced the situation of insurance risk.

Answer to question 2.

In today’s society the insurance consider as one of the important elements to secure

any functions performed by human towards the society. Such advantages are given below;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

INTRODUCTION INSURANCE

1. Provide protection to wealth of society: through the using of various policies the

insurance company generally try to protect the wealth of the society. With the Life

insurance it provide protection from the loss of human wealth. Other general policies

also provide protection against loss due to theft, fire, accident or other natural

calamity.

2. Removal of social evils: providing proper insurance policy to remove the social evils

that are meant to suffering. With such proper policies the insurance company

generally protect the interest of society.

3. Perpetuate standard of living: through the insurance policy the company rescues to

many people who are suffering misfortunes. The insurance company provide them

some high returns so that they are able to maintain high standard of living.

4. Security benefits relating to social: Insurance policies provide some social benefit

through the policies for old peoples and those who are suffering some disabilities.

With such generally company reduced the burden of such peoples.

5. Distribution of losses equally: through the insurance the company generally distribute

the losses in equally so that it not make any burden for suffered peoples.

Answer to question 3.

A physical hazard is defined as a factor that may harm the body without any physical

touches. Such hazards like any unhealthy issues that make negative impacts to the human

beings. In case of fast-food industry, the hazards which may reason to illness for a human

being due to consuming unhealthy products. Some of those physical hazards that generally

occur in fast-food industries are given below;

Unhealthy Food: Often stale food left unsold might be used unethically to make profit which

can harm people eating it.

INTRODUCTION INSURANCE

1. Provide protection to wealth of society: through the using of various policies the

insurance company generally try to protect the wealth of the society. With the Life

insurance it provide protection from the loss of human wealth. Other general policies

also provide protection against loss due to theft, fire, accident or other natural

calamity.

2. Removal of social evils: providing proper insurance policy to remove the social evils

that are meant to suffering. With such proper policies the insurance company

generally protect the interest of society.

3. Perpetuate standard of living: through the insurance policy the company rescues to

many people who are suffering misfortunes. The insurance company provide them

some high returns so that they are able to maintain high standard of living.

4. Security benefits relating to social: Insurance policies provide some social benefit

through the policies for old peoples and those who are suffering some disabilities.

With such generally company reduced the burden of such peoples.

5. Distribution of losses equally: through the insurance the company generally distribute

the losses in equally so that it not make any burden for suffered peoples.

Answer to question 3.

A physical hazard is defined as a factor that may harm the body without any physical

touches. Such hazards like any unhealthy issues that make negative impacts to the human

beings. In case of fast-food industry, the hazards which may reason to illness for a human

being due to consuming unhealthy products. Some of those physical hazards that generally

occur in fast-food industries are given below;

Unhealthy Food: Often stale food left unsold might be used unethically to make profit which

can harm people eating it.

5

INTRODUCTION INSURANCE

Infected serving equipment: Unhygienic utensils that are used to serve food can lead to

causing diseases.

Sharp elements used in kitchen: Fast handling of cutting equipment’s like knives can cause

major or minor cuts.

Slippery floors: Sometimes due to water leakages causing the floors slippery which is

consider as one of the hazards issues.

Dangerous equipment and machineries: In fast food chains, accidents might occur with

equipment’s, such as cylinders

Heavy lifting injuries: In fast working conditions moving around heavy loads by individuals

can result in injuries.

Risk due to crowded workspace: Hot food is served in high demand situation and

sometimes minor accidents happen.

Chemical elements causes burning: Handling inflammable things are part of the trade and

mishandling can lead to injuries.

Answer to question 4.

A reinsurance is generally occurred when several insurance companies are intend to

share their risk through purchasing the insurance policies from the other insurer in case of

limiting their own loss due to disasters.

An example of reinsurance is that an automobile insurer sells an insurance of $100000

at a premium of $500 per annum. The automobile insurer goes to another insurer and

reinsures its insurance on the automobile to the tune of $90000 at a premium of $300 per

annum. Thus the automobile insurer has hedged its business risk to the tune of $ 90000 and is

only facing a risk of $10000 on the insurance (Soederberg,2015).

INTRODUCTION INSURANCE

Infected serving equipment: Unhygienic utensils that are used to serve food can lead to

causing diseases.

Sharp elements used in kitchen: Fast handling of cutting equipment’s like knives can cause

major or minor cuts.

Slippery floors: Sometimes due to water leakages causing the floors slippery which is

consider as one of the hazards issues.

Dangerous equipment and machineries: In fast food chains, accidents might occur with

equipment’s, such as cylinders

Heavy lifting injuries: In fast working conditions moving around heavy loads by individuals

can result in injuries.

Risk due to crowded workspace: Hot food is served in high demand situation and

sometimes minor accidents happen.

Chemical elements causes burning: Handling inflammable things are part of the trade and

mishandling can lead to injuries.

Answer to question 4.

A reinsurance is generally occurred when several insurance companies are intend to

share their risk through purchasing the insurance policies from the other insurer in case of

limiting their own loss due to disasters.

An example of reinsurance is that an automobile insurer sells an insurance of $100000

at a premium of $500 per annum. The automobile insurer goes to another insurer and

reinsures its insurance on the automobile to the tune of $90000 at a premium of $300 per

annum. Thus the automobile insurer has hedged its business risk to the tune of $ 90000 and is

only facing a risk of $10000 on the insurance (Soederberg,2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

INTRODUCTION INSURANCE

Increase the Insurer capacity to write business: Following the above mentioned examples

the insurer through the reinsuring procedures can able to increase the capacity of his personal

business. Using the reinsurance policy an insurer can shift his burden to another insurance

company.in such way the policies increase the capacity of an individual insurer (Sarkar,

2014).

To maintain a proper reserve/liability balance: followed the above example in case of

mention the balance of liability reinsurance policy is an effective way. Through such policy

the insurer try to reduce his obligation towards an insurance objects. Here as per as example

the insurer will liable for only $10000 as he already transfer the balance amount of insurance

policy to another insurance company (Weber, 2017).

Part 2.

Answer to question no 5:

As per the question it can be found that there has been breach of contract because

John Smith was supposed to give the ad on newspaper for sale price of the television

for $500 but the ad was given in the newspaper for $300 and the ad continued for 10

days at same price of $300 but instead it should have been quoted for $500. This

means that Robert Brown on accepting the contract will be in a loss due to breach of

contract from John Smith’s side. This is because he accepted to the terms of the

contract with John Smith as per ad at $300 but he was asked to agree for $500.

Therefore the contract has not been formed as per acceptance of Robert Brown

because there was a loss and miscommunication as a result of breach of contract

(Henderson, 2015).

INTRODUCTION INSURANCE

Increase the Insurer capacity to write business: Following the above mentioned examples

the insurer through the reinsuring procedures can able to increase the capacity of his personal

business. Using the reinsurance policy an insurer can shift his burden to another insurance

company.in such way the policies increase the capacity of an individual insurer (Sarkar,

2014).

To maintain a proper reserve/liability balance: followed the above example in case of

mention the balance of liability reinsurance policy is an effective way. Through such policy

the insurer try to reduce his obligation towards an insurance objects. Here as per as example

the insurer will liable for only $10000 as he already transfer the balance amount of insurance

policy to another insurance company (Weber, 2017).

Part 2.

Answer to question no 5:

As per the question it can be found that there has been breach of contract because

John Smith was supposed to give the ad on newspaper for sale price of the television

for $500 but the ad was given in the newspaper for $300 and the ad continued for 10

days at same price of $300 but instead it should have been quoted for $500. This

means that Robert Brown on accepting the contract will be in a loss due to breach of

contract from John Smith’s side. This is because he accepted to the terms of the

contract with John Smith as per ad at $300 but he was asked to agree for $500.

Therefore the contract has not been formed as per acceptance of Robert Brown

because there was a loss and miscommunication as a result of breach of contract

(Henderson, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

INTRODUCTION INSURANCE

Answer to question no 6:

As per the laws related to insurance the underwriter of risk should predict certain

issues related to the ownership as well as for operation .With respect to ownership the

underwriter should predict with the issue that since the ownership of property has been

transferred to the client’s son why has that not been communicated to him and since not has

been communicated there might be risk involved with this insurance of vehicle owned. He

would not get proper coverage on it. Since he has failed show the change of ownership of

vehicle to the broker then he would not obtain any insurance even. As a result of this issue

benefit of insurance cannot be received. On the other hand with respect to operations he

might predict the issues related to lack of proper documentation, application which has been

delayed as well as insufficient knowledge of insurance (Eckles, Hoyt & Miller, 2014).

Answer to question 7:

The alarm system can be helpful at the time of burglary in terms of business. As per

insurance act ABC Insurance company should have good alarming system but it was found as

per investigation it was found Mr. White did not have so protect his premises. This failure

lead to liability. On the basis of this ABC Insurance Company need not had to pay the

amount if it would had alarm system. The insurance company can only be liable for sum to

get assured if the alarming system in the ABC Company would have been in working

condition. Here ABC Company has to pay the liable sum of insurance for Mr. White

(Castiglionesi et.al.,2014).

Answer to question 8:

Facts about the materials should be made clear to both insurer and the insured. The

insurer keeps the defects of the form confidential and doesn’t inform the insured. Unaware of

this fact, the insured starts to work on the concerned defects. The insured is held responsible

INTRODUCTION INSURANCE

Answer to question no 6:

As per the laws related to insurance the underwriter of risk should predict certain

issues related to the ownership as well as for operation .With respect to ownership the

underwriter should predict with the issue that since the ownership of property has been

transferred to the client’s son why has that not been communicated to him and since not has

been communicated there might be risk involved with this insurance of vehicle owned. He

would not get proper coverage on it. Since he has failed show the change of ownership of

vehicle to the broker then he would not obtain any insurance even. As a result of this issue

benefit of insurance cannot be received. On the other hand with respect to operations he

might predict the issues related to lack of proper documentation, application which has been

delayed as well as insufficient knowledge of insurance (Eckles, Hoyt & Miller, 2014).

Answer to question 7:

The alarm system can be helpful at the time of burglary in terms of business. As per

insurance act ABC Insurance company should have good alarming system but it was found as

per investigation it was found Mr. White did not have so protect his premises. This failure

lead to liability. On the basis of this ABC Insurance Company need not had to pay the

amount if it would had alarm system. The insurance company can only be liable for sum to

get assured if the alarming system in the ABC Company would have been in working

condition. Here ABC Company has to pay the liable sum of insurance for Mr. White

(Castiglionesi et.al.,2014).

Answer to question 8:

Facts about the materials should be made clear to both insurer and the insured. The

insurer keeps the defects of the form confidential and doesn’t inform the insured. Unaware of

this fact, the insured starts to work on the concerned defects. The insured is held responsible

8

INTRODUCTION INSURANCE

and has to compensate for the repairs done or for the expenses occurred till now but he/she

doesn’t have to pay the entire insurance money (Bayer, Ferreira &Ross, 2017).

Part 3.

Answer to question 9:

A mortgage loan also introduces to as a mortgagee. It used by purchasers of actual

property to raise funds to buy real estate, or by existing property owners to increase the funds

for specific use any purpose while putting the lien on the property being mortgaged. The loan

is fixed on the borrower's property. That means that a legal device is set in place which

allows the lender to take ownership and sell the secured property to pay off the loan in the

event that the borrows defaults on the loan or otherwise fails to abide by its terms. Mortgage

borrowers can be the persons mortgaging their home or they can be businesses mortgaging

industrial property. The moneylender will typically be a financial institution, such a bank,

union for credit or society building, depending on the country concerned, and the loan

arrangements can be made either directly or indirectly through intermediaries (Alai et.al.,

2014).

When a business owner, purchases an industrial building with a mortgage, the

mortgage holder will likely require the buyer to ensure the building under an industrial

property policy. That includes a standard mortgage clause. This clause protects the mortgage

holder's right to obtain compensation for a loss even if the policyholder has violated terms of

the policy. Many industrial property policies contain a mortgage clause similar to the one

found in the ISO property policy. Entitled Mortgage holders, this clause is located under the

INTRODUCTION INSURANCE

and has to compensate for the repairs done or for the expenses occurred till now but he/she

doesn’t have to pay the entire insurance money (Bayer, Ferreira &Ross, 2017).

Part 3.

Answer to question 9:

A mortgage loan also introduces to as a mortgagee. It used by purchasers of actual

property to raise funds to buy real estate, or by existing property owners to increase the funds

for specific use any purpose while putting the lien on the property being mortgaged. The loan

is fixed on the borrower's property. That means that a legal device is set in place which

allows the lender to take ownership and sell the secured property to pay off the loan in the

event that the borrows defaults on the loan or otherwise fails to abide by its terms. Mortgage

borrowers can be the persons mortgaging their home or they can be businesses mortgaging

industrial property. The moneylender will typically be a financial institution, such a bank,

union for credit or society building, depending on the country concerned, and the loan

arrangements can be made either directly or indirectly through intermediaries (Alai et.al.,

2014).

When a business owner, purchases an industrial building with a mortgage, the

mortgage holder will likely require the buyer to ensure the building under an industrial

property policy. That includes a standard mortgage clause. This clause protects the mortgage

holder's right to obtain compensation for a loss even if the policyholder has violated terms of

the policy. Many industrial property policies contain a mortgage clause similar to the one

found in the ISO property policy. Entitled Mortgage holders, this clause is located under the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

INTRODUCTION INSURANCE

Additional heading conditions it outlines the obligations the insurer must fulfil if the

mortgaged property is damaged or destroyed (Amromin et.al.,2018).

Answer to question 10:

At any time, an insured may be terminate an insurance policy. Generally, it requires

that the insured express intent to cancel the policy. This may include notifying the insurer in

discontinuing amount of premiums. If the insured stops paying the insurance premiums, the

insurer must provide the insured with notice of its intention to cancel the policy. If the insurer

insured fails to provide advice within the statutory period, the insured may be able to resume

her insurance contract by returning amounts. An insurer is generally limited by statute in its

ability to cancel a policy. Below are the typical situations in which an insurer may cancel a

policy (Baker & Logue, 2017).

The void insurer, conditions in the policy, end of the policy term.

Answer to question 11:

.

INTRODUCTION INSURANCE

Additional heading conditions it outlines the obligations the insurer must fulfil if the

mortgaged property is damaged or destroyed (Amromin et.al.,2018).

Answer to question 10:

At any time, an insured may be terminate an insurance policy. Generally, it requires

that the insured express intent to cancel the policy. This may include notifying the insurer in

discontinuing amount of premiums. If the insured stops paying the insurance premiums, the

insurer must provide the insured with notice of its intention to cancel the policy. If the insurer

insured fails to provide advice within the statutory period, the insured may be able to resume

her insurance contract by returning amounts. An insurer is generally limited by statute in its

ability to cancel a policy. Below are the typical situations in which an insurer may cancel a

policy (Baker & Logue, 2017).

The void insurer, conditions in the policy, end of the policy term.

Answer to question 11:

.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

INTRODUCTION INSURANCE

Answer to question 12:

90% of the Canadian property as well as casualty insurance of the market are represented by

all the members companies of Insurance Bureau of Canada. In order to increase in public

understanding about the home auto as well as insurance related to business IBC has been

working hard towards it. With the help of IBC’s five regional customer centres public

understanding is well forecasted through which personnel those are trained with industry and

of relations of government relations tend to fulfil enquiries and understandings of

approximately ten thousands of customers each and every year.

INTRODUCTION INSURANCE

Answer to question 12:

90% of the Canadian property as well as casualty insurance of the market are represented by

all the members companies of Insurance Bureau of Canada. In order to increase in public

understanding about the home auto as well as insurance related to business IBC has been

working hard towards it. With the help of IBC’s five regional customer centres public

understanding is well forecasted through which personnel those are trained with industry and

of relations of government relations tend to fulfil enquiries and understandings of

approximately ten thousands of customers each and every year.

11

INTRODUCTION INSURANCE

INTRODUCTION INSURANCE

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.