FNSSAM403 Assignment: Prospecting and Client Relationship Building

VerifiedAdded on 2021/04/24

|15

|6046

|552

Homework Assignment

AI Summary

This document presents a comprehensive solution to the FNSSAM403 Prospect for New Clients assignment, a core component of the Certificate IV in Finance and Mortgage Broking. The assignment delves into various aspects of client acquisition and relationship management within the financial services sector. It explores effective prospecting methods, including referrals, networking, and seminars, and analyzes the importance of professional online profiles. The solution addresses cold calling techniques, emphasizing relationship building and tailoring financial products to client needs. It also covers the significance of client data collection, LVR calculations, and responses to client concerns, as well as interpersonal techniques for overcoming client hesitations. Furthermore, the document provides a detailed analysis of a client's financial goals, concerns, and creditworthiness, alongside research and presentation of suitable car loan products, including interest rates, comparison rates, and loan security. This assignment helps students to gain a deeper understanding of the finance and mortgage broking industry.

FNSSAM403 Prospect for new clients

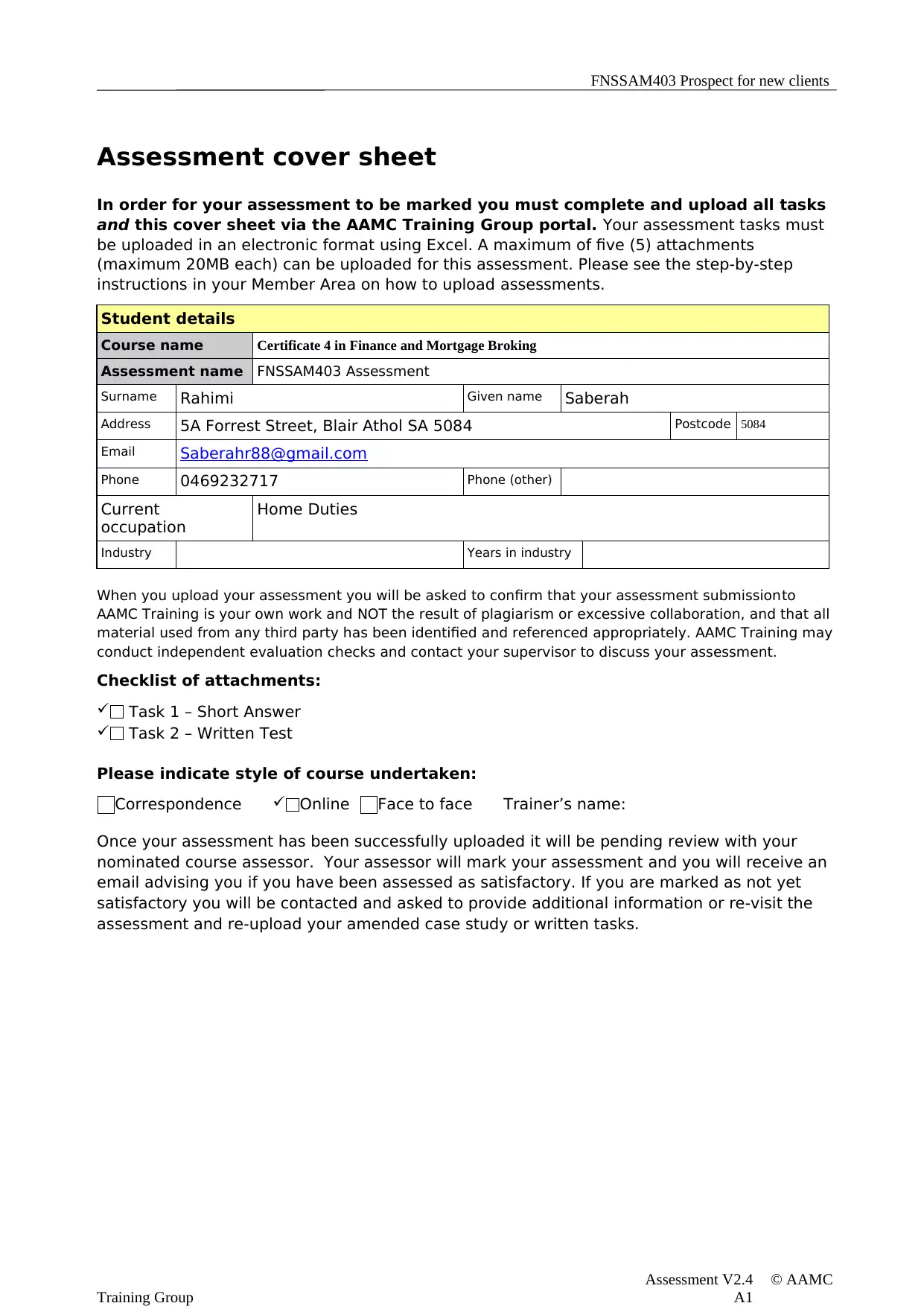

Assessment cover sheet

In order for your assessment to be marked you must complete and upload all tasks

and this cover sheet via the AAMC Training Group portal. Your assessment tasks must

be uploaded in an electronic format using Excel. A maximum of five (5) attachments

(maximum 20MB each) can be uploaded for this assessment. Please see the step-by-step

instructions in your Member Area on how to upload assessments.

Student details

Course name Certificate 4 in Finance and Mortgage Broking

Assessment name FNSSAM403 Assessment

Surname Rahimi Given name Saberah

Address 5A Forrest Street, Blair Athol SA 5084 Postcode 5084

Email Saberahr88@gmail.com

Phone 0469232717 Phone (other)

Current

occupation

Home Duties

Industry Years in industry

When you upload your assessment you will be asked to confirm that your assessment submissionto

AAMC Training is your own work and NOT the result of plagiarism or excessive collaboration, and that all

material used from any third party has been identified and referenced appropriately. AAMC Training may

conduct independent evaluation checks and contact your supervisor to discuss your assessment.

Checklist of attachments:

Task 1 – Short Answer

Task 2 – Written Test

Please indicate style of course undertaken:

Correspondence Online Face to face Trainer’s name:

Once your assessment has been successfully uploaded it will be pending review with your

nominated course assessor. Your assessor will mark your assessment and you will receive an

email advising you if you have been assessed as satisfactory. If you are marked as not yet

satisfactory you will be contacted and asked to provide additional information or re-visit the

assessment and re-upload your amended case study or written tasks.

Assessment V2.4 © AAMC

Training Group A1

Assessment cover sheet

In order for your assessment to be marked you must complete and upload all tasks

and this cover sheet via the AAMC Training Group portal. Your assessment tasks must

be uploaded in an electronic format using Excel. A maximum of five (5) attachments

(maximum 20MB each) can be uploaded for this assessment. Please see the step-by-step

instructions in your Member Area on how to upload assessments.

Student details

Course name Certificate 4 in Finance and Mortgage Broking

Assessment name FNSSAM403 Assessment

Surname Rahimi Given name Saberah

Address 5A Forrest Street, Blair Athol SA 5084 Postcode 5084

Email Saberahr88@gmail.com

Phone 0469232717 Phone (other)

Current

occupation

Home Duties

Industry Years in industry

When you upload your assessment you will be asked to confirm that your assessment submissionto

AAMC Training is your own work and NOT the result of plagiarism or excessive collaboration, and that all

material used from any third party has been identified and referenced appropriately. AAMC Training may

conduct independent evaluation checks and contact your supervisor to discuss your assessment.

Checklist of attachments:

Task 1 – Short Answer

Task 2 – Written Test

Please indicate style of course undertaken:

Correspondence Online Face to face Trainer’s name:

Once your assessment has been successfully uploaded it will be pending review with your

nominated course assessor. Your assessor will mark your assessment and you will receive an

email advising you if you have been assessed as satisfactory. If you are marked as not yet

satisfactory you will be contacted and asked to provide additional information or re-visit the

assessment and re-upload your amended case study or written tasks.

Assessment V2.4 © AAMC

Training Group A1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FNSSAM403 Prospect for new clients

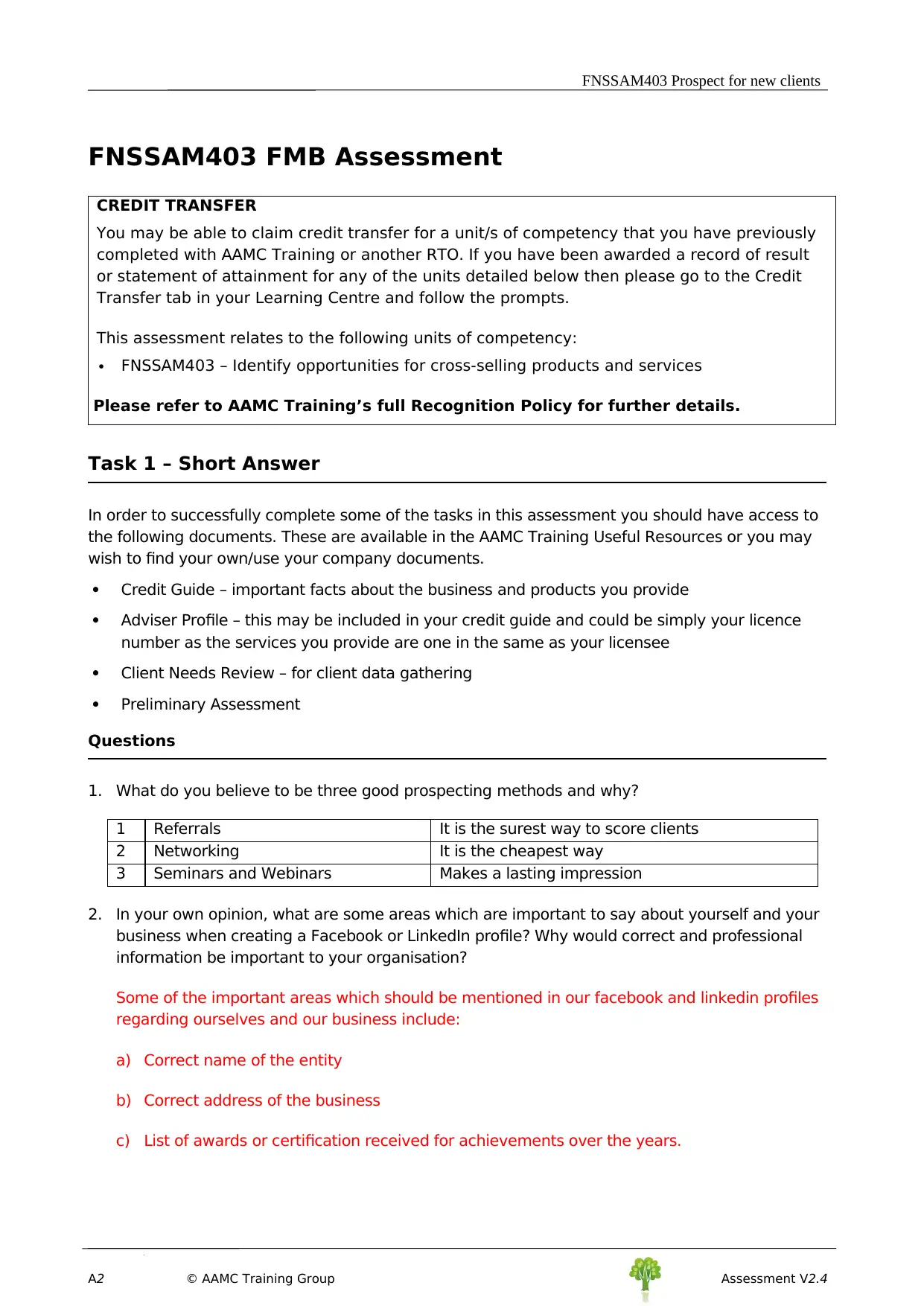

FNSSAM403 FMB Assessment

CREDIT TRANSFER

You may be able to claim credit transfer for a unit/s of competency that you have previously

completed with AAMC Training or another RTO. If you have been awarded a record of result

or statement of attainment for any of the units detailed below then please go to the Credit

Transfer tab in your Learning Centre and follow the prompts.

This assessment relates to the following units of competency:

FNSSAM403 – Identify opportunities for cross-selling products and services

Please refer to AAMC Training’s full Recognition Policy for further details.

Task 1 – Short Answer

In order to successfully complete some of the tasks in this assessment you should have access to

the following documents. These are available in the AAMC Training Useful Resources or you may

wish to find your own/use your company documents.

Credit Guide – important facts about the business and products you provide

Adviser Profile – this may be included in your credit guide and could be simply your licence

number as the services you provide are one in the same as your licensee

Client Needs Review – for client data gathering

Preliminary Assessment

Questions

1. What do you believe to be three good prospecting methods and why?

1 Referrals It is the surest way to score clients

2 Networking It is the cheapest way

3 Seminars and Webinars Makes a lasting impression

2. In your own opinion, what are some areas which are important to say about yourself and your

business when creating a Facebook or LinkedIn profile? Why would correct and professional

information be important to your organisation?

Some of the important areas which should be mentioned in our facebook and linkedin profiles

regarding ourselves and our business include:

a) Correct name of the entity

b) Correct address of the business

c) List of awards or certification received for achievements over the years.

A2 © AAMC Training Group Assessment V2.4

FNSSAM403 FMB Assessment

CREDIT TRANSFER

You may be able to claim credit transfer for a unit/s of competency that you have previously

completed with AAMC Training or another RTO. If you have been awarded a record of result

or statement of attainment for any of the units detailed below then please go to the Credit

Transfer tab in your Learning Centre and follow the prompts.

This assessment relates to the following units of competency:

FNSSAM403 – Identify opportunities for cross-selling products and services

Please refer to AAMC Training’s full Recognition Policy for further details.

Task 1 – Short Answer

In order to successfully complete some of the tasks in this assessment you should have access to

the following documents. These are available in the AAMC Training Useful Resources or you may

wish to find your own/use your company documents.

Credit Guide – important facts about the business and products you provide

Adviser Profile – this may be included in your credit guide and could be simply your licence

number as the services you provide are one in the same as your licensee

Client Needs Review – for client data gathering

Preliminary Assessment

Questions

1. What do you believe to be three good prospecting methods and why?

1 Referrals It is the surest way to score clients

2 Networking It is the cheapest way

3 Seminars and Webinars Makes a lasting impression

2. In your own opinion, what are some areas which are important to say about yourself and your

business when creating a Facebook or LinkedIn profile? Why would correct and professional

information be important to your organisation?

Some of the important areas which should be mentioned in our facebook and linkedin profiles

regarding ourselves and our business include:

a) Correct name of the entity

b) Correct address of the business

c) List of awards or certification received for achievements over the years.

A2 © AAMC Training Group Assessment V2.4

FNSSAM403 Prospect for new clients

d) It is important that we mention our educational background in respect of the professional

degree held by us.

e) Objectives, policies and belief statements of the company.

It is of utmost importance hat only correct and professional information is displayed in the

social media this is because of the fact that the purpose of social media is to attract

various stakeholders including suppliers, prospective clients, investors and employees.

The information provided helps in building our credential.

3. What is cold calling? Is cold calling an effective prospecting method? Explain your answer.

Cold calling is an early stage selling process wherein calls are directly made to prospective

buyers for the purpose of convincing them to buy our product. Cold calling is an effective way

of prospecting. The reasons for this is plenty, some of them include a single person can make

more call sitting in an office than roaming about in the market. This saves effort and time

along with cost on the part of the company. But the effectiveness of the cold calling depends

entirely on the communication skills of the person making the call. Hence the art of cold

calling must be inculcated among the employees before embarking on it.

4. How would you build a relationship with a client through cold calling?

I would help him explore his interests and find his needs, then shape my product according to

the current needs that he requires.

5. In your opinion, why would the following areas of information (found in the Credit Guide) be

important for a new client to understand? How could this information protect all parties?

your role and responsibility as Credit Advisor – due to the level of my understanding of the

needs of the client

the role of the organisation – it is important as it is the domain that matters, if the

organization operates in that domain than it has a vitality.

the identity of and information about the Credit Licence holder – this helps us protect the

identity of the client and the prospective region of inference.

the range of services provided – This handles the current need of the client and its

matching with the services offered

all costs, fees, commissions etc. associated with the transaction – these must be low as

they increase the potential customer might not return

the procedures for handling complaints and disputes. –This helps retain the customer and

also enables him to return for resolution.

6. Why do you believe is it important to encourage prospective clients to express their needs

and goals when completing a data collection?

It is important as to know the client more and to offer him something valuable in return.

Assessment V2.4 © AAMC

Training Group A3

d) It is important that we mention our educational background in respect of the professional

degree held by us.

e) Objectives, policies and belief statements of the company.

It is of utmost importance hat only correct and professional information is displayed in the

social media this is because of the fact that the purpose of social media is to attract

various stakeholders including suppliers, prospective clients, investors and employees.

The information provided helps in building our credential.

3. What is cold calling? Is cold calling an effective prospecting method? Explain your answer.

Cold calling is an early stage selling process wherein calls are directly made to prospective

buyers for the purpose of convincing them to buy our product. Cold calling is an effective way

of prospecting. The reasons for this is plenty, some of them include a single person can make

more call sitting in an office than roaming about in the market. This saves effort and time

along with cost on the part of the company. But the effectiveness of the cold calling depends

entirely on the communication skills of the person making the call. Hence the art of cold

calling must be inculcated among the employees before embarking on it.

4. How would you build a relationship with a client through cold calling?

I would help him explore his interests and find his needs, then shape my product according to

the current needs that he requires.

5. In your opinion, why would the following areas of information (found in the Credit Guide) be

important for a new client to understand? How could this information protect all parties?

your role and responsibility as Credit Advisor – due to the level of my understanding of the

needs of the client

the role of the organisation – it is important as it is the domain that matters, if the

organization operates in that domain than it has a vitality.

the identity of and information about the Credit Licence holder – this helps us protect the

identity of the client and the prospective region of inference.

the range of services provided – This handles the current need of the client and its

matching with the services offered

all costs, fees, commissions etc. associated with the transaction – these must be low as

they increase the potential customer might not return

the procedures for handling complaints and disputes. –This helps retain the customer and

also enables him to return for resolution.

6. Why do you believe is it important to encourage prospective clients to express their needs

and goals when completing a data collection?

It is important as to know the client more and to offer him something valuable in return.

Assessment V2.4 © AAMC

Training Group A3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FNSSAM403 Prospect for new clients

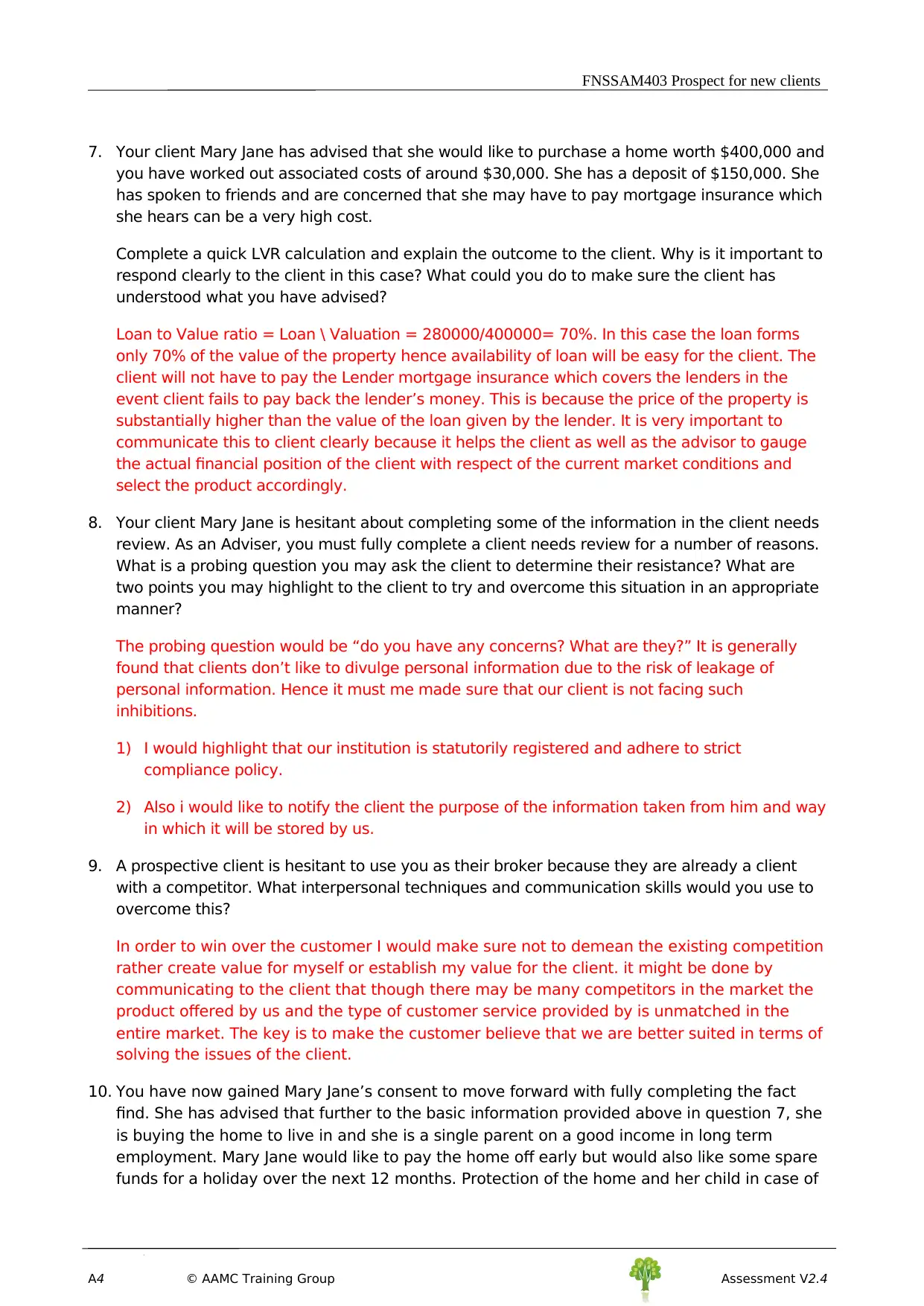

7. Your client Mary Jane has advised that she would like to purchase a home worth $400,000 and

you have worked out associated costs of around $30,000. She has a deposit of $150,000. She

has spoken to friends and are concerned that she may have to pay mortgage insurance which

she hears can be a very high cost.

Complete a quick LVR calculation and explain the outcome to the client. Why is it important to

respond clearly to the client in this case? What could you do to make sure the client has

understood what you have advised?

Loan to Value ratio = Loan \ Valuation = 280000/400000= 70%. In this case the loan forms

only 70% of the value of the property hence availability of loan will be easy for the client. The

client will not have to pay the Lender mortgage insurance which covers the lenders in the

event client fails to pay back the lender’s money. This is because the price of the property is

substantially higher than the value of the loan given by the lender. It is very important to

communicate this to client clearly because it helps the client as well as the advisor to gauge

the actual financial position of the client with respect of the current market conditions and

select the product accordingly.

8. Your client Mary Jane is hesitant about completing some of the information in the client needs

review. As an Adviser, you must fully complete a client needs review for a number of reasons.

What is a probing question you may ask the client to determine their resistance? What are

two points you may highlight to the client to try and overcome this situation in an appropriate

manner?

The probing question would be “do you have any concerns? What are they?” It is generally

found that clients don’t like to divulge personal information due to the risk of leakage of

personal information. Hence it must me made sure that our client is not facing such

inhibitions.

1) I would highlight that our institution is statutorily registered and adhere to strict

compliance policy.

2) Also i would like to notify the client the purpose of the information taken from him and way

in which it will be stored by us.

9. A prospective client is hesitant to use you as their broker because they are already a client

with a competitor. What interpersonal techniques and communication skills would you use to

overcome this?

In order to win over the customer I would make sure not to demean the existing competition

rather create value for myself or establish my value for the client. it might be done by

communicating to the client that though there may be many competitors in the market the

product offered by us and the type of customer service provided by is unmatched in the

entire market. The key is to make the customer believe that we are better suited in terms of

solving the issues of the client.

10. You have now gained Mary Jane’s consent to move forward with fully completing the fact

find. She has advised that further to the basic information provided above in question 7, she

is buying the home to live in and she is a single parent on a good income in long term

employment. Mary Jane would like to pay the home off early but would also like some spare

funds for a holiday over the next 12 months. Protection of the home and her child in case of

A4 © AAMC Training Group Assessment V2.4

7. Your client Mary Jane has advised that she would like to purchase a home worth $400,000 and

you have worked out associated costs of around $30,000. She has a deposit of $150,000. She

has spoken to friends and are concerned that she may have to pay mortgage insurance which

she hears can be a very high cost.

Complete a quick LVR calculation and explain the outcome to the client. Why is it important to

respond clearly to the client in this case? What could you do to make sure the client has

understood what you have advised?

Loan to Value ratio = Loan \ Valuation = 280000/400000= 70%. In this case the loan forms

only 70% of the value of the property hence availability of loan will be easy for the client. The

client will not have to pay the Lender mortgage insurance which covers the lenders in the

event client fails to pay back the lender’s money. This is because the price of the property is

substantially higher than the value of the loan given by the lender. It is very important to

communicate this to client clearly because it helps the client as well as the advisor to gauge

the actual financial position of the client with respect of the current market conditions and

select the product accordingly.

8. Your client Mary Jane is hesitant about completing some of the information in the client needs

review. As an Adviser, you must fully complete a client needs review for a number of reasons.

What is a probing question you may ask the client to determine their resistance? What are

two points you may highlight to the client to try and overcome this situation in an appropriate

manner?

The probing question would be “do you have any concerns? What are they?” It is generally

found that clients don’t like to divulge personal information due to the risk of leakage of

personal information. Hence it must me made sure that our client is not facing such

inhibitions.

1) I would highlight that our institution is statutorily registered and adhere to strict

compliance policy.

2) Also i would like to notify the client the purpose of the information taken from him and way

in which it will be stored by us.

9. A prospective client is hesitant to use you as their broker because they are already a client

with a competitor. What interpersonal techniques and communication skills would you use to

overcome this?

In order to win over the customer I would make sure not to demean the existing competition

rather create value for myself or establish my value for the client. it might be done by

communicating to the client that though there may be many competitors in the market the

product offered by us and the type of customer service provided by is unmatched in the

entire market. The key is to make the customer believe that we are better suited in terms of

solving the issues of the client.

10. You have now gained Mary Jane’s consent to move forward with fully completing the fact

find. She has advised that further to the basic information provided above in question 7, she

is buying the home to live in and she is a single parent on a good income in long term

employment. Mary Jane would like to pay the home off early but would also like some spare

funds for a holiday over the next 12 months. Protection of the home and her child in case of

A4 © AAMC Training Group Assessment V2.4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FNSSAM403 Prospect for new clients

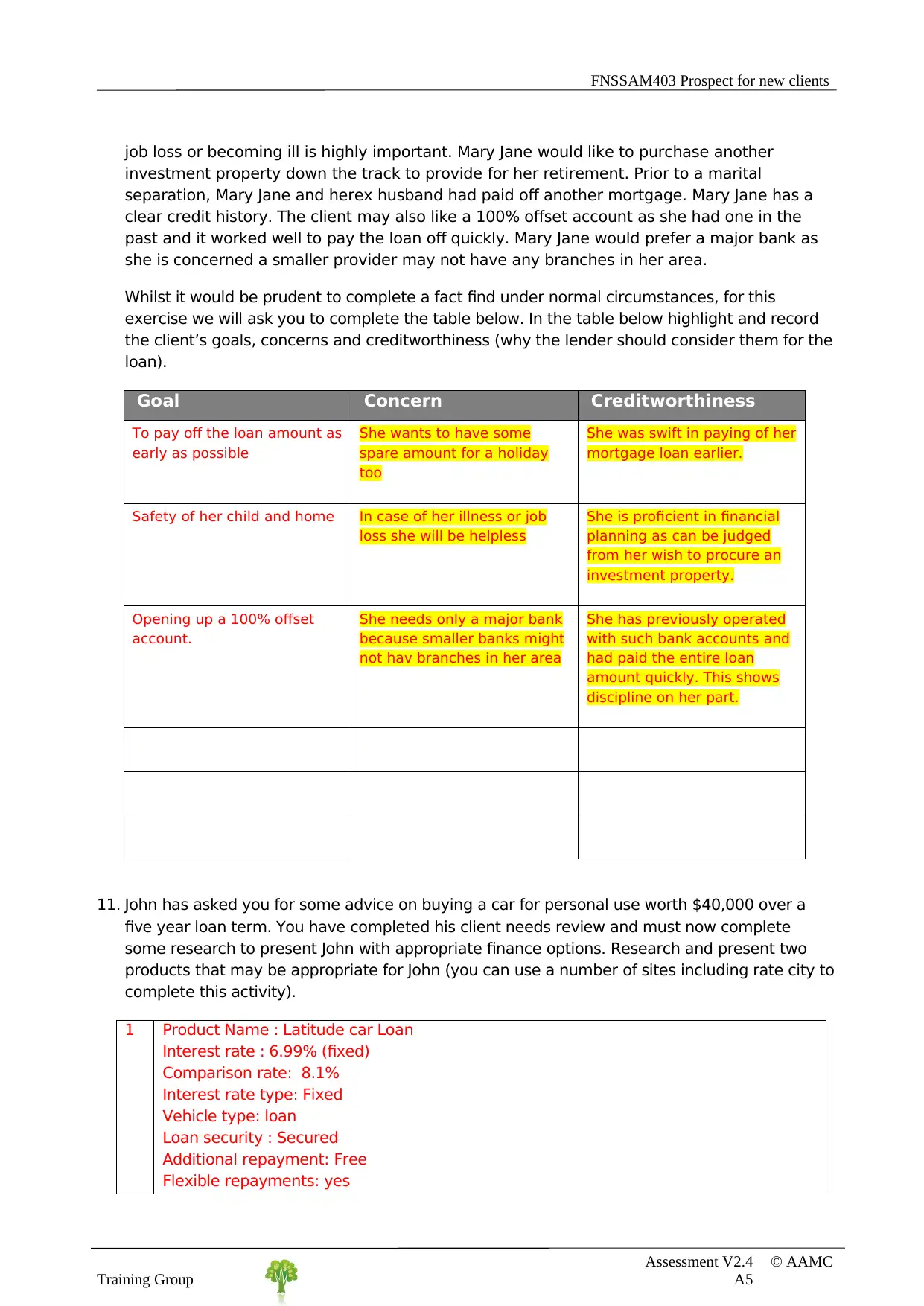

job loss or becoming ill is highly important. Mary Jane would like to purchase another

investment property down the track to provide for her retirement. Prior to a marital

separation, Mary Jane and herex husband had paid off another mortgage. Mary Jane has a

clear credit history. The client may also like a 100% offset account as she had one in the

past and it worked well to pay the loan off quickly. Mary Jane would prefer a major bank as

she is concerned a smaller provider may not have any branches in her area.

Whilst it would be prudent to complete a fact find under normal circumstances, for this

exercise we will ask you to complete the table below. In the table below highlight and record

the client’s goals, concerns and creditworthiness (why the lender should consider them for the

loan).

Goal Concern Creditworthiness

To pay off the loan amount as

early as possible

She wants to have some

spare amount for a holiday

too

She was swift in paying of her

mortgage loan earlier.

Safety of her child and home In case of her illness or job

loss she will be helpless

She is proficient in financial

planning as can be judged

from her wish to procure an

investment property.

Opening up a 100% offset

account.

She needs only a major bank

because smaller banks might

not hav branches in her area

She has previously operated

with such bank accounts and

had paid the entire loan

amount quickly. This shows

discipline on her part.

11. John has asked you for some advice on buying a car for personal use worth $40,000 over a

five year loan term. You have completed his client needs review and must now complete

some research to present John with appropriate finance options. Research and present two

products that may be appropriate for John (you can use a number of sites including rate city to

complete this activity).

1 Product Name : Latitude car Loan

Interest rate : 6.99% (fixed)

Comparison rate: 8.1%

Interest rate type: Fixed

Vehicle type: loan

Loan security : Secured

Additional repayment: Free

Flexible repayments: yes

Assessment V2.4 © AAMC

Training Group A5

job loss or becoming ill is highly important. Mary Jane would like to purchase another

investment property down the track to provide for her retirement. Prior to a marital

separation, Mary Jane and herex husband had paid off another mortgage. Mary Jane has a

clear credit history. The client may also like a 100% offset account as she had one in the

past and it worked well to pay the loan off quickly. Mary Jane would prefer a major bank as

she is concerned a smaller provider may not have any branches in her area.

Whilst it would be prudent to complete a fact find under normal circumstances, for this

exercise we will ask you to complete the table below. In the table below highlight and record

the client’s goals, concerns and creditworthiness (why the lender should consider them for the

loan).

Goal Concern Creditworthiness

To pay off the loan amount as

early as possible

She wants to have some

spare amount for a holiday

too

She was swift in paying of her

mortgage loan earlier.

Safety of her child and home In case of her illness or job

loss she will be helpless

She is proficient in financial

planning as can be judged

from her wish to procure an

investment property.

Opening up a 100% offset

account.

She needs only a major bank

because smaller banks might

not hav branches in her area

She has previously operated

with such bank accounts and

had paid the entire loan

amount quickly. This shows

discipline on her part.

11. John has asked you for some advice on buying a car for personal use worth $40,000 over a

five year loan term. You have completed his client needs review and must now complete

some research to present John with appropriate finance options. Research and present two

products that may be appropriate for John (you can use a number of sites including rate city to

complete this activity).

1 Product Name : Latitude car Loan

Interest rate : 6.99% (fixed)

Comparison rate: 8.1%

Interest rate type: Fixed

Vehicle type: loan

Loan security : Secured

Additional repayment: Free

Flexible repayments: yes

Assessment V2.4 © AAMC

Training Group A5

FNSSAM403 Prospect for new clients

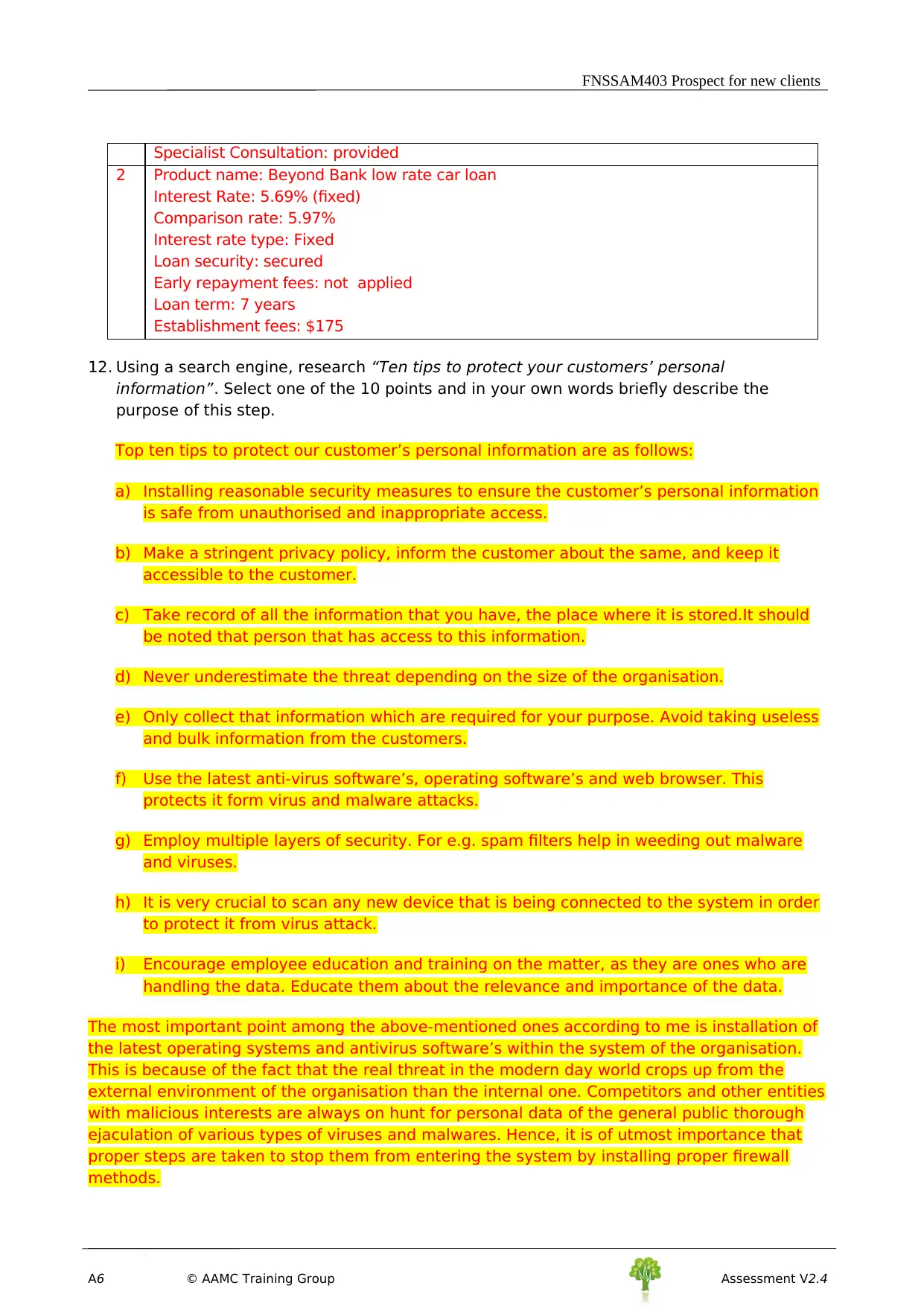

Specialist Consultation: provided

2 Product name: Beyond Bank low rate car loan

Interest Rate: 5.69% (fixed)

Comparison rate: 5.97%

Interest rate type: Fixed

Loan security: secured

Early repayment fees: not applied

Loan term: 7 years

Establishment fees: $175

12. Using a search engine, research “Ten tips to protect your customers’ personal

information”. Select one of the 10 points and in your own words briefly describe the

purpose of this step.

Top ten tips to protect our customer’s personal information are as follows:

a) Installing reasonable security measures to ensure the customer’s personal information

is safe from unauthorised and inappropriate access.

b) Make a stringent privacy policy, inform the customer about the same, and keep it

accessible to the customer.

c) Take record of all the information that you have, the place where it is stored.It should

be noted that person that has access to this information.

d) Never underestimate the threat depending on the size of the organisation.

e) Only collect that information which are required for your purpose. Avoid taking useless

and bulk information from the customers.

f) Use the latest anti-virus software’s, operating software’s and web browser. This

protects it form virus and malware attacks.

g) Employ multiple layers of security. For e.g. spam filters help in weeding out malware

and viruses.

h) It is very crucial to scan any new device that is being connected to the system in order

to protect it from virus attack.

i) Encourage employee education and training on the matter, as they are ones who are

handling the data. Educate them about the relevance and importance of the data.

The most important point among the above-mentioned ones according to me is installation of

the latest operating systems and antivirus software’s within the system of the organisation.

This is because of the fact that the real threat in the modern day world crops up from the

external environment of the organisation than the internal one. Competitors and other entities

with malicious interests are always on hunt for personal data of the general public thorough

ejaculation of various types of viruses and malwares. Hence, it is of utmost importance that

proper steps are taken to stop them from entering the system by installing proper firewall

methods.

A6 © AAMC Training Group Assessment V2.4

Specialist Consultation: provided

2 Product name: Beyond Bank low rate car loan

Interest Rate: 5.69% (fixed)

Comparison rate: 5.97%

Interest rate type: Fixed

Loan security: secured

Early repayment fees: not applied

Loan term: 7 years

Establishment fees: $175

12. Using a search engine, research “Ten tips to protect your customers’ personal

information”. Select one of the 10 points and in your own words briefly describe the

purpose of this step.

Top ten tips to protect our customer’s personal information are as follows:

a) Installing reasonable security measures to ensure the customer’s personal information

is safe from unauthorised and inappropriate access.

b) Make a stringent privacy policy, inform the customer about the same, and keep it

accessible to the customer.

c) Take record of all the information that you have, the place where it is stored.It should

be noted that person that has access to this information.

d) Never underestimate the threat depending on the size of the organisation.

e) Only collect that information which are required for your purpose. Avoid taking useless

and bulk information from the customers.

f) Use the latest anti-virus software’s, operating software’s and web browser. This

protects it form virus and malware attacks.

g) Employ multiple layers of security. For e.g. spam filters help in weeding out malware

and viruses.

h) It is very crucial to scan any new device that is being connected to the system in order

to protect it from virus attack.

i) Encourage employee education and training on the matter, as they are ones who are

handling the data. Educate them about the relevance and importance of the data.

The most important point among the above-mentioned ones according to me is installation of

the latest operating systems and antivirus software’s within the system of the organisation.

This is because of the fact that the real threat in the modern day world crops up from the

external environment of the organisation than the internal one. Competitors and other entities

with malicious interests are always on hunt for personal data of the general public thorough

ejaculation of various types of viruses and malwares. Hence, it is of utmost importance that

proper steps are taken to stop them from entering the system by installing proper firewall

methods.

A6 © AAMC Training Group Assessment V2.4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FNSSAM403 Prospect for new clients

13. You have completed a fact finder, costing analysis, and LVR calculation for a client and

have worked out the due to affordability issues, based on the living expenses they

have provided, the client is unable to borrow the required loan amount. They would be

able to borrow a loan amount of $5,000 less. Referring back to your client needs

review, what additional question/s would you ask the client?

The difference in the loan amount due to the expenses of the client is very minimal. Hence

some of my question to the client will be as follows:

1) Is it possible for him to identify and then reduce non-essential living expenditure in

order to meet up the funds required to finance the entire amount of loan?

2) Is he willing to consider some other affordable options which would not require him to

cut down his present expenses?

14. After you have completed the product research how would you prepare for the next

contact?

In order to prepare for the next contact the following steps will be taken:

a) Use a follow up schedule: it will contain the details regarding when the calls and email

follow-ups should be happening.

b) Use of different contact formats: use of multiple mode of contacts like txt, email etc.

c) Getting agreement on the next steps: further follow-ups with the customers should be

stopped if they do not agree to it. It should be ensured that irrespective of their

enthusiasm, a permission is obtained for further follow ups.

Task 2 – Written Test

1. List six buyer motives and in your own words, analyse and discuss issues relating to two

of them.

1 Profit This motive is most common as it is for a gain, it can be

short term or long term

2 Fear of loss

3 Comfort

4 Security This reason occurs when one want to protect his future.

5 Pride and Prestige

6 Emotional satisfaction

2. Using conflict resolution and persuasion techniques, write a response to the following

examples of buyer resistance:

Not interested It is very justified to be not interested by a short phone call. But,

a first-hand experience of our product will definitely create value

for you with very minimal cost. It will require only fifteen

minutes

Assessment V2.4 © AAMC

Training Group A7

13. You have completed a fact finder, costing analysis, and LVR calculation for a client and

have worked out the due to affordability issues, based on the living expenses they

have provided, the client is unable to borrow the required loan amount. They would be

able to borrow a loan amount of $5,000 less. Referring back to your client needs

review, what additional question/s would you ask the client?

The difference in the loan amount due to the expenses of the client is very minimal. Hence

some of my question to the client will be as follows:

1) Is it possible for him to identify and then reduce non-essential living expenditure in

order to meet up the funds required to finance the entire amount of loan?

2) Is he willing to consider some other affordable options which would not require him to

cut down his present expenses?

14. After you have completed the product research how would you prepare for the next

contact?

In order to prepare for the next contact the following steps will be taken:

a) Use a follow up schedule: it will contain the details regarding when the calls and email

follow-ups should be happening.

b) Use of different contact formats: use of multiple mode of contacts like txt, email etc.

c) Getting agreement on the next steps: further follow-ups with the customers should be

stopped if they do not agree to it. It should be ensured that irrespective of their

enthusiasm, a permission is obtained for further follow ups.

Task 2 – Written Test

1. List six buyer motives and in your own words, analyse and discuss issues relating to two

of them.

1 Profit This motive is most common as it is for a gain, it can be

short term or long term

2 Fear of loss

3 Comfort

4 Security This reason occurs when one want to protect his future.

5 Pride and Prestige

6 Emotional satisfaction

2. Using conflict resolution and persuasion techniques, write a response to the following

examples of buyer resistance:

Not interested It is very justified to be not interested by a short phone call. But,

a first-hand experience of our product will definitely create value

for you with very minimal cost. It will require only fifteen

minutes

Assessment V2.4 © AAMC

Training Group A7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FNSSAM403 Prospect for new clients

Send me some

information

It is possible for me to send entire information available with to you

right now. But, it is seen that it raises more doubts in the minds of

the customer rather than solving them. Hence the better

alternative would be to use just 15 minutes of your time to

consider it and analyse it thereupon.

No money –

Can’t afford it

I am aware about the fact that your aim is to reduce unnecessary

expenditures. I am just suggesting you to evaluate the product and

am confident that you will find it as a small investment rather than

a cost.

You’re wasting

your time

Sir we never consider an interaction with a business professional to

be waste of time. I am assured that after evaluating out product

you will be sure that it can create more returns for you compared

to its meagre cost.

3. How do you successfully undertake cold calling? Explain the process from start to finish.

In order to ensure that the cold calling is carried out successfully the speaker must be

aware about the type of person he is dealing with and the person speaking to the client

must be aware about the subject matter precisely. The process of cold calling can be

summarised as follows:

a) Polite introduction of the person making the call and the product on offer.

b) Asking about the specific requirements of the client related to the product on offer.

c) Patiently listening to the response of the prospective customer and then framing the

next phrase with utmost intelligence so as to ensure that the speaker and the product

will be adding value to the client.

d) Informing the client about the specific product and its utilities and relevance to the

customer but not trying to sell.

e) After informing take notes about the concerns of the customer related to the products

preferably taking of notes in order to address the issues raised by the customer.

4. Read the following article, and answer the questions below.

A8 © AAMC Training Group Assessment V2.4

Send me some

information

It is possible for me to send entire information available with to you

right now. But, it is seen that it raises more doubts in the minds of

the customer rather than solving them. Hence the better

alternative would be to use just 15 minutes of your time to

consider it and analyse it thereupon.

No money –

Can’t afford it

I am aware about the fact that your aim is to reduce unnecessary

expenditures. I am just suggesting you to evaluate the product and

am confident that you will find it as a small investment rather than

a cost.

You’re wasting

your time

Sir we never consider an interaction with a business professional to

be waste of time. I am assured that after evaluating out product

you will be sure that it can create more returns for you compared

to its meagre cost.

3. How do you successfully undertake cold calling? Explain the process from start to finish.

In order to ensure that the cold calling is carried out successfully the speaker must be

aware about the type of person he is dealing with and the person speaking to the client

must be aware about the subject matter precisely. The process of cold calling can be

summarised as follows:

a) Polite introduction of the person making the call and the product on offer.

b) Asking about the specific requirements of the client related to the product on offer.

c) Patiently listening to the response of the prospective customer and then framing the

next phrase with utmost intelligence so as to ensure that the speaker and the product

will be adding value to the client.

d) Informing the client about the specific product and its utilities and relevance to the

customer but not trying to sell.

e) After informing take notes about the concerns of the customer related to the products

preferably taking of notes in order to address the issues raised by the customer.

4. Read the following article, and answer the questions below.

A8 © AAMC Training Group Assessment V2.4

FNSSAM403 Prospect for new clients

Information in this article may not be based on current market

statistics and is for assessment purposes only

Why Melbourne’s Properties Will Keep On Rising

In Australia, over some 120 years or so of not quite so accurate statistics, property

prices have risen at an average compound rate of 10.4%, very slightly ahead of

England. Again, property prices have doubled every 7 years or so despite droughts,

wars, changes of government, interstate and overseas migration, interest rate

movements, exchange rate movements, changing rates of unemployment, CPI

movements, etc.

Property cycles

When one takes a short-term view of property price movements, one can get confused

by apparently contradictory statistics. However, if you understand that property prices

move in 7-10 year cycles, the picture becomes a lot clearer.

Let’s take one obvious example. The movement in NSW and Victorian property prices

tend to be counter-cyclical to Queensland prices (especially South East Queensland).

This is heavily influenced by what is happening in the NSW & Victorian economics which

encourages migration to Queensland, and at other times in the cycle, people returning

to NSW and Victoria.

So, when Queensland prices are moving ahead strongly (because of this additional

demand from interstate migration), prices in NSW and Victoria exhibit slower growth,

and vice versa.

A study of cycles shows that the Sydney market is much more volatile than, for

example, the Melbourne market. Sydney prices rise faster but can also experience

significant falls in each cycle – Melbourne prices tend to rise rapidly (+25%, +20%) in

the first two years of an upturn and then more moderate increases of 3-7% in the

remaining years of the cycle till growth spurts again.

Relative prices in each capital city

Over the last 100+ years in Australia, each of the six State and Territory capitals have

established a fairly stable ranking with each other in terms of their median house and

apartment prices.

Traditionally, Sydney has always been the most expensive followed by Melbourne,

Canberra, Brisbane, Perth, Adelaide, Darwin & Hobart. Increases in prices in each of

these markets, for whatever reasons (mining booms, economic recessions, rural booms

and droughts etc) can cause some temporary shifts in the relative standing of each of

these cities. But these are normally temporary shifts and the long-term standings re-

assert themselves as the various cycles evolve.

continued on the next page

Assessment V2.4 © AAMC

Training Group A9

Information in this article may not be based on current market

statistics and is for assessment purposes only

Why Melbourne’s Properties Will Keep On Rising

In Australia, over some 120 years or so of not quite so accurate statistics, property

prices have risen at an average compound rate of 10.4%, very slightly ahead of

England. Again, property prices have doubled every 7 years or so despite droughts,

wars, changes of government, interstate and overseas migration, interest rate

movements, exchange rate movements, changing rates of unemployment, CPI

movements, etc.

Property cycles

When one takes a short-term view of property price movements, one can get confused

by apparently contradictory statistics. However, if you understand that property prices

move in 7-10 year cycles, the picture becomes a lot clearer.

Let’s take one obvious example. The movement in NSW and Victorian property prices

tend to be counter-cyclical to Queensland prices (especially South East Queensland).

This is heavily influenced by what is happening in the NSW & Victorian economics which

encourages migration to Queensland, and at other times in the cycle, people returning

to NSW and Victoria.

So, when Queensland prices are moving ahead strongly (because of this additional

demand from interstate migration), prices in NSW and Victoria exhibit slower growth,

and vice versa.

A study of cycles shows that the Sydney market is much more volatile than, for

example, the Melbourne market. Sydney prices rise faster but can also experience

significant falls in each cycle – Melbourne prices tend to rise rapidly (+25%, +20%) in

the first two years of an upturn and then more moderate increases of 3-7% in the

remaining years of the cycle till growth spurts again.

Relative prices in each capital city

Over the last 100+ years in Australia, each of the six State and Territory capitals have

established a fairly stable ranking with each other in terms of their median house and

apartment prices.

Traditionally, Sydney has always been the most expensive followed by Melbourne,

Canberra, Brisbane, Perth, Adelaide, Darwin & Hobart. Increases in prices in each of

these markets, for whatever reasons (mining booms, economic recessions, rural booms

and droughts etc) can cause some temporary shifts in the relative standing of each of

these cities. But these are normally temporary shifts and the long-term standings re-

assert themselves as the various cycles evolve.

continued on the next page

Assessment V2.4 © AAMC

Training Group A9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FNSSAM403 Prospect for new clients

In the last 3-4 years, Perth & Darwin prices (and to a lesser extent Adelaide and

Brisbane prices) have increased dramatically due to the boom in mining and oil

company revenues and increased demand for labour (and therefore housing) in those

cities. Sydney and Melbourne prices, while still rising, have slipped behind these other

cities in terms of relative price increases.

Basic demand & supply

The ever-increasing need for housing in Melbourne and Sydney is not based on

temporary boom factors but on underlying (substantial and permanent) shifts in

population. Each city has a strong underlying economy, which is not dependent on one

particular industry. In addition, estimates of Melbourne’s population for 2020 is over

four million people (an approximate increase of 25% in 13 years). This is huge in terms

of population increase and the need to accommodate these extra people.

The reality is that Melbourne’s building industry cannot build more than about 140,000

accommodation units (houses and apartments) per annum due to shortages of qualified

tradespeople of all types and shortage of suitably zoned land and the building permit

process. Demand, on the other hand, is estimated at approximately 170,000

accommodation units per annum. Added to this, State and Federal governments have

all but completely removed themselves from supply of affordable housing.

The inevitable consequence is that house and apartment prices will continue to rise

(quickly over the next 2-3 years and then more moderately). And rentals, which are

already moving up quickly, will continue to rise ahead of CPI.

Relativities with other capital cities will be restored by above average price increases in

Melbourne and then Sydney.

Interest rates

The spectre of a return to 16-17% interest rates (experienced only once in Australia’s

history and then only for a few months in 1990) has loomed large in many would-be

investors’ minds. This fear is understandable but not justified.

Interest rates are now approximately 1-1.5% above the lowest they have been in the

last 40 years. From an economist’s viewpoint, they are currently above the theoretical

long-term average that they should be (arrived at by adding the present CPI increase

and the additional incentive needed to be offered for people to save and lend their

money to others – historically 1.5-2.0%).

Currently rates are above their theoretically justified level. This is not to say that the

Reserve Bank will not use one or even two more 0.25 per cent interest rate rises to send

a message to the market not to get “overheated”. Even two such increases will leave

interest rates within 2% of their 40-year lows. A 0.25% per cent increase in the average

mortgage of around $220,000 is equivalent to an extra $10.60 per week ($45.80 per

month) in repayments.

By comparison, a 10% increase in the median house price in Melbourne is equivalent to

an $817 per week ($3542 per month) increase in the owner’s wealth.

continued on the next page

A10 © AAMC Training Group Assessment V2.4

In the last 3-4 years, Perth & Darwin prices (and to a lesser extent Adelaide and

Brisbane prices) have increased dramatically due to the boom in mining and oil

company revenues and increased demand for labour (and therefore housing) in those

cities. Sydney and Melbourne prices, while still rising, have slipped behind these other

cities in terms of relative price increases.

Basic demand & supply

The ever-increasing need for housing in Melbourne and Sydney is not based on

temporary boom factors but on underlying (substantial and permanent) shifts in

population. Each city has a strong underlying economy, which is not dependent on one

particular industry. In addition, estimates of Melbourne’s population for 2020 is over

four million people (an approximate increase of 25% in 13 years). This is huge in terms

of population increase and the need to accommodate these extra people.

The reality is that Melbourne’s building industry cannot build more than about 140,000

accommodation units (houses and apartments) per annum due to shortages of qualified

tradespeople of all types and shortage of suitably zoned land and the building permit

process. Demand, on the other hand, is estimated at approximately 170,000

accommodation units per annum. Added to this, State and Federal governments have

all but completely removed themselves from supply of affordable housing.

The inevitable consequence is that house and apartment prices will continue to rise

(quickly over the next 2-3 years and then more moderately). And rentals, which are

already moving up quickly, will continue to rise ahead of CPI.

Relativities with other capital cities will be restored by above average price increases in

Melbourne and then Sydney.

Interest rates

The spectre of a return to 16-17% interest rates (experienced only once in Australia’s

history and then only for a few months in 1990) has loomed large in many would-be

investors’ minds. This fear is understandable but not justified.

Interest rates are now approximately 1-1.5% above the lowest they have been in the

last 40 years. From an economist’s viewpoint, they are currently above the theoretical

long-term average that they should be (arrived at by adding the present CPI increase

and the additional incentive needed to be offered for people to save and lend their

money to others – historically 1.5-2.0%).

Currently rates are above their theoretically justified level. This is not to say that the

Reserve Bank will not use one or even two more 0.25 per cent interest rate rises to send

a message to the market not to get “overheated”. Even two such increases will leave

interest rates within 2% of their 40-year lows. A 0.25% per cent increase in the average

mortgage of around $220,000 is equivalent to an extra $10.60 per week ($45.80 per

month) in repayments.

By comparison, a 10% increase in the median house price in Melbourne is equivalent to

an $817 per week ($3542 per month) increase in the owner’s wealth.

continued on the next page

A10 © AAMC Training Group Assessment V2.4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FNSSAM403 Prospect for new clients

Rents

The level of rents (determined by supply & demand) and the value of the properties to

which they relate establish the rental return per annum. The rental return rises and falls

at different times in the cycle as real rents and property prices move up at different rates.

Rental returns on residential property tend to vary between about 3.5-4.0% and 5.5-6.0%.

Melbourne’s rental returns have moved very close to the top end of this range and are

showing every sign of continuing to rise further as vacancy rates continue to show a decline

from over 4% to a little over 1.1% in most parts of Melbourne. The city’s long-term

imbalance between the new accommodation that can be supplied and the level demanded

by increased population/increased member of new household formations noted above,

allows the actual level of rents to continue to rise quite quickly. This will attract new

investors into the residential house and apartment markets, which will, in turn, keep

pushing prices up.

Housing affordability

There is much debate about whether houses have become “unaffordable” for young

couples. Much research has been done on the number of years’ salary it takes to buy

the “average” house, and the proportion of income taken up by mortgage repayments.

This is a very complicated issue, which has received a lot of publicity during this faux

election campaign. Despite all the rhetoric I have seen no viable recommendations

come forward and even less political commitment to solving the problem.

My view is that Australia (which has enjoyed the highest rate of home ownership in the

world) will slip in the world rankings. Those who have parents who can help them will

still be able to buy a home (especially with abundant bank credit persisting) while those

who don’t may be consigned to a life of renting. This will further stratify Australian

society with the rich getting richer and the poor getting comparatively poorer. This,

combined with governments removing themselves from constructing accommodation,

will put more reliance on a healthy private rental market and make it suicidal for

governments to remove or reduce investment incentives.

Where are we now?

The above factors of:

Over 900 years of compound growth in residential property values;

Where Melbourne prices are in the current price cycle;

Where Melbourne prices are vis a vis other capital city prices right now;

The short, medium and long term population forecasts for Melbourne;

The building industry’s restricted capacity to build new accommodation units;

Where we are in terms of interest rates v capital growth;

The continuation in the rise in rents and the very low vacancy factor; and

The lack of any coherent way of easing the pressures on accommodation

5.

Assessment V2.4 © AAMC

Training Group A11

Rents

The level of rents (determined by supply & demand) and the value of the properties to

which they relate establish the rental return per annum. The rental return rises and falls

at different times in the cycle as real rents and property prices move up at different rates.

Rental returns on residential property tend to vary between about 3.5-4.0% and 5.5-6.0%.

Melbourne’s rental returns have moved very close to the top end of this range and are

showing every sign of continuing to rise further as vacancy rates continue to show a decline

from over 4% to a little over 1.1% in most parts of Melbourne. The city’s long-term

imbalance between the new accommodation that can be supplied and the level demanded

by increased population/increased member of new household formations noted above,

allows the actual level of rents to continue to rise quite quickly. This will attract new

investors into the residential house and apartment markets, which will, in turn, keep

pushing prices up.

Housing affordability

There is much debate about whether houses have become “unaffordable” for young

couples. Much research has been done on the number of years’ salary it takes to buy

the “average” house, and the proportion of income taken up by mortgage repayments.

This is a very complicated issue, which has received a lot of publicity during this faux

election campaign. Despite all the rhetoric I have seen no viable recommendations

come forward and even less political commitment to solving the problem.

My view is that Australia (which has enjoyed the highest rate of home ownership in the

world) will slip in the world rankings. Those who have parents who can help them will

still be able to buy a home (especially with abundant bank credit persisting) while those

who don’t may be consigned to a life of renting. This will further stratify Australian

society with the rich getting richer and the poor getting comparatively poorer. This,

combined with governments removing themselves from constructing accommodation,

will put more reliance on a healthy private rental market and make it suicidal for

governments to remove or reduce investment incentives.

Where are we now?

The above factors of:

Over 900 years of compound growth in residential property values;

Where Melbourne prices are in the current price cycle;

Where Melbourne prices are vis a vis other capital city prices right now;

The short, medium and long term population forecasts for Melbourne;

The building industry’s restricted capacity to build new accommodation units;

Where we are in terms of interest rates v capital growth;

The continuation in the rise in rents and the very low vacancy factor; and

The lack of any coherent way of easing the pressures on accommodation

5.

Assessment V2.4 © AAMC

Training Group A11

FNSSAM403 Prospect for new clients

a. Explain three points from this article that would appeal to/encourage investors seeking

to buy more property in Melbourne.

The three points which can be taken out from this article with respect to the high

probability that the investors will be encouraged to buy more property in Melbourne are as

follows:

1) Stability in prices: compared to other states such as Sydney the prices of

Melbourne may rise about 20 -22% in case of an uptrend but doesn’t fall back

drastically like in the case of Sydney. Rather it continues to grow at a slower

rate of 3%-7%.

2) Rise in the demand: it is expected that the population of the city by the year

2020 would be around 4 million and this boils down to the demand of around

170000 accommodations whereas the with all the available resources available

it is only possible to make around 140000 houses per year.

3) Increased rental income: the rental income prevalent In Australia gives a return

of around 3.5%-4% and the rental income of the city has notched itself up to

the higher end of this level. Further the economists believe that it is going to

rise further.

b. Why would it be prudent for a person to hold on to property over the long term?

It is very prudent for any person to hold on to any property he has in Australia for the

longer run. This is because of the everyday rising demand for them. The demand is not

expected to stop as the government is not going to participate in making

accommodation in the new future. Hence the value of the property simply due to the

effect of demand will grow over the period.

c. Why will housing continue to become unaffordable for first home buyers?

The housing will continue to grow costlier for the new buyers because it entails

consumption of their significant portion of their salary. The government is reluctant to

take part in making homes for the people at affordable prices.

5. List six different prospecting methods and in your own words, compare and contrast two

of them.

The six different prospecting methods are as follows:

1) Cold calling

2) Referrals

3) Content marketing

4) Networking

5) Email marketing

A12 © AAMC Training Group Assessment V2.4

a. Explain three points from this article that would appeal to/encourage investors seeking

to buy more property in Melbourne.

The three points which can be taken out from this article with respect to the high

probability that the investors will be encouraged to buy more property in Melbourne are as

follows:

1) Stability in prices: compared to other states such as Sydney the prices of

Melbourne may rise about 20 -22% in case of an uptrend but doesn’t fall back

drastically like in the case of Sydney. Rather it continues to grow at a slower

rate of 3%-7%.

2) Rise in the demand: it is expected that the population of the city by the year

2020 would be around 4 million and this boils down to the demand of around

170000 accommodations whereas the with all the available resources available

it is only possible to make around 140000 houses per year.

3) Increased rental income: the rental income prevalent In Australia gives a return

of around 3.5%-4% and the rental income of the city has notched itself up to

the higher end of this level. Further the economists believe that it is going to

rise further.

b. Why would it be prudent for a person to hold on to property over the long term?

It is very prudent for any person to hold on to any property he has in Australia for the

longer run. This is because of the everyday rising demand for them. The demand is not

expected to stop as the government is not going to participate in making

accommodation in the new future. Hence the value of the property simply due to the

effect of demand will grow over the period.

c. Why will housing continue to become unaffordable for first home buyers?

The housing will continue to grow costlier for the new buyers because it entails

consumption of their significant portion of their salary. The government is reluctant to

take part in making homes for the people at affordable prices.

5. List six different prospecting methods and in your own words, compare and contrast two

of them.

The six different prospecting methods are as follows:

1) Cold calling

2) Referrals

3) Content marketing

4) Networking

5) Email marketing

A12 © AAMC Training Group Assessment V2.4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.