FNSSINC601: Applying Economic Principles in the Financial Industry

VerifiedAdded on 2023/06/08

|13

|3153

|287

Report

AI Summary

This report delves into the application of economic principles within the finance industry, focusing on the oligopolistic nature of the Australian banking sector and the dominance of the 'Big Four' banks. It examines the impact of market concentration, pricing power, and regulatory policies on competition and efficiency. The report also covers key economic concepts such as classical and Keynesian economics, capital adequacy requirements, asset pricing models, and the role of government policies. Additionally, it discusses the importance of economic principles in decision-making, performance evaluation, and understanding market dynamics. The document concludes by highlighting the significance of maintaining a strong understanding of economic policies for effective work in the financial services industry. Desklib provides access to this report and other resources to support students' learning.

Running head: ECONOMIC PRINCIPLES OF FINANCE INDUSTRY

Economic Principles in Finance Industry

Name of the Student

Name of the University

Author note

Economic Principles in Finance Industry

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMIC PRINCIPLES OF FINANCE INDUSTRY

Table of Contents

AS ligopoly inT K 1: O Australian ankingB ............................................................................................2

AST K 2....................................................................................................................................................4

SQUE TION 1.......................................................................................................................................4

SQUE TION 2.......................................................................................................................................5

SQUE TION 3.......................................................................................................................................5

SQUE TION 4.......................................................................................................................................5

SQUE TION 5.......................................................................................................................................6

SQUE TION 7.......................................................................................................................................6

SQUE TION 8.......................................................................................................................................6

SQUE TION 9.......................................................................................................................................7

Activity4.3 ...............................................................................................................................................7

R R C SEFE EN E LI T...................................................................................................................................10

Table of Contents

AS ligopoly inT K 1: O Australian ankingB ............................................................................................2

AST K 2....................................................................................................................................................4

SQUE TION 1.......................................................................................................................................4

SQUE TION 2.......................................................................................................................................5

SQUE TION 3.......................................................................................................................................5

SQUE TION 4.......................................................................................................................................5

SQUE TION 5.......................................................................................................................................6

SQUE TION 7.......................................................................................................................................6

SQUE TION 8.......................................................................................................................................6

SQUE TION 9.......................................................................................................................................7

Activity4.3 ...............................................................................................................................................7

R R C SEFE EN E LI T...................................................................................................................................10

ECONOMIC PRINCIPLES OF FINANCE INDUSTRY

TASK 1: Oligopoly in Australian Banking

Oligopoly in the banking industry is not an unusual phenomenon. The involving

characteristics of banking industry such as economies of scale and small retail margin of

banks. Banking industry in Australia has become increasingly concentrated with four major

banks dominating the industry. It has been determined by the Australian Government that the

four major banks have a significant pricing power. In case of an oligopoly market where only

few firms compete. The “Big four banks” of Australia which have the largest share of the

market are National Australia Bank, Westpac, Commonwealth Bank and Australia and New

Zealand Banking Group(Andrievskaya and Semenova, 2016.). These four banks dominate

the banking industry. However, Australia has a very profitable and competitive financial

sector. The four financial sectors in order to increase their profits can set any prices without

the fear of loosing the market share. These four famous banks of Australia form a cartel

arrangement in a way that the shareholders tries to maximize profits acting as a monopoly

market structure. The cartel formation therefore acts as a barrier to entry for the new entrants

in the banking industry of Australia. These banks have a higher interest margins which makes

them even more profitable. The banking sector of Australia is oligopolistic in way that they

maintain their position in the market with the help of opaque pricing. In case of an oligopoly

market the firms usually depend upon each other while deciding the price(Salim, Arjomandi

and Seufert, 2016). The banking sector in Australia is therefore oligopoly. The four major

banks of Australia comprises of eighty five percent of the banking industry. Due to the

oligopolistic market in the banking sectors of Australia, it is very difficult for any new entrant

to compete with the “big four”.

There is also a presence of market concentration within the four banks. According to a

recent research the biggest four banks of Australia will make a profit of around A$6.2 billion

TASK 1: Oligopoly in Australian Banking

Oligopoly in the banking industry is not an unusual phenomenon. The involving

characteristics of banking industry such as economies of scale and small retail margin of

banks. Banking industry in Australia has become increasingly concentrated with four major

banks dominating the industry. It has been determined by the Australian Government that the

four major banks have a significant pricing power. In case of an oligopoly market where only

few firms compete. The “Big four banks” of Australia which have the largest share of the

market are National Australia Bank, Westpac, Commonwealth Bank and Australia and New

Zealand Banking Group(Andrievskaya and Semenova, 2016.). These four banks dominate

the banking industry. However, Australia has a very profitable and competitive financial

sector. The four financial sectors in order to increase their profits can set any prices without

the fear of loosing the market share. These four famous banks of Australia form a cartel

arrangement in a way that the shareholders tries to maximize profits acting as a monopoly

market structure. The cartel formation therefore acts as a barrier to entry for the new entrants

in the banking industry of Australia. These banks have a higher interest margins which makes

them even more profitable. The banking sector of Australia is oligopolistic in way that they

maintain their position in the market with the help of opaque pricing. In case of an oligopoly

market the firms usually depend upon each other while deciding the price(Salim, Arjomandi

and Seufert, 2016). The banking sector in Australia is therefore oligopoly. The four major

banks of Australia comprises of eighty five percent of the banking industry. Due to the

oligopolistic market in the banking sectors of Australia, it is very difficult for any new entrant

to compete with the “big four”.

There is also a presence of market concentration within the four banks. According to a

recent research the biggest four banks of Australia will make a profit of around A$6.2 billion

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMIC PRINCIPLES OF FINANCE INDUSTRY

over the next four years. As a result of the rise in market concentration in the banking

industry of Australia , there has been decrease in the market competition which lead to

increase in inefficiencies. As a result of these the banks acts as a monopoly and charges a

similar interest rates thereby decreasing market competition(Andrievskaya and Semenova,

2016). The government also supported the oligopoly market of the banking sector in

Australia where the finance minister claimed to support oligopoly in the banking industry.

High level of concentration in the market also reported to have higher prices along with

decrease in the competitiveness in the market. As a result of this the customers used to have

blind faith in these banks and therefore, it also resulted to huge profitability. In the year 2010,

the banks of Australia had also increased its lending rates in case of housing loans.

Oligopolistic markets tends to set up high barriers for entry and also depends on how the

other firms in the market depends. The Australian banking sector therefore has the similar

characteristics. According to the Australian Banking and financial report, the financial

institutions of Australia has both cost and scale advantages along with investment advantage.

The banking industry of Australia had a highly concentrated Herfindahl Hirschman

Index. As a result of the acquisition taken place by Westpac and the Commonwealth Bank of

Australia, there had been increase in the market concentration over the years. As a result of

market concentration there has been rise in the profitability(Turner and Nugent 2015). The

market leaders are therefore able to manipulate the market. The shareholders of the ‘big four”

are similar though the “ big four” are the different entities altogether. However, there had

been a lot of reform in the banking sector of Australia. As a result of rise in the con centration

in the market, there had been a lot of reports of the economic inefficiencies. There had been

also a result of increase in the consumer surplus due to the monopolistic behavior of the

banks. The four pillar policies were made by the Australian government in order to avoid the

mergers of the four major Australian banks. The policies had also been criticized for not been

over the next four years. As a result of the rise in market concentration in the banking

industry of Australia , there has been decrease in the market competition which lead to

increase in inefficiencies. As a result of these the banks acts as a monopoly and charges a

similar interest rates thereby decreasing market competition(Andrievskaya and Semenova,

2016). The government also supported the oligopoly market of the banking sector in

Australia where the finance minister claimed to support oligopoly in the banking industry.

High level of concentration in the market also reported to have higher prices along with

decrease in the competitiveness in the market. As a result of this the customers used to have

blind faith in these banks and therefore, it also resulted to huge profitability. In the year 2010,

the banks of Australia had also increased its lending rates in case of housing loans.

Oligopolistic markets tends to set up high barriers for entry and also depends on how the

other firms in the market depends. The Australian banking sector therefore has the similar

characteristics. According to the Australian Banking and financial report, the financial

institutions of Australia has both cost and scale advantages along with investment advantage.

The banking industry of Australia had a highly concentrated Herfindahl Hirschman

Index. As a result of the acquisition taken place by Westpac and the Commonwealth Bank of

Australia, there had been increase in the market concentration over the years. As a result of

market concentration there has been rise in the profitability(Turner and Nugent 2015). The

market leaders are therefore able to manipulate the market. The shareholders of the ‘big four”

are similar though the “ big four” are the different entities altogether. However, there had

been a lot of reform in the banking sector of Australia. As a result of rise in the con centration

in the market, there had been a lot of reports of the economic inefficiencies. There had been

also a result of increase in the consumer surplus due to the monopolistic behavior of the

banks. The four pillar policies were made by the Australian government in order to avoid the

mergers of the four major Australian banks. The policies had also been criticized for not been

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMIC PRINCIPLES OF FINANCE INDUSTRY

competitive. The banks of Australia had therefore adopted the four pillar policies to avoid

acquisitions. Along with adopting the policies the banks also had monopolistic nature which

lead to the rise in deadweight loss which the society actually suffers. The banking industry

structure of Australia therefore acts similar to an oligopoly market. With the help of

concentration ratio and the Herfindahl Hirschman Index the competition within an industry

can be measured(Salim, Arjomandi and Seufert 2016). The banking sector market of

Australia is dominated by the only four banks out of fifty four banks. In the fiscal year of

2017 it had earned a profit of A$31.5 billion. As a result of highly concentrated market, the

performance of the banks are also affected. However the dominating firms enjoy higher

profitability as they can implement prices and charges according to their will.

The big four banks of Australia therefore seemed to have an oligopolistic market. It

also has a high market concentration along with high HHI index. High concentration in

market has led to low market efficiencies(Andrievskaya and Semenova2016). Therefore, in

order to increase the market efficiencies there is a need of regulation for the banks. However,

the regulation of the large banks will not be possible by the domestic banks as they will not

be able to compete with the large banks. However, the entry of global banks in the Australian

banking sector is recommended which can very well lower the concentration in market.

Therefore, in order to conclude it can be stated that the banking sector of Australia has both

oligopoly and monopolistic competition.

TASK 2

QUESTION 1

a) Classical economics – it originated in the late eighteenth century which refers to the

dominant school of thought for economics whose originator was the economist Adam

Smith.

competitive. The banks of Australia had therefore adopted the four pillar policies to avoid

acquisitions. Along with adopting the policies the banks also had monopolistic nature which

lead to the rise in deadweight loss which the society actually suffers. The banking industry

structure of Australia therefore acts similar to an oligopoly market. With the help of

concentration ratio and the Herfindahl Hirschman Index the competition within an industry

can be measured(Salim, Arjomandi and Seufert 2016). The banking sector market of

Australia is dominated by the only four banks out of fifty four banks. In the fiscal year of

2017 it had earned a profit of A$31.5 billion. As a result of highly concentrated market, the

performance of the banks are also affected. However the dominating firms enjoy higher

profitability as they can implement prices and charges according to their will.

The big four banks of Australia therefore seemed to have an oligopolistic market. It

also has a high market concentration along with high HHI index. High concentration in

market has led to low market efficiencies(Andrievskaya and Semenova2016). Therefore, in

order to increase the market efficiencies there is a need of regulation for the banks. However,

the regulation of the large banks will not be possible by the domestic banks as they will not

be able to compete with the large banks. However, the entry of global banks in the Australian

banking sector is recommended which can very well lower the concentration in market.

Therefore, in order to conclude it can be stated that the banking sector of Australia has both

oligopoly and monopolistic competition.

TASK 2

QUESTION 1

a) Classical economics – it originated in the late eighteenth century which refers to the

dominant school of thought for economics whose originator was the economist Adam

Smith.

ECONOMIC PRINCIPLES OF FINANCE INDUSTRY

b) Keynesian economics – Keynesian economics was founded by John Maynard Keynes

after Great Depression is an economic theory of total spending and its effects on output.

c) Supply side economics- this is a theory of macroeconomics which states that

economic growth can be achieved with the help of tax cuts.

QUESTION 2

a) Mortgages and interest rates- the longer the time taken to pay the mortgage, the

buying cost of the houses become higher because interest is need to be paid for the

longer period of time( Hasan 2013).

b) Insurance premiums for motor vehicles- it is also known as automotive insurance

where the insurer assumes that any loss may incur through the result of accident.

QUESTION 3

Capital adequacy requirement is considered as the amount of capital that the banks or

other financial institutions have to hold as per the requirement by the financial regulators.

This capital adequacy requirement is expressed in the form of capital adequacy ratio of equity

and the banks or other financial institutions are required to hold this ratio as a percentage of

the risk-weighted assets (Fatima 2014).

QUESTION 4

The Capital Asset Pricing Model is considered as a financial model that helps in

describing the relationship between systematic risk and expected returns for the assets or

particular stock. The wide application of capital asset pricing model can be seen throughout

the finance process in order o price the risky securities, to generate expected returns for the

assets and to calculate the costs of capital (Ross 2013).

b) Keynesian economics – Keynesian economics was founded by John Maynard Keynes

after Great Depression is an economic theory of total spending and its effects on output.

c) Supply side economics- this is a theory of macroeconomics which states that

economic growth can be achieved with the help of tax cuts.

QUESTION 2

a) Mortgages and interest rates- the longer the time taken to pay the mortgage, the

buying cost of the houses become higher because interest is need to be paid for the

longer period of time( Hasan 2013).

b) Insurance premiums for motor vehicles- it is also known as automotive insurance

where the insurer assumes that any loss may incur through the result of accident.

QUESTION 3

Capital adequacy requirement is considered as the amount of capital that the banks or

other financial institutions have to hold as per the requirement by the financial regulators.

This capital adequacy requirement is expressed in the form of capital adequacy ratio of equity

and the banks or other financial institutions are required to hold this ratio as a percentage of

the risk-weighted assets (Fatima 2014).

QUESTION 4

The Capital Asset Pricing Model is considered as a financial model that helps in

describing the relationship between systematic risk and expected returns for the assets or

particular stock. The wide application of capital asset pricing model can be seen throughout

the finance process in order o price the risky securities, to generate expected returns for the

assets and to calculate the costs of capital (Ross 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMIC PRINCIPLES OF FINANCE INDUSTRY

QUESTION 5

Some of the major reasons for property revaluation are to gain understanding about

the difference between value and price; to gain effective guideline for the investment

decisions; to get the correct market value of the property at the time of selling or buying; to

obtain the legal documents about the property; to know the extent of tax deduction and others

(Beaglehole 2015).

QUESTION 6

The main use of Compound Interest can be seen for the calculation of interest on the

initial principles along with the accumulated interest of previous period. The main use of Net

Present Value can be seen in analyzing the profitability of a particular project. Internal Rate

of Return is used for the estimation of the profitability aspect of a potential investment (Rossi

2015).

QUESTION 7

Banks provides their customers with different kinds of products, Six of them are

Savings Account that is used to save money; Current Account that is used by businesses;

Debit Cards that are used for money withdrawal; Credit Cards that is used for various

shopping and other payments; Loans and Mortgages (Chochoľákováet al. 2015).

QUESTION 8

Banks are governed by government regulations along with certain requirements like

Basel I, Basel II and Basel III. The banks are needed to consider the monetary policy of the

countries along with the basic banking standards. However, the insurance companies are

regulated by statutory law, administrative regulations and jurisprudence as these regulate the

insurance industry (Baltenspergeret al. 2014).

QUESTION 5

Some of the major reasons for property revaluation are to gain understanding about

the difference between value and price; to gain effective guideline for the investment

decisions; to get the correct market value of the property at the time of selling or buying; to

obtain the legal documents about the property; to know the extent of tax deduction and others

(Beaglehole 2015).

QUESTION 6

The main use of Compound Interest can be seen for the calculation of interest on the

initial principles along with the accumulated interest of previous period. The main use of Net

Present Value can be seen in analyzing the profitability of a particular project. Internal Rate

of Return is used for the estimation of the profitability aspect of a potential investment (Rossi

2015).

QUESTION 7

Banks provides their customers with different kinds of products, Six of them are

Savings Account that is used to save money; Current Account that is used by businesses;

Debit Cards that are used for money withdrawal; Credit Cards that is used for various

shopping and other payments; Loans and Mortgages (Chochoľákováet al. 2015).

QUESTION 8

Banks are governed by government regulations along with certain requirements like

Basel I, Basel II and Basel III. The banks are needed to consider the monetary policy of the

countries along with the basic banking standards. However, the insurance companies are

regulated by statutory law, administrative regulations and jurisprudence as these regulate the

insurance industry (Baltenspergeret al. 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMIC PRINCIPLES OF FINANCE INDUSTRY

QUESTION 9

In case of studying property markets various statistical data are used. Using the

various statistical techniques property markets can be learnt. Property markets are also known

as the real estate. One statistical technique used in the property market is regression, for

example stepwise regression model and correlation can also be used.

4.3 Activity

QUESTION 1

a) Banking industry- the knowledge of the principles of economics are applied to

the different financial industries. There are many functions of money in the

economy

b) Insurance industry- this industry acts as a mediator between policy maker and

capital market. Application of capital asset pricing model is used.

QUESTION 2

Decision making is one of the key factors of managerial economics. The different

economic aspects also help the managers in taking different economic decisions. It is also a

process in which the business makes decision.

QUESTION 3

a) In the finance industry, one major way to evaluate the wok performance is the analysis of

the performance metrics. Some of the crucial performance metrics are revenue per employee,

attendance, turnover, efficiency and others.

QUESTION 9

In case of studying property markets various statistical data are used. Using the

various statistical techniques property markets can be learnt. Property markets are also known

as the real estate. One statistical technique used in the property market is regression, for

example stepwise regression model and correlation can also be used.

4.3 Activity

QUESTION 1

a) Banking industry- the knowledge of the principles of economics are applied to

the different financial industries. There are many functions of money in the

economy

b) Insurance industry- this industry acts as a mediator between policy maker and

capital market. Application of capital asset pricing model is used.

QUESTION 2

Decision making is one of the key factors of managerial economics. The different

economic aspects also help the managers in taking different economic decisions. It is also a

process in which the business makes decision.

QUESTION 3

a) In the finance industry, one major way to evaluate the wok performance is the analysis of

the performance metrics. Some of the crucial performance metrics are revenue per employee,

attendance, turnover, efficiency and others.

ECONOMIC PRINCIPLES OF FINANCE INDUSTRY

(b) The required feedback of the performance can be gained through different appraisal

programs, employee survey and personal view point of other employees.

QUESTION 4

Different types of taxation, interest rates, money supply and the budget of the

government are the different forms of government policies (Guttmann and Rodgers 2015).

Monetary policies and the fiscal policies are the two types of economic policy. This kind of

policy usually influences the behaviour of the economy. Economic principles on the other

hand helps in solving the problems related to business.

QUESTION 5

Positive economics is that branch of economics which is concerned with the

representation of the economic phenomena. Unlike normative economics it is concerned with

the development of statements that are positive.it also includes th4e testing of the theories of

economics. Positive economics also answers “what is” when a certain coursed of action is to

be taken.

QUESTON 6

a) Principles of microeconomics – this usually refers to the fundamentals of

microeconomics. This branch of economics shows how an individual maximizes its

utility.

b) Principles of macroeconomics- the study of the economic issues which affects the

entire nation or economy such as inflation, unemployment rate and interest rates is

defined as macroeconomics.

(b) The required feedback of the performance can be gained through different appraisal

programs, employee survey and personal view point of other employees.

QUESTION 4

Different types of taxation, interest rates, money supply and the budget of the

government are the different forms of government policies (Guttmann and Rodgers 2015).

Monetary policies and the fiscal policies are the two types of economic policy. This kind of

policy usually influences the behaviour of the economy. Economic principles on the other

hand helps in solving the problems related to business.

QUESTION 5

Positive economics is that branch of economics which is concerned with the

representation of the economic phenomena. Unlike normative economics it is concerned with

the development of statements that are positive.it also includes th4e testing of the theories of

economics. Positive economics also answers “what is” when a certain coursed of action is to

be taken.

QUESTON 6

a) Principles of microeconomics – this usually refers to the fundamentals of

microeconomics. This branch of economics shows how an individual maximizes its

utility.

b) Principles of macroeconomics- the study of the economic issues which affects the

entire nation or economy such as inflation, unemployment rate and interest rates is

defined as macroeconomics.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMIC PRINCIPLES OF FINANCE INDUSTRY

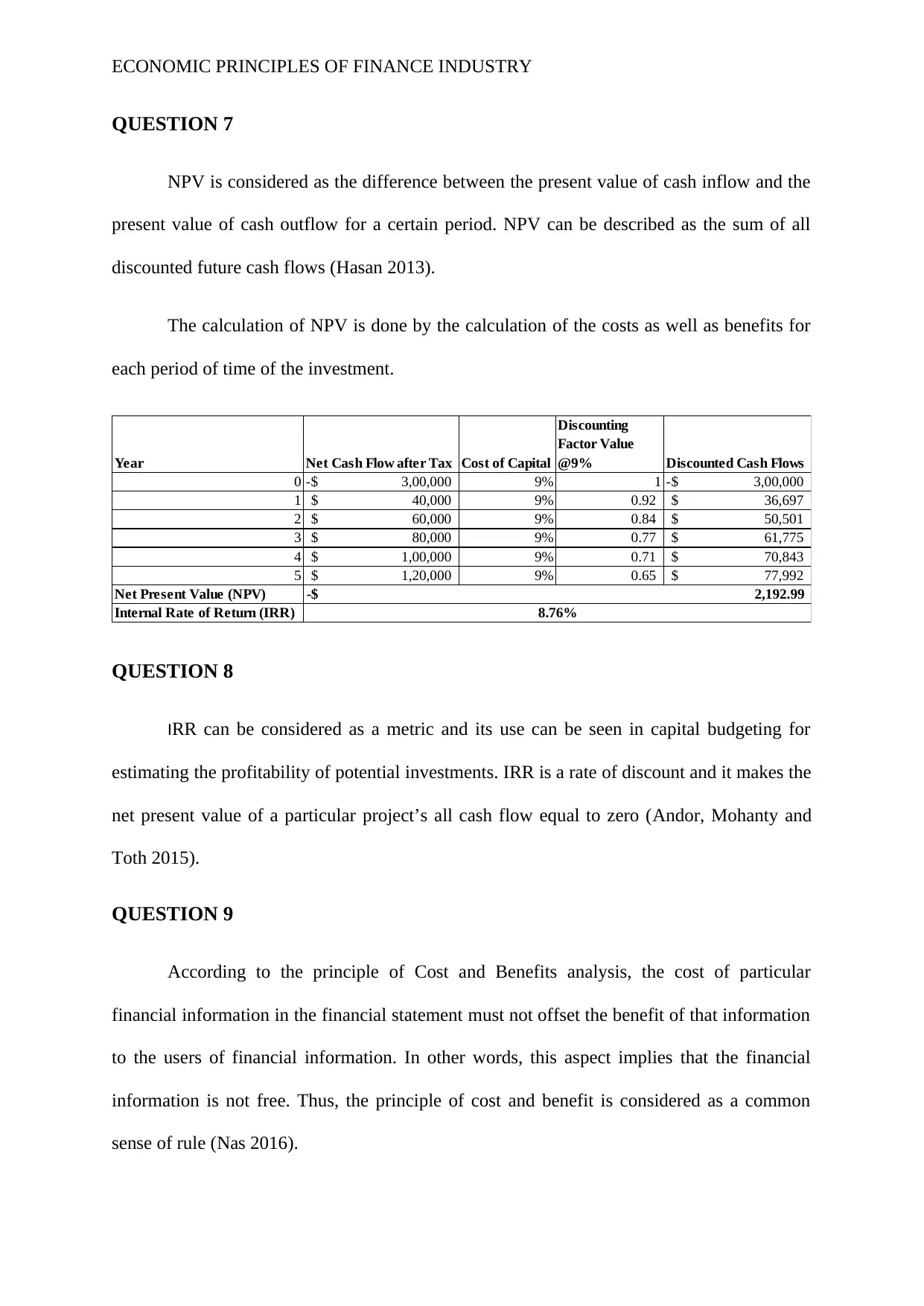

QUESTION 7

NPV is considered as the difference between the present value of cash inflow and the

present value of cash outflow for a certain period. NPV can be described as the sum of all

discounted future cash flows (Hasan 2013).

The calculation of NPV is done by the calculation of the costs as well as benefits for

each period of time of the investment.

Year Net Cash Flow after Tax Cost of Capital

Discounting

Factor Value

@9% Discounted Cash Flows

0 3,00,000-$ 9% 1 3,00,000-$

1 40,000$ 9% 0.92 36,697$

2 60,000$ 9% 0.84 50,501$

3 80,000$ 9% 0.77 61,775$

4 1,00,000$ 9% 0.71 70,843$

5 1,20,000$ 9% 0.65 77,992$

Net Present Value (NPV)

Internal Rate of Return (IRR)

2,192.99-$

8.76%

QUESTION 8

IRR can be considered as a metric and its use can be seen in capital budgeting for

estimating the profitability of potential investments. IRR is a rate of discount and it makes the

net present value of a particular project’s all cash flow equal to zero (Andor, Mohanty and

Toth 2015).

QUESTION 9

According to the principle of Cost and Benefits analysis, the cost of particular

financial information in the financial statement must not offset the benefit of that information

to the users of financial information. In other words, this aspect implies that the financial

information is not free. Thus, the principle of cost and benefit is considered as a common

sense of rule (Nas 2016).

QUESTION 7

NPV is considered as the difference between the present value of cash inflow and the

present value of cash outflow for a certain period. NPV can be described as the sum of all

discounted future cash flows (Hasan 2013).

The calculation of NPV is done by the calculation of the costs as well as benefits for

each period of time of the investment.

Year Net Cash Flow after Tax Cost of Capital

Discounting

Factor Value

@9% Discounted Cash Flows

0 3,00,000-$ 9% 1 3,00,000-$

1 40,000$ 9% 0.92 36,697$

2 60,000$ 9% 0.84 50,501$

3 80,000$ 9% 0.77 61,775$

4 1,00,000$ 9% 0.71 70,843$

5 1,20,000$ 9% 0.65 77,992$

Net Present Value (NPV)

Internal Rate of Return (IRR)

2,192.99-$

8.76%

QUESTION 8

IRR can be considered as a metric and its use can be seen in capital budgeting for

estimating the profitability of potential investments. IRR is a rate of discount and it makes the

net present value of a particular project’s all cash flow equal to zero (Andor, Mohanty and

Toth 2015).

QUESTION 9

According to the principle of Cost and Benefits analysis, the cost of particular

financial information in the financial statement must not offset the benefit of that information

to the users of financial information. In other words, this aspect implies that the financial

information is not free. Thus, the principle of cost and benefit is considered as a common

sense of rule (Nas 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMIC PRINCIPLES OF FINANCE INDUSTRY

QUESTION 10

The circular flow of income states the ways by which money flows to the economy. It

is defined by the flow of money, goods and services which runs in the opposite direction in a

closed circuit. The flow of money is between the consumers and the producers or between the

firms and the households.

QUESTION 11

Modern Capitalism is considered as an economic system that is based on the private

ownership of the production, distribution and exchange means. On the other hand, it can be

said that modern capitalism can be regarded as privately owned production mean economic

system where the products are produced for the purpose of maximizing the profit (Sombart

2017).

QUESTION 12

a) Intrinsic theory of value – it is also known as fundamental value which relates to the

value of goods, company, stock or services.

b) Labour theory of value – according to this theory the economic value of a commodity

depends upon the amount of labour required to produce it.

QUESTION 10

The circular flow of income states the ways by which money flows to the economy. It

is defined by the flow of money, goods and services which runs in the opposite direction in a

closed circuit. The flow of money is between the consumers and the producers or between the

firms and the households.

QUESTION 11

Modern Capitalism is considered as an economic system that is based on the private

ownership of the production, distribution and exchange means. On the other hand, it can be

said that modern capitalism can be regarded as privately owned production mean economic

system where the products are produced for the purpose of maximizing the profit (Sombart

2017).

QUESTION 12

a) Intrinsic theory of value – it is also known as fundamental value which relates to the

value of goods, company, stock or services.

b) Labour theory of value – according to this theory the economic value of a commodity

depends upon the amount of labour required to produce it.

ECONOMIC PRINCIPLES OF FINANCE INDUSTRY

REFERENCE LIST

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of

Central and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Andrievskaya, I. and Semenova, M., 2016. Does banking system transparency enhance bank

competition? Cross-country evidence. Journal of Financial Stability, 23, pp.33-50.

Baltensperger, E., Buomberger, P., Iuppa, A.A., Keller, B. and Wicki, A., 2014. Regulation

and intervention in the insurance industry-fundamental issues. The Geneva Reports, 1(1),

pp.1-63.

Beaglehole, E., 2015. Property: A study in social psychology. Psychology Press.

Chochoľáková, A., Gabčová, L., Belás, J. and Sipko, J., 2015. Bank customers’ satisfaction,

customers’ loyalty and additional purchases of banking products and services. A case study

from the Czech Republic. Economics and Sociology.

Fatima, N., 2014. Capital Adequacy: A Financial Soundness Indicator for Banks. Global

Journal of Finance and Management, 6(8), pp.771-776.

Guttmann, R. and Rodgers, D., 2015. International banking and liquidity risk transmission:

Evidence from Australia. IMF Economic Review, 63(3), pp.411-425.

Hasan, M., 2013. Capital budgeting techniques used by small manufacturing

companies. Journal of Service Science and Management, 6(01), p.38.

REFERENCE LIST

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of

Central and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Andrievskaya, I. and Semenova, M., 2016. Does banking system transparency enhance bank

competition? Cross-country evidence. Journal of Financial Stability, 23, pp.33-50.

Baltensperger, E., Buomberger, P., Iuppa, A.A., Keller, B. and Wicki, A., 2014. Regulation

and intervention in the insurance industry-fundamental issues. The Geneva Reports, 1(1),

pp.1-63.

Beaglehole, E., 2015. Property: A study in social psychology. Psychology Press.

Chochoľáková, A., Gabčová, L., Belás, J. and Sipko, J., 2015. Bank customers’ satisfaction,

customers’ loyalty and additional purchases of banking products and services. A case study

from the Czech Republic. Economics and Sociology.

Fatima, N., 2014. Capital Adequacy: A Financial Soundness Indicator for Banks. Global

Journal of Finance and Management, 6(8), pp.771-776.

Guttmann, R. and Rodgers, D., 2015. International banking and liquidity risk transmission:

Evidence from Australia. IMF Economic Review, 63(3), pp.411-425.

Hasan, M., 2013. Capital budgeting techniques used by small manufacturing

companies. Journal of Service Science and Management, 6(01), p.38.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.