MBA402 Case Study: Governance, Sustainability at Focus Logistics

VerifiedAdded on 2023/06/09

|12

|3020

|133

Case Study

AI Summary

This case study examines the corporate governance, sustainability reporting, and risk management practices of Focus Logistics Pty Ltd. It highlights the importance of establishing a robust corporate governance structure, including building trust with customers, creating value through logistics, managing related party transactions, and working responsibly within the environment and society. The study critiques the views of the company's COO regarding corporate governance and emphasizes the need for sustainability reporting to address environmental, social, and governance goals. It identifies key risks faced by Focus Logistics, such as improper operations, biased management, irregular reporting, and lack of control over sustainability issues, and suggests mitigation strategies. The analysis underscores the significance of transparency, accountability, and stakeholder engagement for the long-term success and reputation of the company, especially as it considers listing on the ASX. Desklib provides access to this and other solved assignments for students.

MBA402 Assessment 3 Case

Study

Study

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Corporate Governance:................................................................................................................3

Sustainability Reporting:.............................................................................................................5

Risk Management & Key Risks:.................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................1

APPENDIX......................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Corporate Governance:................................................................................................................3

Sustainability Reporting:.............................................................................................................5

Risk Management & Key Risks:.................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................1

APPENDIX......................................................................................................................................2

INTRODUCTION

Corporate governance is the governance or control and direction of the corporate which is

exercised by the board of directors over the company. Such board of directors are elected by the

shareholders along with the appointment of the auditors of the company thus ensuring that an

appropriate structure of the corporate governance is put in place to be able to address the issues

of the shareholders leading to an optimum corporate governance. Now, along with corporate

governance, risk management and sustainability report is also essential for an efficient working

of the company which will involve identifying the risks, how will the company get affected by

the risk, looking for solutions and measures to address the risk, implementing the solutions and

monitor their success.

MAIN BODY

Corporate Governance:

For a logistics company like Focus Logistics Pty Ltd setting up of corporate governance is

very essential unlike the views of the company’s COO, Jacob Gardner who thinks that

implementation of corporate governance will slow down the processes and make them more

complicated (Adnan, Hay and van Staden, 2018). Now, to support such an argument following

are some of the good practices of corporate governance which the company shall follow to be

able to be answerable to the management and stakeholders at large-

a) Relationship of trust with customers – For any business whether small or big, listed or

unlisted, relationships with their customers is the most important aspect of the operations

of the business. This involves building of sense of trust among the customers by

providing variety of goods and services to the customers as per their requirements so that

the customers are satisfied and both the customers and business work as the best partners

of each other.

Jacob Gardner of Focus Logistics Pty Ltd is of the view that as they do not fall in

the tax complications therefore, their main objective is maximization of the shareholders’

returns and thus there is no need to adhere to compliance issues and the company can pay

small fines and penalties if legally required rather than following such tedious methods to

follow the compliances.

Such a view is irrational and not following the good corporate governance

practices and thus will lead to degradation of the company’s image in the market as the

Corporate governance is the governance or control and direction of the corporate which is

exercised by the board of directors over the company. Such board of directors are elected by the

shareholders along with the appointment of the auditors of the company thus ensuring that an

appropriate structure of the corporate governance is put in place to be able to address the issues

of the shareholders leading to an optimum corporate governance. Now, along with corporate

governance, risk management and sustainability report is also essential for an efficient working

of the company which will involve identifying the risks, how will the company get affected by

the risk, looking for solutions and measures to address the risk, implementing the solutions and

monitor their success.

MAIN BODY

Corporate Governance:

For a logistics company like Focus Logistics Pty Ltd setting up of corporate governance is

very essential unlike the views of the company’s COO, Jacob Gardner who thinks that

implementation of corporate governance will slow down the processes and make them more

complicated (Adnan, Hay and van Staden, 2018). Now, to support such an argument following

are some of the good practices of corporate governance which the company shall follow to be

able to be answerable to the management and stakeholders at large-

a) Relationship of trust with customers – For any business whether small or big, listed or

unlisted, relationships with their customers is the most important aspect of the operations

of the business. This involves building of sense of trust among the customers by

providing variety of goods and services to the customers as per their requirements so that

the customers are satisfied and both the customers and business work as the best partners

of each other.

Jacob Gardner of Focus Logistics Pty Ltd is of the view that as they do not fall in

the tax complications therefore, their main objective is maximization of the shareholders’

returns and thus there is no need to adhere to compliance issues and the company can pay

small fines and penalties if legally required rather than following such tedious methods to

follow the compliances.

Such a view is irrational and not following the good corporate governance

practices and thus will lead to degradation of the company’s image in the market as the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company is now growing and has the objective of getting listed on the ASX because after

listing the company will be more accountable and responsible to the public at large and

shall keep the betterment of stakeholders on priority.

b) Value creation by logistics – Every business needs to create value for its customers in

the field in which it is operating. Thereby achieving its objective of building good

relationship with the customers and developing a sense of trust and partnership with each

other. Naturally, value creation comes from experience and knowledge gained first hand

by working in the industry. Such knowledge and experience will lead to gaining expertise

over time and achieve the targets of market share and market stability in the long run.

For the Focus Logistics Pty Ltd, it can be seen that, it was established in 1965 by

Mrs. White and had a slogan of ‘go local’ which attracted the customers and community

at large and supported the company to grow and develop in the community (Kovermann

and Velte, 2019). It is said that for the next 30 years, company showed a steady growth

and also expanded its operations in multiple locations.

After Alice took over, the company grew by leaps and bounds i.e., accounting for

19% of market share in total resultantly, being the Australia’s fifth, largest company in

logistics. Also, customer base increased from 28 to 650 in the year 1997 as compared to

the year 1970 and currently operating at the customer base level of 11,500 customers

along with some listed companies as well. Also, effective financial disclosures are

necessary as the potential investors are of the view that the Focus Logistics cannot avail

further funding as it does not possess proper structure of governance and operations to

support such funding and expansions.

c) Related party transactions – All the related party transactions are to be disclosed and

approved by the board of directors of the company and shall be kept at minimum to be

transparent in its transactions and operations. In the case of Focus Logistics Pty Ltd, it

can be observed that the business is still run like a family business with most of the

management positions being occupied by the family and close friends. Such an issue is a

concern for the investors as they are of the view that there is limited control on the

operations and the reporting along with biased management reviews of the performances

and also the board committees are lacking. Such biasedness can be seen in the decision of

listing the company will be more accountable and responsible to the public at large and

shall keep the betterment of stakeholders on priority.

b) Value creation by logistics – Every business needs to create value for its customers in

the field in which it is operating. Thereby achieving its objective of building good

relationship with the customers and developing a sense of trust and partnership with each

other. Naturally, value creation comes from experience and knowledge gained first hand

by working in the industry. Such knowledge and experience will lead to gaining expertise

over time and achieve the targets of market share and market stability in the long run.

For the Focus Logistics Pty Ltd, it can be seen that, it was established in 1965 by

Mrs. White and had a slogan of ‘go local’ which attracted the customers and community

at large and supported the company to grow and develop in the community (Kovermann

and Velte, 2019). It is said that for the next 30 years, company showed a steady growth

and also expanded its operations in multiple locations.

After Alice took over, the company grew by leaps and bounds i.e., accounting for

19% of market share in total resultantly, being the Australia’s fifth, largest company in

logistics. Also, customer base increased from 28 to 650 in the year 1997 as compared to

the year 1970 and currently operating at the customer base level of 11,500 customers

along with some listed companies as well. Also, effective financial disclosures are

necessary as the potential investors are of the view that the Focus Logistics cannot avail

further funding as it does not possess proper structure of governance and operations to

support such funding and expansions.

c) Related party transactions – All the related party transactions are to be disclosed and

approved by the board of directors of the company and shall be kept at minimum to be

transparent in its transactions and operations. In the case of Focus Logistics Pty Ltd, it

can be observed that the business is still run like a family business with most of the

management positions being occupied by the family and close friends. Such an issue is a

concern for the investors as they are of the view that there is limited control on the

operations and the reporting along with biased management reviews of the performances

and also the board committees are lacking. Such biasedness can be seen in the decision of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the board of not preparing sustainability report declaring it to be non-value adding

reporting.

Acknowledging the importance of regular reporting and reviews, board says that

trust and patience are most vital in a family business. All the views of the board are

leading to degradation of the public image of the company and thus shall be addressed for

the long run image of the company.

d) Working within the environment and with the society – Since every company

functions and operates in the environment and with the society affecting the operations of

such entity therefore, it is obligated towards the conservation of such environment and

society. In case of logistics company, the major issue is of vehicles which run to

accommodate the business of logistics (Zaman and et.al., 2022). Such vehicles shall be

able to achieve the objective of green logistics of the company and for such green

logistics initiative, environment friendly measures shall be devised and implemented.

Concerns of the investors are also regarding the reporting of sustainability by the

Focus Logistics Pty Ltd. Investors observed that carbon footprint is huge and specially

the B-Double truck shows consumption of almost 2 million litres of diesel annually and

additional consumption of fuel by the sub-contractors is still unknown (Holmatov,

Hoekstra and Krol, 2019). Mrs. White dismisses such a concern but David Rose is

genuinely concerned about the effects of such an issue on the future of the company. He

argues that the company shall be pioneers in the corporate governance and sustainability

methods looking at the current standing of the company in the market.

Sustainability Reporting:

Sustainability reporting as the name suggests includes reporting by any entity on its

sustainability issues namely – environmental, governance, social and economic goals. Such

issues are needed to be handled with utmost care and are non-financial aspects of the

organization on which reporting is to be done (Aifuwa, 2020). Through such a reporting the

company explain its goals and objectives regarding the non-financials and responsibility of the

company towards its stakeholders and towards the environment in which it is operating

(Gnanaweera and Kunori, 2018). There is no legal obligation of the company to report

sustainability but it shall be done to emphasize on both financial as well as non-financial

information.

reporting.

Acknowledging the importance of regular reporting and reviews, board says that

trust and patience are most vital in a family business. All the views of the board are

leading to degradation of the public image of the company and thus shall be addressed for

the long run image of the company.

d) Working within the environment and with the society – Since every company

functions and operates in the environment and with the society affecting the operations of

such entity therefore, it is obligated towards the conservation of such environment and

society. In case of logistics company, the major issue is of vehicles which run to

accommodate the business of logistics (Zaman and et.al., 2022). Such vehicles shall be

able to achieve the objective of green logistics of the company and for such green

logistics initiative, environment friendly measures shall be devised and implemented.

Concerns of the investors are also regarding the reporting of sustainability by the

Focus Logistics Pty Ltd. Investors observed that carbon footprint is huge and specially

the B-Double truck shows consumption of almost 2 million litres of diesel annually and

additional consumption of fuel by the sub-contractors is still unknown (Holmatov,

Hoekstra and Krol, 2019). Mrs. White dismisses such a concern but David Rose is

genuinely concerned about the effects of such an issue on the future of the company. He

argues that the company shall be pioneers in the corporate governance and sustainability

methods looking at the current standing of the company in the market.

Sustainability Reporting:

Sustainability reporting as the name suggests includes reporting by any entity on its

sustainability issues namely – environmental, governance, social and economic goals. Such

issues are needed to be handled with utmost care and are non-financial aspects of the

organization on which reporting is to be done (Aifuwa, 2020). Through such a reporting the

company explain its goals and objectives regarding the non-financials and responsibility of the

company towards its stakeholders and towards the environment in which it is operating

(Gnanaweera and Kunori, 2018). There is no legal obligation of the company to report

sustainability but it shall be done to emphasize on both financial as well as non-financial

information.

Such a reporting is obviously beneficial for the company as it will help outline the areas on

which the company needs to focus on, such reporting is also a kind of compliance of various

regulations devised by the government applicable on the company, reporting of non-financial

activities of the company and that too those which are undertaken specially for the betterment of

the environment and the society draws more customers towards the company, attract employees

and with genuine talent as the employees will be more interested in the company sensitive

towards the climatic changes, rights of human in general, and social equity, investors are

obviously more interested in the company which is fulfilling its societal obligations along with

other obligations because in this way, it will have a more positive image in the market in the long

run and true and fair sustainability reporting by the company in the long run will provide the

operations of the company with transparency, accountability and credibility as the company will

be held responsible for the sustainability activities it undertakes and the effect of such activities

on the goodwill of the company (8 Benefits of sustainability reporting. 2022.).

Key elements that should be included in the sustainability report of the logistic companies are

enlisted as such:

Stakeholders’ Insights – A sound sustainability report is the one which will include the

disclosures relevant to the requirements of the stakeholders and assist them in the

decision making regarding the company (Boiral and Heras-Saizarbitoria, 2020). Focus

Logistics shall also prepare such sustainability report to assist the stakeholders like

potential investors to make decisions regarding investment in the company.

Visual Presentation – The sustainability report is already based on the non-financial

information of the company and therefore, pure text in the whole report will make the

report tiresome to read and no one will be actually interested in the report therefore, use

of graphs, charts, diagrams, etc. shall be done to make it more attractive.

Benchmarking and relevant Progress – Naturally, any report shall include certain

standards and benchmarks decided by the management and the relevant progress with

respect to such benchmarks if any or failure to meet the benchmarks and degree of failure

to be specifically disclosed (Opferkuch and et.al., 2021). For Focus Logistics, carbon

footprints shall be aimed to be reduced and targeted to be kept at the standard allowed as

per the industry of logistics.

which the company needs to focus on, such reporting is also a kind of compliance of various

regulations devised by the government applicable on the company, reporting of non-financial

activities of the company and that too those which are undertaken specially for the betterment of

the environment and the society draws more customers towards the company, attract employees

and with genuine talent as the employees will be more interested in the company sensitive

towards the climatic changes, rights of human in general, and social equity, investors are

obviously more interested in the company which is fulfilling its societal obligations along with

other obligations because in this way, it will have a more positive image in the market in the long

run and true and fair sustainability reporting by the company in the long run will provide the

operations of the company with transparency, accountability and credibility as the company will

be held responsible for the sustainability activities it undertakes and the effect of such activities

on the goodwill of the company (8 Benefits of sustainability reporting. 2022.).

Key elements that should be included in the sustainability report of the logistic companies are

enlisted as such:

Stakeholders’ Insights – A sound sustainability report is the one which will include the

disclosures relevant to the requirements of the stakeholders and assist them in the

decision making regarding the company (Boiral and Heras-Saizarbitoria, 2020). Focus

Logistics shall also prepare such sustainability report to assist the stakeholders like

potential investors to make decisions regarding investment in the company.

Visual Presentation – The sustainability report is already based on the non-financial

information of the company and therefore, pure text in the whole report will make the

report tiresome to read and no one will be actually interested in the report therefore, use

of graphs, charts, diagrams, etc. shall be done to make it more attractive.

Benchmarking and relevant Progress – Naturally, any report shall include certain

standards and benchmarks decided by the management and the relevant progress with

respect to such benchmarks if any or failure to meet the benchmarks and degree of failure

to be specifically disclosed (Opferkuch and et.al., 2021). For Focus Logistics, carbon

footprints shall be aimed to be reduced and targeted to be kept at the standard allowed as

per the industry of logistics.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Established Frameworks – There are various frameworks established within the country

and even globally regarding sustainability reporting and compliances. And compliance of

such frameworks is an evidence that such reporting is being done as per the applicable

rules and regulations and thus can be trusted and followed. Some of the frameworks may

be Global Reporting Index (GRI), Sustainability Accounting Standards Board (SASB),

etc.

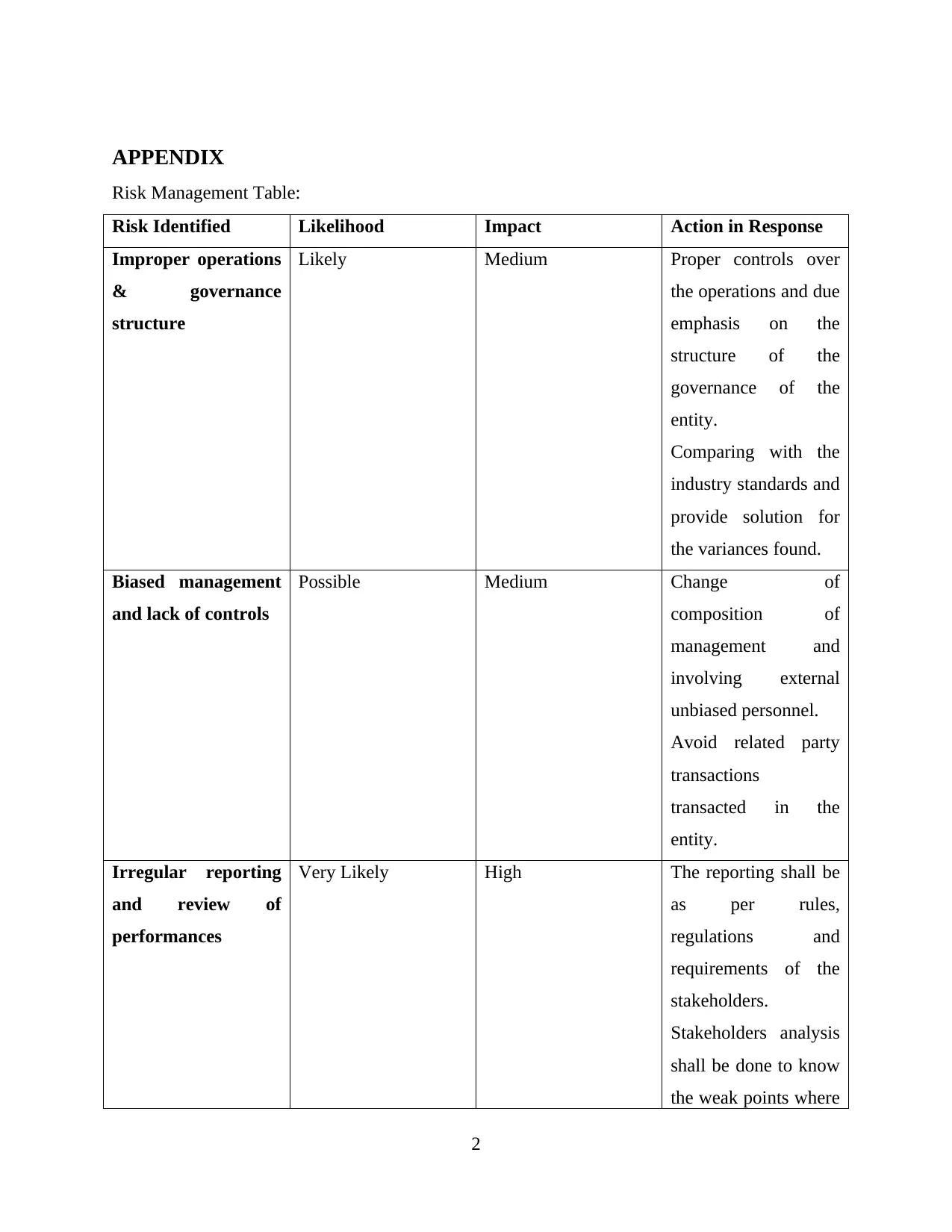

Risk Management & Key Risks:

Risks are a part of any business and such risks are to be duly addressed and solved for to

manage the risks so that the risks are not hindering the operations of the entity (Amarasena, Haag

and Peres, 2019). There are numerous risks in each and every business organisation but

likelihood or probability of happening of such risks depends upon the nature of such risks i.e.,

some risks are less likely to occur while some risks are most likely prevalent in the system of the

organisation and thus will need action plans to combat their effect (Willumsen and et.al., 2019).

Such risks of the Focus Logistics Pty Ltd are as follows:

Improper operations and governance structure – the likelihood of such a risk is likely

i.e., the entity needs to develop action in response to such a risk to seriously mitigate and

this can be done by comparing with the industry standards and providing for the further

improvement wherever needed.

Biased management and lack of controls – it is a possible risk in the entity and thus can

be mitigated by improving the composition of the management and appointment of

unbiased and unrelated personnel in the management.

Irregular reporting and review of performance – the risk of such irregular reporting

and untimely performance review is very likely and shall be managed by following

relevant rules, regulations and policies for such reporting and adhering to requirements of

stakeholders along with stakeholders’ analysis.

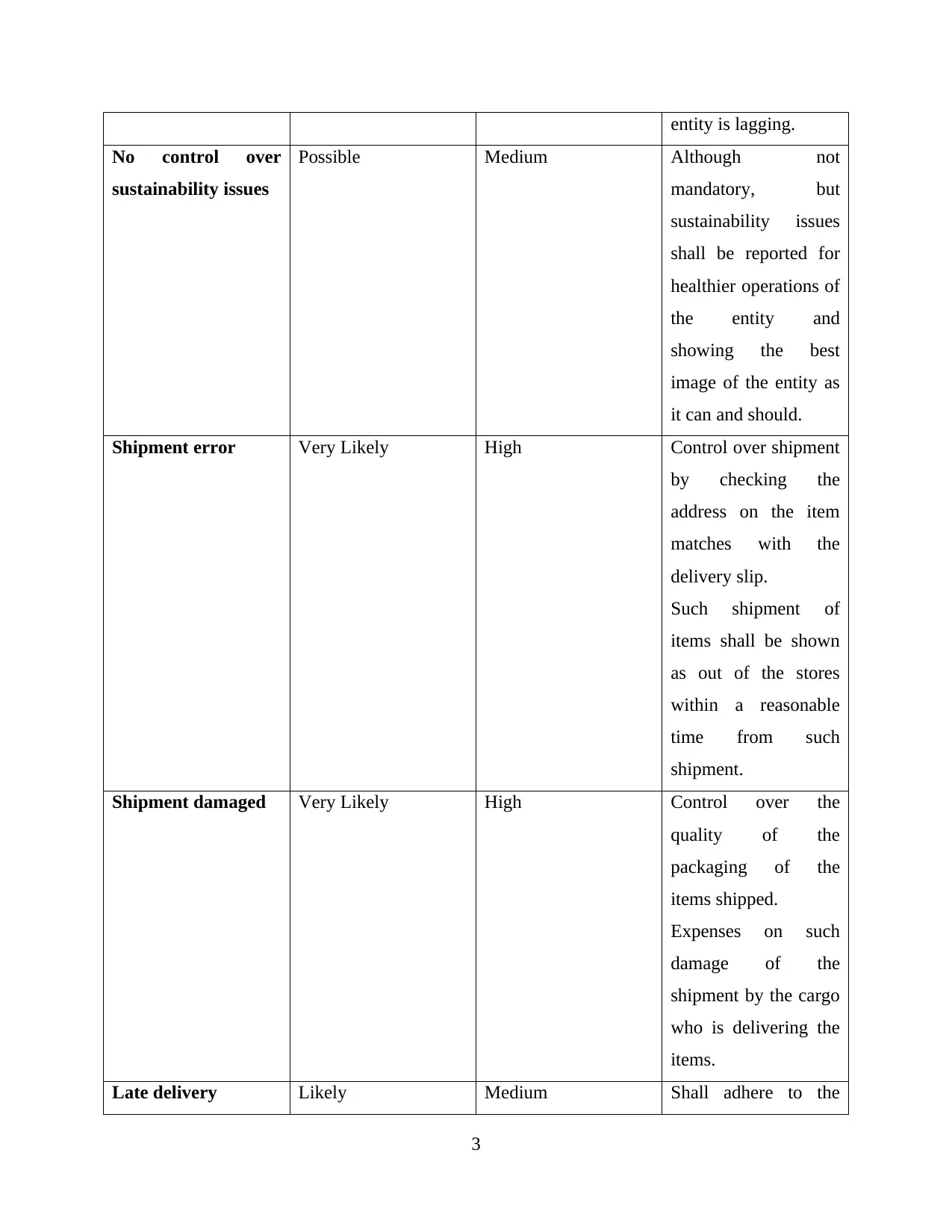

No control over sustainability issues – this risk of not addressing the sustainability

issues has the probability of possible in the entity and such non-control shall be addressed

to avoid long term degradation of the goodwill of the company by reporting such issues

in the sustainability report.

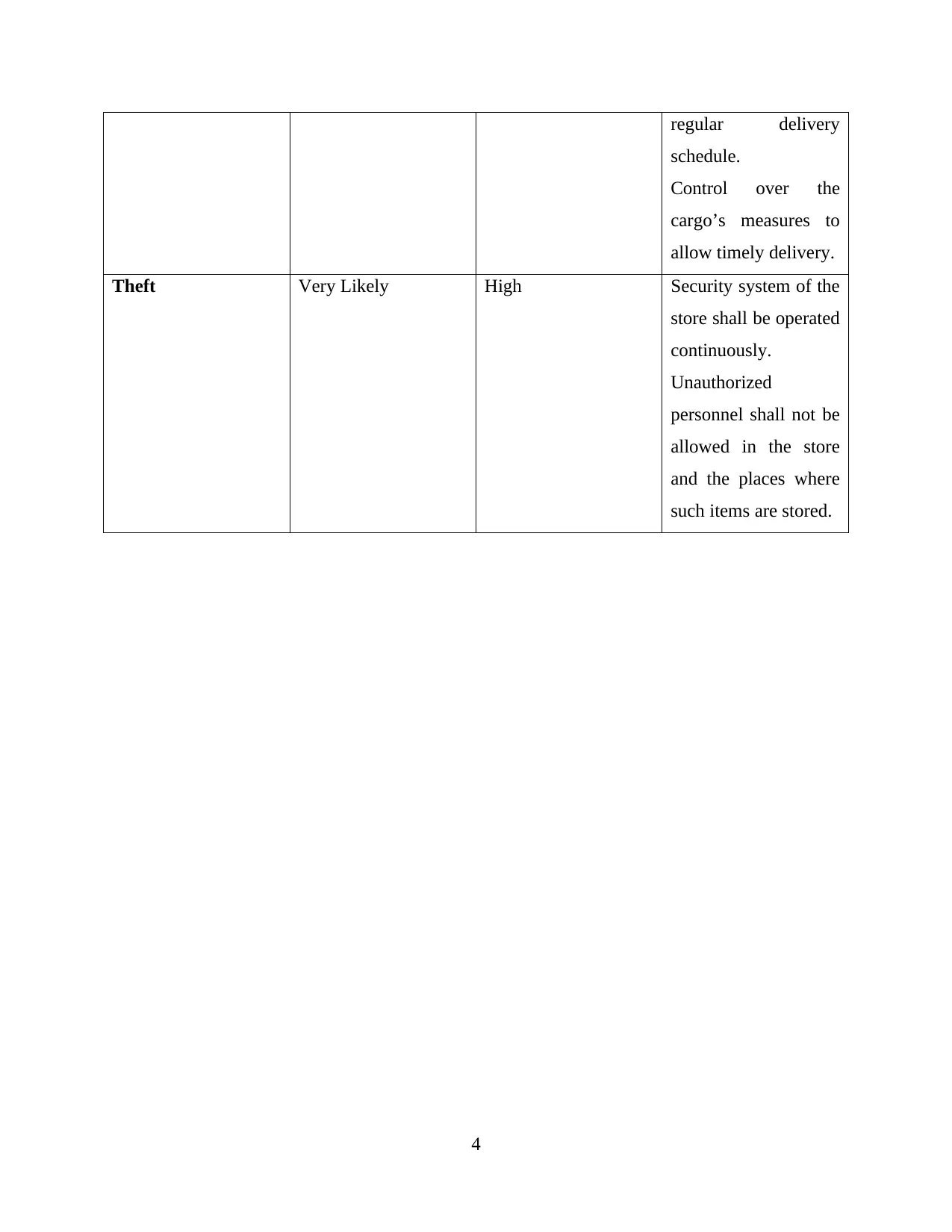

Other issues involve errors in shipment, shipment of the items damaged, late delivery of

the items and theft of such items in transit or from the store (What Is a Risk Matrix?

and even globally regarding sustainability reporting and compliances. And compliance of

such frameworks is an evidence that such reporting is being done as per the applicable

rules and regulations and thus can be trusted and followed. Some of the frameworks may

be Global Reporting Index (GRI), Sustainability Accounting Standards Board (SASB),

etc.

Risk Management & Key Risks:

Risks are a part of any business and such risks are to be duly addressed and solved for to

manage the risks so that the risks are not hindering the operations of the entity (Amarasena, Haag

and Peres, 2019). There are numerous risks in each and every business organisation but

likelihood or probability of happening of such risks depends upon the nature of such risks i.e.,

some risks are less likely to occur while some risks are most likely prevalent in the system of the

organisation and thus will need action plans to combat their effect (Willumsen and et.al., 2019).

Such risks of the Focus Logistics Pty Ltd are as follows:

Improper operations and governance structure – the likelihood of such a risk is likely

i.e., the entity needs to develop action in response to such a risk to seriously mitigate and

this can be done by comparing with the industry standards and providing for the further

improvement wherever needed.

Biased management and lack of controls – it is a possible risk in the entity and thus can

be mitigated by improving the composition of the management and appointment of

unbiased and unrelated personnel in the management.

Irregular reporting and review of performance – the risk of such irregular reporting

and untimely performance review is very likely and shall be managed by following

relevant rules, regulations and policies for such reporting and adhering to requirements of

stakeholders along with stakeholders’ analysis.

No control over sustainability issues – this risk of not addressing the sustainability

issues has the probability of possible in the entity and such non-control shall be addressed

to avoid long term degradation of the goodwill of the company by reporting such issues

in the sustainability report.

Other issues involve errors in shipment, shipment of the items damaged, late delivery of

the items and theft of such items in transit or from the store (What Is a Risk Matrix?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2022.). Such issues can be addressed matching the destinations’ address from the log

book from the delivery slip, improving the quality of the items delivered and borne of

expenses on such damaged items, etc.

CONCLUSION

Concluding, the above report shows the importance of corporate governance, sustainability

report and risk management in the business entity. In the above report, first of all, good corporate

governance practices with respect to operations of Focus Logistic Pty Ltd are being discussed

and explained how these practices will be beneficial for the Focus Logistic Pty Ltd as it is on the

verge of listing on ASX. Next, it addresses the importance of sustainability report for logistic

companies like Focus Logistics and also explains the key elements that shall be the part of the

report and lastly, risk management is analysed along with a risk management table attached as an

appendix.

book from the delivery slip, improving the quality of the items delivered and borne of

expenses on such damaged items, etc.

CONCLUSION

Concluding, the above report shows the importance of corporate governance, sustainability

report and risk management in the business entity. In the above report, first of all, good corporate

governance practices with respect to operations of Focus Logistic Pty Ltd are being discussed

and explained how these practices will be beneficial for the Focus Logistic Pty Ltd as it is on the

verge of listing on ASX. Next, it addresses the importance of sustainability report for logistic

companies like Focus Logistics and also explains the key elements that shall be the part of the

report and lastly, risk management is analysed along with a risk management table attached as an

appendix.

REFERENCES

Books and Journals

Adnan, S. M., Hay, D. and van Staden, C. J., 2018. The influence of culture and corporate

governance on corporate social responsibility disclosure: A cross country analysis. Journal of

Cleaner Production. 198. pp.820-832.

Aifuwa, H. O., 2020. Sustainability reporting and firm performance in developing climes: A

review of literature. Copernican Journal of Finance & Accounting. 9(1). pp.9-29.

Amarasena, N., Haag, D. and Peres, K. G., 2019. A scoping review of caries risk management

protocols in Australia and New Zealand. Australian Dental Journal. 64(1). pp.19-26.

Boiral, O. and Heras-Saizarbitoria, I., 2020. Sustainability reporting assurance: Creating

stakeholder accountability through hyperreality? Journal of Cleaner Production. 243.

p.118596.

Gnanaweera, K. A. K. and Kunori, N., 2018. Corporate sustainability reporting: Linkage of

corporate disclosure information and performance indicators. Cogent Business &

Management. 5(1). p.1423872.

Holmatov, B., Hoekstra, A. Y. and Krol, M. S., 2019. Land, water and carbon footprints of

circular bioenergy production systems. Renewable and Sustainable Energy Reviews. 111.

pp.224-235.

Kovermann, J. and Velte, P., 2019. The impact of corporate governance on corporate tax

avoidance—A literature review. Journal of International Accounting, Auditing and

Taxation. 36. p.100270.

Opferkuch, K. and et.al., 2021. Circular economy in corporate sustainability reporting: A review

of organisational approaches. Business Strategy and the Environment. 30(8). pp.4015-4036.

Willumsen, P. and et.al., 2019. Value creation through project risk management. International

Journal of Project Management. 37(5). pp.731-749.

Zaman, R. and et.al., 2022. Corporate governance meets corporate social responsibility: Mapping

the interface. Business & Society. 61(3). pp.690-752.

Online

8 Benefits of sustainability reporting. 2022. [Online]. Available through:

<https://sustainlab.co/blog/8-benefits-of-sustainability-reporting>

What Is a Risk Matrix? 2022. [Online]. Available through: <https://www.wrike.com/blog/what-

is-risk-matrix/#What-is-a-risk-assessment-matrix-in-project-management>

1

Books and Journals

Adnan, S. M., Hay, D. and van Staden, C. J., 2018. The influence of culture and corporate

governance on corporate social responsibility disclosure: A cross country analysis. Journal of

Cleaner Production. 198. pp.820-832.

Aifuwa, H. O., 2020. Sustainability reporting and firm performance in developing climes: A

review of literature. Copernican Journal of Finance & Accounting. 9(1). pp.9-29.

Amarasena, N., Haag, D. and Peres, K. G., 2019. A scoping review of caries risk management

protocols in Australia and New Zealand. Australian Dental Journal. 64(1). pp.19-26.

Boiral, O. and Heras-Saizarbitoria, I., 2020. Sustainability reporting assurance: Creating

stakeholder accountability through hyperreality? Journal of Cleaner Production. 243.

p.118596.

Gnanaweera, K. A. K. and Kunori, N., 2018. Corporate sustainability reporting: Linkage of

corporate disclosure information and performance indicators. Cogent Business &

Management. 5(1). p.1423872.

Holmatov, B., Hoekstra, A. Y. and Krol, M. S., 2019. Land, water and carbon footprints of

circular bioenergy production systems. Renewable and Sustainable Energy Reviews. 111.

pp.224-235.

Kovermann, J. and Velte, P., 2019. The impact of corporate governance on corporate tax

avoidance—A literature review. Journal of International Accounting, Auditing and

Taxation. 36. p.100270.

Opferkuch, K. and et.al., 2021. Circular economy in corporate sustainability reporting: A review

of organisational approaches. Business Strategy and the Environment. 30(8). pp.4015-4036.

Willumsen, P. and et.al., 2019. Value creation through project risk management. International

Journal of Project Management. 37(5). pp.731-749.

Zaman, R. and et.al., 2022. Corporate governance meets corporate social responsibility: Mapping

the interface. Business & Society. 61(3). pp.690-752.

Online

8 Benefits of sustainability reporting. 2022. [Online]. Available through:

<https://sustainlab.co/blog/8-benefits-of-sustainability-reporting>

What Is a Risk Matrix? 2022. [Online]. Available through: <https://www.wrike.com/blog/what-

is-risk-matrix/#What-is-a-risk-assessment-matrix-in-project-management>

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APPENDIX

Risk Management Table:

Risk Identified Likelihood Impact Action in Response

Improper operations

& governance

structure

Likely Medium Proper controls over

the operations and due

emphasis on the

structure of the

governance of the

entity.

Comparing with the

industry standards and

provide solution for

the variances found.

Biased management

and lack of controls

Possible Medium Change of

composition of

management and

involving external

unbiased personnel.

Avoid related party

transactions

transacted in the

entity.

Irregular reporting

and review of

performances

Very Likely High The reporting shall be

as per rules,

regulations and

requirements of the

stakeholders.

Stakeholders analysis

shall be done to know

the weak points where

2

Risk Management Table:

Risk Identified Likelihood Impact Action in Response

Improper operations

& governance

structure

Likely Medium Proper controls over

the operations and due

emphasis on the

structure of the

governance of the

entity.

Comparing with the

industry standards and

provide solution for

the variances found.

Biased management

and lack of controls

Possible Medium Change of

composition of

management and

involving external

unbiased personnel.

Avoid related party

transactions

transacted in the

entity.

Irregular reporting

and review of

performances

Very Likely High The reporting shall be

as per rules,

regulations and

requirements of the

stakeholders.

Stakeholders analysis

shall be done to know

the weak points where

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

entity is lagging.

No control over

sustainability issues

Possible Medium Although not

mandatory, but

sustainability issues

shall be reported for

healthier operations of

the entity and

showing the best

image of the entity as

it can and should.

Shipment error Very Likely High Control over shipment

by checking the

address on the item

matches with the

delivery slip.

Such shipment of

items shall be shown

as out of the stores

within a reasonable

time from such

shipment.

Shipment damaged Very Likely High Control over the

quality of the

packaging of the

items shipped.

Expenses on such

damage of the

shipment by the cargo

who is delivering the

items.

Late delivery Likely Medium Shall adhere to the

3

No control over

sustainability issues

Possible Medium Although not

mandatory, but

sustainability issues

shall be reported for

healthier operations of

the entity and

showing the best

image of the entity as

it can and should.

Shipment error Very Likely High Control over shipment

by checking the

address on the item

matches with the

delivery slip.

Such shipment of

items shall be shown

as out of the stores

within a reasonable

time from such

shipment.

Shipment damaged Very Likely High Control over the

quality of the

packaging of the

items shipped.

Expenses on such

damage of the

shipment by the cargo

who is delivering the

items.

Late delivery Likely Medium Shall adhere to the

3

regular delivery

schedule.

Control over the

cargo’s measures to

allow timely delivery.

Theft Very Likely High Security system of the

store shall be operated

continuously.

Unauthorized

personnel shall not be

allowed in the store

and the places where

such items are stored.

4

schedule.

Control over the

cargo’s measures to

allow timely delivery.

Theft Very Likely High Security system of the

store shall be operated

continuously.

Unauthorized

personnel shall not be

allowed in the store

and the places where

such items are stored.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.