Detailed Financial Analysis: Ford, Contentin PLC, and Santana PLC

VerifiedAdded on 2020/09/17

|10

|2292

|32

Report

AI Summary

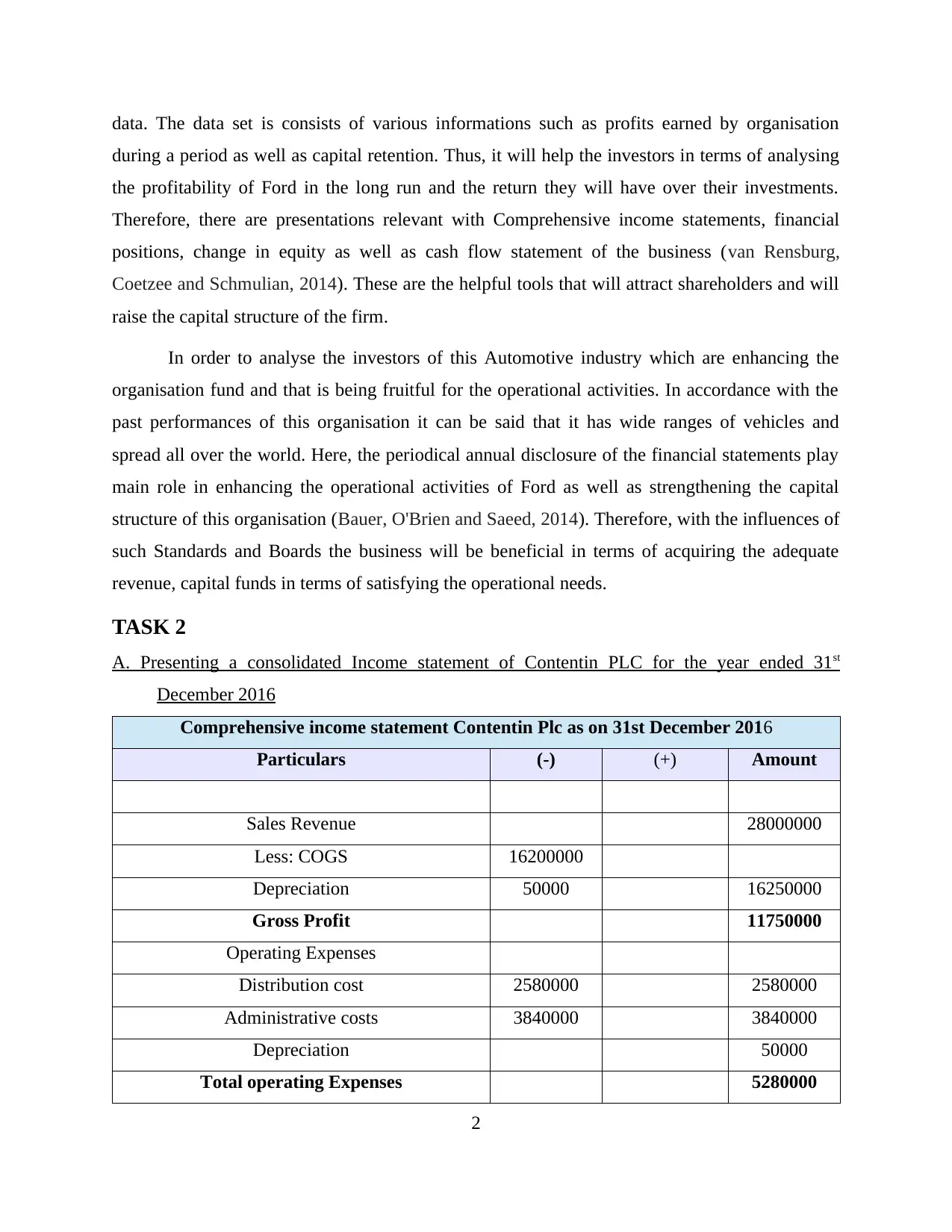

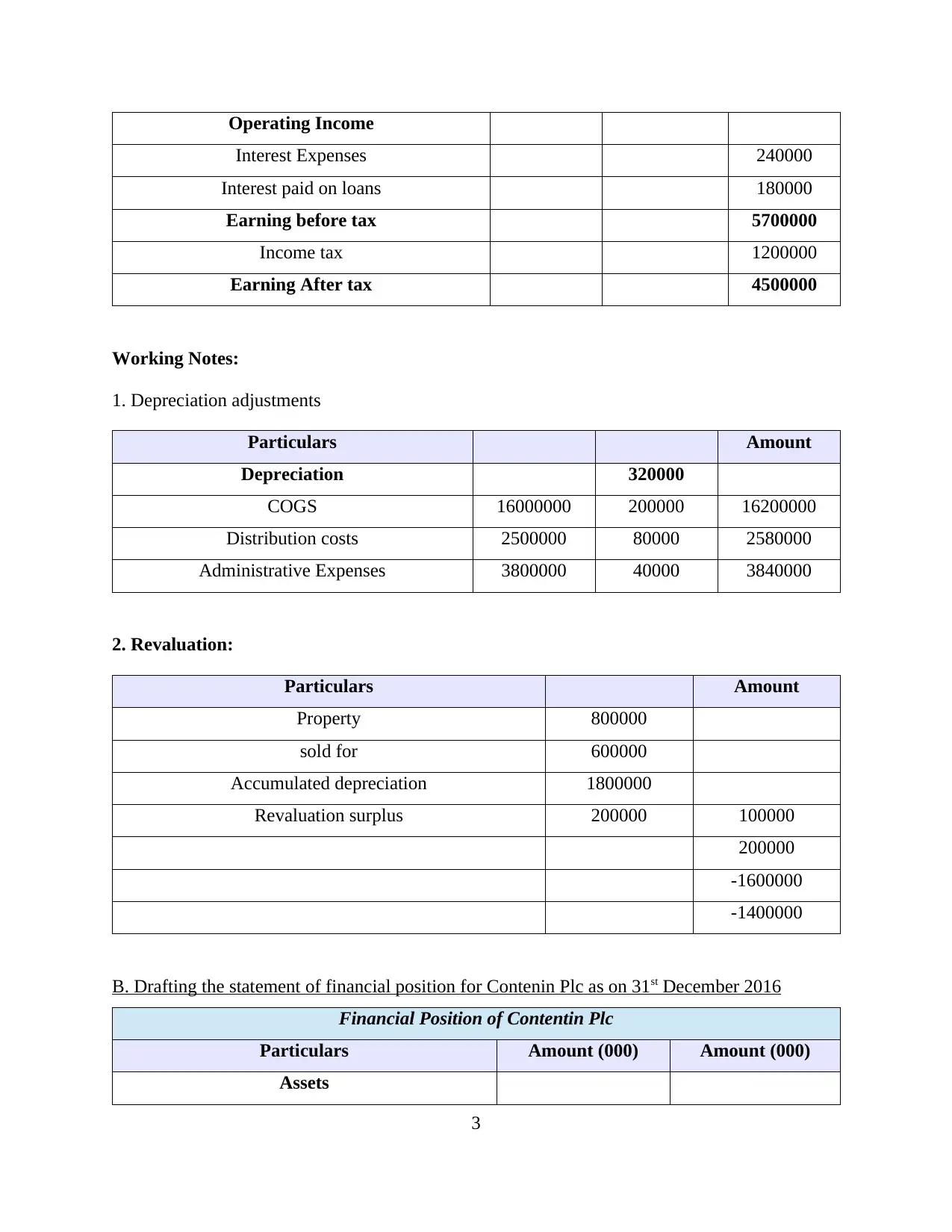

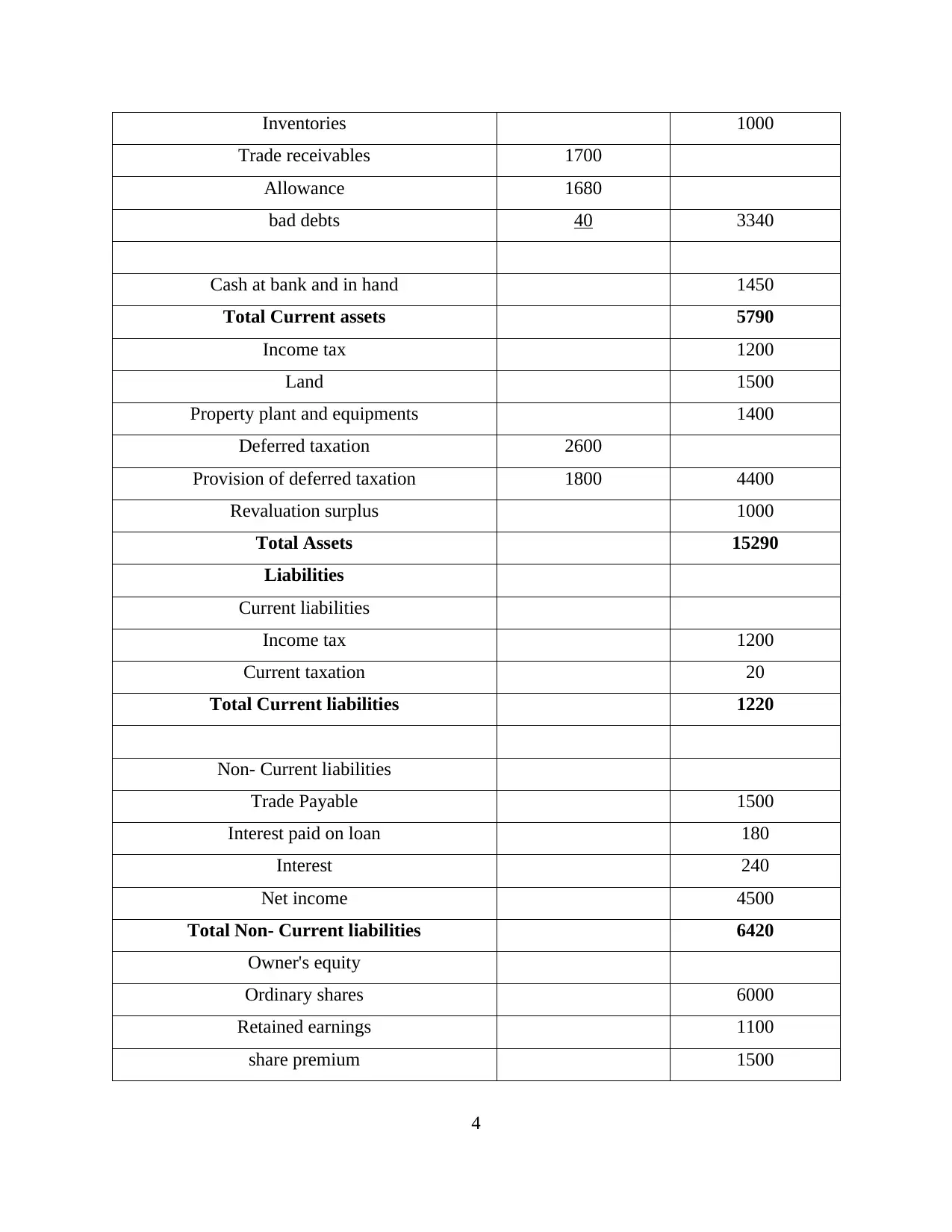

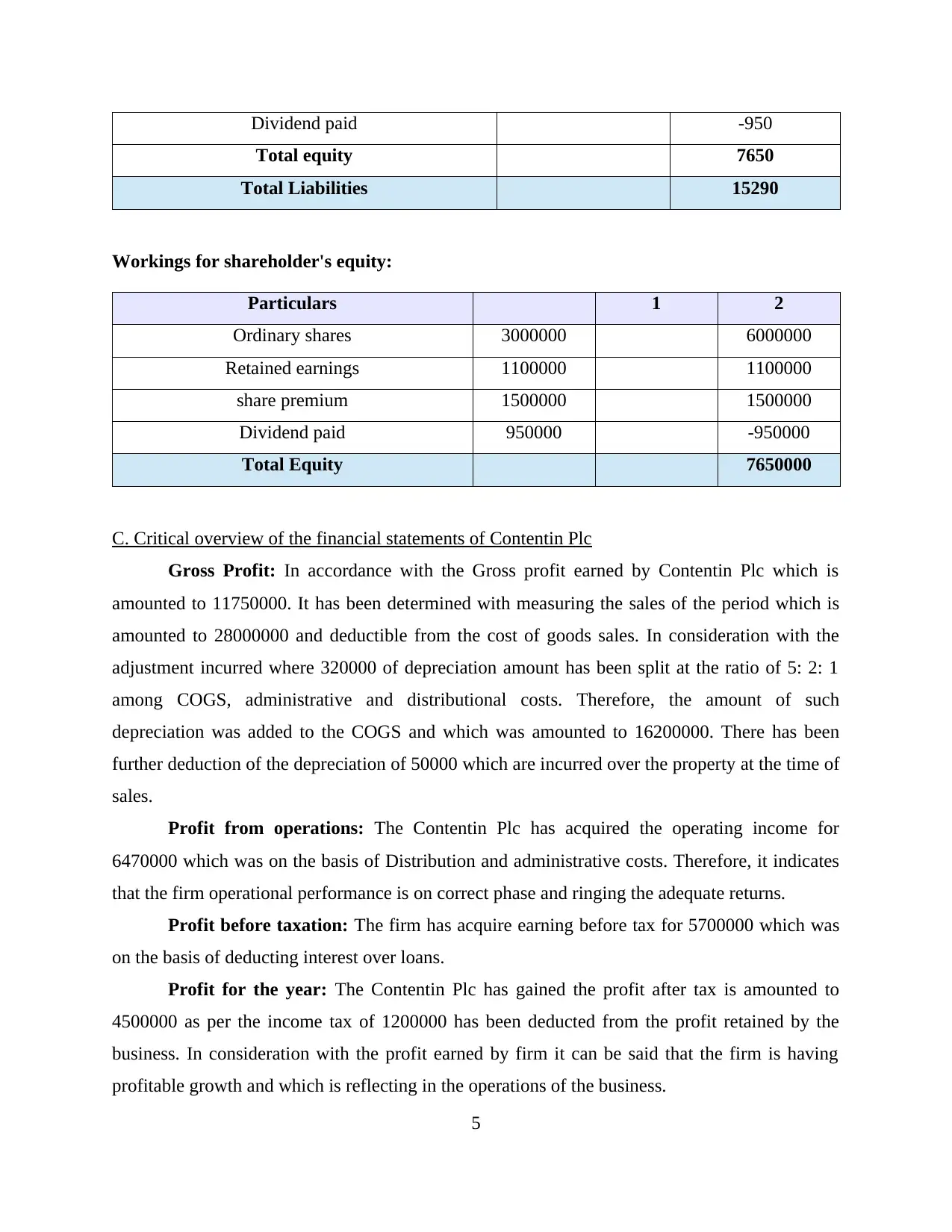

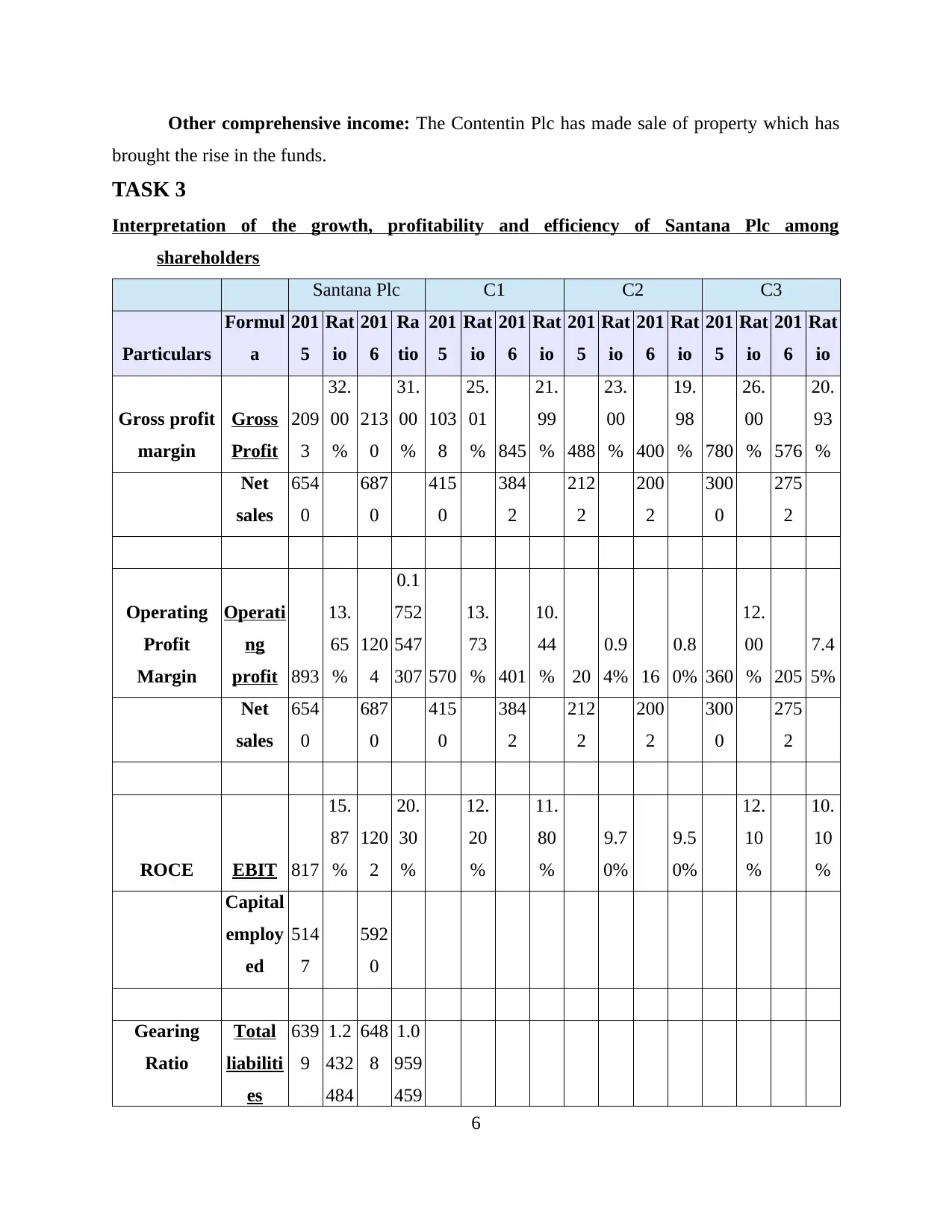

This report delves into the financial accounting practices and performance of several companies, including Ford, Contentin PLC, and Santana PLC. The analysis begins with an examination of the usefulness of the IASB Conceptual Framework for investors in Ford, highlighting its role in providing a universally accepted framework for presenting financial information and attracting investors. The report then presents and critically reviews the consolidated income statement and statement of financial position for Contentin PLC, providing detailed workings and adjustments. Finally, the report interprets the growth, profitability, and efficiency of Santana PLC for shareholders, utilizing financial ratios and comparative analysis to assess the company's performance. The report emphasizes key financial metrics such as gross profit margin, operating profit margin, ROCE, and gearing ratio, offering insights into each company's financial health and operational efficiency. The report includes working notes and references to support the financial analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.