Financial Statement Analysis of Ford Motor Credit Company: Report

VerifiedAdded on 2022/10/19

|6

|1497

|112

Report

AI Summary

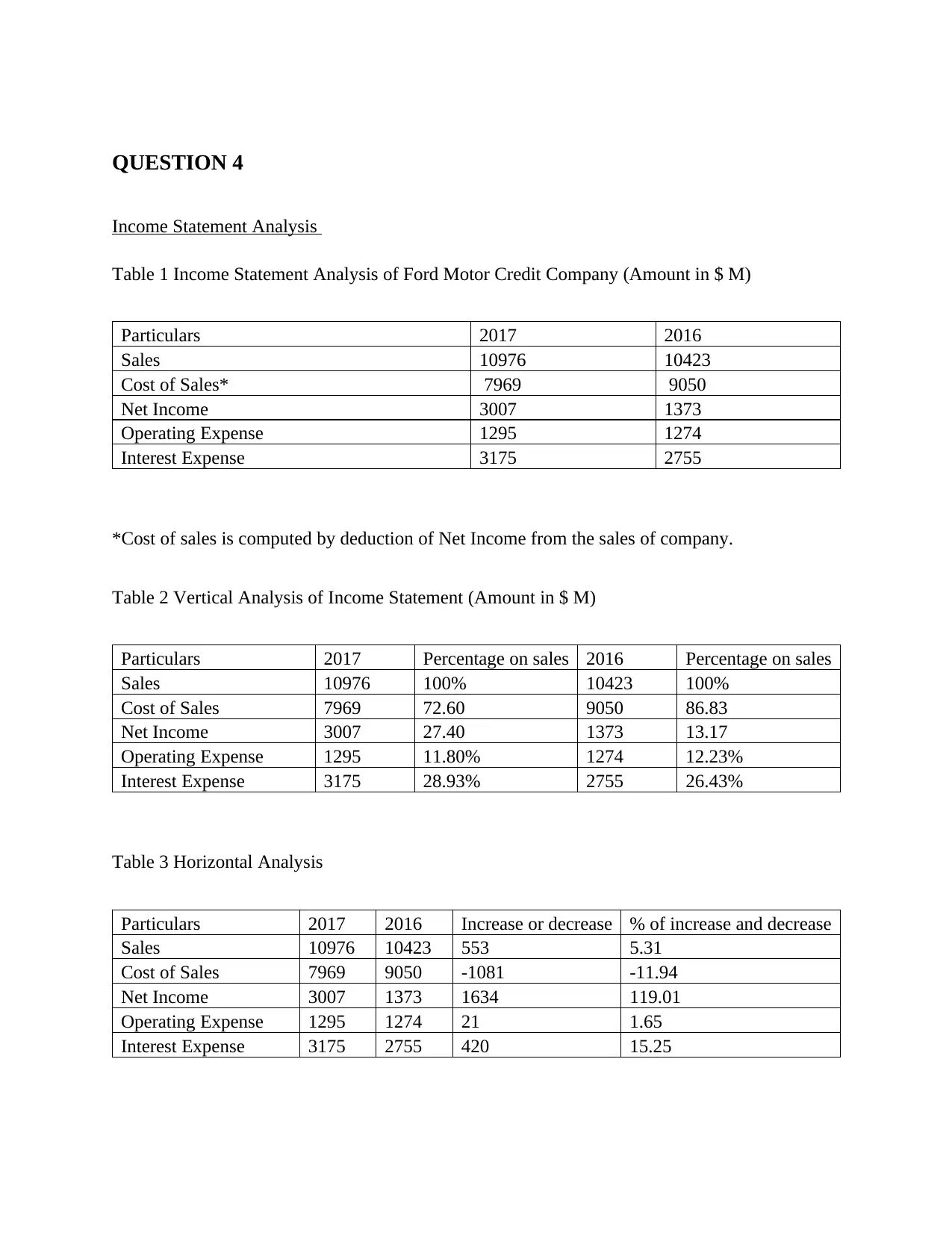

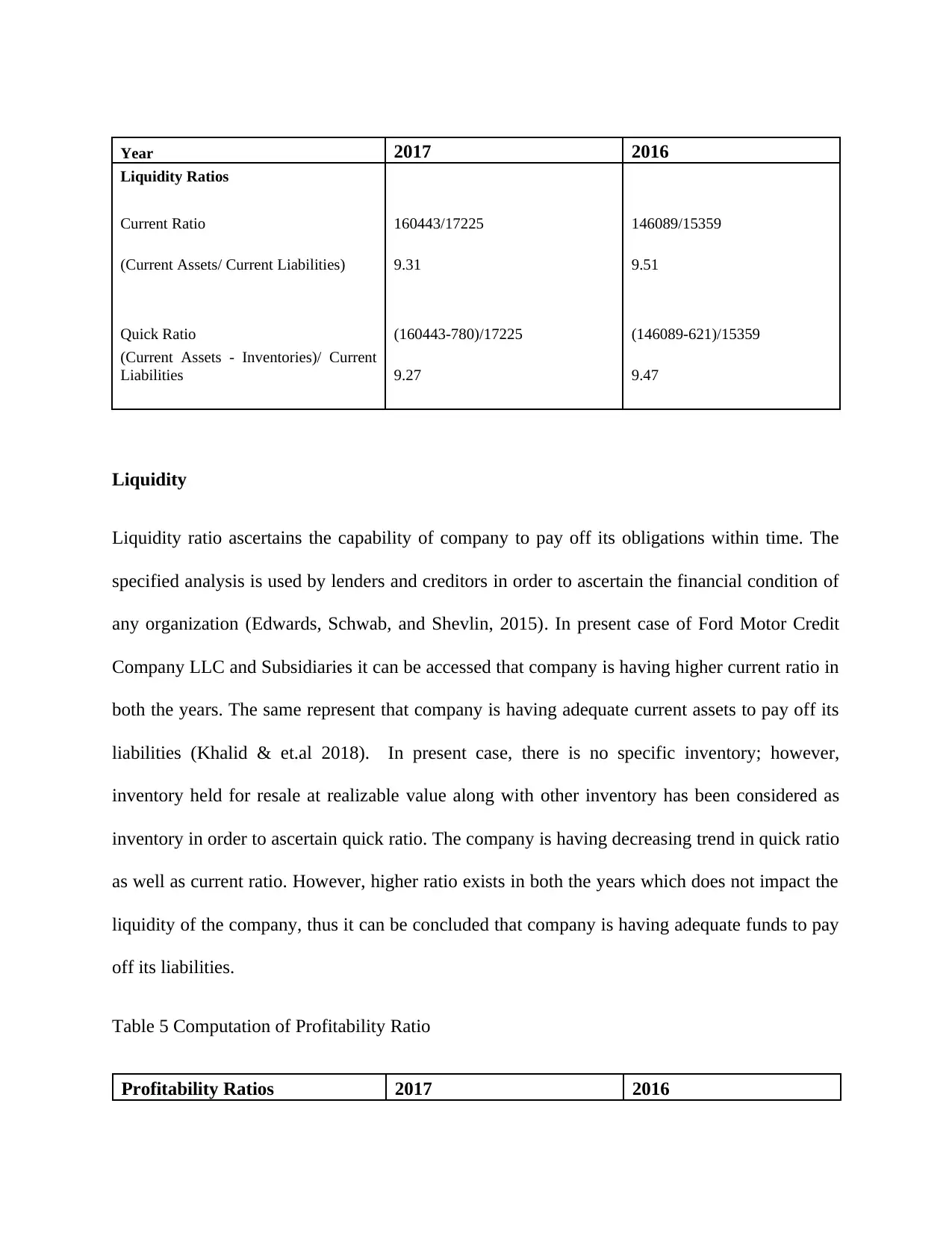

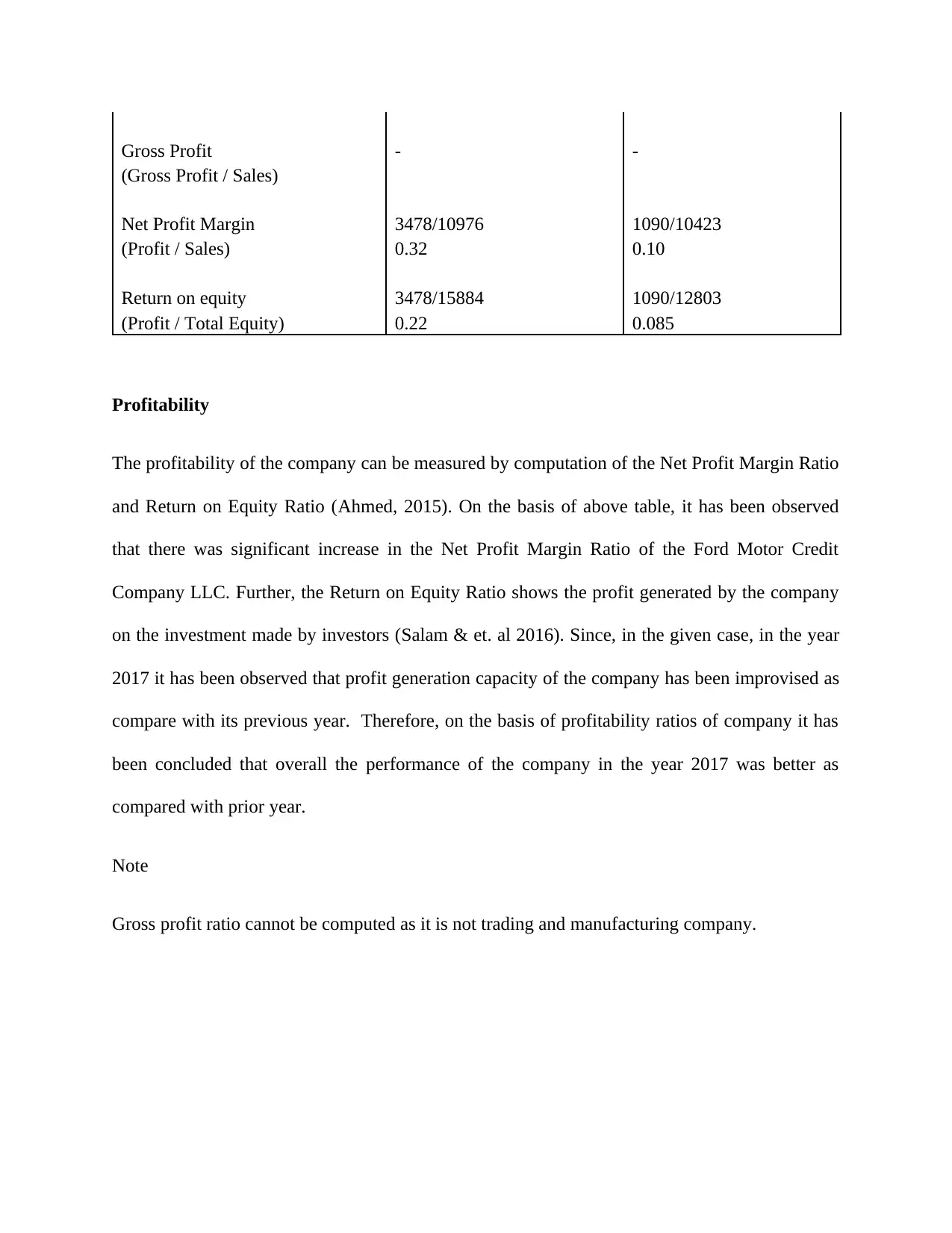

This report presents a detailed financial analysis of Ford Motor Credit Company, focusing on its performance in 2017. The analysis includes an examination of the income statement, utilizing both horizontal and vertical analysis techniques to assess trends and performance relative to sales. Key metrics such as cost of sales, net income, operating expenses, and interest expenses are analyzed to understand the company's profitability and cost management. Furthermore, the report delves into ratio analysis, evaluating liquidity through current and quick ratios and assessing profitability using net profit margin and return on equity. The findings indicate improvements in profitability and financial health in 2017 compared to the previous year, highlighting the company's effective strategies in revenue generation and cost control. The report also discusses the company's leverage position and its implications on financial performance. The analysis is supported by data from the company's financial statements and references relevant academic literature to provide a comprehensive understanding of Ford Motor Credit Company's financial standing.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.