Comprehensive Analysis of UK Taxation for Ford Motor Plc Operations

VerifiedAdded on 2020/12/10

|15

|3952

|180

Report

AI Summary

This report provides a comprehensive analysis of the UK taxation system, specifically examining its implications for Ford Motor Plc. The report begins with an introduction to taxation and the relevant legislations in the UK, followed by a demonstration of the taxation system, including direct and indirect taxes. The report then assesses the taxation systems of various nations, including the EU and US, for comparison. The analysis extends to the evaluation of tax liabilities for unincorporated industries, detailing their characteristics, advantages, and disadvantages. The report also includes the calculation of taxation liabilities for a hypothetical individual, Henry Ford. Finally, the report examines the taxable liabilities of incorporated organizations, such as Ford Motor Plc, and considers the legal and ethical constraints associated with taxation responsibilities. The report concludes with a summary of the key findings and a list of references.

TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Demonstrating the taxation system with consideration of taxation legislations in

UK................................................................................................................................................1

M1 Ascertaining the taxation system in different nations...................................................3

TASK 2............................................................................................................................................3

P2 Evaluating the tax liabilities for unincorporated industries...........................................3

M2 Implication of model and their interpretation..................................................................5

TASK 3............................................................................................................................................6

P3 Demonstration of the taxable liabilities with respect to incorporated organisations.6

TASK4.............................................................................................................................................9

P4 Examining the impact on organisation of legal and ethical constraints associated

with taxation responsibilities....................................................................................................9

M4 Analysing the impacts of legal and ethical constraints which will be applicable to

the organisation.......................................................................................................................10

CONCLUSION.............................................................................................................................11

REFERENCES............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Demonstrating the taxation system with consideration of taxation legislations in

UK................................................................................................................................................1

M1 Ascertaining the taxation system in different nations...................................................3

TASK 2............................................................................................................................................3

P2 Evaluating the tax liabilities for unincorporated industries...........................................3

M2 Implication of model and their interpretation..................................................................5

TASK 3............................................................................................................................................6

P3 Demonstration of the taxable liabilities with respect to incorporated organisations.6

TASK4.............................................................................................................................................9

P4 Examining the impact on organisation of legal and ethical constraints associated

with taxation responsibilities....................................................................................................9

M4 Analysing the impacts of legal and ethical constraints which will be applicable to

the organisation.......................................................................................................................10

CONCLUSION.............................................................................................................................11

REFERENCES............................................................................................................................12

INTRODUCTION

Taxation is the process of analysing a proportionate amount will be payable by an

individual with effect to make adequate analysis over the data base. They will be

charged on the basis of their tax threshold and the level of revenue retained by them. In

respect with such analysis there have been implications of various legislations and laws

which will be governing and adequate in meeting the goals. In the present report, there

will be analysis over Ford Motor Plc for analysing their corporation tax which have been

analysed on the basis of UK taxation system guidelines. Moreover, there will be

discussion based on taxation system of EU and US with comparison to UK tax system.

TASK 1

P1 Demonstrating the taxation system with consideration of taxation legislations in UK

Introduction:

Ford Motor plc have been performing in various nations on which implicating the

regulation of UK for determining the taxable consequences. It has been operating in

various countries such as US and Hungary. Thus, along with US is not performing well

which is regulating reflecting the negative outcomes. Hungary and UK are consistently

retaining appropriate profit from 2013 to 2018.

Taxation:

This is a term on which government levied taxes on various things such as

personal income, business revenue, and of product & services. it brings them the

adequate amount of reserves for the economic development such as infrastructure

development, facilitating the medical and educational facilities among the society.

Taxation system:

In respect with analysing the taxation system in UK on which it has been analysed

that, there have been various rules and regulation which are enacted to establish fair

taxation system. in UK there are three governmental level which governs these policies

such as central, local and development government (Egger and et.al., 2015). In this

aspect, there will be effective control over legislative environment in UK is mainly

governed by HMRC

4 Direct and Indirect taxation systems in UK:

1

Taxation is the process of analysing a proportionate amount will be payable by an

individual with effect to make adequate analysis over the data base. They will be

charged on the basis of their tax threshold and the level of revenue retained by them. In

respect with such analysis there have been implications of various legislations and laws

which will be governing and adequate in meeting the goals. In the present report, there

will be analysis over Ford Motor Plc for analysing their corporation tax which have been

analysed on the basis of UK taxation system guidelines. Moreover, there will be

discussion based on taxation system of EU and US with comparison to UK tax system.

TASK 1

P1 Demonstrating the taxation system with consideration of taxation legislations in UK

Introduction:

Ford Motor plc have been performing in various nations on which implicating the

regulation of UK for determining the taxable consequences. It has been operating in

various countries such as US and Hungary. Thus, along with US is not performing well

which is regulating reflecting the negative outcomes. Hungary and UK are consistently

retaining appropriate profit from 2013 to 2018.

Taxation:

This is a term on which government levied taxes on various things such as

personal income, business revenue, and of product & services. it brings them the

adequate amount of reserves for the economic development such as infrastructure

development, facilitating the medical and educational facilities among the society.

Taxation system:

In respect with analysing the taxation system in UK on which it has been analysed

that, there have been various rules and regulation which are enacted to establish fair

taxation system. in UK there are three governmental level which governs these policies

such as central, local and development government (Egger and et.al., 2015). In this

aspect, there will be effective control over legislative environment in UK is mainly

governed by HMRC

4 Direct and Indirect taxation systems in UK:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

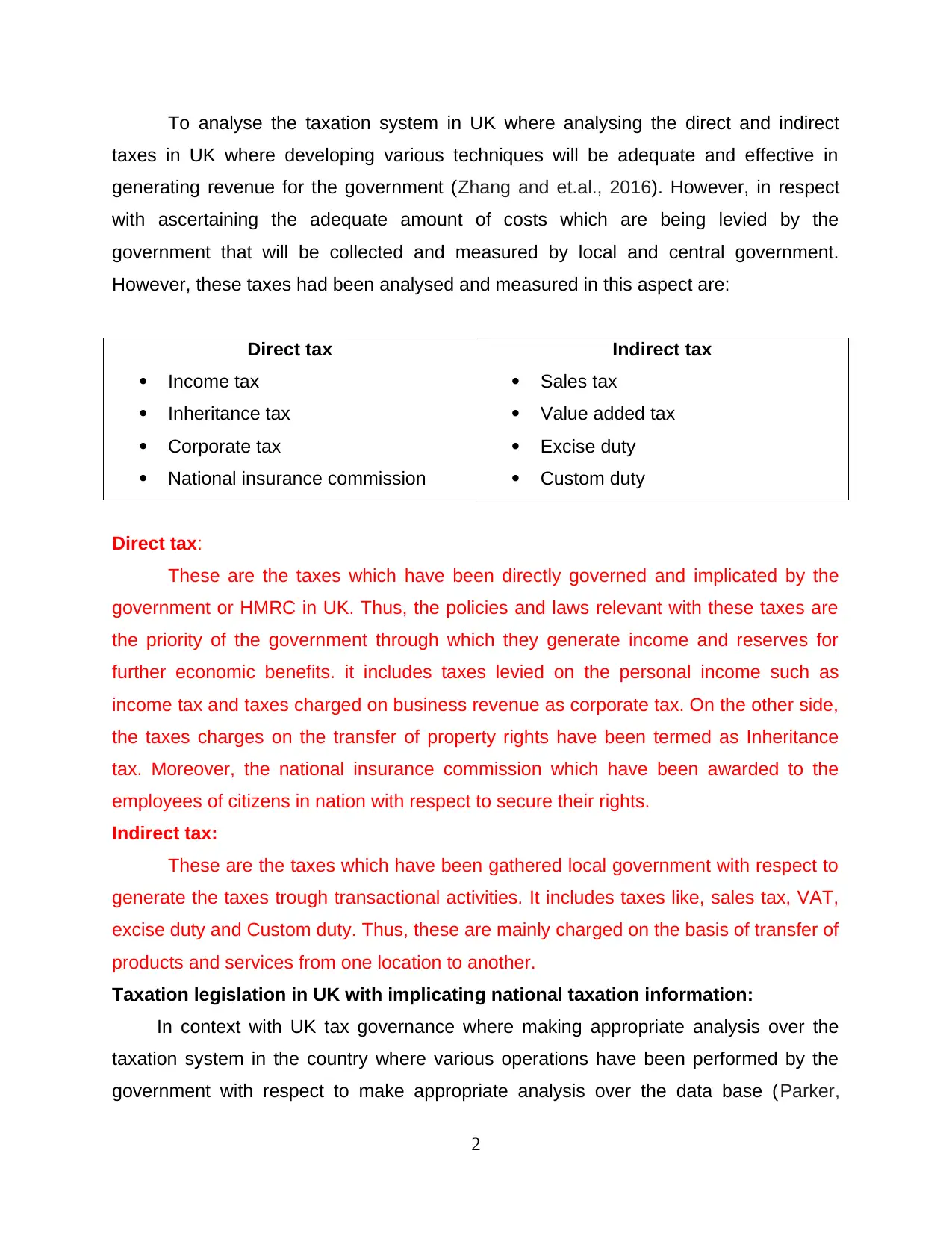

To analyse the taxation system in UK where analysing the direct and indirect

taxes in UK where developing various techniques will be adequate and effective in

generating revenue for the government (Zhang and et.al., 2016). However, in respect

with ascertaining the adequate amount of costs which are being levied by the

government that will be collected and measured by local and central government.

However, these taxes had been analysed and measured in this aspect are:

Direct tax

Income tax

Inheritance tax

Corporate tax

National insurance commission

Indirect tax

Sales tax

Value added tax

Excise duty

Custom duty

Direct tax:

These are the taxes which have been directly governed and implicated by the

government or HMRC in UK. Thus, the policies and laws relevant with these taxes are

the priority of the government through which they generate income and reserves for

further economic benefits. it includes taxes levied on the personal income such as

income tax and taxes charged on business revenue as corporate tax. On the other side,

the taxes charges on the transfer of property rights have been termed as Inheritance

tax. Moreover, the national insurance commission which have been awarded to the

employees of citizens in nation with respect to secure their rights.

Indirect tax:

These are the taxes which have been gathered local government with respect to

generate the taxes trough transactional activities. It includes taxes like, sales tax, VAT,

excise duty and Custom duty. Thus, these are mainly charged on the basis of transfer of

products and services from one location to another.

Taxation legislation in UK with implicating national taxation information:

In context with UK tax governance where making appropriate analysis over the

taxation system in the country where various operations have been performed by the

government with respect to make appropriate analysis over the data base (Parker,

2

taxes in UK where developing various techniques will be adequate and effective in

generating revenue for the government (Zhang and et.al., 2016). However, in respect

with ascertaining the adequate amount of costs which are being levied by the

government that will be collected and measured by local and central government.

However, these taxes had been analysed and measured in this aspect are:

Direct tax

Income tax

Inheritance tax

Corporate tax

National insurance commission

Indirect tax

Sales tax

Value added tax

Excise duty

Custom duty

Direct tax:

These are the taxes which have been directly governed and implicated by the

government or HMRC in UK. Thus, the policies and laws relevant with these taxes are

the priority of the government through which they generate income and reserves for

further economic benefits. it includes taxes levied on the personal income such as

income tax and taxes charged on business revenue as corporate tax. On the other side,

the taxes charges on the transfer of property rights have been termed as Inheritance

tax. Moreover, the national insurance commission which have been awarded to the

employees of citizens in nation with respect to secure their rights.

Indirect tax:

These are the taxes which have been gathered local government with respect to

generate the taxes trough transactional activities. It includes taxes like, sales tax, VAT,

excise duty and Custom duty. Thus, these are mainly charged on the basis of transfer of

products and services from one location to another.

Taxation legislation in UK with implicating national taxation information:

In context with UK tax governance where making appropriate analysis over the

taxation system in the country where various operations have been performed by the

government with respect to make appropriate analysis over the data base (Parker,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2018). Considering the personal and industrial tax which have been collected by the

HMRC and central government.

M1 Ascertaining the taxation system in different nations

Analysing the taxation system in other nations on which there have been

governance over businesses, rules, taxes as well as remedied allowed to the oversea

trading had been ascertained. Therefore, there are various Tarde blocs which enables

the countries to make appropriate trade practices among each other with considering

the remedies and allowance associated with them such as:

European Union (EU): To facilitate the fair-trade practices among the European

countries of the member of EU have been benefits with the various taxable remedies

(Saez and Stantcheva, 2016). There had been lower charges and taxes had been given

to them with respect to bring fair taxation. It has helped in bring the taxable remedies

such as concession in tariffs, custom duties etc.

Asia-Pacific Trade bloc (APEC): It is mainly operating trade bloc facilities in the

Asia-pacific region to help in getting the adequate ascertainment of the operational

practices (What is Asia-Pacific Economic Cooperation, 2017). There will be special

rights and regulation which were being awarded among the countries who are members

to this organisation.

North-American free-trade agreement (NAFTA): This is the trade bloc which is

helpful in facilitating the free trade services among the north American region countries

(Martin and et.al., 2016). They have been benefits with the various taxable allowances

on the sales, services, duties and customs.

TASK 2

P2 Evaluating the tax liabilities for unincorporated industries

Unincorporated industries: To analyse the framework for these organisations

which are determined as the non-trading industries in capital market. Therefore, there

can be influences of partnership and sole proprietor businesses (Storey, 2016).

However, these firms will not make dealings in any share liabilities. There will be single

governance authorities and decision will be made by an individual.

Characteristics and background:

3

HMRC and central government.

M1 Ascertaining the taxation system in different nations

Analysing the taxation system in other nations on which there have been

governance over businesses, rules, taxes as well as remedied allowed to the oversea

trading had been ascertained. Therefore, there are various Tarde blocs which enables

the countries to make appropriate trade practices among each other with considering

the remedies and allowance associated with them such as:

European Union (EU): To facilitate the fair-trade practices among the European

countries of the member of EU have been benefits with the various taxable remedies

(Saez and Stantcheva, 2016). There had been lower charges and taxes had been given

to them with respect to bring fair taxation. It has helped in bring the taxable remedies

such as concession in tariffs, custom duties etc.

Asia-Pacific Trade bloc (APEC): It is mainly operating trade bloc facilities in the

Asia-pacific region to help in getting the adequate ascertainment of the operational

practices (What is Asia-Pacific Economic Cooperation, 2017). There will be special

rights and regulation which were being awarded among the countries who are members

to this organisation.

North-American free-trade agreement (NAFTA): This is the trade bloc which is

helpful in facilitating the free trade services among the north American region countries

(Martin and et.al., 2016). They have been benefits with the various taxable allowances

on the sales, services, duties and customs.

TASK 2

P2 Evaluating the tax liabilities for unincorporated industries

Unincorporated industries: To analyse the framework for these organisations

which are determined as the non-trading industries in capital market. Therefore, there

can be influences of partnership and sole proprietor businesses (Storey, 2016).

However, these firms will not make dealings in any share liabilities. There will be single

governance authorities and decision will be made by an individual.

Characteristics and background:

3

It has been denoted as the separate legal entity which has the formal corporate

status.

The policies and planning for the financial operation have been determined by a

single governing authority (What is Asia-Pacific Economic Cooperation, 2017).

There will be lower debts which are being associated with the business

operations on which determining the operational goals and motives are the prime

concern in the business.

There will be less influences of employees as it is comparatively lower.

Advantages and Disadvantages:

There has been fruitfulness as well as loopholes to the business which can be

determined as:

Advantages:

It has the separate legal entity which will be helpful to the business in terms of

retaining the gains for the longer terms.

Single governance decisions have been made by the professionals in

organisation which will be adequate and attentive in respect to meet the

operational goals at the right time.

Low number of members on which there will be less influences in the decision

making and development of policies for the operations (Devereux, Liu and

Loretz, 2014).

Determination of adequate power and corporate management will be appropriate

in analysing the operational details and management of firm’s activities.

Business have been operating on the small scale of operations on which there

will be limited liabilities and the debts to be paid by firm.

Disadvantages:

There will be issues relevant with the in appropriate allocation of the costs in

each business activities.

There will be risks which are relevant with the capital control and management of

funds.

4

status.

The policies and planning for the financial operation have been determined by a

single governing authority (What is Asia-Pacific Economic Cooperation, 2017).

There will be lower debts which are being associated with the business

operations on which determining the operational goals and motives are the prime

concern in the business.

There will be less influences of employees as it is comparatively lower.

Advantages and Disadvantages:

There has been fruitfulness as well as loopholes to the business which can be

determined as:

Advantages:

It has the separate legal entity which will be helpful to the business in terms of

retaining the gains for the longer terms.

Single governance decisions have been made by the professionals in

organisation which will be adequate and attentive in respect to meet the

operational goals at the right time.

Low number of members on which there will be less influences in the decision

making and development of policies for the operations (Devereux, Liu and

Loretz, 2014).

Determination of adequate power and corporate management will be appropriate

in analysing the operational details and management of firm’s activities.

Business have been operating on the small scale of operations on which there

will be limited liabilities and the debts to be paid by firm.

Disadvantages:

There will be issues relevant with the in appropriate allocation of the costs in

each business activities.

There will be risks which are relevant with the capital control and management of

funds.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

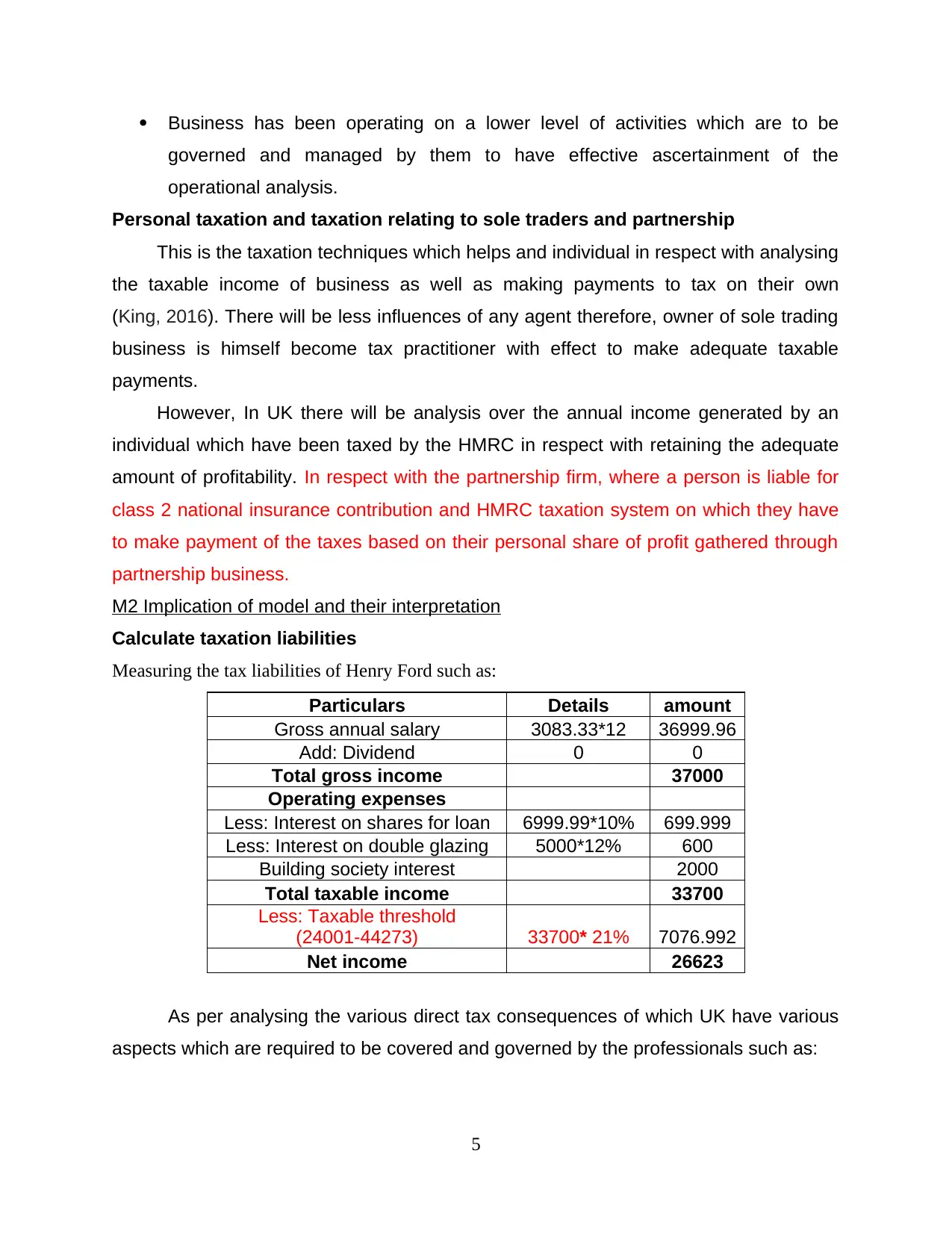

Business has been operating on a lower level of activities which are to be

governed and managed by them to have effective ascertainment of the

operational analysis.

Personal taxation and taxation relating to sole traders and partnership

This is the taxation techniques which helps and individual in respect with analysing

the taxable income of business as well as making payments to tax on their own

(King, 2016). There will be less influences of any agent therefore, owner of sole trading

business is himself become tax practitioner with effect to make adequate taxable

payments.

However, In UK there will be analysis over the annual income generated by an

individual which have been taxed by the HMRC in respect with retaining the adequate

amount of profitability. In respect with the partnership firm, where a person is liable for

class 2 national insurance contribution and HMRC taxation system on which they have

to make payment of the taxes based on their personal share of profit gathered through

partnership business.

M2 Implication of model and their interpretation

Calculate taxation liabilities

Measuring the tax liabilities of Henry Ford such as:

Particulars Details amount

Gross annual salary 3083.33*12 36999.96

Add: Dividend 0 0

Total gross income 37000

Operating expenses

Less: Interest on shares for loan 6999.99*10% 699.999

Less: Interest on double glazing 5000*12% 600

Building society interest 2000

Total taxable income 33700

Less: Taxable threshold

(24001-44273) 33700* 21% 7076.992

Net income 26623

As per analysing the various direct tax consequences of which UK have various

aspects which are required to be covered and governed by the professionals such as:

5

governed and managed by them to have effective ascertainment of the

operational analysis.

Personal taxation and taxation relating to sole traders and partnership

This is the taxation techniques which helps and individual in respect with analysing

the taxable income of business as well as making payments to tax on their own

(King, 2016). There will be less influences of any agent therefore, owner of sole trading

business is himself become tax practitioner with effect to make adequate taxable

payments.

However, In UK there will be analysis over the annual income generated by an

individual which have been taxed by the HMRC in respect with retaining the adequate

amount of profitability. In respect with the partnership firm, where a person is liable for

class 2 national insurance contribution and HMRC taxation system on which they have

to make payment of the taxes based on their personal share of profit gathered through

partnership business.

M2 Implication of model and their interpretation

Calculate taxation liabilities

Measuring the tax liabilities of Henry Ford such as:

Particulars Details amount

Gross annual salary 3083.33*12 36999.96

Add: Dividend 0 0

Total gross income 37000

Operating expenses

Less: Interest on shares for loan 6999.99*10% 699.999

Less: Interest on double glazing 5000*12% 600

Building society interest 2000

Total taxable income 33700

Less: Taxable threshold

(24001-44273) 33700* 21% 7076.992

Net income 26623

As per analysing the various direct tax consequences of which UK have various

aspects which are required to be covered and governed by the professionals such as:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Personal allowances: In respect with analysing the remedies and the help from

government on the income generated by the professionals with respect to meet the

goals at the right time (Berry, 2016). These are the allowances which have been

awarded by the employer to its employees on transportation, education fees, college

fees, meals and similar remedies. however, these are the allowances will help a person

in having lower taxable expenses.

Capital gain tax: These are the taxes which have been charged on the purchase

and sale of an asset. These are the taxes which have been payable by a person or an

organisation with respect to make payment to taxes there are associated with such

deals (Meier and et.al., 2016). It mainly includes assets like land and buildings, Fixtures

and fittings, marketable securities, goodwill and trademarks.

National insurance contribution: These are the tax and the contribution which

have generated by the state government with respect to bring the health insurance to

each citizen or the employees which are earning above 162 pound a week (National

Insurance, 2017).

Inheritance tax: These are the taxes on the property of the person who has

died, and which will be charged through a person who have possession over the

property (Hall and Buckley, 2016). Therefore, in UK it is mainly charged on the rate of

40% which is over the threshold.

Corporation tax: As per developing the tax consequences of the organisation on

which there have been various legislative influences have made incurrence in the

operations. the taxes have been charged on the revenue or profits generated by firms in

a respective year (Devereux and Vella, 2014).

TASK 3

P3 Demonstration of the taxable liabilities with respect to incorporated organisations

Incorporated Organisation:

To analyse the incorporated organisation on which Ford has been operating as

public limited organisation as they sales the marketable securities. Therefore, these

organisations are performing in group as operating in various nations. Similarly, Ford

Motor Plc have been acting as the Public limited organisation as it has various branches

in several nations such as UK, US and Hungary. Therefore, if there is any issue

6

government on the income generated by the professionals with respect to meet the

goals at the right time (Berry, 2016). These are the allowances which have been

awarded by the employer to its employees on transportation, education fees, college

fees, meals and similar remedies. however, these are the allowances will help a person

in having lower taxable expenses.

Capital gain tax: These are the taxes which have been charged on the purchase

and sale of an asset. These are the taxes which have been payable by a person or an

organisation with respect to make payment to taxes there are associated with such

deals (Meier and et.al., 2016). It mainly includes assets like land and buildings, Fixtures

and fittings, marketable securities, goodwill and trademarks.

National insurance contribution: These are the tax and the contribution which

have generated by the state government with respect to bring the health insurance to

each citizen or the employees which are earning above 162 pound a week (National

Insurance, 2017).

Inheritance tax: These are the taxes on the property of the person who has

died, and which will be charged through a person who have possession over the

property (Hall and Buckley, 2016). Therefore, in UK it is mainly charged on the rate of

40% which is over the threshold.

Corporation tax: As per developing the tax consequences of the organisation on

which there have been various legislative influences have made incurrence in the

operations. the taxes have been charged on the revenue or profits generated by firms in

a respective year (Devereux and Vella, 2014).

TASK 3

P3 Demonstration of the taxable liabilities with respect to incorporated organisations

Incorporated Organisation:

To analyse the incorporated organisation on which Ford has been operating as

public limited organisation as they sales the marketable securities. Therefore, these

organisations are performing in group as operating in various nations. Similarly, Ford

Motor Plc have been acting as the Public limited organisation as it has various branches

in several nations such as UK, US and Hungary. Therefore, if there is any issue

6

incurred of crisis occurred the entire group will be responsible instead of a particular

individual. Therefore, the profit of losses has to be divided equally or proportionately

among the group.

Characteristics

There is limited individual liabilities as the business debts have been based on

entire group to be responsible for such debts.

Ownership of an incorporated group can be effective on personal property or a

person entering into a particular group.

There will be governance from everyone which is operating activities in the

business.

Advantages and disadvantages

Incorporated business refers to turning the sole proprietorship of partnership into

a company. It is a legal process which is used to form a corporate entity. Incorporated

business is separate entity different from its owners (Egger and et.al., 2015).

Incorporation of a company limits its individual liability. When the company incorporates

it becomes its own legal structure separate from the individual that founded that

business.

Advantages and disadvantages of Incorporated business

Advantages

Incorporation provides the firm such as sole proprietorship and partnership with

advantages of limited liability by incorporating their business. It helps in

protecting the personal assets of the individual if it has incorporated its business.

Incorporating the business helps the firm in increasing the credibility in the eyes

of customers, lenders, employees etc. due to this capital of the organisation

rises.

Companies gain tax benefits when incorporate. Sole proprietor does not have tax

benefits whereas the corporation enjoys the tax benefits.

It also helps the business in evolution. This includes changes in the article of

association, change in the name of company, changing membership on the

board of directors.

Disadvantages

7

individual. Therefore, the profit of losses has to be divided equally or proportionately

among the group.

Characteristics

There is limited individual liabilities as the business debts have been based on

entire group to be responsible for such debts.

Ownership of an incorporated group can be effective on personal property or a

person entering into a particular group.

There will be governance from everyone which is operating activities in the

business.

Advantages and disadvantages

Incorporated business refers to turning the sole proprietorship of partnership into

a company. It is a legal process which is used to form a corporate entity. Incorporated

business is separate entity different from its owners (Egger and et.al., 2015).

Incorporation of a company limits its individual liability. When the company incorporates

it becomes its own legal structure separate from the individual that founded that

business.

Advantages and disadvantages of Incorporated business

Advantages

Incorporation provides the firm such as sole proprietorship and partnership with

advantages of limited liability by incorporating their business. It helps in

protecting the personal assets of the individual if it has incorporated its business.

Incorporating the business helps the firm in increasing the credibility in the eyes

of customers, lenders, employees etc. due to this capital of the organisation

rises.

Companies gain tax benefits when incorporate. Sole proprietor does not have tax

benefits whereas the corporation enjoys the tax benefits.

It also helps the business in evolution. This includes changes in the article of

association, change in the name of company, changing membership on the

board of directors.

Disadvantages

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Incorporating a business include paying double taxation due to which the

incorporated company have to pay tax twice in a year. Double taxation involves

corporation tax and income tax.

The incorporated company also have disadvantage of lack of ownership as the

business become separate legal entity.

Incorporating a business requires more formalities and paperwork due to which

time is wasted.

Incorporating a business is expensive as it will require more time to set up as

compared to other business. The charges for incorporating a business are more due to

which it becomes as expensive process.

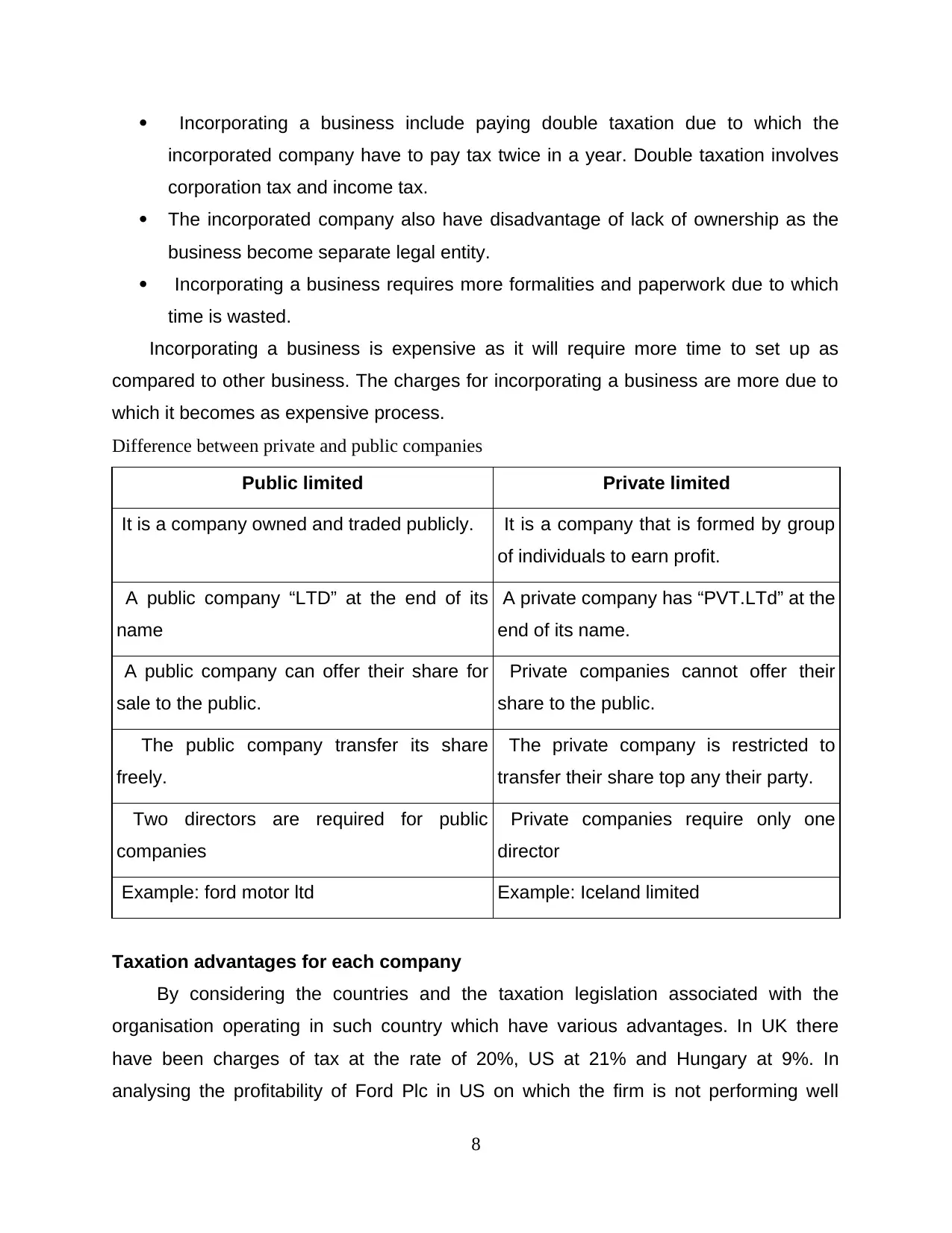

Difference between private and public companies

Public limited Private limited

It is a company owned and traded publicly. It is a company that is formed by group

of individuals to earn profit.

A public company “LTD” at the end of its

name

A private company has “PVT.LTd” at the

end of its name.

A public company can offer their share for

sale to the public.

Private companies cannot offer their

share to the public.

The public company transfer its share

freely.

The private company is restricted to

transfer their share top any their party.

Two directors are required for public

companies

Private companies require only one

director

Example: ford motor ltd Example: Iceland limited

Taxation advantages for each company

By considering the countries and the taxation legislation associated with the

organisation operating in such country which have various advantages. In UK there

have been charges of tax at the rate of 20%, US at 21% and Hungary at 9%. In

analysing the profitability of Ford Plc in US on which the firm is not performing well

8

incorporated company have to pay tax twice in a year. Double taxation involves

corporation tax and income tax.

The incorporated company also have disadvantage of lack of ownership as the

business become separate legal entity.

Incorporating a business requires more formalities and paperwork due to which

time is wasted.

Incorporating a business is expensive as it will require more time to set up as

compared to other business. The charges for incorporating a business are more due to

which it becomes as expensive process.

Difference between private and public companies

Public limited Private limited

It is a company owned and traded publicly. It is a company that is formed by group

of individuals to earn profit.

A public company “LTD” at the end of its

name

A private company has “PVT.LTd” at the

end of its name.

A public company can offer their share for

sale to the public.

Private companies cannot offer their

share to the public.

The public company transfer its share

freely.

The private company is restricted to

transfer their share top any their party.

Two directors are required for public

companies

Private companies require only one

director

Example: ford motor ltd Example: Iceland limited

Taxation advantages for each company

By considering the countries and the taxation legislation associated with the

organisation operating in such country which have various advantages. In UK there

have been charges of tax at the rate of 20%, US at 21% and Hungary at 9%. In

analysing the profitability of Ford Plc in US on which the firm is not performing well

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which have brought them the negative outcomes (Zhang and et.al., 2016). Therefore, in

UK and Hungary the firm is retaining appropriate profitability per year

Advantages of taxation to private companies:

There have been various benefits and appropriate help which have been

awarded to the private industries which were in respect to a limited liability business.

These businesses are personally liable for any financial losses on which there have

been issues relevant with the unprotected financial claims on which things are probably

going wrong.

Advantages of taxation to public companies:

These are the organisation which have created for a specific motive of tax to be

done. Thus, such analysis and ascertainment of businesses have various taxable

remedies in terms of profit sharing as well as have are protected from damages due to

aby financial losses. Thus, with impacts of such securities there are usually large

number of investors.

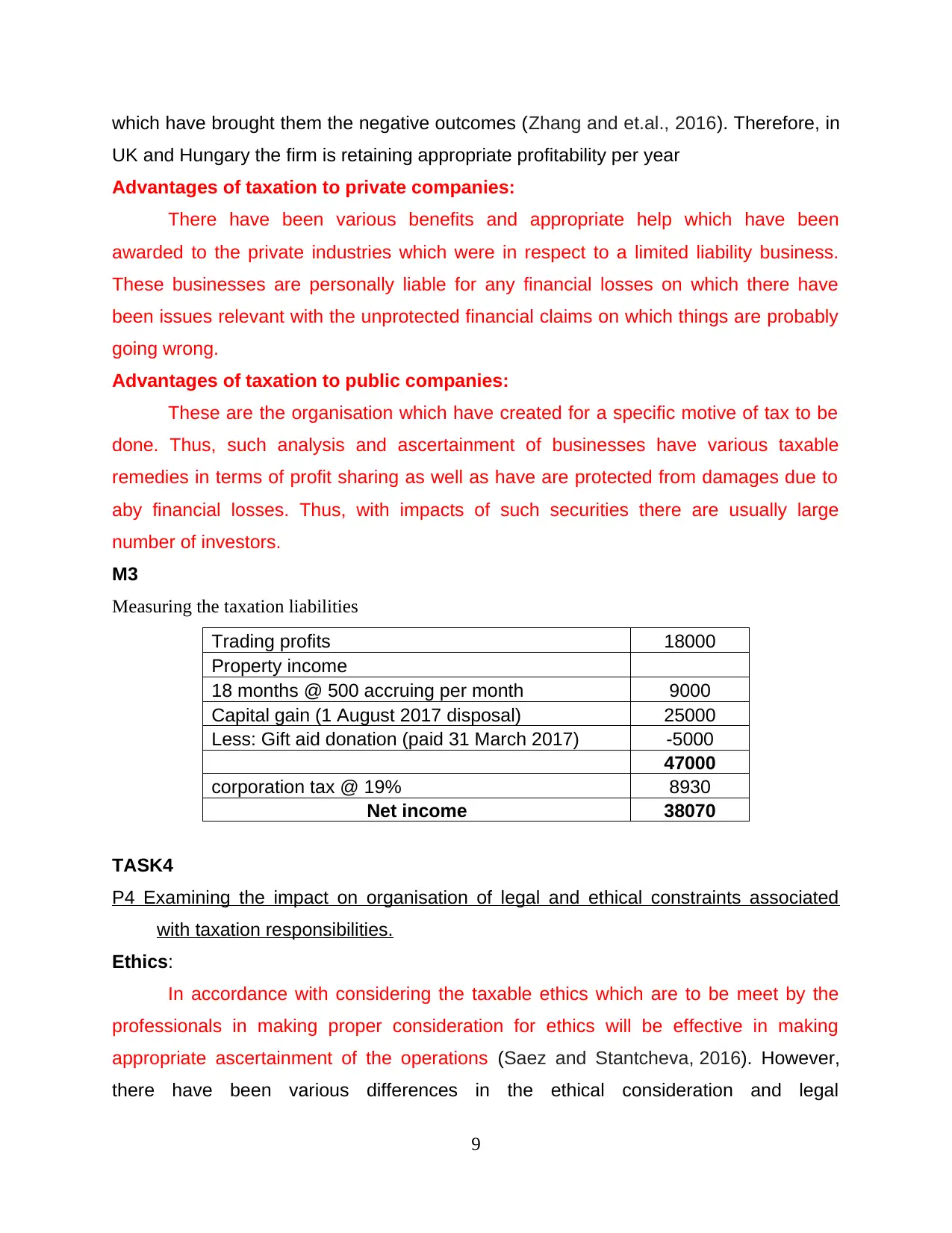

M3

Measuring the taxation liabilities

Trading profits 18000

Property income

18 months @ 500 accruing per month 9000

Capital gain (1 August 2017 disposal) 25000

Less: Gift aid donation (paid 31 March 2017) -5000

47000

corporation tax @ 19% 8930

Net income 38070

TASK4

P4 Examining the impact on organisation of legal and ethical constraints associated

with taxation responsibilities.

Ethics:

In accordance with considering the taxable ethics which are to be meet by the

professionals in making proper consideration for ethics will be effective in making

appropriate ascertainment of the operations (Saez and Stantcheva, 2016). However,

there have been various differences in the ethical consideration and legal

9

UK and Hungary the firm is retaining appropriate profitability per year

Advantages of taxation to private companies:

There have been various benefits and appropriate help which have been

awarded to the private industries which were in respect to a limited liability business.

These businesses are personally liable for any financial losses on which there have

been issues relevant with the unprotected financial claims on which things are probably

going wrong.

Advantages of taxation to public companies:

These are the organisation which have created for a specific motive of tax to be

done. Thus, such analysis and ascertainment of businesses have various taxable

remedies in terms of profit sharing as well as have are protected from damages due to

aby financial losses. Thus, with impacts of such securities there are usually large

number of investors.

M3

Measuring the taxation liabilities

Trading profits 18000

Property income

18 months @ 500 accruing per month 9000

Capital gain (1 August 2017 disposal) 25000

Less: Gift aid donation (paid 31 March 2017) -5000

47000

corporation tax @ 19% 8930

Net income 38070

TASK4

P4 Examining the impact on organisation of legal and ethical constraints associated

with taxation responsibilities.

Ethics:

In accordance with considering the taxable ethics which are to be meet by the

professionals in making proper consideration for ethics will be effective in making

appropriate ascertainment of the operations (Saez and Stantcheva, 2016). However,

there have been various differences in the ethical consideration and legal

9

responsibilities of individual and entity in respect to make payments to the taxes. There

has been payment to the fair taxes as well as ascertainment to the profits which are to

be payable with making profitable analysis.

Along with this, there have been differences in the ethical consideration of the

business in various nations on which they were being liable for making adequate

operational analysis over the income generated by them (Devereux, Liu and

Loretz, 2014). Implication of taxation system in every nation which is based on

controlling the expenses and proper ascertainment of the tax liabilities.

Ethical principles:

In respect with considering the ethical concepts which are being required in the

business on which there are several elements that have to be considered. It includes

Honesty, integrity, loyalty and fairness which will be effective and adequate in terms of

managing the operational liabilities of firm.

Ethical constraints in businesses in UK and compare to other counties:

In respect with analysing the operational constrains of the business which is being

operating in the multi nation as compared with its operations held in UK. However, there

have been various social and ethical tasks which are required to be governed by the

professionals of such industries. There have been consideration over elements such as

operations, freedom of speech, marketing, taxes and bribery of the data base.

M4 Analysing the impacts of legal and ethical constraints which will be applicable to the

organisation

Tax responsibilities with relevant legislations at various level:

In respect with analysing the tax consequences in the corporation on which

developing various plans and objectives which will be adequate and effective in terms of

meeting the goals at the right time. The responsibilities of tax practitioners in

unincorporated and incorporated organisation where they were liable for making

effective taxable adjustments.

Tax responsibilities in references to tax collection:

In UK the mina governance and policy designing have been governed by the central

government and HMRC. Thus, management of such operational aspects will be

adequate and beneficial in relation with meeting the tax consequences of the firm.

10

has been payment to the fair taxes as well as ascertainment to the profits which are to

be payable with making profitable analysis.

Along with this, there have been differences in the ethical consideration of the

business in various nations on which they were being liable for making adequate

operational analysis over the income generated by them (Devereux, Liu and

Loretz, 2014). Implication of taxation system in every nation which is based on

controlling the expenses and proper ascertainment of the tax liabilities.

Ethical principles:

In respect with considering the ethical concepts which are being required in the

business on which there are several elements that have to be considered. It includes

Honesty, integrity, loyalty and fairness which will be effective and adequate in terms of

managing the operational liabilities of firm.

Ethical constraints in businesses in UK and compare to other counties:

In respect with analysing the operational constrains of the business which is being

operating in the multi nation as compared with its operations held in UK. However, there

have been various social and ethical tasks which are required to be governed by the

professionals of such industries. There have been consideration over elements such as

operations, freedom of speech, marketing, taxes and bribery of the data base.

M4 Analysing the impacts of legal and ethical constraints which will be applicable to the

organisation

Tax responsibilities with relevant legislations at various level:

In respect with analysing the tax consequences in the corporation on which

developing various plans and objectives which will be adequate and effective in terms of

meeting the goals at the right time. The responsibilities of tax practitioners in

unincorporated and incorporated organisation where they were liable for making

effective taxable adjustments.

Tax responsibilities in references to tax collection:

In UK the mina governance and policy designing have been governed by the central

government and HMRC. Thus, management of such operational aspects will be

adequate and beneficial in relation with meeting the tax consequences of the firm.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.