Case Study: Forecasting Techniques, Error Analysis, and Model Fitting

VerifiedAdded on 2020/06/05

|7

|851

|173

Case Study

AI Summary

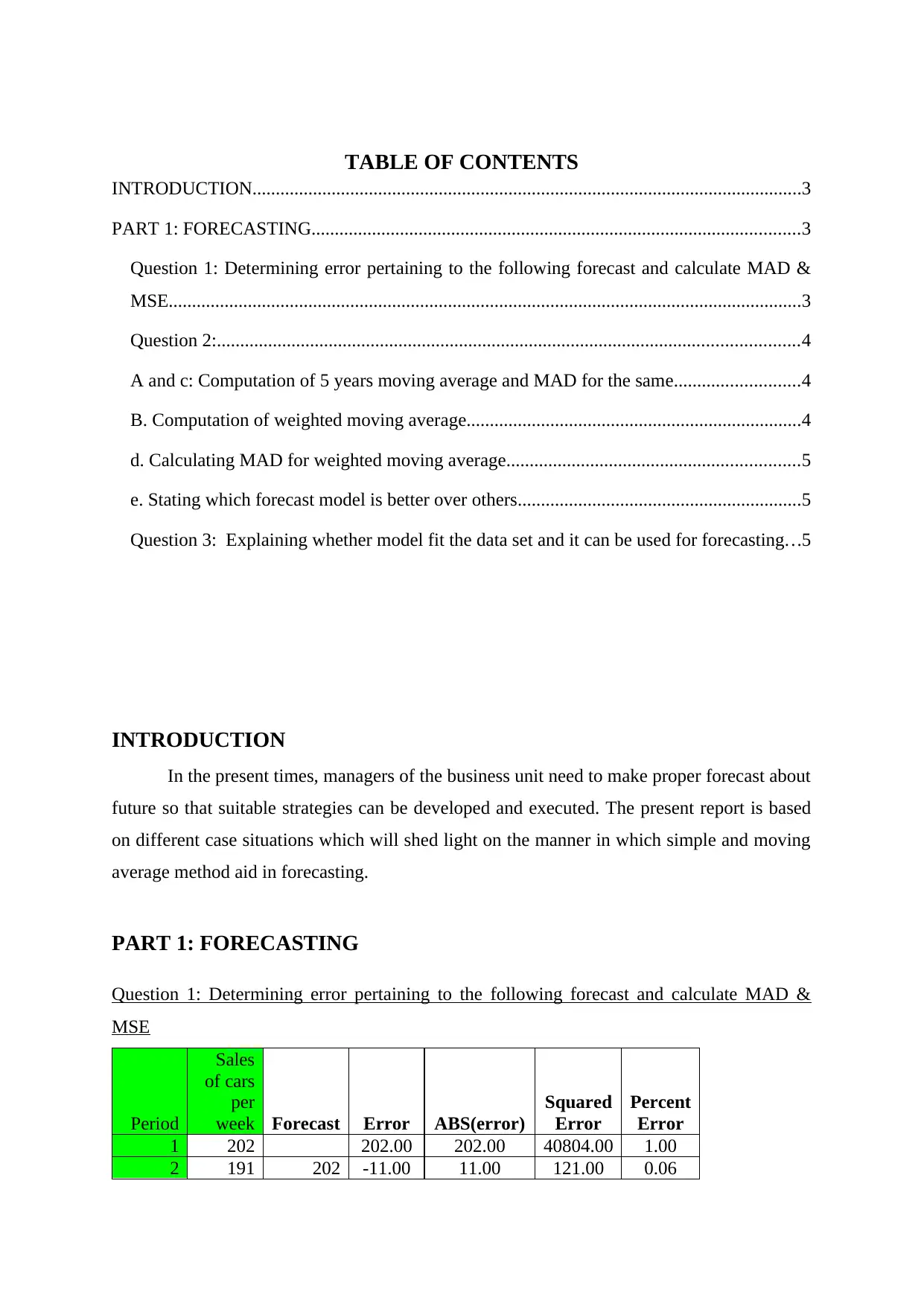

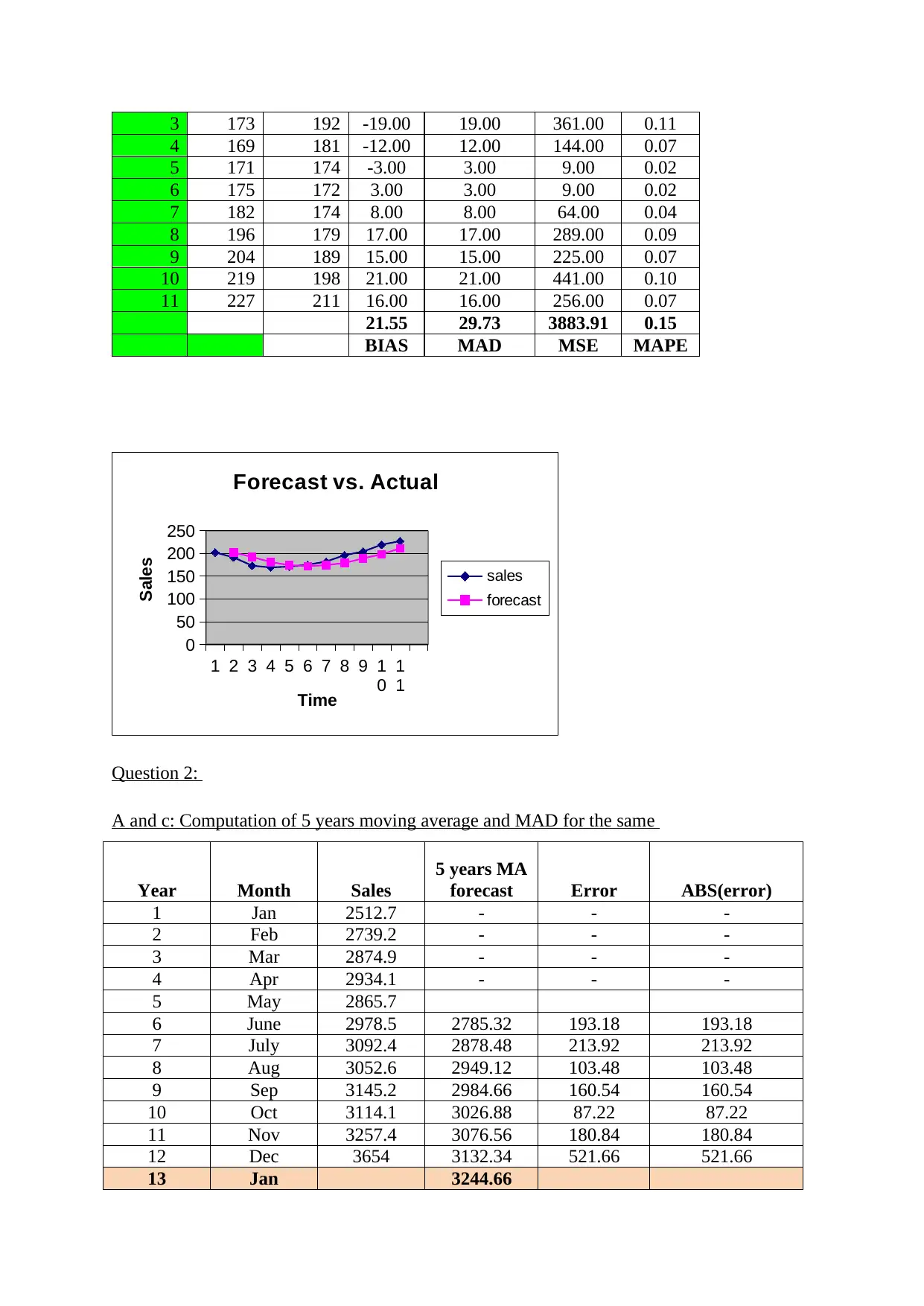

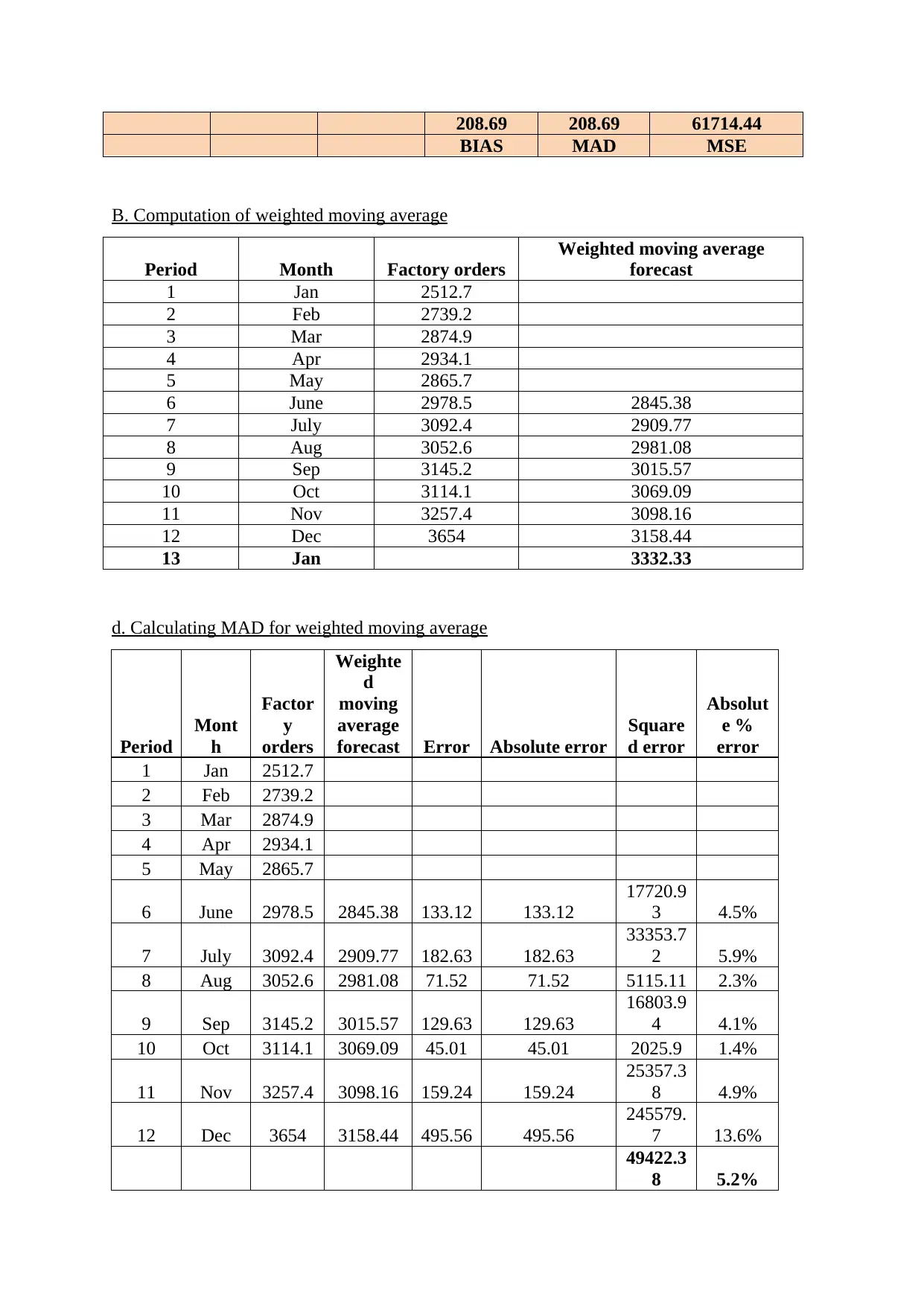

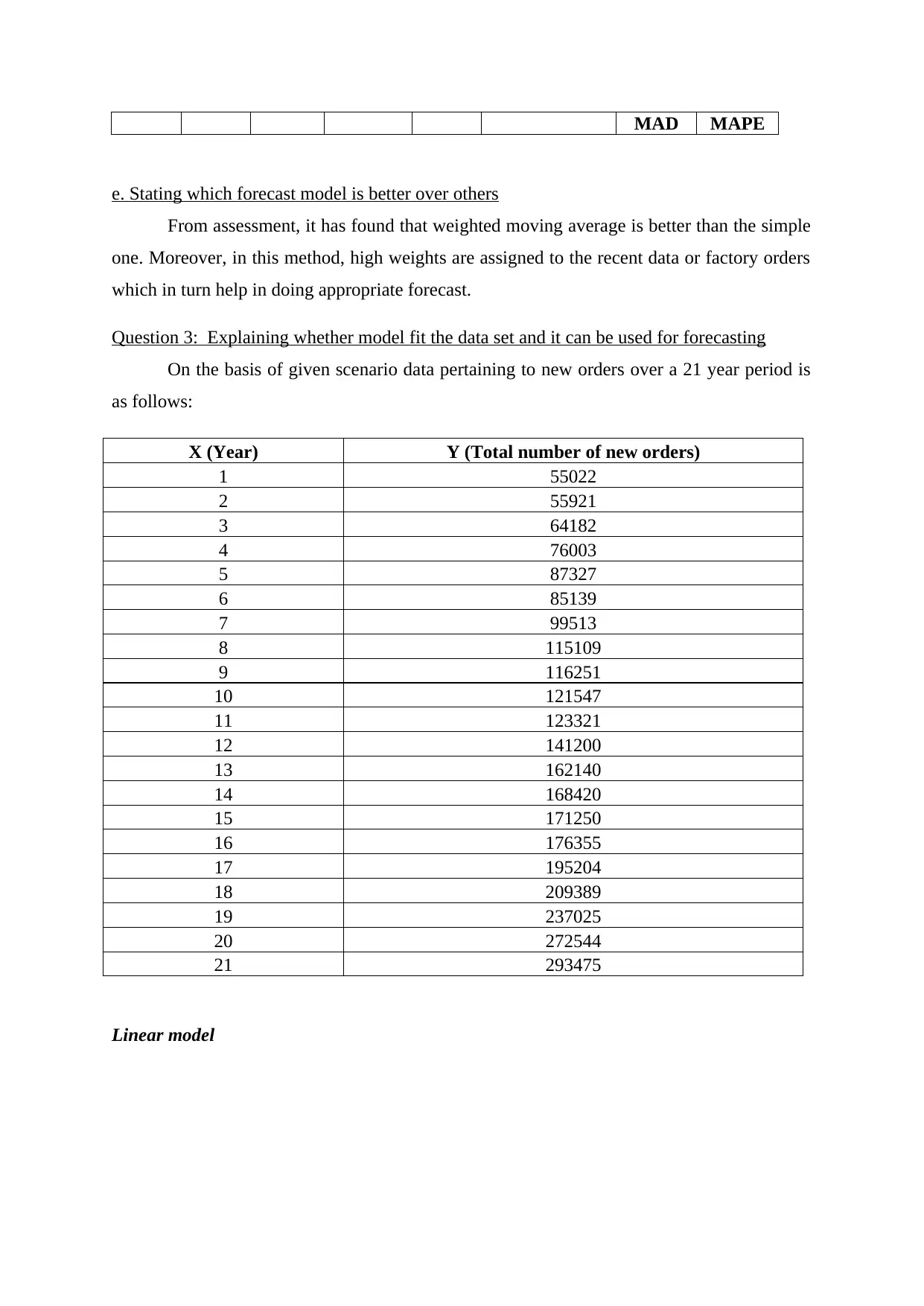

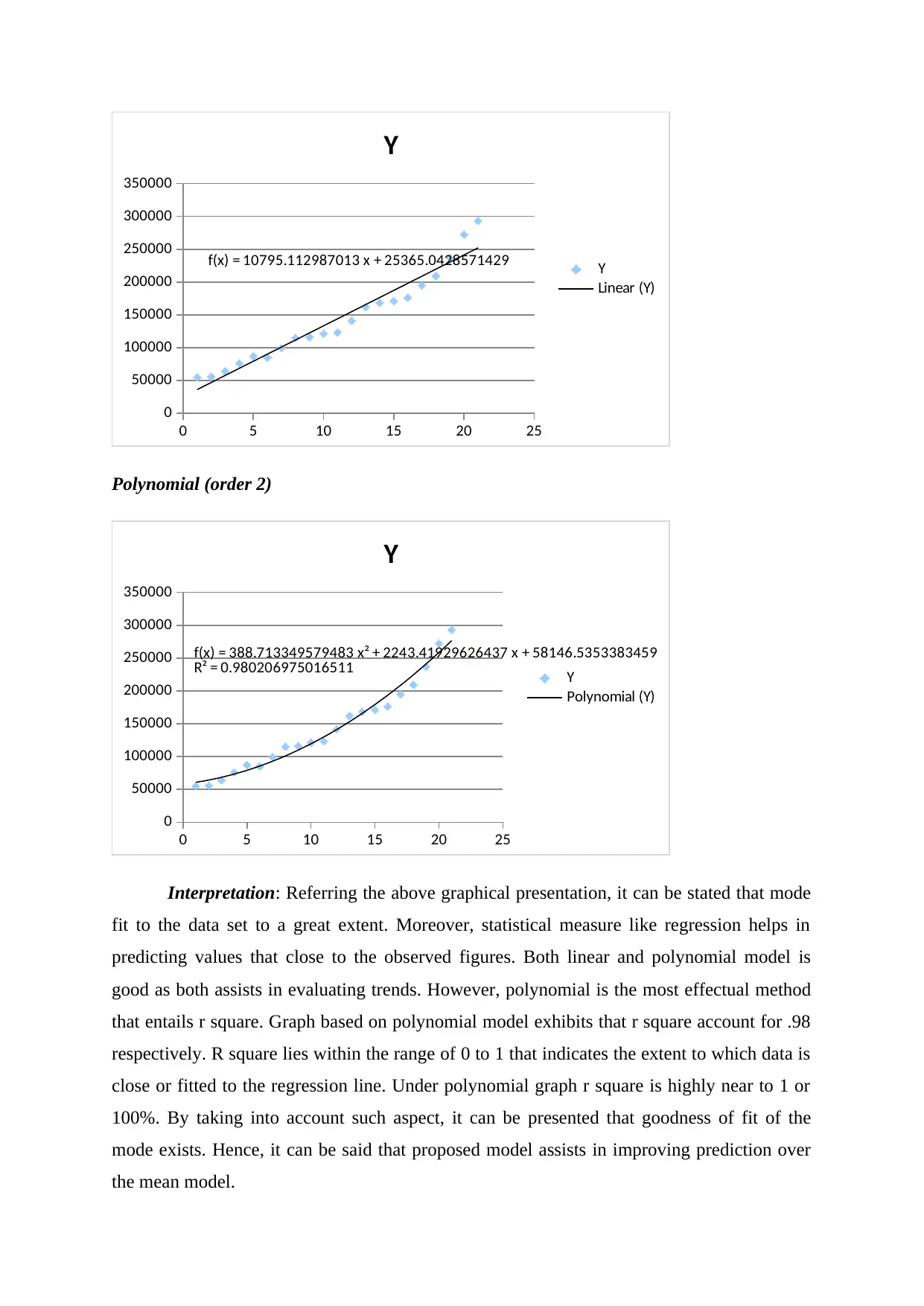

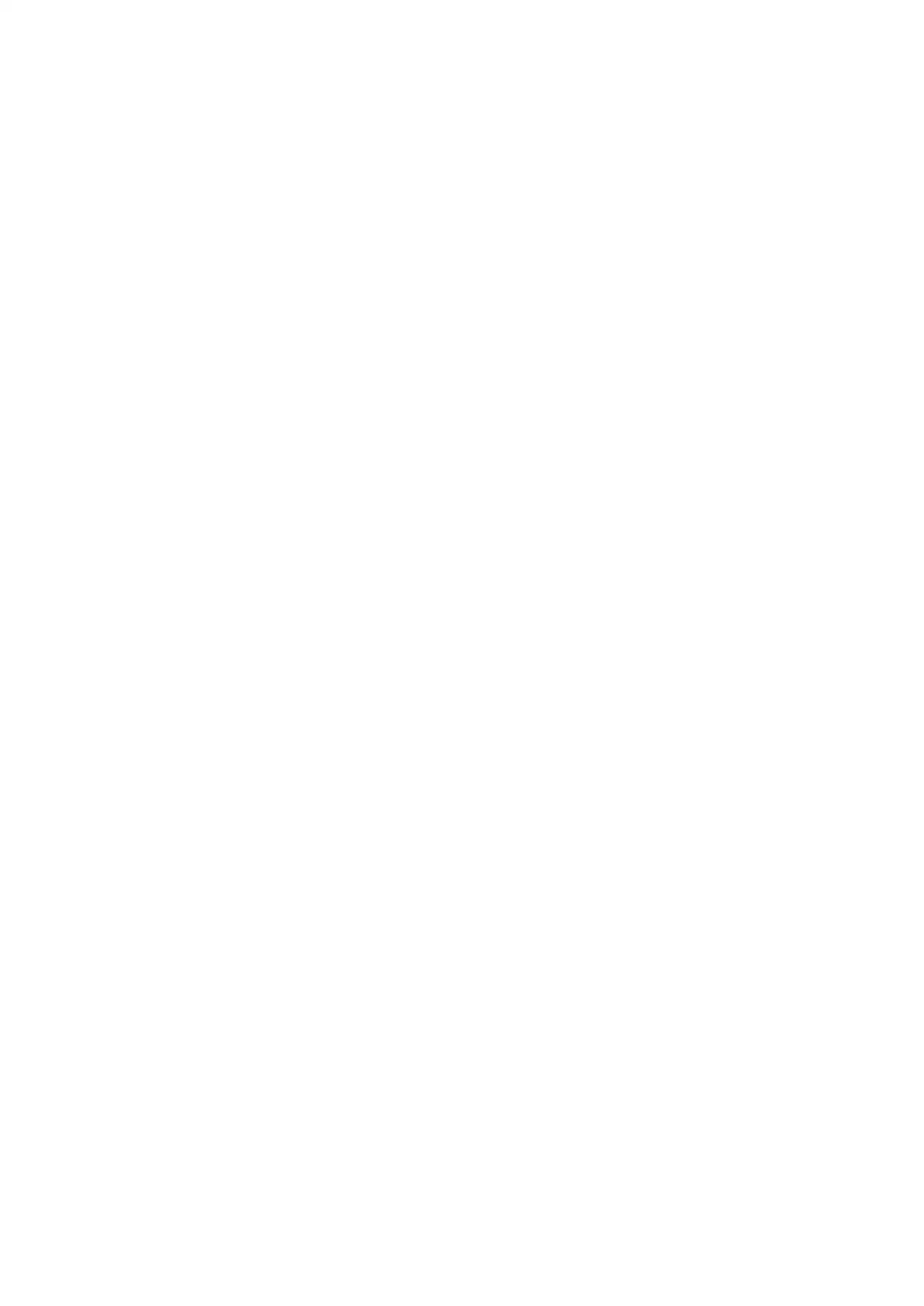

This case study delves into various forecasting techniques, encompassing error analysis and model comparison. It begins by calculating error metrics such as MAD, MSE, and percent error for a given forecast. The analysis extends to the application of moving average methods, including both simple and weighted moving averages, and evaluating their performance. The study further explores model fitting, examining how well different models align with a dataset and their suitability for forecasting future trends. This involves the interpretation of linear and polynomial models, with a focus on the goodness of fit and the use of statistical measures like regression to predict values. Ultimately, the case study provides a comprehensive overview of forecasting methods, error analysis, and model evaluation, highlighting the strengths and weaknesses of each approach.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.