University Research: Forecasting Stock Prices in International Markets

VerifiedAdded on 2023/05/31

|8

|1325

|442

Report

AI Summary

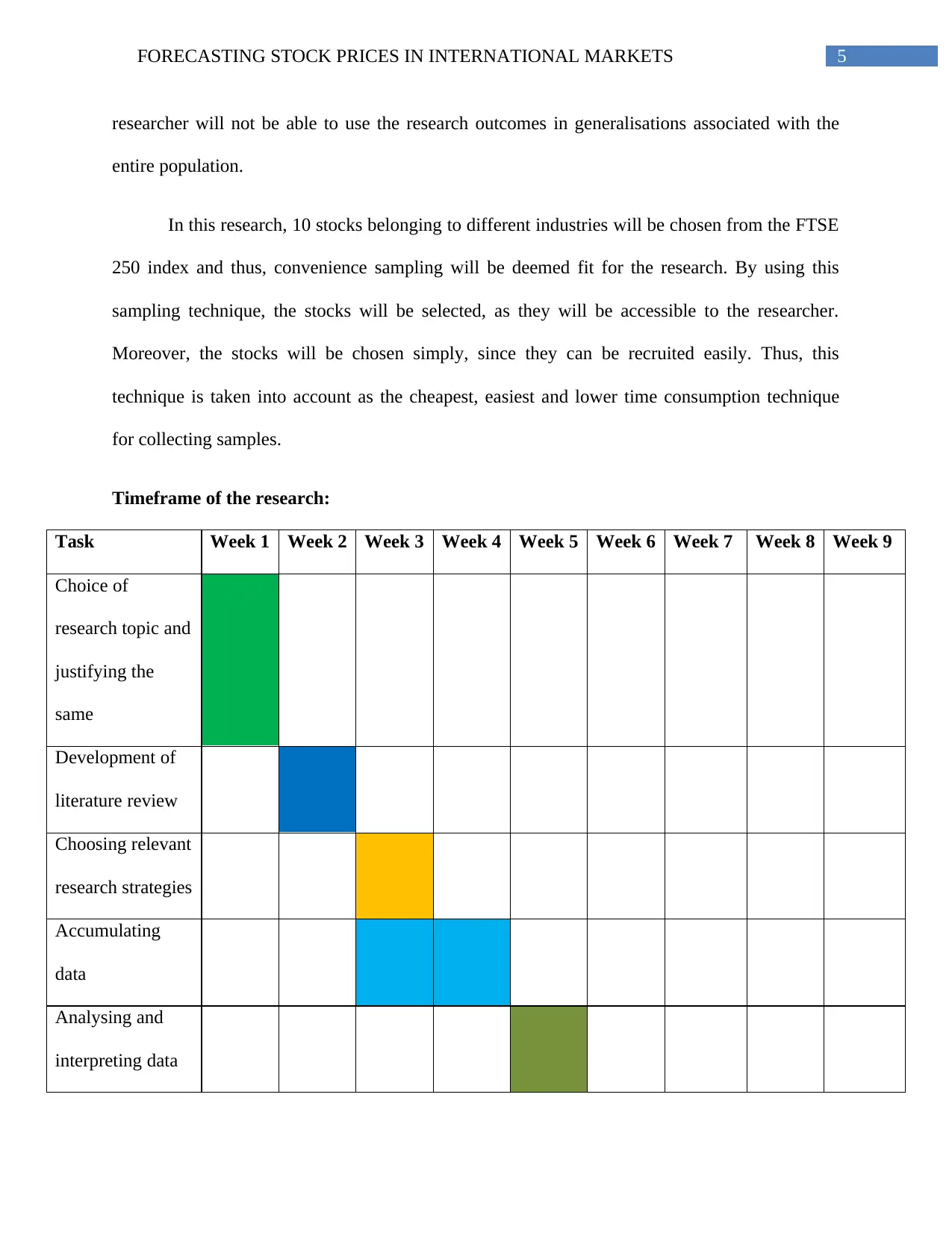

This report delves into the critical area of forecasting stock prices within international markets, addressing key research questions such as the impact of seasonal effects, price reversals, extreme value removal, disagreement, trading volume, and price volatility. The study begins with a brief literature review, highlighting the significance of investor information, the role of equity premium, and the influence of factors like economic, political, and natural events on stock prices. The research methodology section outlines the use of secondary data, specifically from sources like Yahoo Finance and Bloomberg, focusing on the FTSE 250 index. The researcher employs a non-probability sampling technique, selecting 10 stocks from different industries within the index, using convenience sampling due to time and budget constraints. The timeframe for the research is detailed across nine weeks, covering topic selection, literature review, data accumulation, analysis, and report submission. The report aims to contribute to the understanding of stock price forecasting and provide insights for investors and risk managers.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.