Accounting Case Study: Foreign Currency Translation Analysis

VerifiedAdded on 2020/05/11

|6

|489

|63

Case Study

AI Summary

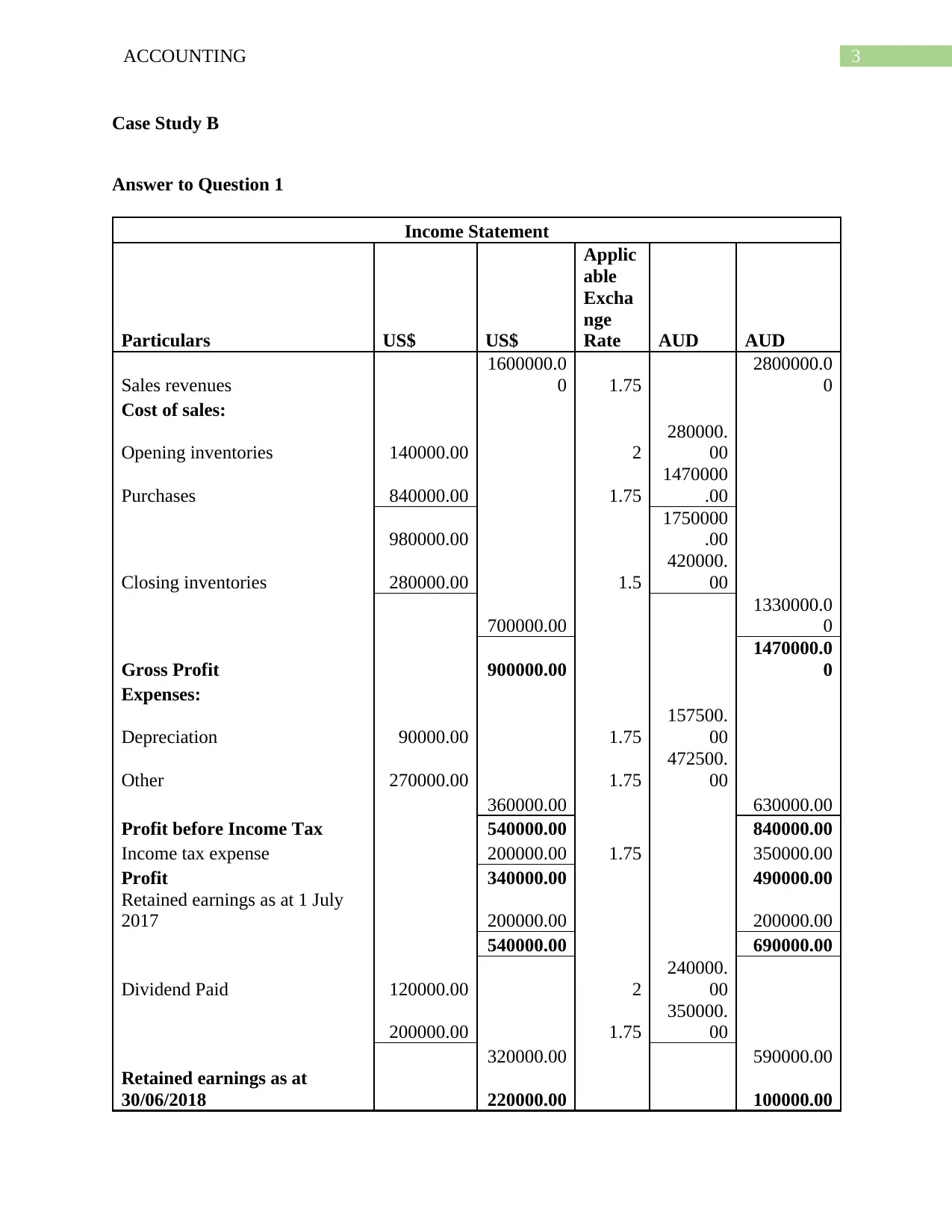

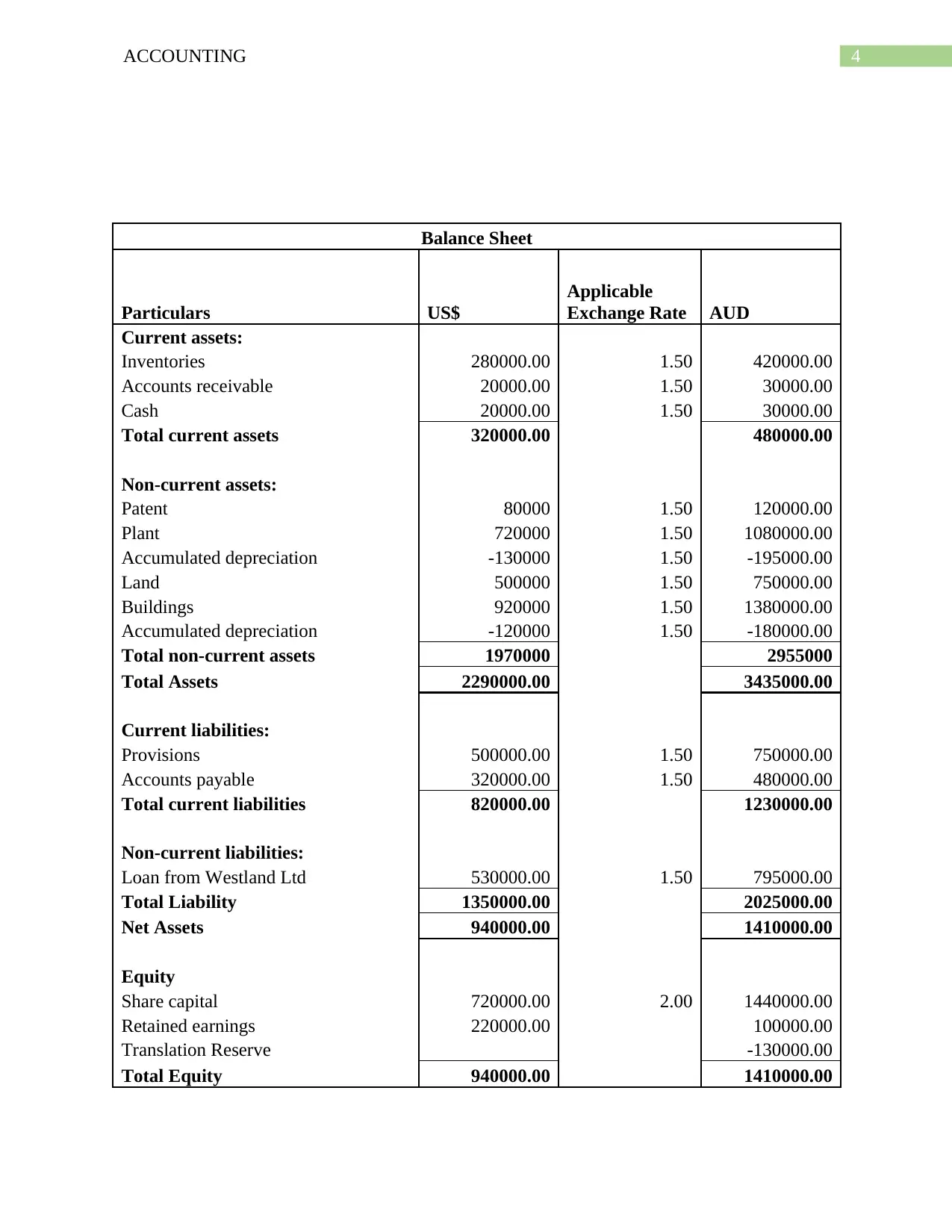

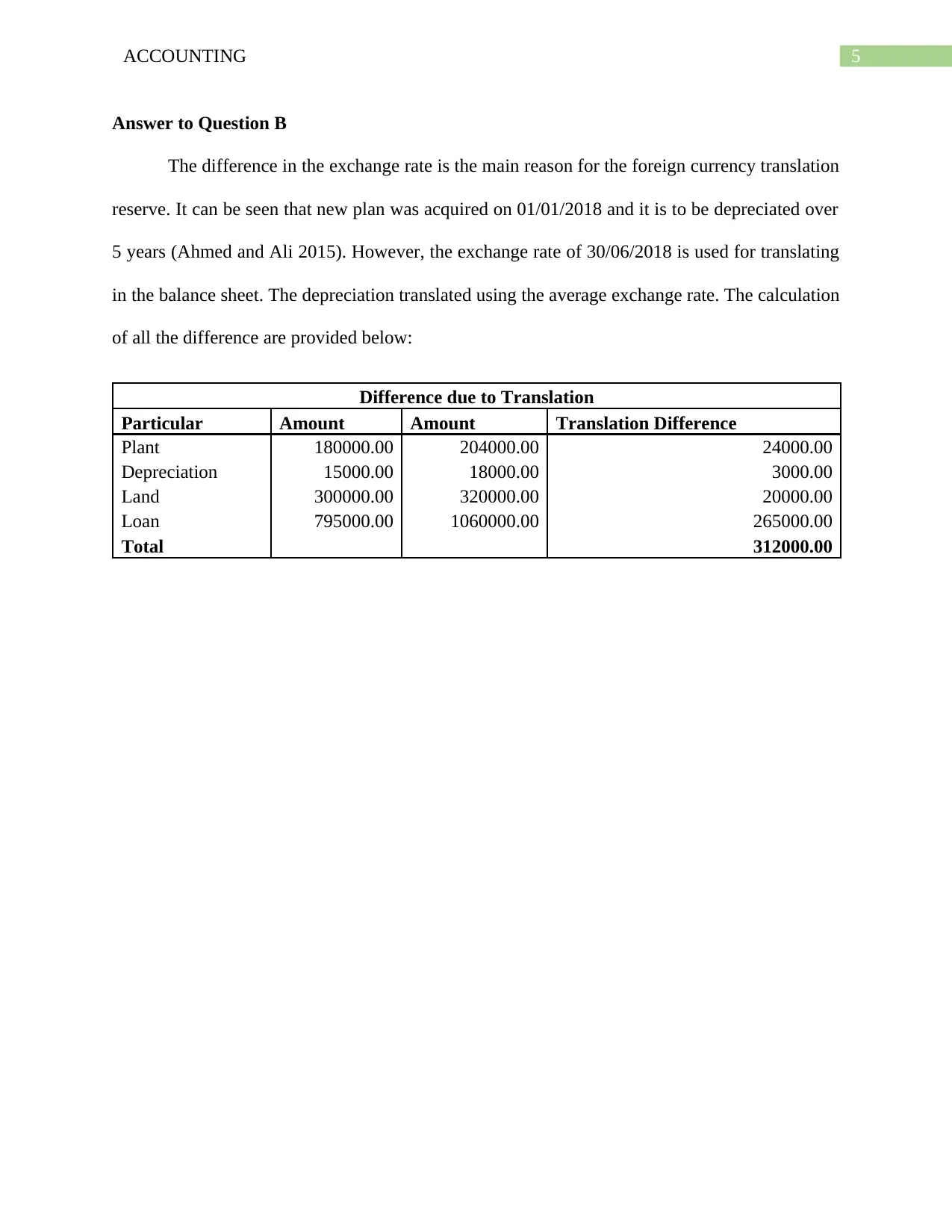

This case study presents a detailed analysis of a company's financial statements, focusing on the impact of foreign currency translation. The assignment includes an income statement and a balance sheet, both presented in US dollars and their equivalent in Australian dollars, highlighting the application of exchange rates. The analysis delves into the calculation of profit, retained earnings, and the effects of depreciation and income tax. Furthermore, the case study explores the reasons behind the foreign currency translation reserve, particularly focusing on the differences arising from exchange rate fluctuations in assets like plant and land, as well as liabilities like loans. It also provides references to relevant academic sources.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.