Analysis of Foreign Currency Translation for Trust Bank Limited 2020

VerifiedAdded on 2023/02/01

|6

|756

|63

Report

AI Summary

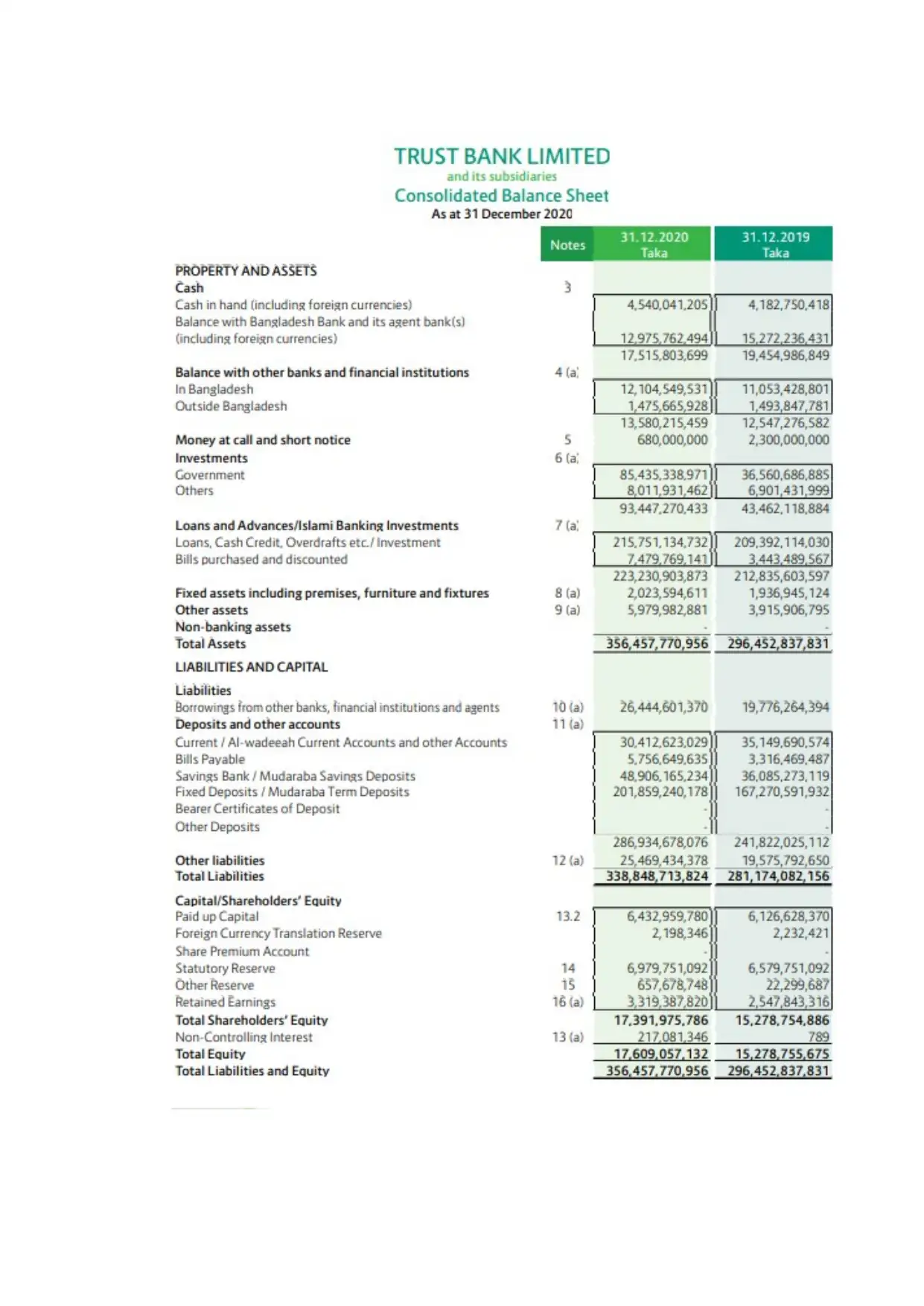

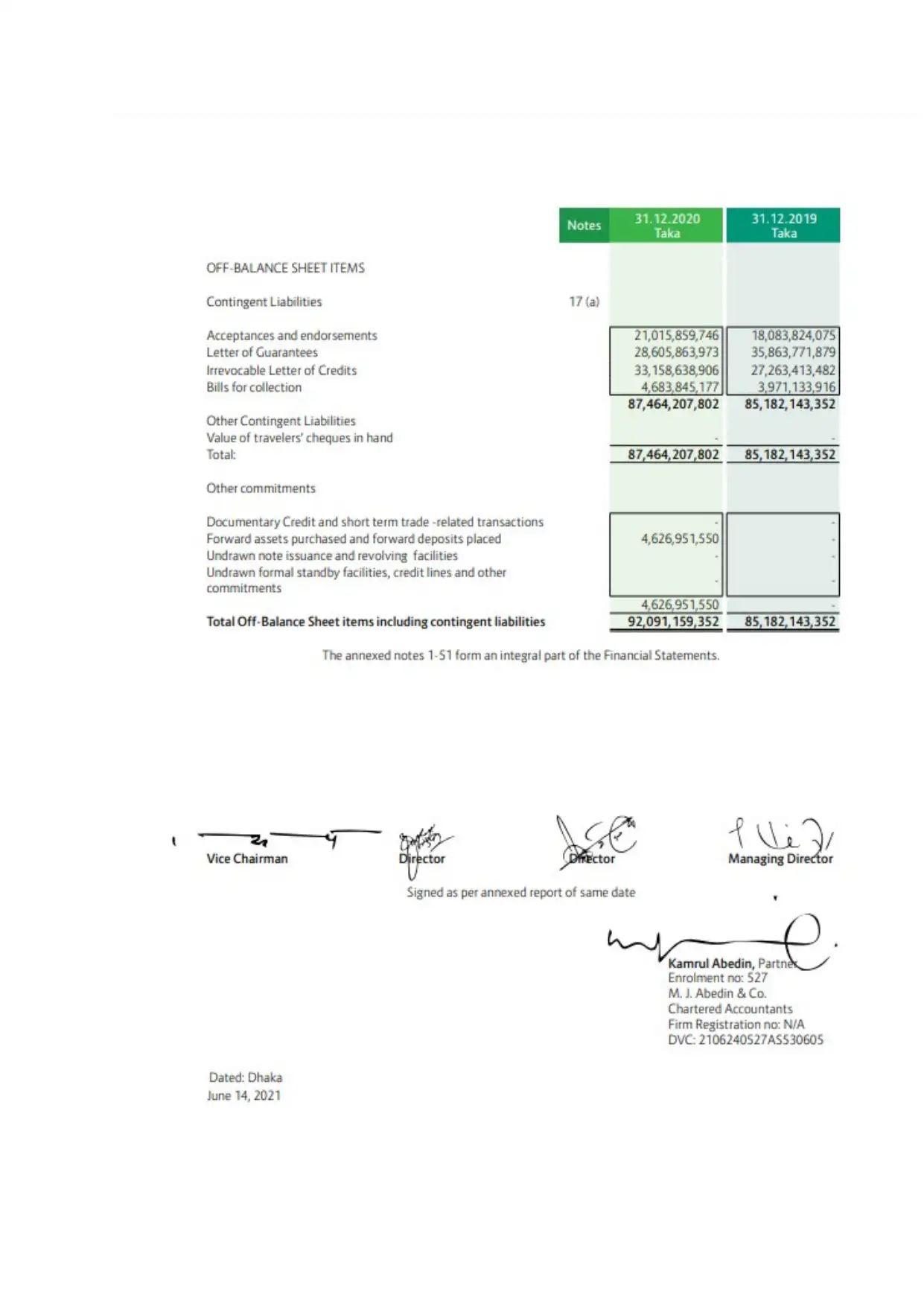

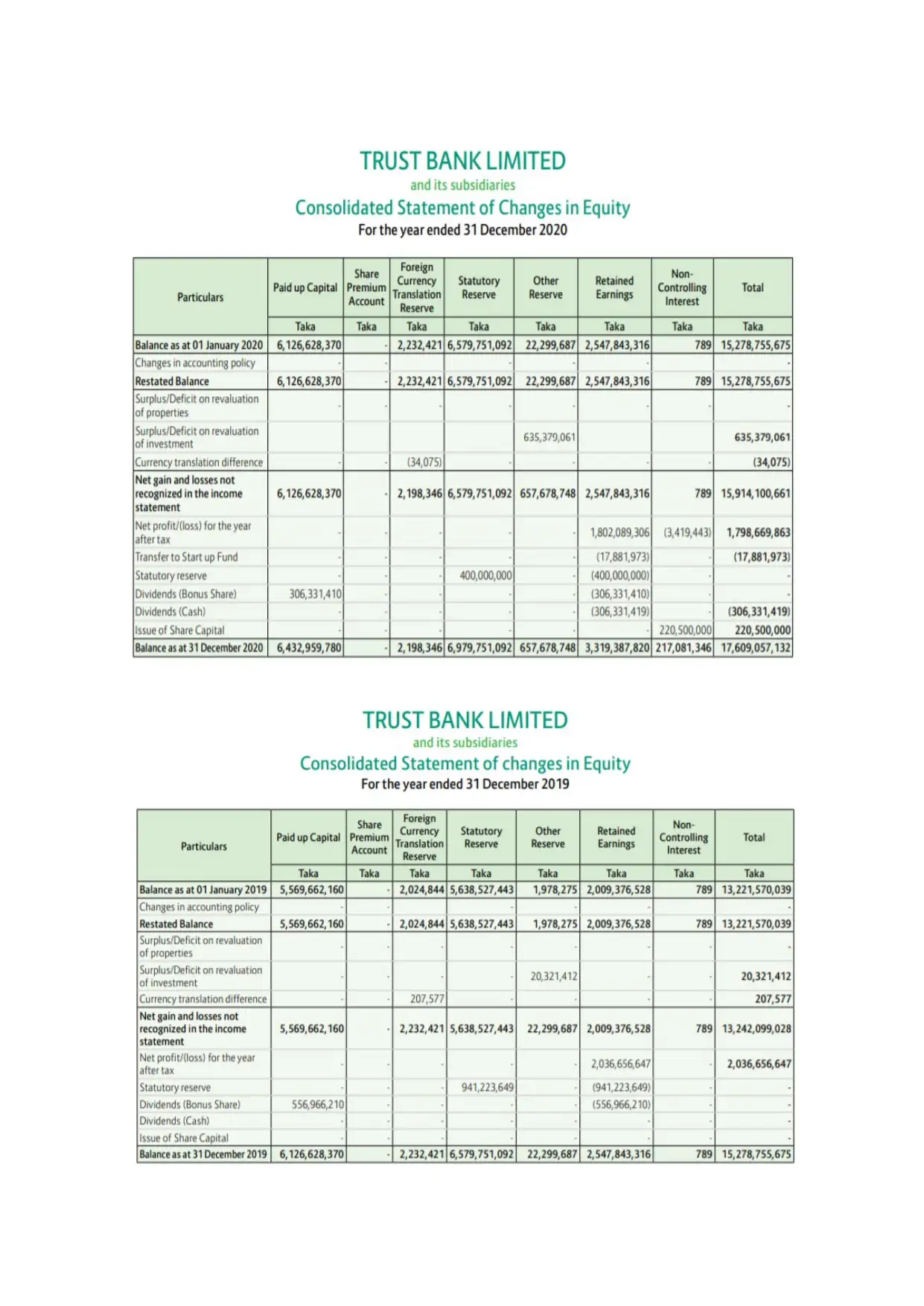

This report examines the foreign currency translation practices of Trust Bank Limited in Bangladesh, focusing on the year 2020. The analysis is based on the bank's consolidated financial statements, including the balance sheet, cash flow statement, and statement of changes in equity. The report details how the bank accounts for foreign currency transactions, including the use of exchange rates as per IAS 21, and the treatment of translation gains and losses. It highlights the conversion methods for different currencies, the handling of commitments and contingent liabilities, and the consolidation of financial statements of foreign operations. The study reveals the impact of currency fluctuations on the bank's equity and profit and loss, providing a clear understanding of the financial implications of foreign exchange transactions. The report also examines the translation of assets, liabilities, income, and expenses of the bank's offshore banking units (OBUs).

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.